I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have a comfortable seat next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini can navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

Chicago’s Union Station

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way, like Omaha, Salt Lake City, and Reno, to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my favorite photos from the trip below, although there is only so much you can do from a moving train and an iPhone 16 Pro.

Somewhere in Iowa

The Thumbnail Portfolio

Equities – buy dips, but sell rallies too Bonds – avoid Foreign Currencies – avoid Commodities – avoid Precious Metals – avoid Energy – avoid Real Estate – avoid

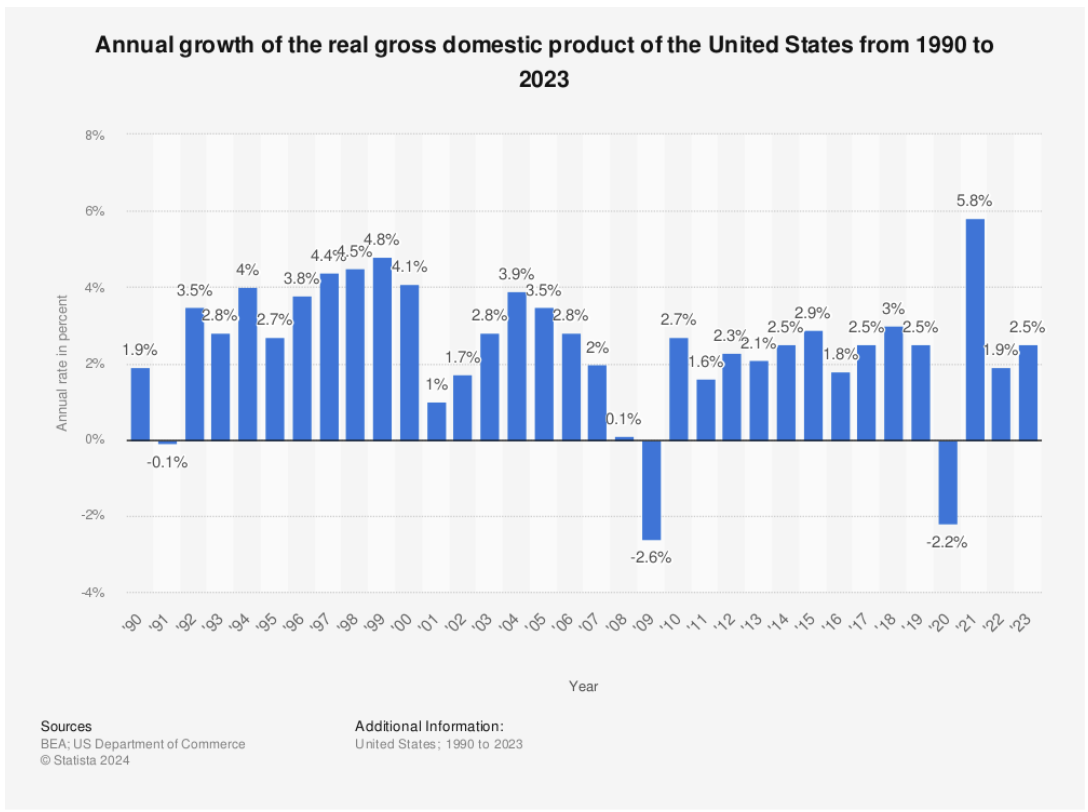

1) The Economy – Cooling

I expect a modest 2.0% real GDP growth with a 4.0% inflation rate, giving an unadjusted shrinkage of the economy of negative -2% for 2025. That is down from 0% in in 2024. This may sound discouraging, but believe me, this is the optimistic view. Some of my hedge fund buddies are expecting a zero return over the next four years.

Virtually all independent economists expect the new administration's economic policies will be a drag on both the US and global economies. Trade wars are bad for everyone. When your customers are impoverished, your own business turns south. This is a big deal, since the Magnificent Seven, which accounted for 70% of stock market gains last year, get 60% of their profits from abroad.

The ballooning National Debt is another concern. The last time Trump was in office, he added $10 trillion to the deficit through aggressive tax cuts and spending increases. If this time, he adds another $10-$15 trillion, the National Debt could reach $50 trillion by 2030.

There are two issues here. For a start, Trump will find it a lot harder and more expensive to fund a National Debt at $50 trillion than $20 trillion. Second, borrowing of this unprecedented magnitude, double US GDP, will send interest rates soaring, causing a recession.

The only question then is whether this will be a pandemic-style recession, which took stocks down 30% and recovered quickly, or a 2008 recession which demolished stocks by 52% and dragged on for years.

Hope for the best but expect the worst, unless you want to consider a future career as an Uber driver.

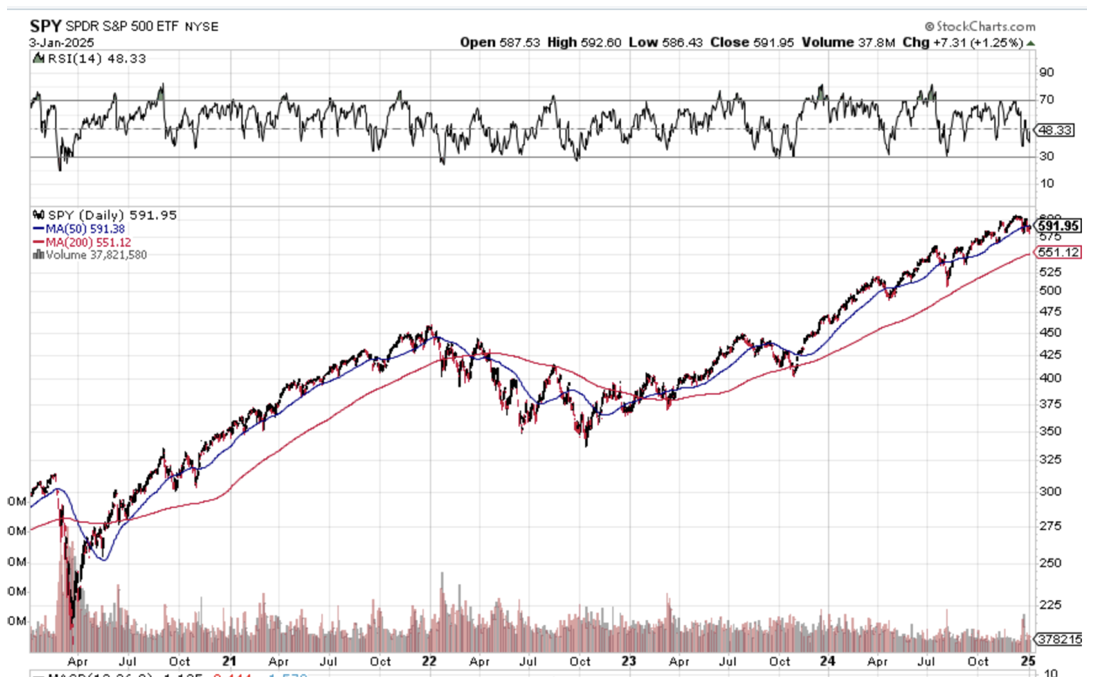

The outlook for stocks for 2025 is pretty simple. You are going to have to work twice as hard to make half the money you did last year with twice the volatility. You will not be able to be as nowhere near aggressive in 2025 as you were in 2024It’s a dream scenario for somebody like me. For you, I’m not so sure.

It’s not that US companies aren't growing gangbusters. I expect 2% GDP growth, 15% profit growth, and 12% net margin growth in 2025. But let’s face reality. Stocks are the most expensive they have been in 17 years and we know what happened after 2008. Much of the stock market gain achieved last year was through hefty multiple expansions. This is not good.

Big tech companies might be able to deliver 20% gains and are still the lead sector for the market. Normally that should deliver you a 15%, or $800 gain in the S&P 500 (SPX). We might be able to capture this in the first half of 2025.

Financials will remain the sector with the best risk/reward, and I mean the broader definition of the term, including banks, brokers, money managers, and some small-cap regional banks. The reason is very simple. Their income statements will get juiced at both ends as revenues soar and costs plunge, thanks to deregulation.

No passage of new laws is required to achieve this, just a failure to enforce existing ones. The hint for this is a new SEC chair whose primary interest is promoting the Bitcoin bubble. Buy (GS), (MS), (JPM), (BAC), (C), and (BLK).

However, this is anything but a normal year. Uncertainty is at an eight-year high, thanks to an incoming administration. If the promised policies are delivered, inflation will soar and interest rates will rise, as they already have. We could lose half or all of our stock market gains by the end of 2025.

The big “tell” for this was the awful market performance in December, down 5%. The Dow Average was down ten days in a row for the first time in 70 years. Santa Claus was unceremoniously sent packing. People Are clearly nervous. But then they should be with a bull market that is approaching a decrepit five years in age.

There is a bullish scenario out there and that has Trump doing absolutely nothing in 2025, either because he is unwilling or unable to take action. After all, if the economy isn’t actually broken, why fix it? Better yet, if you own an economy it is better not to break it in the first place.

Nothing substantial can pass Congress with a minuscule one-seat majority in the House of Representatives. There will be no new presidential action through tariffs and only a few token, highly televised deportations, not enough to affect the labor market.

Stocks will not only hold, but they may add to the 15% first-half gains for the year. I give this scenario maybe a 50% probability.

The first indication this is happening is when the presidential characterization of the economy flips in a few months from the world’s worst to the world’s best with no actual change in the numbers. Trump will take all the credit.

You heard it here first.

Frozen Headwaters of the Colorado River

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD) Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, or dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returned home by train because their religion forbade travel by automobiles or airplanes.

The big question to ask here after a 100-basis point rise in bond yields in only three months is whether the (TLT) has suffered enough. The short answer is no, not quite yet, but we’re getting close. Fear of Trump policies should eventually take ten-year US Treasury bond yields to 5.00%, and then we will be ready for a pause at a nine-month bottom. After that, it depends on how history unfolds.

If Trump gets everything he wants, inflation will soar, bonds will crash, and 5.00% will be just a pit stop on the way to 6.00%, 7.00%, and who knows what? On the other hand, if Trump gets nothing he says he wants, then both bonds stocks and bonds will rise, creating a Goldilocks scenario for all balanced portfolios and investors.

That also sets up a sweet spot for entry into (TLT) call spreads close to 5.00% yields. A politician campaigning on one policy, then doing the opposite once elected? Stranger things have happened. The black swans will live.

If your basic assumption for interest rates is that they stay flat or rise, then you have to love the US dollar. Currencies are all about expected interest rate differentials and money always pours into the highest-paying ones. Tariffs will add fat to the fire because any reduction in international trade automatically reduces American trade deficits and is therefore pro-dollar.

This means that you should avoid all foreign currency plays like the plague, including the Euro (FXE), Japanese yen (FXY), British Pound (FXB), Canadian dollar (FXE), and Australian dollar (FXA).

A strong greenback comes with pluses and minuses. It makes our exports expensive and less competitive and therefore creates another drag on the economy. It demolishes traditional weak dollar plays like emerging markets and precious metals. On the other hand, it attracts substantial foreign investments into US stocks and bonds, which has been continuing for the past decade.

Above all, be happy you are paid in US dollars. My foreign clients are getting crushed in an increasingly expensive world.

5) Commodities (FCX), (BHP), (RIO), (VALE), (DBA) Look at the chart of any commodity stock and you see grim death. Freeport McMoRan (FCX), BHP (BHP), and Rio Tinto (RIO), they’re all the same. They’re all afflicted with the same disease, over-dependence on a robustly growing China, which isn’t growing robustly, if at all.

I firmly believe that this will continue until the current leadership by President Xi Zheng Ping ends. He has spent the last decade globally expanding Chinese interests, engaging in abusive trade practices, hacking, and attacking American allies like Taiwan and the Philippines.You can only wave a red flag in front of the US before it comes back to bite you. A trade war with the US is now imminent.

This will happen sooner than later. The Chinese people don’t like being poor for very long. This is why I didn’t get sucked in on the Chinese long side in the fall, as many hedge funds did.

If China wants to go back to playing nice, as they did in the eighties and nineties, China should return to return to high growth and commodities will look like great “Buys” down here. If they don’t, American growth alone should eventually pull commodities up, as our economy is now growing at a long-term average gross unadjusted 6.00% rate. So the question is how long this takes.

It may pay to start nibbling on the best quality bombed-out names now, like those above.

Snow Angel on the Continental Divide

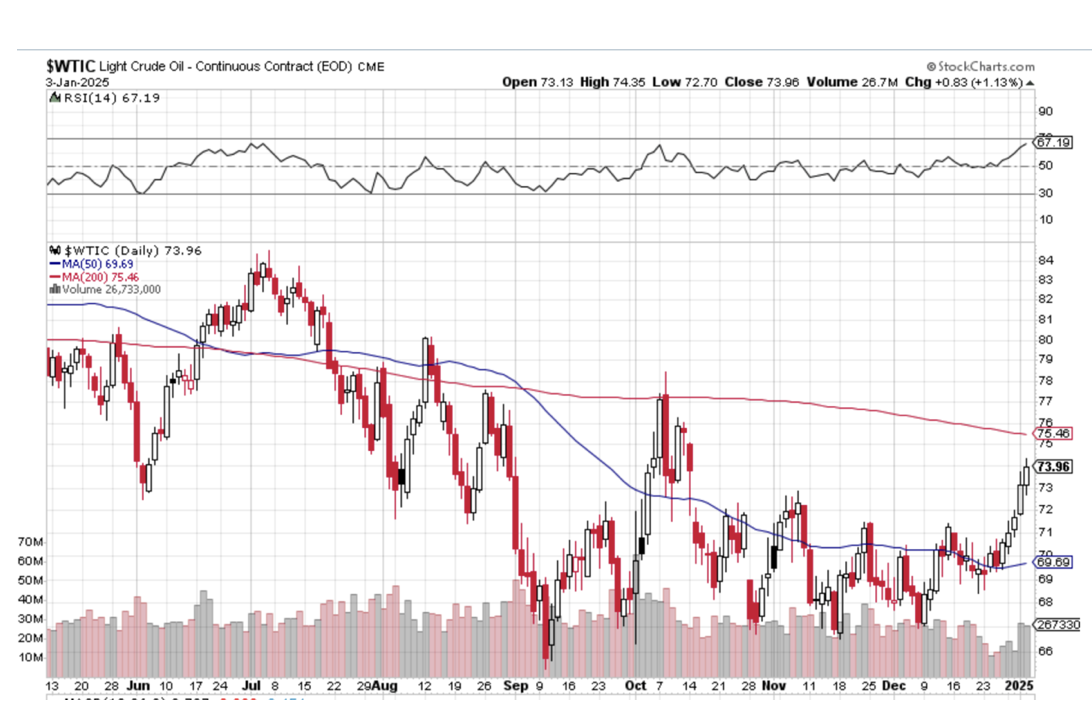

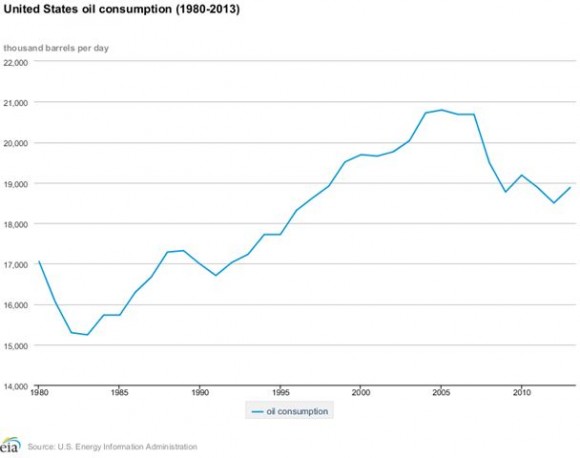

6) Energy (DIG), (USO), (DUG), (UNG), (USO), (XLE), (LNG), (CCJ), (VST), (SMR) Energy was one of the worst-performing sectors in the market for the second year in a row and 2025 is looking no better. New supplies are surging, while demand remains stuck in the mud, with the US now producing an incredible 13.5 million barrels a day. OPEC is dead.

EVs now make up 10% of the US auto fleet, and much more in other countries, are making a big dent. Some 50% of all new car sales in China, the world’s largest market, are EVs. The number of barrels of oil needed to increase a unit of American GDP is plunging, as it has done for 25 years, through increased efficiencies. Remember your old Lincoln Continental that used to get eight miles per gallon? Now it gets 27.

Worse yet, a major black swan hovers over the sector. If the Ukraine War somehow ends, some ten million barrels a day of Russian oil will hit the market. Oil prices should plunge to $50 a barrel.

There are always exceptions to the rule, and energy plays not dependent on the price of oil would be a good one. So is natural gas, which will benefit from Cheniere Energy’s (LNG) third export terminal coming online, increasing exports to China. Ukraine cutting off Russian gas flowing to Europe will assure there is plenty of new demand.

But I prefer investing in sectors that have tailwinds and not headwinds. Better leave energy to the pros who have the inside information they need to make money here.

If someone is holding a gun to your head tell you that you MUST invest in energy, go for the new nuclear plays like (CCJ), (VST), and (SMR). We are only at the becoming of the small modular reactor trend, which could accelerate for decades.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side. In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year. We also see countless abandoned 19th-century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

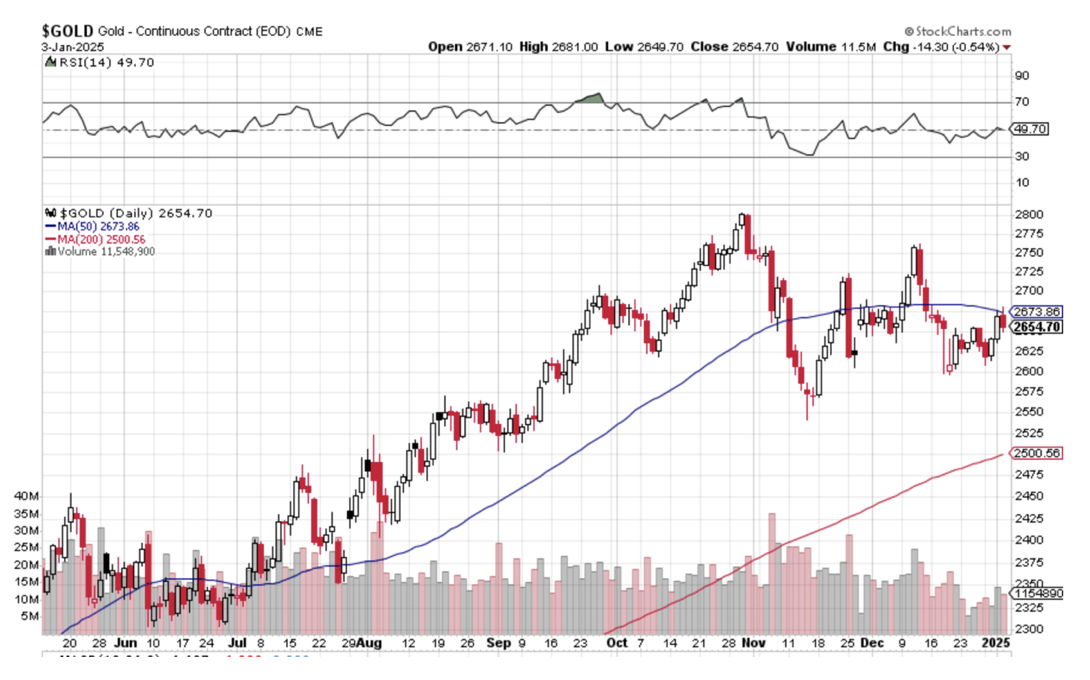

We certainly got a terrific run on precious metals in 2025, with gold at its highs up 33% and silver up 65%. The miners did even better. Even after the post-election selloff, it was still one of the best-performing asset classes of the year.

But the heat has definitely gone out of this trade. The prospect of higher interest rates for longer in 2025 has sent short-term traders elsewhere. That’s because the opportunity cost of owning precious metals is rising since they pay no interest rates or dividends. And let’s face it, there was definitely new competition for hot money from crypto, which doubled after the election.

The sector is not dead, it is resting. Central bank buying of the barbarous relic continues unabated, especially among sanctioned countries, like Russia and China. Gold is still the principal savings vehicle for many Chinese. They are not going to recover confidence in their own currency, banks, or government anytime soon. And there is still slow but steadily rising industrial demand from solar sectors.

Gold supply has also been falling for years, while costs are rising at least at double the headline inflation rate. So it’s just a matter of time before the supply/demand balance comes back in our favor. Where the final bottom is anyone’s guess as gold lacks the traditional valuation parameters of other asset classes, like dividends or interest paid. We’ll just have to wait for Mr. Market to tell us, who is always right.

Give (GLD), (SLV), (GDX), (GOLD), and (WPM) a rest for now but I’ll be back.

Crossing the Great Nevada Desert Near Area 51

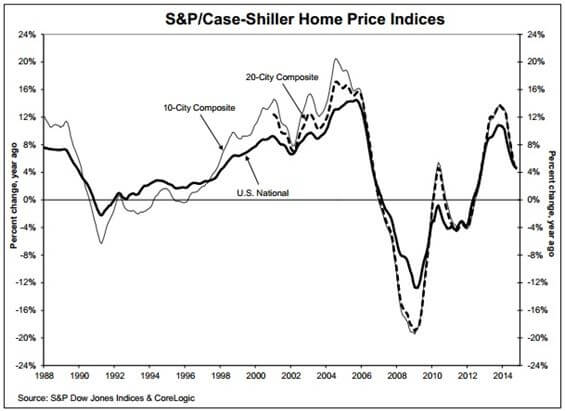

8) Real Estate (ITB), (LEN), (KBH), (PHM), (DHI)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada. It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley, California. Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Real estate was a nice earner for us in 2024 in the new homes sector. The election promptly demolished this trade with the prospect of higher interest rates for longer. Expect this unwelcome drag to continue in 2025.

I am not expecting a housing crash unless interest rates take off. More likely it will continue to grind sideways on low volume. That’s because the market has support from a structural shortage of 10 million homes in the US, the debris left over from the 2008 housing crash. That’s why there is still a Millennial living in your basement. Homebuilders now prioritize profit margins over market share.

I expect this sector to come back someday. New homebuilders have the advantage of offering free upgrades and discounted in-house financing. Avoid for now (DHI), (KBH), (TOL), and (PHM).

Crossing the Bridge to Home Sweet Home

9) Postscript We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff have made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been cooling in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 80 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just coming into view across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro, iPad, and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak tonight and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2025!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2025!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Zephyr.jpg342451april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-08 09:00:172025-02-20 12:40:412025 Annual Asset Class Review

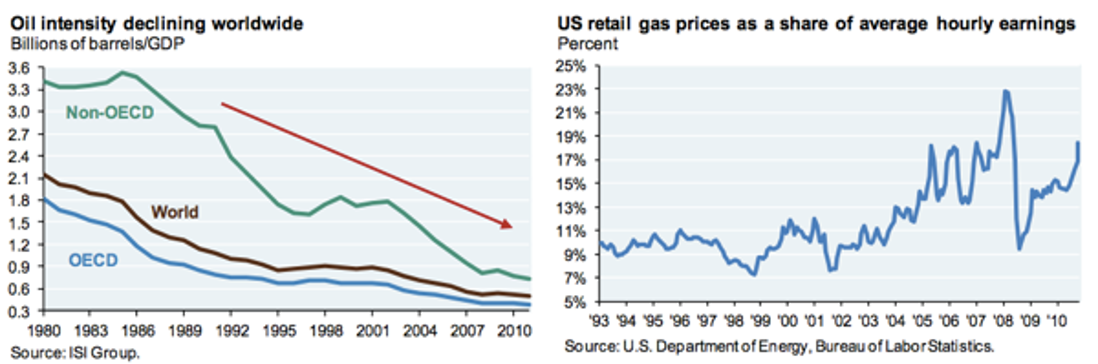

Virtually every analyst has been puzzled by the endless weakness in oil prices (USO), (DIG), (DUG), which have been in a downward spiral for more than a year. Since Russia first invaded Ukraine, the price of Texas tea has collapsed from $132 to $66 a barrel.

In fact, oil ain’t what it used to be.

The first chart below shows the number of barrels of oil needed to generate a unit of GDP, which has been steadily declining for 40 years. The second reveals the percentage of hourly earnings required to buy a gallon of gasoline in the US, which has been mostly flat for three decades, although it has recently started to spike upwards.

The bottom line is that conservation, the rollout of more fuel-efficient vehicles and hybrids, and the growth of alternatives, are all having their desired effect. Notice how small all the new cars on the road are these days, many of which get 40 mpg with conventional gasoline engines.

As for my own household, it has gone all electric. Some 15% or all the new cars sold in the US are EVs, which don’t use oil at all, except for a tiny amount of grease on the wheels and suspension

Developed countries are getting six times more GDP growth per unit of oil than in the past, while emerging economies are getting a fourfold improvement.

The world is gradually weaning itself off of the oil economy. But the operative word here is “gradually”, and it will probably take another two decades before we can bid farewell to Texas tea, at least for transportation purposes.

But the Mileage is Great!

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/horse-car.jpg510660Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-03-17 09:04:182023-03-17 10:32:15Oil Isn't What It Used to Be

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 14 Pro Max.

Here is the bottom line which I have been warning you about for months. In 2023, we will probably top the 84.63% we made last year, but you are going to have to navigate the reefs, shoals, and hurricanes. Do it and you can laugh all the way to the bank. I will be there to assist you to navigate every step.

The first half of 2023 will be all about trading. After that, I expect markets to go straight up.

And here is my fundamental thesis for 2023. After the Fed kept rates too low for too long, then raised them too much, it will then panic and lower them again too fast to avoid a recession. In other words, a mistake-prone Jay Powell will keep making mistakes. That sounds like a good bet to me.

Let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2023

1) When will the Fed pivot?

2) How much of a toll will the quantitative tightening take?

3) How soon will the Russians give up on Ukraine?

4) When will buyers return to technology stocks from value plays?

5) Will gold replace crypto as the new flight to safety investment?

6) When will the structural commodities boom get a second wind?

7) How fast will the US dollar fall?

8) How quickly will real estate recover?

9) How fast can the Chinese economy bounce back from Covid-19?

10) How far will oil prices keep falling?

Whether we get a recession or not, you can count on markets fully discounting one, which it is currently doing with reckless abandon.

Anywhere you look, the data is dire, save for employment, which may be the last shoe to fall. Technology companies seem to be leading us in the right direction with never-ending mass layoffs. Even after relentless cost-cutting though, there are still 1.5 tech job offers per applicant, which is down from last year’s three.

The Fed is currently predicting a weak 0.5% GDP growth rate for 2023, the same feeble rate we saw for 2022. What we might get is two-quarters of negative growth in the first half followed by a sharp snapback in the second half.

Whatever we get, it will be one of the mildest recessions or growth recessions in American economic history. There is no hint of a 2008-style crash. The banking system was shored up too well back then to prevent that. Thank Dodd/Frank.

Since my job is to make your life incredibly easy, I am going to narrow my equity strategy for 2023.

It's all about falling interest rates.

When interest rates are high, as they are now, you only look at trades and investments that can benefit from falling interest rates.

In the first half, that will be value plays like banks, (JPM), (BAC), (C), financials (MS), (GS), homebuilders (KBH), (LEN), (PHM), industrials (X), capital goods (CAT), (DE).

As we come out of any recession in the second half, growth plays will rush to the fore. Big tech will regain leadership and take the group to new all-time highs. That means the volatility and chop we will certainly see in the first half will present a generational opportunity to get into the fastest-growing sectors of the US economy at bargain prices. I’m talking Cadillacs at KIA prices.

A category of its own, Biotech & Healthcare should do well on their own. Not only are they classic defensive plays to hold during a recession, technology and breakthrough new discoveries are hyper-accelerating. My top three picks there are Eli Lily (ELI), Abbvie (ABBV), and Merck (MRK).

Block out time on your calendars because whenever the Volatility Index (VIX) tops $30, I am going pedal to the metal, and full firewall forward (a pilot term), and your inboxes will be flooded with new trade alerts.

There is another equity subclass that we haven’t visited in about a decade, and that would be emerging markets (EEM). After ten years of punishment by a strong dollar, (EEM) has also been forgotten as an investment allocation. We are now in a position where the (EEM) is likely to outperform US markets in 2023, and perhaps for the rest of the decade.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a new business. This time, bonds face the gale force headwinds of three promised interest rate hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

With a major yield advantage over the rest of the world, the US dollar has been on an absolute tear for the past decade. After all, we have the world’s strongest economy.

That is about to end.

If your primary assumption is that US interest rates will see a sharp decline sometime in 2023, then the outlook for the greenback is terrible.

Currencies are driven by interest rate differentials and the buck is soon going to see the fastest shrinking yield premium in the forex markets.

That shines a great bright light on the foreign currency ETFs. You could do well buying the Australian Dollar (FXA), Euro (FXE), Japanese yen (FXE), and British Pound (FXB). I’d pass on the Chinese yuan (CYB) right now until their Covid shutdowns end.

5) Commodities (FCX), (VALE), (DBA)

Commodities are the high beta play in the financial markets. That’s because the cost of being wrong is so much higher. Get on the losing side of commodities and you will be bled dry by storage costs, interest expenses, contangos, and zero demand.

Commodities have one great attribute. They predict recessions earlier than any other asset class. When they peaked in March of 2022, they were screaming loud and clear that a recession would hit in early 2023. By reversing on a dime on October 14, they also told us that the recovery would begin in July of 2023.

You saw this in every important play in the sector, including Broken Hill (BHP), Peabody Energy (BTU), Freeport McMoRan (TCX), and Alcoa Aluminum (AA). Excuse me for using all the old names.

The heady days of the 2011 commodity bubble top are about to replay. Now that this sector is convinced of a substantially weaker US dollar and lower inflation, it is once more a favorite target of traders.

China will still demand prodigious amounts of imported commodities once its pandemic shutdown ends, but not as much as in the past. Much of the country has seen its infrastructure built out, and it is turning from a heavy industrial to a service-based economy, much like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase three-fold in a decade to accommodate this increase, no easy task, or prices will have to rise.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate all commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (XLE), (AMLP)

Energy was the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero sooner than you think. However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are bailing on their own industry. Instead of reinvesting profits back into their future exploration and development, as they have for the last century, they are paying out more in dividends and share buybacks.

Take the money and run.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and share prices for the energy industry.

Energy now counts for only 5% of the S&P 500. Twenty years ago, it boasted a 15% weighting.

The gradual shutdown of the industry makes the supply/demand situation infinitely more volatile.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

And guess who the world’s best oil trader was in 2022? That would be the US government, which drew 400 million barrels from the Strategic Petroleum Reserve in Texas and Louisiana at an average price of $90 and now has the option to buy it back at $70, booking a $4 billion paper profit.

The possibility of a huge government bid at $70 will support oil prices for at least early 2023. Whether the Feds execute or not is another question. I’m advising them to hold off until we hit zero again to earn another $18 billion. Why we even have an SPR is beyond me, since America has been a large net energy producer for many years now. Do you think it has something to do with politics?

To understand better how oil might behave in 2023, I’ll be studying US hay consumption from 1900-1920. That was when the horse population fell from 100 million to 6 million, all replaced by gasoline-powered cars and trucks. The internal combustion engine is about to suffer the same fate.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2022 was a terrible year for precious metals until we got the all-asset class reversal in October. With inflation soaring, stocks volatile, and interest rates soaring, gold had every reason to fall. Instead, it ended up unchanged on the year, thanks to a 15% rally in the last two months.

Bitcoin stole gold’s thunder until a year ago, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand were just not enough to keep gold afloat. That is over now for good and that is why gold is regaining its luster.

Chart formations are starting to look very encouraging with a massive head-and-shoulders bottom in place. So, buy gold on dips if you have a stick of courage on you, which I hope you do.

Higher beta silver (SLV) will be the better bet as it already has been because it plays a major role in the decarbonization of America. There isn’t a solar panel or electric vehicle out there without some silver in them and the growth numbers are positively exponential. Keep buying (SLV), (SLH), and (WPM) on dips.

Crossing the Great Nevada Desert Near Area 51

8) Real Estate (ITB), (LEN), (KBH), (PHM)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Those in the grip of a real estate recession take solace. We are in the process of unwinding 2022’s excesses, but no more. There is no doubt a long-term bull market in real estate will continue for another decade, once a two year break is completed.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s. You don’t have a real estate crash when we are short 10 million homes.

The reasons, of course, are demographic. There are only three numbers you need to know in the housing market for the next ten years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The boomers (between ages 58 and 76) have been unloading dwellings to the Gen Xers (between ages 46 and 57) since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis. That has created a massive shortage of housing, both for ownership and rentals.

There is a happy ending to this story.

Millennials now aged 26-41 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes. They are also just entering the peak spending years of middle age, which is great for everyone.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to the pandemic and Zoom, many are never returning to the cities. That has prompted massive numbers to move from the coasts to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should continue to rise during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are considered. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 16 years. The 50% of small home builders that went under during the Financial Crisis never came back.

We are still operating at only a half of the 2007 peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

There is a new factor at work. We are all now prisoners of the 2.75% 30-year fixed rate mortgages we all obtained over the past five years. If we sell and try to move, a new mortgage will cost double today. If you borrow at a 2.75% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free. That’s why nobody is selling, and prices have barely fallen.

This winds down towards the end of 2023 as the Fed realizes its many errors and sharply lowers interest rates. Home prices will explode…. again.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now after you throw in all the tax breaks. It’s also a great inflation play.

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

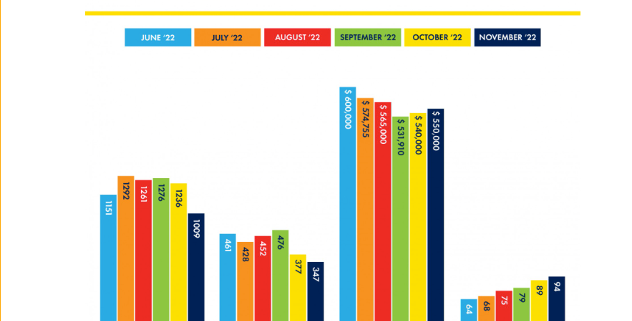

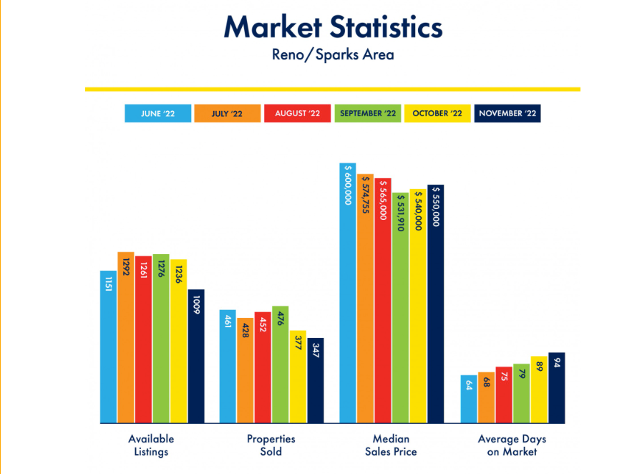

Recent Reno Real Estate Statistics

Crossing the Bridge to Home Sweet Home

9) Postscript

We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff has made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2023!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2023!

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/market-statistics.png474632Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-04 15:00:552024-01-03 10:44:502023 Annual Asset Class Review

I am once again writing this report from a first class sleeping cabin on Amtrak?s California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into bunk beds, a single and a double. There is a shower, but only Houdini could get in and out of it.

I am not Houdini, so I go downstairs to use the larger public showers.

We are now pulling away from Chicago?s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American accomplishment.

I am headed for Emeryville, California, just across the bay from San Francisco. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure, and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Spellchecker can catch most of the mistakes, but not all of them.

Thank goodness for small algorithms.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied searches during stops at major stations along the way to chase down data points.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains a lot about our country today. I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 6.

After making the rounds with strategists, portfolio managers, and hedge fund traders, I can confirm that 2015 was one of the toughest to trade for careers lasting 30, 40, or 50 years. Even the stay-at-home index players had their heads handed to them.

With the Dow gaining 3.1% in 2015, and S&P 500 almost dead unchanged, this was a year of endless frustration. Volatility fell to the floor, staying at a monotonous 12% for eight boring consecutive months before spiking repeatedly many times to as high as 52%. Most hedge funds lagged the index by miles.

My Trade Alert Service, hauled in an astounding 38.8% profit, at the high was up 48.7%, and has become the talk of the hedge fund industry.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

The Four Key Variables for 2016

1) Will the Fed raise interest rates more or not?

2) Will China?s emerging economy see a hard or soft landing?

3) Will Japanese and European quantitative easing increase, or remain the same?

4) Will oil bottom and stay low, or bounce hard?

Here are your answers to the above: no, soft, more later, bounce hard later.

There you go! That?s all the research you have to do for the coming year. Everything else is a piece of cake.

The Ten Highlights of 2015

1) Stocks will finish higher in 2016, almost certainly more than the previous year, somewhere in the 5% range and 7% with dividends. Cheap energy, a recovering global economy, and 2-3% GDP growth, will be the drivers. However, this year we have a headwind of rising interest rates and falling multiples.

2) Expect stocks to take a 15% dive. That gives us a -15% to +5% trading range for the year. Volatility will remain permanently higher, with several large spikes up. That means you are going to have to pedal harder to earn your crust of bread in 2016.

3) The Treasury bond market will modestly grind down, anticipating the next 25 basis point rate rise from the Federal Reserve, and then the next one after that.

4) The yen will lose another 5% against the dollar.

5) The Euro will fall another 5%, doing its best to hit parity with the greenback, with the assistance of beleaguered continental governments.

6) Oil stays in a $30-$60 range, showering the economy with hundreds of billions of dollars worth of de facto tax cuts.

7) Gold finally bottoms at $1,000 after one more final flush, then rallies $250. (My jeweler was right, again).

8) Commodities finally bottom out, thanks to new found strength in the global economy, and begin a modest recovery.

9) Residential real estate has made its big recovery, and will grind up slowly from here for years.

10) The 2016 presidential election will eat up immense amounts of media and research time, but will have absolutely no impact on financial markets. Give your money to charity instead.

The Thumbnail Portfolio

Equities - Long. A rising but high volatility year takes the S&P 500 up to 2,200. Technology, biotech, energy, solar, consumer discretionary, and financials lead. Energy should find its bottom, but later than sooner.

Bonds - Short. Down for the entire year, but not by much, with long periods of stagnation.

Foreign Currencies - Short. The US dollar maintains its bull trend, especially against the Yen and the Euro, but won't gain nearly as much as in 2015.

Commodities - Long. A China recovery takes them up eventually.

Precious Metals - Buy as close to $1,000 as you can. We are overdue for a trading rally.

Agriculture - Long. El Nino in the north and droughts in Latin American should add up to higher prices.

Real estate - Long. Multifamily up, commercial up, single family homes up small.

1) The Economy - Fortress America

I think real US economic growth will come in at the 2.5%-3% range.

With a generational demographic drag continuing for five more years, don?t expect more than that. Big spenders, those in the 46-50 age group, don?t return in larger numbers until 2022.

But this negative will be offset by a plethora of positives, like hyper-accelerating technology, global expansion, and the lingering effects of the Fed?s massive five year quantitative easing.

US corporate profits will keep pushing to new all time highs. But this year we won?t be held back by the collapsing economies of Europe, China, and Japan, which subtracted about 0.5% from American economic growth, nor weak energy.

US Corporate earnings will probably come in at $130 a share for the S&P 500, a gain of 10% over the previous year. During the last six years, we have seen the most dramatic increase in earnings in history, taking them to all-time highs.

Technology and dramatically lower energy costs are the principal sources of profit increases, which will continue their inexorable improvements. Think of more machines and software replacing people.

You know all of those hundreds of billions raised from technology IPO?s in 2015? Most of that is getting plowed right back into new start ups, increasing the rate of technology improvements even further, and the productivity gains that come with it.

We no longer have the free lunch of zero interest rates. But the cost of money will rise so slowly that it will barely impact profits. Deflation is here to stay. Watch the headline jobless rate fall below 5% to a full employment economy.

Keep close tabs on the weekly jobless claims that come out at 8:30 AM Eastern every Thursday for a good read as to whether the financial markets will head in a ?RISK ON? or ?RISK OFF? direction.

For the first time in seven years, earnings multiples are going to fall, but not by much. That is the only possible outcome in a world with rising interest rates, however modestly.

If multiples fall by 5%, from the current 18X to 17.1X, profits increase by 10%, and you throw in a 2% dividend, you should net out a 7% return by the end of the year.

S&P 500 earnings fell by 6% in 2015, but take out oil and they grew by 5.6%. In 2016, energy will be a lesser drag, or not at all. That makes my 10% target doable.

That is not much of a return with which to take on a lot of risk. But remember, in a near zero interest rate world, there is nothing else to buy.

This is not an outrageous expectation, given the 10-22 earnings multiple range that we have enjoyed during the last 30 years.

The market currently trades around fair value, and no market in history ever peaked out here. An overshoot to the upside, often a big one, is mandatory. Yet, that is years off.

After all, my friend, Janet Yellen, is paying you to buy stock with cheap money, so why not? Borrowing money at close to zero and investing in 2% dividend paying stocks has become the world?s largest carry trade.

Rising interest rates will have one additional worrying impact on stock prices. They will pare back mergers and acquisitions and corporate buy backs in 2016.

Together these were the sources of all new net buying of stocks in 2015, some $5.5 trillion worth. Call it financial engineering, but the market loves it.

Although energy looks terrible now, it could well be the top-performing sector by the end of the year, to be followed by commodities.

Certainly, every hedge fund and activist investor out there is undergoing a crash course on oil fundamentals. After a 13-year expansion of leverage in the industry, it is ripe for a cleanout.

Solar stocks will continue on a tear, now that the 30% federal investment tax subsidy has been extended by five more years. Look at Solar City (SCTY), First Solar (FSLR), and the solar basket ETF (TAN). Revenues are rocketing and costs are falling.

After spending a year in the penalty box, look for small cap stocks to outperform. These are the biggest beneficiaries of cheap energy and low interest rates.

Share prices will deliver anything but a straight-line move. Expect a couple more 10% plus corrections in 2015, and for the Volatility Index (VIX) to revisit $30 multiple times. The higher prices rise, the more common these will become.

Amtrak needs to fill every seat in the dining car, so you never know who you will get paired with for breakfast, lunch, and dinner.

There was the Vietnam vet Phantom jet pilot who now refused to fly because he was treated so badly at airports. A young couple desperate to get out of Omaha could only afford seats as far as Salt Lake City, sitting up all night. I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a ?See America Pass.? Mennonites returning home by train because their religion forbade airplanes.

I have to confess that I am leaning towards the ?one and done? school of thought with regards to the Fed?s interest rate policy. We may see a second 25 basis point rise in June, but only if the economy takes off like a rocket and international concerns disappear, an unlikely probability.

If you told me that US GDP growth was 2.5%, unemployment was at a ten year low at 5.0%, and energy prices had just plunged by 68%, I would have pegged the ten-year Treasury bond yield at 6.0%. Yet here we are at 2.25%.

We clearly are seeing a brave new world.

Global QE added to a US profit glut has created more money than the fixed income markets can absorb.

Virtually every hedge fund manager and institutional investor got bonds wrong last year, expecting rates to rise. I was among them, but that is no excuse.

Fixed income turned out to be a winner for me in 2015, as I sold short every bond price spike from the summer onward. It worked like a charm.

You might as well take your traditional economic books and throw them in the trash. Apologies to John Maynard Keynes, John Kenneth Galbraith, and Paul Samuelson.

The reasons for the debacle are myriad, but global deflation is the big one. With ten year German bunds yielding a paltry 62 basis points, and Japanese bonds paying a paltry 26 basis points, US Treasuries are looking like a steal.

To this, you can add the greater institutional bond holding requirements of Dodd-Frank, a balancing US budget deficit, a virile US dollar, the commodity price collapse, and an enormous embedded preference for investors to keep buying whatever worked yesterday.

For more depth on the perennial strength of bonds, please click here for ?Ten Reasons Why I?m Wrong on Bonds?.

Bond investors today get an unbelievable bad deal. If they hang on to the longer maturities, they will get back only 80 cents worth of purchasing power at maturity for every dollar they invest a decade down the road.

But institutions and individuals will grudgingly lock in these appalling returns because they believe that the potential losses in any other asset class will be worse.

The problem is that driving eighty miles per hour while only looking in the rear view mirror can be hazardous to your financial health.

While much of the current political debate centers around excessive government borrowing, the markets are telling us the exact opposite.

A 2% handle on the ten-year yield is proof to me that there is a Treasury bond shortage, and that the government is not borrowing too much money, but not enough.

There is another factor supporting bonds that no one is looking at. The concentration of wealth with the 1% has a side effect of pouring money into bonds and keeping it there. Their goal is asset protection and nothing else.

These people never sell for tax reasons, so the money stays there for generations. It is not recycled into the rest of the economy, as conservative economists insist. As this class controls the bulk of investable assets, this forestalls any real bond market crash, at lest for the near term.

So what will 2016 bring us? I think that the erroneous forecast of higher yields I made last year will finally occur this year, and we will start to chip away at the bond market bubble?s granite edifice.

I am not looking for a free fall in price and a spike up in rates, just a move to a new higher trading range.

We could ratchet back up to a 3% yield, but not much higher than that. This would enable the inverse Treasury bond bear ETF (TBT) to reverse its dismal 2015 performance, taking it from $46 back up to $60.

You might have to wait for your grandchildren to start trading before we see a return of 12% Treasuries, last seen in the early eighties. I probably won?t live that long.

Reaching for yield suddenly went out of fashion for many investors, which is typical at market tops. As a result, junk bonds (JNK) and (HYG), REITS (HCP), and master limited partnerships (AMLP) are showing their first value in five years.

There is also emerging market sovereign debt to consider (PCY). If oil and commodities finally bottom, these high yielding bonds should take off on a tear.

This asset class was hammered last year, so we are now facing a rare entry point.

There is a good case for sticking with munis. No matter what anyone says, taxes are going up, and when they do, this will increase tax-free muni values.

The collapse of the junk bond market suddenly made credit quality a big deal last year. What is better than lending to the government, unless you happen to live in Puerto Rico or Illinois.

So if you hate paying taxes, go ahead and buy this exempt paper, but only with the expectation of holding it to maturity. Liquidity could get pretty thin along the way, and mark to markets could be shocking.

Be sure to consult with a local financial advisor to max out the state, county, and city tax benefits.

One question I always get asked at lunches, conferences, and lectures is what is going to happen to the budget deficit?

The short answer is that it disappears in 2018 with no change in current law, thanks to steady growth in tax revenues and no big new wars.

And Social Security? It will be fully funded by 2030, thanks to a huge demographic tailwind provided by the addition of 86 million Millennials to the tax rolls.

A bump up in US GDP growth from 2% to 4% during the 2020?s will also be a huge help, again, provided we don?t start any more wars.

It looks like I am going to be able to collect after all.

Without much movement in interest rates in 2016, you can expect the same for foreign currencies.

Last year, we saw never ending expectations of aggressive quantitative easing by foreign central banks, which never really showed. What we did get, was always disappointing.

The decade long bull market in the greenback continues, but not by much. You can forget about those dramatic double digit gains the dollar made against the Euro at the beginning of last year, which we absolutely nailed.

The fundamental play for the Japanese yen is still from the short side. But don?t expect movement until we see another new leg of quantitative easing from the Bank of Japan. It could be a long wait.

The problems in the Land of the Rising Sun are almost too numerous to count: the world?s highest debt to GDP ratio, a horrific demographic problem, flagging export competitiveness against neighboring China and South Korea, and the world?s lowest developed country economic growth rate.

The dramatic sell off we saw in the Japanese currency since December, 2012 is the beginning of what I believe will be a multi decade, move down. Look for ?130 to the dollar sometime in 2016, and ?150 further down the road.

I have many friends in Japan looking for an overshoot to ?200. Take every 3% pullback in the greenback as a gift to sell again.

With the US having the world?s strongest major economy, its central bank is, therefore, most likely to continue raising rates the fastest.

That translates into a strong dollar, as interest rate differentials are far and away the biggest decider of the direction in currencies. So the dollar will remain strong against the Australian and Canadian dollars as well.

For a sleeper, use the next plunge in emerging markets to buy the Chinese Yuan ETF (CYB) for your back book. Now that the Yuan is an IMF reserve currency, it has attained new respectability.

But don?t expect more than single digit returns. The Middle Kingdom will move heaven and earth in order to keep its appreciation modest to maintain their crucial export competitiveness.

There isn?t a strategist out there not giving thanks for not loading up on commodities in 2015, the preeminent investment disaster of the year. Those who did are now looking for jobs on Craig?s List.

It was another year of overwhelming supply meeting flagging demand, both in Europe and Asia. Blame China, the one big swing factor in the global commodity.

The Middle Kingdom is currently changing drivers of its economy, from foreign exports to domestic consumption. This will be a multi decade process, and they have $3.5 trillion in reserves to finance it.

It will still demand prodigious amounts of imported commodities, especially, oil, copper, iron ore, and coal, all of which we sell. But not as much as in the past. This trend ran head on into a decade long expansion of capacity by the industry.

The derivative equity plays here, Freeport McMoRan (FCX) and Companhia Vale do Rio Doce (VALE), have all taken an absolute pasting.

The food commodities were certainly the asset class to forget about in 2015, as perfect weather conditions and over planting produced record crops for the second year in a row, demolishing prices. The associated equity plays took the swan dive with them.

Not even the arrival of one of the biggest El Nino events in history could bail them out.

However, the ags are still a tremendous long term Malthusian play. The harsh reality here is that the world is making people faster than the food to feed them, the global population jumping from 7 billion to 9 billion by 2050.

Half of that increase comes in countries unable to feed themselves today, largely in the Middle East. The idea here is to use any substantial weakness, as we are seeing now, to build long positions that will double again if global warming returns in the summer, or if the Chinese get hungry.

The easy entry points here are with the corn (CORN), wheat (WEAT), and soybean (SOYB) ETF?s. You can also play through (MOO) and (DBA), and the stocks Mosaic (MOS), Monsanto (MON), Potash (POT), and Agrium (AGU).

The grain ETF (JJG) is another handy fund. Though an unconventional commodity play, the impending shortage of water will make the energy crisis look like a cakewalk. You can participate in this most liquid of assets with the ETF?s (PHO) and (FIW).

You are now an oil trader, even if you didn?t realize it. Yikes!

The short-term direction of the price of Texas tea will be the principal driver for the prices of all asset classes, as it was for the 2015.

The smartest thing I did in 2015 was to ignore the professional traders, who called the bottom in oil monthly, based on key technical levels.

Instead, I hung on every word uttered by my old drilling buddies in the Barnett Shale, who only saw endless supply.

Guess whom I?ll be paying attention to this year?

I expect oil to bottom in 2016, and then launch a ferocious short covering rally. But when and where is anyone?s guess.

If energy legends John Hamm, John Arnold, and T. Boone Pickens have no idea where the absolute low will be, who am I to second-guess them?

When that happens, a trillion dollars will pour out of the sidelines into this troubled sector. Energy shares should be top-performers in 2016.

That makes energy Master Limited Partnerships, now yielding 10%-15%, especially interesting in this low yield world. Since no one in the industry knows which issuers are going bankrupt, you have to take a basket approach and buy all of them.

The Alerian MLP ETF (AMLP) does this for you in an ETF format (click here for details). At its low this fund was down by 41% this year. The last printed annualized yield I saw was 10%. That kind of return will cover up a lot of sins. Our train has moved over to a siding to permit a freight train to pass, as it has priority on the Amtrak system. Three Burlington Northern engines are heaving to pull over 100 black, brand new tank cars, each carrying 30,000 gallons of oil from the fracking fields in North Dakota.

There is another tank car train right behind it. No wonder Warren Buffet tap dances to work every day, as he owns the railroad.

Who knew that a new, younger Saudi king would ramp up production to once unimaginable levels and crush prices, turning the energy world upside down?

They aren?t targeting American frackers, who at 1 million barrels a day in a 92 million barrel a day demand world barely move the needle. Their goal is to destroy the economies of enemies Iran, Yemen, Russia, and of course ISIS, which need high prices to stay in business.

So far, so good.

Cheaper energy will bestow new found competitiveness on US companies that will enable them to claw back millions of jobs from China in dozens of industries.

At current prices, the energy savings works out to an eye popping $550 per American driver per year!

This will end our structural unemployment faster than demographic realities would otherwise permit.

We have a major new factor this year in considering the price of energy. The nuclear deal with Iran promises to add 500,000 to 1 million barrels a day to an already glutted global market. Iraq is ramping up production as well.

We are also seeing relentless improvements on the energy conservation front with more electric vehicles, high mileage conventional cars, and newly efficient building. Anyone of these inputs is miniscule on its own. But add them all together and you have a game changer.

Enjoy cheap oil while it lasts because it won?t last forever. American rig counts are already falling off a cliff and will eventually engineer a price recovery.

As is always the case, the cure for low prices is low prices. But we may never see $100/barrel crude again.

Add to your long term portfolio (DIG), Exxon Mobil (XOM), Cheniere Energy (LNG), the energy sector ETF (XLE), Conoco Phillips (COP), and Occidental Petroleum (OXY).

Skip natural gas (UNG) price plays and only go after volume plays, because the discovery of a new 100-year supply from ?fracking? and horizontal drilling in shale formations is going to overhang this subsector for a very long time.

It is a basic law of economics that cheaper prices bring greater demand and growing volumes, which have to be transported. However, major reforms are required in Washington before use of this molecule goes mainstream.

These could be your big trades of 2016, but expect to endure some pain first, nor to get much sleep at night.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders. The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a train over on to its side.

In the snow filled canyons we sight a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It?s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken down wooden trestles leading to them, relics of previous precious metals busts. So it is timely here to speak about precious metals.

As long as the world is clamoring for paper assets like stocks and bonds, gold is just another shiny rock. After all, who needs an insurance policy if you are going to live forever?

We have already broken $1,040 once, and a test of $1,000 seems in the cards before a turnaround ensues. There are more hedge fund redemptions and stop losses to go. The bear case has the barbarous relic plunging all the way down to $700.

But the long-term bull case is still there. Gold is not dead; it is just resting.

If you forgot to buy gold at $35, $300, or $800, another entry point is setting up for those who, so far, have missed the gravy train. The precious metals have to work off a severely, decade old overbought condition before we make substantial new highs.

Remember, this is the asset class that takes the escalator up and the elevator down, and sometimes the window.

If the institutional world devotes just 5% of their assets to a weighting in gold, and an emerging market central bank bidding war for gold reserves continues, it has to fly to at least $2,300, the inflation adjusted all-time high, or more.

This is why emerging market central banks step in as large buyers every time we probe lower prices. China and India emerged as major buyers of gold in the final quarter of 2015.

They were joined by Russia, which was looking for non-dollar investments to dodge US economic and banking sanctions.

For me, that pegs the range for 2016 at $1,000-$1,250. ETF players can look at the 1X (GLD) or the 2X leveraged gold (DGP).

I would also be using the next bout of weakness to pick up the high beta, more volatile precious metal, silver (SLV), which I think could hit $50 once more, and eventually $100.

What will be the metals to own in 2015? Palladium (PALL) and platinum (PPLT), which have their own auto related long term fundamentals working on their behalf, would be something to consider on a dip.

With US auto production at 18 million units a year and climbing, up from a 9 million low in 2009, any inventory problems will easily get sorted out.

Would You Believe This is a Blue State?

8) Real Estate (ITB)

The majestic snow covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebears in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80.

There is no doubt that there is a long-term recovery in real estate underway. We are probably 5 years into a 17-year run at the next peak in 2028.

But the big money has been made here over the past two years, with some red hot markets, like San Francisco, soaring. If you live within commuting distance of Apple (AAPL), Google (GOOG), or Facebook (FB) headquarters in California, you are looking at multiple offers, bidding wars, and prices at all time highs.

While the sales figures have recently been weak, it is a shortage of supply that is the cause. You can?t sell what you don?t have, at least in the real estate business.

From here on, I expect a slow grind up well into the 2020?s. If you live in the rest of the country, we are talking about small, single digit gains. The consequence of pernicious deflation is that home prices appreciate at a glacial pace.

At least, it has stopped going down, which has been great news for the financial industry.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer?s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xer?s since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That's what caused the financial crisis.

If they have prospered, banks won?t lend to them. Brokers used to say that their market was all about ?location, location, location?. Now it is ?financing, financing, financing?.

Banks have gone back to the old standard of only lending money to people who don?t need it. But expect to put up your first-born child as collateral, and bring in your entire extended family in as cosigners if you want to get a bank loan.?

There is a happy ending to this story. Millennials, now aged 21-37 are already starting to kick in as the dominant buyers in the market. They are just starting to transition from 30% to 70% of all new buyers in this market. The Great Millennial Migration to the suburbs has begun.

As a result, the price of single family homes should rocket tenfold during the 2020?s, as they did during the 1970?s and the 1990?s, when similar demographic influences were at play.

This will happen in the context of a coming labor shortfall and rising standards of living. Inflation returns.

Rising rents are accelerating this trend. Renters now pay 35% of the gross income, compared to only 18% for owners, and less when multiple deductions and tax subsidies are taken into account.

Remember too, that by then, the US will not have built any new houses in large numbers in 10 years. We are still operating at only a quarter of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($18,000 for a four bedroom brownstone in Brooklyn in 1922).

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now.

If you borrow at a 3% 5/1 ARM rate, and the long-term inflation rate is 3%, then over time you will get your house for free.

How hard is that to figure out?

Crossing the Bridge to Home Sweet Home

9) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff have made the 20 mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that?s all for now. We?ve just passed the Pacific mothball fleet moored in the Sacramento River Delta and we?re crossing the Benicia Bridge. The pressure increase caused by an 8,200 foot descent from Donner Pass has crushed my water bottle.

The Golden Gate Bridge and the soaring spire of the Transamerica Building are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 6, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten mile night hike up Grizzly Peak and still get home in time to watch the opener for Downton Abbey's final season.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I?ll shoot you a Trade Alert whenever I see a window open on any of the trades above.

Good trading in 2016!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2016!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/JT-at-work.jpg478635Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-05 01:05:382016-01-05 01:05:382016 Annual Asset Class Review

I am once again writing this report from a first class sleeping cabin on Amtrak?s California Zephyr. By day, I have two comfortable seats facing each other next to a broad window. At night, they fold into bunk beds, a single and a double. There is a shower, but only Houdini could get in and out of it.

We are now pulling away from Chicago?s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I am headed for Emeryville, California, just across the bay from San Francisco. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure, and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Spellchecker can catch most of the mistakes, but not all of them. Thank goodness for small algorithms.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied searches during stops at major stations along the way to chase down data points.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS. Who knew that 95% of America is off the grid? That explains a lot about our politics today. I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone.

After making the rounds with strategists, portfolio managers, and hedge fund traders, I can confirm that 2014 was one of the toughest to trade for careers lasting 30, 40, or 50 years. Yet again, the stay at home index players have defeated the best and the brightest.

With the Dow gaining a modest 8% in 2014, and S&P 500 up a more virile 14.2%, this was a year of endless frustration. Volatility fell to the floor, staying at a monotonous 12% for seven boring consecutive months. Most hedge funds lagged the index by miles.

My Trade Alert Service, hauled in an astounding 30.3% profit, at the high was up 42.7%, and has become the talk of the hedge fund industry. That was double the S&P 500 index gain.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

The Ten Highlights of 2015

1) Stocks will finish 2015 higher, almost certainly more than the previous year, somewhere in the 10-15% range. Cheap energy, ultra low interest rates, and 3-4% GDP growth, will expand multiples. It?s Goldilocks with a turbocharger.

2) Performance this year will be back-end loaded into the fourth quarter, as it was in 2014. The path forward became so clear, that some of 2015?s performance was pulled forward into November, 2014.

3) The Treasury bond market will modestly grind down, anticipating the inevitable rate rise from the Federal Reserve.

4) The yen will lose another 10%-20% against the dollar.