Global Market Comments

November 19, 2019

Fiat Lux

Featured Trade:

(BLACK FRIDAY DISCOUNT OFFER FOR THE MAD HEDGE TECHNOLOGY LETTER),

(ADBE), (EBAY), (PANW)

Global Market Comments

November 19, 2019

Fiat Lux

Featured Trade:

(BLACK FRIDAY DISCOUNT OFFER FOR THE MAD HEDGE TECHNOLOGY LETTER),

(ADBE), (EBAY), (PANW)

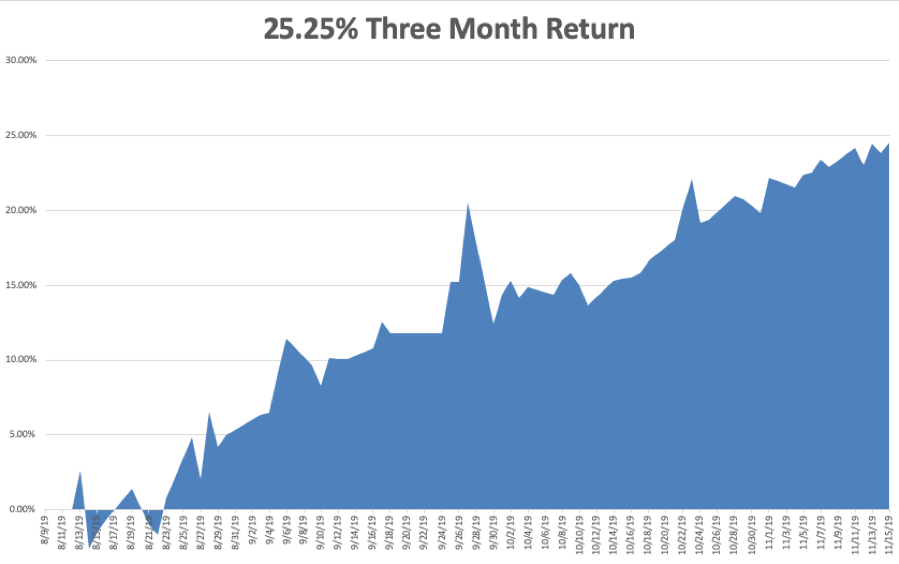

The Mad Hedge Technology Letter has been on an absolute tear lately.

It has posted an eye-popping 25.25% net profit since August. The last 14 consecutive trade alerts have been profitable, a success rate of 100%. Some 20 out of the last 22 trade alerts have been profitable, a success rate of 90.9%.

We nailed the 27.3% move in the multimedia software company, Adobe (ADBE). We killed the 23.28% pop in e-commerce leader eBay (EBAY). And we hit a total home run with a positively ballistic 30.42% gain in cybersecurity giant Palo Alto Networks (PANW).

And here’s the method to our madness. While no one was looking, the stock market has made a dramatic shift from buying in large-cap tech techs to smaller cap ones. In order words, we’ve moved from the FANGs to the mini FANG’s, and WE CAUGHT ALL OF IT!

Which brings me to the topic at hand. You absolutely HAVE to get in on this move, the most important of the year. And I’m going to make it incredibly easy for you to do so. For here at Mad Hedge Fund Trader, Black Friday comes early.

I am offering the Mad Hedge Technology Letter at an insanely bargain-basement price of $998. That is a full 61% discount to the $2,500 list price offered on our website.

I’m not doing this to make money. I am chopping prices so YOU can make money. And there is nothing I like better than happy, money-making customers. For focusing in on this one crucial sector will be the most important investment decision you make in your lifetime.

With the Mad Hedge Technology Letter, you will get:

*A three times weekly morning newsletter covering the most important technology stocks and trends of our time.

*Technology trade alerts sent out at market sweet spots telling when and where best to enter the market.

*Trade alerts sent out at market tops on where best to take profits or stop out of the rare losers.

*Invitations to biweekly Strategy Webinars with live Q&A.

*The best customer support in the industry with same day answers to all questions.

*Access to a searchable ten-year database of technology research.

*Invitations to Mad Hedge Strategy Luncheons around the world (the last one was in Zermatt, Switzerland).

In order to take advantage of this one time only offer, please click here.

Let me give you a warning. We are only accepting 25 orders at this deep discounted one-time offer so it’s a first-come, first-served basis.

I look forward to working with you.

John Thomas

CEO & Publisher

The Mad Hedge Technology Letter

Mad Hedge Technology Letter

August 2, 2019

Fiat Lux

Featured Trade:

(THE GREAT LATIN AMERICAN INTERNET PLAY),

(MELI), (PYPL), (AMZN), (EBAY)

How do you get exposure to the e-commerce story in Latin America?

The best way to do that is to dive into Mercado Libre (MELI), meaning “free market” in Spanish, an Argentine company incorporated in the United States that operates online marketplaces dedicated to e-commerce and online auctions, including mercadolibre.com.

Mercado Libre was established as an Argentine company in 1999 and Founder & CEO Marcos Galperin, while attending Stanford University, acquired funding from HM Capital Partners co-founder John Muse to start his brainchild.

Mercado Libre received additional funding from JPMorgan Partners, Flatiron Partners, Goldman Sachs, GE Capital, and Banco Santander Central Hispano.

The company has used M&A along with organic growth to drive the company.

Relevant examples are of eBay (EBAY) buying a 19.5% stake in the company and then selling its stake in Mercado Libre in 2016, but the companies continue to expand eBay sellers into Latin America.

The cooperation remains strong with eBay opening its first branded store on the Mercado Libre marketplace from Chile in March 2017.

Mercado Libre has acquired iBazar Como, the Brazilian subsidiary of eBay's earlier acquisition, iBazar S.A.

The success culminated with becoming the first Latin American technology company to be listed on the NASDAQ, under the ticker symbol MELI.

The firm offers investors a way to invest in one of the fastest-growing e-commerce markets in the world.

The company has 280 million registered users out of 644 million people who live in Latin America.

The stock has soared 543% in the last five years making the firm one of the fastest growing e-commerce companies in the world by many metrics.

The main drag is that the valuation looks frothy at these price levels.

Mobile payments have mushroomed naturally because of its title, the "eBay of Latin America."

They can also claim to be the PayPal of the region, thanks to robust growth happening in the MercadoPago digital payments business.

In the first quarter, total payment volume rose 82.5% year-over-year.

Off-marketplace payment volume is up 194% – accelerating each and every quarter.

Off-marketplace payments now comprise 45% of the company's total payment volume, and management sees high penetration trends happening in certain areas.

PayPal (PYPL) have become huge supporters of MercadoLibre with an investment of $750 million into MercadoPago.

The deal will join the firms together to work on the shared vision to digitize the economy, especially for the underbanked, in Latin America.

It's a stamp of approval of Mercado's brand recognition in the region that PayPal chose to invest in the company instead of competing.

How fast is the addressable market growing?

Investors have been seduced by the company's impressive growth in payments, but the core marketplace business is still doing backflips.

Gross merchandise volume (GMV) expanded 27% year-over-year in the first quarter, driven by 70% growth in Mexico.

Brazil is the largest market and expanded GMV by 18% year-over-year in the quarter.

Management referenced supermarket items in Mexico and increasing apparel selection as two areas that are showing strong results.

Apparel is the fastest-growing category, up 79% year-over-year last quarter.

With signs that new development is headed in the right direction, new categories and the company expanding its logistics footprint, the market will definitely expand.

MercadoLibre can grow beyond the marketplace business to become a formidable fintech company.

As it expands into other services, Mercado is fortifying its strong brand across Latin America.

Even as Amazon.com (AMZN) enters the high stakes industry, Mercado's first mover advantage can’t be underestimated.

The stock is pricey so lay off it for the time being but add with any major dips.

Global Market Comments

July 11, 2019

Fiat Lux

Featured Trade:

(THE INSIDER’S VIEW ON THE FUTURE OF TECHNOLOGY),

(AMZN), (GOOG), (DELL), (MSFT), (EBAY),

(MY DATE WITH HITLER’S GIRLFRIEND)

How would you like to learn the latest, most important technology trends hitting the global economy today, prepared by one of the most knowledgeable and experienced people in the industry?

It's very simple. Just click on the link below for a wrist-breaking .pdf file packed with 360 slides. It was prepared by my old friend and former Morgan Stanley colleague, Mary Meeker.

Meeker gained fame as the legendary investment banker for technology issues during the Dotcom Boom. She brought to market such blockbusters as Netscape. She also piled investors very early into Amazon (AMZN), Google (GOOG), Dell Computer (DELL), Microsoft (MSFT), and eBay (EBAY) when many of these stocks were trading at single-digit prices. You can understand why she is so popular.

Since 2010, Mary has been with the leading Silicon Valley venture capital firm Kleiner, Perkins, Caufield & Byers. She initially prepared Internet Trends 2018 as a broad ranging 50,000-foot view of technology for her firm. It has since been presented at a number of conferences.

Depending on your interest in technology, you may want to just quickly scroll through the report or analyze each and every single slide. Each slide is a gold mine of information for geeks such as myself. I list a few sample ones below.

The report also gives you some indication of the deep research in which the Diary of a Mad Hedge Fund Trader and the Mad Hedge Technology Letter engage to get you winning Trade Alerts.

To download the report in full please click here.

Enjoy.

Mad Hedge Technology Letter

March 4, 2019

Fiat Lux

Featured Trade:

(RIDING THE EBAY BOOM),

(EBAY), (ETSY), (W)

Investors following the eBay (EBAY) saga should be cheering from the sidelines as the master plan from Elliot Management and Starboard are pressuring eBay’s management into the radical changes the investors initially called out for.

Rewarding the vulture funds with two board seats along with spearheading a comprehensive review of the business model appears more probable than not.

The forced changes have imminent repercussions to the stock price as the breaking up of the company into individual pieces is seen as coaxing out more embedded value while separating out the main e-commerce platform for a long-awaited fix.

These are two highly bullish signals.

Elliot’s reasons for altering eBay’s business model were essentially blamed on two issues - shoddy management and the commingling of growth assets with its inferior e-commerce platform within the eBay umbrella hindering value appreciation.

Even though prospects look bright on this fix, Elliot doesn’t always get its way.

Four years ago, Elliot was the primary investor in Samsung's construction division and rebuffed efforts from Jay Y. Lee, the South Korean business elite and the vice chairman of Samsung Group serving as de facto head, to have another division of Samsung purchase the construction arm for $8 billion.

In 2017, Lee was convicted of bribery and imprisoned and sentenced to three years, Elliot sold their Samsung construction shares after the tide went against them and could not prevent the eventual purchase.

Lee was later set free in 2018 demonstrating the unfettered power of the ruling Korean families and Elliot was up against it in someone else’s backyard.

Even with that setback, Elliot has been ultra-successful abroad, examples are plentiful such as in May 2018, Elliott Management seized control of Telecom Italia controlling two-thirds of Telecom Italia's board seats.

This vulture fund has been specialists at pinpointing ill-ran operations and squeezing the fat off the edges to later sell off assets for a profit.

These tactics have usually centered around cost-cutting, financial engineering, or draining the upper management swamp if need be.

Personally, eBay has the foundations to be competitive with the top e-commerce companies and they need an activist investor to turn this ship around.

In this way, the turnaround will occur much quicker than an organic method because Elliot will apply pressure on all the cancerous parts of the model and stamp them out as fast as possible.

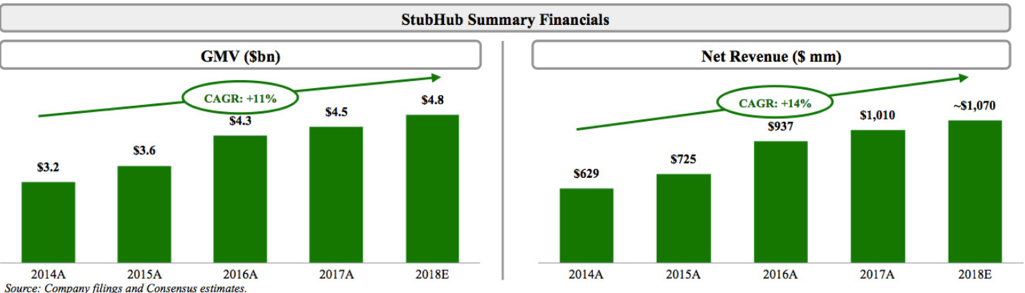

Elliot now has a golden path to two board seats and spinning off StubHub, its uber-growth online events tickets selling platform, will guarantee Elliot and Starboard walk away from this transaction with a heavy profit.

StubHub was bought on the cheap in 2007 when online assets were trading cheaply for $310 million.

The firm contributes 11% to eBay’s top line.

The classified ads business is the other part of the high-growth online portfolio that could be sold for a profit. They operate mainly in Germany and the United Kingdom and comprise almost 10% of sales.

The plan after these premium assets are sold is to focus on mending its wounded e-commerce business.

The core business would need a flushing out of current management.

Bringing in some established hands to reroute the company’s course will boost the shares another 25%.

The phrase “more efficient use of resources” or a similar version of this meaning was used six times in Elliot Management’s letter to eBay Shareholders.

They cited in the letter that EBITDA margins have declined YOY for 12 straight quarters proving that revenue-boosting initiatives have failed spectacularly.

Elliot hopes a better run company will constitute in higher operating margins to the tune of “32% in 2021.”

In the next 3 years, Elliot wants to raise operating expenses by $250 million but reduce “wasteful spend” which they outlined as one of the main reasons hamstringing the company.

Missed opportunities is another major opportunity cost contributing to the underperformance of eBay.

eBay has been left out of the niche e-commerce areas where former eBay employees exploited this untapped source of growth.

The success of Wayfair (W), the furniture e-commerce platform, and Etsy (ETSY), the personalized crafts e-commerce platform, are two glaring examples of sales that should have been registered by eBay but gobbled up by two minnows.

In short, Elliot’s flawless execution and aggressive plan are ideally playing itself out how they wrote it up from the beginning.

It’s hard not to see eBay’s stock higher a year from now as long as Elliot and Starboard get their way.

The brilliant part of this whole turnaround is that eBay doesn’t have to become Amazon to reap share appreciation, they merely need to be not as bad as they were which at the first stage of rebooting the business is the lowest hanging fruit out there.

Once the company becomes mature and more successful, growth and beating relative expectations are harder to achieve.

I am bullish eBay - buy on the next pullback.

Mad Hedge Technology Letter

January 24, 2019

Fiat Lux

Featured Trade:

(ACTIVISTS LAY IN ON EBAY),

(EBAY), (AMZN), (PYPL), (GOOGL)

A highly compelling argument – that was my initial reaction after diving into Elliot Management’s letter to eBay’s (EBAY) shareholders after the ruthless investor activist announced an over 4% stake in one of the original online marketplace giants.

Not only that, hedge fund Starboard Value LP also has gotten in on the act with a position of less than 4%.

Starboard has doubled down agreeing with the general points of Elliot Management’s prognosis on the weakness of eBay’s business model

There are no two ways about it - eBay has been condemned to tech purgatory as of late and is in dire need of a facelift.

If you’re a manager of any sort of magnitude at e-commerce platform eBay, this was the letter of doom and gloom you hoped you would never get.

The equity Gods have been harsh to eBay as PayPal (PYPL), one of the Mad Hedge Technology Letter’s favorite picks in 2019, has risen over 130% after spinning off from eBay in 2015.

eBay is down substantially since that point in time reflecting a poorly run business in a secular growth industry that has produced home runs most evident in the performance of Jeff Bezos’ Amazon.com (AMZN).

The gist of Elliot’s diagnosis centered around the terrible operational execution at the Silicon Valley firm.

It essentially repeats this premise over and over throughout the content.

Current management is historically bad that any efficiencies implemented into the platform would boost growth reverting it back to a point closer to a trajectory that echoes closer to a normal high growth e-commerce company.

How did eBay peter out to mediocrity?

Let me explain.

There is a time-established pattern that Elliot Management identified – eBay management increasing spend to stimulate growth, failing to deliver the goods and reverting back to square one.

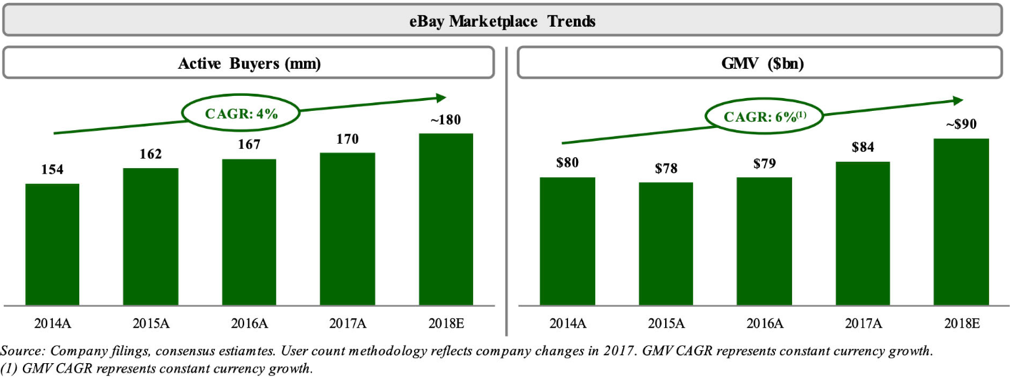

The result is paltry growth in the mid-single digits which can be seen in minimal growth numbers in the gross merchandise volume (GMV), a metric established to gauge the total amount of volume pushed through eBay.

The activist hedge fund claimed that shares could potentially double if their calculated plan could shortly be deployed.

The plan was straight forward and there was no innovative x-factors described or pivot to augmented reality or machine learning that many firms like to hype up.

Elliot’s strategy is purely operational relating to the core business – where is Tim Cook when you need him!

The argument originates from whether eBay management can allocate resources more efficiently, focus on boosting foundational growth in the core marketplace, and develop new verticals that were completely missed in its development, then the stock would react favorably.

I would even double down and say that if they do half of what they promise in the Elliot’s letter, shares should pop at least 30%.

eBay exists under a backdrop of massive secular drivers fueling e-commerce.

The industry is the most robust in the economy and is expanding in the mid-20% even as global sales are about to eclipse the $3 trillion mark.

E-commerce just has a penetration rate of 10% and the runway is long which should enable mainstay companies to grow their top and bottom line if not botched completely.

Average consumer spending is in the throes of major disruption from analog brick and mortar stores to digital e-commerce, and eBay’s strategic position offers an advantageous platform to carve out e-commerce success moving forward.

The first thing Elliot wants to do is reach up their sleeve for a little financial engineering magic by spinning out in-house mega-growth assets of StubHub, the e-ticket event vendor, and its portfolio of premium classified properties that possess double-digit sales growth and elevated margins.

Elliot argues that these two assets would perform better on a standalone basis because they wouldn’t be bogged down by eBay turning around the core business which could possibly result in some misallocated capital and delays.

The valuation of eBay’s Classified Groups assets is around $4.5 billion, but segment that out and the value could represent $10 billion.

The same boost in valuation applies to event ticket seller platform StubHub. The company is valued at just $2.2 billion under the umbrella of eBay but tear the baby out of eBay’s uterus and suddenly the valuation balloons to a rosier $4 billion.

Watching from afar, Elliot has pinpointed management’s “self-inflicted mis-execution” and management must summon all their power and resources to direct “singular attention to growing and strengthening marketplace.”

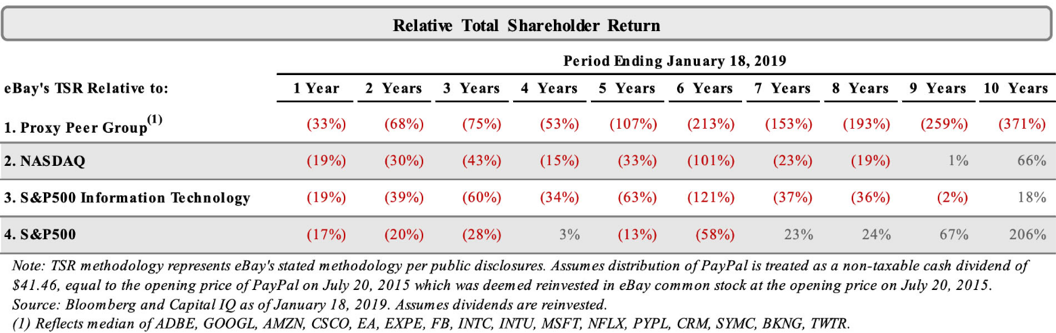

eBay has severely underperformed in share price relative to its peers by 107% in the past 5 years. Extrapolate the time horizon to 10 years and the underperformance shoots up to 371%.

These have been the tech golden years and there is no feasible excuse to why this company hasn’t been able to perform better or equal relative to their peer group.

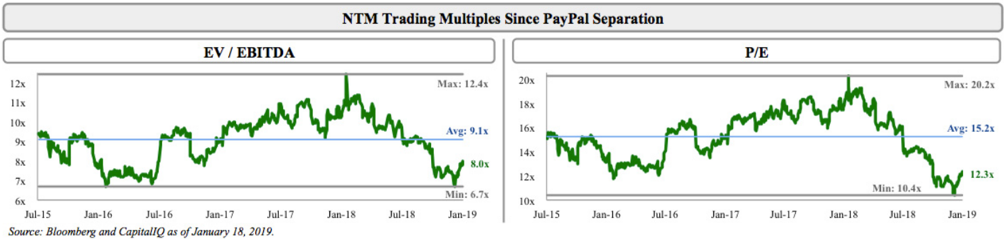

eBay is the second biggest e-commerce platform in the world but only trades at a PE of 12 showing the malaise of investor sentiment surrounding this name.

This is unfortunate because eBay has strong embedded actionable communities in South Korea, Australia, Italy, Germany, U.K., U.S., and Canada.

The tools are there but it is hard to take a stab when the tool is blunted by poor management.

Compare slow growth with the rocket-fueled growth of asset StubHub which has almost doubled revenue in the past 5 years.

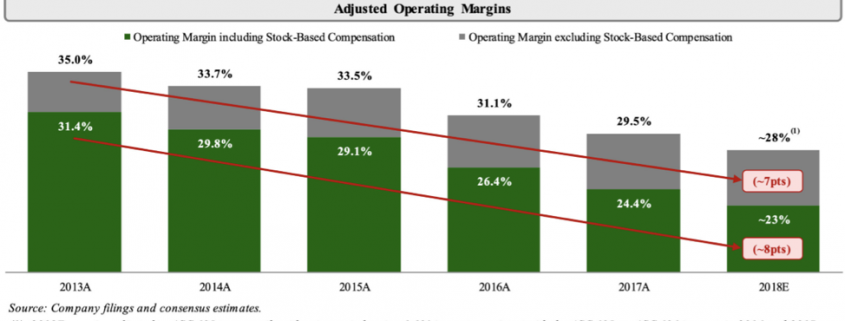

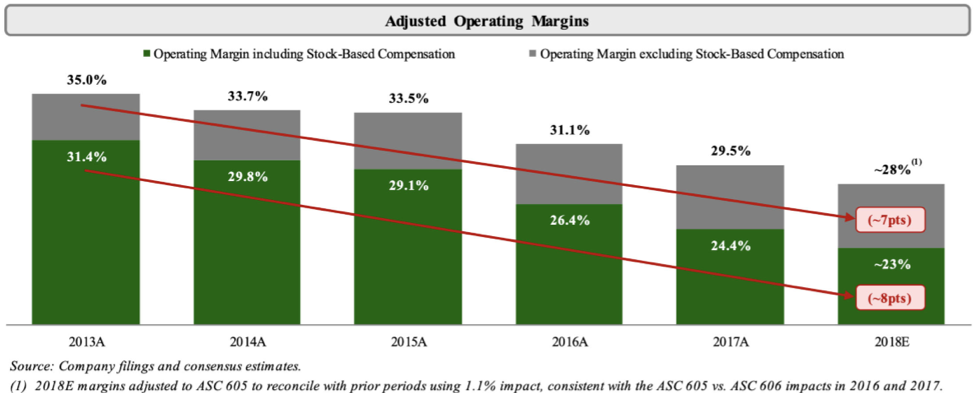

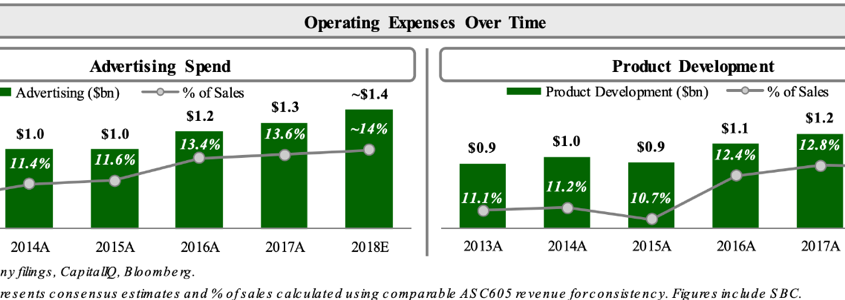

eBay has lifted advertising spend by 70% since 2013 and revved up product development by 45% as well. This has surprisingly led to material margin declines because of the failure of these initiatives to take hold.

One of the missteps resulting in this margin softness is the dysfunctional execution of its online platform infected by technical problems and operational headwinds.

A few notable events were a 2014 broad-based password hack and the botched fix to that problem exacerbated by a muddied communication strategy.

During this time, eBay was outmaneuvered by Google’s (GOOGL) search algorithm resulting in a massive decline in traffic as a result of this painful change.

The next year was similarly awful with a shoddy mobile application that did not resonate with customers and was put out to pasture shortly after rolling it out.

An online marketplace offering a platform for over four million buyers and sellers to carry out business requires high-level functioning. A failure to deliver this experience has caused long-time users to jump ship to other niche vertical platforms.

Innovative endeavors aren’t part of this new strategy to remake the company.

The underlying strategy effectively spells out that eBay needs to become more like Amazon and any sort of moderate success in doing that will positively boost the stock price – let’s call it what it is – an operational overhaul and nothing more than that.

The complaints don’t stop there and last year eBay was inundated with technical issues that included incorrect billing, deleted photos, warped title presentation, and senior management took the blame in a podcast confessing that management needs to pull things together and they “don’t want to repeat (the same mistakes) on a number of levels. And the technology issues that we have had with the platform are on top of the list.”

eBay is not a startup and presides over a profitable business.

Returning capital to shareholders was part of the plan as well.

This entails repurchasing shares of up to $5 billion which was $1 billion more than the original guidance – Elliot Management is an activist investor after all hoping to super-charge shareholder income streams.

Elliot wants to implement a 1.5% dividend yield due to eBay’s high free cash flow model.

After 2020, Elliot wants to allocate 80% of free cash flow for share repurchases and earmark the other 20% for M&A activity.

It is difficult to surmise if this plan will work smoothly or not, but if Elliot can bring in the correct team to execute this plan, I would give them the benefit of the doubt as making this plan into a viable success seems realistic.

But it is yet to be seen how laborious it will be to get the people they want through the door.

eBay is truly a unique asset and the chopped-down nature of its shares would stage a remarkable turnaround if some proven management from Amazon’s executive team could be captured and convinced that eBay is a legitimate option.

Easier said than done, but this is a step in the right direction.

My Luger is firmly in my holster and waiting for some action - if there are any whiffs of a real turnaround then I’ll shoot out some eBay trade alerts.