This could be the proverbial canary in the coal mine for the consumer falling off a cliff.

There have been soft signals showing that credit card debt is piling up, but the truth is that Americans are spending more money on things they need and not on luxuries.

Snap (SNAP) recording a disastrous earnings report is showing us rapidly slowing growth and digital ad spend is usually first to go in the broader economy.

This leading indicator is essential to understanding the economy because companies don’t and won’t advertise when they understand the incremental marketing spend won’t result in meaningful sales.

Companies are just losing money at that point.

What happens is just a complete freeze of ad spend only to hibernate until the next cycle picks up again and demand returns.

The same dynamics apply to the other digital ad players like Google (GOOGL), Facebook (FB), and Twitter (TWTR) which is why we are seeing 10% selloffs in Google.

The benefit to being such a big and strong company is that Google sells off by 10% while Snap drops by 45%.

Not exactly fair but long-term holders won’t dump Google right away unless there are real structural problems.

To break it down even further, the recession is quickly approaching and the economy is now going into reverse.

Next will be job layoffs and laid-off workers won’t buy much if marketed to.

Snaps’ macroeconomic environment has deteriorated further and faster than anticipated since its last earnings update just a month ago.

Digital ad spend goes quicker than local TV and radio following shortly after.

National TV was much later, and ad agency spend was also later than cycle media buying.

Roku and FuboTV will be hardest hit initially. The length and depth of the recessionary slowdown will determine whether or not pain makes its way to the longer cycle areas of the ad market.

In its first-quarter earnings disclosure in April, Snapchat’s daily active users hit 332 million, an increase from 319 million at the end of 2021.

Snap accounts for only a small low-single digit percentage of total digital advertising, but the macro factors cited should be relevant for all companies.

I believe the read-through is most negative for Twitter, which is 75% dependent on brand ad revenue and has 15-20% exposure to Europe.

Facebook also has significant European exposure (25% of its ad revenue), though its brand advertising exposure is likely well under 25%.

The Nasdaq continues to be a sell the rally type of market because there are no dip buyers.

For years, the dip buyers would save the Nasdaq.

Not only that, but the widespread destruction of tech has also forced many big whales to sit on the sidelines.

Why buy now when the risk reward isn’t favorable?

So now we are headed to a recession and traders are waiting for the recessionary data to flow to confirm these Snap earnings.

If this occurs, don’t be surprised to see a negative feedback loop that triggers algorithms to sell.

The Fed still hasn’t nearly been aggressive enough as well and is selling this false belief that there won’t be a recession and the consumer is strong.

That is yet to be priced into technology shares.

The upcoming data will reflect that the opposite is happening which means the buyer strike continues.

Avoid the dip and sell the rip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-25 15:02:342022-05-25 16:06:17Ad Marketing Craters

Below please find subscribers’ Q&A for the May 18 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: When do you see the banks returning to glory?

A: When recession fears go away, which should happen this summer. A recession will either have come and gone, or we will have confirmation by the end of summer that there is no recession in sight for the next few years at least. This will likely trigger a monster rally in the banks, which could all jump 50% from here. Obviously, Warren Buffet is putting his money where his mouth is by loading up on Citibank (C) yesterday. This would take us to new all-time highs by the end of the year. So, again, use these down-1000-point days to go cherry-picking among the generals who have been executed. If that’s not mixing metaphors, I don’t know what is!

Q: Should I listen to CNBC?

A: No, do not listen to the talking heads on TV. They are on TV because they don’t know how to make money. If they did know how to make money, they’d be locked up in a dark basement somewhere like me, grinding out millions for their firms. In fact, watching TV is the perfect money destruction machine because on down days, they bring out the uber bears, and on up days they bring up the hyper bulls. They are trying to egg you to get you to do the exact opposite of what you should be doing. They’re not interested in you making money; they’re interested in getting traffic on their websites and making money for themselves. CNBC can be highly dangerous to your financial health.

Q: Will we get stagflation?

A: No, because I think that once the year-on-year comparisons kick in—literally in a month or two—inflation will drop from the current 8.3% to down maybe 4% by the end of the year. That also is another factor in your monster second-half rally.

Q: Do you think the bounce in the market yesterday is the beginning of an upward trend or a dead cat bounce?

A: Definitely a dead cat bounce. I expect we’ll keep chopping around in the current range for the next 3, 4, and 5 months, and then we catapult into a monster year-end rally. That is a typical bottoming-type process.

Q: Is the wisdom “Go away in May” still alive or is your best bet that this year may prove different and the market goes up in the latter part of the year?

A: Actually, you should have gone away in November. That’s when all tech stocks peaked; only energy went up after that. If you’d gone away in November and said “come back in August” that would have been a good strategy because I think that’s when the year-end rally begins. If anything, May could be the bottom of the entire move.

Q: Is it time for LEAPS (Long Term Equity Anticipation Securities)?

A: Not yet—it’s too soon for LEAPS territory. You only want to do LEAPS when you are on a sustained long-term uptrend in a stock. We are nowhere near sustained anything, we are still in a bottoming phase, and could be there for months. At the end of those months is when we’ll be looking at LEAPS, where you can double your money every 6 months.

Q: Is it time to start nibbling on China stocks (FXI) now that COVID news is marginally better?

A: I’m going to avoid Chinese stocks because the American ones are so much better. You want to buy the quality at the discount, not the marginal, high-risk political footballs at a discount. And China will remain high-risk as long as they are abandoning capitalism. If you have to buy one Chinese stock, I would say Alibaba (BABA); you could get a double on that. But remember it is a high-risk trade—if the Chinese government wants to roll Jack Ma up in a carpet and kidnap him to Western Chinese re-education camp, the stock will get slaughtered. And that’s been happening increasingly with the heads of major companies in the Middle Kingdom.

Q: When this current route comes to an end, should we look to enter the market with 50% margin on stocks like Tesla (TSLA)?

A: It’s never sensible to go to 50% margin because if the stocks drop 50%, you are completely wiped out—you’ve lost everything. Plus, coming back from a loss is one thing; coming back from zero is impossible. So, I would not recommend that. You might do a safe stock like Apple (APPL), with a 2% dividend, and then at least you’re getting a double dividend. You only do the 50% margin on the safest, high dividend stocks.

Q: Amazon (AMZN) is on its way down. What is your expectation for the $3200/$3400 vertical bull call spread in January 2023?

A: I think you could make money on that. It may not be the full amount of the spread, but you’ll definitely get a big increase from current levels, because when we do get a second half rally, it will be tech-led, and Amazon has already had a horrific decline. What you might consider is rolling your strike down, taking the loss on the 3200/3400 and rolling down to like a $2,000/$2,200 in twice the size, and you’ll make your money back that way.

Q: For those of us thinking about LEAPS, how should we start to buy in—20, 30, 50% right now?

A: Well, first of all, you only do them on down days like today, when the market is down 800, and you scale in. 20% now, 20% higher or lower, and 20% again higher or lower. But you really want to be saving cash for days like this because You want to feel smarter than everybody else, and they absolutely will hit any bid on a down day, and that's where your LEAPS fills are really excellent, is on a down day like this.

Q: Can the Fed avoid another policy mistake? Because it seems that not only are they heading for high inflation, but layoffs are coming as well, and even with that I’m sure they will perform a soft landing of sorts.

A: For sure, when you take massive amounts of stimulus out of the economy, as we have in the last year, that is recessionary. In fact, the US government is close to running a balance budget right now because Biden can’t get anything through Congress other than money for Ukraine. Good for Ukraine economy, not for ours. And yes, they can do a soft landing, but has it ever been done before? No. Though this is the Fed that just keeps on surprising, so who knows. In the meantime, I'm willing to trade the ranges, and that may be all you get to do for a while.

Q: Target (TGT) shares are down 25%, as they cited higher costs that will result in rising prices for their customers. Would you buy the dip?

A: No, I generally don’t like retailers anyway. It’s a business that operates on a 2% profit margin. I like 40 or 50% profit margin businesses—those tend to be technology stocks.

Q: Would you buy retailers going into a recession?

A: No, that’s the worst thing in the world to own.

Q: Could Fluor Corp (FLR) be a Ukraine infrastructure stock?

A: Yes, once the war ends there will be a massive effort to rebuild Ukraine. Every company in the world will be involved, and Fluor and Bechtel will be the biggest, though Fluor is the only one where you can buy the stock. We already have the money to do this with all of the money that was seized from Russia. I predict discount sales on mega yachts.

Q: Why do you think all that money is going to Ukraine?

A: Because a weakened Russia is in the national interest of the United States, and it’s better that their soldiers are doing the dying than ours. I’ve done the latter and definitely prefer the former, using the other country's’soldiers as cannon fodder.

Q: On down days like today, should I be putting on one-month trades like the June options?

A: Yes, because the minimizes your risk and cuts the cost of mistakes. Waiting for the second half of the year when we get a prolonged uptrend to look at LEAPS—that is the correct way to do it.

Q: Over the next 12 months, do you think the S&P 500 will outperform Nasdaq?

A: No—for the next 3 months the S&P 500 will outperform NASDAQ. After that, NASDAQ will become an enormous outperformer for the rest of the decade. So, choose your entry points wisely.

Q: Do you think that housing is peaking out and will start to decline?

A: No, we still have a long-term structural shortage of 10 million homes in the US and I think we will flatline housing for years until we catch up with that shortfall.

Q: What are your thoughts on the Metaverse?

A: Too soon. Right now, the Metaverse involves spending only—no revenues. It could be years before you actually see any profits. So that’s why I'm avoiding Meta or Facebook (FB). But then, you could have made the same argument about the internet 25 years ago and semiconductors 50 years ago. If you waited long enough, however, you obviously made a fortune.

Q: China is hoarding 69% of their wheat reserves. Is this because they plan to invade Taiwan?

A: No, it’s because there’s a global food crisis going on. Many countries, like India, have banned exports of food to protect themselves. People miss this about China: China will never have a war or invade anybody, because the second they do, their food supplies get cut off by us, who are the world’s largest producer of food. Plus, their trade would get shut off to pay for it, so they can’t buy it from somewhere else, and that’s done with us also. So, they need to be in our good graces in order to eat. That's the bottom line and that’s why Taiwan will never get invaded. Russia’s economy can operate independently for a while, but China’s can’t.

Q: Is the baby food shortage further evidence of a food crisis?

A: No, the baby formula crisis is being caused by a monopoly of three companies that control 100% of the baby food market; and the largest of these companies, accounting for a 40% market share of the baby food making, is producing baby food that is poisonous. That's why they got shut down. This has been going on for years, and for some reason, they got a free pass on regulation and inspections by the previous administration, which is ending now, and all of a sudden we’re finding out that 40% of the country’s baby food is contaminated and is being pulled off the market. So, it really has nothing to do with the global food crisis. That’s more related to Climate change—surprise, surprise—as it’s not raining in the right places like California, the war in Ukraine, which removed 13% of the world’s calories practically overnight.

Q: Should I bet the farm here with the ARK Innovation Fund (ARKK)? I like Cathie Woods’ bet on innovation or five-year time horizon. It’s a great thing, don’t you think?

A: Not so great when you drop 70% in the last year. And it is a high-risk bet that of her ten largest holding companies, you only need one of them to work for the fund to bring in a decent return. Of course, you may have to write off nine other companies to do that. But yes, it’s a great thing to own on the way up, not so great on the way down. I know some people who started scaling into ARK in November and came to regret it. I would wait on it—this is your highest leverage technology play, and if you really want some punishment, there’s a hedge fund that’s bringing out a 2X long ARK fund in the next couple of months. Then it’s basically option money you’re throwing out. If you want to put some money in that, you could get a 10x on the 2x ETF if you’re playing a recovery in ARK. So watch it; don’t touch it now because ARK is having another heart attack today, but something to consider if you like gambling.

Q: I am full up with a thousand shares of PayPal (PYPL). It’s now down 76%. What should I do?

A: I recommend you learn the art of stop losses. I stopped out of this thing last fall, and it’s continued to go down virtually every day. Whenever you buy a new position, automatically enter into your spreadsheet your stop loss for that position. Because things can drop by 80 or 90% and you work too hard for your money to throw it away on these big losses.

Q: What do you think about Steve Wynn and Wynn Hotels?

A: I’d be buying down here down 62%; it was announced today that Steve Wynn has secretly been acting as an agent for the Chinese government where (WYNN) has a major part of its operations. Who knew? With all those high rollers being flown in on private jets from China, sitting at the tables in the closed rooms. So yes, this is a recovery play and it will do just as well as all other recovery plays, but remember it’s a China recovery play. And I think, in any case, his ex-wife owns a big part of the company anyway. So I don’t think Steve Wynn is that closely connected with Wynn hotels because of past transgressions with the female staff.

Q: Is it time to scale into Freeport-McMoRan (FCX)?

A: I’d say yes. On a longer-term view, I expect (FCX) to go to $100. And for those who have the May $32/$35 call spread that expires on Friday, my bet is that you get the max profit—but you may not sleep before then.

Q: What do you have to say about a post-Putin scenario and impact on the market?

A: The day Putin dies of a heart attack, you can count on the market being up 10%, if that happens right now—less if it happens at a later date. But it would be hugely bullish for the entire global stock market, and oil would also collapse, which is why I refuse to put on oil plays here. That is a risk. Putin can give up, have an accident, or get overthrown. When the Russian people see their standard of living decline by 90%, this is a country that has a long history of revolutions, putting their leaders in front of firing squads and throwing the bodies down wells. So, if I were Putin, I wouldn't be sleeping very well right now.

Q: What's the reason for air tickets (UAL), (ALK), (DAL) going up sharply?

A: 1. Shortage of airplanes 2. Soaring fuel costs 3. Labor shortages and strikes 4. It is all proof of an economy that is definitely NOT going into recession.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With Lieutenant Uhuru

https://www.madhedgefundtrader.com/wp-content/uploads/2016/12/John-Thomas-with-Lt-Uhuru.jpg353434Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-20 16:02:182022-05-20 17:37:50May 18 Biweekly Strategy Webinar Q&A

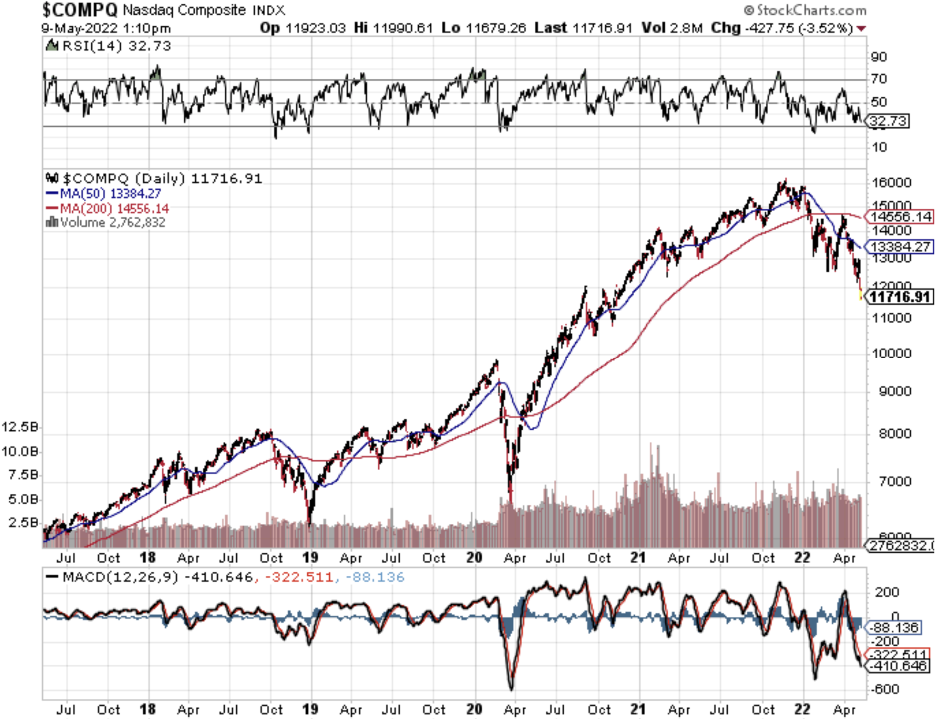

The buyer strike roars ahead as the 10-year U.S. treasure accelerates its rate of decline touching 3.2%.

We are dealing with a major deleveraging of the tech sector as a massive rotation flood into commodity-linked assets, the US dollar, and shorting bonds.

Sadly, we got another kick up the rear side when US Central Bank governor Jerome Powell committed yet another policy mistake by attempting to save the stock market.

Things could get ugly from here.

Many investors believed the Fed would self-correct after the “transitory” inflation nonsense.

It’s not so much the actual 3.2% rate today, but the velocity of the move which is creating many air pockets that are not being filled.

Why?

Investors are betting that Powell will most likely make a third policy mistake which could create another suicidal spiral downwards.

Investors have no incentive to buy stocks when the Fed has not only lost credibility but appears to not understand what is going on with real inflation tearing apart economic health.

This looks a lot like the 1970s just before former US Fed Chair Paul Volcker was brought in to slam the economy and raise interest rates to 18%.

Powell doesn’t seem like he has the guts to do that which is why the prolonging of this failed interest rate policy will mean a longer and more painful economic recession in the future.

I see many pundits going on record saying that the “risk reward has improved.”

Besides stating the obvious, this analysis doesn’t take into consideration that yields could go higher which would cause tech stocks to plummet further.

So yes, the risk reward has improved, but it can improve even more from here.

That doesn’t tell us much about anything.

All signs are now pointing to a souring paradigm shift among tech firms and dramatic changes under the hood.

Facebook (FB) is pausing hiring, a previously unthinkable prospect.

The company blamed macroeconomic challenges and Apple’s privacy changes for its slowest revenue growth in 10 years last quarter.

Almost 12 months after Apple launched App Tracking Transparency, a new analysis predicts its second year will still see big losses to advertisers on FB and YouTube and more collectively losing around $16 billion.

In total, FB will sink $10 billion into its new business with no revenue in 2022.

In February, Amazon (AMZN) announced it would raise its base pay cap from a maximum of $160,000 for most roles to $350,000.

The news comes after employees listed insufficient base pay as the second-most common reason they're looking to leave Amazon in an internal survey conducted last year.

I don’t have an issue with raising salaries, but AMZN had to boost it by far more than double showing readers the intense pressures on current expenses.

Even more problematic now is that new recruits won’t want to accept restricted stock options because of the tech selloff making their stock options less valuable.

Nobody wants to catch a falling knife, me included.

This will put more cash flow pressure on tech companies as new employees will reject stock options and demand a higher net cash salary.

The incremental micro negatives are causing tech companies to miss earnings and guide lower adding yet another negative layer to the grim outlook.

I would argue that even with earnings beats and positive guidance, the tech sector losses would be less.

However, we are experiencing a perfect storm of poor macro events and bad operational data.

Even though the risk reward has improved, it could improve more as the Fed will be forced to ratchet up rates more than expected to compensate for the latest policy mistake.

The market has sniffed this out and is unwilling to buy the dip until the Fed does what is necessary to seriously fight inflation.

The nonsense needs to stop.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-09 17:02:572022-05-09 17:26:13Buyer Strike Has Legs

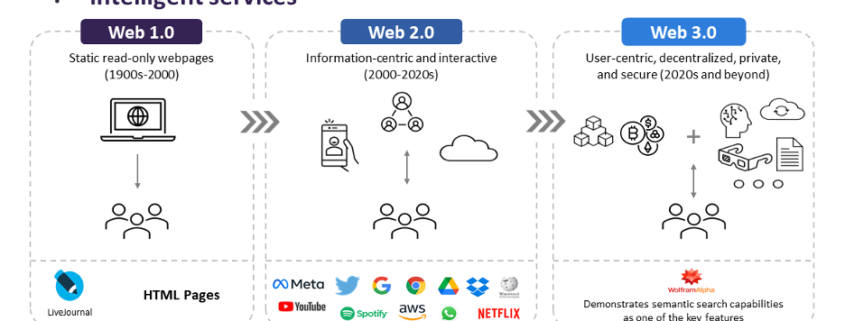

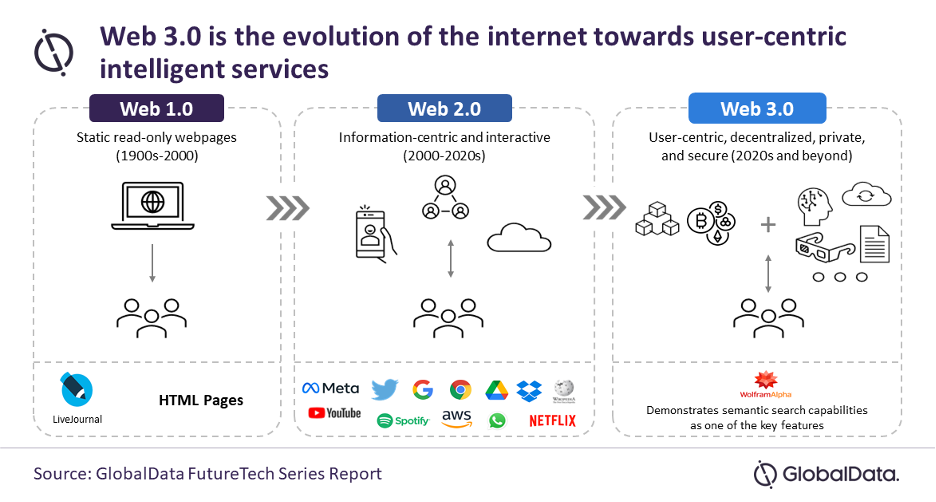

Advanced technologies such as cryptocurrencies and (non-fungible) tokens will play a leading role in Web 3.0, since they reflect a sense of ownership in decentralized blockchain networks.

Much of this is totally new and the programming and design behind it won’t be able to mesh well with what happened before.

Think of the latest hype of NFTs, or non-fungible tokens, which shifts the ownership of a certain form of money, which is the case with cryptocurrencies, to the ownership of many other digital assets, from artworks to memes and tweets.

Internet 2.0 programmers won’t be able to just seamlessly integrate into this new language and help develop this new world.

Web 3.0 enables the spread of cooperative governance frameworks for formerly centralized products.

There are few qualified Web 3.0 developers and they are able to ask for astronomical compensation for their service.

This won’t stop anytime soon as companies like Meta (FB), who have cash, are willing to throw money at this limited pool of developers.

There are many costs involved in being a Web 3.0 developer. The initial start-up cost is typically high, but this is offset by the increased flexibility it affords. As you build your portfolio of Web 3.0 projects, the costs will gradually decrease.

This technology would make the web more transparent and user-centric, while also opening the door for the blockchain. In the future, websites and apps could trade cryptocurrencies and other coins.

Becoming a Web 3.0 developer is not easy, but the rewards are well worth it. Those who have mastered the basics of the new framework can build an excellent website.

The cost of learning to become a Web 3.0 developer varies, but can be extremely high. After all, it takes a lot of time to build a successful business on this technology. There are also plenty of challenges involved with it.

The technology is not yet mainstream, but a handful of projects are attempting to build channels through the interoperability of blockchain networks.

You must have an understanding of web development, understand the trade-offs between different types of technologies, and be able to see trends and future directions in the industry.

A free course on Blockchain and cryptocurrencies can help you master the skills you need. Harvard University’s CS50 course will teach you the basics of computer programming, including data handling and Blockchain. Blockchain is crucial for Web3.0 developers because it is not only related to crypto coins, but can also run cutting-edge DApps and full backends.

The Web3.0 technology is a fast-growing field, and it is much like the dot-com era in the early 2000s.

A career as a Web3.0 developer is highly likely the best type of career to focus on for anyone getting into tech these days.

The risk-reward is skewed so much to the reward that many “full-time” developers are setting their workweeks at only a maximum of 24 hours per week or three days.

Not only that, web 3.0 developers are asking for starting salaries of $200,000 per year and if a company is interested in adding a 4th day of work, then that starting salary spikes to $300,000.

Remember these sums aren’t just it, these developers require a good amount of stock options.

Lastly, these web developers are refusing any job as “independent contractors” and won’t look at any offers that are anything other than a full-time employee with those implied rights.

Even under these terms, these web 3.0 developers have a line outside the door of companies willing to pay this type of compensation to get them in the door.

Web 3.0 is proposed to become the next iteration of the internet, but right now, the only people winning in this race are the people putting it together.

Until this new version of the internet comes online, companies won’t be able to fully monetize or onboard consumers.

This of course is important because crypto will be the medium of payment in this internet 3.0.

The lead up to that moment means that companies will need billions just to get a seat at the table.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/05/web-3.0.png502936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-05 15:02:192022-05-05 20:02:30Costs Spike for New Crypto-Supported Internet

It’s not that easy to make money in big tech these days – that is what the big takeaway was with the Google (GOOGL) or Alphabet earnings report that came out after the close yesterday.

The glory years are long gone.

First, it was almost like Groundhog Day with the Netflix-like streaming catastrophe that has now victimized yet another tech company.

YouTube competes differently with other streamers and is reliant on the digital ad model which is why an ad shows every 10 seconds when we watch YouTube.

I know it’s annoying but that’s how they grow revenue, and the blame was squarely attributed to China’s TikTok which is a short-form video platform eating everyone else’s lunch.

YouTube led all platforms in the first quarter of 2022 when respondents were asked which platform they used most often for mobile video, but YouTube dropped to 35% of respondents vs. 45% in the first quarter of 2021 while TikTok was #2 with 22%.

Besides, YouTube is literally entertainment, and with the health situation normalized again and the weather heating up, don’t blame others for grabbing a beer or two with their friends whom they haven’t seen for ages.

That clearly doesn’t help the YouTube ad revenue when people are out and about.

Google will need to deal with this TikTok problem because it’s real and it’s not disappearing anytime soon.

Google has a TikTok copy called YouTube Shorts and it’s not going that well if we compare it to TikTok which has surged to well over 1 billion subscribers.

If management allows the platform to get stale, it could become another dying tech company like Facebook.

The sum of the parts wasn’t particularly impressive either and that is weird to say based on Google’s history of outperformance.

Investors almost never see them miss on the top and bottom line and the EPS miss was not even close.

Things are getting more expensive for all of us, and Google just laid bare what we knew it our guts.

Just look at their research and development spend, it went from $7.5 billion to $9.1 billion which is a $1.6 billion increase in nominal spend.

They are also getting less revenue from Google Play which lowered developer fees to 15% or less for 99% of apps, down from 30% previously.

The bright spots were search advertising and cloud businesses.

Google Cloud has been growing quickly, but still remains unprofitable. It grew sales 43% for the first quarter to reach $5.8 billion, which was about in line with expectations. However, operating losses were wider than expected at $931 million.

Investing aggressively in the cloud is Google’s silver bullet, and that’s clearly having an impact in terms of the free cash flow numbers as well as the higher expenses and the margin compression we’re seeing not only in that segment but in the broader business.

Big Tech is decelerating, and external forces are magnifying the weakness in growth.

I do believe much of the negativity has been priced into GOOGL’s stock and this isn’t the case of a broken business model like Netflix (NFLX) or Facebook (FB).

I believe GOOGL shares will have a positive second half of the year.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-27 18:02:162022-04-27 20:48:49Google Lays an Egg

Mad Hedge Technology Letter

April 25, 2022 Fiat Lux

Featured Trade:

(HIGH STAKES OF TECH EARNINGS) (AAPL), (MSFT), (AMZN), (NFLX), (FB)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-25 16:04:112022-04-25 19:45:25April 25, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.