Mad Hedge Technology Letter

March 2, 2020

Fiat Lux

Featured Trade:

(TECH’S BIG CORONA HIT)

(COMPQ), (TESLA), (UBER), (EXPE), (CSCO), (CSPR)

Mad Hedge Technology Letter

March 2, 2020

Fiat Lux

Featured Trade:

(TECH’S BIG CORONA HIT)

(COMPQ), (TESLA), (UBER), (EXPE), (CSCO), (CSPR)

Mass layoffs are on the horizon, thanks to the tech market slowdown sapping vitality for risk in the IPO market, and the widening contagion stemming from the coronavirus.

At a moment in Silicon Valley’s history where the market is rethinking its appetite for risk, it is customary for the loftiest and hottest growth names to drop the most in times like this.

For instance, Tesla (TSLA) was rocked by 32% and ride-hailing app Uber (UBER) gave up 25% in an epic downturn.

In general, tech that isn’t integral to the intricate global supply chain will also be penalized because of cratering overall business demand.

The vacuum of demand isn’t applied to only digital products but most others, as the world literally becomes a walled garden of self-quarantine areas.

The odds are still high that this global phenomenon squeaks by, but the far reach of the virus worries even experts and making crucial decisions on how to cut losses is becoming a pressing and imminent issue.

Airlines have been first to announce a potential readjustment to staff numbers such as Finland’s flagship airline Finn Air, but mass layoffs will start to trickle in from Silicon Valley.

Front-running the layoff parade was online travel tech company Expedia (EXPE) who expects to say adiós to 3,000 employees and network infrastructure company Cisco (CSCO) who announced restructuring plans because they expect revenue to fall between 1.5%-3.5% in Fiscal 2020.

I have been unwavering in my core thesis that tech procuring revenue from Mainland China is nothing more than a short-term Faustian bargain, and now the downsides of that bargain are finally appearing and frankly uncontainable.

The viral coronavirus is escalating on the heels of a new round of layoffs from Silicon Valley’s startups who just don’t know how to make money such as robot pizza startup Zume and car-sharing company Getaround who slashed more than 500 jobs.

Online DNA testing company 23andMe, logistics startup Flexport, Firefox internet browser Mozilla and social platform Quora restructured staff as well.

The “disruptors” are finally getting disrupted out of existence because of a sudden referendum on the health of balance sheets.

The situation turned ugly just before the coronavirus and this health crisis just adds fuel on the fire.

In total, more than 30 startups have cut over 8,000 jobs over the past four months with aggressive venture capital investments pulling back significantly.

The latest to flop at the starting line was Casper Sleep (CSPR) who marketed themselves as the “Nike of sleep” only because they sell online mattresses.

Mr. Market is purging these marginal businesses that over-promise, over-hype, and under-deliver.

The IPO pricing was underwhelming with Casper taking down the price range to the point where it went public at over $13.

The stock is now at $8.

No doubt that some of this negative sentiment was stoked by office-sharing company WeWork, who had an epic fall from grace and cut its valuation by 80% late last year while permanently shelving an IPO.

Now the coronavirus is on the verge of scoring the empty net goal as companies go into full-blown crisis mode.

SoftBank bet two ranches on Uber and WeWork, then poured money into Colombian delivery startup Rappi and Indian hotel startup Oyo.

All have sputtered with mass firings recently.

Poor investment decisions led SoftBank to report a $2 billion operating loss in the last quarter of 2019 from their venture capitalist arm named the Vision Fund.

After Nasdaq flourished in a memorable 10-year run post the financial crisis, flip the parabola upside down and markets are tanking with many experts already contrasting the coronavirus sell-off to the dot-com bust of 2001.

Irrational optimism is part of the DNA of San Francisco.

Entrepreneurs are quietly preparing to change the world, but the climate has soured so quickly that many investors believe many of these current entrepreneurs are unlucky.

The rules of the game deem unprofitable models temporarily obsolete in the current market environment.

In the land where spending money in uneconomic ways is a time-honored tradition, turning to more “responsible” models is gut-check time.

Talent is forgoing chances to enter the start-up world too, instead opting for big box corporates who provide a lower ceiling but higher salary and benefits.

Café X, which operated robot coffee shops and raised $14.5 million in venture funding, fired its own robots and closed three stores in San Francisco recently.

The brightest stars of the IPO pipelines might be able to go public this year, but at a cut-rate price which is a tough pill to swallow for Airbnb and online delivery platform DoorDash.

With no new blood going live on the public tech markets, we focus on the ones already there and recent news is alarming.

Apple whose 42 stores in China have been closed since January and Foxconn, which produces Apple products, are running at around 30%-40% capacity, then it’s ring-the-alarm time.

The most likely scenario is that big tech will need to write off this quarter until the public health crisis improves setting up a bullish second half of 2020.

Even that could get stopped in its tracks.

The only silver lining is that the run-up in shares in January means that the best of tech has only returned one month of share appreciation, but for the weaker companies, they aren’t afforded those types of luxuries in malicious trading conditions and have returned 4-6 months of share appreciation already.

Mad Hedge Technology Letter

February 19, 2020

Fiat Lux

Featured Trade:

(BUY THE CORONA DIP),

(VZ), (T), (TMUS), (S), (AAPL), (BABA), (CSCO), (EXPE)

The coronavirus hammer finally came down and hit one of the dominant soldiers of big tech.

Apple (AAPL) led morning headlines nationwide by slashing quarterly revenue guidance stemming from production delays and weak demand in China.

Deleting the China demand for new iPhones is enough for the company to signal a looming revenue miss and rightly so, coronavirus has been 24-hour news for the past 2 months on the Asian continent.

As we speak, the cruise liner named the Diamond Princess is parked outside the port of Yokohama with the victims of infected rising by the day.

The optics are ugly, and China’s cover-up of the spreading went awfully awry and now pandora’s box is open.

Naturally, tech stocks can expect a few percentage points shaved off of this year’s annual growth targets and short-term sluggishness in shares exposed to China revenue.

What are the ramifications?

Telecom companies are in the incubation period of building out 5G wireless networks.

Naturally, tech shares will receive a bounce as network deployment gains traction as management commentary, during company earnings calls, on 5G business heats up.

However, the Mobile World Congress was cancelled by organizers stealing the chance for 5G stocks to hype up their position in 5G.

It is almost guaranteed at this point that China coronavirus will slow down the schedule for 5G wireless network buildouts.

Think about this, SARS lasted roughly half a year during 2002-2003, and the coronavirus appears to be worse than that.

Chinese telcoms will need to delay 5G and related equipment along with business that has around 150 million Chinese ensnared by the domestic quarantine.

Apple’s 5G iPhones in late 2020 could be delayed if there is no meaningful breakthrough in the contagion of the coronavirus and its ill effects on global business.

Apple stock appreciated on the hope that 5G iPhones aim to deliver the first meaningful consumer upgrade cycle in several years with a hefty price tag of $1,250.

This next generation iPhone could get pushed back to 2021 as Apple’s supply chain has been put on ice in mainland China.

If Verizon Communications (VZ), AT&T (T), T-Mobile US (TMUS) and Sprint (S) desire to aggressively expand their 5G networks, they might be in for a rude awakening because semiconductor companies might be stretched to limit and cannot provide the right components with supply chains pressured everywhere.

The truth is that supply chains are impacting diverse and interconnected sectors of the electronics industry.

And the epidemic, arriving at dawn of 5G's mainstream deployment phase, is guaranteed to disrupt the progress of the next-generation wireless standard, as the crisis slows the production of key smartphone components, including displays and semiconductors.

Chip companies and their shares have naturally been rocked by the recent news and they aren’t the only ones.

Expedia (EXPE), the online travel company, revealed it will avoid providing a full-year forecast as the online travel services company reevaluates the impact of the coronavirus outbreak on its operations.

Investors can imagine that on mainland China, the situation is grim exerting a fundamental impact on the country’s consumers and merchants and will slice off revenue growth in the current quarter.

Alibaba (BABA), the Amazon of China, told investors that the virus is undermining production and output in the economy because many workers are stuck at home.

The virus has also changed the commerce patterns of consumers by pulling back on discretionary spending, including travel and restaurants.

The Chinese e-commerce giant’s revenue surged year-over-year by an impressive 38% to 161.5 billion yuan ($23.1 billion), while net income rose 58% to 52.3 billion yuan, but that could symbolize the high-water mark.

Chief Executive Officer Daniel Zhang and Chief Financial Officer Maggie Wu were explicit in mentioning that risks from the pandemic could deaden a piece of revenue moving forward and they weren’t shy about stating this.

Sound bites such as “overall revenue will be negatively impacted,” and expecting growth to be “significantly” negative is quite black and white.

China is almost certain to print weak GDP growth numbers because of cratering imports and a big drop in demand.

Echoing Alibaba’s weakness was network infrastructure company Cisco (CSCO) with a revenue shortfall of 3.5% year-over-year as major product categories like Infrastructure Platforms and Applications were hit.

Cisco must find new cycles in core activities to regain any momentum and chip companies must do the same as the administration turns the screws on Huawei and injects more barriers to U.S. chip companies selling abroad.

This adds to the broader risks of elevated corporate debt and the upcoming U.S. election where tech management is nervous that a new President could throw big tech under the bus.

The coronavirus pours fuel on the flames.

The silver lining is the blows to these companies are softened by the ironic fact that big tech has become the safety trade to the coronavirus and even if 5G is delayed, chip stocks will eventually benefit from a fresh wave of revenue drivers when the 5G network is finally deployed.

However, it is way too early to announce the death of big tech, there are far too many secular tailwinds driving these companies.

The tech bull market is still intact and there will be opportunity to buy.

Mad Hedge Technology Letter

January 27, 2020

Fiat Lux

Featured Trade:

(HOW TO PLAY THE CHINESE PANDEMIC)

(TRIP), (TCOM), (GOOGL), (EXPE)

Am I going to rant about Peloton today?

No, I’ll save that for another day.

Let’s get straight to the chase – the epidemic from Wuhan is crushing tech stocks.

If you want a way to play the Chinese coronavirus outbreak, then look no further than Trip.com Group Limited (TCOM).

This company owns a series of reputable Chinese travel apps from Trip.com, Skyscanner, and Ctrip.com.

The Mad Hedge Technology Letter doesn’t tend to do tech alerts on Chinese companies listed in America as American depository receipts.

We rather not expose readers to the high risk of one of them suddenly being kicked off of one of the exchanges.

American investors have zero rights of recouping any losses if Alibaba or Baidu delists or even announces to switch its listing on the Shenzhen tech exchange.

Remember that founder of Alibaba Jack Ma signed over the PayPal of China Alipay to himself without even telling Yahoo about it.

Yahoo was also locked out of any profits from the decision as well even though they were seed investors in Alibaba.

That is China in a nutshell for you!

So what’s happening now? Tourists are staying home in droves and the ones that support the economy which are the Chinese ones during the peak travel season of Chinese New Year.

Cities are getting quarantined left and right in China and the mainland has ordered all travel agencies to suspend sales of domestic and international tours.

Chinese shares have felt the pain with shares of China Southern Airlines Co. – the carrier most exposed to the site of the outbreak – cratering 20% since the second death from the virus was confirmed.

If the situation unfolds like the SARS outbreak of 2003, things could turn bleak quickly.

Remember that in just one month of the SARS outbreak, Chinese air passenger traffic fell 71%, and Trip.com was rerated and has fell off the face of the earth.

I am predicting the same type of devastating numbers to the online travel world.

Trip.com has struggled to keep up with competition from digital rivals like Meituan Dianping and Alibaba, and even if the virus is conquered, business might never come back.

Despite the trade war and Hong Kong’s protests, the world has been held up by the Chinese tourist.

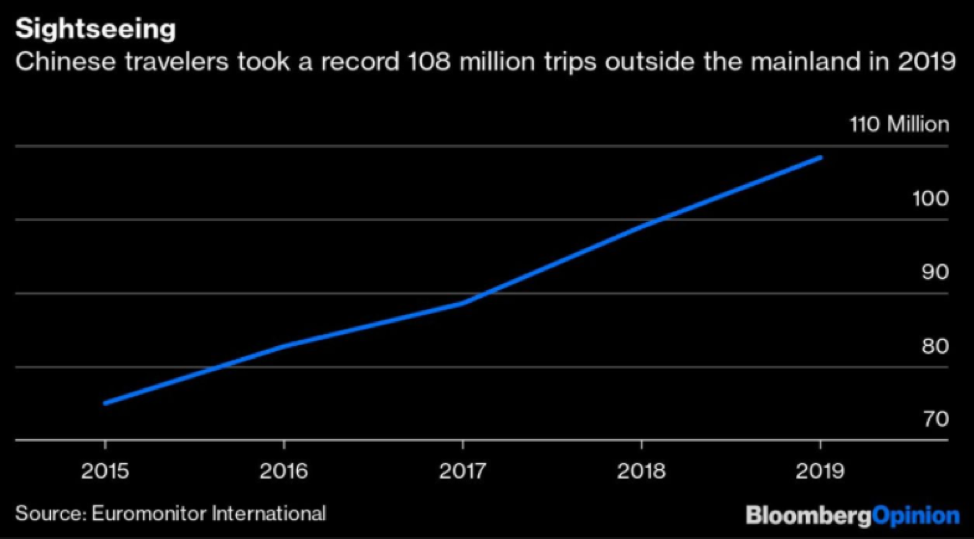

108.39 million Chinese overseas trips were taken last year, a 9.5% gain, after surging 11.7% in 2018.

Flight volume was brimming along nicely until the virus, but the hotel-booking sector is getting crowded.

Meituan Dianping has recently overtaken Trip.com as China’s top site, and now has 47% of China's market, 13% higher than Trip.com.

Now, Meituan is moving further onto Trip.com’s turf with luxury hotels, while chains like Marriott International Inc. are pushing for direct booking on their China websites.

Alibaba said part of the $13 billion it raised from its Hong Kong listing in November would go toward fliggy.com, its online travel group site.

The way the Mad Hedge Technology Letter is playing the sudden drop in overseas travel confidence is through the travel app I dislike the most – TripAdvisor (TRIP).

I actually don’t have a personal problem with the functionality, but the business behind it is terrible.

That was the main reason I strapped on a put spread and I can’t see TripAdvisor outperforming dramatically in the next few weeks in the face of a global pandemic.

This was a short-term trade that TripAdvisor won’t rise 11% in 30 day

I didn’t like this company before the coronavirus and now that Chinese tourists are home sitters for the Chinese New Year, this could put a dent into TripAdvisor’s new China initiative.

Trip.com Group had taken the lead in the day-to-day running of TripAdvisor China. It owns the majority share, with TripAdvisor claiming a 40 percent stake.

Chinese were supposed to increasingly travel the world while its customer base is also becoming more global, in particularly with Trip.com and Skyscanner.

But that is all on hold now.

Yes, it is possible that there could be a dead cat bounce in shares if the virus is tamed, but the 2-week travel season is something you can’t get back once it’s over for TripAdvisor.

I believe this will come out in the numbers along with details about Google’s algorithms further destroying TripAdvisor’s relevancy in the online travel industry.

Then take into account that the company just announced a 200-employee purge for the explicit reason of increased competition from Google and things seem to be going from bad to worse.

The company has done a proverbial deal with the devil by positioning itself to be utterly tied to Google’s search algorithm while Google is going head-to-head with them.

Google has upgraded its travel search tools recently to turn the screws on several trip booking websites like TripAdvisor, Booking.com and Priceline.

In its last earnings release, TripAdvisor noted that Google has placed ads at the top of its search results, forcing companies like it to buy more ads.

The company had a rough last quarter, reporting adjusted earnings of 58 cents a share, down from 72 cents a year earlier and short of analysts’ estimates of 69 cents.

Rhetoric from management was equally as disappointing with them saying, “Google (is) pushing its own hotel products in search results and siphoning off quality traffic that would otherwise find TripAdvisor via free links and generate high margin revenue in our hotel click-based auction.”

“Google has got more aggressive. We’re not predicting that it’s going to turn around.” TripAdvisor CEO Stephen Kaufer said at the time and I don’t see how our put spread will lose money in the short-term.

I will advise readers to take profits when the time comes. Be aware that TripAdvisor also has an earnings report coming up in 2 weeks that could gyrate the stock.

I expect broad-based weakness in guidance and poor performance last quarter in the report.

Mad Hedge Technology Letter

November 8, 2019

Fiat Lux

Featured Trade:

(WANDERLUST TAKES A HIT),

(TRIP), (EXPE)

I have slaughtered travel tech nonstop for quite a while now and today is the day that the bearishness turned ugly.

Let’s take a look at why.

I believe travel tech is a vulnerable group waiting to be taken to the emergency room.

We are approaching the dying embers of the economic bull cycle for better or worse, mostly the latter.

Europe is already mired in a recessionary-like environment and hiring has ground to a halt.

When German automobile manufacturers aren’t doing well, usually the rest of the continent follows suit.

No new jobs mean no new money to travel with and austerity usually whacks off luxuries like hotel stays and cross border travel.

Reading the tea leaves, it’s hard not to think that travel tech could be in for a rough next year with revenue growth sliding like Expedia’s vacation rental business in the third quarter.

The company is signaling slowed momentum in its high growth category leading to a lowered profit forecast for 2020.

The short-term rental unit reported revenue growth of 14% to $467 million, lower than the 17% rate in the previous period and missed analysts’ estimates of $462.4 million.

Total revenue grew 8.6% to $3.56 billion, in line with consensus but as we turn the page, there’s not much to like.

Expedia attempts to juice up home-sharing division, VRBO, in a quest to unseat rivals Airbnb Inc. and Booking Holdings Inc. in the booming home-share market will fall flat.

While VRBO is strong in the U.S. for purely vacation rentals, Airbnb and Booking capture a much larger share of the broader global $34 billion alternative accommodation market, which also includes non-traditional hotels and home-sharing.

Expedia is now set for 2020 adjusted Ebitda growth of 5% to 9%, down from a previous forecast of 15% growth.

VRBO only pulls in just over 10% of Expedia’s overall revenue, but its growth prospects revolve around this one asset.

To reach its targets, Expedia will need a greater dependence on higher-cost marketing channels in a secular flat hotel ADR (average daily rate) environment while grappling with the uncertainty around VRBO weathering a change in brand name.

Many tech companies are finding out that now is the wrong time to champion growth at any costs and travel tech is grossly reliant on exorbitant marketing costs to drive incremental home-sharing revenue.

I can’t say what TripAdvisor (TRIP) is doing is much better than Expedia because it is certainly not.

They have just announced a joint venture and global licensing agreement with China’s Trip.com Group which includes assets Ctrip, Trip.com, Qunar, and Skyscanner.

This is probably the worst time in the past 30 years for an online travel company to dive straight into China.

As I read through the detail, there was one red flag that stood out and that was the bit about “sharing inventory.”

I am doubtful that TripAdvisor is able to have an enforceable mechanism for misbehavior.

For example, if a hotel booked through TripAdvisor China is rerouted into the Trip.com portfolio and executed by the Chinese mainland array of digital assets, how would TripAdvisor respond?

There are too many lurking risks that could easily result in Trip.com Group gaming this agreement to tilt the benefits in their favor.

A cynical part of me tells me that this is just a ruse for Trip.com Group to use TripAdvisor’s brand name which dominates in western developed countries to siphon away foreign tourism revenue.

On a personal level, I have found that Trip.com Group has subsidized its prices which is a boon to consumers but is a way to undercut and pervert competition.

TripAdvisor can’t operate freely in China as it stands, but I wouldn’t desperately decide on a joint venture just to get a shoe in the door.

Better off looking elsewhere or keeping their ammunition dry.

Whether its weakness in VRBO in Expedia or a poor licensing agreement between TripAdvisor and China’s Trip.com Group, there is a lack of good ideas since Airbnb created this industry out of thin air.

Probably better to wait for Airbnb to go public if you want to get into travel tech, they have revolutionized the industry and are profitable or invest in Google who is stealing market share from the old guard.

The higher competition will certainly lead to higher marketing costs, lower growth, and a race to zero commissions.

Mad Hedge Technology Letter

May 15, 2019

Fiat Lux

Featured Trade:

(TRUE COST OF THE CHINA TRADE WAR)

(EXPE), (TRIP), (GOOGL), (CTRP)

As the trade misunderstanding escalates to a new stratum of ferociousness, certain parts of the economy are ripe to be battered.

Tourism and in particular, international travel, will be one of the first luxuries to be sliced off consumers' list.

China’s most popular online travel agent Ctrip.com (CTRP) has suffered a damaging drop in demand from would-be international travelers.

Jonathan Grella, spokesman at the US Travel Association said, “The US runs a US$28 billion travel and tourism trade surplus with China” and preliminary numbers appear that Chinese travel to the US in the past year has dropped around 20%.

Compounding the woes is the weakening of the Chinese yuan which could become collateral damage from the trade negotiations if American and Chinese corporations repurpose supply chains to other countries and stop sending dollars to the mainland.

The ball is already rolling with 93 percent of Chinese companies considering making some changes to their supply chains to mitigate the effects of trade tariffs in an ingenious way to circumvent extra costs.

Of these, 18% are open to a complete supply chain remake and production transformation, with 58% making meaningful changes.

A further 17% plan to make minor tweaks in response to the trade war, with only 7% making no changes at all.

Chinese and American companies are reconsidering their Chinese manufacturing bases to avoid the tariffs placed on US$250 billion of Chinese exports by US President Donald Trump.

The unintended consequence will be a powerful surge in economic activity in South East Asia with also India benefitting from the chaos.

Apart from the supply chain complexities, the worsening of Chinese yuan strength could put a massive damper on Chinese international travel plans.

The annual Chinese international travel growth rate of 5.5% would be in dire straits translating into current travel demand rerouted to lower margin Asian countries such as Thailand, Vietnam, and Malaysia which are quite popular for budget travelers.

If lower sales do not manifest itself because tourists opt to forego expensive western countries, this demand will correlate into fewer dollars per traveler because of cheaper destinations which might force companies to double down on promotions to lure higher volume.

The same goes for American consumers who will be on the hook for the tariff-loaded consumer items that trickle onto our shores.

Decaying relations have already poisoned the US tourism sector that’s seen its growth flatline for the first time in 10 years.

And while only a small percentage of the 80 million visitors to the US in 2018 were Chinese, the potential for that segment’s growth remains robust.

Only 6 percent of Chinese citizens have passports signaling an imminent rise in outbound Chinese tourists that will reach 220 million by 2025.

The opportunity cost of these dollars migrating to other locations will be a kick in the teeth.

I reiterate my negative call for American online travel companies with recent damage control coming from TripAdvisor for last quarter’s debacle when the company reported dismal top-line results combined with a drop in monthly average unique visitors.

The company’s first-quarter revenues of $376 million missed badly up against the consensus forecast of $386.8 million.

TripAdvisor’s quarterly revenues fell 1% YOY as a result of the core hotel business underperforming and revenues from TripAdvisor’s Hotels, Media & Platform (or HM&P) showing zero growth at $254 million.

Revenues from its fringe businesses, which includes rentals, Flights/Cruise, SmarterTravel, and Travel China, plunged 33% to $42.

The proof is in the pudding with the company’s falling unique visitor count putting the kibosh on TripAdvisor’s growth prospects.

The company’s average monthly unique visitors cratered 5% YOY to 411 million users in the first quarter, contrasting with TripAdvisor’s performance last year when it reported an 11% YOY unique visitor growth.

Google is the boogie man in the equation with the company rolling out a more holistic travel product to integrate flight and hotel search functions while organizing people’s travel plans and saving research.

Alphabet will also repurpose more travel data on Google Maps, and integrate hotel and restaurant reservations for customers who are logged on.

Linking the Google travel and map functions seem like a no brainer to me and will be the precursor before the company starts selling ads on Google Maps including travel ads.

Google’s pivot into online travel marks an existential crisis for the incumbents and will strengthen its position in travel by driving further searches and potential higher-qualified leads for its partner companies, such as airlines and hotels.

Consumers have already recognized Google as the go-to place where to do travel research.

In a zero-sum game, Expedia (EXPE) and TripAdvisor (TRIP) will directly lose out.

Highlighting the erosion was Expedia’s super growth asset Vrbo whose gross bookings totaled $4.16 billion, up a paltry 5 percent from a year earlier.

The growth rate was less than half of the main online travel agency business which should sound off alarm bells.

As it stands now, Google generates referral traffic although it does process some bookings on its own site for other travel merchants.

Unlike travel agencies such as Expedia or Priceline, Google doesn’t directly sell travel products such as hotel rooms or airline tickets but that could change quickly.

This ties back to my continuing thesis of the low-value proposition of broker apps in the tech ecosystem, either there will be one with a monopoly, or a bigger fish will hijack their business model and become the new monopolistic dominator.

Such is the high stakes of Silicon Valley in 2019.