Mad Hedge Technology Letter

January 29, 2024

Fiat Lux

Featured Trade:

(THE DATA CENTER STOCK READERS SHOULD LOOK AT)

(EQIX)

Mad Hedge Technology Letter

January 29, 2024

Fiat Lux

Featured Trade:

(THE DATA CENTER STOCK READERS SHOULD LOOK AT)

(EQIX)

Equinix (EQIX) is a tech company from Redwood City, California that specializes in building data centers.

That corner of technology is definitely where the growth is.

Everybody and anybody has heard a few things about this ongoing AI boom and remembers this secular trend hinges on the explosion of data and its incredible volume of it.

The processing of data requires data centers much like the processing of driver's licenses requires the Department of Motor Vehicles (DMV).

It’s not a surprise that the intense demand for data has meant a monumental need to supply new data centers and EQIX exists to deliver that new supply.

EQIX has performed admirably recently with solid revenue growth, a strong forward pipeline, and continued optimism about a differentiated ability to deliver compelling value to shareholders.

In the last quarter, they consummated 4,200 deals across more than 3,100 customers, including record numbers from high-value targeted customers.

EQIX was also able to upsell these companies on data center services, and digital services offerings, all coming together to address the evolving demands.

On the AI front, EQIX continues to cultivate and win significant opportunities across its existing customer base and with AI-specific prospects.

A recent Gartner poll found that 55% of organizations are in pilot or production mode with generative AI.

This is manifesting in accelerated interest from both enterprise customers and from emerging service providers looking to service this demand.

I am witnessing strong similarities between the evolving AI demand and the multi-tiered architectures that have characterized cloud build-out for the past eight years.

I think EQIX is perfectly positioned to capture high-value opportunities across the AI value chain along various key vectors.

First, in the retail business, EQIX will aggressively pursue magnetic AI service provider deployments to support on-ramps and smaller-scale training needs.

EQIX is well positioned here with nearly 40% market share of the on-ramps to the major cloud service providers, key players in the AI ecosystem.

Second, EQIX will meaningfully augment its advanced portfolio of specific data centers, including in North America to pursue strategic large-scale AI training deployments with the top hyperscalers and other key AI ecosystem players, including the potential to serve highly targeted enterprise demand.

I expect a build-out of data centers in retail campuses like the newly announced Silicon Valley 12x asset while other builds will be larger-scale campuses in locations with access to significant power capacity.

I also anticipate a dramatic acceleration in workloads and see Equinix as well positioned to deliver performance and economic benefits derived from network density and cloud adjacency.

While still early, I am seeing broad-based demand for private AI from digital leaders with specific wins in the transportation, education, public sector, and healthcare verticals, including Harrison.ai, a clinician-led healthcare artificial intelligence company that is dedicated to addressing the inequality and capacity limitations in the US healthcare system, by developing AI-powered tools in radiology and pathology.

Recurring revenues from customers deployed in more than one region stepped up 1% quarter over quarter to 77% as customers continued to move to more distributed architectures.

The brilliance of EQIX is that revenue is not a one-off event and companies will return with new data center needs.

If a company is not incorporating the processing of additional data, it most likely means they are not growing revenue.

This gives EQIX the chance to partner with high-quality companies that are at the heart of the digital transformation.

EQIX’s stock speaks volumes about where the company is as the stock has doubled in the past 5 years. They also deliver a 2.10% dividend to shareholders. I believe readers need to buy big dips and hold long-term in EQIX.

Mad Hedge Technology Letter

September 15, 2021

Fiat Lux

Featured Trade:

(TRY THIS RELIABLE DATA CENTER STOCK)

(EQIX)

One of the seismic outcomes from the current rollout of 5G is the plethora of generated data and data storage that will be needed from it.

In the land of tech stocks — more data means more money.

If one fashions themselves as a cloud purist and wants to bet the ranch on data being the new oil (and one would be daft not to realize it is) then look no further than Equinix (EQIX).

This is a tech firm that connects the world's leading businesses to their customers, employees, and partners inside the most interconnected data centers.

We are really talking about the backbone of the internet.

This is what the company represents and without this spine, the internet would be way more primitive and not as robust.

On this global platform for digital business, companies fuse together worldwide on five continents to reach everywhere, interconnect everyone and integrate everything they need to reap a digital windfall.

And whether we like it or not, the future will be more interconnected than ever because of the explosion of data and the 5G that harnesses the data.

This is precisely why the data will motivate businesses to extend their reach across the globe and expand their addressable audience.

It’s not me just talking up these bunch of overachievers; the numbers back me up fully.

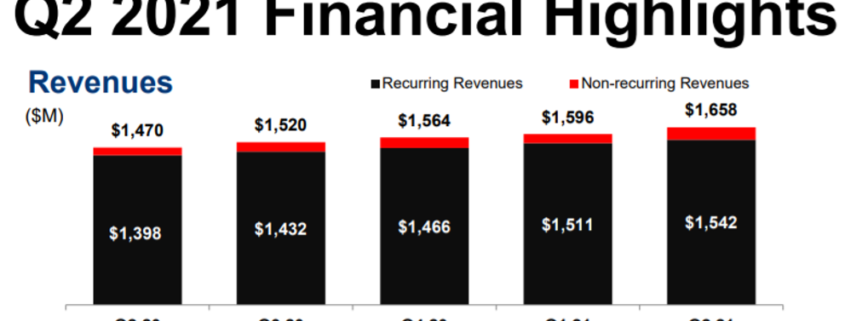

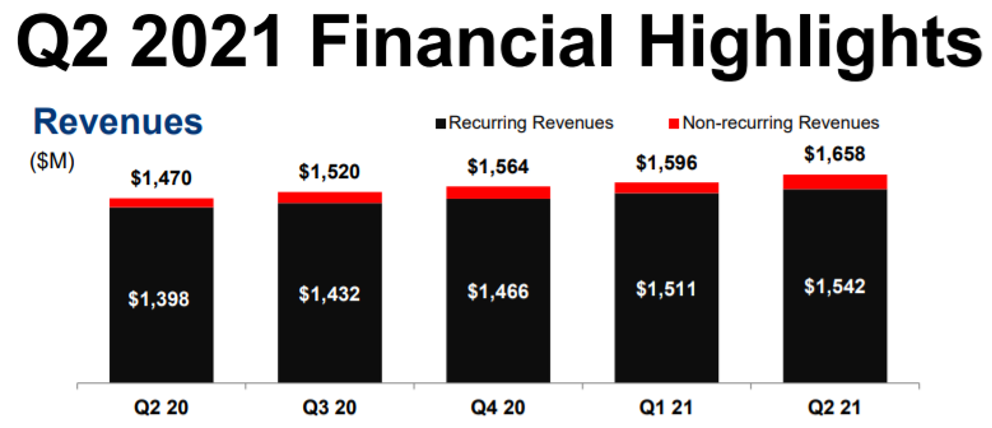

This past quarter Q2 revenues were $1.658 billion, up 8% over the same quarter last year due to strong business performance across EQIXs platform, led by the Americas region.

And as expected, nonrecurring revenues increased quarter-over-quarter to 7% of revenues due to a meaningful step-up in joint venture fees in Asia and Europe and custom installation work across all three regions.

As we must grapple with, nonrecurring revenues are inherently lumpy and therefore, as a result, EQIX expects Q3 nonrecurring revenues to decrease by $8 million compared to Q2. Cloud and IT verticals also captured strong bookings led by SaaS as the cloud diversifies towards a hybrid multi-cloud architecture.

High single digits might not look so glossy at first, but this is not a $1 billion per year in revenue company.

It’s probably one of the most stable businesses around since, unlike software, they can go out of fashion quite quickly if the next version bombs, yet storage space is more about economies of scale.

Other won deals lately include a leading SaaS provider expanding to support growth in new markets and with the Federal Government as well as an AI-powered commerce platform upgrading to enhance user experience support a rapidly growing customer base.

As digital transformation accelerates, the enterprise vertical continues to be Equinix’s sweet spot led by healthcare, legal, and travel sub-segments this quarter and the main catalysts to why I keep recommending readers this data storage company.

Other expansions this quarter included Zoom, a leading video communications platform, expanding coverage and scale to support market demand, and a cloud-delivered enterprise network security provider deploying infrastructure to support offerings in new locations.

EQIX’s enterprise vertical achieved record bookings, with broad global strength punctuated by an exceptionally strong quarter in the Americas across several subsegments, including healthcare, consumer services, business and professional services, and retail. New wins and expansions included Red Bull, a major sports energy drink manufacturer, deploying infrastructure across all three regions to take advantage of EQIX's cloud ecosystem.

EQIX can boast 65 consecutive quarters of increasing revenues, which eclipses every other company in the S&P 500, and it anticipates 8%-10% in annual revenue growth through 2022.

But now they are rolling out upgraded 2021 guidance by $15 million, forecasting to grow 10% to 12% year over year.

This represents a company that cuts across every nook and cranny of the tech sector by taking advantage of the unifying demand and storage requirements of big data.

This company will only become more vital once 5G goes blooms and being the global wizards of the data center will mean the stock goes higher in the long-term.

The momentum behind digital transformation is as robust as ever and shows no signs of letting up.

As a world digital infrastructure company, Equinix plays a unique role in this evolving story and is positioned to be both a catalyst and a key beneficiary as they partner with customers to unlock the enormous promise of digital.

They will continue to scale, doubling down on the strength of their core business, investing to further scale a go-to-market machine to win new customers, putting capital to work to add capacity in existing markets, and executing on targeted operational improvements to standardize, simplify and automate, driving expanded operating margins and providing a better experience for customers and partners.

Delivering advanced features to sustain momentum in EQIXs market-leading interconnection franchise and driving adoption of digital infrastructure services to deepen our relevance to customers is still paramount for the firms’ prospects.

I recommended this stock at $491 and now it sits nicely at $840.

My premise of buying and holding long term still holds true and any dip should be bought to take advantage of dollar-cost averaging.

I expect Equinix to be a slow and steady climb because let’s face it, it’s not a 40% per year growth story, but the stock does the job and rarely declines while providing a stable dividend.

Mad Hedge Technology Letter

June 3, 2020

Fiat Lux

Featured Trade:

(ABOUT YOUR RIOT-PROOF PORTFOLIO),

(COMPQ), (WMT), (APPL), (AMZN), (TGT), (JWN), (EQIX), (GOOGL), (MSFT)

Social unrest will have NO material effect on tech shares moving forward.

Some investors expected the Nasdaq (COMPQ) index to roll over big time, throttled by a national insurrection. Anti-police-violence protests, some becoming riots, have broken out in more than 60 cities.

However, it appears to be another false negative for the Nasdaq as it motors upwards acting on the momentum of outperformance during the coronavirus.

One thing that the coronavirus pandemic, as well as protests, have taught investors is the unwavering faith in technology’s strength will continue powering the overall market rebound.

Any social unrest will not stop tech shares because they simply don’t subtract from their revenue models.

This will perpetuate into the rest of 2020 and beyond.

Much of the public reaction from big tech has been paying some form of lip service about the national situation being untenable followed up with a small donation.

Apple (AAPL) says it's making donations to various groups including the Equal Justice Initiative, a non-profit organization based in Montgomery, Alabama that provides legal representation to marginalized communities.

To read more about big tech’s donations, click here.

Aside from some PR formalities, it will be business as usual after things settle down.

Apple might suffer some slight inconveniences of having some stores looted, but that doesn’t mean consumers can’t buy products online.

Tech companies simply contort to fit the new paradigm and that is what they are best at doing.

Apple has charged hard into the digital service as a subscription world that has served Amazon, Apple, Google (GOOGL), and Microsoft (MSFT) so well.

To read more about the robust performance of software stocks, please click here.

Many of these tech companies don’t need a physical presence to drive forward earnings, revenue models, and widen their competitive advantages.

That’s the beauty of it and their brands are so entrenched that it doesn’t matter what happens in the outside world at this point.

It’s true that a few tech companies might have to scale back or modify operations until the storm subsides but not at a great scale that will worry investors.

Amazon is reducing deliveries and changing delivery routes in some areas affected by the protests.

Big tech dodged a bullet with the majority of the financial burden falling on the shoulders of big-box retailers like Walmart (WMT) and Target (TGT) and city center-located businesses.

Walmart closed hundreds of stores one hour early on Sunday, but most are slated to reopen. Nordstrom (JWN) temporarily closed all its stores on Sunday.

Amazon (AMZN)-owned Whole Foods are often located in neighborhoods that are perceived likely to escape the bulk of the turmoil.

The events of the last few days will have significant side effects on the normalcy of society or the new normal of it.

Combined with the pandemic, consumers will opt for more spacious housing options in less concentrated areas of the U.S.

The social unrest once again delivers the goodies into the hands of e-commerce as people will be less inclined to leave their house to consume.

A stock that really sticks out during all of this is the leader in interconnected data centers Equinix (EQIX) because of the explosion of data being consumed from the stay-at-home revolution.

Sadly, the price of tech share does not account for life quality which is part of the reason we see stocks lurching higher.

By the time all the different crises, including coronavirus and protests, are snuffed out, we could be in a world where the only strong companies left are technology, "big tech".

They have an insurmountable lead at this point with guns still blazing.

When you add the windfall of trillions in cash the Fed has pumped out and unwittingly diverted into tech shares recently, it is hard to envision ANY scenario in which the Nasdaq will be down a year from now.

I am bullish on the Nasdaq index and even more bullish on big tech.

Even the supposed “rotation” to value has only meant that tech shares haven’t gone down.

A dip now in tech shares means shares dip for two hours before resurging.

Why would anyone want to sell the best and highest growth industry in the public markets with unlimited revenue-generating potential?

Mad Hedge Technology Letter

May 23, 2019

Fiat Lux

Featured Trade:

(ANOTHER 5G PLAY TO LOOK AT)

(EQIX), (CSCO), (GOOGL), (MSFT), (ORCL)

One of the seismic outcomes from the upcoming rollout of 5G is the plethora of generated data and data storage that will be needed from it.

If you are a cloud purist and want to bet the ranch on data being the new oil, then look no further than Equinix (EQIX) who connects the world's leading businesses to their customers, employees, and partners inside the most-interconnected data centers.

On this global platform for digital business, companies come together worldwide on five continents to reach everywhere, interconnect everyone and integrate everything they need to reap a digital windfall.

And whether we like it or not, the future will be more interconnected than ever because of the explosion of data and the 5G that harnesses the data will allow business to reach across the globe and expand their addressable audience.

The stock has reacted like you would have thought with a victorious swing up after a tumultuous last winter.

The cherry on top was the positive earnings report earlier this month.

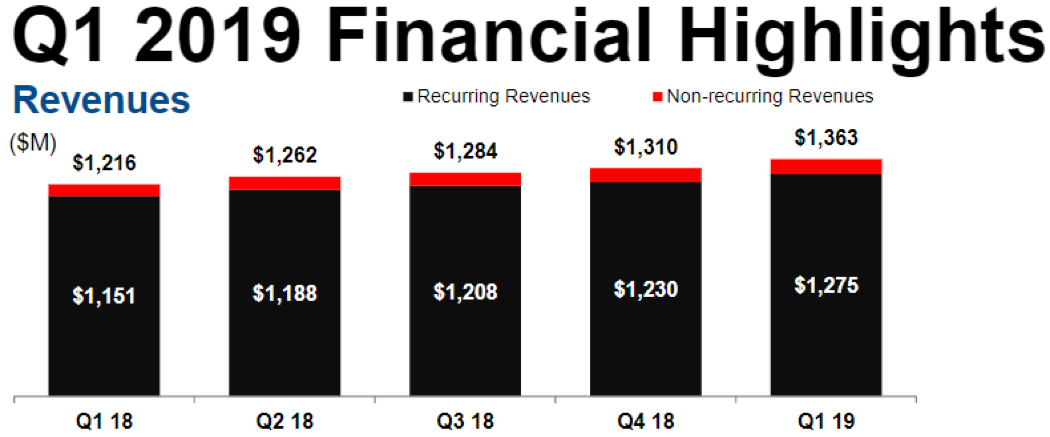

The highlights were impressive and plentiful with revenues for Q1 coming in at $1.36 billion, up 11% year-over-year meaningfully ahead of management expectations.

Equinix’s market-leading interconnection franchise is performing well, with revenues continuing to outpace colocation, growing 12% year-over-year, as the cloud ecosystem continues to scale.

Penetration in “lighthouse accounts” or early adopters increased nearly 50% from the Fortune 500 and 35% from the Global 2,000 demonstrating the expanding opportunity as Equinix unearths more value from the enterprise industry.

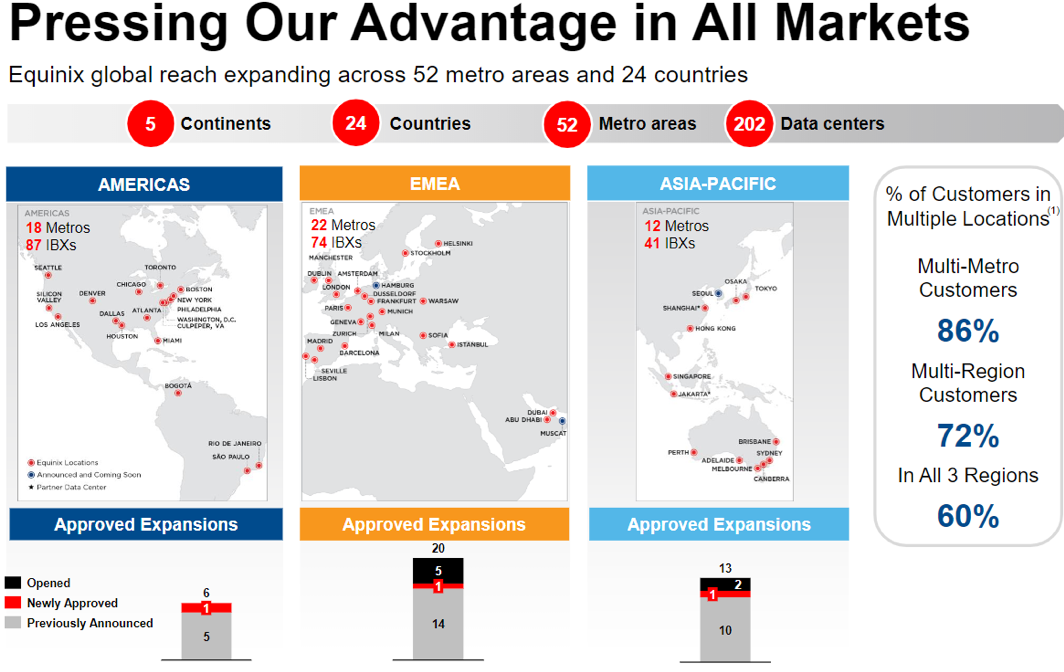

Equinix is now the market leader in 16 out of the 24 countries in which they operate, and they’re expanding its platform with 32 projects announced across 27 markets, with Q1 openings in Frankfurt, Hong Kong, London, Paris, and Shanghai.

Equinix’s network vertical experienced solid bookings led by strength in Access Point (AP), which is a hardware device or a computer's software that acts as a communication hub for users of a wireless device to connect to a wired LAN.

APs are important for providing heightened wireless security and for extending the physical range of service a wireless user has access to and driven by major telecommunication companies, mobile operators, and NSP resale.

Expansions this quarter include Hutchison, a leading British mobile network operator upgrading their infrastructure to support 5G and cloud services, as well as a leading Asian communication provider, migrating subsea cable notes and connecting to ECX Fabric for low latency.

Equinix’s financial services vertical experienced record bookings led by Europe, the Middle East and Africa (EMEA) and rapid growth in insurance and banking.

New contracts include a fortune 500 Global insurer transforming IT delivery with a cloud-first strategy, a top three auto insurer transforming network topology while securely connecting to multiple clouds, and one of the largest global payment and technology companies optimizing their corporate and commercial networks.

Demand in the social media sub-segment as providers are hellbent on improving user experience and expanding the scope of their business models.

Equinix’s gaming and e-commerce sub-segment grew the fastest year-over-year led by customers, including Tencent, neighbor, and roadblocks.

Cloud and IT verticals also captured strong bookings led by SaaS as the cloud diversifies towards a hybrid multi-cloud architecture.

A robust pipeline can be rejoiced around as cloud service providers continue to push to new frontiers and roll out additional services.

Developments include a leading SaaS provider expanding to support growth in new markets and with the Federal Government as well as an AI-powered commerce platform upgrading to enhance user experience support a rapidly growing customer base.

As digital transformation accelerates, the enterprise vertical continues to be Equinix’s sweet spot led by healthcare, legal and travel sub-segments this quarter and main catalysts to why I keep recommending reader into enterprise software companies.

The chips are being counted with new contracts from Air Canada, a top five North American airline deploying a hybrid multi-cloud strategy, Space X deploying infrastructure to interconnect dense network and partner ecosystems and one of the big four audit firms regenerating networks and interconnecting to multi-cloud to improve the user experience for both employees and clients.

Channel bookings also registered continued strength delivering over 20% of bookings with accelerated growth rates selling to Equinix’s key cloud players and technology alliance partners, including Cisco (CSCO), Google (GOOGL), Microsoft (MSFT), and Oracle (ORCL).

New channel wins this quarter includes a win with Anixter for a leading French transportation and freight logistics company deploying mobility platform, as well as a win with AT&T for a top-five U.S. Bank accessing our network and cloud provider.

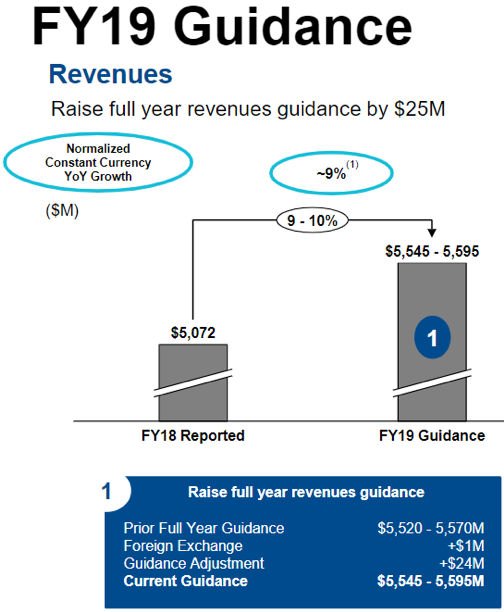

Management signaled to investors they are expecting a great year with full-year revenue guidance of $5.6B, a 9-10% year-over-year boost and a $25M revision from the previous guidance.

Equinix can boast 65 consecutive quarters of increasing revenues, which eclipses every other company in the S&P 500, and it anticipates 8%-10% in annual revenue growth through 2022.

This is an incredibly stable yet growing business and the 2.17% dividend yield, although not the highest, is another sign of a healthy balance sheet for a profitable company.

If you had any concerns about this stock, then just take a look at its 3-year EPS growth rate of 73% which should tell you that the massive operational scale of Equinix is starting to allow efficiencies to take hold dropping revenue straight down to the bottom line.

If you are searching for a company that cuts across every nook and cranny of the tech sector by taking advantage of the unifying demand and storage requirements of big data, then this is the perfect company for you.

This company will only become more vital once 5G goes online and being the global wizards of the data center will mean the stock goes higher in the long-term.