Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE TOP DOG IN ANIMAL HEALTHCARE)

(ZTS), (AMGN), (PFE), (JNJ), (ELAN)

Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE TOP DOG IN ANIMAL HEALTHCARE)

(ZTS), (AMGN), (PFE), (JNJ), (ELAN)

You've likely witnessed a scene like this: You're at the park, and you see a young couple playing fetch with their golden retriever.

The dog is absolutely loving life, jumping and bounding after the ball, tail wagging furiously. It's a heartwarming scene, and it's one that's becoming more and more common these days.

In fact, just the other day, over coffee, a veterinarian buddy of mine spilled the beans.

"You wouldn't believe how people are pampering their pets these days," she said, shaking her head in amusement. "It's no longer just about the basics—food and health. Nope, we're talking top-tier, VIP treatment. They're ready to drop serious cash to ensure their furry friends are living their best lives."

It's a whole new world for pets, and their owners are leading the charge, wallets wide open.

And that is where Zoetis (ZTS) comes in. This company is the top dog (pun intended) in the animal healthcare space, and it's been making some serious waves in the market lately.

Now, I know what you're thinking - "What about those big-shot human healthcare stocks like Amgen (AMGN), Johnson & Johnson (JNJ), and Pfizer (PFE)?"

Well, let me tell you, Zoetis has been giving them a run for their money since spinning off from Pfizer back in 2013. This company has been posting positive annual EPS growth every single year, with an average annual EPS growth rate of a whopping 15.9%.

But that's not all — Zoetis has also been dishing out some seriously impressive dividend growth, with a CAGR of nearly 25% since it was spun off. That's right, this stock is checking all the boxes for dividend growth investors.

And if you think this is just an income play, think again.

Zoetis has been absolutely crushing the S&P 500, posting price returns of 492% compared to the market's measly 176% gains over the last decade.

So, what's the secret behind Zoetis' success?

Well, it all comes down to our furry (and sometimes scaly) friends. You see, people are lonelier than ever these days, and they're turning to pets for that much-needed companionship.

The US Surgeon General even called loneliness an epidemic, sounding the alarm on its dire impacts on health, likening its risks to smoking up to 15 cigarettes a day.

From the gripping claws of loneliness among young adults to the isolation felt by mothers with young children, the pandemic has only deepened this crisis, affecting a staggering 36% of Americans.

More than that, this loneliness trend isn't just about having a buddy to binge-watch Netflix (NFLX) with. It's actually impacting our species' survival. Studies show that sexual activity is on the decline, and technology is distorting the way we interact with each other.

It's a bit of a downer, I know, but here's where Zoetis shines through. As people turn to pets for love and affection, they're also shelling out some serious cash to keep their furry friends healthy and happy.

The American Pet Products Association says that nearly 87 million U.S. households own pets (roughly 66%), and it's not just the younger generations who are getting in on the action. Baby Boomers and Gen Xers are also big-time pet owners.

What does all this pet love mean for the industry? Well, the pet industry is expected to be a $150 billion behemoth in 2024.

Now, what really sets Zoetis apart from the pack? It all comes down to pricing power and growth potential.

In the animal health market, drug prices aren't determined by pesky regulations, government buyers, or PBMs. That means Zoetis can charge premium prices for their trusted, name-brand drugs without having to jump through hoops.

Plus, with less competition in the animal health space, Zoetis' products have longer growth runways and aren't constantly battling generic copycats.

For context, Elanco (ELAN), Zoetis' pure-play competitor, only managed to bring in $4.4 billion in sales.

So, what's the bottom line here?

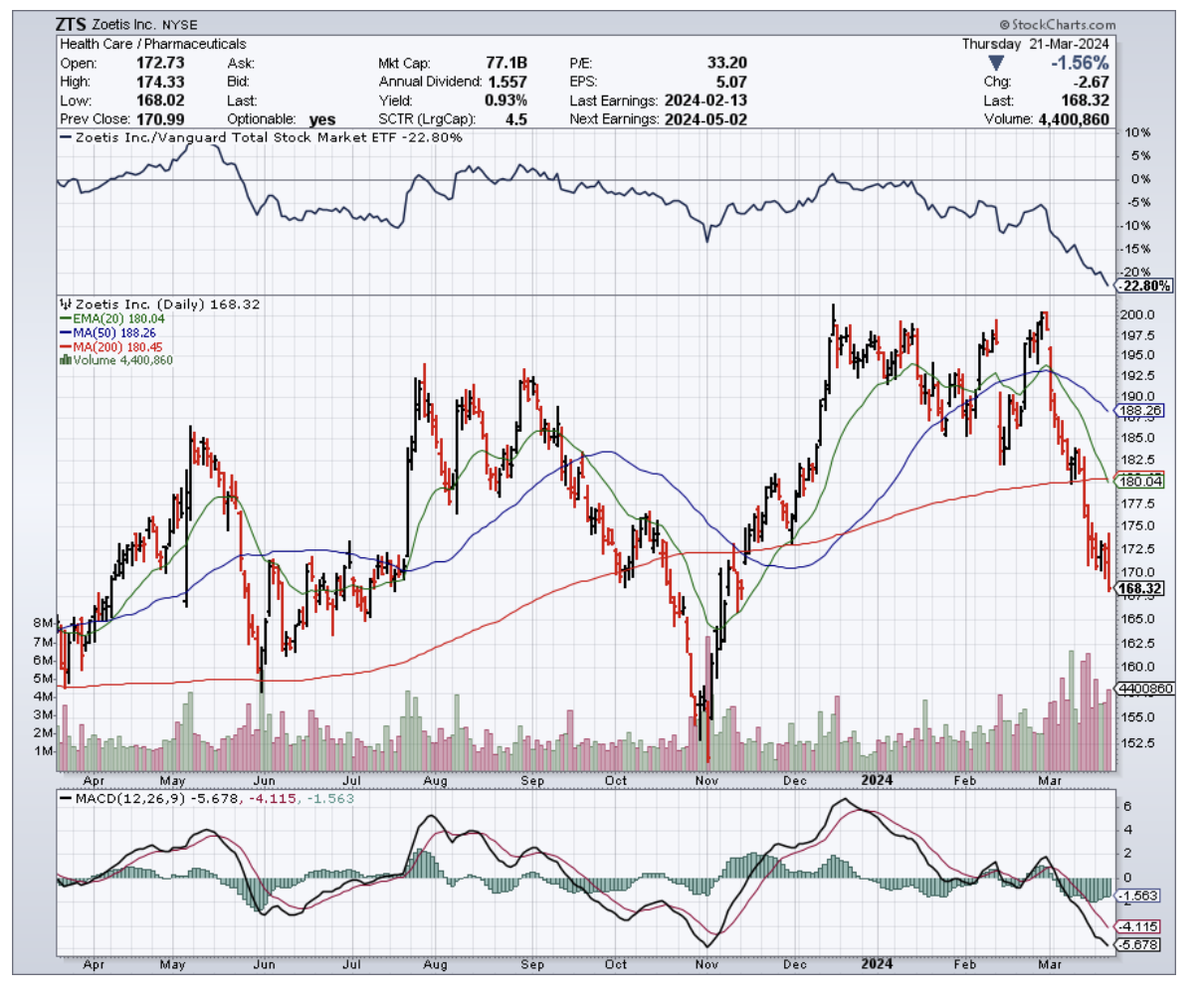

Zoetis is a best-in-breed play on the booming animal healthcare market, with a safe and growing dividend to boot. As this sell-off continues, Zoetis keeps climbing higher on my personal watch list. I'm ready to back up the truck and load up on shares come April when I put my March dividends to work.

If you're looking for a unique way to play the healthcare space with a company that's got plenty of bark and bite, Zoetis might just be the stock for you.

Mad Hedge Biotech and Healthcare Letter

November 17, 2022

Fiat Lux

Featured Trade:

(A QUALITY BEATEN-DOWN STOCK)

(ZTS), (ELAN)

Always focus on the bright side. Not only does that perspective get you in a better mood, but it can also work as good advice when it comes to making money. This becomes especially effective with the downturn of the stock market.

It’s pretty easy to discover beaten-down stocks in today’s environment. However, finding businesses that are worth your money at current levels and holding on to them for a long time is an entirely different story. Long-term stocks are not your run-of-the-mill companies, especially since many businesses with declining shares are better left alone.

While it didn’t suffer as much as the other sectors, the biotech and healthcare industry still has some beaten-down stocks that are worth buying. One of them is Zoetis (ZTS).

It has been a particularly rough year for Zoetis, with shares of this animal health company falling by over 40%. Things didn’t get better when it disclosed its third-quarter earnings report for 2022.

Going direct to the point, neither Zoetis’ earnings nor updated guidance. Zoetis dialed down its full-year guidance for 2022, estimating its initial expected revenue, which was between $8.225 billion and $8.325 billion, to fall to $8.08 billion instead.

As expected, the market reacted negatively to these figures, with the stock declining by 11%.

Although this might not appear to be a substantial drop in comparison to how other companies are performing this earnings season, it’s still a significant one-day drop for Zoetis. For context, this latest drop was the company’s second-biggest one-day decline in the past 10 years—only second to the one they recorded when COVID struck.

Reviewing the “numbers” section of Zoetis’ earnings report, one of the major causes of the lower-than-anticipated growth was supply constraints. This issue affected both US and international markets, albeit involving the former more.

Actually, “supply” was the most important issue discussed during the earnings call—so much so that the term “supply” was uttered a whopping 62 times.

It wasn’t just Zoetis that suffered from supply-related issues. These concerns affected practically the entire animal health sector this year, including another major competitor, Elanco (ELAN).

Knowing the root of the issue behind Zoetis’ recent decline is key to determining whether this remains a good stock. It always helps if we can understand the factors in play that led to the earnings report and add some context around the figures presented.

After all, the figures at times portray one thing and miss out on what is under the surface—the things that we need to understand and know about to interpret the results better.

At this point, Zoetis can still be considered an excellent company that needs to deal with some supply issues. When these are resolved, it will do just fine as a long-term investment.

Moreover, the animal health market has an incredibly bright future ahead.

This industry is projected to record a compound annual growth rate of 10% through 2030.

Pet ownership has climbed notably during the pandemic and is projected to sustain its upward trajectory in the years to come.

In addition, population growth will result in an increased demand for protein-rich food sources like livestock. That would translate to an expanded revenue stream for animal health companies, which offer products geared towards these demands.

With a market capitalization of $69.11 billion and a broad reach both in the US and across the globe, Zoetis is well-positioned to profit from this projected growth.

Moreover, this company is currently recognized as the market leader in animal health for cattle, swine, companion animals, and fish, while it ranks #5 in the global poultry market.

Overall, Zoetis is worth adding to your portfolio. While it’s facing some short-term challenges, this animal healthcare business is a pretty solid buy.

Mad Hedge Biotech & Healthcare Letter

June 24, 2021

Fiat Lux

FEATURED TRADE:

(AN ANIMAL HEALTH CARE STOCK WORTH A LOOK)

(ZTS), (PFE), (ELAN), (LLY), (IDXX), (CHWY), (FRPT)

The animal health industry has been expanding rapidly over the past years, particularly on the pet side.

If you’re treating your pets more like people, then you’re part of the growing number of customers doing the same thing.

While the “humanization” of animals has actually been going on for years, house pets have made an inexorable transition from the backyard to the couch as more and more people treat their pets as family, especially during the pandemic.

Sales for pet supplies continue to surge as pet owners splurge on everything for their furry friends, from kibble to supplements.

In fact, animal health product sales went up 7% in 2020, generating roughly $11 billion despite the pandemic—a trend that’s expected to gain even more momentum as retail sales start to shift from vet clinics to stores and online platforms.

Pfizer’s (PFE) spinoff company, Zoetis (ZTS), is the undisputed leader in the animal healthcare industry with a proven track record and a rich history spanning 65 years.

The way the company handled the challenges in 2020 showcased its ability to not only rise to the occasion but also turn red-hot despite the setbacks.

Meanwhile, Zoetis stock experienced continuing growth in 2021.

Revenues from its Simparica franchise, which fights off heartworms and other parasites in dogs and cats, grew by 133% year-on-year in the first quarter of 2021 thanks to its expansion in the US, Europe, Australia, and Canada markets.

Next to the US, Zoetis’ biggest market is China. In the first quarter of this year, the company saw a 75% climb in its revenues in the region, raking in $123 million for the period.

Simparica Trio, which generated $90 million in the first quarter alone, also received approvals in new markets, such as Japan and Mexico.

Its predecessor, Simparica, also continues to rake in good numbers, with $74 million in sales during the same period.

However, another player appears to be making big moves to dethrone the company.

Elanco Animal Health (ELAN), which is a spinoff of Eli Lilly (LLY), struck an impressive $440 million deal to acquire Kindred Biosciences (KIN) in an effort to bolster its drug pipeline.

This deal, which is expected to close in the third quarter of this year, will focus primarily on Elanco’s pet dermatology segment.

The move to invest in dermatology is a great decision for Elanco. Dermatology has become one of the fastest growing divisions of pet care.

For context, Zoetis’ 2020 revenues for this segment reached $925 million, recording a $170 million boost from its 2019 earnings.

The dermatology segment grew 24% year on year in the first quarter of 2021 as well, recording $245 million in revenues for this period.

Looking at the performance of the products in this segment, Zoetis is on track to exceed the $1 billion revenue estimate for 2021.

Outside its dermatology segment, Zoetis also enjoyed a 47% year-on-year growth in its diagnostics sector in the first quarter—a trend that’s anticipated to improve in the long run due to the company’s continuous expansion globally.

Zoetis stock is projected to continue its momentum throughout 2021 and well beyond 2022.

For this year, the company estimates revenue growth by 9% to 11%, which would be driven by the pet care segment, additional product launches, and rising demand for their existing drugs. The reopening of the economy also plays a key role in this growth.

Other than Elanco and Zoetis, some companies working on dominating the booming animal health care sector include Idexx Laboratories (IDXX), Chewy (CHWY), and FreshPet (FRPT).

Overall, Zoetis stock has offered excellent returns for its investors. Looking at its pipeline programs and future plans, the company shows great potential for growth in the coming years.

Investors on the lookout for a stock in the animal health industry would be wise to take Zoetis into serious consideration.

Mad Hedge Biotech & Healthcare Letter

April 22, 2021

Fiat Lux

FEATURED TRADE:

(THE PFIZER OF ANIMAL HEALTHCARE IMPRESSES WITH GROWTH DRIVERS)

(ZTS), (PFE), (ELAN), (IDXX)

The World Health Organization has yet to offer definitive proof that animals can infect humans with COVID-19.

However, there had been cases where humans infected the animals, including tigers, minks, lions, and domestic cats and dogs.

This might seem insane to some since we’re not even done vaccinating humans yet, but it definitely presents a large and potentially lucrative market.

Recently, Russia launched the first and only registered COVID-19 vaccine for animals, Carnivac-Cov.

Not to be outshone, Zoetis (ZTS), the leader in animal healthcare in the United States, also started working on its own COVID-19 vaccine.

In fact, Zoetis has already commenced testing its candidate on some great apes at San Diego Zoo earlier this month.

So far, the company administered two vaccine shots to three gorillas, four orangutans, and six bonobos.

Zoetis’ efforts date back to last year when news broke that dogs and cats in Hong Kong were also getting infected with COVID-19.

While the USDA has not yet approved the vaccines for dogs and cats, the organization is leaning towards giving the green light for minks.

As it turns out, minks are extremely susceptible to COVID-19, so vulnerable that Denmark actually ordered a mass culling of millions after an outbreak in November 2020.

To date, several zoos have already reached out to Zoetis to avail of its experimental COVID-19 vaccine.

Considering that all these started with the cross-species transmission, experts are also hoping to learn more about it with the help of the company to prevent future pandemics.

Zoetis is ideally positioned to lead this charge since it’s the frontrunner in the pharmaceutical sector for pets and livestock.

This company used to be a branch of Pfizer (PFE), but was later spun off in 2012 to stand on its own.

In terms of competitors, the two most relatable companies to Zoetis are Elanco Animal Health (ELAN) and IDEXX Laboratories (IDXX).

Both offer virtually the same products, but Zoetis is the biggest among the three with approximately $75 billion in market capitalization.

In comparison, IDXX has roughly $41.55 billion, while ELAN has $13.61 billion.

Knowing that there’s more than a single way to expand its business, Zoetis has been favoring acquisitions as one of its growth options.

In the past years, Zoetis has been on a buying spree, making no less than eight acquisitions so far.

Half of these are geared towards veterinary diagnostics, with the intention of dominating the fastest-growing sector of the animal healthcare industry.

All its recent acquisitions put Zoetis directly in competition with IDEXX, which is currently the undisputed leader in the veterinary diagnostics space.

To show the disparity of their current standing, IDEXX raked in $2.4 billion in revenue from diagnostics in 2020, while Zoetis only generated $305 million.

Needless to say, Zoetis has a lot of catching up to do.

Zoetis initiated its venture with a splashy $2 billion acquisition of Abaxis in 2018, which provided the ex-Pfizer company with a powerful foundation in the diagnostics sector.

This was immediately followed by a $35 million deal to buy ZNLabs in 2019. In that same year, Zoetis bought Phoenix Lab for $150 million and then continued its streak to acquire Ethos Diagnostic Science in 2020.

Apart from its venture in the diagnostics space, Zoetis has been working on bolt-on acquisitions to enhance its operations.

A good example is its $140 million acquisition of Performance Livestock Analytics in 2020, which added a software platform that Zoetis could market to farmers to help them make their farms more efficient.=

Another one is its $20 million deal with Fish Vet Group, which basically created the same platform as Performance Livestock Analytics but modified it for fish producers.

Looking at Zoetis’ acquisitions, the company is clearly building a diverse portfolio of products that go beyond pharmaceuticals.

It’s evident that it aims to enhance its leverage on tangential businesses like diagnostics and even farm management.

While these new revenue sources are definitely interesting, they’re not moving the needle just yet. Zoetis is still primarily relying on its sales of pet and livestock drugs.

Aside from developing a COVID-19 vaccine, Zoetis has been working on a strong drug pipeline.

Despite separating from Pfizer, the strategies it implemented in building its extensive and diverse portfolio of blockbuster products pretty much follow the same path and trajectory as its previous parent company.

For context, “blockbuster” drug is any product that generates a minimum of $100 million in sales annually.

Using this metric, Zoetis holds an impressive lineup of 13 blockbuster products.

In 2020, Zoetis released a “triple threat” product called Simparica Trio, which can protect dogs from heartworms, eliminate ticks and fleas, and treat and prevent hookworms and roundworms.

This is the first-ever product that offers combined protection for all three—fleas, heartworms, and ticks—in a single treatment.

Despite the financial impact of the pandemic, Simparica Trio still raked in an impressive $150 million in its first year.

Reviewing its future product pipelines, Zoetis has two more potential blockbusters slated this year: Librela and Solensia. These two will also be the first-of-a-kind treatments for osteoarthritis in cats and dogs.

Delving deeper, Zoetis holds No. 1 spot in the companion animals or pets, fish, and livestock cattle segments. It ranks No. 2 in the swine market and No. 3 in the poultry sector.

In total, Zoetis has more than 300 product lines launched in the market, and the company still has more lined up for release soon.

Akin to Pfizer’s approach, Zoetis’ style is to dominate in select core markets, developing numerous blockbuster brands that generate billions every year.

Admittedly, the human healthcare market is substantially more profitable than its animal counterpart, but for Zoetis, this also represents significantly less competition from other drug developers.

At this point, Zoetis is not only in a strong position in the animal healthcare industry, but also dominating in a market that still has incredible room for growth.

In 2020, the total pet industry market was estimated to be worth $99 billion in the United States alone.

More importantly, this segment is projected to climb in the mid-single digits in the next few years.

A key approach in Zoetis’ growth is its strategy to develop and sustain a product pipeline with an average lifespan or age of at least 30 years.

The company also constantly launches new drugs and announces enhancements to their current products.

These are seen in the over 1,100 new products and improvements Zoetis has introduced over the past five years.

Judging from the company’s performance and future plans, it’s reasonable to expect a $200 price target for Zoetis over the next 12 months, which would indicate about 26.50% upside potential based on the current trading levels.

Taking into consideration the potential 5% downside risk, shares could pull back to reach $153 before starting to rebound again.

Meanwhile, the highest price target for Zoetis could be $210.

Overall, I believe Zoetis is a stable company with strong upside potential in the next months, and growth investors would be remiss to ignore the achievements of this company.