A better headline for this piece might have been “Ten stocks to Buy at the Bottom”, except that you have to redefine the word “bottom.”

The rules of the greatest liquidity-driven market of all time demand a different explanation of The NEW bottom, and that is something that hasn’t gone up lately.

And that would be big tech, which appears ready to blast out to the upside from a six-month long sideways “time” correction.

It would be a perfectly rational thing to see in these highly irrational markets. After all, these names just announced blockbuster earnings presaging greater things to come. And these companies actually HAVE earnings, compared to recent market frontrunners, which have none at all.

Coming in here and betting the ranch is now a no-lose trade. If I’m right, the pandemic ends in three months, stocks will soar. If I’m wrong and the global epidemic explodes from here, you’ll be dead anyway and won’t care that the stock market crashed further.

Needless to say, I have a heavy tech orientation with this list, far and away the source of the bulk of earnings growth for the US economy for the foreseeable future. If anything, the coronavirus will accelerate the move away from shopping malls and towards online commerce as consumers seek to shy away from direct contact with the virus.

What would I be avoiding here? Directly corona-related stocks like those in airlines, hotels, casinos, and cruise lines. Avoid human contact at all cost! There is no way of knowing when or where these stocks will bottom. Only the virus knows for sure.

Microsoft (MSFT) – still has a near-monopoly on operating systems for personal computers and a huge cash balance. Their inroads with the Azure cloud services have been impressive.

Apple (AAPL) – Even with the Coronavirus, Apple still has a cash balance of $225 billion. Its 5G iPhone launches in the fall, unleashing enormous pent-up demand. Apple’s rapid move away from a dependence on hardware to services continues.

Alphabet (GOOGL) – Has a massive 92% market share in search and remains the dominant advertising company on the planet.

QUALCOMM (QCOM) – Has a near-monopoly in chips needed for 5G phones. It also won a lawsuit against Apple over proprietary chip design. In the very near future, you won’t be able to do ANYTHING without 5G. It’s also not a bad idea to own a chip stock during the worst global chip shortage in history.

Amazon (AMZN) – The world’s preeminent retailer is growing by leaps and bounds. Dragged down by its association with the world’s worst industry, (AMZN) is a bargain relative to other FANGs.

Visa (V) – The world’s largest credit company is a call on the growth of the internet. We still need credit cards to buy things. And guess what? Coronavirus will accelerate the move of commerce out of malls where you can get sick to online where you can’t.

American Express (AXP) – Ditto above, except it charges higher fees and has snob appeal (read higher margins). Its stock has lagged Visa and MasterCard in recent years.

NVIDIA (NVDA) – The leading graphics card maker that is essential for artificial intelligence, gaming, and bitcoin mining. Another great chip play that has flatlined for half a year.

Advanced Micro Devices (AMD) – Stands to benefit enormously from the chip shortage created by the coming 5G and the explosion of the cloud.

Target (TGT) – The one retailer that has figured it out, both in their stores and online. It can’t be ALL tech.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Looks Like a “BUY” Signal to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/buy-signal.png484864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-12 10:02:012021-02-12 10:09:26Ten Stocks to Buy Before You Die

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ASSET SHORTAGE),

(INDU), (PFE), (MRNA), (PTON), (DOCU), (ETSY),(CAT), (JPM), (BABA),(TSLA), (TLT), (ABNB), (DIS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-14 09:04:542020-12-14 09:39:35December 14, 2020

Markets are wonderful arbiters of the laws of supply and demand.

When there is a shortage of a particular security, Wall Street has a magical ability to manufacture more by running the printing presses to meet supply, or in the modern incarnation, open the spreadsheets.

Except for this time.

The amount of new cash created by global quantitative easing and the prolific saving habits of locked up Americans are creating more demand than even this efficient highly process can accommodate.

Which means that prices can only go up.

How long and how far is anyone’s guess. My target for the Dow Average is 120,000 in ten years, but even I don’t expect that to take place in a straight line. So, we are all sitting on our hands waiting for the next pullback to buy into, which may….or may not ever happen.

A lot of Dotcom Bubble memories are rising up from the dead. Analysts in 1999 made outlandish forecasts of stocks rising 50% in a year, which then took place in four days. That happened to Tesla (TSLA) last month and Airbnb (ABNB) last week.

In the meantime, the smartest traders, call them the oldest traders, are taking profits on the best years of their careers.

Of course, the short-term direction of the market will be determined by the January 5 Georgia Senate election, where the polls are in a dead heat. The last time this happened, during the presidential election, the Democrats won by a microscopic 15,000 vote margin.

If history repeats itself, the Biden administration will get an extra $6 trillion to play with to restore the shattered US economy. Think $2 trillion for infrastructure spending in all 50 states, $2 trillion for the rescue of bankrupt states and municipalities, $1 trillion for alternative energy and EV subsidies, and another $1 trillion in odds and ends. Needless to say, much of this will end up in the stock market.

I am getting a lot of questions these days regarding what will end this once-in-a-generation runaway bull market. The pandemic created this bull market by accelerating technology, business evolution, and corporate profitability by ten years. I bet a year ago, you weren’t spending your day on Zoom meetings, as I was.

The great irony is that the Pfizer (PFE) and Moderna (MRNA) vaccines may not only kill Covid-19 but the bull market as well. That’s because money will then come out of stocks and go back to the real economy.

That makes pandemic darlings like Peloton (PTON), DocuSign (DOCU), and Etsy (ETSY) especially risky. But then 6% growing GDPs were never what stock market crashes were made of, so any declines will be modest.

As for my own positions, I have a rare 100% long portfolio, mostly Tesla, but also the (TLT), (CAT), (JPM), and (BABA), 80% of which expires with the option expiration on Friday, December 18.

After that, I’ll take it easy with 10% short (TLT) and 10% long (TSLA) and wait for the market, or Georgians to tell me what to do. A flood of money is to hit the stock market, says hedge fund legend Ray Dalio. The US is facing a perfect storm in favor of all risk assets. There is no reason why price earnings multiples for American stocks can’t reach 50X, double the current 25X. Buy what the central banks are buying. The funny thing is that I agree with Ray on everything. Buy risk on dips.

Stocks will keep soaring into 2021, says JP Morgan strategist Marko Kolanovik. The more risk the better. The Fed will keep interest rates low for at least another year, and ultra-low rates will force big institutions out of bonds and into stocks. Volatility (VIX) will decline. It all sounds like a great long stock/short bond trade to me. Hmmmmm.

Tesla completed a $5 Billion share issue, after a move to $650, up $142 from my November Mad Hedge BUY recommendation. The stock seems hell-bent on testing the Goldman Sachs $780 price recommendation before the December 18 S&P 500 entry. Elon Musk’s creation is now worth a staggering $608 billion. It’s the best recommendation in the 13-year history of the Mad Hedge Fund Trader.

San Francisco rents dive 35%, as tech workers flee to the suburbs. A lot of remote work is now permanent. Studio apartments are now a mere $2,100, and a one-bedroom can be had for $2,716. For a two-bedroom if you have to ask, you don’t need to know. Shocking! Sales of million-dollar homes are soaring, as ultra-low interest rates persist and people spend much more time at home. So, bigger for your pod is better. Mortgages over $766,000 are up 57% YOY. Jamie Diamond says he wouldn’t touch bonds with a ten-foot pole, and nor would I. A 91-basis point yield just doesn’t do it for the chairman of JP Morgan Chase (JPM), one of my recurring longs. Stocks are a much better choice, even if there is a bubble in progress. Keep selling every rally in fixed income, especially the (TLT).

Weekly Jobless Claims soar to 853,000, up a massive 153,000 from the previous week. To see this happen during the Christmas hiring season is heartbreaking. With 200,000 a day falling to Covid-19, I’m surprised it's not higher, which means it will be. This is what peaks look like. Washington has totally given up. An $800 billion payday for the bay area. That is the amount of wealth created by just two companies, Tesla (TSLA) and Airbnb (ABNB), since March. And the great majority of shareholders live in the San Francisco Bay Area, including its venture capital and pension funds. No wonder home prices in the suburbs are up 20% YOY. The great irony is that (ABNB) received a massive government bailout only in March. I hope they repay the loans early. Is Cuba the next big play? A Biden détente could lead to the emerging market investment opportunity of the decade with the $43 million Herzfeld Caribbean Basin Fund (CUBA). It just had its best month in 11 years (like many of us). With Fidel Castro long dead, what’s the point in continuing a 60-year-old cold war. A big market for American products and services beckons, not to mention the tourism and cruise opportunities. But can Biden afford to lose the Florida Cuban vote in the next election? When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

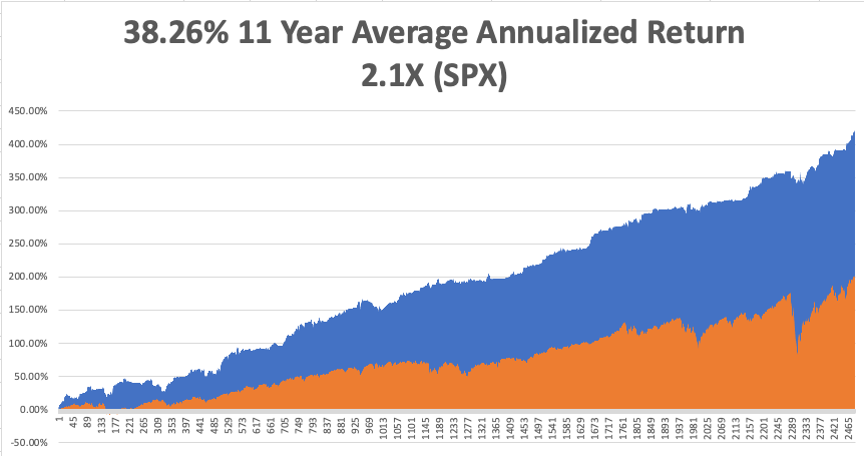

My Global Trading Dispatch catapulted to another new all-time high. December is up 8.55%, taking my 2020 year-to-date up to a new high of 64.99%.

That brings my eleven-year total return to 420.90% or more than double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.26%. My trailing one-year return exploded to 66.30%, the highest in the 13-year history of the Mad Hedge Fund Trader.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 16 million and deaths 300,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 14 at 12:00 PM EST, US Consumer Inflation Expectations for November are released.

On Tuesday, December 15 at 11:00 AM, the New York Empire State Manufacturing Index for December are published.

On Wednesday, December 16 at 8:00 AM, US Retail Sales for November are printed.

On Thursday, December 17 at 8:30 AM, the Weekly Jobless Claims are published. We also get November Housing Starts.

On Friday, December 18, at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was stunned to learn that 84 million people are watching The Mandalorian, the latest Star Wars installment Disney (DIS) launched in its hugely successful streaming service a year ago.

It reminds me of when I first saw Star Wars in 1977. I was changing planes in Vancouver, Canada on the way to Tokyo and used a long layover to take a taxi to the nearest theater to catch a film I’d heard so much about.

I was amazed when I realized that the guy sitting in the next seat had memorized the entire script and was mouthing all the words. The only other time I have ever seen this happen was sitting on the benches at Shakespeare’s Globe Theater in London. At least then, they were reciting Romeo and Juliet.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/11yr-dec14.png456864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-14 09:02:542020-12-14 09:38:13The Market Outlook for the Week Ahead, or The Great Asset Shortage

In 1919, President Woodrow Wilson traveled to Europe to negotiate the end of WWI and the Versailles Treaty. Midway through the talks, he suffered a major stroke and was hustled back to the US in an American battleship, the USS George Washington.

The Spanish Flu pandemic was underway, killing millions, so it was thought best to keep the whole matter secret. The president’s wife essentially ran the country for the last three years of Wilson’s administration, claiming to represent the president’s wishes.

This was the history that flashed through my mind when I learned of President Trump’s Covid-19 infection on Thursday night. The presidential election is now effectively over. All fundraising has ceased. It is now an open question whether Trump can even live until the November 3 election. He is, after all, a high-risk patient. Any remaining public campaign events on which the president thrived is out of the question.

The minute the president got sick, media coverage has been wholly devoted to Covid-19. That was not in the Trump plan. Not at all.

The London betting markets soared from a 60% chance of a Biden win to 90% minutes after the Covid-19 news broke. The only question is the extent of the landslide. This election won’t go anywhere near the courts or the Supreme Court, as the stock market has been pricing in. If there is another big gap down, you should be picking up stocks by the bucket load as fast as you can.

Fund managers who thought Trump had a chance of returning will spend this weekend pouring over Biden’s economic policies. All investment decisions will now be made based on the assumption that these will be the policies in force for the next 4, 8, or 12 years.

Think:

higher taxes

more economic stimulus

big infrastructure spending

more quantitative easing

grants to state and local municipalities

no inflation

low-interest rates

more alternative energy subsidies

the return of the Paris Climate Accord

more regulation of the oil industry

end of the trade wars

rejoining the NATO alliance

Oh, and the huge technological advancements and the burgeoning profit opportunities that have emerged in response to the pandemic? We get to keep those.

That is great news for long-term investors. All of this combined is very pro-investment and pro stock market. It firmly solidifies my own Dow target of 120,000 in a decade and another Roaring Twenties and coming American Golden Age. Now, we even have the trigger.

That explains why the market made back a hefty 500 points in hours, even turning positive on the day for a few fleeting moments. On a six-month view, the upside risks are far greater than the downside ones. An S&P 500 of $3,500-$3,700 by yearend is within range, up 6%-12% from here.

The September Nonfarm Payroll Report bombed, coming in at 661,000, well below expected. The headline Unemployment Rate is at a historically high 7.9%. The U-6 real “discouraged worker” jobless rate is at 12.6%. Leisure & Hospitality was the big winner at 318,888, Healthcare gained 107,000, and Retail posted 142,000. Local Government lost a staggering 232,000 jobs and towns run out of money.

US Q2 GDP came in at a horrific negative 31.4% in the final read, the worst in US history. It’s a tough economic record to run for office on. The first Q3 GDP read will not be released until October 29, five days before the presidential election, and should be up huge.

US Capital Goods hit a six-year high, up 1.8% in August. July was revised upward as well. The boost may be short-lived as stimulus money runs out.

Office Rents won’t recover until 2025, says commercial real estate leader Cushman & Wakefield. Some 215 million square feet of demand has been lost due to the pandemic. Many knowledge-based workers are never coming back to the office.

Pending Homes Sales hit a record high in August, up a mind-blowing 8.8% from July and a staggering 24.5% YOY. Hot housing markets are seeing 11%-20% YOY price increases. The northeast saw the biggest gains. This trend has another decade to run. Buy before they run out of stock.

Case Shiller rose 4.8% in July as its National Home Price Index shows. Phoenix (9.2%), Seattle (7.0%), and Charlotte (6.0%) were the price leaders. A stampede to the suburbs fueled by record-low interest rates is the main driver. Look for these trends to continue for years.

Consumer Confidence soared in September, from 84.8 last month to 101.8. Those who have money are spending it. Those who don’t are waiting in lines at food banks, disappearing from the economy. New York bankruptcies surged 40%. If you haven’t spent the past decade investing in your online presence or yourself, you’re toast.

Disney (DIS) laid off 28,000 to stem hemorrhaging losses at its theme parks, hotels, and cruise line. It will take a year to come back. Clearly, their recent $78.3 billion purchase of 21st Century Fox movie and TV studios last year was poorly timed, just before the pandemic, and they borrowed massively to close it. And they had a major presence in China! It’s one of the biggest mass layoffs since Corona began to decimate the economy.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch pushed through to a new all-time high last week on the strength of a position that I kept for a single day. All I needed was the 700-point dive in the Dow Average in 24 hours to realize half the maximum profit in my short (SPY) position. When the market offers me a gift like that, I take it, no questions asked. I am back to a rare 100% cash position, waiting for a bigger dump to buy.

The risk/reward in the market now is terrible. I believe we have to test the 200-day moving averages before it’s safe to go back in with the indexes and single stocks.

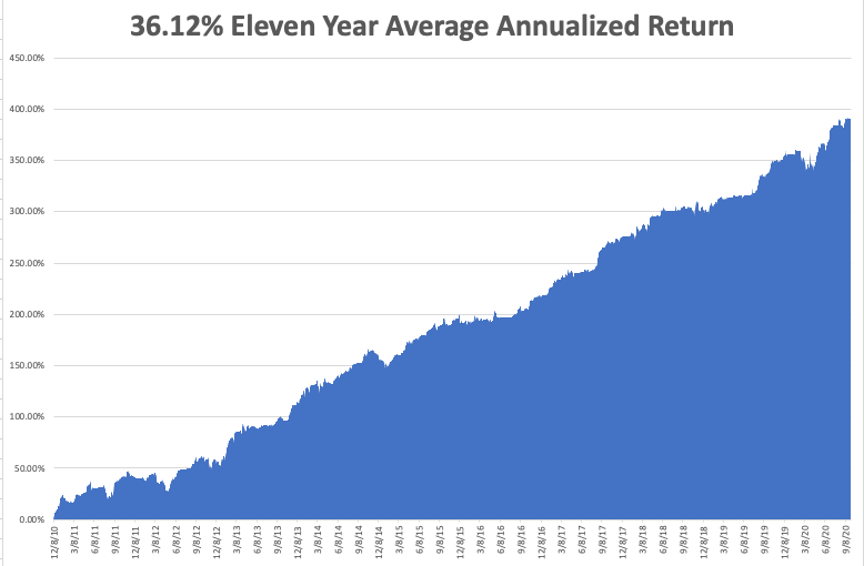

That takes our 2020 year-to-date performance back up to a blistering +35.46%, versus a loss of 2.87% for the Dow Average. October shot out the gate at +0.96%. That takes my 11-year average annualized performance back to +36.12%. My 11-year total return returned to another new all-time high at +391.37%. My trailing one-year return popped back up to +51.82%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 210,000, which you can find here.

On Monday, October 5 at 10:00 AM, the ISM Non-Manufacturing PMI Index for September is released.

On Tuesday, October 6 at 9:00 AM EST, the JOLTS Job Openings for August is published.

On Wednesday, October 7 at 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 PM EST, the Fed Minutes from the last Open Market Committee Meeting six weeks ago are disclosed.

On Thursday, October 8 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, October 9, at 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I’m headed up to Lake Tahoe again to escape the thick clouds of choking smoke in the San Francisco Bay Area. Also, the polls for the presidential election in Nevada open on October 17 and I have to VOTE!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Is History Repeating Itself?

No Smoke Here

https://www.madhedgefundtrader.com/wp-content/uploads/2020/10/woodrow-wilson2.png352430Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-05 08:02:172020-10-05 09:09:12The Market Outlook for the Week Ahead, or Is History Repeating Itself?

Below please find subscribers’ Q&A for the September 30 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Which is a better buy, NVIDIA (NVDA) or Advanced Micro Devices (AMD)?

A: NVIDIA is clearly the larger, stronger company in the semiconductor area, but AMD has more growth ahead of it. You’re not going to get a ten-bagger from NVIDIA from here, but you might get one from Advanced Micro Devices, especially if a global chip shortage develops once we’re out the other side of the pandemic. So, I vote for (AMD), and did a lot of research on that company last week. You can find the report at www.madhedgefundtrader.com but you have to be logged in to see it.

Q: Do you have any thoughts on the JP Morgan Chase Bank (JPM) spoofing cases, where they had to pay about a billion in fines? Is this a terrible time to invest in banks?

A: No, this is a great time to invest in banks because this is the friendly administration to banks now; the next one will be less than friendly. On the other hand, an awful lot of bad news is already in the price; buying these companies at book value or discount of book like JP Morgan, it's a once in a lifetime opportunity. All the bad behavior they’re being fined on now happened many years ago. So yes, I still like banks, but you really have to be careful to buy them on the dip, just in case they stay in a range. If you stay in a range, you’re buying them call spread, you always make money. The bigger drag on share prices will be the Fed ban on bank share buybacks but that may end after Q4.

Q: Is it time to buy Disney (DIS) after they laid off 28,000?

A: This is a company that practically every fund manager in the company wants to have in their portfolio. However, it could be at least a year before they get back to normal capacity in the theme parks, meaning customers packing in shoulder-to-shoulder. So, it could be another wait-for-a-turnaround, buy-on-the dip situation for sure. This company is so well managed that you’re always going to have to pay up to get into the Mouse House. By the way, my dad did business with Disney during the 1950s so we got Disneyland opening day tickets and I got to shake Walt Disney’s hand.

Q: How desperate is General Motors (GM) in buying the fake Tesla (TSLA) company, Nikola (NKLA), who've been exposed as giant frauds? Is GM hopeless?

A: Yes, the future is happening too fast for a giant bureaucracy like General Motors to get ahead of the curve. The fact that they’re trying to buy in outside technologies shows how weak their position is, and of course, it’s a great way to get stuck with a loser, as Tesla selling out to anyone. The Detroit companies are all stuck with these multibillion-dollar engine factories so they can’t afford to go electric even if they wanted to. So, I expect all the major Detroit car companies to go under in the next 5 years or so. Electric cars are already beating conventional internal combustion engines on a lifetime cost basis and will soon be beating them, within 3 years, on an up-front cost basis as well.

Q: Will Netflix (NFLX) pass $600 before the year's end?

A: I’m expecting a monster after-election rally to new all-time highs in the market and Netflix will be one of the leaders, so easy to tack on another hundred bucks to Netflix. That’s one of my targets for a call spread if we can get in at a lower price. And if you really want to be conservative, buy 2-year LEAPS, two-year call options spreads on Netflix, and you’ll get an easy 100% return on those.

Q: Who will win, Trump or Biden?

A: Neither. You will win. I am not a member of any political party as I would never join any club that would stoop to have me as a member. Groucho Marx told me that just before he died in the early 70s. Don’t ask me, ask the polls. Suffice it to say that the London betting polls are 60%-40% in favor of Biden, having just added another 5% for Biden after the debate. My expectation is that Biden picks up another point in the opinion polls in all the battleground states this weekend. So, Biden will be up anywhere from 6-10% in the 6 states that really count.

Q: What will the market impact be?

A: It makes no difference who wins. The mere fact that the election is out of the way is worth a 10% move up in the stock market.

Q: Should we keep the January 2022 (TLT) 140/143 bear put spread?

A: Absolutely, yes. That’ll be a chip shot and we in fact should go in the money on those number sometime next year. A huge cyclical recovery will create an enormous demand for funds and crowding out by the government will crush the bond market.

Q: Do you think it would be better to wait a week or two to lock in refis on home loans?

A: I think we are at the low in interest rates in the refi market. Even if the Fed lowers interest rates, banks aren’t going to lower their lending rates anymore because there's no money in it for them. It’s also taking anywhere from 2-4 months to close on a loan, as the backlogs are so enormous. If you can even get a loan officer to return a phone call, you’re lucky. So, I wouldn't be too fancy here trying to pick absolute bottoms; I would just refi now and whatever you get is going to be close to a century low.

Q: Why so few trade alerts?

A: Well, very simple. We only do trade alerts when we see really good sweet spots in the market. There aren’t sweet spots in the market every day; you’re lucky if you get 1 or 2 in a month. Then we tend to pour in and out of the market very quickly with a lot of alerts. There is no law that says you have to have a position every day of the year. That buys the broker’s yacht, not yours. You should only have positions when the risk reward is overwhelmingly in your favor. That is not now when our market timing index is hugging the 50 level. At 50, you actually have the worst possible entry point for new trades, long or short, so I’d rather wait for it to get away from that level before we get aggressive again. We have gone 100% invested multiple times in the last two months and made a ton of money. So, you just have to wait for your turn to get a sweet spot, and then you’ll make a very quick 10% or 15% in the market. Patience is rewarded in this business.

Q: Would you wait for the election because of the high implied volatility?

A: No, I would not wait. The game is to get in at the lowest price before the election. When the implied volatilities drop after the election, the profits you can make on these deep out of the money LEAPs drop by about half. Thank the volatility while it’s here because it’s creating great trading opportunities now, not in two months after the volatility Index (VIX) has collapsed.

Q: What about Zoom (ZM)?

A: As much as Zoom has had a 10-fold return since we recommended it a year ago, it looks like it wants to go higher. The Robinhood traders just love this stock; it’s a stay at home stock, stay at home is lasting a lot longer than anyone thought. Zoom is just coining it on that.

Q: Is the best outcome a Biden presidency and a Republican Senate?

A: No, that is the worst outcome. When you have a global pandemic going on, you don’t want gridlock in Washington. You want a very active Washington, controlled by a single party that can get things done very quickly. That is not now, which is possibly a major reason that we have the highest Covid-19 death rate in the world. It’s because Washington is doing absolutely nothing to stop the virus; the president won’t even wear a mask, so yes, you need one party to control everything so they can push stuff through. If it works, great, and if not then you kick them out of office next time and let the other guys have a try.

Q: Will property markets be up 20% by the end of the year?

A: If you live in a suburb of New York or San Francisco, then yes it will be up that much. For the whole rest of the country, the average is more like 5% gains year on year. In the burbs of these big money-making cities, prices are going absolutely nuts. My neighbor put his house up and it sold in a week for a $1 million over asking. So, the answer to that is yes, hell yes.

Q: Can you explain why the IPO market is suddenly booming now?

A: A lot of these companies like Palantir (PLTR) have been in development for 20 years, and prices are high. On valuation terms, we are at dot com bubble peaks now. That is the very best time to take your company public and get a huge premium for your stock. When the world is baying for paper assets, you print more of them.

Q: What is the best way to play real estate?

A: Buying the single home building companies like Pulte Homes (PHM), Lennar Homes (LEN), and KB Homes (KBH).

Q: What is your Tesla overview in China?

A: Tesla’s already announced that they’re doubling production of the Shanghai factory, from 250,000 units a year to 500,000. They built the last one in 18 months. It would take (GM) like 5 years to build something like that.

Q: Why has gold (GLD) lost its risk-off status?

A: It’s now a quantitative easing asset—like tech stocks, like bitcoin, and the stay at home stocks. It is being driven much more by QE-driven speculators flush with free cash than anyone looking for a flight to safety bid. When this group sells off, gold drops as well. The only risk-off asset right now is cash. That is the only “no risk” trade.

Q: What does reversal in lumber prices tell you?

A: Lumber was another one of those QE assets—it tripled. But you have this monster increase in new home building, huge demand for new homes in the suburbs, huge import duties leveled by the Trump administration on lumber coming from Canada. Also, a lot of people are getting COVID-19 in the lumber mills. So, they’re having huge problems on the production side in lumber, as a result of the pandemic.

Q: Are there any alternative ways to buy the Australian dollar besides (FXA)?

A: You go into the futures market and buy the Australian dollar futures. That is an entirely new regulatory regime so can be a huge headache. It requires you to register with the Commodities Futures Trading Commission, which is the worst of all the major regulators, but that is an alternative. If you’re an individual and not regulated instead of being a professional money manager, then it’s much easier.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Summit of Mount Rose

https://www.madhedgefundtrader.com/wp-content/uploads/2020/10/john-mount-rose.png358478Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-02 12:02:312020-10-02 12:17:40September 30 Biweekly Strategy Webinar Q&A

I don’t get into food tech that often but one company that I have been highly bullish on that keeps delivering month over month is plant-based meat provider Beyond Meat (BYND).

The deals just keep rolling in for Beyond Meat as it announced that it had expanded its distribution deal with Walmart (WMT).

The all-American supermarket will now carry Beyond Meat in 2,400 of its stores, up from 800 before, and is a decisive victory for Beyond Meat whose non-animal-based meat is quickly becoming ubiquitous all over the U.S.

Their footprint is really expanding at a rapid clip because Walmart is actually the biggest grocer in the U.S. by sales. Now, Beyond Meat products will be in about half of the retailer’s U.S. stores.

The plant-based burger company has had a breakout year and has rallied nearly 120% as we speak and I recommended buying this stock in the low 70s.

That stock has made a double from that recommendation.

The first-mover advantage combined with the health pandemic has worked wonders for this company that hopes to supplant animal-based meat as the staple food for decades to come.

Now we are grappling with problems that every publicly traded company hopes to have – high valuations.

The current valuation is perceived as high because the growth engine powering Beyond Meat is clicking on all cylinders.

For companies like Beyond Meat, expanded distribution can immediately boost revenue because the capacity to deliver meat increases in an instant.

Beyond Meat typically recognizes revenue when products are delivered to retail and food-service locations, not when they finally sell through to the end consumer, so they have incentives to get their product in as many places as possible.

Beyond’s expanded distribution deal with Walmart validates the growth story to outside investors and legitimates the road map that management has aggressively targeted.

Beyond Meat’s latest move to expand the distribution of Beyond Burger meshes well with the company’s efforts to make its products more accessible across grocery chains.

It's rumored that Walmart and Beyond have cultivated an extremely healthy working relationship setting the stage for more collaboration in the future and, of course, more products in the store window.

Beyond Meat’s frozen products were first launched at Walmart’s stores in 2015. Since then, the company has expanded its in-store offerings at Walmart to include Beyond Burger and Beyond Sausage in the in-person fresh meat section, while the Beyond Breakfast Sausage patties were recently added in the freezer aisle.

This is all while consumers haven’t absorbed the full scope of health benefits incurred by eating substitute meat products.

The pandemic has created a new generation of health-obsessed consumers and Beyond Meat is well placed to cater to such growing interests.

In fact, Beyond Meat has doubled down on being a leading provider of healthy plant-based meat alternatives whose products are made from simple ingredients.

The numbers speak for themselves as Beyond Burger contains 35% less saturated fat and has no added cholesterol, antibiotics, or hormones. It is also free of GMOs, soy, or gluten. Beyond Burger — made out of peas, mung bean, and rice — closely mirrors the taste of a traditional beef burger.

The stay-at-home food preparation revolution was catalyzed by the pandemic, relative deliveries to dining establishments have been killed off.

During the second quarter, strong retail channel sales volumes drove the company’s top line that surged 69% year on year.

The company’s efforts to expand and diversify retail channel offerings are likely to bear fruit. Last week, the company announced the expansion of its frozen Beyond Breakfast Sausage patties to more than 5,000 additional stores across the United States. The added distribution locations include grocery chains like Kroger KR, Harris Teeter, Target's TGT Super Target stores, Publix. Earlier this month, the company launched Beyond Meatballs across grocery stores. Markedly, Beyond Meatballs marks the company’s third new retail product introduced in 2020, following the launches of Beyond Breakfast Sausage and Cookout Classic.

The one potential headwind to keep note of that could dampen enthusiasm for Beyond is the growing competition right around the corner that has led to various analysts to downgrade the stock.

JPMorgan was one of them citing market share loss at grocery stores to its biggest competitor, Impossible Foods Inc.

Analysts also cited waning volume at restaurants, which are slower to add “complexity” to the menu during the COVID-19 pandemic.

Other brands getting in on the fun are Morningstar brand, expanding its Incogmeato line of plant-based proteins with help from Walt Disney Co. (DIS), with the launch of Mickey Mouse shaped Chick’n Nuggets.

The item is meant to appeal to families and could create a market of lifelong plant-based meat eaters.

Dr. Praeger’s launched beef and chicken plant-based sliders this week.

Meatless Farm, a British-based food company, has landed in the U.S. And another global plant-based food company, Chile-based NotCo, is planning to bring its products to the U.S. after recently closing an $85 million round of funding.

Beyond is still a true growth stock and putting money in the early innings will harvest alpha.

Keeping tabs on the competition is something that any trader can’t ignore, and even though the moat isn’t that wide, if Beyond keeps operating at a high level, shares should be bought and held.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-02 10:02:392020-10-14 17:28:06The Jewel of Food Tech

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-18 09:04:502020-09-18 11:06:20September 18, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.