Global Market Comments

October 3, 2025

Fiat Lux

Featured Trade:

(OCTOBER 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CCJ), (CST), (SMR), (TSLA), (F), (GM),

(USO), (FCX), (GLD), (SLV), (OXY), (BRK/B)

Global Market Comments

October 3, 2025

Fiat Lux

Featured Trade:

(OCTOBER 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CCJ), (CST), (SMR), (TSLA), (F), (GM),

(USO), (FCX), (GLD), (SLV), (OXY), (BRK/B)

Global Market Comments

August 25, 2025

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or LEADING INTO A PUNCH),

(UUP), (AAPL), (GM), (F), (RKT), (PLD) (AMT),

(PEP), (DUK), (ZION), (IJR), ($SPX), (QQQ), (MS)

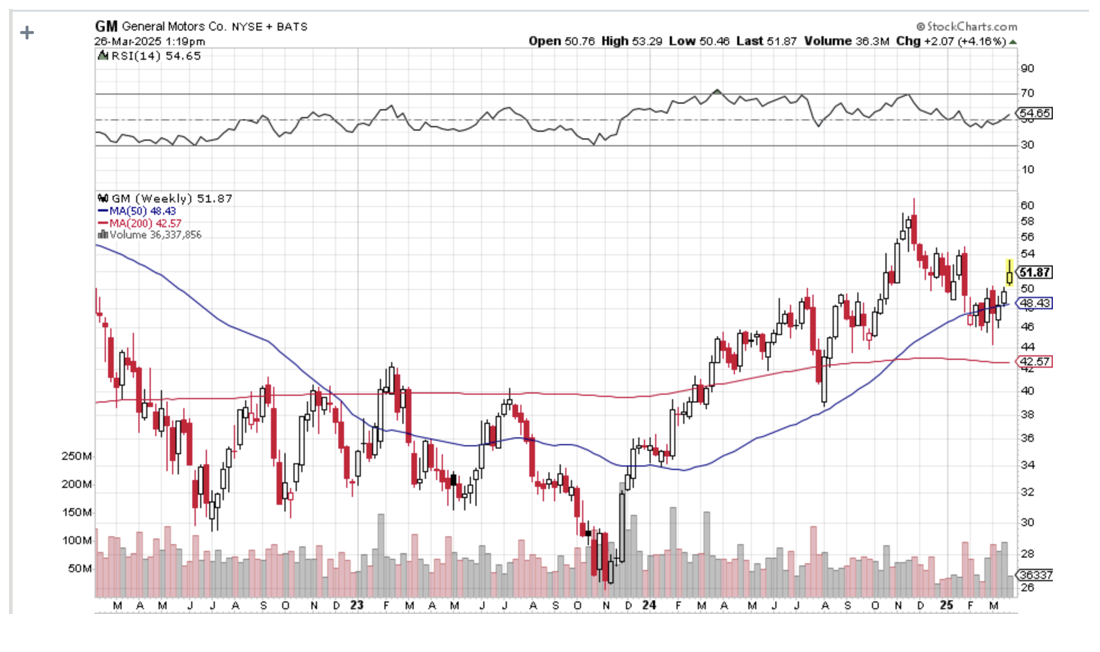

Global Market Comments

March 27, 2025

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

One of the most fascinating things I learned when I first joined the equity trading desk at Morgan Stanley during the early 1980s was how to parallel trade.

A customer order would come in to buy a million shares of General Motors (GM), and what did the in-house proprietary trading book do immediately?

It loaded the boat with the shares of Ford Motors (F).

When I asked about this tactic, I was taken away to a quiet corner of the office and read the riot act.

“This is how you legally front-run a customer,” I was told.

Buy (GM) in front of a customer order, and you will find yourself in Sing Sing shortly.

Ford (F), Toyota (TM), Nissan (NSANY), Daimler Benz (DDAIF), BMW (BMWYY), and Volkswagen (VWAPY), were all fair game.

The logic here was very simple.

Perhaps the client completed an exhaustive piece of research concluding that (GM) earnings were about to rise.

Or maybe a client's old boy network picked up some valuable insider information.

(GM) doesn’t do business in isolation. It has thousands of parts suppliers for a start. While whatever is good for (GM) is good for America, it is GREAT for the auto industry.

So through buying (F) on the back of a (GM) might not only match the (GM) share performance, it might even exceed it.

This is known as a Primary Parallel Trade.

This understanding led me on a lifelong quest to understand Cross Asset Class Correlations, which continues to this day.

Whenever you buy one thing, you buy another related thing as well, which might do considerably better.

I eventually made friends with a senior trader at Salomon Brothers while they were attempting to recruit me to run their Japanese desk.

I asked if this kind of legal front-running happened on their desk.

“Absolutely,” he responded. But he then took Cross Asset Class Correlations to a whole new level for me.

Not only did Salomon’s buy (F) in that situation, they also bought palladium (PALL).

I was puzzled. Why palladium?

Because palladium is the principal metal used in catalytic converters, it removes toxic emissions from car exhaust and has been required for every U.S.-manufactured car since 1975.

Lots of car sales, which the (GM) buying implied, ALSO meant lots of palladium buying.

And here’s the sweetener.

Palladium trading is relatively illiquid.

So, if you catch a surge in the price of this white metal, you would earn a multiple of what you would make on your boring old parallel (F) trade.

This is known in the trade as a Secondary Parallel Trade.

A few months later, Morgan Stanley sent me to an investment conference to represent the firm.

I was having lunch with a trader at Goldman Sachs (GS) who would later become a famous hedge fund manager, and asked him about the (GM)-(F)-(PALL) trade.

He said I would be an IDIOT not to take advantage of such correlations. Then he one-upped me.

You can do a Tertiary Parallel Trade here by buying mining equipment companies such as Caterpillar (CAT), Cummins (CMI), and Komatsu (KMTUY).

Since this guy was one of the smartest traders I ever ran into, I asked him if there was such a thing as a Quaternary Parallel Trade.

He answered “Abso******lutely,” as was his way.

But the first thing he always did when searching for Quaternary Parallel Trades would be to buy the country ETF for the world’s largest supplier of the commodity in question.

In the case of palladium, that would be South Africa (EZA).

Since then, I have discovered hundreds of what I call Parallel Trading Chains and have been actively making money off of them. So have you, you just haven’t realized it yet.

I could go on and on.

If you ever become puzzled or confused about a trade alert I am sending out (Why on earth is he doing THAT?), there is often a parallel trade in play.

Do this for decades as I have and you learn that some parallel trades break down and die. The cross relationships no longer function.

The best example I can think of is the photography/silver connection. When the photography business was booming, silver prices rose smartly.

Digital photography wiped out this trade, and silver-based film development is still only used by a handful of professionals and hobbyists.

Oh, and Eastman Kodak (KODK) went bankrupt in 2012.

However, it seems that whenever one Parallel Trading Chain disappears, many more replace it.

You could build chains a mile long simply based on how well Apple (AAPL) or NVIDIA (NVDA) is doing.

And guess what? There is a new parallel trade in silver developing. Whenever someone builds a solar panel anywhere in the world, they use a small amount of silver for the wiring. Build several tens of millions of solar panels and that can add up to quite a lot of silver.

What goes around comes around.

Suffice it to say that parallel trading is an incredibly useful trading strategy.

Ignore it at your peril.

Global Market Comments

February 14, 2025

Fiat Lux

Featured Trade:

(FEBRUARY 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(MCD), (FSLR), (META), (GOOG), (AMZN), (JNK), (HYG), (F), (GM), (NVDA), (PLTR), (INTC)

Below, please find subscribers’ Q&A for the February 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

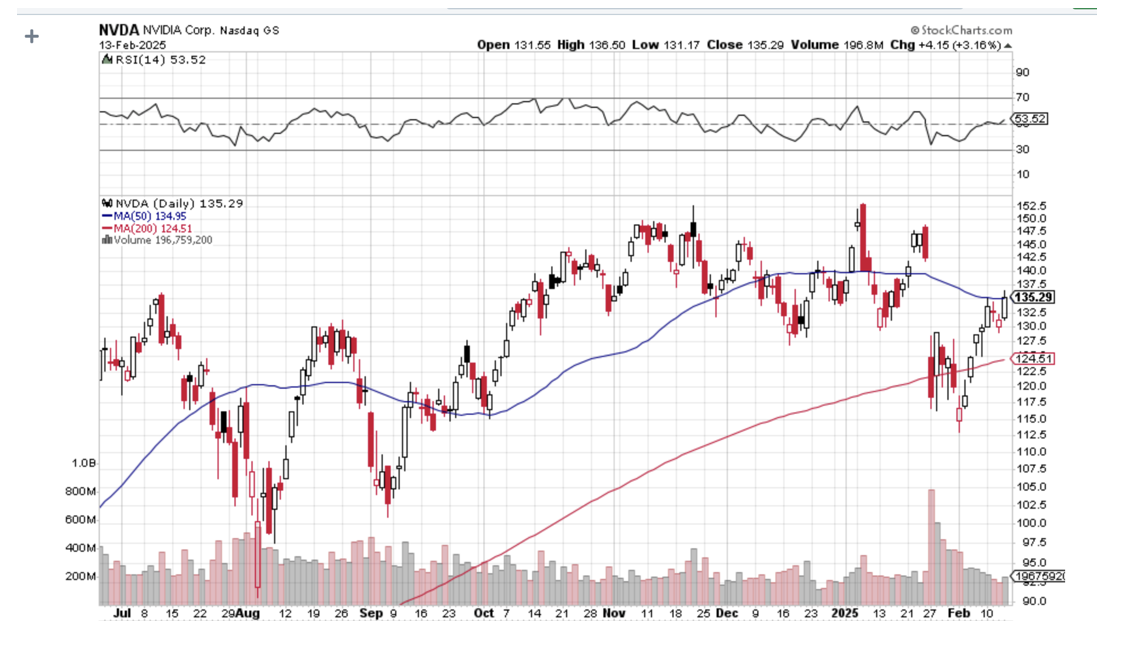

Q: Can Nvidia (NVDA) go to $200 in the next three years?

A: I would imagine probably, yes. They still have a fabulous business—enormous orders and record profits. But it's not going to happen in the next six months. You need to get us out of the current stock market malaise before anything moves dramatically one way or the other, except for META, which is at an all-time high. Their basic business is still great, and the threat posed by DeepSeek is wildly overblown.

Q: Why is McDonald's (MCD) seeing declining sales?

A: Partly, it's because they have been cutting prices. So, of course, that automatically feeds into declining sales. Also, I think the weight loss drugs Mounjaro or Ozempic are having an impact. People just don't go in and eat three Big Macs for lunch anymore. They may not need any Big Macs at all. And forget about the fries and the super-size high fructose corn syrup drink. When these drugs first came out, it was speculated that fast food companies would be the number one victim of these drugs, and that is turning out to be true. Some 15.5 million people in the United States suddenly aren't hungry anymore; they just take one bite of a meal and then push their food around the plate with their fork. That’s better than taking amphetamines, which people like Judy Garland used to take to lose weight. I think that will affect not only McDonald's, but all fast-food companies which I avoid like the plague anyway because my doctor says I shouldn't eat that food.

Q: Should I buy First Solar (FSLR) based on the revised higher sales outlook?

A: I don't want to touch alternative energy anything right now. I think the government will eliminate all subsidies for all alternative energy—be it solar, windmills, hydrogen, nuclear, whatever—and turn us back into an all-oil and coal economy. That is the announced goal of the new administration. So that eliminates the subsidies for sure. It certainly will be a blow to the earnings of all solar-type companies. If you are going to do an energy form, I would do nuclear, which benefits from deregulation, if that ever happens.

Q: Do price caps fix supply problems? Because Europe is thinking about capping energy prices in the short term.

A: Price caps never work, nor does any other attempt to artificially control prices, because all it does is dry up supply. If you cap the prices, and therefore the profits that energy companies can make, they'll quit. They'll abandon the energy business, or they'll pare it down, or they won't expand. One way or the other, you reduce the return on capital. Capital is like water; it will go where it gets the highest return, and price caps certainly are not part of that formula. But what do I know? I only drilled for natural gas for six years.

Q: What's your top AI choice?

A: Well, I would say it's Nvidia (NVDA) still, and the big AI users which include Meta (META), Google (GOOG), and Amazon (AMZN). Nothing has changed here.

Q: Is there any chance that Ford Motors (F) will be bought out anytime soon or never?

A: My view of all of the legacy car companies, including Stellantis, which is the old Chrysler, Ford (F), and General Motors (GM), is that they are basically giant mountains of scrap metal and only have a scrap metal value, which is about 5 cents on the dollar. That's what they fell to in the 2008 financial crisis, and all of them except for Ford went bankrupt. So I am not a big fan of the legacy auto industry now. And now, they have a trade war. They happen to be one of the biggest victims of trade wars because to stay competitive with Tesla, they moved a lot of their production to Canada and Mexico, and now those plans are going up in flames. So it seems like they're damned if they do and they're damned if they don't. I'm happy driving my Tesla, but I'm wondering if my next car is a BYD. Prices are so low, it might even be worth paying 100% duty just to get a cheaper car that has better self-driving capability. But the future is unknown, to say the least.

Q: Is the next big rotation out of Silicon Valley and into Chinese tech stocks?

A: Over the long term, that may happen, but with the current administration and China (the number one target in restraint of trade and trade wars), I don't want to touch anything Chinese. There are too many better things to do in the U.S. Imagine you buy a Chinese stock, and then the administration announces a total cutoff of trade with China the next day. Not good. Chinese stocks are incredibly cheap. Most of the big ones are now single-digit multiples compared to multiples in the 20s, 30s, and 40s for our stocks. But they come with a very high political risk, and that has been true for several years now. There are better fish to fry than in China. I'd rather buy Europe than China right now if you really do want to go international. But I have no idea why they're going up unless they're discounting an end to the Ukraine War.

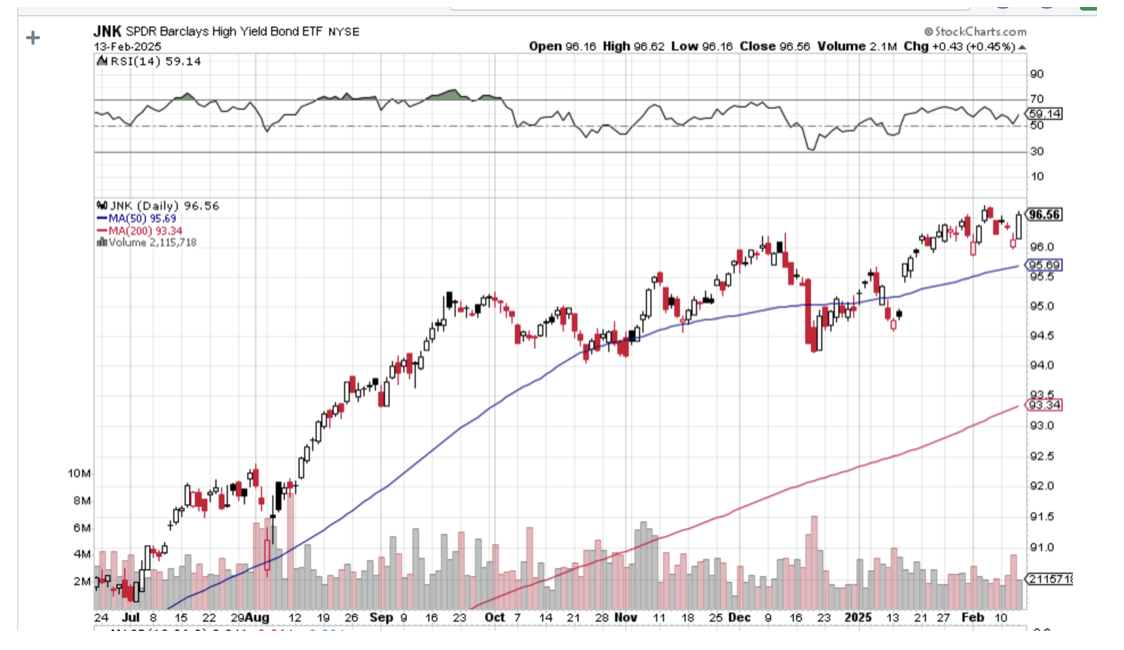

Q: Are junk bonds (JNK) and (HYG) a good play?

A: I would say yes. Their default risk has always been over-exaggerated thanks to their unfortunate name. They're yielding 6.54% and change, but it's a very slow mover. If we do get any improvement, any economy without inflation junk will go to $100. It's currently around $96. And you know, yield is a nice thing to have these days since the capital gain side seems to have dried up and turned into dust on almost any asset class.

Q: How can I decide when to sell the stocks that we bought on your recommendations?

A: Well, our trade alerts always have a buy recommendation and a sell recommendation or an expiration date. If you bought the stocks and kept it, just read Global Trading Dispatch for an updated market view. Watch our Mad Hedge Market Timing Index. When we get up into the 70s and 80s, that is definitely sell territory. It's hard for individuals to have an economic view going out to the rest of the year, but even the people who are economists have no idea what's going to happen right now. As I said, uncertainty is at an 8-year high, and that is being reflected in the market. So nothing beats cash, especially when you can earn 4.2% on 90-day US treasury bills. No one ever got fired for taking a profit.

Q: Can Intel (INTC) make a comeback this year?

A: No. I'm sorry, but they won’t. They had a horrible manager. They dumped him after a couple of disastrous years. I knew he was a horrible manager. I fought off all the pressure to buy Intel. So far, that's working. I mean, the stock has been terrible, so it is very cheap, but there is no guarantee that they will ever recover and, in fact, may get taken over by somebody else. So—too many better things to do. I'd rather be buying more Nvidia right now at these prices than sticking my neck out and praying for a miracle at Intel.

Q: A couple of years ago, I bought a bunch of Palantir (PLTR) on your recommendation for the next 10 bagger. I now have a 10 bagger. What should I do?

A: You know, we did recommend Palantir about 10 years ago, and it did nothing for the longest time. And then last year, it just took off like a rocket—I think it's up 400% last year. Price-earnings multiples are insanely high now. So what I would do is sell half your position. That way, the remaining half is all profit. You're playing with the house's money, and you're reducing your risk in a high-risk environment. Sell half, keep the other half. If it looks like it's starting to roll over and die, then you sell your remaining half.

Q: What's your favorite currency this year, and what should we do about it?

A: My favorite currency is the US dollar. If we're not going to get any interest rate cuts this year, the dollar will remain the highest-yielding currency in the world, and then everybody wants to buy it. It's really that simple. It’s all about interest rate differentials. Everybody else in the world has low interest rates, so stick with the dollar and don't touch the foreign currencies yet.

Q: Inflation expectations have exploded higher in view of today's number. Do you expect it to get worse?

A: If the trade war continues, it will absolutely get worse. 25% price increases are inflationary—period. End of story. A price increase is the definition of inflation, and right now, we are increasing the number of countries subject to high punitive tariffs, not decreasing them. You can expect markets to worry about that. And even if they put a temporary hold on these, people are raising prices now. They are not waiting for the actual tariff to hit; they are front-running that right now. So if you don't believe me, go to the grocery store where prices are through the roof. I actually went to a grocery store the other day, and I couldn't believe what things cost.

Q: I'd like to hedge my Nvidia (NVDA) position with a covered call. Which one should I do?

A: Well, it's not actually a hedge. What a covered call does is reduce your cost price and increase income. Right now, we have NVDA at $135. If you shorted something like the February $145 calls, you might get a dollar for that. That reduces your average price by a dollar. If you shorted the March $145 calls, that'll bring in probably $5, reduce your costs by $5, or bring in an extra $5 in income. And if you keep doing this every month and Nvidia stays stuck in a range, you can end up taking $10, $20, or even $30 in premium income over the next six months. And I have a feeling that will be the winning strategy for the first half of this year, using rallies to sell covered calls. You really could get your average cost down quite a lot; that way, if we have a massive sell-off, a lot of that loss will already be covered. If we get a massive rally, your stock just gets called away, and you buy it back on the next dip. The only negative here is the tax consequences of taking capital gains on the call-aways.

Q: You mentioned that the US has a demographic problem coming up; how will that affect the market in the short term?

A: It doesn't affect the market in the short term. Demographics are a long-term game. You have to think in terms of a generation being the round lot, which is about 20 years. Suffice it to say, when demographics go against you, like they did in Japan for 30 years, markets are horrible. Demographics are going against China now, and you're getting horrible markets. Demographics are good now in the US because we have millennials just entering their peak spending years, and that's when economies boom, and that should continue up to 2030. That is how to play demographics, and we keep updated here, although the government has suddenly ceased making available all demographic data to the public—I don't know why, but it's going to make the science of demographics much more difficult to follow without the government data. I don't know why they did that. I don't know what they hope to gain by clouding the demographic picture. Maybe it has to do with the allocation of congressional seats to the states or something like that.

Q: Do you have information on how to place a LEAPS order?

A: Just go to www.madhedgefundtrader.com, go to the search box, put in LEAPS in all caps, and you will find an encyclopedia of information on how to do LEAPS or Long Term Equity Anticipation Securities.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 27, 2024

Fiat Lux

Featured Trade:

(WHY YOU MUST AVOID ALL EV PLAYS EXCEPT TESLA),

(TSLA), (GM), (F), (RIVN), (NKLA), (F-SRNQ)

Markets live on fads.

Once a certain investment theme takes hold, the imitators start coming out of the woodwork in droves.

In 1989, all of the largest Japanese banks stampeded issuing naked short put options on the Nikkei Average by the billions of dollars when the index was at an all-time high. The Nikkei then fell by 85% causing tens of billions worth of losses.

I remember signing the paperwork on a $3 billion deal for the Industrial Bank of Japan on behalf of Morgan Stanley. It’s been 35 years, and I’m still waiting for those investors to come after me.

Then there was the peak of the Dotcom Bubble in 2000 and no less than five online pet food delivery companies raised billions. (remember Webvan and those cute sock puppets?) Every one of them went under.

So, what has been one of the biggest fads of 2024?

That would be electric vehicles.

You no longer have to wear Birkenstocks, grow your hair long, and smoke pot to drive an electric car. They have become a major part of the American economy. According to Adam Jonas at Morgan Stanley, EVs account for 8% of the total car market today and will grow to 10% by 2025 and 25% by 2030.

I have been involved with Tesla (TSLA) since its earliest days way back in 2003. Then it was one rich man’s hobby, with technology that was a reach at best, and unlikely to ever see the light of day as a public company. There it remained for seven years.

Then Tesla brought out the Model S in 2010, which I snapped up as fast as I could, picking up chassis no. 125 at the Fremont factory. My signature is still on the wall there as are those for all of the first 125 buyers. Every time I pick up a new Tesla I check if it is still there.

If the Model S worked it had the potential to be a real car. If it didn’t, I would wind up with $100,000 worth of inert aluminum, steel, silicon, rubber, lithium, and copper with only scrap metal value.

The trials were then only just beginning for Musk. He faced nervous breakdowns, sleeping in factories, and SEC prosecutions. After a decade of abuse, suddenly everything clicked. Total Tesla production is now running at a 1.7 million vehicle annual rate. The shares leaped 180-fold to a split-adjusted $425 from their post-IPO low of $2.40. That move financed a lot of retirements among my readers.

I remember what Steve Jobs once told me; “Like many overnight successes, this one took decades to pull off.”

Suddenly, making electric cars looked easy. Raising money to finance them looked even easier.

The problem is that all the new EV entrants now have a hyper-aggressive Tesla to compete against. Tesla has already locked up long-term supplies of crucial commodities essential for EV production, like copper, lithium, and chromium for stainless steel.

It has a 66% market share. It was a lock on experienced EV engineering talent. It has a near monopoly with a 48,000-strong national charging network which Ford (F) had no choice but to sign up for.

The best competitors can hope for is to peel off experienced employees from Tesla at inflated salaries, and then get sued by Tesla.

Enter the hoards, which I list below, a roll call of the shameless:

Nikola Badger (NKLA) – Has a hydrogen fuel cell power source that hasn’t a hope in hell of ever becoming economic. As I never tire of explaining to investors, while electric power is digital and infinitely scalable, hydrogen is analog and isn’t. Maybe that’s why the stock has been a disaster. Too many unbelievable promises and no actual functioning model. Gravity was their only actual power source. It just announced a recall of its electric trucks because of a coolant leak in the battery that caused fires.

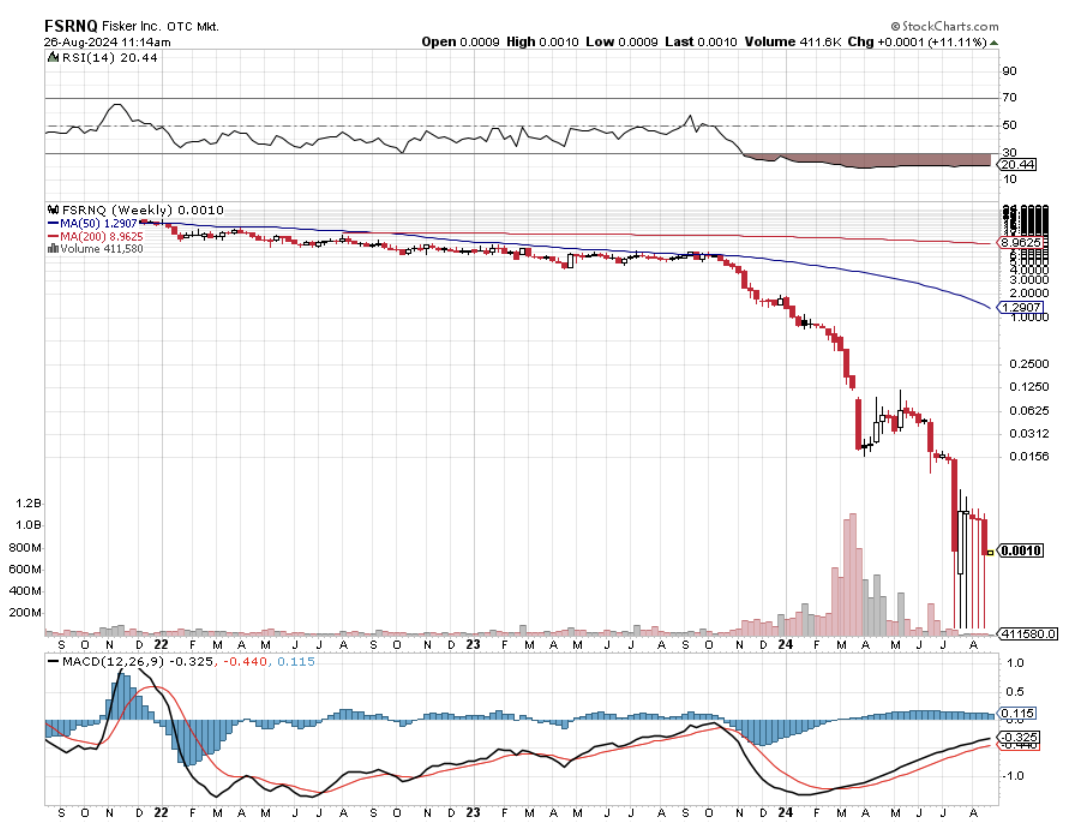

Fisker (F-SRNQ) – If at first, you don’t succeed, why not fail again? This VEHICLE had double the number of parts of a conventional international combustion engine. Its chief claim to fame was that it got a free factory from the government in Joe Biden’s home state and the fact that Justin Bieber drove one. More flailing at the wind. It recently went bankrupt….again.

Aspark Owl – A $3.2 niche supercar with an appeal to maybe three car-collecting Saudi princes.

Bollinger B1 – Is a $125,000 SUV expected from a Michigan startup with only a 200-mile range. Why not pay nearly double the cost of a Tesla Model X and get half the performance?

The Byton M-Byte – Is a $45,000 crossover car from a Chinese start-up. China has actually been building electric cars longer than Tesla, but they have a tendency to break down or catch on fire. Quality and safety problems have until now kept them out of the US, and probably always will.

Genesis Essentia – A Croatian-based start-up with a major investment from South Korea’s Hyundai. It will most likely never get off the drawing board. The last time Croatia built cars was for the Austria-Hungarian Empire during WWI.

Rivian R1T (RIVN) – A start-up with a reasonably priced truck and up to 400 miles of range that will only make it because they have a 100,000-unit order from the largest shareholder, Amazon (AMZN). It’s perfect for local deliveries. The cars are beautiful and there is a two-year waiting list for the $80,000 list price vehicles. (RIVN) is the only alternative EV maker that will probably make it.

By now, virtually every major car manufacturer has or is about to roll out its entry in the electric car race. I list them below, skipping those that are more than two years out over the horizon. Notice the profusion of the letter “e” in the names. In fact, there are an astonishing 527 EVs either on, or about to hit the market.

They include the Porsche Taycan, Audi eTron, Jaguar I-Pace, Austin Mini Electric, Fiat 500e, Kia Niro EV, BMW i3, Chevy Bolt EV, Hyundai Kona Electric, and the Hyundai Ioniq Electric, Ford F-150 Electric, Ford Mustang Mach-E, and Nissan Ariya.

Not one of these comes even close to the price/performance and battery density of the Tesla cars. Tesla is a decade ahead of the competition and is accelerating its lead. At best, they will sell a few electric cars to those who are intensely loyal to their brands and lose money doing it.

In the meantime, Tesla hasn’t been sitting on its hands. Elon Musk plans to bring out a $25,000 model in two years that will bar entry to the field from any other competitor. It has its own $250,000 supercar, the Tesla Plaid, which will go zero to 60 MPH in 1.9 seconds and has a 600-mile range. The Tesla Cyber Truck at $60,000 has the specs to take on the enormous US pickup market. Did I mention that the company is on the verge of developing technology that will improve battery performance by a staggering 20-fold?

So Tesla is branching out to suck up every profit in every branch of the entire global auto industry.

And this is what most traders, especially the short sellers, got wrong about Tesla. The data is worth more than the car. The miles driven provide a springboard from which the company can offer very high value-added and profitable services, like autonomous driving. Not even Alphabet (GOOGL) can replicate this.

When I bought my first Tesla more than a decade ago, I knew I was betting on the company. The big risk was that General Motors (GM) would step in with their own cheap electric car and drive Tesla out of business.

In the end (GM) did that, but too little, too late. Its Chevy Bolt EV didn’t hit the market until the end of 2016. Today it offers a boring design, lacks autonomous driving, possesses only a 259-mile range for $36,620, and is subject to recall, thanks to recurring battery fires (click here for the link).

The quality is, well, Chevy quality. The company has already announced it will discontinue production.

Tesla is approaching 2 million. It’s too late to close the barn door after the horse has “bolted,” as GM is earning. Over the past decade, Tesla shares were up 180 times at the high. GM shares are nearly unchanged during the greatest bull market of all time.

It is competing against Teslas that are 20 years from the future, are fully autonomous, go to street-autonomous driving next year, and upgrade itself once or twice a month.

Make mine Tesla, please, which will soon become the world’s first trillion-dollar car company. Don’t waste your time or money on the others, either as a driver or investor.

I’ll Go with Tesla

This earnings season is chugging along exactly like I thought it would play out.

The haves are covering for the have-nots.

Sadly, the pixie dust isn’t encompassing all tech stocks, but just enough sprinkles so investors don’t start selling.

That is what matters most and sure, investors can knit-pick all they want, but there have been just enough positive numbers to be repackaged as a win for AI and the advancement of tech even if the proverbial goalposts are widening.

Competition has reared its ugly head as tech services fight for the extra consumer and enterprise dollar in a global economy where demand is being squeezed by sticky inflation.

That’s not good news for many of the smaller companies that are unproven and tap debt by delivering a promising story to prospective investors.

Remember that Mr. Market is undefeated and price will always find its natural equilibrium.

The question is how long will it take to find that natural equilibrium?

Since 2020, many would say that the irresponsible monetary policy in many areas of the world has contributed to markets unable to match up buyers and sellers at a reasonable price.

There is some truth to that but let’s see who that benefits.

My belief is that strong tech companies have overly benefited from this type of fiscal backdrop because they can always fall back on a strong balance sheet like in Google’s case where it suddenly issued a dividend.

View it as a rainy day fund if you will where they can wield when need be.

The extra buffer zone of safety has allowed a company like Microsoft to focus on Azure growth, of which 7% was related to AI, up from 6% of impact in the previous quarter.

Microsoft provides cloud services for the ChatGPT chatbot from startup OpenAI, and companies have been increasingly adopting Azure AI services to develop their capabilities for summarizing information and writing documents.

It’s a good problem to have when capacity bottleneck cuts into the AI portion of Azure growth.

Companies tapping that AI story are the only tech companies in 2024 that Mr. Market is keeping safe and that must scare or enthrall you depending on who you are.

Meta (META) materially lifted its full-year capital expenditures guidance and signaled even bigger spending in 2025 — all because of unknown AI projects. Running tech businesses isn’t getting cheaper so imagine how small companies feel about that.

It’s Ford (F) losing lots of money on EVs because of higher-than-expected costs.

Meanwhile, IBM (IBM) CFO Jim Kavanaugh struck a more cautious note when asked about soft sales at its lucrative consulting business blaming the macroeconomic backdrop.

It’s not all smooth sailing in tech land and readers need to be vigilant.

It’s not the time to take some speculative Hail Mary on some far reach.

Don’t draft a 7th-round prospect in the 1st round.

Price action has been unkind to tech firms with poor balance sheets in 2024 and I believe that trend to continue until the Fed can finally tamper inflation back to reasonable levels.

Global Market Comments

March 22, 2024

Fiat Lux

Featured Trade:

(MARCH 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(DIS), (GLD), (BITB), (UUP), (FXY), (F), (TSLA), (NVDA), (FCX), (UNG), (TLT), (MCD)