Global Market Comments

March 4, 2022

Fiat Lux

Featured Trade:

(MARCH 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (TSLA), (FCX), (JPM), (BAC), (MS), (TLT),

(TBT),(BA), UPS (UPS), (CAT), (DIS), (DAL),

(GOLD), (VIX), (VXX), (CAT), (BA)

Global Market Comments

March 4, 2022

Fiat Lux

Featured Trade:

(MARCH 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (TSLA), (FCX), (JPM), (BAC), (MS), (TLT),

(TBT),(BA), UPS (UPS), (CAT), (DIS), (DAL),

(GOLD), (VIX), (VXX), (CAT), (BA)

Below please find subscribers’ Q&A for the March 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Do you think Vladimir Putin will give up?

A: He will either be forced to give up, run out of resources/money, or he will suddenly have an accident. When the people see their standard of living go from a per capita income of $10,000/year today to $1,000—back to where it was during the old Soviet Union—his lifespan will suddenly become very limited.

Q: Would you be buying Invesco Trusts (QQQs) on dips?

A: I think we have a few more horrible days—sudden $500- or $1,000-point declines—but we’re putting in a bottom of sorts here. It may take a month or two to finalize, but the second buying opportunity of the decade is setting up; of course, the other one was two years ago at the pandemic low. So, do your research, make your stock picks now, and once we get another absolute blow-up to the downside, that is your time to go in.

Q: Materials have gone up astronomically, are they still a buy?

A: Yes, on dips. I wouldn't chase 10% or 20% one-week moves up here—there are too many other better trades to do.

Q: Is it time to go long aggressively in Europe?

A: No, because Europe is going to experience a far greater impact economically than the US, which will have virtually none. In fact, all the impacts on the US are positive except for higher energy prices. So, I think Europe will have a much longer recovery in the stock market than the US.

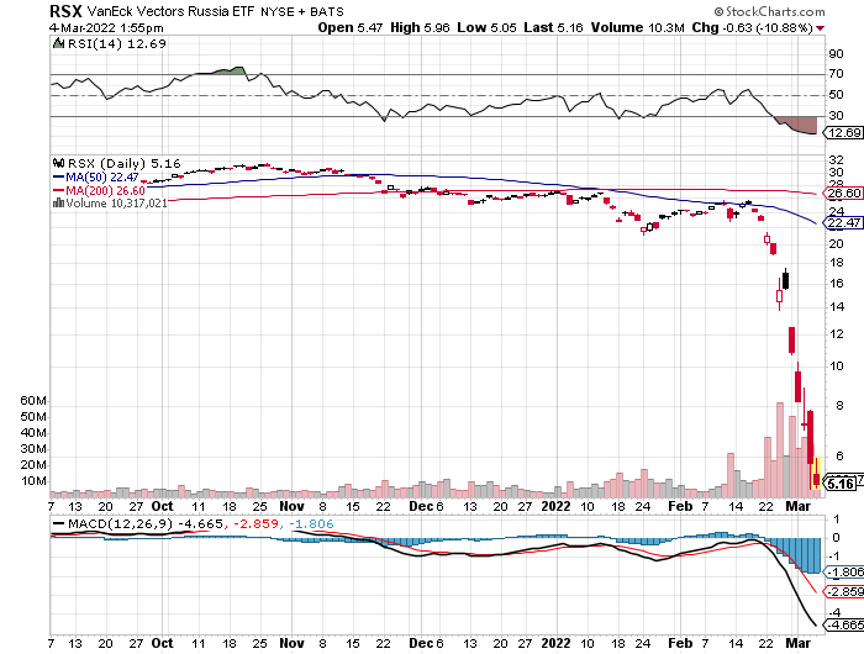

Q: Would you take a flier on a Russian ETF (RSX)?

A: No, most, if not all, of them are about to be delisted because they have been banned or the liquidity has completely disappeared. The (RSX) has just collapsed 85%, from $26 to $4. Virtually all of Russia is for sale, not only stocks, bonds, junk bonds, ETFs, but also joint ventures. ExxonMobil, Shell and BP are all dumping their ownership of Russian subsidiaries as we speak.

Q: Time for a Freeport-McMoRan (FCX) LEAP?

A: No, November was the time for an (FCX) LEAP—we’ve already had a massive run now, up 66% in five months, so wait for the next dip. The next LEAPS are probably going to be in technology stocks in a few months.

Q: My iShares 20 Plus Year Treasury Bond ETF (TLT) call $130 was assigned, What should I do?

A: Call your broker immediately and tell them to exercise your 127 to cover your short in the 130. They usually charge a few extra fees on that because they can get away with it, but you’ve just made the maximum profit on the position. If you haven’t been exercised yet, that 127/130 call spread will expire at max profit in 10 days.

Q: What if I get my short side called away on a position?

A: Use your long side calls to execute immediately to cover your short side. These call spreads are perfectly hedged positions, same name, same maturity, same size, just different strike prices. If your broker doesn’t hear from you at all, they will just exercise the short call and leave you long the long call, and that can lead to a margin call. So the second you get one of these calls, contact your broker immediately and get out of the position.

Q: Is it safe to put 100% of your money in Tesla (TSLA) for the long term?

A: Only if you can handle a 50% loss of your money at any time. Most people can't. It’s better to wait for Tesla to drop 50%, which it has almost done (it’s gotten down to $700), and then put in a large position. But you never bet all your money on one position under any circumstances. For example, what if Elon Musk died? What would Tesla’s stock do then? It would easily drop by half. So, I’ll leave the “bet the ranch trades” for the younger crowd, because they’re young enough to lose all their money, start all over again, and still earn enough for retirement. As for me, that is not the case, so I will pass on that trade. You should pas too.

Q: Do you foresee NASDAQ (QQQ) being up 5-10% or 10-20% by year-end?

A: I do actually, because business is booming across tech land, and the money-making stocks are hardly going down and will just rocket once the rotation goes back into that sector.

Q: We could see an awful earnings sequence in April, which could put in the final bottom on this whole move.

A: That is right. We need one more good capitulation to get a final bottom in, and then we’re in LEAP territory on probably much of the market. We know we’re having a weak quarter from all the anecdotal data; those companies will produce weak earnings and the year-on-year comparisons are going to be terrible. A lot of companies will probably show down turns in earnings or losses for the quarter, that's all the stuff good bottoms are made out of.

Q: What should we make of the Russian threats of WWIII going Nuclear?

A: I think if Putin gave the order, the generals would ignore it and refuse to fire, because they know it would mean suicide for the entire country. Mutual Assured Destruction (MAD) is still in place, and it still works. And by the way, it hasn’t been in the media, but I happen to know that American nuclear submarines with their massive salvos of MIRVed missiles, have moved much closer to Russian waters. So, you're looking at a war that would be over in 15 minutes. I think that would also be another scenario in which they replace Putin: if he gives such an order. This has actually happened in the past; people without top secret clearance don’t know this but Boris Yeltsen actually gave an order to launch nuclear missiles in the early 90s when he got mad at the US about something. The generals ignored it, because he was drunk. And something else you may not know is that 95% of the Russian nuclear missiles don’t work—they don’t have the GDP to maintain 7,000 nuclear weapons at full readiness. Plutonium is one of the world’s most corrosive substances and very expensive to maintain. Only a wealthy country like the US could maintain that many weapons because it’s so expensive. So no, you don’t need to dig bomb shelters yet, I think this stays conventional.

Q: Banks like (JPM), (BAC), AND (MS) are at a low—are they a buy?

A: Yes, but not yet; wait for more shocks to the system, more panic selling, and then the banks are absolutely going to be a screaming buy because they are on a long-term trend on interest rates, strong economy, lowering defaults—all the reasons we’ve been buying them for the last year.

Q: Should I short bonds or should I buy Freeport up 60%?

A: Short bonds. Next.

Q: Should I buy Europe or should I short bonds?

A: Short bonds. That should be your benchmark for any trade you’re considering right now.

Q: How much and how quickly will we see a collapse in defense stocks?

A: Well, you may not see a collapse in defense stocks, because even if Russia withdraws from Ukraine, they still are a newly heightened threat to the West, and these increases in defense spending are permanent. That’s why the stocks have gone absolutely ballistic. Yeah sure, you may give up some of these monster gains we’ve had in the last week, but this is a dip-buying sector now after being ignored for a long time. So yes, even if Russia gives up, the world is going to be spending a lot more on defense, probably for the rest of our lives.

Q: Just to confirm, LEAP candidates are Boeing (BA), UPS (UPS), Caterpillar (CAT), Disney (DIS), Delta Airlines (DAL)?

A: I would say yes. You may want to hold off, see if there’s one more meltdown to go; or you can buy half now and half on either the next meltdown or the melt-up and get yourself a good average position. And when I say LEAPS, I mean going out at least a year on a call spread in options on all of these things.

Q: Is $143 short safe on the (TLT)?

A: Definitely, probably. In these conditions, you have to allow for one day, out of the blue, supers pikes of $3 like we got last week, or $5 trins week, only to be reversed the next day. The trouble is even if it reverses the next day, you’re still stopped out of your position. So again, the message is, don’t be greedy, don’t over-leverage, don’t go too close to the money. There’s a lot of money to be made here, but not if you blow all your profits on one super aggressive trade. And take it from someone who’s learned the hard way; you want to be semi-conservative in these wild trading conditions. If you do that, you will make some really good money when everyone else is getting their head handed to them.

Q: Would you go in the money or out of the money for Boeing (BA) and Caterpillar (CAT)?

A: It just depends on your risk tolerance. The best thing here is to do several options combinations and then figure out what the worst-case scenario is. If you can handle that worst-case scenario without stopping out, do those strikes. These LEAPS are great, unless you have to stop out, and then they will absolutely kill you. And usually, you only do these with sustained uptrends in place; we don’t have that yet which is why I’m saying, watch these LEAPS. Don’t necessarily execute now, or if you do, just do it in small pieces and leg in. That is the smart answer to that.

Q: What’s the probability that the CBOE Volatility Index (VIX) makes a new high in the next 2 weeks?

A: I give it 50/50.

Q: Call options on the VIX?

A: No, that’s one of the super high-risk trades I have to pass on.

Q: How low can the VIX go down this month?

A: High ten’s is probably a worst-case scenario.

Q: LEAPS on Barrick Gold Corporation (GOLD)?

A: No, that was a 3-month-ago trade. Now it’s too late, never consider a LEAP at an all-time high or close to it.

Q: Time to short oil?

A: Not yet. We have some spike top going on in oil. It’s impossible to find the top on this because, while bottoms are always measurable with PE multiples and such, tops are impossible to measure because then you’re trying to quantify human greed, which can’t be done. So yeah, I would stand by; it’s something you want to sell on the way down. This is the inverse of catching a falling knife.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 24, 2022

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or PARACHUTING WITHOUT A PARACHUTE),

(AAPL), (SPY), (MSFT), (TLT), (TBT), (TDOC), (NFLX), (DIS), (VALE), (FCX), (USO), (JPM), (WFC), (BAC), (TSLA), (AMZN), (NVDA)

It has been the worst New Year stock market opening in history.

After a two-day fake-out to the upside, stocks rolled over like the Bismarck and never looked up. NASDAQ did its best interpretation of flunking parachute school without a parachute, posting the worst month since 2008.

Markets can’t hold on to any rally longer than nanoseconds, and the last hour of the day has turned into one from hell.

What is even more confusing is that stocks are now trading like commodities, with massive one-way moves, while commodities, like oil (USO), copper( FCX), and iron ore (VALE) have resumed a steady grind up.

We had a lovefest going on here at Incline Village, Nevada for Technology and Bitcoin researcher Arthur Henry has been staying with me for the week to plot market strategy.

Once the market showed its hand, I sold short Microsoft (MSFT), which elicited torrents of complaints from readers. Then Arthur sold short Netflix (NFLX), inviting refund demands. Then I sold short Apple (AAPL), prompting accusations of high treason. Then Arthur sold short Teledoc (TDOC). There wasn’t a lot of talking, but frenetic writing and emailing instead.

Followers cried all the way to the bank.

In a mere two weeks, the price earnings multiple for the S&P 500 plunged from 22X to 20X. A lot of traders were only buying stock because they were going up. Take out the “up” and Houston we have a problem.

The entire streaming industry seems to have gone up in smoke and ex-growth practically overnight. Netflix (NFLX) delivered a gob smacking 29.5% swan dive in the wake of disappointing subscriber growth forecasts. Walt Disney (DIS), which ate the Netflix lunch, was dragged down 10% through guilt by association.

It is often said that the stock market has discounted 12 of the last six recessions. It is currently pricing in one of those non-recessions. What we are seeing is a sudden growth scare of the first order.

Despite last week’s carnage, stocks are still the most attractive asset class in the world, offering a potential 10% return in 2022. The problem is that they may make that 10% profit starting from 10% lower than here.

Despite all the red ink, big tech stocks are still on track to see a 30% earnings growth this year, and they account for a hefty 28% of the market.

Let’s look at Apple’s past declines for guidance on this meltdown.

Steve Jobs’ creation gave back 60% in the 2008 Great Recession, 34% during the 2015 growth scare, 48% during the great 2018 Christmas collapse, and 28% in the 2020 pandemic crash. So, the good news is that you won’t get killed by this selloff, you’ll just lose an arm and a leg. But they’ll grow back.

Remember, it’s always darkest just before it goes completely black. This correction is survivable, although it may not seem so at the moment.

It does vindicate my 2022 view that the first half will be about survival and that big money can be had in the second half.

So far, so good.

The Market is De-Grossing Big Time. That means cutting total market exposure and selling everything, regardless of stock or sector. The market is discounting a recession and bear market that isn’t going to happen, which occurs often. When it ends in a few weeks, interest rate sensitives, especially the banks, will bounce back hard, but tech won’t. Buy (JPM), (WFC), and (BAC) on bigger dips.

The Bond Collapse Goes Global, with German 10-year bunds going positive for the first time in three years, up 40 basis points in a month. Yes, inflation is finally hitting the Fatherland, home of post-WWI billion percent inflation. Eurozone inflation just topped 5%, well above its 2% target. British inflation hit a 30-year high. The move has lit a fire under all Euro currencies. Methinks the down move in (TLT) has more to go.

Fed to Raise Rates Eight Times, says Marathon Asset Management. That’s what will be needed to curb the current runaway inflation now at 7.0% and still rising. Personally, I think it will be 12 quarter-point increments to peak out at a 3 ¼% overnight rate. Any more and Powell might bring on a recession.

NASDAQ is Officially in Correction, down 10%, in the wake of poor performance this month. It’s the fourth one since the pandemic began two years ago. Tesla (TSLA), Amazon (AMZN), and NVIDIA (NVDA) have been leading the swan dive, all felled by rapidly rising interest rates. This could go on for months.

Weekly Jobless Claims Hit 286,000, a four-month high, as omicron sends workers fleeing home.

Goldman Sachs (GS) Gets Crushed, down 8%, on disappointing earnings. Tough market conditions are fading trading volumes while 2021 bonuses were through the roof. The move is particularly harsh in that buyers were flooding in right at support at the 200-day moving average.

China GDP (FXI) Grows 8.1% YOY but is rapidly slowing now, thanks to Omicron. China was first in and first out with the pandemic but is getting hit much harder in this round. That has prompted new mass lockdowns which will make out own supply chain problems worse for longer. In Chinese, “lockdown” means they weld your door shut, unlike here. Harsh, but it works.

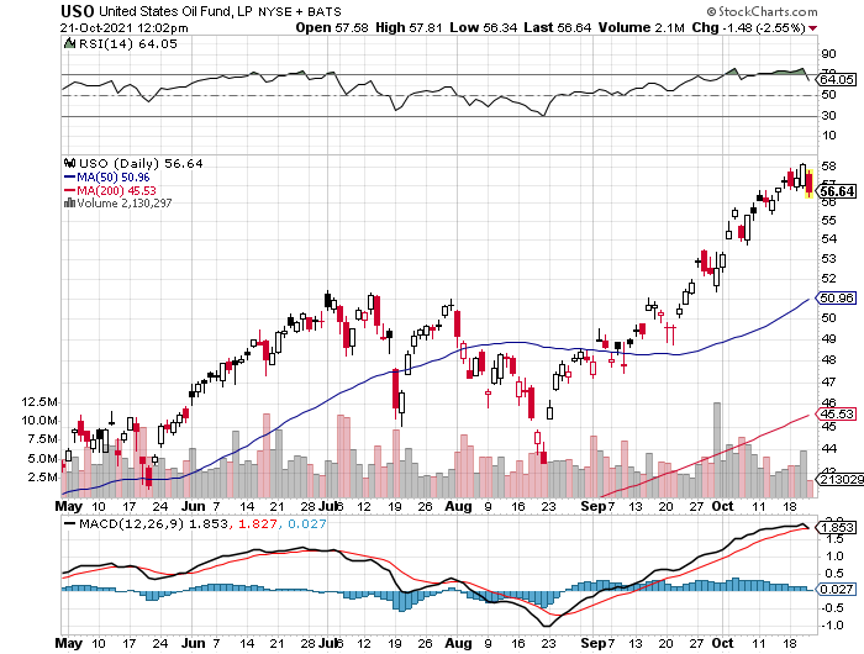

Oil (USO) Hits Seven-Year High, as inventories hit a 21-year low. No new capital is entering the industry, crimping supplies as old fields play out. The threat of a Russian invasion of the Ukraine is prompting advance stockpiling. Russia is the world’s second-largest oil exporter.

Existing Homes Sales Hit a 15-Year High, at 6.12 million, the best since 2006. December fell 4.6%. Extreme inventory shortage is the issue, with only 910,000 homes for sale at the end of the year, an incredibly low 1.8-month supply. You can’t find anything on the market now, to buy or rent. The median price of a home sold in December was $358,000, a 15.8% gain YOY.

Bitcoin (BITO) Crashes, decisively breaking key support at $40,000. Non-yielding assets of every description are getting wiped. Bail on all crypto options plays asap.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my January month-to-date performance bounced back hard to 5.05%. My 2022 year-to-date performance also ended at 5.05%. The Dow Average is down -6.12% so far in 2022.

Once stocks went into free fall, I piled on the short positions as fast as I could write the trade alerts, including in Microsoft (MSFT), Apple (AAPL), and a double short in the S&P 500 (SPY). I also increased my shorts in the bond market (TLT) to a triple position. When prices became the most extreme, when the Volatility Index (VIX) hit $30, I bought both (SPY) and (TLT).

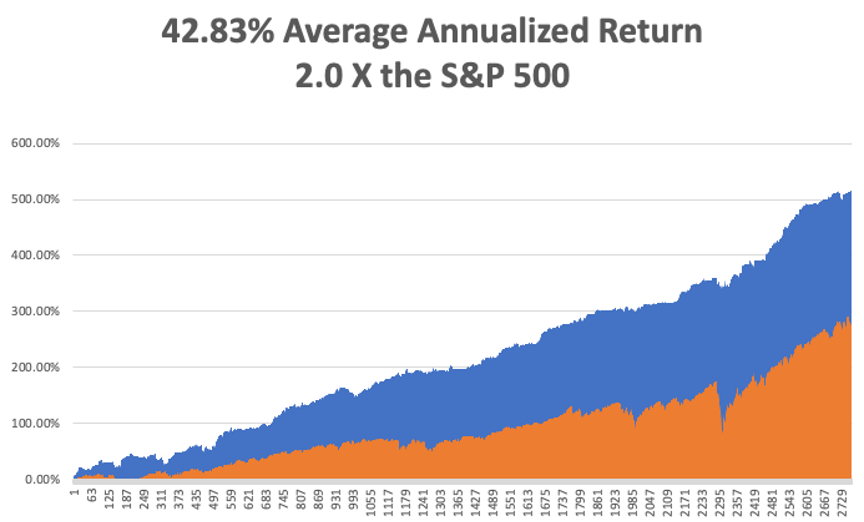

If everything goes our way, we should be up 14.26% by the February 18 options expiration.

That brings my 12-year total return to 517.61%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.82% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 71 million and rising quickly and deaths topping 866,000, which you can find here.

On Monday, January 24 at 6:45 AM, The Market Composite Flash PMI for January is out. Haliburton (HAL) reports.

On Tuesday, January 25 at 6:00 AM, the S&P Case Shiller National Home Price Index for November is released. American Express (AXP) reports.

On Wednesday, January 26 at 7:00 AM, the New Home Sales for December are published. At 11:00 AM The Federal Reserve interest rate decision is announced. Tesla (TSLA), Boeing (BA), and Freeport McMoRan (FCX) report.

On Thursday, January 27 at 8:30 AM the Weekly Jobless Claims are disclosed. We also get the first look at US Q4 GDP. Alaska Air (ALK) and US Steel (X) report.

On Friday, January 28 at 5:30 AM EST US Personal Income & Spending is printed. Caterpillar (CAT) reports. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I drove up to visit my pharmacist in Incline Village, Nevada, I warned him in advance that I had a question he never heard before: How good is 80-year-old morphine?

He stood back and eyed me suspiciously. Then I explained in detail.

Two years ago, I led an expedition to the South Pacific Solomon Island of Guadalcanal for the US Marine Corps Historical Division (click here for the link). My mission was to recover physical remains and dog tags from the missing-in-action there from the epic 1942 battle.

Between 1942 and 1944, nearly four hundred Marines vanished in the jungles, seas, and skies of Guadalcanal. They were the victims of enemy ambushes and friendly fire, hard fighting, malaria, dysentery, and poor planning.

They were buried in field graves, in cemeteries as unknowns, if not at all left out in the open where they fell. They were classified as “missing,” as “not recovered,” as “presumed dead.”

I managed to accomplish this by hiring an army of kids who knew where the most productive battlefields were, offering a reward of $10 a dog tag, a king's ransom in one of the poorest countries in the world. I recovered about 30 rusted, barely legible oval steel tags.

They also brought me unexploded Japanese hand grenades (please don’t drop), live mortar shells, lots of US 50 caliber and Japanese 7.7 mm Arisaka ammo, and the odd human jawbone, nationality undetermined.

I also chased down a lot of rumors.

There was said to be a fully intact Japanese zero fighter in flying condition hidden in a container at the port for sale to the highest bidder. No luck there.

There was also a just discovered intact B-17 Flying Fortress bomber that crash-landed on a mountain peak with a crew of 11. But that required a four-hour mosquito-infested jungle climb and I figured it wasn’t worth the malaria.

Then, one kid said he knows the location of a Japanese hospital. He led me down a steep, crumbling coral ravine, up a canyon and into a dark cave. And there it was, a Japanese field hospital untouched since the day it was abandoned in 1943.

The skeletons of Japanese soldiers in decayed but full uniform laid in cots where they died. There was a pile of skeletons in the back of the cave. Rusted bottles of Japanese drugs were strewn about, and yellowed glass sachets of morphine were scattered everywhere. I slowly backed out, fearing a cave-in.

It was creepy.

I sent my finds to the Marine Corps at Quantico, Virginia, who traced and returned them to the families. Often the survivors were the children or even grandchildren of the MIAs. What came back were stories of pain and loss that had finally reached closure after eight decades.

Wandering about the island, I often ran into Japanese groups with the same goals as mine. My Japanese is still fluent enough to carry on a decent friendly conversation with the grandchildren of their veterans. It turned out I knew far more about their loved ones than they. After all, it was our side that wrote the history. They were very grateful.

How many MIAs were they looking for? 30,000! Every year, they found hundreds of skeletons, cremated in a ceremony, one of which I was invited to. The ashes were returned to giant bronze urns at Yasakuni Ginja in Tokyo, the final resting place of hundreds of thousands of their own.

My pharmacist friend thought the morphine I discovered had lost half of its potency. Would he take it himself? No way!

As for me, I was a lucky one. My dad made it back from Guadalcanal, although the malaria and post-traumatic stress bothered him for years. And you never wanted to get in a fight with him….ever.

I can work here and make money in the stock market all day long. But my efforts on Guadalcanal were infinitely more rewarding. I’ll be going back as soon as the pandemic ends, now that I know where to look.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

True MIAs, the Ultimate Sacrifice

My Collection of Dog Tags and Morphine

My Army of Scavengers

Dad on Guadalcanal (lower right)

Mad Hedge Technology Letter

November 12, 2021

Fiat Lux

Featured Trade:

(PEAK STREAMING GROWTH ISN’T THE END OF STREAMING)

(DIS), (NFLX), (AMZN)

Peak streaming — that’s what the indicators are telling us.

It’s been a good run — lots of money made so far.

The streaming industry is resting after the pandemic pulled revenue forward a few years.

It won’t be as easy now, as the maturity of the industry means that it becomes a war inside the war, instead of the tide-lifts-all-boats type of growth.

The latter is what everyone hopes, but doesn’t always get.

The world’s largest entertainment company, Disney, posted a significant slowdown in subscriber sign-ups at its flagship streaming service in the most recent quarter.

Disney+ added only two million subscribers last quarter bringing its total to 118.1 million.

Analysts had expected this quarter’s total to come to 125.3 million. During the previous quarter, Disney+ had added more than 12 million new subscribers.

First, the follow-through from consumers just wanting to experience outside and the services attached to them ring true.

The price hikes are also another net negative, as it makes consumers less enthused about signing up.

This had to be expected and many of these streaming companies would honestly admit that they couldn’t continue the pandemic era performance.

A reversion to the mean is not the end of streaming and Disney’s streaming services.

It is still on track to reach previous guidance of between 230 million and 260 million paid Disney+ subscribers globally by the end of fiscal 2024.

Dig deeper into the streaming data and it shows that customers in India didn’t sign up because of a delay of Indian Premier League cricket games that were to air on the service.

Another indicator of the pivot to outside business is the Disney theme park revenue climbing 99%.

The trend towards outdoor activities means a slew of cancellations of the monthly subscriptions.

Netflix was the rare streaming company that bucked the trend.

Netflix streaming service added 4.4 million subscribers—or about a million more than it had forecast—on the strength of new popular shows like “Squid Game.”

Moving forward, the bar rises quite a bit for the quality of content.

Viewers are demanding more or they are riding Space Mountain in Anaheim.

Streaming companies won’t be able to pedal out mediocre shows and movies, and secondly, there is no patience for customers as the number of streaming options has multiplied.

The deeper underbelly shows us that the general trend of linear TV cancellations and streaming signups appears to be continuing even if the rate of signups is slowing.

Disney, WarnerMedia, and AMC Networks all reaffirmed previous full-year and future year forecasts. And while pandemic gains may have slowed, production slowdowns and shutdowns have also ended, which will lead to a surge of new content for all of the streaming services.

Disney investors will be zeroed in to see if the company can pump out some blockbusters, but a glut of content might mean not enough eyeballs to digest these blockbusters.

Coronavirus-related production delays continue to disrupt its pipeline of content delivery.

Disney subscriber growth could ramp back up in the latter half of 2022 when they have better titles coming to market.

Another issue for Disney is if they are willing to produce more adult content and veer away from the younger cohort they are used to entertaining.

I don’t mean X rated, but the 25-44 aged bunch, everyone is sick of the superhero movies.

When it comes to attracting subscribers to Disney+, the company in November and December will be relying on a Beatles documentary, “The Beatles: Get Back,” additional Marvel Studios and Lucasfilm Ltd. shows and films that include a new “Home Alone” feature.

In April, Jeff Bezos said more than 175 million Amazon Prime members had streamed shows and movies in the past year.

Beyond the big three — Netflix, Disney+, and Amazon Prime — things get cloudier.

In July, NBCUniversal’s Peacock reported 54 million net new subscribers and more than 20 million monthly active accounts.

Other players with potentially strong platforms include WarnerMedia’s HBO Max, with a reported 69.4 million global subscribers, and Apple TV+, which is rumored to have about 20 million U.S. subscribers.

The major streaming competitors are also actively expanding their footprint abroad to acquire more growth, but the issue I have there is that the average revenue per user (ARPU) is nothing close to what it is in North America.

Although oversees revenue could provide a little bump to earnings, it won’t recreate their earnings composition.

Which leads me to a broader take on tech, it’s slowing down because we have been in the same cycle which was essentially initiated by the smartphone, the cloud, 3G super apps, and high-speed internet.

Those super levers are showing exhaustion.

It’s not a coincidence that Facebook’s Mark Zuckerberg was desperately trotting out his vision for the Metaverse and Apple removing personal data tracking from its ecosystem.

These are late cycle signs that shouldn’t be missed.

Big tech has become a great deal more mercantilist during the latter half of this bull market, yet we aren’t at the point of cannibalization, but I do envision that moment 5-7 years out from now.

Until then, high quality tech will grind higher while slowly raising their monthly prices, and the low-quality tech products will fall by the wayside because they lack the killer content.

Global Market Comments

October 22, 2021

Fiat Lux

Featured Trade:

(OCTOBER 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(DIS), (TLT), (TBT), (FXI), (BABA), (BIDU), (JD), (USO), (JPM), (MS), (GS), (BITO), ($BTCUSD)

Below please find subscribers’ Q&A for the October 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Why are stocks so high? Won’t inflation hurt companies?

A: Inflation hurts bonds (TLT), not companies, which is why we are short the bond market and have been short for most of this year. Inflation actually helps companies because it allows them to raise prices at a faster rate. The ability to raise prices is the best that it’s been in 45 years, and that is enabling them to either maintain or increase profit margins.

Q: Where is all this liquidity coming from to drive the stocks high after the Fed ends Quantitative easing?

A: In the last 20 years, the liquidity of the US has gone from 6% of GDP to 47% of GDP. That is an enormous increase, and most of that money has gone into stocks and real estate, which is why both have been on a tear for the last 11 years. And I expect that to continue; the Fed isn’t even hinting at taking liquidity out of the system until well into 2023. On top of that, you have corporate profit exploding from $2 trillion last year to $10 trillion this year, adding another $8 trillion to the system, and outpacing any Fed taper by a five to one margin. Corporations alone are using these profits to buy back more than $1 trillion of their own stock this year.

Q: I’m hearing so much about the supply chain problems these days. Is that just a short-term fixable problem or a long-term structural one?

A: Absolutely it’s short-term. This actually isn’t a pandemic-related problem but a private capital investment one. It’s being caused by the record growth of the US economy which is sucking in more imports than it has ever seen before. We’ve actually exceeded pre-pandemic levels of imports a while ago. Import infrastructure isn’t big enough to handle it. If it was there wouldn’t be enough truckers to handle it. We had a shortage of 50,000 truckers before the pandemic, now we’re short 100,000. Some of these guys are making up to $100,000 a year, not bad for a high school level education. Expect it to get worse before it gets better, but it will get better eventually. That is why Amazon is having trouble, because supply chain problems may bring a weak Christmas, which is the most profitable time of year for them. If we get any big selloff at Amazon for this reason, you want to buy that bottom because it’ll double again in 3 years.

Q: Walt Disney (DIS) has pretty much sideways the whole year around $70, is this going down or should I buy?

A: I would look to buy but I would buy an in-the-money LEAPS, like a $150-$170 one year out. Disney’s been hit with a lot of slowdowns lately, slowdowns with park reopening, movie releases, new streaming customers. But these are all temporary slowdowns and will pick up again next year. Disney is the classic reopening play, so you will get another bite at the apple with a second reopening. Maybe “bite of the mouse” is a better metaphor.

Q: Global growth is down because of China (FXI) with their PMI under 50; do you think they will drag down the entire global economy in 2022?

A: No, if we recover, their largest customer, they will recover too. Remember their pandemic cases are only a tiny fraction of what ours were, some 4,000 or so, and their economy is still export-driven. You can't have major port congestion in Los Angeles and a weak economy in China, those are just two ends of one chain. I would look for a recovery in China next year. As for the stocks, I don’t know because that’s an entirely political issue; Baidu (BIDU), (JD), and Alibaba (BABA) are still getting beaten like a redheaded stepchild. We don’t know when that’s going to end; it’s an unknown. So, stand aside on Chinese plays, especially when the stuff at home is so much better with all these financials and tech stocks to invest in.

Q: What do you think about meme stocks?

A: I think you should avoid them like the plague. When there are so many good quality stocks with long term uptrends, why bother dumpster diving? You’re better off buying a lottery ticket.

Q: Which US bank should I invest in?

A: If you want the gold standard, you buy JP Morgan (JPM) which just announced blowout earnings. If you want a broker, go for Morgan Stanley (MS), which also just announced blowout earnings last week. And I want you to make my monthly pension payment secure, as it comes from Morgan Stanley. Keep those checks coming!

Q: Are we headed to $150 oil (USO)?

A: No, what we’re seeing here is a short-term spike in prices due to supply chain problems, OPEC discipline, a booming economy, and Russia trying to squeeze Europe on energy supplies. I don’t see it continuing much per year as the stocks could be popping out, so avoid oil and energy plays. The solar plays, like (TAN), (FSLR), and (SPWR) on the other hand, all look like they have miles to go.

Q: You said in your Webinar that you can still get a 50% Return on the United States Treasury Bond Fund (TLT) LEAPS. Can you give me the specifics?

A: If you went a year out on Tuesday when I recorded this webinar, you could buy the (TLT) October 2022 $150-$150 vertical bear put spread for $3.40 for a maximum profit on expiration at $5.00 of $47%. That’s where you buy the $155 put and sell short the $150 put against it. Since then, bonds have fallen by $3.00, and it is now trading at $3.60 giving you a 39% return. Try to establish this position on the next (TLT) rally.

Q: What is your yearend target for Bitcoin?

A: Now that we have broken the old high at $66,000, we should be able to make it to $100,000 by January. The SEC approving that new ProShares Bitcoin Strategy ETF (BITO) ETF unlocks trillions of dollars which can now go into Bitcoin, those regulated by the Investment Company Act of 1940. Crypto is now the fastest-growing segment of the financial markets. It’s inflation that driving this, and the Fed is throwing fuel on the fire by taking no action in the face of a red hot 5.4% Consumer Price Index. Even if the Fed does taper, the action will be more than offset by the massive $8 trillion increase in corporate profits. Companies are not only buying their own stocks, they are also using these profits to buy Bitcoin. I see this as a Bitcoin node myself. Be sure to dollar cost average your position by putting in a little bit of money every day because Bitcoin is wildly volatile, up 140% since August 1. By the way, it’s not too late to subscribe to the Mad Hedge Bitcoin Letter, which we are taking down from the store on Monday for a major upgrade by clicking here. We are raising prices after that.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on the paid service you are currently in (GLOBAL TRADING DISPATCH, TECH LETTER, or BITCOIN LETTER), then select WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good luck and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 1, 2021

Fiat Lux

Featured Trade:

(CONNECTED TV IS ON FIRE)

(TTD), (DIS), (FUBO)

One of my favorite ad tech companies has to be The Trade Desk (TTD).

They are a middleman of sorts, using an in-house platform to match the inventory of digital ads with the advertisers themselves.

They have been extremely effective at harnessing data to deliver the right ads to the right people and many major streaming companies and Fortune 500 companies are reaching out to them to figure out how to deploy ads in the most systematic way possible.

Let’s just say there is a lot of slippage going on in the linear industry where wrong ad placement is common.

Performance of late has been strong in TTD — more of the world's top advertisers and their agencies signed up or expanded their use of TTD’s platform, which just continues to validate their business strategy.

Companies are now increasingly embracing the opportunities of the open Internet in contrast to the limitations of walled gardens.

The highlight of last quarter’s performance is led by Connected TV (CTV) and premium video.

What is CTV in advertising? CTV is short form, skippable online advertising targeted to relevant content channels and/or audience groups. Connected TV (CTV) refers to any TV that can be connected to the internet and access content beyond what is available via the normal offering from a cable provider.

The CTV growth coincides with a broad move from broadcast and cable to digital on-demand content that is happening all over the world.

CTV as a percentage of TTD’s business continues to grow very rapidly and is, by far, their fastest-growing channel.

Overall, total revenue was up 101% from a year ago to $280 million, significantly surpassing in-house expectations.

Growth occurred mainly because of TTD’s latest platform launch, Solimar, which is the result of more than two years of engineering work, and it addresses many of the opportunities in front of agencies and brands today.

Just to provide some context on growth in CTV, through just the first half of this year, the number of brands spending more than $1 million in CTV to TTD has already more than doubled year over year.

And it's not just larger advertisers that are taking advantage of CTV anymore. The number of advertisers spending over $100,000 has also doubled. In total, TTD has nearly 10,000 CTV advertisers, up over 50% compared to last year.

That exponential growth speaks to how rapidly the TV landscape is evolving. The accelerated consumer shift to digital video is real, including CTV. And that shows no signs of slowing down.

In fact, TTD reached more households via CTV in the U.S. today than are reachable through linear TV. Today, TTD reaches more than 87 million households. Those trends are now well established.

MoffettNathanson recently reported that the ad-supported video-on-demand market is growing from $4.4 billion in 2020 to about $18 billion as early as 2025.

And every major ad-supported platform, whether it's Disney's Hulu, Peacock, Discovery Plus, ViacomCBS' Paramount and Pluto, FOX's 2B or fuboTV and many others, all are reporting record viewership or ad spend figures.

Broadcasters recognize that the traditional upfront process is a mismatch. It doesn't work in a digital world where data and personalization are required to succeed.

The legacy upfront process is really hard to run in an environment with lots of change and lots of uncertainty. I believe that this year will mark a turning point in how the process is managed. In today's fragmented TV environment, linear audiences continue to erode, linear supply is shrinking and the prices are rising simply because of the scarcity. This year, broadcasters use that scarcity to their advantage and lock up commitments as the demand for growth intensifies.

When compared to parallel linear TV ad campaigns, CTV delivered a 51% incremental reach and a four times improvement when analyzing cost per household reach. These are not isolated cases.

Retail is a point of emphasis this year with Walmart integrating Walmart shopper data on TTD’s platform. This is a leading example of how TTD is working with advertising customers to help unlock the value of retail data estimated at $100 billion to $200 billion market.

This is a highly volatile stock and 2021 has been a year of consolidation.

If TTD comes down to $60 from the $70 today, that should represent an optimal entry point into one of the hottest sub-industries in tech.