Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

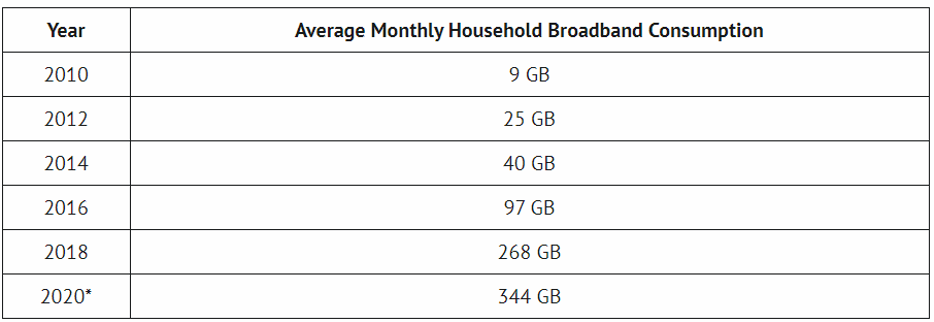

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Global Market Comments

December 14, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ASSET SHORTAGE),

(INDU), (PFE), (MRNA), (PTON), (DOCU), (ETSY), (CAT), (JPM), (BABA), (TSLA), (TLT), (ABNB), (DIS)

Markets are wonderful arbiters of the laws of supply and demand.

When there is a shortage of a particular security, Wall Street has a magical ability to manufacture more by running the printing presses to meet supply, or in the modern incarnation, open the spreadsheets.

Except for this time.

The amount of new cash created by global quantitative easing and the prolific saving habits of locked up Americans are creating more demand than even this efficient highly process can accommodate.

Which means that prices can only go up.

How long and how far is anyone’s guess. My target for the Dow Average is 120,000 in ten years, but even I don’t expect that to take place in a straight line. So, we are all sitting on our hands waiting for the next pullback to buy into, which may….or may not ever happen.

A lot of Dotcom Bubble memories are rising up from the dead. Analysts in 1999 made outlandish forecasts of stocks rising 50% in a year, which then took place in four days. That happened to Tesla (TSLA) last month and Airbnb (ABNB) last week.

In the meantime, the smartest traders, call them the oldest traders, are taking profits on the best years of their careers.

Of course, the short-term direction of the market will be determined by the January 5 Georgia Senate election, where the polls are in a dead heat. The last time this happened, during the presidential election, the Democrats won by a microscopic 15,000 vote margin.

If history repeats itself, the Biden administration will get an extra $6 trillion to play with to restore the shattered US economy. Think $2 trillion for infrastructure spending in all 50 states, $2 trillion for the rescue of bankrupt states and municipalities, $1 trillion for alternative energy and EV subsidies, and another $1 trillion in odds and ends. Needless to say, much of this will end up in the stock market.

I am getting a lot of questions these days regarding what will end this once-in-a-generation runaway bull market. The pandemic created this bull market by accelerating technology, business evolution, and corporate profitability by ten years. I bet a year ago, you weren’t spending your day on Zoom meetings, as I was.

The great irony is that the Pfizer (PFE) and Moderna (MRNA) vaccines may not only kill Covid-19 but the bull market as well. That’s because money will then come out of stocks and go back to the real economy.

That makes pandemic darlings like Peloton (PTON), DocuSign (DOCU), and Etsy (ETSY) especially risky. But then 6% growing GDPs were never what stock market crashes were made of, so any declines will be modest.

As for my own positions, I have a rare 100% long portfolio, mostly Tesla, but also the (TLT), (CAT), (JPM), and (BABA), 80% of which expires with the option expiration on Friday, December 18.

After that, I’ll take it easy with 10% short (TLT) and 10% long (TSLA) and wait for the market, or Georgians to tell me what to do.

A flood of money is to hit the stock market, says hedge fund legend Ray Dalio. The US is facing a perfect storm in favor of all risk assets. There is no reason why price earnings multiples for American stocks can’t reach 50X, double the current 25X. Buy what the central banks are buying. The funny thing is that I agree with Ray on everything. Buy risk on dips.

Stocks will keep soaring into 2021, says JP Morgan strategist Marko Kolanovik. The more risk the better. The Fed will keep interest rates low for at least another year, and ultra-low rates will force big institutions out of bonds and into stocks. Volatility (VIX) will decline. It all sounds like a great long stock/short bond trade to me. Hmmmmm.

Tesla completed a $5 Billion share issue, after a move to $650, up $142 from my November Mad Hedge BUY recommendation. The stock seems hell-bent on testing the Goldman Sachs $780 price recommendation before the December 18 S&P 500 entry. Elon Musk’s creation is now worth a staggering $608 billion. It’s the best recommendation in the 13-year history of the Mad Hedge Fund Trader.

San Francisco rents dive 35%, as tech workers flee to the suburbs. A lot of remote work is now permanent. Studio apartments are now a mere $2,100, and a one-bedroom can be had for $2,716. For a two-bedroom if you have to ask, you don’t need to know. Shocking!

Sales of million-dollar homes are soaring, as ultra-low interest rates persist and people spend much more time at home. So, bigger for your pod is better. Mortgages over $766,000 are up 57% YOY.

Jamie Diamond says he wouldn’t touch bonds with a ten-foot pole, and nor would I. A 91-basis point yield just doesn’t do it for the chairman of JP Morgan Chase (JPM), one of my recurring longs. Stocks are a much better choice, even if there is a bubble in progress. Keep selling every rally in fixed income, especially the (TLT).

Weekly Jobless Claims soar to 853,000, up a massive 153,000 from the previous week. To see this happen during the Christmas hiring season is heartbreaking. With 200,000 a day falling to Covid-19, I’m surprised it's not higher, which means it will be. This is what peaks look like. Washington has totally given up.

An $800 billion payday for the bay area. That is the amount of wealth created by just two companies, Tesla (TSLA) and Airbnb (ABNB), since March. And the great majority of shareholders live in the San Francisco Bay Area, including its venture capital and pension funds. No wonder home prices in the suburbs are up 20% YOY. The great irony is that (ABNB) received a massive government bailout only in March. I hope they repay the loans early.

Is Cuba the next big play? A Biden détente could lead to the emerging market investment opportunity of the decade with the $43 million Herzfeld Caribbean Basin Fund (CUBA). It just had its best month in 11 years (like many of us). With Fidel Castro long dead, what’s the point in continuing a 60-year-old cold war. A big market for American products and services beckons, not to mention the tourism and cruise opportunities. But can Biden afford to lose the Florida Cuban vote in the next election?

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

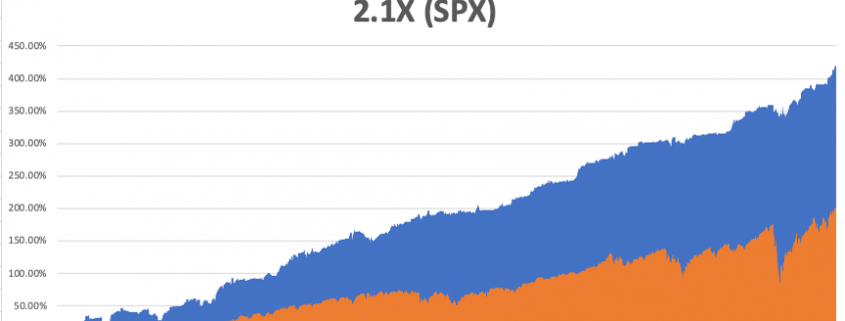

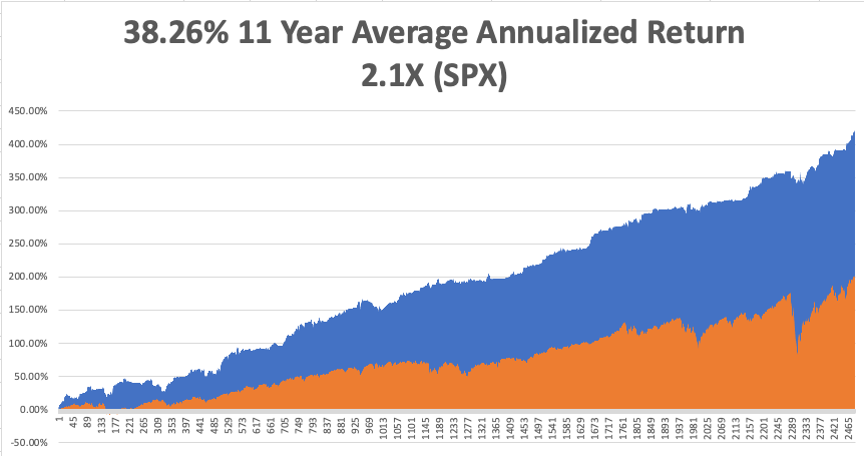

My Global Trading Dispatch catapulted to another new all-time high. December is up 8.55%, taking my 2020 year-to-date up to a new high of 64.99%.

That brings my eleven-year total return to 420.90% or more than double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.26%. My trailing one-year return exploded to 66.30%, the highest in the 13-year history of the Mad Hedge Fund Trader.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 16 million and deaths 300,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 14 at 12:00 PM EST, US Consumer Inflation Expectations for November are released.

On Tuesday, December 15 at 11:00 AM, the New York Empire State Manufacturing Index for December are published.

On Wednesday, December 16 at 8:00 AM, US Retail Sales for November are printed.

On Thursday, December 17 at 8:30 AM, the Weekly Jobless Claims are published. We also get November Housing Starts.

On Friday, December 18, at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I was stunned to learn that 84 million people are watching The Mandalorian, the latest Star Wars installment Disney (DIS) launched in its hugely successful streaming service a year ago.

It reminds me of when I first saw Star Wars in 1977. I was changing planes in Vancouver, Canada on the way to Tokyo and used a long layover to take a taxi to the nearest theater to catch a film I’d heard so much about.

I was amazed when I realized that the guy sitting in the next seat had memorized the entire script and was mouthing all the words. The only other time I have ever seen this happen was sitting on the benches at Shakespeare’s Globe Theater in London. At least then, they were reciting Romeo and Juliet.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

June 29, 2020

Fiat Lux

Featured Trade:

(TIME TO DO SOME SHOPPING AT ETSY)

(ETSY), (AMZN)

The ecommerce story just keeps getting brighter and Etsy (ETSY) is one of those companies that are at the leading edge of the movement.

Out of the same vein of Amazon (AMZN), I am increasingly optimistic about Etsy’s long-term prospects aided by monstrous secular tailwinds.

Heralded for its vintage and handmade goods, I have upped my targets to $150 which is a no brainer for a company that grows revenue more than 30% and one I believe will grow 80% in 2021.

The growing pie of ecommerce tells just part of the story.

In the throes of a hysterical once-in-a-century multi-faceted crisis, consumers have gravitated towards trusted and reliable retailers.

As a result, we can expect the top 10 ecommerce retail businesses to expand at above-average rates of 21.8% in 2020.

Amazon will gain even more US ecommerce market share this year, while Walmart's accelerating ecommerce success will put it directly behind Amazon for the first time.

Even though Etsy is no Walmart or Amazon, they are a known commodity with a growing number of repeat and loyal buyers which goes a long way in today’s ecommerce climate.

They have effectively elbowed their way clearing out a niche in personalized handicrafts that cannot be copied on a large scale.

In the U.S. alone, ecommerce will account for 19% of retail by 2024, up from 11% of domestic sales last year, totaling some $1.1 trillion.

Simply put, the bronco is out of the barn, and many consumers are not inclined to return to the physical store experience.

Ecommerce has also validated themselves as models that work as good as the in-store experience or better.

Before the sushi hit the fan in March, most ecommerce outfits were projecting unspectacular ecommerce growth of 2-3% to $6 trillion in total US retail sales by the end of 2020.

After updating models, we now expect there's to be a 10.5% decline in total retail spend, with a 14.0% drop in brick-and-mortar.

Ecommerce has performed admirably and is poised to grow 18% following a 14.9% gain in 2019, further signaling the pivot towards digital.

Consumers have downloaded Etsy’s app at rapid rates further hinting that this boost in revenue has staying power.

Shares of Etsy have more than tripled from a March low and are trading at record levels. The stock is up more than 130% this year easily outperforming the broader Nasdaq index.

Etsy's quarterly revenue grew 32% year over year to $1.4 billion and when The Centers for Disease Control recommended the use of face masks to thwart the spread of the coronavirus, masks flew off the digital shelves.

CEO Josh Silverman aptly described the situation in Etsy's Q1 earnings call saying, “It was like waking up and discovering that it was Cyber Monday.”

Even excluding face masks, April sales were still up 79% from April 2019. All told, the company expects upcoming Q2 results to show an 80% to 100% year-over-year gain for gross merchandise sales. And it anticipates revenue growth of 70% to 90%.

As masks become mandated by state governments because of record coronavirus cases, Etsy is the go-to platform for personalized masks.

It goes to show that a native digital strategy might be the best of the bunch in 2020 and as masks are mandated by state governments, Etsy will harvest the low-hanging fruit with its army of personalized mask sellers on its platform.

This will truly be a year Etsy will never forget tattooing them firmly in the digital realm as a legitimate ecommerce juggernaut.

Mad Hedge Technology Letter

December 4, 2019

Fiat Lux

Featured Trade:

(THE RUSH TO BUY ONLINE),

(AMZN), (WMT), (TGT), (W), (ETSY), (SHOP), (ADOBE)

There are several overarching seminal tech trends that I swear by.

The generational broad-based migration from analog to digital is a critical foundation that underpins the success of not only tech stocks as a unified sector, but the outperformance of the Mad Hedge Technology Letter.

You’ll be pleased to discover that 2019 is right on queue with digital sales exploding by the American consumer over the holiday shopping period and Americans ditching brick and mortar stores in droves.

Amazon (AMZN) broke records on Cyber Monday bragging that in terms of the number of items sold, it had its "single biggest shopping day."

Black Friday was a big success too selling “hundreds of millions" of products between Thanksgiving and Cyber Monday.

Consumers scooped up the toys, home, fashion and health, and personal care products on Amazon’s e-commerce platform.

Hot ticket items on Black Friday included Amazon's own Echo Dot and Fire TV Stick with Alexa Voice Remote, Play-Doh Sweet Shoppe Cookie Creations, Keurig K-Cafe Coffee Maker and LEGO City Ambulance Helicopter Kit.

Adobe (ADBE) Analytics estimates that the sales for the shopping bonanza easily eclipsed $29 billion, or 20% of total revenue for the full holiday season.

This is the aha moment when digital integration into shopping forced a paradigm shift to the business environment by capturing the focal point of American wallets.

Digital used to be the minority, but going forward, it will dictate the terms of engagement.

What does this mean in the bigger scope of things?

Mobile is the biggest winner of this brave new world.

Shopping apps gave consumers the platform to use their phones as a digital wallet.

Salesforce data discovered that Thanksgiving sales as a proportion of U.S. digital sales grew 17% and mobile sales rose 35% on Black Friday with 65% of total e-commerce executed through a mobile device.

“Black Friday broke mobile shopping records and even when shoppers went to stores, they were now buying nearly 41% more online before going to the store to pick up,” said Taylor Schreiner, principal analyst and head of Adobe Digital Insights.

Shopify (SHOP) did over $900 million in sales this year and 69% were from phones and only 31% from desktop computers.

Black Friday was "the biggest day ever for mobile," tracking $2.9 billion in sales from smartphones alone, or 39% of all e-commerce sales, a 21% increase year over year.

The data also showed that smaller e-commerce outfits had a harder time driving sales than large e-commerce platforms.

The network effect truly works both ways and the success of the biggest and best also correlated to a meaningful decline of physical shopping visit to stores of 6% on Black Friday.

According to The NPD Group's Holiday Purchase Intentions Survey, 20% of sales were picked up in the store. This click-and-collect business has been a huge winner for the likes of Walmart (WMT).

E-commerce leaders are having enormous success introducing omnichannel approaches to the selling channels.

The average order value on Black Friday rose 5.9% year over year to $168, a new record, in part because shoppers have become more comfortable buying expensive items online because the sales are even juicier.

Unfortunately, the rise in volume has meant lower margins.

Discounts averaged between 37% to 47% and home and consumer electronics products were popular.

With all the rumblings of tariff trauma and an approaching recession, the American consumer displayed robustness that largely met the consensus of analysts.

The takeaway is that e-commerce is as healthy as ever and should prolong not only the strength in e-commerce companies but the overall American economy.

The winners are the behemoths of Amazon, Target (TGT), Shopify, and Walmart. Shares should receive a moderate tailwind through the New Year.

Avoid smaller niche players like Etsy (ETSY) and Wayfair (W).

Mad Hedge Technology Letter

October 16, 2019

Fiat Lux

Featured Trade:

(IS 3D PRINTING A WASTE OF SPACE?)

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

If you need a new investment theme – here’s one.

3D printing.

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

Believe me, I’ve been there and done that.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology like e-commerce company Etsy (ETSY) who focuses on personalized handcrafts.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was tedious.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can be Super Bowl quarterback Tom Brady.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is heaps better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand, but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are percolating together at the perfect time.

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in its infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in perfect in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus - 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could potentially consist up to 25% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins close to 60%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a multi-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 is applying a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE has already started mass production of the 3D printed brackets at its Auburn, Alabama facility.

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

As it stands, Stratasys is the industry leader in this field and if you believe in this long term then this stock would be for you.

It’s nonetheless still a speculative punt but a compelling pocket of the tech industry.