Mad Hedge Technology Letter

July 26, 2019

Fiat Lux

Featured Trade:

(WHY 3D PRINTING WILL BOOST THE AIRPLANE INDUSTRY),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

Mad Hedge Technology Letter

July 26, 2019

Fiat Lux

Featured Trade:

(WHY 3D PRINTING WILL BOOST THE AIRPLANE INDUSTRY),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

If you need a new investment idea – here’s one.

3D printing.

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

The teething pains echo bitcoin which was the fad of 2017, on the contrary, this technology it is built on is rock solid, yet the path to sustainability is littered with corpses.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology.

Etsy (ETSY) e-commerce participants gravitate towards 3D printing because it gets firms from paper to the real world in a fraction of the time.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was time-draining and aggravating.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can wake up one day in their pajamas and convince themselves they will be the next starting quarterback to lead an NFL team to the Super Bowl.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is a lot better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand like Netflix (NFLX), but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are brewing together at the perfect time.

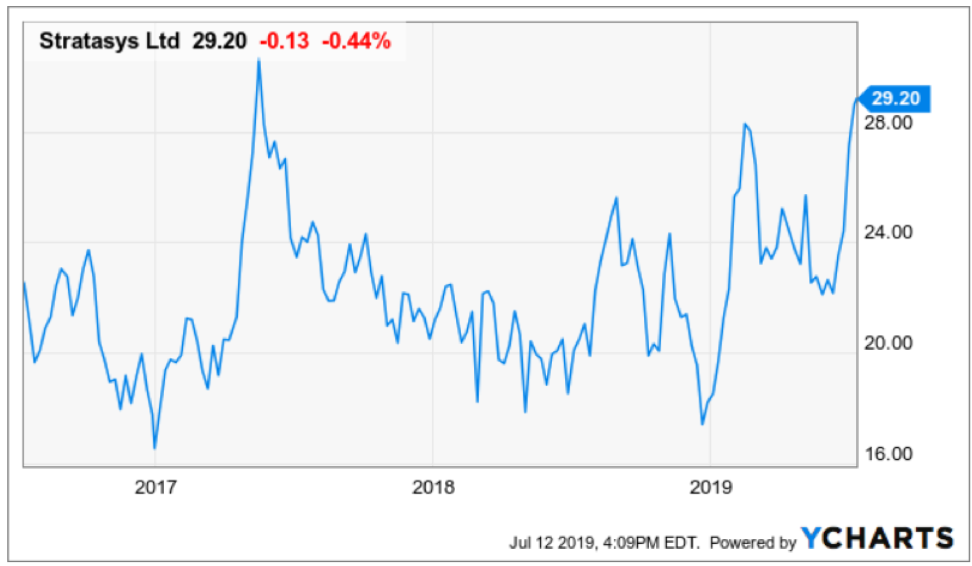

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus, 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could consist up to 20% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins to up to 50%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a five-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

Only last November, GE announced that GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 will apply a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE is preparing to begin imminent mass production of the 3D printed brackets at its Auburn, Alabama facility.

Eric Gatlin, general manager of GE Aviation’s additive integrated product team gushed that “It’s the first project we took from design to production in less than ten months.”

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

Further emphasis on cornering the North America aerospace market could cement this stock as a no-brainer buy of 2019 as the (FAA) embraces more of the technology opening up the addressable market for the active participants.

As it stands, Stratasys is the industry leader in this field, and placing best of breed tech companies into your portfolio will put you in better position to weather the squalls of the capricious tech sector.

The company is still relatively unknown even though it has been around for ages.

Stratasys is a company to put on your radar and remember this space as the 3D printing market blossoms.

It’s nonetheless still a speculative punt but a compelling part of the tech industry.

Mad Hedge Technology Letter

March 4, 2019

Fiat Lux

Featured Trade:

(RIDING THE EBAY BOOM),

(EBAY), (ETSY), (W)

Investors following the eBay (EBAY) saga should be cheering from the sidelines as the master plan from Elliot Management and Starboard are pressuring eBay’s management into the radical changes the investors initially called out for.

Rewarding the vulture funds with two board seats along with spearheading a comprehensive review of the business model appears more probable than not.

The forced changes have imminent repercussions to the stock price as the breaking up of the company into individual pieces is seen as coaxing out more embedded value while separating out the main e-commerce platform for a long-awaited fix.

These are two highly bullish signals.

Elliot’s reasons for altering eBay’s business model were essentially blamed on two issues - shoddy management and the commingling of growth assets with its inferior e-commerce platform within the eBay umbrella hindering value appreciation.

Even though prospects look bright on this fix, Elliot doesn’t always get its way.

Four years ago, Elliot was the primary investor in Samsung's construction division and rebuffed efforts from Jay Y. Lee, the South Korean business elite and the vice chairman of Samsung Group serving as de facto head, to have another division of Samsung purchase the construction arm for $8 billion.

In 2017, Lee was convicted of bribery and imprisoned and sentenced to three years, Elliot sold their Samsung construction shares after the tide went against them and could not prevent the eventual purchase.

Lee was later set free in 2018 demonstrating the unfettered power of the ruling Korean families and Elliot was up against it in someone else’s backyard.

Even with that setback, Elliot has been ultra-successful abroad, examples are plentiful such as in May 2018, Elliott Management seized control of Telecom Italia controlling two-thirds of Telecom Italia's board seats.

This vulture fund has been specialists at pinpointing ill-ran operations and squeezing the fat off the edges to later sell off assets for a profit.

These tactics have usually centered around cost-cutting, financial engineering, or draining the upper management swamp if need be.

Personally, eBay has the foundations to be competitive with the top e-commerce companies and they need an activist investor to turn this ship around.

In this way, the turnaround will occur much quicker than an organic method because Elliot will apply pressure on all the cancerous parts of the model and stamp them out as fast as possible.

Elliot now has a golden path to two board seats and spinning off StubHub, its uber-growth online events tickets selling platform, will guarantee Elliot and Starboard walk away from this transaction with a heavy profit.

StubHub was bought on the cheap in 2007 when online assets were trading cheaply for $310 million.

The firm contributes 11% to eBay’s top line.

The classified ads business is the other part of the high-growth online portfolio that could be sold for a profit. They operate mainly in Germany and the United Kingdom and comprise almost 10% of sales.

The plan after these premium assets are sold is to focus on mending its wounded e-commerce business.

The core business would need a flushing out of current management.

Bringing in some established hands to reroute the company’s course will boost the shares another 25%.

The phrase “more efficient use of resources” or a similar version of this meaning was used six times in Elliot Management’s letter to eBay Shareholders.

They cited in the letter that EBITDA margins have declined YOY for 12 straight quarters proving that revenue-boosting initiatives have failed spectacularly.

Elliot hopes a better run company will constitute in higher operating margins to the tune of “32% in 2021.”

In the next 3 years, Elliot wants to raise operating expenses by $250 million but reduce “wasteful spend” which they outlined as one of the main reasons hamstringing the company.

Missed opportunities is another major opportunity cost contributing to the underperformance of eBay.

eBay has been left out of the niche e-commerce areas where former eBay employees exploited this untapped source of growth.

The success of Wayfair (W), the furniture e-commerce platform, and Etsy (ETSY), the personalized crafts e-commerce platform, are two glaring examples of sales that should have been registered by eBay but gobbled up by two minnows.

In short, Elliot’s flawless execution and aggressive plan are ideally playing itself out how they wrote it up from the beginning.

It’s hard not to see eBay’s stock higher a year from now as long as Elliot and Starboard get their way.

The brilliant part of this whole turnaround is that eBay doesn’t have to become Amazon to reap share appreciation, they merely need to be not as bad as they were which at the first stage of rebooting the business is the lowest hanging fruit out there.

Once the company becomes mature and more successful, growth and beating relative expectations are harder to achieve.

I am bullish eBay - buy on the next pullback.

Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

I wrote to readers that I expected online commerce company Etsy to “smash all estimates” in my newsletter Online Commerce is Taking Over the World last holiday season, and that is exactly what they did as they just announced quarterly earnings.

To read that article, click here.

I saw the earnings beat a million miles away and I will duly take the credit for calling this one.

Shares of Etsy have skyrocketed since that newsletter when it was hovering at a cheap $48.

The massive earnings beat spawned a rip-roaring rally to over $71 - the highest level since the IPO in 2015.

Three catalysts serving as Etsy’s engine are sales growth, strength in their core business, and high margin expansion.

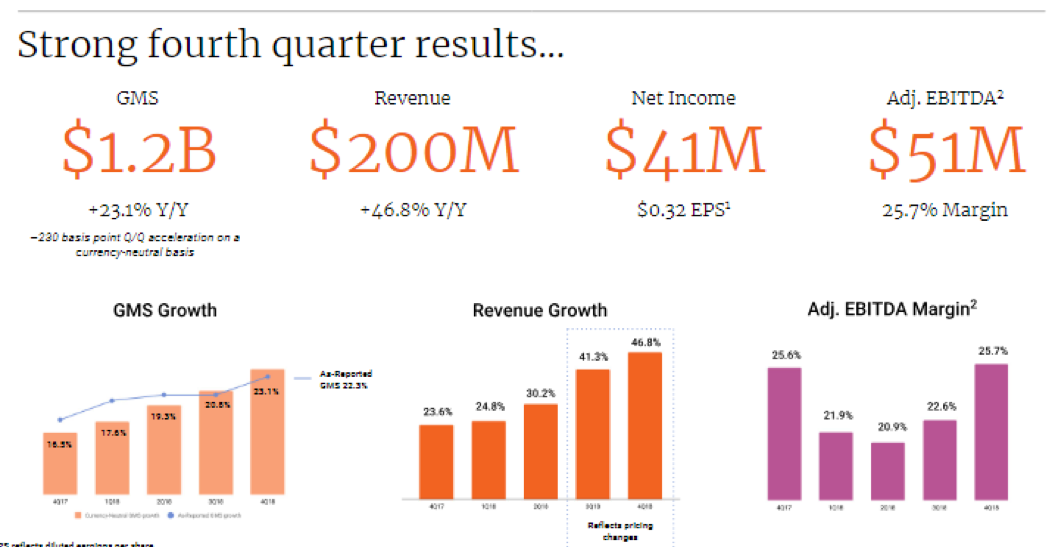

Sales growth was nothing short of breathtaking elevating 46.8% YOY – the number sprints by the 3-year sales growth rate of 27% signaling a firm reacceleration of the business.

The company has proven they can handily deal with the Amazon (AMZN) threat by focusing on a line-up of personalized crafts.

Some examples of products are stickers or coffee mugs that have personalized stylized prints.

This navigates around the Amazon business model because Amazon is biased towards high volume, more likely commoditized goods.

Clearly, the personalized aspect of the business model makes the business a totally different animal and they have flourished because of it.

Active sellers have grown by 10% while active buying accounts have risen by 20% speaking volumes to the broad-based popularity of the platform.

On a sequential basis, EPS grew 113% QOQ demonstrating its overall profitability.

Estimates called for the company to post EPS of 21 cents and the 32 cents were a firm nod to the management team who have been working wonders.

Margins were healthy posting a robust 25.7%.

The holiday season of 2018 was one to reminisce with Amazon, Target (TGT), and Walmart (WMT) setting online records.

Pivoting to digital isn’t just a fad or catchy marketing ploy, online businesses harvested the benefits of being an online business in full-effect during this past winter season.

Etsy’s management has been laser-like focusing on key initiatives such as developing the overall product experience for both sellers and buyers, enhancing customer support and infrastructure, and tested new marketing channels.

Context-specific search ranking, signals and nudges, personalized recommendations, and a host of other product launches were built using machine learning technology that aided towards the improved customer experience.

New incremental buyers were led to the site and returning customers were happy enough to buy on Etsy’s platform multiple times voting with their wallet.

The net effect of the deep customization of products results in unique inventory you locate anywhere else, differentiating itself from other e-commerce platforms that scale too wide to include this level of personalization.

Backing up my theory of a hot holiday season giving online retailers a sharp tailwind were impressive Cyber Monday numbers with Etsy totaling nearly $19,000 in Gross Merchandise Sales (GMS) per minute marking it the best single-day performance in the company’s history.

Logistics played a helping hand with 33% of items on Etsy capable to ship for free domestically during the holidays which is a great success for a company its size.

This wrinkle drove meaningful improvements in conversion rate which is evidence that product initiatives, seller education, and incentives are paying dividends.

Overall, Etsy had a fantastic holiday season with sellers’ holiday GMS, the five days from Thanksgiving through Cyber Monday, up 30% YOY.

Forecasts for 2019 did not disappoint which calls for sustained growth and expanding margins with GMS growth in the range of 17% to 20% and revenue growth of 29% to 32%.

Execution is hitting on all cylinders and combined with the backdrop of a strong domestic economy, consumers are likely to gravitate towards this e-commerce platform.

Expanding its marketing initiatives is part of the business Josh Silverman explained during the conference call with Etsy dabbling in TV marketing for the first time in the back half of 2018, and finding it positively impacting the brand health metrics particularly around things like intending to purchase.

However, Etsy has a more predictable set of marketing investments through Google that offers higher conversion rates and the firm can optimize to see how they can shift the ROI curve up.

Etsy can invest more at the same return or get better returns at the existing spend from Google, it is absolutely the firm's bread and butter for marketing, particularly in Google Shopping, and some Google product listing ads.

With all the creativity and reinvestment, it’s easy to see why Etsy is doing so well.

Online commerce has effectively splintered off into the haves and have-nots.

Those pouring resources into innovating their e-commerce platform, customer experience, marketing, and social media are likely to be doing quite well.

Retailers such as JCPenney (JCP) and Macy’s (M) have borne the brunt of the e-commerce migration wrath and will go down without a fight.

Basing a retail model on mostly physical stores is a death knell and the models that lean feverishly on an online presence are thriving.

At the end of the day, the right management team with flawless execution skills must be in place too and that is what we have with Etsy CEO Josh Silverman and Etsy CFO Rachel Glaser.

Buy this great e-commerce story Etsy on the next pullback - shares are overbought.

Mad Hedge Technology Letter

January 16, 2019

Fiat Lux

Featured Trade:

(3D PRINTING GETS A SECOND WIND),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

At our weekly Monday staff meeting, coworkers were griping and grimacing about their failed internet connections and annoying glitches to their favorite e-commerce sites during the mad rush to find the best deal during Black Friday and Cyber Monday.

Internet traffic was that torrential when sites were driven offline for minutes and some, hours by a bombardment of gleeful shoppers hoping to splash their credit card numbers all over the web on sweet discounts.

The crashing of system servers epitomizes the robust transition to online commerce that has most of us pinned to our devices surfing our go-to platforms all day long.

According to data from Adobe (ADBE) analytics, Black Friday sales jumped 23.6% YOY to $6.22 billion, and it was the first time in history that mobile sales broke the $2 billion threshold.

It is a clear victory for e-commerce and, in particular, mobile shopping that has become more integrated into modern tech DNA.

Mobile sales comprised 33.5% of total sales and were up from 29.1% last year, signaling that more is yet to come from this transcending movement that is shoving everything from content, digital ads, entertainment, banking and pretty much everything you can think of to your handheld smartphone.

CEO of Kohl’s (KSS) Michelle Gass confirmed the e-commerce strength by saying, “80 percent of traffic online came from mobile devices.”

The beauty of this movement is that it’s not an “Amazon (AMZN) takes all” scenario with other players allowed to feast on a growing size of the e-commerce pie.

“Click and collect” has been a strategy that has paid off handsomely with sales up 73% YOY during the shopping holidays.

This all supports my prior claim that e-commerce is one of the most innovative and dynamic parts of technology especially the grocery space, and the buckets full of capital attempting to reconfigure the e-commerce spectrum is creating an enhanced customer experience for the final buyer resulting in better products, superior delivery methods, and cheaper prices.

Some other retailers spicing up their e-commerce strategy are dinosaur big-box retailer’s intent to defend their business from the Amazon death star.

If you can’t innovate in-house, then “borrow” the innovation from somewhere else.

That is exactly what Target (TGT) has chosen to do announcing last week that it would grant free 2-day shipping with no minimum sale threshold.

The tactic is bent on undercutting Walmart (WMT) who currently operate a 2-day free shipping policy with a minimum order of $35.

Most shoppers will buy in bulk easily eclipsing the $35 per order mark minimizing the rot of small orders.

And if they aren’t eclipsing the $35 per order mark, it demonstrates the firm’s offerings lack the diversity and quality to compete with Amazon.

Capturing the incremental sale squarely rests on the e-tailers ability to coax out the buyers’ impulses to move on the can’t-miss items.

The lesser known retailers fail miserably at matching the lineup of products that Amazon can roll out.

The bountiful product selection at Amazon leads customers to pay for 3, 4, 5, 6 or more items on Amazon.com.

That said, I am bullish on Walmart’s e-commerce strategy. The “click and collect” strategy has shown to be an outsized winner increasing industry sales of this type 120% YOY.

Walmart is at the center of this strategy and they are refurbishing their supercenters to accommodate this growth in collecting from the curb.

Effectively, this gives customers the option to skip the queue instead of bracing the hoards and navigating the crowds of shoppers in the supercenter.

Other changes are minor but will help, such as offering online product location maps to customers beforehand and allowing customers to pay for large items like big-screen televisions on the spot.

The biggest windfall is derived from the cataclysmic demise of Toy “R” Us, giving Walmart a new foothold into the toy business.

Walmart is beefing up toy items by 40% in the stores and layering that addition with another 30% increase in their e-commerce division.

Adobe’s upper management recently said in an interview that interactive toys have been a wildly popular theme this year amid a backdrop of the best holiday shopping season ever recorded.

Another attractive gift selling like hotcakes are video games, titles boding well for sales at Activision (ATVI), EA Sport (EA), and Take-Two Interactive (TTWO).

Reliant IT infrastructure will be a key component to executing these holiday sales bonanzas.

Clothing retailer J. Crew and home improvement chain Lowe's (LOW) were grappling with sudden disruptions to their IT systems before they managed to get back online.

More than 75 million shoppers parade the internet to shop during Black Friday and Cyber Monday, and the opportunity cost swallowed to a tech glitch is a CEO’s worst nightmare.

Ultimately, what does this all mean?

Focusing on the positive side of the surging holiday sales is the right thing to do because the avalanche of momentum will have a knock-on effect on the rest of the economy.

Certain companies are positioned to harvest the benefits more than others.

Amazon guided its 4th quarter estimates conservatively and is in-line to beat top and bottom line forecasts.

Other pockets of strength are Walmart’s tech pivot, albeit from a low base. Walmart still has more room to maneuver and they are in the 2nd inning of their tech transformation snatching the low-hanging fruit for now.

Another interesting e-commerce company swinging its elbows around is Etsy (ETSY).

They sell vintage and handmade craft adding the personalized touch that Amazon can’t destroy.

Margins will be higher than the typical low-cost, value e-commerce platform, but scaling this type of business will be more difficult.

Sales grew 41% sequentially and just in time for a winter holiday blowout.

Etsy became profitable in 2017 after three straight loss-making years, and 2018 is poised to become its best year ever.

The profitability bug is hitting Etsy at the perfect time with its EPS growth rate up 36% sequentially.

They report at the end of February and I expect them to smash all estimates.

There are some deep ramifications for the long term of e-commerce that is beginning to suss itself out.

For one, shipping times will continue to be slashed with a machete. If you are enjoying the 2-day free shipping from Amazon and Target now, then wait until 2-day becomes 1-day free shipping.

Then after 1-day free shipping, customers will get 10-hour shipping, and this won’t stop until goods are shipped to the customer’s door in less than 1-hour or less.

This is what the massive $50 billion in logistical investments over the next five years by the likes of Uber and Amazon are telling us.

It will take years for the efficiencies to come to fruition, but it is certainly in the works.

In the next five years, America’s logistics infrastructure will have to accommodate the doubling of e-commerce packages from 2 billion to 4 billion per year.

Another trend is that omnichannel offerings are sticking and won’t go away anytime soon.

It was once premised that online sales would destroy brick and mortar, yet moving forward, a mix of different sales channels will be the most efficient way of moving goods in the future.

Pop-up stores have been an intriguing phenomenon of late, and surprisingly, 60% of consumers still require interaction with the product to be convinced it's worthy of buying.

Certain products such as fashionable dresses and designer shoes must be given a whirl before a decision can be made. This won’t change anytime soon.

The timing of the sales and marketing push has been moved forward as competitors are eager to get a jump on one another.

Management is agnostic to the timing of the sale.

Thus, discounted sales will show up a week before Thanksgiving as pre-Thanksgiving sales in the future elongating the holiday shopping season cycle by starting it early and delaying the finish of it.

Lastly, the record numbers prove that the e-commerce renaissance and the pivot to mobile is not just a flash in the plan.

What does this mean for tech equities?

The temporal tech sell-off of late is largely a result of outside macro forces and is not indicative of the overall health of the tech sector that has experienced record earnings.

If the markets can keep its head above the February lows, it sets up an intriguing December fueled by Americans flashing their digital wallets on online platforms.