Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Why am I bullish on Alphabet (GOOGL) short-term?

Video has muscled its way to the peak of the digital content value chain.

If you don't have video streaming, then you are significantly depriving yourself of the necessary ammunition capable of battling against legitimate content originators.

The optimal type of content is short form yet engaging.

Interesting enough, the format method integrated into systems of Facebook (FB) and Twitter (TWTR) has experienced unrivaled success.

They have been leaning on this model as growth levers that will take them to the next stage of revenue acceleration and rightly so.

This has seen smartphone apps such as Instagram become game-changing revenue machines destroying all types of competition.

The x-factor that stands out in Instagram's, Facebook’s, YouTube’s model is that it's free and they do not absorb heavy expenses from content creation.

It’s certainly cheap when the user is the product.

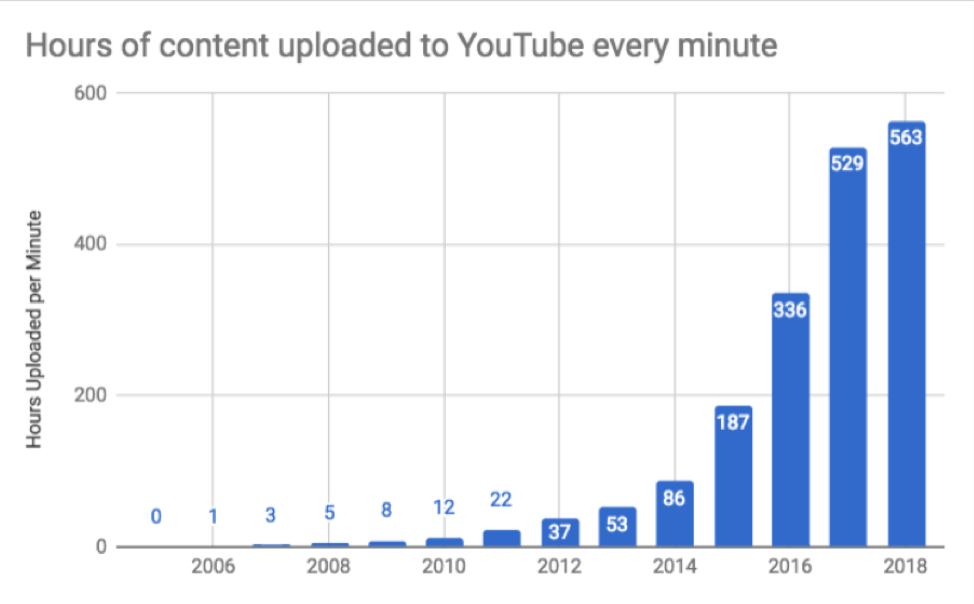

Google’s YouTube service has morphed into something of a phenomenon.

Its interface is easy to use, and followers have a simple time navigating around its platform.

Familiar news outlets such as Sky News, Bloomberg News, and even CNBC news have recently installed their live feeds on YouTube's main platform scared of losing aggregate eyeballs.

And even more intriguing is that YouTube has become a legitimate competitor to Netflix's (NFLX) online video streaming platform.

YouTube has sensed the outsized pivot to their free platform and has double down hard by installing 5-second ads at the front end and middle of videos.

Of Alphabet’s total $39.3 billion revenue pocketed in Q4 2018, ads constituted 83% or an astounding $32.6 billion.

I feel that Alphabet shares are currently undervalued, and I believe that we will see outperformance from Alphabet shares for the rest of 2019 based on YouTube's performance relative to expectation.

YouTube’s ever-growing presence showing up in the top line will offer the growth investors desire to pile into these shares as the company wrestles with future projects such as Waymo.

That's not to say that their traditional advertisement business of Google Search is failing.

Investors can expect continuous 20% to 25% growth in this cash cow business, but the reason why Alphabet share has not been able to break out is that investors have baked this into the pie.

Therefore, YouTube is really the X Factor and will take them to this new promised land with shares surging past the $1,250 mark and more importantly, staying at that level.

YouTube brought in about $15 billion in 2018 and that consisted of about 10% of Alphabet’s total annual revenue.

However, the company is just scratching its surface of what it can accomplish with this fast-growing revenue driver and I can extrapolate this growth segment turning into 20% or 25% of the company’s annual revenue in the next few years.

Google does not strip out YouTube revenue in its reporting, therefore, it's difficult to put my finger on exactly how much YouTube is carving out in terms of revenue.

I can also assume that if Netflix continues to raise the cost of monthly subscription, this strategy will directly hurt its revenue acceleration ability as it relates to competing with Google's YouTube because YouTube's free service is demonstrably attractive to viewers hoping to discover high-quality content relative to a $20 per month Netflix subscription.

I do agree that Netflix is a great company and a great stock, but as they slowly raise the price of content, this will gift YouTube a huge chunk of Netflix’s marginal audience freeing itself from the shackles of Netflix’s price rises.

At some point, online video streaming will become as expensive as the cable bundles now, and at that point, we know that saturation is imminent boding negative for Netflix.

What I do envision in the short-term future are consumers in America will pay into several unique bundles such as Netflix, maybe Disney (DIS), ESPN and merely stick with these as their base content generators as more consumers cut their cord and hard pivot from traditional cable packages that are becoming less appealing by the day.

And don't forget that at some point, Netflix will have to demonstrate profitability and the huge cash burn that permeates throughout the business will be exposed when subscription growth starts to fade away.

In every possible variant, YouTube will become an outsized winner in the media wars because the quality of the free content keeps improving, the cost for consumers stays at 0, and their best of breed ad tech migrating from their Google search into YouTube just keeps getting more surgical and efficient.

Not only are the positive synergies from the best of breed ad tech aiding YouTube’s model, but just think about YouTube having access to the Google cloud and saving expenses by accessing this function to store data onto the Google Cloud.

If this was a standalone service, they would have to subcontract cloud storage functions to third-party cloud company causing the content service to spend millions and millions of dollars per year in expenses.

This would have the potential of crushing the bottom line.

That is just one example of the synergies that Google can take advantage of with YouTube under its umbrella of assets.

And think about self-driving vehicles, Google could potentially equip YouTube as a pre-programmed application inside of autonomous vehicle platform tech with YouTube popping up on the multiple screens.

I assume that there will be multiple screens inside of cars with self-phone driving technology because of the lack of driving required.

The worst maneuver that Alphabet could do right now is spinoff YouTube into its own company, and if that happens, YouTube won't be able to take advantage of the various synergies and benefits of being an Alphabet asset.

We are just scratching the surface of what YouTube can accomplish, and I believe this upcoming overperformance isn’t in the price of the stock yet.

If the Fed continues its “patient” strategy towards interest rates at a macro level, Alphabet will easily soar past $1,250 and it can easily gain another 10% in 2019.

If any “regulation” risk as a result of extremist content rears its ugly head, buy shares on the dips because the algorithms are in place to eradicate this material and any fine will be manageable.

Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

Global Market Comments

October 12, 2018

Fiat Lux

Featured Trade:

(WHY THE STOCK MARKET IS BOTTOMING HERE),

(SPY), (INDU),

(NETFLIX SAYS WE BECOME A NATION OF COUCH POTATOES),

(NFLX), (M), (AMZN), (TSLA), (DIS), (GOOG)

That would be Netflix (NFLX), whose earnings have been on a tear all year, sending the shares soaring.

By this summer the company boasted a staggering 130 million subscribers, with much of the recent growth coming from overseas.

Traders went gaga over the numbers.

Indeed, the firm tracks every keystroke you make.

Watch the sultry tropical thriller Bloodline (sadly scheduled for cancellation), and the company’s clever AI will steer you straight into a like-minded series.

It’s like the “roach motel” network. Once you check in, you can never check out.

Analysts briefly worried about Netflix when Disney (DIS) announced it was pulling its offerings from the omniscient online streaming company, a major seller.

To watch Buzz Lightyear, Woody, and an interminable number of nearly identical princesses (I have three daughters) you’ll have to seek out Disney’s own distribution channel sometime in the future.

But the firm shot back with an $8 billion budget for original content for 2018, in one fell swoop making it one of the largest Hollywood production firms.

Now Netflix is a regular feature of the annual Oscar presentations. Last month it won an impressive 23 Emmys, tying AT&T Warner Media’s HBO for the first time.

They say a picture is worth a thousand words, and I just found 3,000 of them.

Look at three stock charts and you will immediately understand some of the most important structural trends now sweeping through our economy.

Those would be the charts for Amazon (AMZN), Netflix (NFLX), and Macy's (M).

Retail Sales are clearly in a secular long-term decline. Indeed, Macy’s (M) announced last year that it is closing 100 of its 769 stores.

Are these numbers revealing a major new trend in our society? Are we soon to have our every need catered to without lifting a finger?

Have We Become a Nation of Couch Potatoes?

After spending weeks preparing a major research piece for a private client on artificial intelligence, I would have to say that the answer is an overwhelming “Yes!”

Artificial intelligence, or AI, is far more pervasive than you think. Half of all apps now rely on some form of AI, and within five years, all of them will.

Within a decade, AI will cure cancer and most other human maladies, drive our cars, decide our elections, and do our shopping.

You probably all know that Northern California has been besieged with wildfires lately.

Guess what has suddenly started populating my screen? Adds for smoke detectors!

AI has become the leading market theme for 2018.

People my age all remember George Jetson, the space age cartoon series, who only had to work an hour a day because machines did the rest of the work for him.

The modern incarnation of his ultra-light workweek will be far darker and more sinister.

Instead of a one-hour day, it is far more likely that one person will keep a full time eight-hour a day job, while another seven unfortunates become full time unemployed.

By the way, I am determined to be that one guy with a job. So should you.

Indeed, I am increasingly coming across dire predictions that 30% of all jobs will disappear within ten years.

I’m sure that they will.

The real question is whether that 30%, or more, will be replaced by jobs yet to be invented. I bet they will.

Evolution and creative destruction are now happening on fast forward.

After all, some 25% of the professions listed on the Department of Labor website did not exist a decade ago.

SEO manager? Concert social media buzz creator? Online affiliate manager? Solar panel installer? Reputation defender?

What does the stock market do in this new dystopian society? It goes through the roof.

After all, far fewer workers creating a greater output generate much larger earnings that send share prices soaring.

It is all a crucial part of my “Golden Age” scenario for the 2020s.

Having said all that, I think I’ll go binge-watch Netflix’s tropical film noir “Bloodline.” I hear it’s hot.

“Game of Thrones” and “House of Cards” don’t restart until next year.

Global Market Comments

August 7, 2018

Fiat Lux

Featured Trade:

(DON'T MISS THE AUGUST 8 GLOBAL STRATEGY WEBINAR),

(TAKING THE E-TICKET RIDE WITH WALT DISNEY),

(DIS), (NFLX), (FOX),

(A VERY BRIGHT SPOT IN REAL ESTATE)

I'll never forget the first time I met Walt Disney. There he was at the entrance on opening day of the first Disneyland in Anaheim, Calif., in 1955 on Main Street shaking the hand of every visitor as they came in. My dad sold the company truck trailers and managed to score free tickets for the family.

At 100 degrees on that eventful day it was so hot that the asphalt streets melted. Most of the drinking rooms and bathrooms didn't work. And ticket counterfeiters made sure that 100,000 jammed the relatively small park. But we loved it anyway. The band leader handed me his baton and I was allowed to direct the musicians in the most ill-tempoed fashion possible.

After Disney took a vacation to my home away from home in Zermatt, Switzerland, he decided to build a roller-coaster based on bobsleds running down the Matterhorn on a 1:100 scale. In those days, each ride required its own ticket, and the Matterhorn needed an "E-ticket," the most expensive. It was the first tubular steel roller coaster ever built.

Walt Disney shares have been on anything but a roller-coaster ride for the past four years. In fact, they have absolutely gone nowhere.

The main reason has been the drain on the company presented by the sports cable channel ESPN. Once the most valuable cable franchise, the company is now suffering from on multiple fronts, including the acceleration of cord cutting, the demise of traditional cable, the move to online streaming, and the demographic abandonment of traditional sports such as football.

However, ESPN's contribution to Walt Disney earnings is now so small that it is no longer a factor.

In the meantime, a lot has gone right with Walt Disney. The parks are going gangbusters. With two teenaged girls in tow I have hit three in the past two years (Anaheim, Orlando, Paris).

The movie franchise is going from strength to strength. Pixar has Frozen 2 and Toy Story 4 in the pipeline. Look for Lucasfilm to bring out a new trilogy of Star Wars films, even though Solo: A Star Wars Story was a dud. Its online strategy is one of the best in the business. And it's just a matter of time before they hit us with another princess. How many is it now? Nine?

It is about to expand its presence in media networks with the acquisition of 21st Century Fox (FOX) assets, already its largest source of earnings. It will join the ABC Television Group, the Disney Channel, and the aforementioned ESPN.

It has notified Netflix (NFLX) that it may no longer show Disney films, so it can offer them for sale on its own streaming service. Walt Disney is about to become one of a handful of giant media companies with a near monopoly.

What do you buy in an expensive market? Cheap stuff, especially quality laggards. Walt Disney totally fits the bill.

As for old Walt Disney himself, he died of lung cancer in 1966, just when he was in the planning stages for the Orlando Disney World. All that chain smoking finally got to him. Despite that grandfatherly appearance on the Wonderful World of Color weekly TV show, friends tell me he was a complete bastard to work for.

Mad Hedge Technology Letter

July 25, 2018

Fiat Lux

Featured Trade:

(PICHAI YOURSELF, EARNINGS ARE REALLY THAT GOOD),

(GOOGL), (MSFT), (AMZN), (AAPL), (TWTR), (DIS), (TGT)

Google Translate, Alphabet's (GOOGL) free, multilingual machine, foreign language translation service, translates an unimaginable143 billion words per day.

These were one of the pearls divulged in the conference call from Google's CEO Sundar Pichai.

A bump in usage coincided with the 2018 World Cup in Russia, and in the age of low-cost airfare and overpopulation, it could be Alphabet's new cash cow.

Google Translate has the potential to morph into one of the premier foreign language applications used by anyone and everyone.

Forget about the Amazon effect, the Alphabet effect could be just as pungent, albeit away from the trenches of e-commerce.

Thank goodness the application is still ad-free.

No doubt it would be inconvenient to sit through a 15 second ad while interacting with a concierge at a bed and breakfast in the South of France.

Analysts did not sound out Pichai's plans for Google Translate, but he did mention there are some monetization opportunities on the horizon.

The latest earnings report is the most recent indication that the FANGs along with Microsoft are pulling away from the rest.

The equity price action in 2018 vindicates this fact with more than 80% of the gains spread around just a few high caliber tech names.

Is this fair? No. But life isn't fair.

The too slow too late regulation that was supposed to put a cap on the vaunted FANG group has had the opposite effect, squeezing the small guy out of the picture.

The runway is all clear for the FANGs, and the only way they will be stopped is if they stop themselves or an antitrust ruling.

This all adds up to why Alphabet has been a perennial recommendation for the Mad Hedge Technology Letter.

Duopolies are few and far between and monopolies even rarer.

They are great for earnings and as the global digital ad pie grows, it falls down to Google's bottom line.

On the news of stellar earnings, Facebook shares jumped higher in aftermarket trading and powered on to trade around 5% the following day.

Expect a great earnings report from Facebook with robust ad revenue growth.

Nothing less would be a failure of epic proportions.

The migration to mobile is real and investors need to understand analysts cannot keep up with the rising year-end targets in these shares.

Alphabet had a high bar over which to pole vault, and it still managed to beat it handily.

And the $5 billion fine for bundling its in-house apps on Android fell on deaf ears.

Alphabet has $102 billion in the coffers, and $5 billion will do nothing to materially affect the company.

The cash reserves are up from $34 billion in 2010.

The market trampled on any sniff of a risk-adverse sentiment and powered into the green with the Nasdaq reaching another all-time high.

Let's not get too carried away. Alphabet's bread and butter is still its digital ad business with Alphabet CFO Ruth Porat confirming this fact saying, "One of the biggest opportunities for investment continues to be in our ads business."

Alphabet still breaks off 86% of revenue from its distinguished ad business.

"Other" is a category commingling Google Cloud, Google Play, and hardware that only comprised 13 percent of total revenue.

"Other Bets" brings up the rear with 1% of total revenue comprising Waymo, Alphabet's self-driving unit, which is an industry leader putting Tesla and Uber in their place.

Waymo plans to shortly roll out a massive commercial operation. Along with Google Translate, it could carve out a nice position in Alphabet's portfolio going forward.

The most important metric was Alphabet's total ad revenue, which it locked in at $28.1 billion, a 23.9% YOY improvement.

Aggregate paid clicks, a model in which the advertiser pays Google for a user to click an ad, has been steadily rising to 58%, up from 52% from the same time last year.

The masterful efficiency circles back to Google's ad tech team, which is by far the best in the business and has outstanding management.

The Cloud is an area that Alphabet highlights as a place for improvement.

Alphabet's cash war chest allows the company to throw hoards of cash at a problem. When mixed with brilliant management it usually works out kindly.

CFO Porat mentioned that costs were particularly higher in the quarterly head count because of large investments in cloud talent.

Google is tired of playing third fiddle to Amazon (AMZN) and Microsoft (MSFT), and views enhancing the enterprise business as imperative.

This explains Alphabet's head count surge to more than 89,000 employees, sharply higher than the 75,600 employed a year earlier.

Every FANG and high-tier tech company is spending its brains out to compete with each other.

Expanding data centers is not cheap. Neither are the people to deploy it.

Alphabet has the cash to compete with the Amazons and Apples (AAPL) of the world.

They do not have to borrow.

The potential trip wire in Alphabet's earnings report was Google's traffic acquisition cost (TAC).

Alphabet's (TAC) is described as money paid to other companies to direct user traffic to its suite of Google products.

(TAC) went up to $6.4 billion, which is 23% of Google's ad revenue but down on a relative percentage basis of 24%.

This was enough to keep investors from sounding the alarm and was welcomed by analysts.

Alphabet pulled out all the stops this quarter and the momentum is palpable.

Top-line growth from its core ad business shows no sign of slowing.

Acceptable (TAC) was the cherry on the sundae for the quarter at a time when many industry insiders thought it would be around 25% or higher.

Hardware offered less punch than before, which is what all high-quality tech companies desire.

There were no obvious weaknesses and the 34 straight quarters of 23% YOY growth is hard to top.

Google pulls in 10% of all global digital ad dollars in one business.

Other highlights were Waymo eclipsing the 8-million-mile mark of self-driving on public roads as it is the next business to come to the fore.

Google cloud is at an inflection point attempting to win over corporate management.

It has already won contracts with heavy hitters such as Twitter (TWTR) and Disney (DIS).

Pichai mentioned Target (TGT) as a key new cloud client that just signed on with Google last quarter.

More importantly, Alphabet's brilliant quarter bolsters the macroeconomic picture heavily reliant on tech earnings to usher the market through the gauntlet.

Regulation has proved irrelevant. Whatever fine they are slapped with does not change that Google reaps the benefits from its market position as one of the duopolies in the global ad business.

Alphabet has been trading from the bottom left to the upper right via a consistent channel.

Do not chase the new all-time high of $1,270. Use any weakness around the $1,100 level to initiate new positions.

Owning a company this dominant has little downside. The regulatory burden was a myth and Pichai has handled this operation beautifully.

I am bullish on Alphabet and its partner in crime Facebook.

________________________________________________________________________________________________

Quote of the Day

"Man is still the most extraordinary computer of all," said the 35th President of the United States John F. Kennedy.

Mad Hedge Technology Letter

July 18, 2018

Fiat Lux

Featured Trade:

(IS NETFLIX DEAD?),

(NFLX), (AMZN), (FB), (TWTR), (DIS), (GOOGL), (QQQ)