Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)

Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)

It was early.

The real recession doesn’t kick into gear for another quarter or so.

This was just a quick fake-out.

The bond market freaking out and pricing in 1.25% Fed Funds’ cuts was a generous gift to tech stocks.

Why do I say that?

It is a dip in which we can get into tech prices at cheaper prices – probably the last time before the U.S. election.

We are starting to receive confirmation from many earnings reports that the consumer is starting to get cold feet.

The pullback in consumer strength runs the whole gamut from home improvement to restaurant eating.

I cover tech and the weakness is multi-pronged stemming from hardware to software.

The latest to ring the alarm about sluggish consumer spending was the digital accommodation platform Airbnb (ABNB).

Airbnb earned sales of $2.7 billion for the same quarter last year and now they have told investors that for next year they plan to target $2.5 billion of sales.

The culprit blamed by Airbnb management is the American consumer.

Americans are shortening their Airbnb stays and soon they could be sacrificing Airbnb altogether. Although we aren’t at that point yet, US consumers simply can’t stomach this new wave of price increases for the cost of living, and reigning back discretionary travel is this logical item to shave from the budget.

The second quarter continued a trend of decelerating bookings growth for Airbnb. The total value of all bookings through Airbnb grew 11% year over year to $21.2 billion for the three-month period. That's down from 12% booking growth in Q1, 15% growth in the final quarter of 2023, and 17% growth in September-ended third quarter of 2023.

In 2022 and 2023, Airbnb, Booking Holdings (BKNG), and Expedia Group (EXPE) benefited from a bounce-back in travel after the harsh lockdowns prevented many types of travel in 2020 and into 2021. So-called revenge travel powered strong sales growth for the companies. But the picture appears to be shifting.

It is hard to see the US consumer just bouncing back with a V-shaped trajectory and that could affect Airbnb sales.

Reports out of high costs states like Washington and New York peg $150,000 per year in income as “lower middle class.”

There has also been a huge migration shift from wealth moving out of blue states to red states in the hope of maintaining purchasing power through these high inflation times.

The fact of the matter is that $35 trillion in Federal debt is the most important topic for this upcoming U.S. President Election, but this topic has been completely sidelined from the national discourse.

This surely means higher debt down the road and a further deterioration in the US consumer profile.

Tech companies with large moats around their business models will get through these times, but for Airbnb, they don’t have this type of moat because consumers don’t necessarily need to travel. Consumers do need to eat, sleep, and drive a car to work.

They can simply just delay travel for a few years before they reload financially.

It is high time to unload stocks like Airbnb even if they are leaders in the home-sharing sub-sector in tech.

Airbnb shares are down around 32% in the past few months highlighting the need for overly expensive tech stocks to adjust to the new reality.

I do believe there is another leg down in shares before an optimal window to buy on the dip presents itself, but that appears to be around $90-$100 per share.

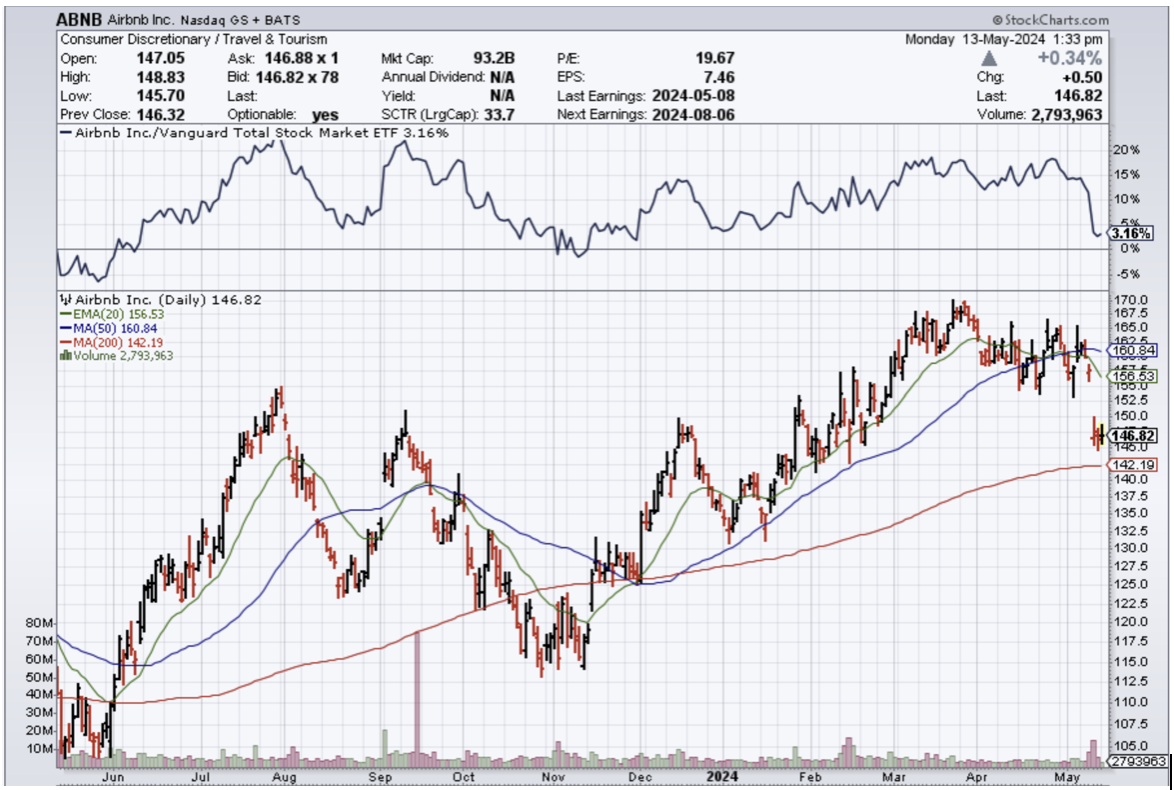

Mad Hedge Technology Letter

May 13, 2024

Fiat Lux

Featured Trade:

(BUY THE TOURIST PLATFORM TECH STOCK)

(ABNB), (EXPE)

Any type of selloff in Airbnb (ABNB) shares will be short-lived as we approach the summer Olympics and European soccer summer tournament.

Global Events of a month-long will get people out of their homes and spending their cash.

These premium events will move the needle for Airbnb revenue-wise in Europe.

The heart of world travel is Western Europe so it’s convenient that these mega-events are in France and Germany and not in some backwater.

Better luck next time if you haven’t locked up your Airbnb in Germany or France by now.

Travelers even have the option to stay through September and enjoy the annual Oktoberfest in Bavaria.

There isn’t lodging to be found in Western Europe in the summer months and even though the economy is starting to weaken around the edges, we are still in for another summer of travel post-pandemic style.

Tourists are splurging like there is no tomorrow held up by the higher income bracket.

Italy is famous for hosting 8 million Americans per year and is otherwise known as Americans' favorite European destination.

That number is poised to balloon to 12 million by 2030 and that means revenue growth for Airbnb as Italian Airbnb’s are rampant everywhere you go in Italy.

As for the company, the business model has been doing great ever since CEO and Founder Brian Chesky put a tight leash on expenses after being caught wrongfooted during the pandemic.

The stock sold off on the earnings even with the nice beat and the Mad Hedge tech letter executed a call spread on the underlying shares.

Weak guidance has been a hallmark of this past earnings season as the economy softens.

Management needs a lower bar to jump over for later this year.

Revenue increased 18% year over year to $2.14 billion last quarter, ahead of the $2.06 billion consensus.

The surge in profit margins was due in part to a shift in the Easter holiday to the first quarter, strong interest income, and leverage from its revenue growth and cost discipline.

The stock is now down 13% from its year-to-date peak and at its lowest point in close to three months.

Airbnb competes with hotels and other types of overnight accommodations, but its closest competitors are other home-sharing platforms like Expedia's VRBO.

But Airbnb already dominates the home-sharing niche with a leading market share among those platforms, and the company appeared to strengthen its position in the first quarter. Revenue at Expedia (EXPE) increased 8% in the period, while its B2C division which includes VRBO was up just 3%.

Competitors have been unable to overcome the powerful network effect present on Airbnb's platform, allowing it to continue growing its lead.

The shareholder returns program is beefing up.

The company continues to return capital to shareholders, buying back $750 million in stock last quarter. With $2.5 billion in total share repurchases over the past year,

Airbnb has reduced its shares outstanding by nearly 3% over that period. While 3% might not sound like much, this strategy compounds over time, and Airbnb should be able to increase buybacks as profits grow.

Additionally, the company is benefiting from higher interest rates as it's on track to generate close to $1 billion in interest income this year, giving it a significant boost on the bottom line.

I’m betting on an uptick in shareholder interest in the short term at these price levels.

I was a little uncomfortable chasing it higher from $170, but $150 is more reasonable and I do believe the Fed pivot tailwinds could catapult us into profits with this trade.

Mad Hedge Technology Letter

November 2, 2022

Fiat Lux

Featured Trade:

(POOR OUTLOOK FOR TRAVEL TECH)

(ABNB), (BKNG), (EXPE)

The big sell-off in Airbnb (ABNB) this morning was not about the great quarter it just had, but what investors have guessed the company faces in 2023.

Prospects look weak next year.

The re-opening and revenge travel surge came through in such a way that growth was brought forward at a blistering rate.

The number's back up my thesis, with ABNBs revenue expanding by 29% or $2.9 billion, ahead of expectations at $2.84 billion.

On the bottom line, earnings per share jumped 47% to $1.79, breezing past the consensus at $1.47.

Yet the stock is down 9% in this morning’s trading, with a textbook “buy the rumor and sell the news” type of price action.

The US is barreling towards a recession in 2023, although the job numbers have stayed extremely resilient in the face of rate hikes.

If jobs can muscle through these next rate rises, then I do believe that a recession can be put off until 2024.

However, it will take time for the market to reflect the new realities and until then, ABNB is poised for a slowdown.

What do I mean by a slowdown?

The company forecasts around a 17% increase in sales which severely underperforms the 29% they registered last quarter.

While the forecast is not something to freak out about, investors are taking profits today and rotating capital elsewhere that isn’t growth.

Unless there is another forced lockdown, I don’t see ABNB beating the 29% expansion in revenue in the near future.

While sales won’t drop off a cliff next year, I don’t see how they get back to the 30% sales growth until we get to the other side of the recession which could be somewhere around 2024.

The downgrade in forecast in the travel industry was consensus.

At the individual level, the astronomical price rises for travel and leisure will have to abate somewhat to attract the incremental customer from now.

Most people have budgets, and they saved for 2 years to blow it all on a summer to remember (or forget).

Competitors such as Booking Holdings (BKNG) and Expedia (EXPE) have yet to report third-quarter earnings, and their guidance should be informative for overall travel trends. The two leading online travel agencies are likely to forecast a similar deceleration into the fourth quarter.

As the travel market evolves, Airbnb will continue to outperform because it’s a monopoly in the home-sharing business and other firms like booking.com don’t come close.

I would definitely classify ABNB as a solid long-term investment and to add on big down days.

Unfortunately, ABNB's core business is being overshadowed by the macro picture these days, which is highly negative for technology stocks.

The silver linings are there, as the business model has also turned from a net loss-making model to a nice profit machine this year.

Even if profits are under $1 billion per year, they were bleeding money just a few years ago as they worked to improve the unit economics in this unique industry.

The 17% increase next year will turn out to be a blip on the radar long term and I believe that once we get over the hump and interest rates start trending down, ABNB will be one stock that will shoot from the bottom left to the upper right.

Mad Hedge Technology Letter

July 13, 2022

Fiat Lux

Featured Trade:

(HOT INFLATION NUMBER BODES POORLY FOR TECH STOCKS)

(LYFT), (UBER), (AMZN), (SHOP), (GOOGL), (SNAP), (META), (TWTR), (MELI), (EXPE), (TRIP)

Fed swaps now fully price in 150 basis points of hikes over the next two meetings after awful inflation numbers came in showing inflation heading in the wrong direction.

The 9.1% inflation print was an acceleration of the 8.6% which was what we got last time.

I don’t want to beat a dead horse, but inflation accelerating and beating the expectations of 8.8%, is paramount to the trajectory of tech shares.

The awful number also underscores the magnitude of policy mistakes that the U.S. Fed Central Bank has overseen.

This is the only thing that matters because macro liquidity drives the trajectory of equities in the short term.

These clowns aren’t serious about tackling inflation, as I said a few times already and this proves it!

Itty bitty rate rises won’t stamp out 9.1% inflation and in fact, encourages it.

The Fed would need to raise the Fed Funds rate by 7.35% to 9.1% immediately from the current 1.75% for the real inflation rate to be non-inflationary.

According to the official Fed website, the Fed targets 2% inflation because they call this level “healthy.”

By their own measure, to achieve this 2% inflation, they would still need to raise rates by 5.35% immediately, but they absolutely won’t because Powell simply has no interest in doing his job, period.

These core expenses skyrocketing is why I keep and kept mentioning that Americans have less money to splurge on tech gadgets and software and again, this inflation report validates my thesis.

Think about pitiful tech stocks that didn’t work in bull markets like ride chauffeurs Lyft (LYFT) and Uber (UBER), I fully expect these companies to perform terribly over the next 6 months amid a rising rate backdrop.

Not only are they growth tech, but their business is directly tied to energy prices.

They are the poster boys for the pain tech companies will feel from hyperinflation.

The outlook is quite poor for technology in the short term, and we are still waiting to form a bottom. It will come back but we need a capitulation.

The accelerated rate of inflation means that we push back the big recovery in tech stocks.

Ecommerce stocks will suffer like Amazon (AMZN), Shopify (SHOP), and MercadoLibre (MELI) because of the decline in discretional spending for the consumer.

Digital ad giants like Google (GOOGL), Snap (SNAP), Meta (META), and Twitter (TWTR) will need to reckon with smaller ad budgets from 3rd party ad purchasers as companies cut back on marketing spend.

Don’t need to increase marketing spend when people have no money to spend on products.

Travel tech stocks like Expedia (EXPE) and Tripadvisor (TRIP) can expect summer to mark peak travel as Americans get more concerned about food and oil budgets after the summer of travel revenge from the arbitrary lockdowns.

It also means there will be a meaningful next leg down for tech stocks as many CFOs are now furiously crunching the new revenue and margin downgrades to reflect this heightened risk.

The new re-rating isn’t reflected yet in tech shares.

It’s already been a few months on the trot where many analysts say this is the top, they have been inaccurate every time.

Even if it is the top, inflation will stay higher for longer and stagflation is the consensus for 2023.

The clowns at the Fed not doing their job means that economic cycles will be shorter and a great deal more volatile because the smoothing effect of moderated inflation is now stripped out of calculations. This effectively means a contracted boom-bust trajectory for tech stocks which is unequivocally what we are seeing in market behavior.

Mad Hedge Technology Letter

November 18, 2020

Fiat Lux

Featured Trade:

(HOT TECH STOCKS GOING INTO THE RECOVERY)

(YELP), (EXPE), (TRIP)

It’s hard to be net short these days when we are staring at an imminent recovery and by this, I mean not a recovery like the past 6 months where extreme optimism was surrounded by the ceaseless spreading of the virus.

Multiple companies such as Moderna and Pfizer have announced the successful creation of Covid-19 vaccine meaning that consumer behavior and the global economy will come back to normal earlier than first thought.

This is great news for a digital ad company like Yelp (YELP) because they rely on the high volume of businesses open.

Their model is based on consumers offering free reviews and they sell digital ad space on their platform.

With one fell swoop, the virus crushed their business model which was why shares halved during the worst bits of the pandemic.

Sentiment has revered and Yelp stock has been on a remarkable tear, gaining ground for nine straight days and rallying 53% in the process.

The rally started a few days ahead of the company’s better-than-expected third-quarter earnings report, gained momentum when the numbers were released.

Yelp is one of the tech sector’s most outsized profit chances on the reopening of the economy—and investors have jumped aboard.

In my estimation, Yelp is a $40 stock masquerading at $30 today.

Travel-related internet stocks given the potential for a Covid-19 vaccine will feel the same tailwinds and stocks that come to mind are Expedia Group, Inc. (EXPE) and TripAdvisor, Inc. (TRIP).

The beaten-up cyclicals have re-rated over the last several days, Yelp is a standout as a name that should have a clear path towards both multiple and estimate upside from here.

In fact, Yelp’s revenue decline hasn’t been as bad as that of the travel sector, thanks in part to stronger-than-expected restaurant demand.

Even though we have experienced stringent lockdowns, Europeans largely traveled in the summer inside of Europe and Americans still found a way to domestically travel even if more localized.

If the market supports a return post-vaccine for the travel industry, it is clearly confirmation that Yelp’s business will recover fast even if not to the peak of summer 2019.

At these price levels, Yelp has a relatively attractive valuation and improving fundamentals.

When a Covid-19 vaccine is developed and comes available, the company should benefit substantially in terms of foot traffic for businesses on its platform as well as its app volume.

Yelp recently reported a net loss of $1 million, or 1 cent a share, compared with profit of $1 million, or 14 cents a share, in the year-earlier period, and although down, it could have been much worse.

Revenue dropped 16% to $220.8 million from $262.4 million.

"Yelp’s third-quarter results demonstrate our business’s considerable resilience, highlighted by positive year-over-year revenue growth in two key areas of our long-term strategy: home and local services and our self-serve sales channel," Co-Founder and Chief Executive Jeremy Stoppelman said in a statement.

Even though travel and retail outlets were affected, Stoppelman indicated new businesses are being created to serve this new type of economy where the home is the center of businesses.

No doubt there will a surge of new services that will support technological infrastructure for the home and home maintenance.

Yelp’s strong balance sheet and increased sales efficiency will allow Yelp to return to sustainable growth in the new year while still managing the impacts of the pandemic.

The company has clearly shown they are on top of the ball, they use their agility to morph with their times and at this price level, Yelp is an unequivocal buy.