A company such as Facebook (FB) simply must be on investors’ radar all the time because of the profitability element to it.

In a truncated period where growth stocks are out of favor, these bottom-line tech behemoths can weather the storm.

This tech firm doesn’t produce any real products because the user is the product.

A favorable expense layout is why net income this past quarter was $9.5 billion on $26.17 billion revenue.

Even a grossly profitable company such as Apple (AAPL) does a lot worse per dollar generated.

For every $3.79 billion in revenue at Apple, they only profit $1 billion, which is great compared to the status quo except Facebook.

Yes, it costs money to source raw materials and supplies to construct iPhones, iPads, and iMacs, which makes Apple’s operation much more impressive than Facebook.

Strip the hassle of making stuff like iPhones and iMacs and you have Facebook, an online portal to post stuff and serves no real purpose but to display ads to people.

Their attempts to get into the device and ecosystem games have utterly fizzled because users simply have no trust in Facebook management and how they fumble around personal data.

Why buy a Facebook Portal, the firms’ microphone video tablet, when there are trustful options out there without sacrificing the quality?

Before releasing the Portal, during the product announcement, Facebook initially claimed that data obtained from Portal devices would not be used for targeted advertising.

One week after the announcement, Facebook changed its position and stated that “usage data such as length of calls, frequency of calls” and “general usage data, such as aggregate usage of data will also feed into the information that we use to serve ads”.

So Facebook is quite stuck with what they have now, which is a blossoming Instagram and legacy Facebook portal both of which are cash cows.

They aren’t able to do M&A because of fear of anticompetitive legislation and their debauchery of privacy has locked them out of the hardware market.

Facebook wants to monetize WhatsApp, Facebook’s wildly popular chat app, but is finding resistance in funneling user data with an updated user agreement being criticized heavily worldwide with users deleting the app and downloading an alternative mainly the app Telegram.

Facebook rescinded the user agreement and has delayed their WhatsApp targeting ad division until they can ram the updated agreement down WhatsApp users’ throats.

I will say that “what they have” has been working out extremely well for the company when Facebook reported daily active users reaching 1.88 billion, up 8% or 144 million compared to last year.

Q1 total revenue was $26.2 billion, up 48% and this is attributed to growth in advertising revenue largely driven by continued strength in product verticals such as online commerce.

If investors don’t remember, Facebook was dragged down to the 20% revenue growth level just a few quarters ago on all the privacy hullabaloo.

To reaccelerate revenues is a major win for Facebook that can’t be understated.

Growth was broad-based across all advertiser sizes, with particular strength from small- and medium-sized advertisers.

Facebook’s year-over-year ad revenue growth also benefited from lapping pandemic-related demand headwinds experienced during March of last year. On a user geography basis, ad revenue growth accelerated in all regions.

Facebook’s bread and butter are the strength of their advertising revenue growth in the first quarter of 2021, which was driven by a 30% year-over-year increase in the average price per ad and a 12% increase in the number of ads delivered.

What is Facebook doing to branch out revenue channels?

They haven’t quit the hardware game with their Virtual Reality (VR) headset product called Oculus Quest 2 and management only played it down by saying they saw “sustained strength” without busting out any specific metrics.

I read the tea leaves as this isn’t doing enough for management to offer real data on it.

When I analyze the Oculus Quest 2 VR headset, the $299 retail price, it practically means they are losing money on it by a wide margin.

There is no premium in the pricing because the price is one of the few ways that consumers can overlook data privacy issues.

The $299 gets you a robust virtual reality headset with 6GB of RAM, a Qualcomm Snapdragon XR2 CPU, 64GB of storage, 1832x1920 per eye display, and a pair of controllers.

The jury is out whether the stickiness of VR will actually continue and if it does, how long full-scale adoption will take.

But it is painfully clear that Facebook will be losing money even on Oculus Quest products until there’s a 5th or 6th or even 7th iteration or even further.

There is nothing to suggest that VR is on the verge of full-scale adoption.

CEO and Founder Mark Zuckerberg must be tearing his hair out about how he has effectively been locked out of hardware products since the inception of his empire.

And no, data centers, their largest expense along with remunerations, to hold the data you give him don’t count as hardware.

A few headwinds to take note of, in the third and fourth quarters of 2021, Facebook expects year-over-year total revenue growth rates to significantly decelerate sequentially as they are facing tough comparable data from the prior year.

Lastly, Facebook will continue to expect increased ad targeting headwinds in 2021 from regulatory and platform changes, notably the recently launched Apple iOS 14.5 update, which will have an impact in the second quarter.

As the global economy and US economy open back up in a roaring fashion, it’s hard not to like this stock.

Ad budgets are on the verge of exploding and Facebook is still one of a nicely forged duopoly.

Even if they haven’t been able to branch out, they are incredibly proficient at what they do, and serving ads to a 2 billion plus user base will become more voluminous and expensive as the year advances.

No surprise the stock is at $325, another all-time high, and even if I personally hate the company, the stock is a viable candidate to buy on any dip.

As we move into the next part of the year, I do believe the buyback story will accelerate for big tech and cash cows like Facebook, and its stock will hit $400 by the year-end.

At the end of the day, this a story of the big getting bigger.

OCULUS QUEST 2 – THE NEXT DISASTROUS FACEBOOK HARDWARE?

https://www.madhedgefundtrader.com/wp-content/uploads/2021/05/fbhardware.png392658Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-05-03 14:02:532021-05-05 01:01:50Buy Facebook on the Dip?

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:04:402021-04-26 10:44:52April 26, 2021

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

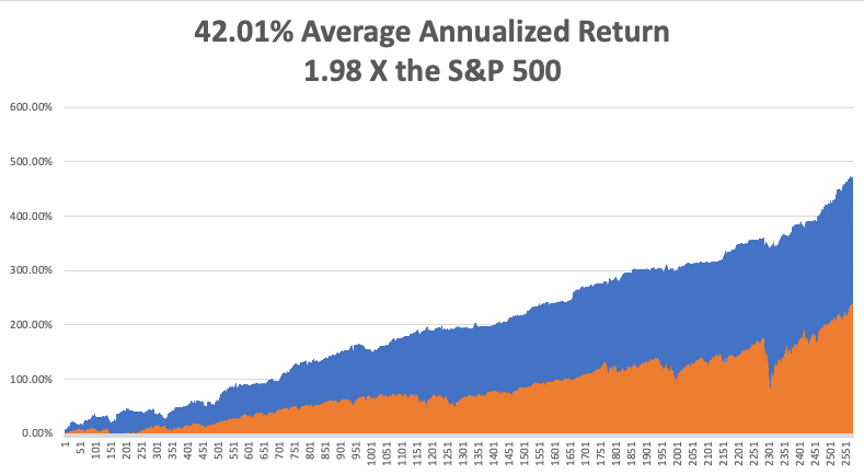

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & HealthcareLetter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-lakeshore-e1608229033313.png338450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-01 11:02:522021-04-01 14:14:23March 31 Biweekly Strategy Webinar Q&A

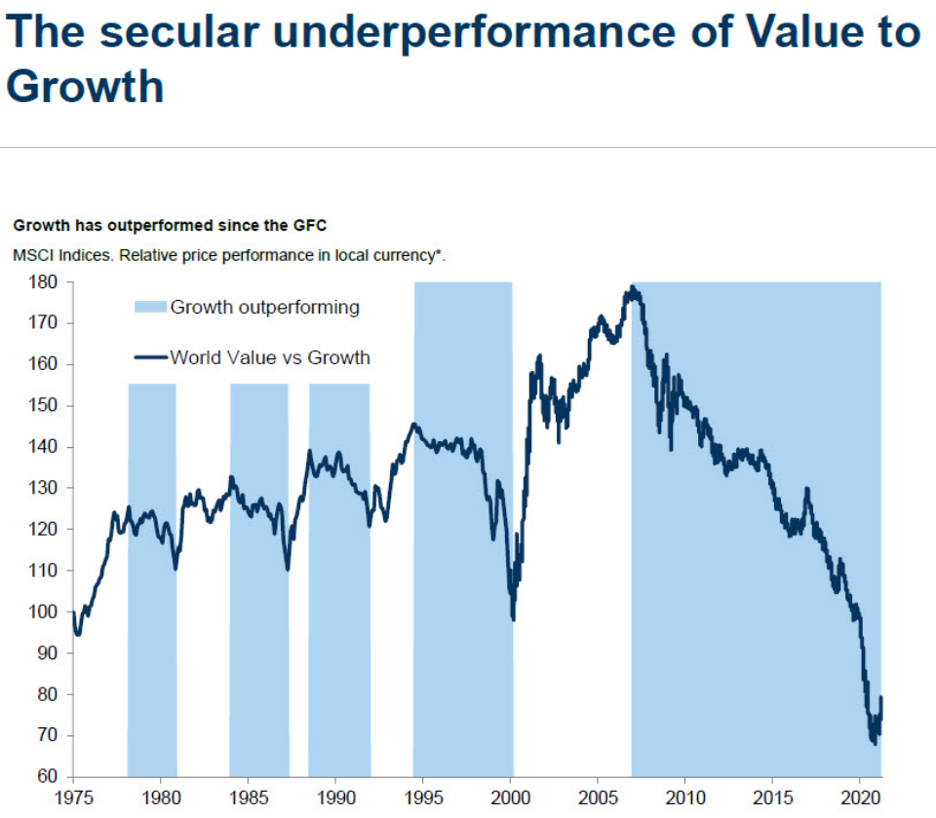

As we zoom out from tech, energy and industrials stocks have muddled through lately relatively well, while growth tech has been lethargic.

I cannot argue that we are in the middle of a rotation away from growth with capital migrating into value stocks.

Issuing low-interest rate corporate debt and spinning around to unload it to the debt market is advantageous because growth projects can be initiated without worrying about a crushing amount of future interest payments.

There is an expectation of three rate hikes by the end of 2023 which the market must absorb.

Then a mid-term expectation that the domestic economy will come roaring back is now penalizing expensive cloud services and digital communications stocks.

So now, here we are at a rock and hard place with growth with the broader market attempting to digest these roadblocks before the Nasdaq turns higher.

Just take a look at the ultimate growth stock Amazon (AMZN) or even Facebook (FB) to see a frustrating sideways consolidation from last September.

As much of this is quite disheartening for the tech investor, the tech sector remains one of the best places to look for companies creating innovative products and services that transcend industries.

I view this more as a buy the dip opportunity with the dip being elongated with numerous external events working against tech stocks.

So what are tech’s secular drivers?

According to IDC, investments in digital transformation will nearly double by 2023 to $2.3 trillion, representing more than 50% of total IT spending worldwide.

Deloitte recently released a report revealing that during the next 18 months, they expect to witness global companies embrace the bespoke-for-billions trend by exploring ways to use human-centered design and digital technology to create personalized, digitally enriched interactions at scale.

The study found that digital engagement was essential in 2020, with 96% of business leaders reporting companies who did not digitize customer engagement would experience severe negative repercussions.

These problems include a reduction in competitiveness and an inability to meet customer demands.

The companies who chose to embrace software agility meant empowering their developers to prepare tech firms for the unknown and meeting these customer expectations.

Whether it's a meteor hitting the earth, or anything else that is threatening to disrupt an industry or a business, the companies who do best can change on a dime to suit themselves for conditions in the current marketplace.

The health crisis accelerated transformation overnight.

Healthcare had to accelerate the adoption of telemedicine, and commerce companies accelerated their e-commerce plans.

The funnel that led to the consumer wallet has forever changed and in 2021, we will see further strength and momentum where we left off from last year.

Given the increased importance of digital engagement to the company's success moving forward, nearly all business leaders surveyed, 95%, expect to increase investment in digital tools after the pandemic.

Firms are now hyper-targeting a model revolving around customer engagement platforms that truly serve the end-to-end life cycle of all customer engagement in the enterprise.

Why? Because companies need to understand who their customers are, what products they're looking for, what products they bought, and where customers are interacting with their brand across multiple touchpoints.

Platforms allow the developers of the world to build, to take all of those bits of data that are siloed throughout the company to build a cohesive picture of the customer, build a world-class customer service experience and deliver the right communication over the right channel at the right time.

The endgame is to meaningfully improve every interaction every business has with every customer.

That's incredibly valuable to enterprises because it allows them to create differentiated customer experiences and all of the successful tech companies have participated in this trend.

I think that the infrastructure to build great digital products and great digital experiences spans many categories.

This rich area of opportunity will unlock developer influence and developers' ability in tech companies to build the future of these companies.

Now that every other company and industry needs tech to reach the end-user and to even initiate the selling cycle, tech is entrenched as the long-term winner.

Global business will cease to exist without software and no company will reach full potential without being powered by the best tech tools in the world, period.

And as the digital transformation is suppressed momentarily by external factors out of the control of the tech companies themselves, tech investors wait for signals for when the consolidation is over.

Tech already comprises 40% of the S&P, and by 2030, that number will be close to 75%.

This is still an industry that nobody should bet against in the long term.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/growth.png818936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-29 12:02:482021-03-29 17:31:59The Secular Tailwinds are Intact

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WAKE UP CALL),

(TLT), (JPM), (BAC), (C), (MS), (GS),

(JNJ), (AAPL), (FB), (AMZN), (GOOGL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-01 10:04:162021-03-01 10:17:47March 1, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.