Global Market Comments

November 30, 2018

Fiat Lux

Featured Trade:

(NOVEMBER 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(VXX), (VIX), (GE), (ROKU), (AAPL),

(MSFT), (SQ), (XLK), (SPLS), (EWZ), (EEM)

Global Market Comments

November 30, 2018

Fiat Lux

Featured Trade:

(NOVEMBER 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(VXX), (VIX), (GE), (ROKU), (AAPL),

(MSFT), (SQ), (XLK), (SPLS), (EWZ), (EEM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader November 28 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

Q: Is it time to get out of semiconductor stocks?

A: The time to get out is before it drops 60%, not afterwards. So, if you have semiconductor stocks, I would look for the next major rally to get out. I think we will get one of those rallies into December/January. We went negative on this sector in June, took all our profits, and didn’t go back in until last week.

Q: Is it time to buy semiconductor stocks?

A: No, that is the group you want to buy at the absolute bottom of the next recession which might be next year sometime. They lead on the downside, and they will lead on the upside as soon as they sniff a recovery in the economy.

Q: I held on to my position in Square (SQ). Should I sell now for a small profit?

A: Yes, in recessions, big companies prosper much more than small companies like Square; that’s why it had such a tremendous selloff; down 55% in six weeks. A small technology stock is not what you want to own in a recession. Big companies slow down, small ones die. At least that’s how conservative investors see it.

Q: What do you make of Fed comments this morning that asset prices are high?

A: I agree with them. They were certainly overpriced with a P/E multiple of 20 that we saw in September; they’re moderately priced now with a P/E multiple of 14.9. I think real estate markets are the overpriced assets that the Fed is talking about though, far more than the stock market, and markets like San Francisco, Seattle, and Vancouver are still way too high.

Q: What are your comments on Apple (AAPL)?

A: There’s an interesting thing going on here; you’ve just had a massive move out of hardware stocks like Apple, which basically makes phones and computers, into software stocks like Microsoft (MSFT), which is growing their cloud business like crazy. You may see this as a long-term industry trend, out of hardware stocks into software stocks. It’s all about the cloud now. The future is in software and that is where Apple is going to with services like the cloud, iTunes, streaming, and advertising, although they are doing it slowly.

Q: Will Trump be able to persuade Fed Chair Powell to stop hiking interest rates?

A: He will not, Powell is one of the few principled people in the government. He’s going to stick to his discipline, only look at the data, and that is going to require him to keep raising interest rates. One of the big black swans for 2019 may be that Trump fires Powell and gets a friendly rent-a-Fed chair in there who lowers interest rates on command. If Trump can hold on for nine months though, even Powell will see the economy’s in trouble and will have to respond accordingly by capping or even lowering interest rates.

Q: Why are you not stopping out of Roku (ROKU)?

A: We haven't yet approached our upper strike price on the December $30-$35 vertical bull call spread. That’s usually where I bail out; I like to give stocks plenty of room to do the right thing. Stocks have to breathe and I pick strike prices to compensate for that. Otherwise, you’d be stopping out of every trade immediately.

Q: Should we close the iPath S&P 500 VIX Short Term Futures ETN (VXX) trade or leave it open?

A: I’m looking for a bit more of a rally in stocks and a drop in the Volatility Index (VIX); then we’ll try to grab whatever additional couple of pennies we can get out of that.

Q: What do you think of Brazil (EWZ)?

A: Avoid emerging markets (EEM) as long as the U.S. is raising interest rates and the dollar is strong. Rising dollar means rising debt for emerging markets and less ability to service that debt, all bad for business.

Q: Morgan Stanley (MS) says “buy emerging markets”; are they nuts?

A: For the short term yes, for the multi-year long term they are a screaming buy. They are at historical lows in terms of valuation and already have a recession priced into them. But jumping in too soon could be painful.

Q: What are your expectations for the yield curve?

A: I expect all levels of the fixed income market to drop in price and rise in yield with the sharpest move in overnight rates. This eventually leads to a very steep inverted yield curve which causes recessions and bear markets.

Q: Thoughts on Master Limited Partnerships?

A: They could be relatively safe now that oil is at $50. There have been big selloffs recently. The yield on these are high and there is going to be big infrastructure building for energy going forward. I would say don’t put all your eggs in one basket and diversify your risk. In the Great Recession, many of these went bankrupt. I would look at the Alerian MLP (AMLP), which has fallen 15% in six weeks.

Q: Should I be rotating out of the Tech (XLK) stocks on rallies into more defensive stocks like Staples (SPLS)?

A: That’s half right. You should be rotating out of Tech stocks and rotating into cash which yields up to 2-3% these days. Nothing does well in a real bear market except cash. Defensive stocks still go down, just at a slower rate.

Q: Is General Electric (GE) good for the long term?

A: Yes, if anyone can turn around GE it’s the current management. That said, it could be a long-term slog—that’s why I had a long-term leap in this thing before it collapsed. It could turn around and still go up but these are throwaway, chapter eleven level type prices that we’re getting now. And now they are going to have to do a turnaround going into a recession.

Q: Do you see GE as good for a long-term trade?

A: Long term and trade don’t belong in the same sentence; but I’d say for a long-term investment at these levels, probably yes. It certainly is a bargain from $30 down to $7.40 in a year.

Q: Is this webinar archived?

A: A: Yes, they are always posted on the website within two hours of recording. Just go to www.madhedgefundtrader.com/, login and then hover your cursor over “MY ACCOUNT” click on “GLOBAL TRADING DISPATCH,” “Mad Hedge Technology Letter” or “Newsletter” depending on your membership then click on the Webinars button. The last ten years of webinars should show up, with the most recent one at the top.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 19, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MASS EVACUATION)

(SPY), (WMT), (NVDA), (EEM), (FCX), (AMZN), (AAPL), (FCX), (USO), (TLT), (TSLA), (CRM), (SQ)

I will be evacuating the City of San Francisco upon the completion of this newsletter.

The smoke from the wildfires has rendered the air here so thick that it has become unbreathable. It reminds me of the smog in Los Angeles I endured during the 1960s before all the environmental regulation kicked in. All Bay Area schools are now closed and anyone who gets out of town will do so.

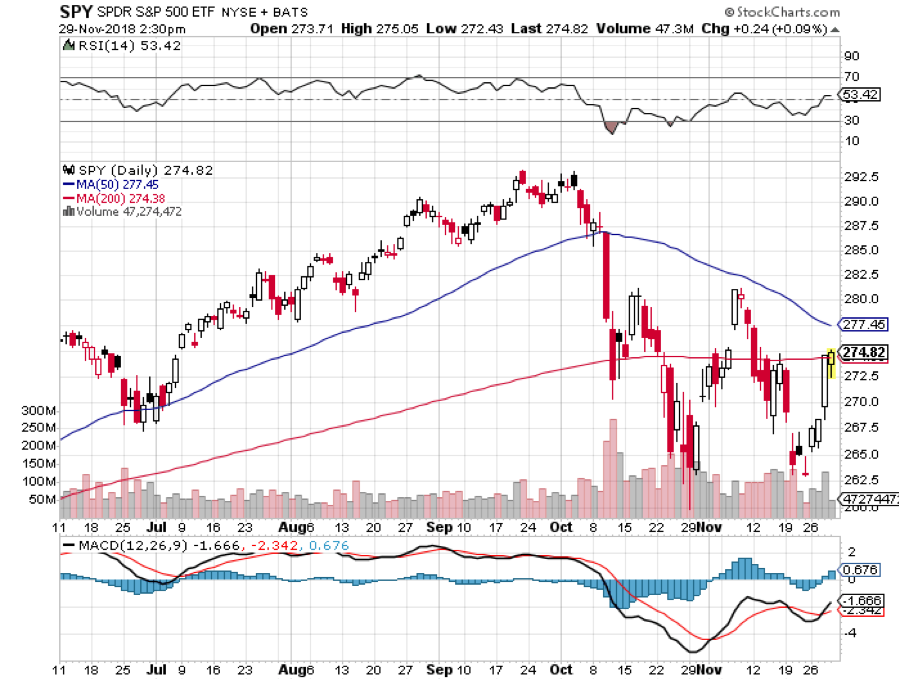

There has been a mass evacuation going on of a different sort and that has been investors fleeing the stock market. Twice last week we saw major swoons, one for 900 points and another for 600. Look at your daily bar chart for the year and the bars are tiny until October when they suddenly become huge. It’s really quite impressive.

Concerns for stocks are mounting everywhere. Big chunks of the economy are already in recession, including autos, real estate, semiconductors, agricultural, and banking. The FANGs provided the sole support in the market….until they didn’t. Most are down 30% from their tops, or more.

In fact, the charts show that we may have forged an inverse head and shoulders for the (SPY) last week, presaging greater gains in the weeks ahead.

The timeframe for the post-midterm election yearend rally is getting shorter by the day. What’s the worst case scenario? That we get a sideways range trade instead which, by the way, we are perfectly positioned to capture with our model trading portfolio.

There are a lot of hopes hanging on the November 29 G-20 Summit which could hatch a surprise China trade deal when the leaders of the two great countries meet. Daily leaks are hitting the markets that something might be in the works. In the old days, I used to attend every one of these until they got boring.

You’ll know when a deal is about to get done with China when hardline trade advisor Peter Navarro suddenly and out of the blue gets fired. That would be worth 1,000 Dow points alone.

It was a week when the good were punished and the bad were taken out and shot. Wal-Mart (WMT) saw a 4% hickey after a fabulous earnings report. NVIDIA (NVDA) was drawn and quartered with a 20% plunge after they disappointed only slightly because their crypto mining business fell off, thanks to the Bitcoin crash.

Apple (AAPL) fell $39 from its October highs, on a report that demand for facial recognition chips is fading, evaporating $170 billion in market capitalization. Some technology stocks have fallen so much they already have the next recession baked in the price. That makes them a steal at present levels for long term players.

The US dollar surged to an 18-month high. Look for more gains with interest rates hikes continuing unabated. Avoid emerging markets (EEM) and commodities (FCX) like the plague.

After a two-year search, Amazon (AMZN) picked New York and Virginia for HQ 2 and 3 in a prelude to the breakup of the once trillion-dollar company. The stock held up well in the wake of another administration antitrust attack.

Oil crashed too, hitting a lowly $55 a barrel, on oversupply concerns. What else would you expect with China slowing down, the world’s largest marginal new buyer of Texas tea? Are all these crashes telling us we are already in a recession or is it just the Fed’s shrinkage of the money supply?

The British government seemed on the verge of collapse over a Brexit battle taking the stuffing out of the pound. A new election could be imminent. I never thought Brexit would happen. It would mean Britain committing economic suicide.

US Retails Sales soared in October, up a red hot 0.8% versus 0.5% expected, proving that the main economy remains strong. Don’t tell the stock market or oil which think we are already in recession.

My year-to-date performance rocketed to a new all-time high of +33.71%, and my trailing one-year return stands at 35.89%. November so far stands at +4.08%. And this is against a Dow Average that is up a miniscule 2.41% so far in 2018.

My nine-year return ballooned to 310.18%. The average annualized return stands at 34.46%. 2018 is turning into a perfect trading year for me, as I’m sure it is for you.

I used every stock market meltdown to add aggressively to my December long positions, betting that share prices go up, sideways, or down small by then.

The new names I picked up this week include Amazon (AMZN), Apple (AAPL), Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and a short position in Tesla (TSLA). I also doubled up my short position in the United States US Treasury Bond Fund (TLT).

I caught the absolute bottom after the October meltdown. Will lightning strike twice in the same place? One can only hope. One hedge fund friend said I was up so much this year it would be stupid NOT to bet big now.

The Mad Hedge Technology Letter is really shooting the lights out the month, up 8.63%. It picked up Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and Apple (AAPL) last week, all right at market bottoms.

The coming week will be all about October housing data which everyone is expecting to be weak.

Monday, November 19 at 10:00 EST, the Home Builders Index will be out. Will the rot continue? I’ll be condo shopping in Reno this weekend to see how much of the next recession is already priced in.

On Tuesday, November 20 at 8:30 AM, October Housing Starts and Building Permits are released.

On Wednesday, November 21 at 10:00 AM, October Existing Home Sales are published.

At 10:30 AM, the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 22, all market will be closed for Thanksgiving Day.

On Friday, November 23, the stock market will be open only for a half day, closing at 1:00 PM EST. Second string trading will be desultory, and low volume.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I'd be roaming the High Sierras along the Eastern shore of Lake Tahoe looking for a couple of good Christmas trees to chop down. I have two US Forest Service permits in hand at $10 each, so everything will be legit.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 24, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or IT’S FED WEEK),

(SPY), (XLI), (XLV), (XLP), (XLY), (HD), (LOW), (GS), (MS), (TLT),

(UUP), (FXE), (FCX), (EEM), (VIX), (VXX), (UPS), (TGT)

(TEN TIPS FOR SURVIVING A DAY OFF WITH ME)

20/20 hindsight is a wonderful thing, especially when all of your predictions come true.

In February, I announced that markets would trade in broad ranges until the run-up to the midterm elections. That is what has happened to a tee, with the decisive upside breakout taking place last week. From here on. You’re trying to buy dips for a year-end run-up to higher highs.

For many months I was the sole voice in the darkness crying out that the bull market was still alive, it was just resting. Now quality laggards are taking the lead, such as in Industrials (XLI), Health Care (XLV), Consumer Staples (XLP), and Consumer Discretionary (XLY).

Home Depot (HD), which I recommended a month ago has taken off for the races, as has competitor Lowes (LOW), thanks to a twin hurricane boost. Even the long dead banks have recently showed a pulse (MS), (GS).

Technology stocks are taking a long-needed rest after a torrid two-and-a-half-year run. But they’ll be back. They always come back.

It’s not only stocks that have broken out of ranges, so has the bond market (TLT), the U.S. dollar (UUP), and foreign currencies (FXE). Will commodity companies like Freeport-McMoRan (FCX) and emerging markets (EEM) be the last to pick themselves off the mat, or do they really need to see the end of the trade wars first?

Markets are essentially acting like the trade war is over and we won. Why would traders believe this? That’s what a Volatility Index touching $11 tells you and is why I have been telling them to avoid buying it all week. Because the president told them so.

Another not insignificant positive is that multinationals have been slow to repatriate foreign funds, so there is a lot more still abroad to buy back their own stocks.

Weekly jobless claims hit another half century low at 201,000. Major U.S. companies such as UPS (UPS) and Target (TGT) are planning record levels of Christmas hiring. By the way, this is what economic peaks look like.

The Senate passes a mini spending bill that keeps the government from shutting down until December 7. The budget deficit keeps on soaring, but apparently, I am the only one who cares. Live through a debt crisis like we had during the early 1980s and you’d feel the same way.

The data for housing continues to be terrible, and we saw our first increase in inventories in three years.

Finally, with people camping out overnight and lines around the block, Apple’s CEO Tim Cook opens the doors to the Palo Alto, CA, store at 9:00 AM sharp on Friday to three new phones. But did the stock peak at $230, as it has in past release cycles?

Last week, the performance of the Mad Hedge Fund Trader Alert Service forged a new all-time high and then gave it up on one bad trade. September is now unchanged at -0.32%. My 2018 year-to-date performance has retreated to 26.69%, and my trailing one-year return stands at 38.23%.

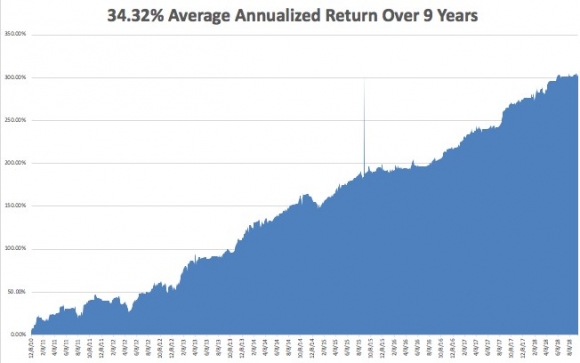

My nine-year return appreciated to 303.16%. The average annualized Return stands at 34.32%. I hope you all feel like you’re getting your money’s worth.

This coming week is all about the Fed, plus a plethora of housing data.

On Monday, September 24, at 10:30 AM, we learn the August Dallas Fed Manufacturing Survey.

On Tuesday, September 25, at 9:00 AM, the new S&P Corelogic Case-Shiller National Home Price Index for July, a three-month lagging indicator.

On Wednesday September 26, at 10:00 AM, the August New Home Sales is published. At 2:00 the Fed Open Market Committee announced its decision to raise interest rates by 25 basis points.

Thursday, September 27 leads with the Weekly Jobless Claims at 8:30 AM EST, which dropped 3,000 last week to 201,000, a new 43-year low. At the same time an update on Q2 GDP is published.

On Friday, September 28, at 9:45 AM, we learn the August Chicago Purchasing Managers Index. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me,

Good luck and good trading.

Global Market Comments

September 21, 2018

Fiat Lux

Featured Trade:

(SEPTEMBER 19 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (VIX), (VXX), (GS), (BABA), (BIDU), (TLT), (TBT),

(TSLA), (NVDA), (MU), (XLP), (AAPL), (EEM),

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 19 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Do you expect a correction in the near term?

A: Yes. In fact, we may even see it in October. Markets (SPY) have been in extreme, overbought territory for a month now, the macro background is terrible, trade wars are accelerating, and interest rates are rising sharply. The only thing holding the market up is the prospect of one more quarter of good earnings, which companies start reporting next month. So once that’s out of the way, be careful, because people are just hanging on to the last final quarter before they sell.

Q: I just got out of my cannabis stock, what should I do now?

A: Thank your lucky stars you got away with that—it was an awful trade and you made money on it anyway. Stay away in droves. After all, the cannabis industry is all about growing a weed and how hard is that? This means the barriers to entry are zero. In fact, I’m thinking of growing some in my own backyard. My tomatoes do well, so why not Mary Jane?

Q: The Volatility Index (VIX) is now at $11.79—should I buy?

A: No, the rule of thumb for the (VIX) is to wait for it to sit on a bottom for one to two weeks and let some time decay work itself out. You’ll see that in the ETF, the iPath S&P 500 VIX Short-Term Futures ETN (VXX). When it stops breaking to new lows, that means it’s ready for another bounce. I would wait.

Q: What do you think about banks here? Is it time to get in?

A: No, these are not promising charts. If anything, I’d say Goldman Sachs (GS) is getting ready to do a head and shoulders and go to new lows. I would stay away from financials unless I see more positive evidence. The industry is ripe for disruption from fintech, which has already started. That’s said, they are way overdue for a dead cat bounce. That’s a trade, not an investment.

Q: Would you short Alibaba (BABA) and Baidu (BIDU) here?

A: No. Shorting is what I would have done six months ago; now it’s far too late. If anything, I would be a buyer of those stocks here, based on the possibility that we will see progress or an end to the trade war in the next couple of months. If the trade wars continue, they will put the U.S. in recession next year, and then you don’t want to own stocks anywhere.

Q: Is Apple (AAPL) going to get hit by the trade wars?

A: So far, this has not been the case, but they are whistling past the graveyard right now—an obvious target in the trade wars from both sides. For instance, the U.S. could suddenly start applying a 25% import duty to iPhones from China, which would make your $1,000 phone a $1,250 phone. Similarly, the Chinese could hit it in China, restricting their manufacturing in one way or another. I’m being very cautious of Apple for this reason. The stock already has one $10 drop just because of this worry.

Q: Can the U.S. ban China from selling bonds?

A: No, they can’t. The global U.S. Treasury bond market (TLT) is international by nature—there is no way to stop the selling. It would take a state of war to reach the point where the Fed actually seizes China’s U.S. Treasury bond holdings. The last time that happened was when Iran seized the U.S. embassy in Tehran in 1979. Iran didn’t get its money back until the Iran Nuclear Deal in 2015. Before that you have to go back to WWII, when the U.S. seized all German and Japanese assets. They never got those back.

Q: What are your thoughts on the chip sector?

A: Stay away short-term because of the China trade war, but it’s a great buy on the long term. These stocks, like NVIDIA (NVDA) and Micron Technology (MU) have another double in them. The fundamentals are outrageously good.

Q: Is the market crazy, or what?

A: Yes, it is crazy, which is why I’m keeping 90% cash and 10% on the short side. But “Markets can remain irrational longer than you can stay liquid,” as my friend John Maynard Keynes used to say.

Q: What’s your take on the Consumer Staples sector (XLP)?

A: It will likely go up for the rest of the year, into the Christmas period; it’s a fairly safe sector. The uptrend will remain until it doesn’t.

Q: Should we buy TBT now?

A: No, the time to buy the ProShares Ultra Short 20+ Year Treasury ETF (TBT) was two months ago. Now is the time to sell and take profits. I don’t think 10-year U.S. Treasury yields (TLT) are going above 3.11% in this cycle, and we are now at 3.07%. Buy low and sell high, that’s how you make the money, not the opposite.

Q: Does this webinar get posted on the website?

A: Yes, but you have to log in to access it. Then hover your cursor over My Account and a drop-down menu magically appears. Click on Global Trading Dispatch, then the Webinars button, and the last nine years of webinars appear. Pick the webinar you want and click on the “PLAY” arrow. Just give us a couple of hours to get it up.

Q: Can Chinese companies use Southeast Asia as a conduit to export to the U.S.?

A: Yes. This is an old trick to bypass trade restrictions. For example, most of the Chinese steel coming into the U.S. is through third countries, like Singapore. Eventually they do get found out, at which point companies or imports from Vietnam will be identified as Chinese origin and get hit with the import duties anyway, but it could take a year or two for those illegal imports to get discovered. This has been going on ever since trade started.

Q: Will the currency crisis in Argentina and Turkey spread to a global contagion?

A: Yes, and this could be another cause of a global recession late next year. The canaries in the coal live there (EEM).

Q: Would you use the DOJ probe to buy into Tesla (TSLA)?

A: No, buy the car, not the stock as it is untradeable. This is in fact the third DOJ investigation Tesla has undergone since Trump came into office. The last one was over how they handled the $400 million they have in deposits for their 400,000 orders. It turns out it was all held in an escrow account. There are easier ways to make money. It’s a black swan a day with Tesla. This is what happens when you disrupt about half of the U.S. GDP all at once, including autos, the national dealer network, big oil, and advertising. All of these are among the largest campaign donors in the U.S.

Global Market Comments

September 17, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD),

(AAPL), (CBS), (EEM), (BABA), (UUP), (MSFT), (VIX), (VXX), (TLT),

(TUESDAY, OCTOBER 16, 2018, MIAMI, FL, GLOBAL STRATEGY LUNCHEON)

Talking to hedge fund managers, financial advisors, and portfolio managers around the country de-risking seems to be the name of the game. It’s like they expect a category five hurricane to hit the markets tomorrow.

Even my friend, hedge fund legend David Tepper, says that the stock market is fairly valued and that he is cutting back his equity exposure. However, he is hanging onto his position in Micron Technology (MU), which he believes is deeply oversold. Will the last person to leave Dodge please turn out the lights?

You can expect a real hurricane, Florence, to impact the coming economic data. The usual pattern is for GDP growth to take an initial hit when the big storms hit, and then make back more as reconstruction and government spending kicks in. The scary thing is that there are three more hurricanes on the way.

The big event of the week was Apple’s (AAPL) roll out of its new product line, which will beat the daylights out of competitors. Think better and more expensive across the board, with the top iPhone now costing an eye-popping $1,499.

If you are Life Alert, the private company that sells safety devices to seniors, Apple just ate your lunch. Welcome to the cutthroat world of technology investing.

The drama at CBS (CBS) played out with the departure of CEO Les Moonves. He basically generated virtually all the profits for the company for the past two decades. But in this modern age not keeping your zipper zipped carries a heavy price.

A happier departure was seen by Alibaba’s (BABA) Jack Ma, China’s richest man to focus on philanthropic activity.

Emerging markets (EEM) continued their relentless meltdown, only given a brief respite by profit taking in the U.S. dollar (UUP) on Friday.

A coming strike by the United Steelworkers may mark the onset of new wage demands by labor nationwide. In the meantime, the JOLTS report hit a new all-time high with 650,000 job openings.

For the final “screw you” of the week, Trump indicated he was going forward with tariffs on another $200 billion in Chinese imports. Consumer goods will dominate the new black list in the lead up to the Christmas shopping season. Beat the Grinch and shop early!

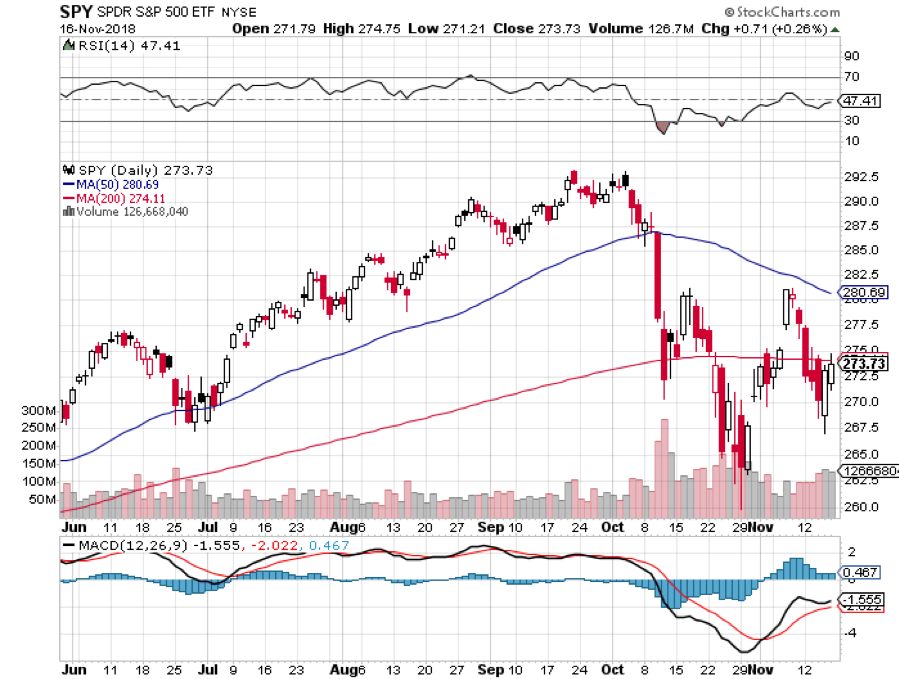

With the Mad Hedge Market Timing Index ranging from 50 to 78 last week the market keeps trying and failing to reach new all-time highs on small volume. Volatility (VIX) hit a one-month low.

Thank goodness I took profits on my iPath S&P 500 VIX Short Term Futures ETN (VXX) long. The January $40 call options have cratered from $3.60 to only $1.96. Still, there was enough price action to allow us to take nice profits on our bond short (TLT) and Microsoft (MSFT) long. Microsoft was the top-performing Dow stock last and we got in early!

Last week, the performance of the Mad Hedge Fund Trader Alert Service forged a new all-time high. September has given us a middling return of 2.42%. My 2018 year-to-date performance has clawed its way back up to 29.43% and my trailing one-year return stands at 41.35%.

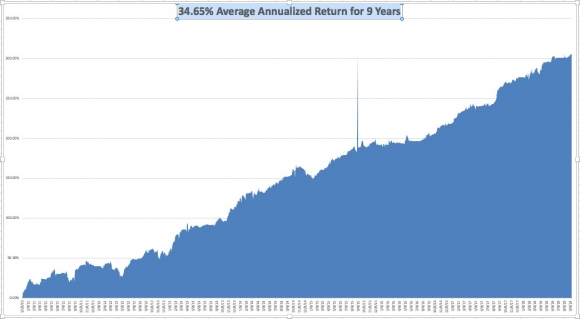

My nine-year return appreciated to 305.90%. The average annualized Return stands at 34.65%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 29.41%. I hope you all feel like you’re getting your money’s worth.

This coming week is pretty flaccid in terms of economic data releases.

On Monday, September 17, at 8:30 AM, we learn the August Empire State Manufacturing Survey.

On Tuesday, September 18, at 10:00 AM, the National Association of Homebuilders Home Price Index is released. August Home Sales is out at 10:00 AM EST.

On Wednesday September 19, at 8:30 AM, the August Housing Starts is published.

Thursday, September 20 leads with the Weekly Jobless Claims at 8:30 AM EST, which dropped 1,000 last week to 204,000.

On Friday, September 21, at 8:30 AM, we learn August Retail Sales. The Baker Hughes Rig Count is announced at 1:00 PM EST. Last week saw a gain of 7.

As for me, the harvest season in nearby Napa Valley is now in full swing, so I’ll be making the rounds picking up my various wine club memberships. Screaming Eagle check, Duckhorn check, Chalk Hill check.

Good luck and good trading.