Mad Hedge Biotech and Healthcare Letter

October 24, 2024

Fiat Lux

Featured Trade:

(A HEALTHCARE STOCK THAT OWNS TOMORROW)

(UNH), (HUM), (ELV), (CVS)

Mad Hedge Biotech and Healthcare Letter

October 24, 2024

Fiat Lux

Featured Trade:

(A HEALTHCARE STOCK THAT OWNS TOMORROW)

(UNH), (HUM), (ELV), (CVS)

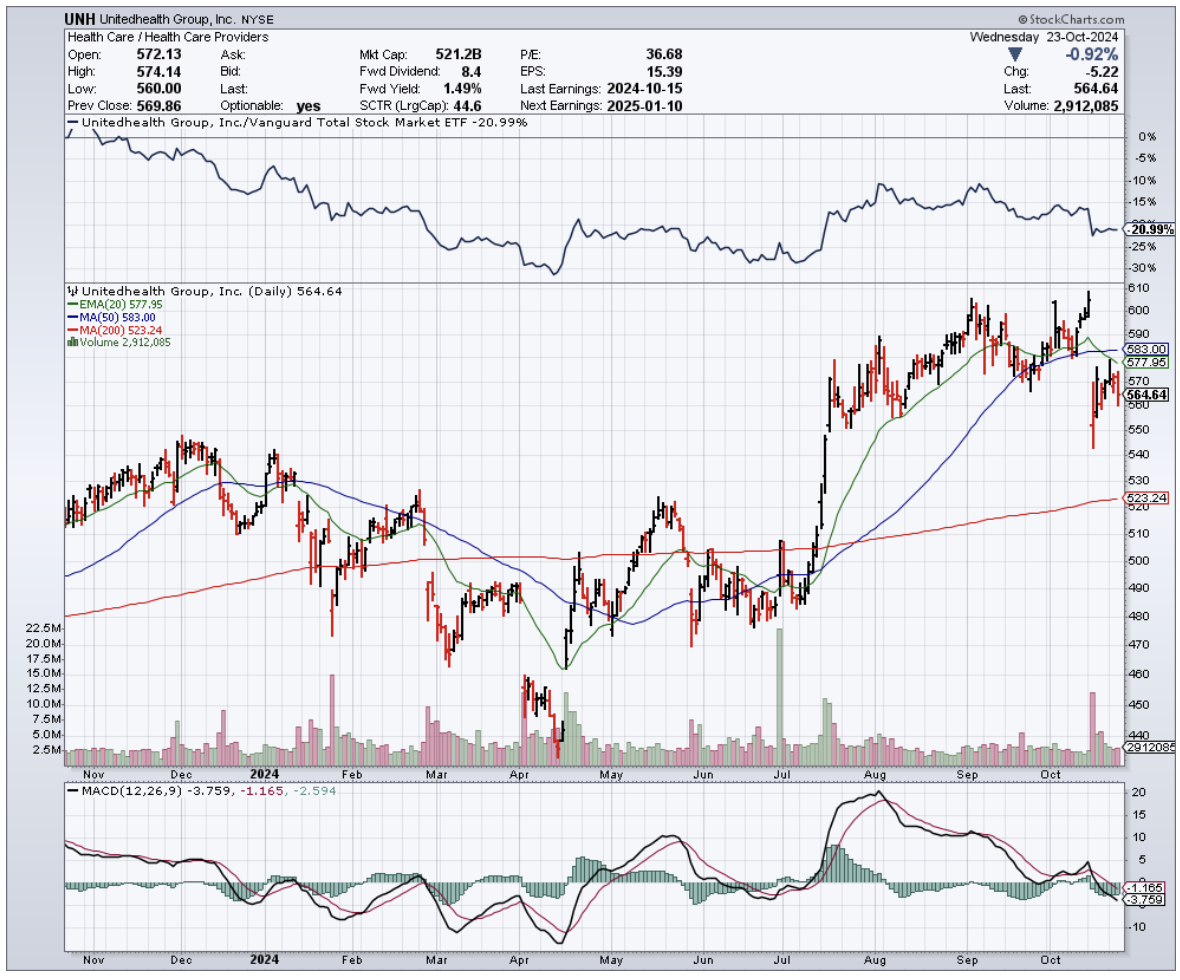

After decades of watching healthcare stocks, I've learned one immutable truth - demographics always win. And right now, demographics are handing UnitedHealth Group (UNH) the keys to the kingdom.

The numbers tell an impressive story. UnitedHealth just reported Q3 2024 revenue of $100.82 billion, up 9.2% year-over-year. That's a billion dollars above what Wall Street expected, even after weathering a nasty cyberattack on their Change Healthcare unit in February.

Let's put this in perspective. By 2031, America's national health expenditure will hit $7.17 trillion - more than the GDP of Japan and Germany combined. This isn't just another growth story.

Besides, having managed hedge fund money through multiple market cycles, I’d like to think that I know the difference between lucky timing and structural advantage. From the looks of how things are going, UnitedHealth has engineered themselves the latter.

The company's UnitedHealthcare segment tells only part of the story, bringing in $74.85 billion in Q3, up 7.2% from last year.

Their Medicare Advantage enrollment grew from 7.65 million to 7.81 million people, while their U.S. commercial health plans expanded from 27.25 million to 29.73 million members.

Yes, they took a hit on their global numbers after selling their Brazilian business - dropping from 5.48 million to 1.34 million customers. But sometimes the best deals are the ones you don't do.

The real story here is Optum and its aggressive push into value-based care.

While competitors are still figuring out how to merge technology with healthcare delivery, UnitedHealth has already built a fortress. Their $13 billion acquisition of Change Healthcare wasn't just about processing claims - it was about owning the healthcare data highway.

Optum's revenue jumped 12.5% to $63.79 billion, with their pharmacy division surging 18.5% to $34.21 billion. They processed 410 million prescriptions in Q3 alone - that's 30 million more than last year.

What Wall Street is missing is UnitedHealth's positioning for the post-COVID healthcare landscape. They're not just riding the telehealth wave - they're reshaping it.

Their OptumRx digital platform now handles 80% of all prescription transactions, while their virtual care visits have grown tenfold since 2019.

In fact, the regulatory environment plays into their hands.

While smaller players struggle with Medicare Advantage rate adjustments and value-based care requirements, UnitedHealth's scale and technology infrastructure turn these challenges into opportunities.

Their compliance systems and data analytics capabilities give them a moat that gets wider every quarter.

Wall Street expects Q4 revenue between $100.48 billion and $104.14 billion. Their P/S ratio of 1.41x looks rich compared to Humana (HUM) at 0.29x and Elevance Health (ELV) at 0.57x. But in this market, scale and execution command a premium.

Looking ahead, I see UnitedHealth hitting $552 billion in revenue by 2028. The catalysts are clear: aging demographics, rising chronic disease management post-COVID, and the unstoppable march toward value-based care.

Their Q3 non-GAAP EPS of $7.15 beat estimates by 12 cents. By 2028, I expect EPS to reach $44, with their P/E ratio dropping from 22.75x to 12.99x.

Their balance sheet remains rock solid - net debt/EBITDA ratio below 1.5x, with investment-grade ratings from S&P Global (SPGI), Fitch, and Moody's (MCO).

UnitedHealth also keeps growing its dividend by double digits, maintains a predictable business model, and outperforms competitors like CVS Health (CVS) and Humana on ROE.

Admittedly, they slightly lowered their 2024 adjusted EPS guidance, spooking some traders. But in my experience, Wall Street's short-term panic creates long-term opportunities.

So, what’s the play here? I suggest you build a position in UnitedHealth now while the stock has pulled back. Scale in gradually if you're concerned about timing, but don't miss this opportunity.

Remember, in the end, this isn't just about healthcare - it's about owning a piece of America's unstoppable demographic destiny. And that's a trend even a skeptic like me can believe in.

Mad Hedge Biotech and Healthcare Letter

January 25, 2024

Fiat Lux

Featured Trade:

(FROM BIG TO BIGGER)

(UNH), (CI), (ELV), (CVS)

Today, let's talk about where the smart money's at in our whirlwind economy – healthcare and insurance.

And who's the king of the hill in this game? None other than UnitedHealth Group (UNH).

It's not just any old company; it's a health insurance juggernaut that's been on a growth tear, doubling its value in just five years. That's definitely something to write home about.

With a market cap closing in at $500 billion and revenues of $372 billion in 2023, it's a force to be reckoned with. If it doubles again, we're looking at a $1 trillion giant. That's uncharted territory for healthcare stocks.

Before anything else, let's hop in our time machine for a sec.

Around 10 years back, UnitedHealth was a mere $75 billion baby. Fast forward to today, and it's ballooned to around half a trillion. We're talking about top-dog status in the healthcare world.

Now, let's get down to brass tacks. UnitedHealth's bottom line might not be the stuff of legends – a 6% profit margin over the past year.

But hold your horses – with over $300 billion in annual revenue, that 6% turns into a cool $18 billion-plus in profit.

And guess what? They've been raking in even more lately – $21.7 billion over four quarters.

"But will it double in value in a year or two?" you ask. Maybe not that fast, but hey, it's done it in five years before.

So, could UnitedHealth hit that mind-boggling $1 trillion mark by 2030? I wouldn't bet against it.

After all, UnitedHealth isn't just playing in the health insurance sandbox. It's the biggest kid in the playground – the largest health insurer in the United States and the biggest healthcare company globally.

For context, its closest peers are Cigna (CI) with $90.44 billion in market cap, Elevance (ELV) with $111.87 billion, and CVS (CVS) with $95.08 billion. You get the picture.

But here's the juicy part – UnitedHealth loves to shop. It's like the Pac-Man of healthcare, gobbling up companies left and right.

Just last year, it bagged Amedisys for a cool $3.3 billion, hot on the heels of its $5.4 billion acquisition of LHC Group. Talk about making moves.

Now, for my fellow investors, here's the sweetener: UnitedHealth also pays dividends, with a 1.4% yield. It might not sound like much, but this company's got a knack for growing dividends. It's like owning a golden goose that keeps laying more golden eggs.

So, what's the secret sauce for UnitedHealth potentially hitting that $1 trillion valuation? Simple – growth, growth, and more growth. It's not just selling insurance; it's into analytics and isn't shy about snapping up companies to beef up its portfolio.

Let's talk numbers. Management is eyeing an annual earnings growth somewhere between 13% and 16%. If UnitedHealth keeps hitting these home runs, its stock value climbing higher isn't just a possibility – it's a likelihood.

"But is it a good buy?" I hear you ask. Well, trading at around 23 times its earnings, it's a bargain compared to the average healthcare stock at 28 times earnings.

Simply put, this baby's got room to grow, and investors might just be willing to pay a premium for this gem.

So, when will it hit $1 trillion? If UnitedHealth sticks to the S&P 500 index's average 10% annual growth, we're looking at 2030 for that milestone.

But knowing UnitedHealth, which often outperforms the market, it could be sooner if it keeps up its projected annual growth rate.

In a nutshell, UnitedHealth Group isn't just a safe bet – it's a potential goldmine. With its continued growth, strategic acquisitions, and reasonable price tag, it's a shining star in any investment portfolio.

Mark my words – this is one stock that could make its investors very, very happy by 2030.

Mad Hedge Biotech and Healthcare Letter

December 8, 2022

Fiat Lux

Featured Trade:

(THE MASTODON OF HEALTHCARE)

(UNH), (HUM), (CI), (ELV), (CVS)

Most earnings reports across all industries recently include the terms “inflationary pressures,” “short-term macroeconomic conditions,” “labor shortages,” and, of course, “supply chain issues” to justify why revenues are down or flat. The S&P 50 index has declined by over 20% to date, with signs of sliding further.

Clearly, the economy cannot be described as recession-proof. It typically follows a relatively predictable, albeit irregular, path commonly called the economic cycle. Needless to say, recessionary periods can be heartbreaking and brutal for the market and its investors.

However, some sectors are somewhat immune to the ups and downs of the economy. These industries provide investors with recession-proof stocks that can be held onto during these challenging periods. One of them is the healthcare industry.

Healthcare stocks, particularly high-quality businesses, tend to be viewed as recession-proof. Despite the economic turbulence, companies in this sector still enjoy relatively solid and steady demand. That’s not entirely shocking since people can’t exactly just cancel their healthcare needs.

No matter what’s happening in the world, when you’re unwell, you have no other option but to see a doctor and get medicine.

Within the healthcare sector, not all businesses are created equal. Some still felt the recession's nasty consequences, while others managed to thrive.

One name that continues to impress amid the economic turmoil is UnitedHealth Group (UNH).

Basically, UNH operates 2 main segments.

One is UnitedHealthcare, which offers a complete range of healthcare insurance. The other is Optum Health, which provides data-driven healthcare gathered from partner surgery centers. It also obtains information from OptumRx, UNH’s pharmacy management arm.

Both UnitedHealthcare and Optus Health delivered excellent results to date, boosting the company’s full-year guidance from $20.85 to $2105 in terms of EPS. In comparison, UNH recorded an annual EPS of $18.08 back in 2021.

In the first 9 months of 2022, UNH raked in $192.5 billion in revenue. This shows a 14% increase year over year. Meanwhile, its earnings per share climbed to $16.15 compared to the $13.82 it reported during the same period in 2021.

One of the key drivers for these results is the boost in the number of subscribers to UNH’s services, which rose by 850,000 in 2022. Apart from these, the company has an attractive dividend that keeps investors satisfied. For the 13th consecutive year, UNH has raised its dividend, announcing a quarterly boost of 14% to reach $1.65.

Keep in mind that the health insurance industry climbs higher each year, and COVID-19 has forced everyone to reconsider and review their perspectives towards healthcare.

On top of these, UNH’s long-term growth is supported by the inevitable: the continuous and increasingly expensive demands of an aging population. That is, the company has a massive addressable market that keeps on expanding year after year.

Looking at the trajectory of this industry, it is estimated that 73.5 million individuals will be enrolled in Medicare by 2027. This represents a 28.5% boost from the 57.2 million reported in 2017.

Due to the increasing demands in healthcare in the coming years, particularly among the aging population, spending in this segment is also anticipated to rise rapidly. In fact, healthcare spending is projected to hit $6 trillion annually by 2028.

Thus far, UNH is hailed as the leading company in healthcare. The company’s hegemony looks and feels incomparable, and none of its competitors appear to be strong enough to dethrone it. For context, the leading rivals of UNH in the US include Humana (HUM), Cigna (CI), Elevance (ELV), and CVS Health (CVS).

For these competitors to stand a chance at beating or at least competing with its on equal grounds, they would need to merge—a move they’ve all attempted in the past but were blocked by regulators.

Overall, UNH remains a solid choice, especially during these trying times. This company is a widely respected mastodon in the insurance market worldwide, showing off substantial growth in revenue and profit practically every year. Buy the dip.