Regular readers of this letter are well aware of my fascination with demographics as a market driver.

They go a long way towards explaining if asset prices are facing a long-term structural headwind or tailwind.

The great thing about the data is that you can get precise, high quality numbers 20, or even 50 years in advance. No matter how hard governments may try, you can?t change the number of people born 20 years ago.

Ignore them at your peril. Those who failed to anticipate the coming retirement of the baby boomer generation in 2006 all found themselves horribly long and wrong in the market crash that followed shortly.

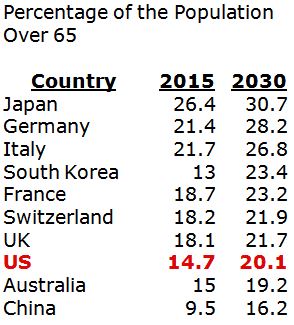

The Moody?s rating agency (MCO) has published a report predicting that the number of ?super aged? countries, those with more than 7% of their population over the age of 65, will increase from three to 13 by 2020, and 34 in 2030.

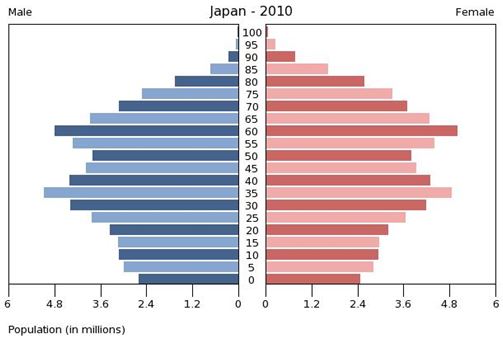

Currently, only Japan (26.4%) (EWJ), Italy (21.7%) (EWI), and Germany (EWG) are so burdened with that number of old age pensioners. France (EWQ) (18.7%), Switzerland (EWL) (18.2%), and the UK (EWU) (18.1%) are about to join the club.

The implication is that the global demographic dividend the world has enjoyed over the last 40 years is about to turn into a tax, a big one. The consequence will be lower long-term growth, possibly by 0.5%-1.0% less than we are seeing today.

This is what the bond market may already be telling us with its unimaginably subterranean rates for its long term bonds (Japan at -0.13%! Germany at 0.14%! The US at 1.75%!).

Traveling around Europe last summer, I was struck by the number of retirees I ran into. It certainly has taken the bloom off those topless beaches (I once saw one great grandmother with a walker on the beach in Barcelona).

For the list of new entrants to the super aged club, see the table below.

This is all a big deal for long-term investors.

Countries with inverted population pyramids have lots of seniors saving money, spending very little, and drawing hugely on social services.

For example, in China, the number of working age adults per senior plunges from 6 in 2020, to 4.2 in 2030, to only 2.6 by 2050!

Financial assets do very poorly in such a hostile environment. Your money doesn?t want to be anywhere near a country where diaper sales to seniors exceed those to newborns.

You want to bet your money on countries with positive demographic pyramids. They have lots of young people who are eager to work and to spend on growing families, drawing on social services little, if at all.

Fewer seniors to support keeps tax and savings rates low. This is all great for business, and therefore, risk assets.

Be careful not to rely solely on demographics when making your investment decisions. If you did that, you would have sold all your American stocks in 2006, had two great years, but then missed the tripling in markets that followed.

According to my friend, noted demographer Harry S. Dent, Jr., the US will not see a demographic tailwind until 2022.

When building a secure retirement home for yourself, you need to use all the tools in your toolbox, and not rely just on one.

A demographic headwind does not permanently doom a country to investment perdition.

The US is a prime example, where a large number of women joining the labor force, high levels of immigration, later retirement ages, and lower social service payouts all help mitigate a demographic drag.

A hyper accelerating rate of technological innovation also provides a huge cushion.

You Want to Invest in This Pyramid?

...Not This One

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/Lady-Raspberries-e1434408537142.jpg291400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-05-11 01:06:022016-05-11 01:06:02The Cost of an Aging World

When British Prime Minister, Winston Churchill, was informed that Italy joined the side of the Germans in the Second World War, he infamously replied, ?Well, that?s only fair. They were our allies in the First World War.?

Many investment strategists are similarly vexed today, trying to decide what to do about the home of the Roman Empire. Over the past 12 months, the Italy iShares ETF (EWI) has added a blistering 57%, beating the Dow, the S&P 500, and yes, even the shares of much worshipped Apple (AAPL).

The land of Cicero, Seneca, and Julius Caesar has produced one of the world?s best performing stock markets. The problem is: Now What?

That question becomes particularly urgent when one examines the recent price action of the Italian stock market, which is showing a distressing topping action.

Has the world suddenly fallen in love with pasta, Parmesan and polenta to deliver such performance? The answer is a little more complicated than that.

First and foremost, you can thank plunging Italian interest rates. Since the bad old days at the end of 2010, the yield on ten-year Italian government bonds has cratered, falling from 7.2% to 2.7%. Cheaper money brings lower costs and larger profits for companies south of the Alps.

It also encourages investors to borrow money to buy assets, pushing prices northward. This is all great news for the stock market. Flip the chart of the Italian bond market for the past four years upside down, and you get a chart of the Italian stock market.

Another positive development has been the long awaited departure of bad boy prime minister, Silvio Berlusconi. Voters grew weary of the media magnate?s tawdry personal behavior, relations with underage prostitutes and criminal tax convictions.

The ?bunga bunga? room, which I drove past on the island of Sardinia a few weeks ago, is no more. In fact, Berlusconi?s palatial estate there is now on the market for a staggering $630 million. Whatever happened to humility? The new, more responsible government has inspired investors to pour even more Euro?s into Italian shares.

Just looking at the numbers, Italy is not a country where you would rush to pour your entire life savings into. The Economist magazine expects Italy to generate a microscopic 0.2% in economic growth in 2014. Inflation is at zero. Yet the headline unemployment rate is at a monstrous 8.6% and the real figure is probably much higher.

Europe?s third largest economy disturbingly has a smaller GDP, or gross domestic product, per person than it did in 1999. Its national debt exceeds a staggering $134 billion and is almost in as much trouble as nearly bankrupt Greece.

These numbers are hardly a ringing endorsement for investment.

Italy suffers from two gigantic structural problems.

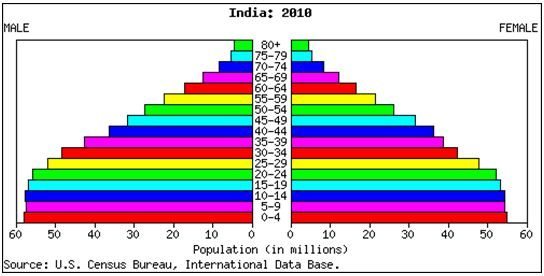

One is that they?re just not making Italians anymore. Each Italian couple is producing only 0.9 children between them. That compares to 1.9 in the US and a replacement rate of 2.1. This means the country is suffering from a demographic implosion of Biblical proportions.

The population pyramids are going from bad to worse (see below). This predicts that a shrinking young population will have to support an ever growing number of old age pensioners. Countries with these characteristics have historically suffered from weak economies, falling currencies, burgeoning debt, and are usually terrible investments.

The second is the structural problem that has plagued the European Monetary System since its inception. Before the Euro was invented in 1999, a country with a weak economy, like Italy, could simply devalue its way to prosperity. It could also borrow and spend heavily to reflate the economy, with few consequences.

A lower currency means that its products become cheaper and more competitive in the international marketplace. Italy did exactly that, taking the Lira down from 600 to the dollar when I first visited there in the 1960?s, to 1,800 just prior to its entry to the European currency block. That effectively dropped the cost of anything you bought in Italy by two thirds, which is great for business.

Since then, all of Europe has shared a common currency, the Euro. That means that Italy now shares a currency with Germany, perennially the strongest economy on the continent. The Germans are only interested in pursuing policies that suit a healthy economy. That means no borrowing and keeping a lid on inflation as a top priority.

The devaluation, borrowing and spending tools have thus been thrown out of the Italian monetary toolbox. So while business is weak, there is not much anyone can do about it. Greece, Spain, and Portugal all face the same dilemma.

The solution to these structural problems would be for Europe to more closely mimic America by creating a true United States of Europe. An empowered and centralized Ministry of Finance would coordinate all continent wide borrowing and spending. The European Central Bank would be given vastly expanded Federal Reserve type powers.

The new agency would issue a single pan European bond, much like the Treasury bonds in the US. As a result, Germany would have to pay slightly higher interests in this brave new world. But the weaker countries would pay much lower interest rates, as the risks for such borrowing would be spread among the Community?s 28 members, thus boosting their economies.

The problem is that such ground-breaking reforms would require a far greater level of trust and cooperation than the Europeans have managed until now. It has been 15 years since that last important structural change in Europe. It could take an additional 15 years before we see another big one.

Until then, Italy twists slowly in the wind.

That is, not if the new Italian Prime Minister, Matteo Renzi, has anything to say about it. The mildly socialist Democratic Party?s standard bearer has behaved much like a bull in a china shop, proposing desperately needed changes for the economy as fast as his overworked printer can print them. His goal is to bring Italy into the 21st century, kicking and screaming all the way, and end a half-century of economic torpor.

The 39 year old former mayor of Florence is now the youngest prime minister in history. He is next in line to become the president of the entire European Community. German Chancellor, Angela Merkel refers to him as the ?Matador.?

Renzi has already implemented important tax reform, cutting the monthly bill for low waged workers by $110 a month. Deregulation is in the air, and Renzi has promised to take the scalpel to the country?s notoriously bloated bureaucracy.

It costs an eye popping $150,000 in fees and licenses to open a restaurant in central Rome. That?s why your eggplant Parmesan is so expensive these days. When I first came to the Eternal City 46 years ago, I lived on $2 a day. Now, I can barely scrape by on $2,000. (My tastes have gotten more expensive).

Renzi plans to privatize many government entities, modernize an arthritic legal system, and bring institutional corruption to an end.

It all reminds me of when Margaret Thatcher was elected PM in 1979 and proceeded to read the riot act to her people for a decade. The London stock market skyrocketed as a result.

If Renzi is successful, the bull market in Italian stocks is not ending; it is just taking a breather before another leg up.

The easiest way to participate is through the iShares Italy ETF (EWI). You could also take rifle shots at single companies, based around your favorite sector call.

Fiat (FIATY) is prospering from the new renaissance in the US car market, where miracle worker, Sergio Marchionne, has engineered a spectacular turnaround at its Chrysler subsidiary.

ENI (E) is a play on the global energy boom. Telecom Italia Media is your classic big cap communications play. Luxottica Group (LUX) is the world?s largest maker of eyeglass frames and gives you participation in a global consumer spending rebound. ST Microelectronics is headquartered in Switzerland, but has the bulk of its operations in Italy, and is a favored technology bet.

If you do decide to participate in the delights of the Italian stock market, don?t forget to hedge out your currency risk, as the Euro is expected to remain weak against the US dollar for years. Eventual 1:1 parity is not out of the question. You can do this through selling short the Euro (FXE) against your Italian holdings, or via buying the short Euro 2X leveraged ETF (EUO).

Or you can let someone else do all the work for you. The Wisdom Tree Europe Hedged Equity ETF (HEDJ) buys a basket of European stocks, and hedges out the currency risk. It has been a favorite of hedge fund managers for the past year.

As for me, it?s arrivaderci for now. The spaghetti carbonara beckons!

Italian Ten Year Government Bond Yields

It?s All About Renzi

Ciao, Baby!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/John-Thomas-Roman-Colosseum-e1433979704751.jpg300400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-07-28 01:03:322014-07-28 01:03:32What to do About Italy?

It looks like the (FXE) gave us the double top at $133 which I predicted in my August 28 webinar, which very conveniently, was the lower strike of my Currency Shares Euro Trust (FXE) September, 2013 $133-$135 bear put spread. We have since backed off $3, and lower levels beckon.

I originally wrote this Trade Alert on July 18 while on the express train from Berlin to Frankfurt. I had to wait until we stopped at a station before I could send it on my iPhone. My friends in the German government had just painted a picture of the European economy which approximated Hieronymus Bosch?s vision of hell. My later discussions with European central bankers and CEO?s confirmed the worse.

Since then the Euro has appreciated against the dollar almost everyday, slowly draining profits from my model-trading portfolio. Lugging this position in the baggage of my summer vacation was no fun. That abruptly ended last week when traders returning from vacation, well rested and feeling their oats, decided collectively to take another run at the beleaguered European currency.

As of this morning, the market priced our spread at $1.92, just eight cents short of its maximum potential profit. That leaves 77% of the profit for us. So I am going to take the money and run. This reduces our risk for the month of September, when we are threatened by Syria and the regional contagion that will follow, the debt ceiling crisis, the taper, the identity of Ben Bernanke?s replacement, and a giant asteroid destroying the earth.

Since I sold short the Euro, almost every continental economic data point has been positive. Just this morning, we learned that the August Eurozone PMI Index rose from 50.5 to 51.5, a two year high. The UK August Business Activities Index leapt from 60.2 to 60.5, a six and a half year peak, no doubt in part due to the wad of money I dropped there a few weeks ago. The trend is your friend here, and like a giant supertanker slowly turning, the information flow is gradually turning from red to green.

If anything, I am now inclined to start examining European equity markets, which may bounce back stronger than those in the US. On the short list will be Germany (EWG), which is already in a solid uptrend, and Italy (EWI) for a turnaround play. Greece (GREK) has already made its move, nearly tripling off the bottom.

On to the next trade.

Things Weren?t So Bad After All

https://www.madhedgefundtrader.com/wp-content/uploads/2013/09/Picture-Strange.jpg389516Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-09-05 10:38:582013-09-05 10:38:58Taking Profits on My Euro Shorts

You couldn?t mistake the meaning of the cries of topless female protesters as they flung themselves at police guarding Italian polling stations on Monday. Basta! Basta! Enough! Enough! The purpose of their demonstration was visibly scrawled in large letters across their nubile bodies in black ink for all to see. Mille grazieProfesoressaFrancesca for being my Rosetta Stone!

Global equity investors could well be screaming enough, enough as well. Right when it became clear that the Italian election was not going according to script, the major indexes rolled over from substantial gains to even more impressive losses. The Volatility Index (VIX) blasted 35% to the upside, the biggest move since November, 2011, the last time the Land of Julius Caesar threatened a meltdown. The Italian Index ETF (EWI) really got decimated, posting an intraday fall of 18%, while the Euro (FXE), (EUO) took a two and a half cent dive against the greenback.

Up until today, the smart money was betting on a win by socialist Pier Luigi Bersani and some continuation of the recent reformist policies. What we got was a much stronger than expected showing by Silvio Berlusconi, who is using his billions of Euros to get elected to avoid going to prison. His platform is to undo all of the reforms of recent years, and basically send Europe back to the crisis days of 2010, when the European currency traded as low as the $1.17 handle. Note to self: the smart money isn?t always right.

Of course, I have been warning anyone who would listen that something like this was headed our way (click here for ?Is the Party Over? ). I was even so precise in my predictions that I said the trigger might come from the next leg of the European financial crisis.

To see the exact levels where major support kicks in on the charts for this selloff, please follow the link above. For the Legions who follow my market beating Trade Alert Service, take solace in the fact that our entire portfolio expires in just 13 trading days, and these levels only need to hold until then. After that, we want everything to go to zero, where we can buy them cheap.

Unhappy Italian Voter

Long Time No See

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Black-Swan.jpg444587Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-02-26 09:59:322013-02-26 09:59:32Suddenly Those Italian Lessons Are Paying Off

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

...Not This One

...Not This One