Mad Hedge Technology Letter

March 16, 2022

Fiat Lux

Featured Trade:

(THE GENIUS AT SOFTBANK GETS EXPOSED)

(SFTBY), (ARKK), (DIDI), (BABA), (CPNG)

Mad Hedge Technology Letter

March 16, 2022

Fiat Lux

Featured Trade:

(THE GENIUS AT SOFTBANK GETS EXPOSED)

(SFTBY), (ARKK), (DIDI), (BABA), (CPNG)

Mad Hedge Technology Letter

March 4, 2022

Fiat Lux

Featured Trade:

(RUSSIA BRINGS DOWN CHINESE TECH)

(BABA), (DIDI)

Don’t buy Chinese tech stocks.

I’m not saying to avoid them because of Chinese Xi Jinping’s “common prosperity” campaign, although that isn’t ideal.

The Eastern European war has meant draconian sanctions levied on the Russian economy and these sanctions also have a tech angle to them, particularly a Chinese tech angle.

Chinese companies could find themselves subject to regulatory fines and other penalties for breach of sanctions if they continue to work with targeted Russian entities.

In effect, we could see a sudden exodus of Chinese tech companies from Russia if they determine that the juice isn’t worth the squeeze.

The same avoidance is happening with ships circling America with Russian oil, are buyers of these commodities certain they won’t face sanctions if they buy Russian oil?

Policy becomes quite muddled when a band of politicians shouts new proposals for harsh sanctions and it affects the middleman as much as the end buyer.

If Chinese companies bolt Russia, many Chinese companies would need to take a revenue haircut and guide down.

Under US export sanctions imposed on Russia, any technology goods made in foreign countries using US machinery, software or blueprints will be banned from being exported to Russia. So you see how this applies directly to Chinese tech firms in Russia. Companies in Taiwan, South Korea, and Japan have quickly said they will comply.

Chinese laptop maker Lenovo has already shut down manufacturing and sales in Russia.

The Chinese are mercantilist and their much-publicized friendship with Russia doesn’t mean it will stay strong forever.

I don’t want to wade into politics but if Russia becomes too much of a pariah, Chinese tech firms might also reconsider the reputational risk at stake.

They aren’t the only ones to stop sales to Russia.

Rival Dell and chip supplier Intel have also closed up shop.

This has all led to a great de-risking of Chinese tech and I believe readers need to abstain from reading Wall Street research urging you to buy the Chinese tech dip.

Owning Chinese tech stocks, in general, is a terrible idea even though Berkshire’s Charlie Munger has doubled down on Alibaba (BABA) shares.

He has lost a lot of money from that trade and I find it ironic that Munger complains a lot about how bad America is and plays the fearmongering card yet his own money is in Alibaba shares.

The pain hasn’t been confined just to Alibaba, food delivery giant Meituan sold off again after Beijing on Friday ordered it to cut fees.

Tencent is facing new scrutiny of its core businesses.

The Hong Kong Hang Seng Index has more than halved from last year’s February peak with Beijing’s anti-monopoly campaign far from over.

Earnings will drop significantly as higher costs from increasing social responsibility incrementally handcuff Chinese tech companies from making decisions best for their shareholders.

The technology sector’s bullish run had lasted for decades before the “common prosperity” push brought it to an abrupt halt. The clampdown that began in late 2020 has hit almost every corner in the industry, from data security, digital business to online games and overseas listings.

The impact on tech earnings will be on show again on Thursday when Alibaba is due to report an estimated 60% drop in quarterly profit.

All told, this has been a highly negative past 7 days for autocratic regimes in the East as the West finally did an about-face to the status quo of turning a blind eye to corrupt money and deployment of power that lassoed crony capitalists.

Avoid all Chinese stocks and don’t follow Mr. Munger into Alibaba (BABA).

Mad Hedge Technology Letter

November 8, 2021

Fiat Lux

Featured Trade:

(HOW SOFTBANK GOT GLOBALIZATION ALL WRONG)

(SFTBY), (DIDI), (BABA), (CPANG)

Softbank’s Vision Fund, a technology-biased venture capitalist fund, is basically a leveraged massive bet on synchronized bullish behavior on the future earnings of global tech companies.

It assumes that technology is one of the critical underpinnings to global business and it's more or less a wager on an increased rate of harmonic globalization.

I get what they are trying to do, but in 2021, globalization is far from harmonic, and there are many in the camp that the world is wrought by a current phase of deglobalization.

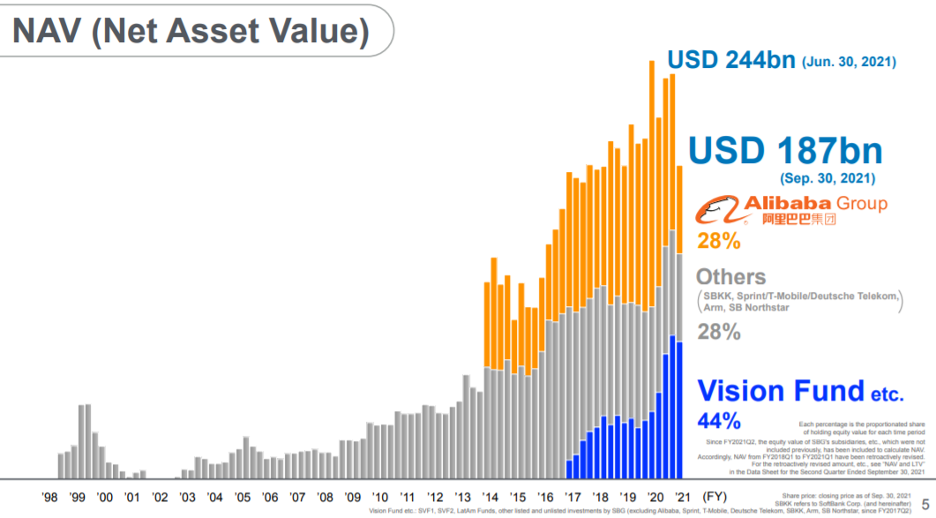

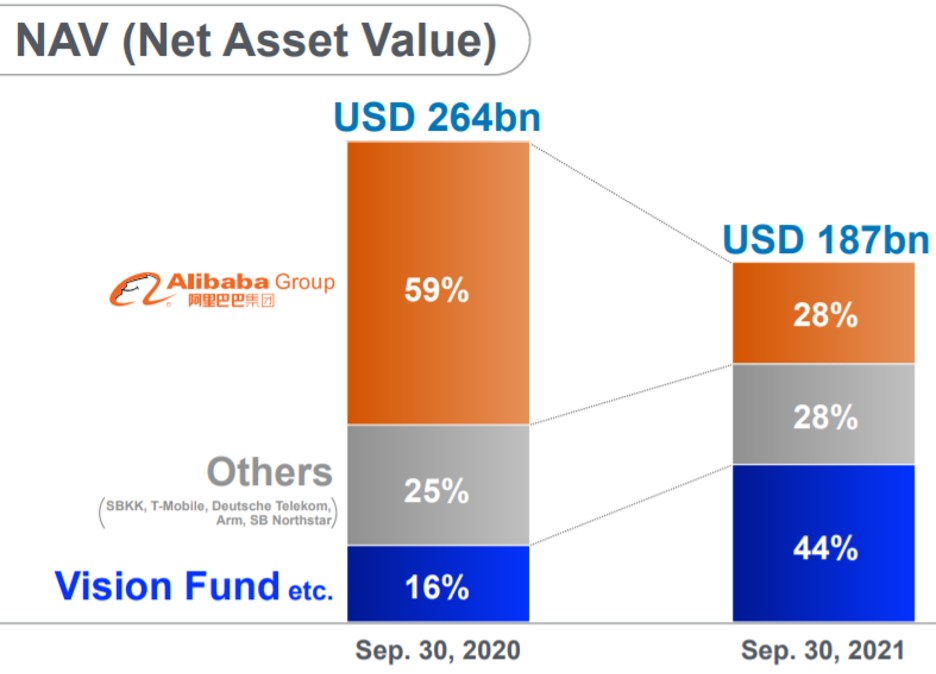

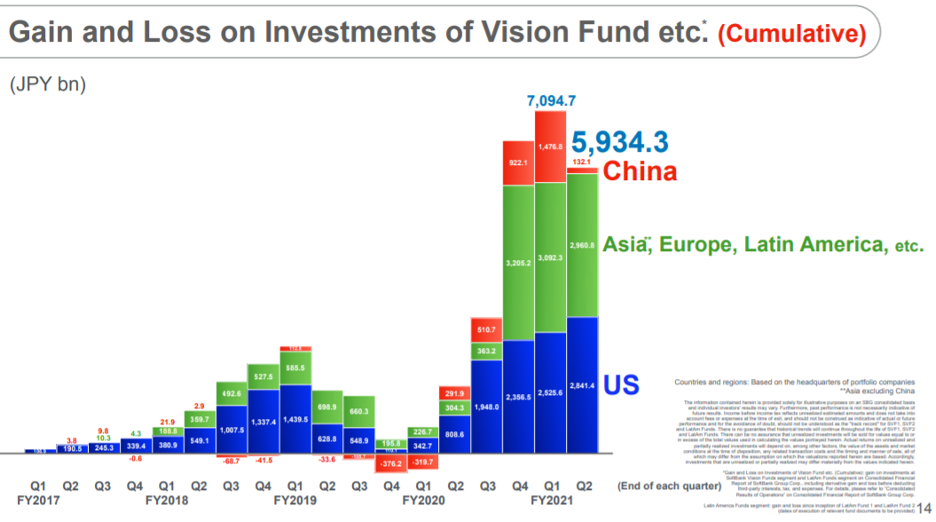

This past quarter, Softbank presided over a precipitous drop in the Net Asset Value of their technology investments from $244 billion to $187 billion.

The -24.6% return and the pain from it were mainly induced from Softbank’s vast array of Chinese investments specifically dreadful performance from its bellwether leader Alibaba (BABA) whose stock has halved since the crackdown started.

CEO of Softbank Masayoshi Son, an ethnic Korean with a Japanese passport, described its current predicament as being “right in the middle of a storm.”

The problem with that is not being in a storm per se, but the timeline into transitioning into sunnier climate because just 1-2 quarters out from now, prospects appear bleak.

If one might remember, DiDi Global Inc. (DIDI), the Chinese ride-sharing platform, was the big shebang going public at a valuation that pegged the company at $68 billion.

Since then, not much has gone right as it was later found out that (DIDI) went public without the tacit approval of the Chinese Communist Party.

Falling out with the good graces of their overlords has meant a halving of the stock and Softbank has taken a loss of $6.1 billion on DiDi.

Even worse for the firm, there appears to be no savior or “next DiDi” IPO to save their Net Asset Value in the upcoming quarters.

That means we could be staring at the high-water mark which occurred 2 quarters ago.

Thank God for the outperformance in Europe and the United States that, in effect, accomplished some damage control for the bottom line.

And their recent short-term track record has been overwhelmingly poor.

Let’s take a glimpse into the other investments that have been chop blocked at the knees.

The losses keep rolling off the tongue with Uber-like trucking startup Full Truck Alliance Co. down $1.2 billion.

KE Holdings Inc., which runs the Beike online property service, lost $2.2 billion of value — the stock is down more than 70% from its peak and is trading below the IPO price.

And the failings weren’t just in China, take a stock that I have extensively bashed on — the biggest ecommerce company in South Kora — Coupang (CPANG).

Their poor past quarter’s performance meant that Softbank booked a quarter performance of a horrific -$6.7 billion.

I told readers to stay away from this one not because it is a bad company.

It was crystal clear in the underlying data that its business was saturated in Seoul, and there are no other big cities in South Korea, and I couldn’t see where the next phase of incremental growth would come from.

The idea was to grow abroad but everywhere else in Asia has been monopolized by local or brand-named ecommerce companies.

That was the bad news, and the silver lining is that ex-China, particularly the United States, they have been doing well and are highly profitable.

Slippage from this Vision Fund is quite notorious, from its misallocation of funds of shared office space company WeWork to overpaying for many other companies with a vanilla idea that technology will overcome any obstacle.

I would say that at a management level, not a lot is well thought out at Softbank.

I would like to remind readers that many of these new China investments by Softbank have just plain out ignored the geopolitical tensions.

They have nobody to blame but themselves because they certainly had time to divest from China and take profits which would have been the right move to do at that time.

Softbank’s parent company’s stock is basically half of what it was in March 2020 thanks to China and the Vision Fund will need to rely on its ex-China investments to pull itself out of this “storm.”

Another big plus is that the China losses are unrealized, but China has offered zero indication that their monumental crackdown on private business is over, and no amount of kowtowing will sway them from their lofty perch.

This could just be the start of their reign of terror over private business and that’s a scary thought right there.

Honestly, I opt for the more conservative stance of never buying Chinese stocks.

Why invest in Chinese tech when United States tech is so much better?

Not enough growth for you?

Then use options.

Softbank should and could have just poured all their investments into Silicon Valley, or just one company like Google, or even the digital gold of Bitcoin.

Good thing there is no ETF that tracks the performance of Softbank!

Invest at your own peril.

Mad Hedge Technology Letter

August 11, 2021

Fiat Lux

Featured Trade:

(HIGHER HIGHS FOR THE NASDAQ?)

(UBER), (DIDI), (BABA), (COIN), (HOOD), (SFTBY)

The blowback from the Chinese tech crackdown has been quite tough to take for Softbank (SFTBY) because of the decision to maneuver deeply into Chinese tech shares.

It looked good at the time, as China was the center of every Wall Street analyst’s growth proposition short and long term.

However, troubles in China crystallize the massive shift of deglobalization and many investment funds are finding a new world as we turn the page.

Gone are the days when aggressive investors could just dabble in all sorts of exotic markets believing that globalized forces would be a wind at its back.

So much so that nobody ever batted an eye if you told them you had investment theses playing out in Mongolia or Brazil.

Emerging markets are blowing up and now even the passport with which you do business has never been more prominent.

Rich countries are going the way of Europe – that of intense and mind-numbing regulation to make up for a shortage of tax revenues to pay for these costly programs.

The global canary in the coal mine can be traced back to Alibaba’s founder Jack Ma effectively being muzzled by the Chinese Communist Party. This was the nail in the coffin for the China story as it relates to foreign money waterfalling in the Middle Kingdom.

That’s the end of it.

Softbank will need to go back to the drawing board and probably pluck China off the board as top dog and reset their draft board.

The pain is now being found in Softbank’s balance sheet with net profit down 40%.

Let’s look at some of Softbank’s investments which include Chinese e-commerce giant Alibaba (BABA), car-share giant Didi Global (DIDI), and short-video app TikTok owner ByteDance Ltd.

Around 35%-40% of Softbank’s investments are tied up in China and its net profit is down to 761.5 billion yen, equivalent to $6.9 billion.

The incremental buyer has dried up and Softbank is now saddled with an illiquid Chinese tech portfolio they can’t get rid of.

Softbank founder Mr. Son said that SoftBank’s shares have fallen so low that the price is now only around half of the value of the company’s assets, after subtracting debt. Given that discount, SoftBank will unveil more share buybacks at some point, and is now discussing the timing and size.

He also said that SoftBank will continue the furious pace of investment at Vision Fund 2, which has stakes in 161 companies and has been funding startups at a rate of nearly one per day in recent months.

SoftBank’s new investment in pharmaceutical company Roche Holding AG signals that the Japanese company might resort to safer stocks with stable free cash flow.

Compounding the situation might be that Softbank feels that they have been burnt by tech investment one time too many.

The ripple effect of China tech going down affects their assets as a whole and have concluded that the balance sheet needs trimming and re-upping.

Even if Softbank can find some balance sheet rejuvenation - they no longer feel they can take these extraordinary tech risks that achieve high beta which is required to satisfy investors.

Overall, we could be dealing with a dearth of real, legitimate tech opportunities in proven business models which could be a reason for Softbank rotating into sectors like pharmaceuticals.

No doubt I believe they will keep their eye out for tech opportunities, but they aren’t set on it from the beginning like the past 2 decades.

Or perhaps, this could be the segue into riskier investments than before - remember Uber (UBER) was a company that no VC wanted to touch with a 10-feet pole and Softbank took it on and made a lot of money. but where is the next Uber after Uber?

It's possible that there are no real, transformative companies in the pipeline after the Coinbase (COIN), Robinhood (HOOD) IPOs, these investments usually take 10-20 years to take profits from the initial seed funding.

It could also signal further advancements into the derivatives market with the company looking for leverage bets instead of holding vanilla equities and standard ETF index funds.

Their foray into derivate exposure gave them the nickname the “Nasdaq whale” when the company bought a torrent of call options profiting in the billions from the tech lurch up.

Even retail traders have gotten into options with their profit possibilities which are able to surpass any equity trade that only have a 2:1 leverage ratio.

Softbank could be finding tech too overvalued and looking to jump short-term into another industry almost like a day trader, although tech, for them, is something that is a long-term core objective.

We can analyze this whichever way we want but its meaning is clear – the low hanging tech fruit is gone, and it will be harder to fight for your crust of bread even much so that the Nasdaq whale is looking into morphing into the S&P whale or a different type of whale all together.

I can tell you that deep down in the weeds as a trader, I am seeing a rapidly evolving rotation that has rewarded cyclicals that are back from the dead and financials that are breaking out benefiting from the massive amount of stimulus deposits.

We need to acknowledge that the consumer is currently in the best health of our lifetime because of the free payouts, PPP loan forgiveness, and other goodies. And that doesn’t necessarily mean that tech will go up in the short-term as we skim all-time highs.

Technical charts still look positive for tech, but it is true that the sector has cooled off even if the trend will be higher long-term. It’s getting that much harder to eke out higher highs in the Nasdaq.

Mad Hedge Technology Letter

July 9, 2021

Fiat Lux

Featured Trade:

(BUYER BEWARE)

(DIDI), (PGJ), (FB), (AMZN), (GOOGL), (NFLX), (AAPL)

Chinese regulators announced on our Independence Day that they were banning downloads of Uber’s China DiDi in the app stores in the country because it poses cybersecurity risks and broke privacy laws.

This was after DiDi raised $4.4 billion by listing its shares in New York.

However, unnamed sources leaked that China's cybersecurity watchdog suggested to DiDi that it delay its IPO before it happened.

Delaying a wealth generating event like the IPO is controversial.

At this point, DIDI, the Uber of China, is worth a speculative trade at $1 and that’s if the Chinese tech firm doesn’t delist before that.

No — scratch that — it’s not even worth your time at $1 if you hold currency denominated in USD or anything even half as credible.

But if you’re from somewhere like Venezuela wielding infamous bolivars then take a wild stab around $1 or double up at $0.50 for a trade.

There is a reason that I have never in the history of the Mad Hedge Technology Letter recommended buying a Chinese technology stock.

The astronomical risk isn’t justified.

The evidence is now out in public with Chinese big tech and the Chinese Communist Party (CCP) airing their dirty laundry.

Most sensitive business dealings are usually dealt with in-house in the land of pan-fried dumplings and Beijing roasted duck, so things must be spiraling out of control on the inside.

No doubt that inflation spikes are causing chaos everywhere, but China is particularly vulnerable because of the high volume of Chinese living in poverty.

It’s unrelated to this IPO, but another valid reason why Chinese “growth” is weakening fast.

Stateside, cashing out is normal for tech growth companies who want to reward earlier seed investors, their own management teams, and in this case the early-stage investors were Japanese Softbank (21.5%), Silicon Valley’s Uber (12.8%), and China’s Tencent (6.8%).

This was pretty much a big middle finger to these three along with the other Chinese investors which were about to profit big.

This is on the heels of the CCP nixing the Jack Ma Alipay IPO.

Chinese big tech has gone from darlings to pariahs in a short time proving that in the U.S., you get too big to fail, but in China, you get too big to exist.

Silicon Valley tech princelings are also validated for leaving China such as Facebook (FB), Google (GOOGL), Amazon (AMZN) and Netflix (NFLX).

If local Chinese tech can’t flourish in China, then forget about foreign tech in China.

It’s a non-starter.

Apple (AAPL) is the only exception because they are grandfathered in when China had no smartphone and now they provide too many local jobs to be kicked out.

There is definitely a plausible case that U.S. retail investors who were part of that $4.4 billion holdings should be refunded their capital because DiDi didn’t truthfully disclose the risk of potential Chinese regulations properly.

There is also the logic that Chinese companies should never be able to list in New York in the first place which would be sensible.

As it stands, Chinese companies don’t need to follow U.S. GAAP accounting standards and cannot be prosecuted by the U.S. legal system if they commit fraud, embezzlement, or any other financial crime and decline to leave Chinese soil.

This incentivizes Chinese companies listed in the U.S. to cheat U.S. investors with fraudulent accounting and deceitful behavior because they aren’t accountable at the end of the day.

The Invesco Golden Dragon China ETF (PGJ), which tracks the performance of US-listed Chinese stocks, has lost more than one-third of its value since February.

I can tell you from close friends who call themselves frontier investors that investing in China is not worth your time and the fear of missing out (FOMO) rationale is all marketing chutzpah and nothing much else.

China’s economy hasn’t had any positive growth in the past 10 years according to Chinese insiders off record.

This FOMO narrative is often peddled by Wall Street “professionals” who are making exorbitant fees for selling retail investors Chinese junk stocks masquerading as real companies.

Out of many financial pros I have talked to, China leads in terms of horror stories from foreign investors.

The Chinese financial system is a hoax created to lure foreign capital in and for it to never leave often viewed as a free lunch for the local recipients.

And I am not only talking about Chinese tech, but this phenomenon also extends to every reach of the financial system there.

At the end of the day, China’s tech aristocracy wished they originated in the United States which is why they went public here because our markets work and theirs don’t.

They got to New York in the first place by marketing false numbers to U.S. investors and concealing regulatory issues, and U.S. investors must not fall for this trap.

If you look at the Shanghai Stock Exchange Composite Index ($SSEC), it’s gone nowhere in the past year and rightly so.

Even Chinese investors don’t buy Chinese stocks because there is no trust in their financial system. They buy property instead or buy U.S. tech stocks.

Don’t be the next sucker.