Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics are destiny, then America’s future looks bleak. You see, they’re just not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the number of middle-aged big spenders is falling, risk markets plunge.

Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

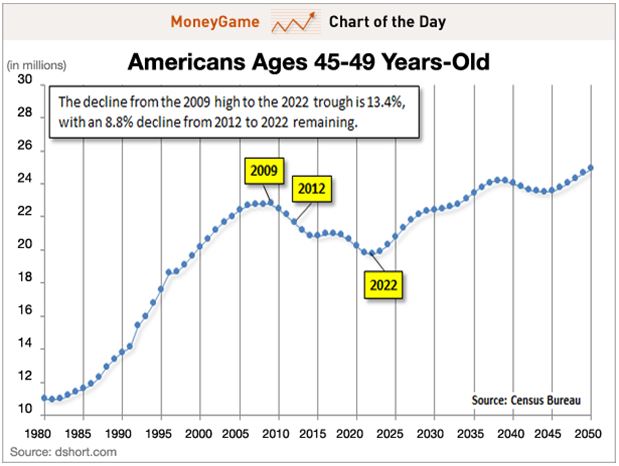

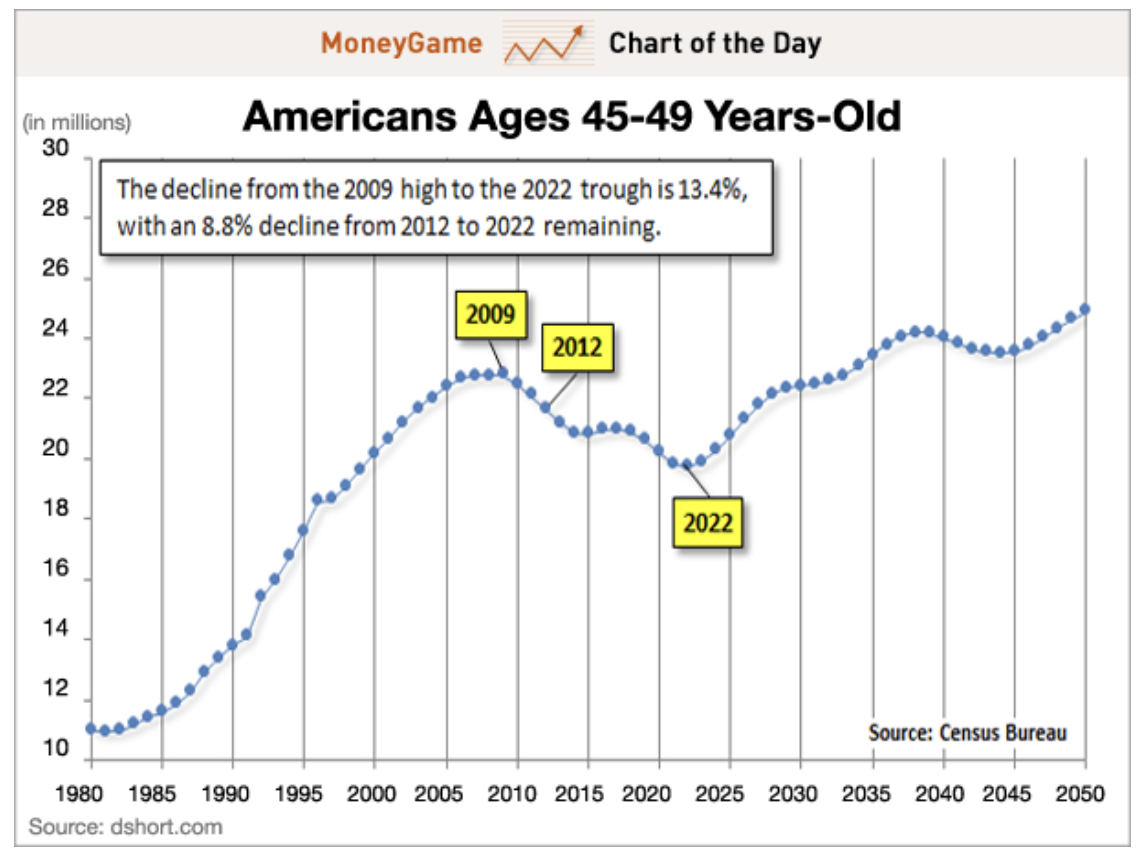

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, but they also backtest with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country, and you can develop a highly reliable timetable for when and where to invest.

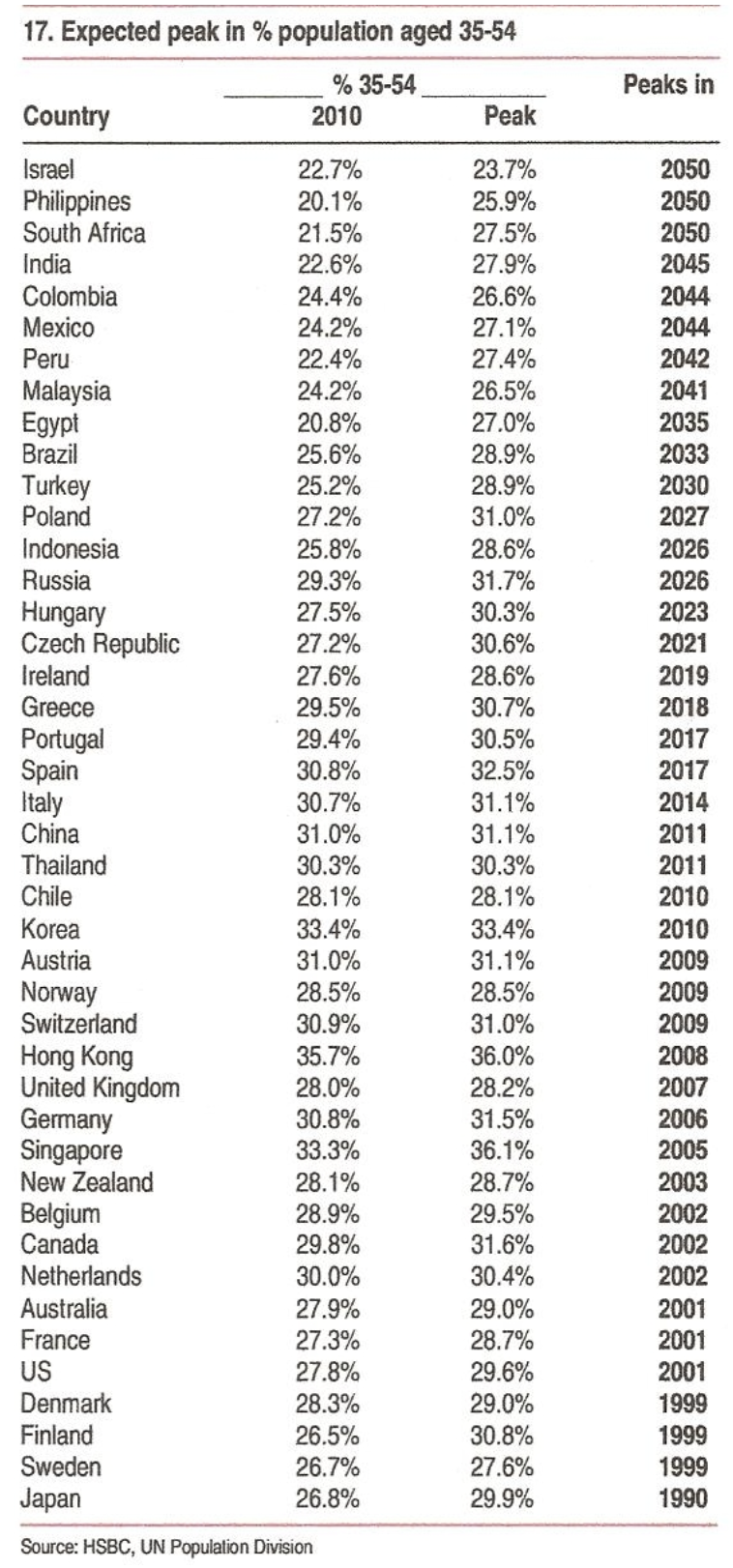

Instead of poring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

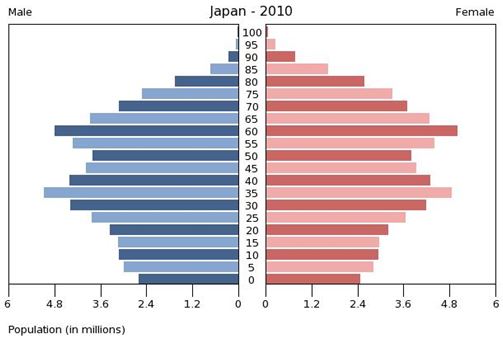

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice back test.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2,000’s, and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate, peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle-aged not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan), while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

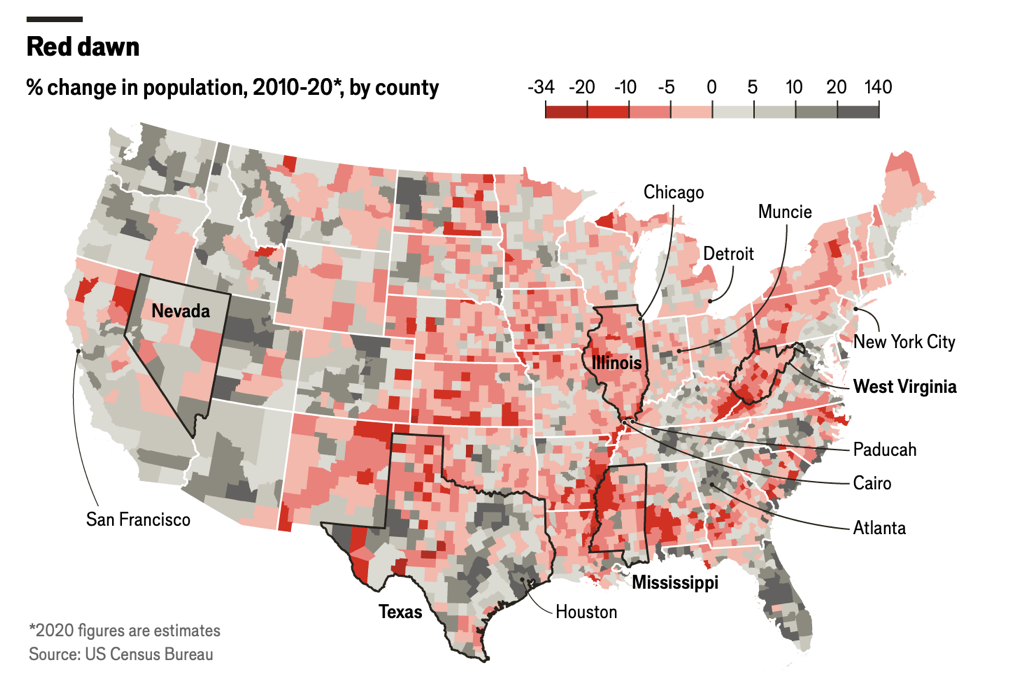

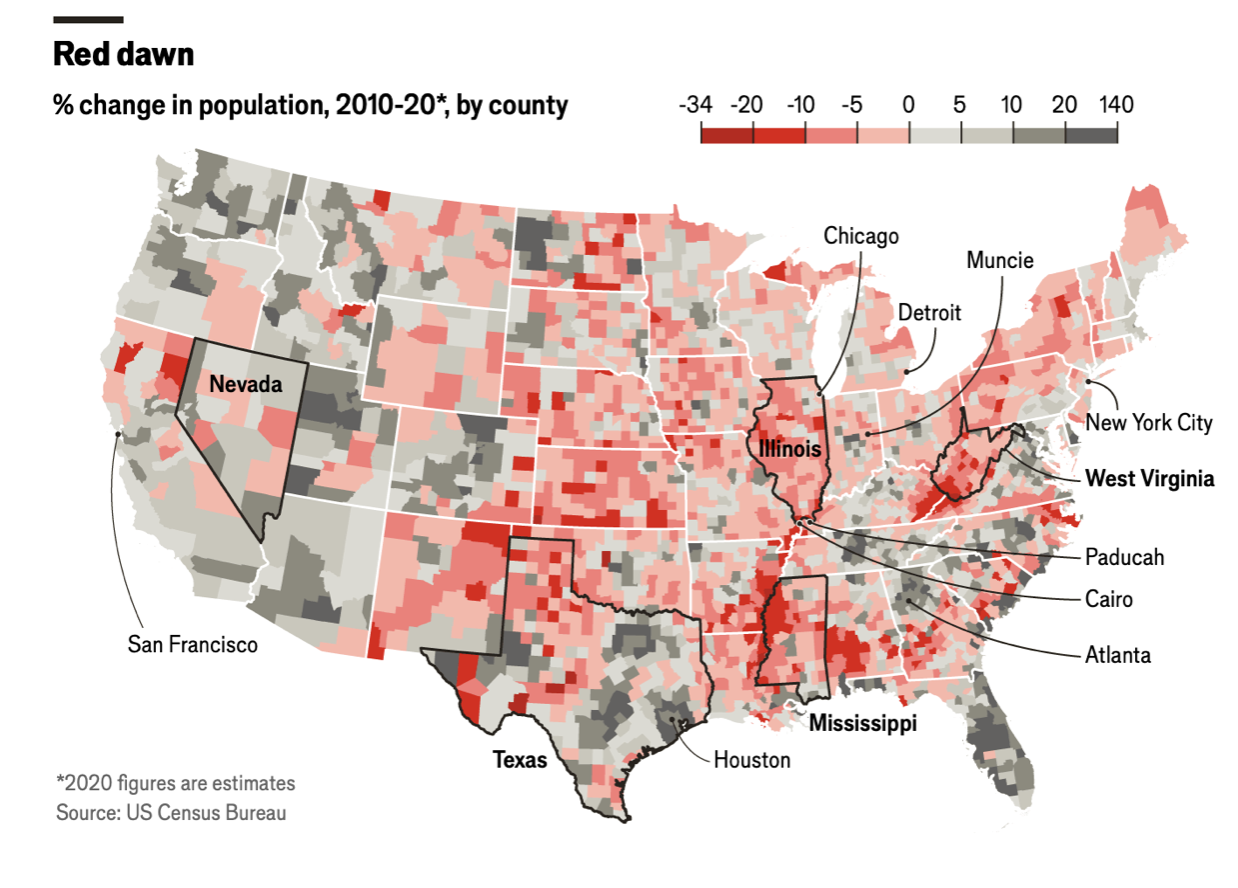

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills is picking up speed, and the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

April 24, 2024

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics is destiny, then America’s future looks bleak. You see, they’re not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the numbers of the middle-aged big spenders are falling, risk markets plunge. Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, they also back-test with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country and you can develop a highly reliable timetable for when and where to invest.

Instead of pouring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice backtest.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2000s and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle age not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan) while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills picking up speed, the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Regular readers of this letter are well aware of my fascination with demographics as a market driver.

They go a long way towards explaining if asset prices are facing a long-term structural headwind or tailwind.

The great thing about the data is that you can get precise, high quality numbers 20, or even 50 years in advance. No matter how hard governments may try, you can?t change the number of people born 20 years ago.

Ignore them at your peril. Those who failed to anticipate the coming retirement of the baby boomer generation in 2006 all found themselves horribly long and wrong in the market crash that followed shortly.

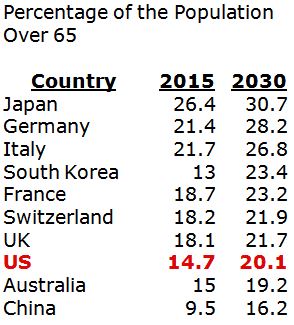

The Moody?s rating agency (MCO) has published a report predicting that the number of ?super aged? countries, those with more than 7% of their population over the age of 65, will increase from three to 13 by 2020, and 34 in 2030.

Currently, only Japan (26.4%) (EWJ), Italy (21.7%) (EWI), and Germany (EWG) are so burdened with that number of old age pensioners. France (EWQ) (18.7%), Switzerland (EWL) (18.2%), and the UK (EWU) (18.1%) are about to join the club.

The implication is that the global demographic dividend the world has enjoyed over the last 40 years is about to turn into a tax, a big one. The consequence will be lower long-term growth, possibly by 0.5%-1.0% less than we are seeing today.

This is what the bond market may already be telling us with its unimaginably subterranean rates for its long term bonds (Japan at -0.13%! Germany at 0.14%! The US at 1.75%!).

Traveling around Europe last summer, I was struck by the number of retirees I ran into. It certainly has taken the bloom off those topless beaches (I once saw one great grandmother with a walker on the beach in Barcelona).

For the list of new entrants to the super aged club, see the table below.

This is all a big deal for long-term investors.

Countries with inverted population pyramids have lots of seniors saving money, spending very little, and drawing hugely on social services.

For example, in China, the number of working age adults per senior plunges from 6 in 2020, to 4.2 in 2030, to only 2.6 by 2050!

Financial assets do very poorly in such a hostile environment. Your money doesn?t want to be anywhere near a country where diaper sales to seniors exceed those to newborns.

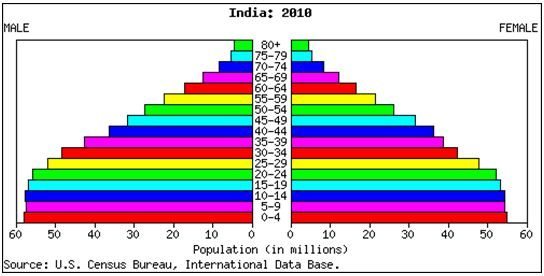

You want to bet your money on countries with positive demographic pyramids. They have lots of young people who are eager to work and to spend on growing families, drawing on social services little, if at all.

Fewer seniors to support keeps tax and savings rates low. This is all great for business, and therefore, risk assets.

Be careful not to rely solely on demographics when making your investment decisions. If you did that, you would have sold all your American stocks in 2006, had two great years, but then missed the tripling in markets that followed.

According to my friend, noted demographer Harry S. Dent, Jr., the US will not see a demographic tailwind until 2022.

When building a secure retirement home for yourself, you need to use all the tools in your toolbox, and not rely just on one.

A demographic headwind does not permanently doom a country to investment perdition.

The US is a prime example, where a large number of women joining the labor force, high levels of immigration, later retirement ages, and lower social service payouts all help mitigate a demographic drag.

A hyper accelerating rate of technological innovation also provides a huge cushion.

You Want to Invest in This Pyramid?

You Want to Invest in This Pyramid?

...Not This One

...Not This One

I have got a lot right in the markets lately, especially this year, when 90% of my Trade Alerts went well. But as they say in karate school in Japan, you can?t block all the punches. I certainly missed the opportunity of a lifetime to load up on the stocks of a certain country, which I am about to visit. I?ll give you a hint up front: think edelweiss.

Yes, you guessed it. The Swiss economy has been barely eked out any positive GDP growth ever since Europe began its meltdown a few years ago. Q1, 2013 saw a gain of 0.6%, bringing the year on year figure to a lackluster 1.1%.

While broad swaths of the economy are weak, chemicals, pharmaceuticals, precision instruments, watches and jewelry, the things the Swiss are best at, seem to be holding their own. But it makes America?s 2.5% rate look positively robust by comparison.

Switzerland is certainly a country with many attractions. It is home to world-class companies, like, Nestle, Roche, Novartis, and Swatch. It has perennially run a strong current account surplus. Its 347 banks control assets amounting to seven times the country?s GDP, and account for 40% of stock market capitalization (compared to 10% in the US).

Despite shunning membership in the European Community, it has developed a first class export industry. It is not all about watches, cheese, cowbells, and Swiss army knives.

None of this explains why the Swiss franc has been so weak. Since the August, 2011 peak, the Swiss Franc has plunged by a gut churning 28%, and has been one of the world?s weakest currencies against the greenback. Note that the ETF (FXF) is priced in the inverse to the cash market, meaning that it takes $1.05 to buy one Swiss franc. To give you some long-term perspective on this, the dollar is now 72% cheaper than when I first visited this alpine paradise 43 years ago, when it cost SF3.00 to purchase a buck.

As strong as the fundamentals are for Switzerland, they have nothing to do with the strength of the currency. It has long been the flight to safety currency of choice for Europeans. While a director of Swiss Bank Corporation, I personally saw gold bars imprinted with the German eagle secreted there by high-ranking Nazi?s and never reclaimed. This is one theory why the Germans didn?t invade Switzerland during WWII.

Later, asset-protecting investors believed that the Swiss Army?s formidable mountain redoubts could hold the Soviet army at bay. To this day, there are still formidable stockpiles of weapons in the basements of the big Swiss banks, and most of the senior staff double as army officers.

One reason the Swiss franc has been a speculative target is that the country has a Lilliputian GDP of $635 billion, only 4.1% of America?s.

In 2011, the country faced a major currency crisis, as fears of a dollar and euro collapse drove the Swiss franc to an unbelievable all time high of 70 centimes to the dollar. While I was there during the summer, the local newspapers were chock full of stories about factory closings and mass layoffs. The strong Swiss franc was rapidly driving the economy out of business. Much business decamped for Germany, where the cost of production was denominated in far cheaper euros.

In September, 2011 the Swiss National Bank took drastic action. It immediately devalued the Swiss franc against the euro by 10%, and then pegged it there, vowing to spend whatever it takes to maintain the cheaper rate. It took on all comers.

The bold strategy was a huge success, as you can see from the charts below. Some friends at the central bank tipped me off that action was imminent, enabling me to get my readers into the most successful Trade Alert since the inception of this service. Over the course of a weekend, they made close to 400% on Swiss franc puts.

Here comes my big miss. I didn?t execute the second half of the trade. Basic Macro Hedge Trading 101 tells us that weak currencies are always great for local stock markets. That was definitely the case in Switzerland, where the equity ETF (EWL) has since posted an eye popping 55% return. That makes it one of the top performing European bourses, despite its feeble economy.

Did I do the trade? Nope? Perhaps one 4X gain in Switzerland was enough?

As penance for my oversight, I shall be punished severely. When I visit Switzerland in a few weeks for a fresh round of high altitude climbing, the mountains will no doubt claim their share of blisters, cuts, and rope burns. A hangover or two as well may enter the picture, as well. Those guides drink like fish.

At least the fondue, r?sti potatoes, raclette, and schnapps will be cheaper.