Global Market Comments

October 17, 2025

Fiat Lux

Featured Trade:

(OCTOBER 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (SPX), (SLV), ($INDU), (GS), (PLTR), (UUP),

(FSLR), (ENPH), (NVDA), (AMD), (NFLX), (BTC)

Global Market Comments

October 17, 2025

Fiat Lux

Featured Trade:

(OCTOBER 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (SPX), (SLV), ($INDU), (GS), (PLTR), (UUP),

(FSLR), (ENPH), (NVDA), (AMD), (NFLX), (BTC)

Call this the Dr. Jekyll and Mr. Hyde market.

On the up days, we see the kindly ministrations of Dr. Jekyll.

On the down days, we suffer from the evil hand of Mr. Hyde.

To say that traders are confused would be an understatement. Many seasoned pros have told me that this is one of the most difficult markets they have ever seen.

Fridays have been particularly treacherous when weekly options expire. Some 56% of all options trading now takes place with expirations of five days or less. Trading before 4:00 PM sees billions of dollars of hot money trying to force closing prices just in or out of the money for key at-the-money strike prices.

What is especially disturbing is that some 80% of the gain in the S&P 500 (SPY) this year has been in just seven names, Meta, (META), Alphabet (GOOGL), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Tesla (TSLA). Most other stocks went nowhere….or down. That much concentration means that any rallies lack confidence and will fail….for now.

Remember these names because when we finally do get a real upside breakout, they will be the leaders. You can take that to the bank.

Thanks to turmoil in the House of Representatives intent on a national default, bonds have given up 70 of the 120-basis point drop in yields since October. That deprives us of one of our biggest money makers of 2022, our long bond trades.

That means were are also seeing the automatic flip side of the bond trade, a strong US Dollar (UUP), and weak precious metals, (GLD) and (SLV), and emerging markets (EEM).

This too shall end.

If it was excess liquidity that caused stocks to rocket for 13 years, then maybe we should be focusing on what little liquidity is left. That would be the font of government money pouring into infrastructure and alternative energy plays.

Some $370 billion I know available for investment in ESG, would most of it going into the battery industry for the burgeoning electric vehicle industry. Even foreign firms like Finland’s Neste is moving to the US to cash in on federal munificence, converting an old US oil refinery to produce diesel fuel out of animal and vegetable fat (click here for the link).

Probably the best bet here is in California-based Enphase Energy (ENPH), which makes a 40% gross profit margins on microinverters for solar panels and has just seen a 42% dive in its share price. That makes (ENPH) a BUY. Hint: solar stocks always follow the price of oil to which it is tied, which has lately been down.

Some nimble and aggressive trading managed to push me back in the green for February, taking me up +0.93% on the month. That’s a dramatic improvement of +5.48% from a week ago.

You might even call it making a silk purse from a sow’s ear.

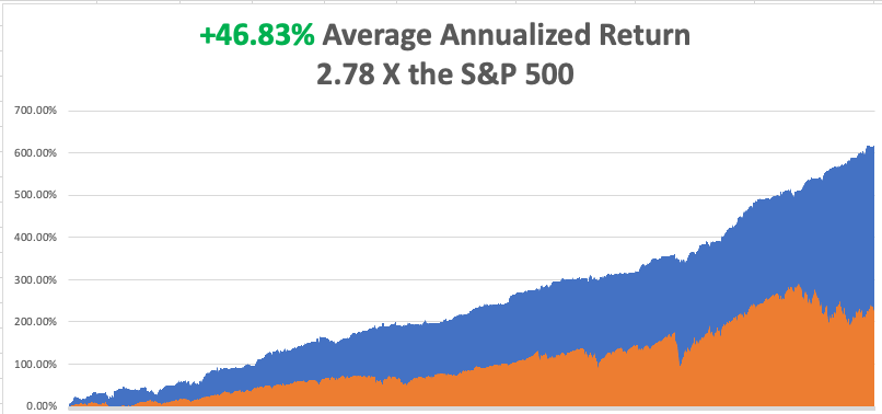

My 2023 year-to-date performance is still at the top at +23.28%. The S&P 500 (SPY) is up +4.32% so far in 2023. My trailing one-year return maintains a sky-high +86.58% versus -12.97% for the S&P 500.

That brings my 15-year total return to +620.47%, some 2.78 times the S&P 500 (SPX) over the same period. My average annualized return has recovered to +46.83%, still the highest in the industry.

Last week, I piled on a Tesla (TSLA) March $155-$260 short strangle betting that the stock can stay within a $95 range for 19 trading days. I also added a deep in-the-money long in the bond market for the first time in six weeks. Both positions turned immediately profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

Q4 GDP Dips, from 3.9% to 2.7% in the October-December quarter. Consumption took a dive, which is amazing over the holidays. This is nowhere near a recession.

Fed Minutes Show More Hikes to Come, with the emphasis on the plural. That could take the overnight borrowing rate to a 5.40% high. It certainly pees on the parade for the falling interest rates crowd.

The Tail is Wagging the Dog, with short, dated options, often same-day expiration dominating trading every Friday. Billions of dollars are battling around key strike prices attempting to force expirations in or out of the money. No place for the little guy. Better to take Fridays off.

Netflix Slashes Prices in 30 countries, taking the stock down a modest 3%. (NFLX) is still the leader in the sector with 231 million subscribers, followed by Amazon (200 million), Disney Plus (162 million, HBO Max (95 million, Peacock (18 million), and Hulu 47 million). Buy (NFLX) and (AMZN) on dips.

Individual 401k’s Lost 23% in 2022, according to a study from Fidelity. High inflation is shrinking the remaining purchasing power even faster. A rising number of workers are also borrowing against their 401k’s to make ends meet. Such loans can go up to 50% of the principal. Better start making up the losses or you’ll be spending your golden years working at Taco Bell.

Apple to Add Glucose Monitor on its Watches, to aid diabetic clients. Some 38 million Americans have diabetes and given the obesity epidemic that figure is certain to rise. It highlights Big Tech’s move into the low-hanging fruit in health care.

Existing Home Sales Dive 0.7% in January, to a 4 million annualized rate, the weakest since October 2010. That makes 12 consecutive months of falling sales. The Median Home Price sold rose to $359,000. An imminent national debt crisis and spiking interest rates is not a great environment in which to sell your home.

Biden Ukraine Visit Tanks Gas and Oil Prices, cutting Russia’s chances of a win and eventually leading to a flood of oil on the market. Biden’s visit is sending the message to Putin that there’s no chance of a win here. Energy is hitting two-year lows across the board. Only energy stocks are staying high. Energy is getting so cheap it might be worth a trade.

Germany Accelerates Move Towards Alternatives, permanently cutting all ties with Russia energy. Europe’s biggest economy, and the fourth largest in the world, hopes to get 80% of its electricity from solar and wind by 2030. Hydrogen is also entering the picture. Other countries will follow.

On Monday, February 27 at 8:30 AM EST, US Durable Goods are out.

On Tuesday, February 28 at 9:00 AM, the S&P Case Shiller National Home Price Index for December is released.

On Wednesday, March 1 at 10:00 AM, the ISM Manufacturing PMI is printed.

On Thursday, March 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 3 at 8:30 AM, the ISM Non-Manufacturing PMI. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elisabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if broadcast came from the White House.

After Roosevelt’s death, the Potamac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potamac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point there was an attempt to turn it into a floating disco.

In 1980 a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, Ca for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down-to-the-rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former coast guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. No body was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm

Mad Hedge Technology Letter

August 2, 2021

Fiat Lux

Featured Trade:

(ENPHASE IS WORTH A LOOK)

(ENPH)

Despite the global pandemic destroying large swaths of the U.S. economy, the solar sector has been a revelation and is one of the few industries that benefits from global warming.

Enphase Energy (ENPH) founded in 2006 has long been regarded as the world leading microinverter manufacturer.

What is a Micro Inverter?

A micro inverter is a very small inverter designed to be attached to each individual solar panel.

Based in the US, Enphase launched the first micro inverter, the M175 in 2008 but it wasn’t until the next-gen M190 was launched in 2009 that sales really took off.

Enphase has since established itself as an industry leader in micro inverter technology and has a huge market share in North America.

Under normal seasonality, the solar industry typically strengthens each quarter with the first quarter being the weakest boding well for the end of 2021.

The company reported revenue of $316.1 million, shipped approximately 2.36 million microinverters and 43-megawatt hours of Enphase storage systems, achieved non-GAAP gross margin of 40.8%.

The demand for microinverter systems continues to be well ahead of supply.

In Q2, Enphase experienced component constraints on the supplier AC Fed drivers, which resulted in microinverter shipment volume slightly lower as compared to Q1.

For the third quarter, Enphase continue to expect to remain constrained on microinverters, but the supply situation is better than what it was in the second quarter.

One of Enphase's critical competitive advantages is that the company operates more as a technology company than a commodity manufacturer.

While other companies do produce its main power inverter product, Enphase has market dominance in the micro-inverter segment.

For residential solar applications, micro-inverters do offer an advantageous alternative. Enphase's shipment growth over the past couple of years is the empirical evidence.

Even more salient, the company avoids ruinous capital expenditures by deploying contract manufacturing similar to peers with proprietary technology.

By leveraging these variables, Enphase has accelerated its high gross margins above 30% and now up to 40% in Q2 2021.

The company's lower margins last year were in part due to higher expedited shipping costs to satisfy demand but has solved that bottleneck and boosted gross margins.

Enphase's stable high gross margin is the x-factor.

Most solar module producers have high fixed costs which deteriorate margins and drag down utilization rates.

As a result, not only do shipments gyrate between industry cycles but also gross margin. While Enphase is also exposed to industry fiscal cliffs, high gross margins should be highly constructive even in down years.

During up cycles, Enphase's high gross margins and lower operating structure give it abnormally advantageous earnings leverage.

Enphase's earnings leverage will be even more dramatic once revenue growth reaccelerates after the pandemic filters through the U.S. economy.

Up until now, Enphase has been pigeonholed as an inverter company within the solar industry.

The company did offer a battery storage option, but it was not an overwhelming segment of total revenues.

This may change moving forward after the company's next-generation Encharge storage option released lately has shown glimpses of stardom among its competition.

Democrats hellbent on adopting clean energy might unearth an opportunity for sweeping change for US solar companies such as Enphase.

It’s already trending in that direction as a mega growth industry like technology.

Also, the Democrats are trying to crowbar in any climate-related infrastructure spending with adjacent bills.

If annual residential solar installations double with a slightly higher per home average, about one million homes would be converted to solar annually.

With over 139 million homes in the US, only a small fraction would be converted to produce solar electricity over the next decade or two, even if the US residential solar market doubled.

The main takeaway is that the solar market in the US still has huge upside under the Democrats and U.S. President Joe Biden.

Enphase has a current micro-inverter capacity of 10 million units annually and based on its per-unit assumption of 325 watts, can supply 3.25 GW annually.

Should the US solar market double due to beneficial policies, Enphase's potential market share will rise above 34%.

Ultimately, Enphase's high margins and fixed cost structure should not be underestimated especially under a systemic industry shift led by the US economy laser-focused on green infrastructure.

The secret recipe of high gross margin and low-cost structure make Enphase incredibly leveraged to top-line growth.

Lately, a new storage revenue stream and continued shipment growth in a rapidly expanding solar market should result in overperforming earnings growth.

New storage products will meaningfully add to earnings next year without diluting gross margin.

I first recommend this stock when it was trading at $120 in November 2020 and readers who bought into this story made a killing with the stock already at $189 today.

Enphase said its sales in the coming quarter should range from $335 million to $355 million, up about 1.5% from Q3 2020, and slightly above analyst expectations.

Gross profit margin, however, will move into reverse, continuing to fall below 40%, and perhaps as low as 37% therefore I would wait for a substantial correction before getting back into this one.

Mad Hedge Technology Letter

November 6, 2020

Fiat Lux

Featured Trade:

(IN THE KNOW ABOUT ENPHASE ENERGY)

(ENPH)

Tech has been trending downwards for the past 2 months apart from this relief rally celebrating potential gridlock in the senate.

There is a high probability that tech will be dormant in the short-term offering me a great opening to focus on alternative industries adjacent to tech that is also forward-looking.

Despite the global pandemic destroying large segments of the U.S. economy, the solar sector has been a revelation.

This is not much of a surprise for long-time solar industry nerds since a similar decoupling occurred in 2009 when many economics were hard hit by the Financial Crisis of 2008.

Under normal seasonality, the solar industry typically strengthens each quarter with the first quarter being the weakest boding well for the last 2 months of 2020

Enphase Energy, Inc. (ENPH) is the company I would like to fill you in on today and they design, develop, manufacture, and sell home energy solutions for the solar photovoltaic industry in the United States.

Looking forward, Enphase expects third quarter revenues to range between $160 to $175 million.

One of Enphase's critical competitive advantages is that the company operates more as a technology company than a commodity manufacturer.

While other companies do produce its main power inverter product, Enphase has market dominance in the micro-inverter segment.

For residential solar applications, micro-inverters do offer an advantageous alternative. Enphase's shipment growth over the past couple of years is the empirical evidence.

Even more salient, the company avoids ruinous capital expenditures by deploying contract manufacturing similar to peers with proprietary technology.

By leveraging these variables, Enphase has accelerated its high gross margins above 30%.

The company's lower margins last year were in part due to higher expedited shipping costs to satisfy demand but has solved that bottleneck and boosted gross margins to over 40% this year.

Enphase's stable high gross margin is the x-factor.

Most solar module producers have high fixed costs which deteriorate margins and drag down utilization rates.

As a result, not only do shipment gyrate between industry cycles but also gross margin. While Enphase is also exposed to industry fiscal cliffs, high gross margins should be highly constructive even in down years.

During up cycles, Enphase's high gross margins and lower operating structure give it abnormally advantageous earnings leverage.

Enphase's earnings leverage will be even more dramatic once revenue growth reaccelerates after the pandemic filters through the U.S. economy.

Up until now, Enphase has been pigeonholed as an inverter company within the solar industry.

The company did offer a battery storage option, but it was not an overwhelming segment of total revenues.

This may change moving forward after the company's next generation Encharge storage option released lately has shown glimpses of stardom among its competition.

As the election grinds down to a bitter finish, Presidential candidate Biden has already announced a $2 trillion climate plan which obviously would include expanding solar installations and be on the table if Biden eventually claims victory.

While a Democratic blue wave could have opened up an opportunity for sweeping change for US solar companies such as Enphase, flipping the US Senate to Democratic control is not a prerequisite for the solar industry to be successful.

It’s already trending in that direction as a mega growth industry like technology.

Also, the Democrats will try to crowbar in any climate-related infrastructure spending with any potential stimulus bill which could add more dollars behind the solar industry.

If annual residential solar installations double with a slightly higher per home average, about one million homes would be converted to solar annually.

With over 139 million homes in the US, only a small fraction would be converted to produce solar electricity over the next decade or two, even if the US residential solar market doubled.

The main takeaway is that the solar market in the US still has a huge upside under the right policies.

Enphase has a current micro-inverter capacity of 10 million units annually and based on its per-unit assumption of 325 watts, can supply 3.25 GW annually.

Based on comments in the company's second quarter earnings conference call, capacity could potentially be raised to 16 million annually with the expansion of its Mexico-based facility and a new India-based contract manufacturer.

Given the lead time required to ramp, actual shipment capacity next year may only be equivalent to 4 GW. If the company's geographic mix remains steady with last year's 83.9% US exposure, about 3.36 GW would be allocated to the US market. This would represent about 68.6% of the total US residential and commercial market during 2019.

Should the US solar market double due to beneficial policies, Enphase's potential market share will rise above 34%.

This would represent about a 10% increase in US market share from Q4 2019.

Ultimately, Enphase's high margins and fixed cost structure should not be underestimated especially under a systemic industry shift such as a Biden-led US economy laser-focused on green infrastructure.

Enphase is one of a few cost-effective US solar companies with attractive products that could get a boost from favorable governmental policies.

Expanded US market share due to favorable policies could push annual earnings well above any expected scenario.

The secret recipe of high gross margin and low-cost structure make Enphase incredibly leveraged to top-line growth.

Lately, a new storage revenue stream and continued shipment growth in a rapidly expanding solar market should result in overperforming earnings growth.

New storage products will meaningfully add to earnings next year without diluting gross margin and Enphase's high US exposure could benefit under a Democratic administration more biased to renewable energy.

Enphase is an unequivocal buy and hold stock and it’s no surprise that shares are up 400% in 2020 at the time of the writing.