Mad Hedge Technology Letter

October 14, 2020

Fiat Lux

Featured Trade:

(TECH OPTION VOLUME UNHINGED)

($COMPQ), (APPL), (FB), (MSFT), (GOOGL), (NFLX)

Mad Hedge Technology Letter

October 14, 2020

Fiat Lux

Featured Trade:

(TECH OPTION VOLUME UNHINGED)

($COMPQ), (APPL), (FB), (MSFT), (GOOGL), (NFLX)

The euphoria in big cap tech shares is the catalyst moving the Nasdaq index recently.

Call option activity is taking the top off of tech shares with usual low beta stocks surging over 5% in single trading sessions.

This unfortunately is causing our options trades to experience heightened stock volatility and the knock-on effect is our strikes getting blown out.

Some of the excess volatility comes down to traders making big bets in the run-up to the election.

Remember when Trump won in 2016, the market exploded higher when many “experts” guaranteed a massive sell-off would ensue.

In the short-term, the unsustainable pace of speculation in derivatives will translate into wild price swings. Monday brought the biggest rally for the Nasdaq 100 Index since April, but measures of volatility rallied as well.

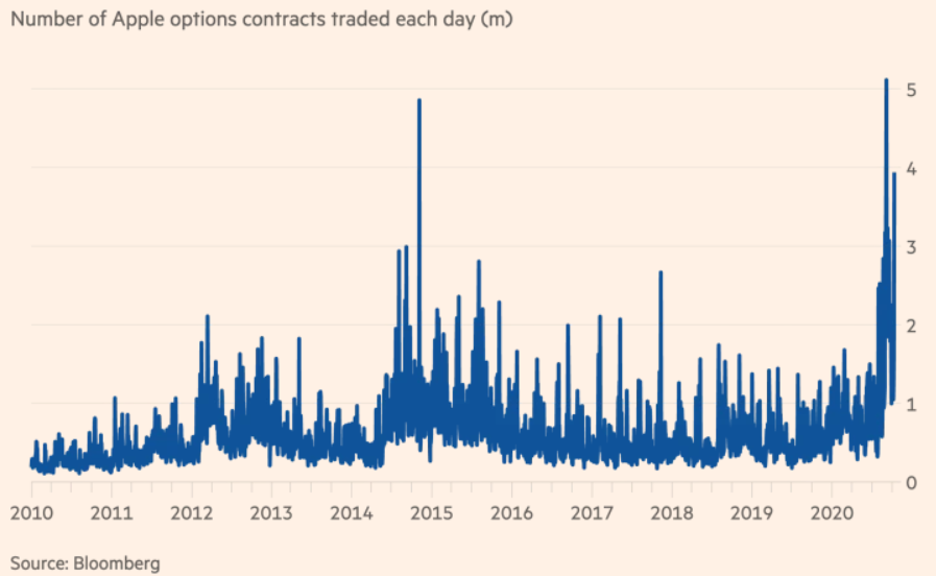

One proxy for the froth still latent in options, the percentage of overall volume represented by single-stock contracts, remains up 19% from a year ago.

Most of the action is concentrated in mega cap technology and momentum-driven shares.

A consensus is coalescing around a few big buyers coming into the options market to corner it with rumors of purchases around $300 million worth of call contracts on tech stocks in a single day.

The Nasdaq 100 Index has gained in all but two sessions this month and just notched its best week since July after last month’s sharp drop.

Whipsawing markets are also possible when liquidity remains thin.

Trading in options showed itself capable of influencing share movement in August and September when dealer hedging (demand from people who sell options for the underlying stock) created feedback loops that helped drive the Nasdaq higher.

That dynamic can also make sell-offs worse than they should be as well as sellers adjust positions.

Big trades in thin markets, especially in technology or momentum trades considered overbought or oversold, increase the potential for exacerbated stock moves as dealers hedge exposure.

Call open interest in Facebook (FB), Amazon (AMZN), Netflix (NFLX), Alphabet (GOOGL), Apple (APPL) and Microsoft (MSFT) has averaged 12.8 million contracts over the 30 days through Friday, the highest since early 2019.

The tech-heavy Nasdaq index has gyrated an average of 1.8% per day since the beginning of September, while the broader market gauge has fluctuated by 1.2% over that time period.

Recent options activity has been momentum-based, meaning that stocks tend to attract more interest in calls when it’s rallying versus when it trades lower.

Throw in structural forces that are contributing to a sustained high implied volatility environment, and election hedgers have their work cut out for them.

There are fewer short-volatility players as well in the wake of the health crisis.

There’s also less volatility selling by retail investors after the delisting of some popular VIX products earlier this year like the volatility ETF ticker symbol XIV.

It could take a few years for the imbalances to work itself through the system.

Then there’s the resurfacing of an event similar to the “Nasdaq whale” which is reported as Softbank acting like a hedge fund and buying as many big tech call options they could afford.

Softbank CEO has essentially turned his failed hedge fund named the Vision Fund from a start-up investor into a speculative hedge fund in risky option contracts solely betting on the rise of Silicon Valley tech in the age of the coronavirus.

After being burnt by Uber and WeWork, he finally decided to stay out of the messy acquisitions/seed funding and just speculative through derivatives from Tokyo.

The avalanche of options volume will no doubt cause the tech markets to become jittery and it certainly puts a floor under tech implied volatility for a while.

Retail investors have taken notice of this insane volume and largely stayed on the sideline.

At the apex of the madness, retail traders spent more than $511 billion in notional value on call options and that figure was slashed to $343 billion in the first week of October.

Retail traders tend to buy less-expensive short-dated contracts which tend to have greater convexity and ability to exacerbate share movements.

The level of risk-taking occurring in the public markets is at an all-time high.

Just look at America’s most elite university endowments who have slashed their exposure to the stock markets to the lowest levels since before the crash of 1929. And now they’re betting the ranch on secretive, illiquid, and high-risk private-equity funds and hedge funds.

A US teachers’ pension fund has sued Allianz Global Investors, accusing one of the world’s biggest asset managers of employing a “reckless strategy” that cost retirees almost $800m during this year’s market turmoil.

This is just one example of the high-risk strategies taking place with pension money.

In a lawsuit filed on Monday in New York, the Arkansas Teacher Retirement System claims that Alpha Funds, investment vehicles marketed by AllianzGI, had placed bets against an escalation of market volatility in an effort to recover losses they incurred from the same strategy in February.

So here we stand with derivative trading in tech options and general equity strategies leveraged to the hills that are betting on the system not breaking, or at least not breaking yet.

Even if the system reaches breaking point, many of these private investors are betting on governments to come rescue them perpetuating the feedback loop and offers a conundrum to savvy asset managers to miss or partake in the gaps up themselves.

Global Market Comments

October 9, 2020

Fiat Lux

Featured Trade:

(THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR),

(GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU),

(TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)

Global Market Comments

September 23, 2020

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (FB)

Last weekend, I had dinner with one of the oldest and best performing technology managers in Silicon Valley. We met at a small out of the way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables to meet current COVID-19 requirements.

The service was poor and the food indifferent as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information I had to promise the utmost confidentiality. If I mentioned his name, you would say “oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on this lowest of margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer who, once in, buys more services.

Apple (AAPL) is his second holding. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 40X. It now trades at 30X. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from up-front sales to a lifetime subscription model will also give it the boost.

Half of these are more than four years old, positively geriatric in the tech world. More than half of these are outside the US. 5G will add a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over the top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 21 Emmys this year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world. Tech growth will accelerate in 2021 and 2022.

5G will enable better Internet coverage for everyone and will increase the competitiveness of the telecom companies. Factory automation will be another big area for 5G, as it is reliable and secure and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government threatened breakups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies if its own, views big American tech companies simply as a source of revenues through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Facebook (FB) control 70% of the advertising market between them, which is inherently a slow-growing market, expanding at 5% a year at best. (FB)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised value tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings, it is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract services revenues from their cars, like Apple has. Tesla will grow revenues 30%-50% a year for the next two or three years. They should sell several million of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. But interest rates are much lower by comparison. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

When rates rise in a year or so, tech stocks may have to come down. They have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your shortlist for LEAPS to buy at the coming market bottom.

Mad Hedge Technology Letter

September 14, 2020

Fiat Lux

Featured Trade:

(THOUGHTS ON THE FUTURE OF U.S. TECH)

(AMZN), (GOOGL), (FB), (AAPL)

The world, technology, and U.S. economy are rapidly approaching a paradigm shift and investors will need to keep their finger on the pulse to adjust and adapt to the new normal.

This tech letter is about a recent note from Deutsche Bank that landed in my inbox and the contents are so pertinent that I must address it and what it means for the U.S. tech sector.

The note essentially said that the “era of globalization” is over and hunker down for the “age of disorder” where millennials are disenfranchised, poor, and largely disconnected from the financial benefits mostly harvested by the boomer generation.

The coronavirus has woken up the sleeping giant of Americas’ youth - they have come to grips that even though they use the flashy apps of Facebook (FB), Google (GOOGL), Amazon (AMZN) on their shiny Apple (AAPL) iPhone, they don’t exactly build wealth from these companies.

In fact, it’s the other way around.

According to Deutsche Bank, the next step in the development of the U.S. tech sphere is taking “revenge and redistributing wealth” from the old to the young.

The bottoming of tech stocks in March and the explosive price action have mainly benefited the shareholders who are from an older cohort and then the hardest hit was the youngest.

As Millennials start to grow in to positions of power, inheriting Apple or Amazon stock will most likely become costlier because the inheritance tax could balloon.

Boomers who mostly hold Congress seats have also stonewalled regulation on tech.

Tech, in fact, has the least amount of regulation out of any industry in the U.S. and nothing has been done to stop them from building up ironclad monopolies.

This could culminate in not only a tech tax on realized gains, but REAL regulation that won’t happen until political power is shifted over to the Millennials.

Climate change has been wreaking havoc in the Western region of the United States, but Deutsche Bank says that an even greater risk is the “intergenerational conflicts” that are about to explode.

The truth is that many young people feel alienated and stifled by the status quo as if the “establishment” is the only group in the U.S. that has benefited.

According to Deutsche Bank, Millennials also feel that the government is only working for corporations and the “elite.”

This data also doesn’t necessarily pinpoint one racial or ethnic group in the Millennial category but is a broad analysis that cuts across all shades of the spectrum.

As of July 2020, 52% of millennials were living in their parents’ home, up from 47% in February, according to the Pew analysis of Census Bureau data.

Young people simply cannot afford to live independently now.

If this power pivot does take place, corporate taxes will meaningfully go up, irrespective of what Biden does if he gets elected, and that is terrible news for the likes of Facebook, Google, Amazon, Apple, Microsoft, and so on.

These “redistributive policies” will be seen as a desperate act of saving Millennial’s financial lives as the increasing debt load will exacerbate inflation, meaning it will be more expensive each day to be an American wielding a weakening dollar.

The group of 7 big cap tech stocks will have to adjust to these new conditions, and clearly the riskiest company is Facebook who has been overstepping data privacy laws and destroying democracy for years.

These issues will finally be addressed when Millennials age into power.

Millennials are sure to take a hatchet to Boomers' pension benefits as the debt built up will need to be repaid and cuts along the financial chain must be accepted to the detriment of Boomers' inheritance plans.

It appears as if making money hand over fist, that mostly the Boomers enjoyed, will certainly be tested moving forward.

As the world quickly deglobalizes, tech companies won’t be able to outsource semi chips to Taiwan and assemble devices in China on the cheap.

These strategies must move inward and locally to support American jobs.

The inquest is out, and unfettered globalization and capitalism have been handed a guilty verdict by the Millennial generation.

The deeper ramification is that unfettered asset appreciation will likely be a relic of the past.

If you look at these tech charts, they basically appreciate in a straight line. Get ready for more zig-zags, and if regulation hits hard, we could also be facing zeroes in certain strategic tech firms.

Honestly, a company like Facebook doesn’t produce anything and is overvalued for it.

Then there is the issue of whether Millennials are content on the ever-growing problem of financing zombie companies that now comprise 37% of the S&P because of artificially low-interest rates.

Fed Governors like Jerome Powell will soon become obsolete and blamed in the history books for recklessness.

I define zombie companies as companies that cannot even pay back interest on debt let alone principal payments.

These companies are a serious drag on innovation because they perpetually fund companies that should not exist adding to the debt load.

The artificially low rates have boosted tech shares and broader markets for years along with the Trump corporate tax cut.

Buybacks will eventually become illegal because of the conflict of interests.

Just take a look at the big airlines whose management milked the cash cow and left the rainy-day fund barren to only get bailed out billions of dollars.

That won’t happen again.

Corporate funding will get significantly harder in the next year of corporate America. Investors should take note that management is rushing to capital markets to get every last penny of funding before the election because terms of financing could sour quickly in November.

US and China geopolitical relations will worsen and we are already seeing it play out as China has notified the U.S. that they would prefer TikTok to be deleted instead of generating a sale.

All Chinese tech apps will be removed, and Chinese tech companies won’t be allowed to list on U.S. public exchanges.

Don’t expect anymore “Chinese investment” into Silicon Valley for the foreseeable future, and that goes for education where the Chinese Communist Party has bought off Harvard University for a $1 billion.

U.S. Millennials now must compete with the Chinese government who are glad to fund their zombie companies in a race to the bottom.

This doesn’t exactly scream a higher-quality life for future Millennials exacerbating the problem.

Climate change is on the verge of compounding from bad to worse as California is grappling with not only apocalyptic air quality but a pandemic.

Who knows the next time anyone will be able to go outside in California?

Do you think rolling blackouts will encourage tech start-ups to continue operations in California?

Computers and internet don’t function without electricity – someone should tell California Governor Gavin Newsom.

Tech startups will never happen in California again, likely catalyzing a renaissance in zero state income states with cheap property markets.

Ultimately, we are currently in the midst of a technology revolution with astonishing equity valuations reflecting expectations for serious disruption to the status quo.

Call it a bubble or whatever you want, but the fragility of this bubble is real and we only need one external event for a major correction.

Then there is the thorny issue of whether markets will flip out over negative interest rates if that actually happens.

The report goes on to say that there is a “bipolar standoff as both the US and China seek to prevent encirclement by the other. Companies that have embraced globalization will be stuck in the middle if relations sour as we fear.”

It’s clear to the naked eye that the prior strategy of “scaling” a tech company like Facebook and Apple just won’t work anymore because so many territories will be off-limits.

Creating the next unicorn will be that much harder as many of the tailwinds boosting tech the last 25 years are on the verge of winding down.

As we enter this transition stage, I expect one of the big tech companies to falter through regulation or some other black swan event.

These developments favor active tech stock managers who must recalibrate daily according to wild swings that we will experience.

Buckle up because this will be a wild ride.

Global Market Comments

September 8, 2020

Fiat Lux

Featured Trade:

This isn’t the “Big One.”

This isn’t even a Middle One.”

This is no more than a 10%-15% correction typical for long term bull markets.

Sure, we saw every technical indicator known to man scream “SELL” in the run-up to the recent market top. There were other factors at play as well.

The bulk of the buying focused on only the top six stocks, more concentrated than seen during the Dotcom Bubble Top in 2000.

There really was only one buyer. That would be my friend Masayoshi Son’s Softbank (SFTBY). He bought $4 billion worth of big tech call options in the run-up to the top with an exercise value of $30 billion. When he started to sell last Monday, the market for these options vaporized and stocks plunged.

The fact that both Apple (AAPL) and Tesla (TSLA) shares split the same day also defined a market top that I have been warning readers about for weeks.

This is all in the face of the incredible reality that 50% of all S&P 500 (SPY) stocks are down over the past two years. It really has been a stock picker’s market with a turbocharger.

And this isn’t just any old bull market. We are in fact 11 ½ years into a bull market that started in March 2009 that has another decade to run. We have completed the first 400% gain. What lies ahead of us is another stock market increase of 400%, taking us up to 120,000 in the Dow Average by 2030.

And this is a bull market that has suffered plenty of 10%-15% corrections since its inception. The one that began in Thursday is no different. The sole exception to this analysis was the COVID-19-induced 37% meltdown that began in February. That little event only lasted six weeks.

For you see, the fundamentals have not changed one iota. No, I’m not talking about earnings, valuations, or sales growth. That is so 20th century.

No, I’m referring to the only fundamental that counts in the 21st century: Liquidity.

And liquidity isn’t shrinking, it is in fact increasing. That includes the unprecedented expansion of quantitative easing by the Federal Reserve, massive deficit spending by the US government, and zero interest rates, which Fed governor Jay Powell has promised us will continue for another five years.

During the last Dotcom Bubble top, the FAANGs and Tesla (TSLA) did not even exist. Apple was just coming out of its flirtation with bankruptcy and Amazon (AMZN) had just barely gone public. Google (GOOGL) and Facebook (FB) were still but glimmers in their founders’ eyes.

Except now we have a new bullish fundamental to discount: a Biden win in November. Since Biden decisively pulled ahead in the polls in May, the stock market has risen almost every day. He is 4%-10% ahead in every battleground state poll.

Even if Trump were to win every red and red-leaning state accounting for 163 electoral college votes, plus all 63 votes from toss-up states (AZ, NC, IA, FL, GA, OH), he would still lose the election, where 270 votes are needed to win. Just THAT is a 1:100 event, on the scale of Harry Truman’s historic 1948 compact, and Trump is no Harry Truman.

So what of Biden wins?

You can count on the $3 trillion stimulus bill passed by the House in March to go through, which primarily allocates money to keep states and local municipalities from firing policemen, firemen, and teachers.

Next to come are another $3 trillion in infrastructure spending. And I absolutely know from past experience that markets love this kind of stuff. It enhanced liquidity even more.

As I say, cash is still trash, and it may remain so for years.

The Top is in, with a horrific two-day 1,500-point selloff in the Dow Average ($INDU) coming out of the blue on no news and signaling the end of the current rally. Whatever went up the most is now going down the most as the Robinhood traders flee in panic. This was long overdue. Margin calls are running rampant.

Volatility (VIX) soared to $38, up 70% in two days, meaning that we may be close to the end of this correction. The (SPX) is down 24 points, 6.7% from the Wednesday high. The last (VIX) peak was at $44 in June and $80 in March. Time to start buying stocks for a yearend rally? Look at the banks.

Was Apple (AAPL) really up 400%? Did Tesla gain 500%? You might be fooled if you didn’t know that these stocks just split, Apple at 4:1 and Tesla for 5:1. In fact, both stocks posted robust gains in real terms, Apple up 5% and Tesla up 10%. Tesla just hit my five-year split-adjusted target of $2,500. Every other analyst had a much lower target or were bearish. Time to run a mile as splits often herald intermediate market tops.

Apple hit a $2.3 trillion in market cap at the peak, up a staggering $300 billion in days. We are truly in La La Land here. The price-earnings multiple has soared from 9X to 40X. That 5G iPhone better deliver. Didn’t you hear that 5G was causing Coronavirus, a popular internet conspiracy theory?

The Dow Average just lost its Apple turbocharger. Some 1,000 of the 2,000 points the Dow Average gained in August were due to Apple alone. With the Dow rebalancing today, with (XOM), (PFE), and (RTX) out and (CRM), (AMGN), and (HON) in, Apple’s influence has been greatly diluted. With the (VIX) back up above $26, the worst is yet to come. The stock market is screaming for a correction.

Copper (FCX) hit a new 3-year high, with demand soaring in China. They were the first to cap Covid-19 and restore their economy. The red metal is a great call on the recovery of the global economy. Those who bought the Freeport McMoRan (FCX) LEAPS I recommended in March are sitting pretty. The shares are up 228% since then.

Tesla to sell $5 billion in stock to finance the construction of new factories in Nevada, TX, and Germany. (TSLA) fell 5% on the news. I had been advising clients to sell all week. It won’t be a conventional secondary stock offering but an effort to sell into every stock spike. More proof that Elon hates Wall Street as if we needed more. With a market cap of $450 billion, investors are finally viewing Tesla as a data company rather than a car company.

US car sales recover to 15.2 million in August on an annualized basis. That brings us almost back to pre-pandemic levels. This is the best indicator yet that the US is returning to a semi-normal economy. Of course, zero interest rates and other unprecedented incentives are a big help.

Consumer Spending popped, up 1.9% in July, which accounts for two-thirds of the US economy. Those who have money are spending like there’s no tomorrow, and with a global pandemic, maybe there won’t be. New car purchases were a big winner as buyers take advantage of 0% financing everywhere.

Weekly Jobless Claims dropped to 880,000, still terrible, but less terrible than last week. California claims have topped 8 million since the pandemic began. Continuing claims drop to 13.3 million, down from the 25 million peak in May.

US Unemployment Rate plunged to 8.4% in August, from 10.2%. The August Nonfarm Payroll report jumps by 1.37 million. It’s a much faster improvement than expected. Retail gained 248,000, Education & Health Services were up 147,000, and Leisure & Hospitality were up 174,000, Government was up 344,000. It’s all thanks to the miracle of government spending. The Dow Average is down 500 points anyway.

China to dump US Treasury bonds in response to Trump's escalating trade war, putting $200 billion in paper up for sale. They hold $1.07 trillion in total and is our largest single creditor. The (TLT) is down two points on the news, where I am running a double short position. Who is going to fund America’s massive borrowing?

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch bounced back hard with some super aggressive buying of stocks right at the Thursday and Friday market bottoms and selling short of bonds at the top.

By going full speed ahead, damn the torpedoes, I brought in the best two-day return in the 13-year history of the Mad Hedge Fund Trader, up a heroic 8.27%.

It started out as a terrible week, getting flushed out of one of my short positions in the (SPY) for a big loss as the market hit a new all-time high.

Then I got long banks (JPM), Apple (AAPL), Amazon (AMZN), Visa (V), and went triple short bonds (TLT). I still retain one short in the (SPY), which is now profitable. I would have bought Bank of America (BAC) and Citigroup (C), but the market ran away before I could write the trade alerts.

The instant crash was yet another gift. Right after I shorted bonds, the Chinese hinted that they would unload $200 million worth of their US Treasury bond holdings. The harder I work, the luckier I get.

If these positions expire at max profit in eight trading days, I will be back at new all-time highs. Notice that I am shifting my longs away from tech and toward domestic recovery plays.

You only need 50 years of practice to know when to bet the ranch.

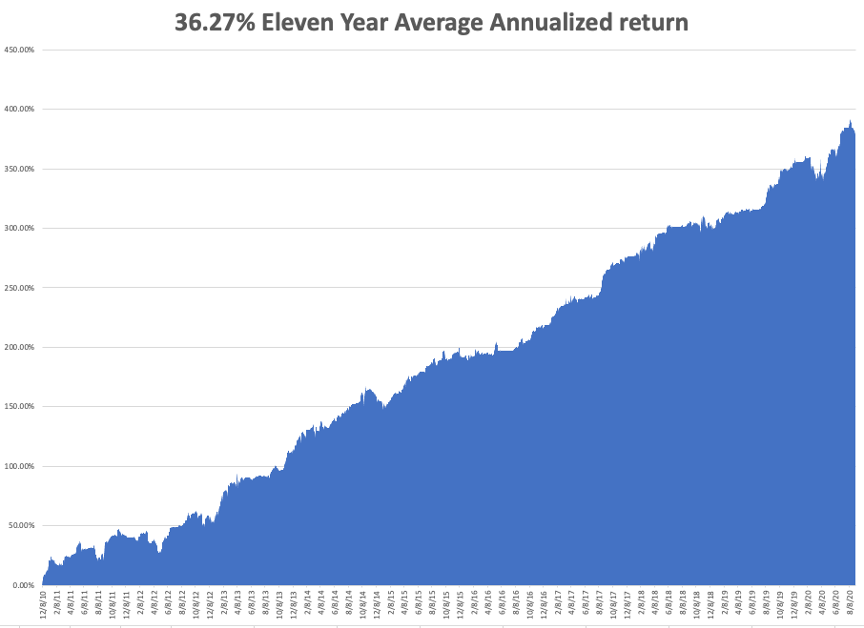

That takes our 2020 year to date back up to 30.99%, versus -0.70% for the Dow Average. September stands at 4.44%. That takes my eleven-year average annualized performance back to 36.27%. My 11-year total return returned to 386.90%. My trailing one-year return popped back up to 51.60%.

It is a quiet week as always following the fireworks of the jobs data.

The only numbers that really count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, September 7, it is Labor Day in the US, and markets are closed.

On Tuesday, September 8 at 10:00 AM EST, the Economic Optimism Index for September is released.

On Wednesday, September 9, at 8:13 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, September 10 at 8:30 AM EST, the Weekly Jobless Claims are announced. US Core Producer’s Price Index for August is also out.

On Friday, September 4, at 8:30 AM EST, the US Inflation Rate for August is printed. At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I am headed back to Lake Tahoe to flee the horrific smoke in the San Francisco Bay Area drifting our way from the rampant California wildfires. If people don’t believe in global warming, they should come here where we have it in spades. We’ll even give you some.

At least we’ve been getting spectacular sunsets.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 31, 2020

Fiat Lux

Featured Trade: