Twitter’s (TWTR) earnings offer a rough snapshot into the health of current internet users and Twitter pulling off a strong quarterly performance is a strong indication of how tech earnings as a whole will pan out.

Readers of the Mad Hedge Technology Letter know well that CEO of Twitter Jack Dorsey is one of my favorite tech CEO’s in the valley and I believe he should be leading Apple instead of Twitter and Square.

Twitter had an ideal quarter smashing estimates by surpassing every meaningful metric.

This company has turned the corner and has become the choir boy of social media in relative terms.

Purging the bots in the summer of 2018 was the right move in hindsight, and the performance in the first quarter vindicates Dorsey in making the tough decisions to clean out its system.

As Twitter grows in its Daily Active Usership (DAU), they risk becoming too large to regulate and grabbing back control over their model was the smart thing to do at the time.

Twitter has shifted from emphasizing Monthly Active Users (MAUs) to Daily Active Users (DAUs) in a sign of intent preferring to become integrated with users on a daily basis.

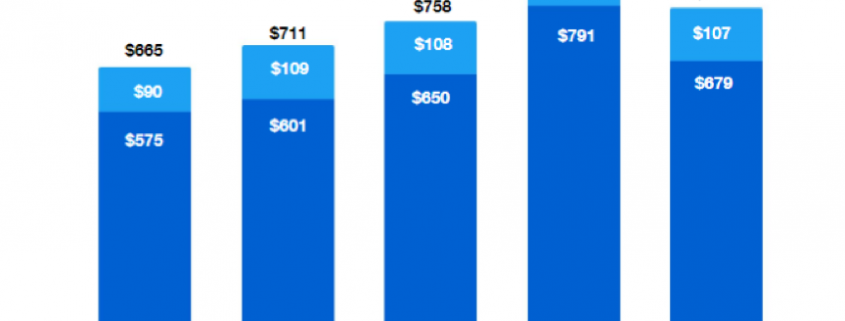

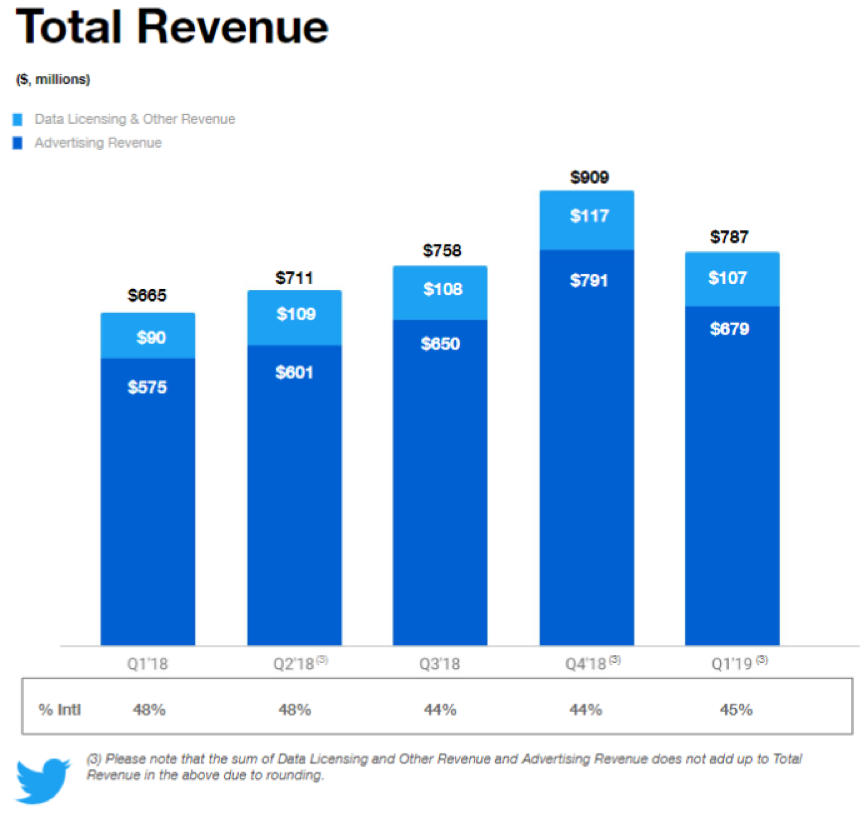

Total revenue of $787 million was up 18% YOY batting away any whispers that the company could be decelerating.

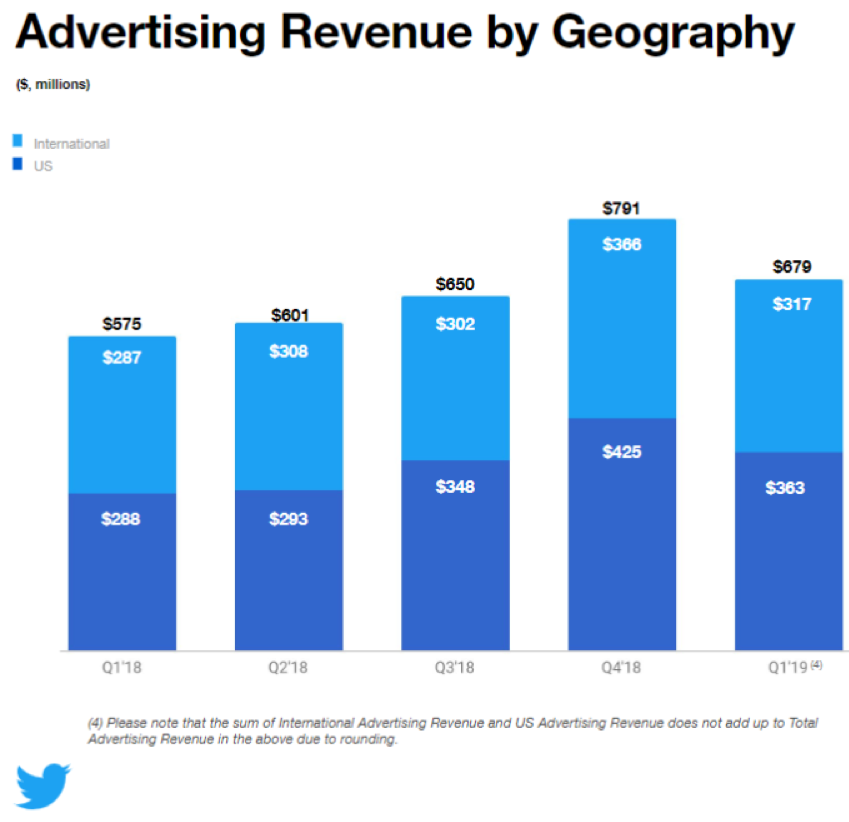

Another bonus was the diversity in ad revenue with 46% coming from the international segment signaling to investors that Twitter is not over-reliant on American Tweets.

American ad revenue rose 26% compared with international ad revenue rising just 10% showing that if you do social media properly instead of hatching cunning plans, it is still a growth business at its core.

The company has started to rev up profitability by reporting first-quarter earnings per share of 37 cents crushing the consensus of 15 cents.

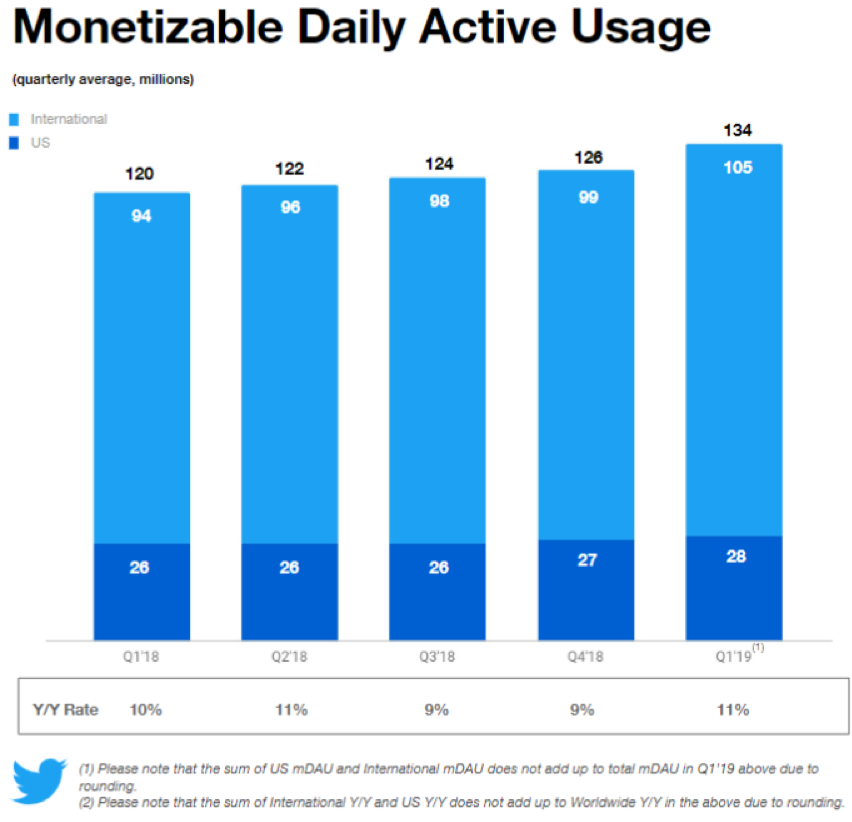

The healthy trajectory of the company is summed up by its rise in Daily Active Users to 134 million, an increase of 11% YOY in an environment where Twitter’s competitors aren’t growing at all.

The concerns that I had about last quarter’s tech earnings report had more to do with forward guidance than the past quarter’s performance because of the supposed deceleration of the global economy.

Twitter passed with flying colors predicting next quarter’s revenue should come in between $770 million to $830 million and operating income between $35 million to $70 million.

Dorsey sees no let down in the coming quarters as the domestic economy will attempt to push its way into its 11th year of expansion.

Headcount is estimated to rise 16% in 2019 after a 2018 where staff grew by 18%.

Total ad engagements increased 23% resulting from higher ad impressions and improved clickthrough rates (CTR) across most ad formats.

Cost per ad engagement (CPE) decreased 4% due to like-for-like price decreases across most ad formats because of an improved CTR which results in advertisers achieving the same number of engagements at a lower price, and a mix shift toward video ad formats that have lower CPEs and higher CTRs.

CPE can differ from one period to another based on geographical performance, ad formats, campaign objectives, and auction dynamics.

Just as important, the customer experience for advertisers is always improving with enhancements to Twitter’s ad platform and ad formats.

Twitter is committed to delivering better relevance making it simpler for advertisers to declare their objective, initiate a campaign, and measure performance.

The possible destructive black swan strongly hovering over social media and its business model is the threat of data privacy and the subsequent regulation to it.

Facebook (FB) and less so Twitter have been dragged into the data privacy debacle, but I believe Twitter has made the moves to get the monkey off their back for at least the next two quarters.

They have also benefitted from being more conservative in how they handle data and from the bulk of tweets being parts of public discourse instead of personalized baby photos.

The structure of Twitter has led to less chaos than Facebook, and Twitter tightening the amount of acceptable mainstream topics even more will close more loopholes into the extreme parts of society that want to disperse content through Twitter.

Twitter is taking a more proactive approach to reducing abuse on the platform and its effects in 2019 with the aim of reducing the burden on victims of abuse and, where possible, taking action before abuse is reported.

As a result, enhancements in Q1 revolved around proactive detection of rule violations and physical, or off-platform, safety — including making it easier to report Tweets that share personal information, helping Twitter remove 2.5 times more of this type of content.

Twitter has also deployed upgraded machine-learning models to detect potential policy violations enabling Twitter to pinpoint Tweets to agents for review, proactively.

The result is Twitter removing more abusive content with better efficiency.

The data backs up Twitter’s abuse prevention initiative with approximately 38% of categorized abuse proactively detected.

Twitter has been profitable for a string of quarters now, responded well to looming regulation fears, and as long as the economy chugs along at its current rate, I believe Twitter will outperform the rest of tech and the domestic economy.

The short-term health of social media also opens the path for Facebook to continue the positive momentum as the summer approaches.

Wait for an entry point on the dip to buy Twitter.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/total-rev-1.png816864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-25 06:05:272019-07-10 21:48:29The Resilience of Twitter

Netflix came out with earnings yesterday and revealed guidance that many industry analysts were dreading.

It appears that Netflix’s relative subscriber growth rate has reached the high-water mark for now.

Competition is rapidly encroaching Netflix’s moat.

In a letter to shareholders, management opined revealing that they do not “anticipate these new entrants will materially affect our growth.”

I am quite bothered by this statement because one would have to be blind, deaf, and dumb to believe that Disney (DIS) or Apple’s (AAPL) new products will not take away meaningful eyeballs from Netflix.

These companies are all competing in the same sphere – digital entertainment.

Papering over the cracks with wishy washy rhetoric was not something I was doing backflips over.

Netflix’s management knew this earnings report had nothing to do with results because everyone wanted to reassess how bad the new entrants would make life for Netflix.

Disney has the content to inflict major damage to Netflix’s business model.

The mere existence of Disney as a rival weakens Netflix’s narrative substantially in two ways.

First, Disney’s entrance into the online streaming game means Netflix will not have a chance to raise subscription prices for the short to medium term.

The last price hike was done in the nick of time and even though management mentioned it followed through “as expected,” losing this financial lever gives Netflix less ammunition going forward and caps EPS growth potential.

Second, another dispiriting factor is the premium for retaining and acquiring original content will skyrocket with more firms jockeying for the same finite amount of actors, producers, directors, and writers.

This particular premium cannot be quantified but firms might try to bid up the cost of certain talent just so the other guy has to foot a bigger bill, this is done in professional sports all the time.

Firms might even take actors off the table with exclusive contracts just to frustrate the supply of content generators.

Uncertainty perpetuates with the future cost of content unable to be baked into the casserole yet, and represents severe downside risk to a stock which trots out an expensive PE ratio of 133.

Growth, growth, and more growth – that is what Netflix has groomed investors to obsess on with the caveat of major strings attached.

This model is highly effective in a vacuum when there are no other players that can erode market share.

Delivering on growth justifies heavy cash burn, and to Netflix’s credit, they have fully delivered in spades.

The strings attached come in the form of steep losses in order to create top of the line content.

Planning to revise down annual cash flow from $3 billion to $3.5 billion in 2019 will serve as a litmus test to whether investors are ready to shoulder the extra losses in the near term.

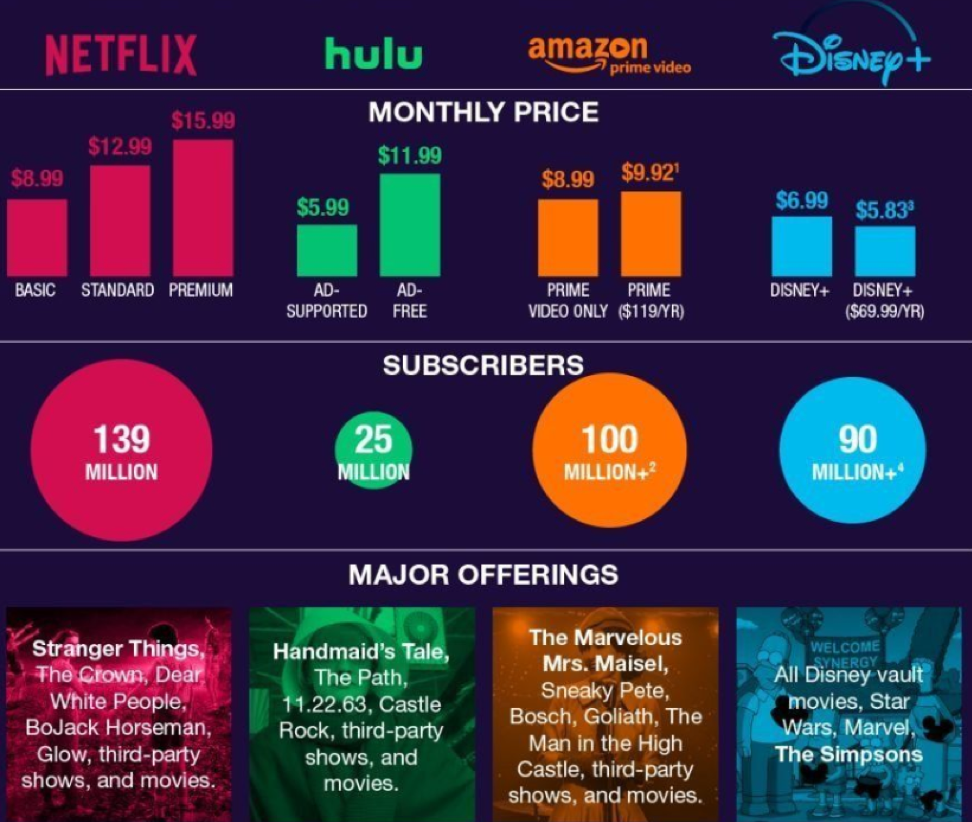

I found it compelling that Disney Plus will debut at $6.99 per month – add that to the price of Netflix’s standard package of $12.99 and you get a shade under $20.

Disney hopes to dictate spending habits by psychologically grouping Disney and Netflix for both at under $20.

The result of breaching the $20 threshold might push customers into ditching Netflix and sticking with the $6.99 Disney subscription.

Then there is the thorny issue of Netflix’s growth – the quality and trajectory of it.

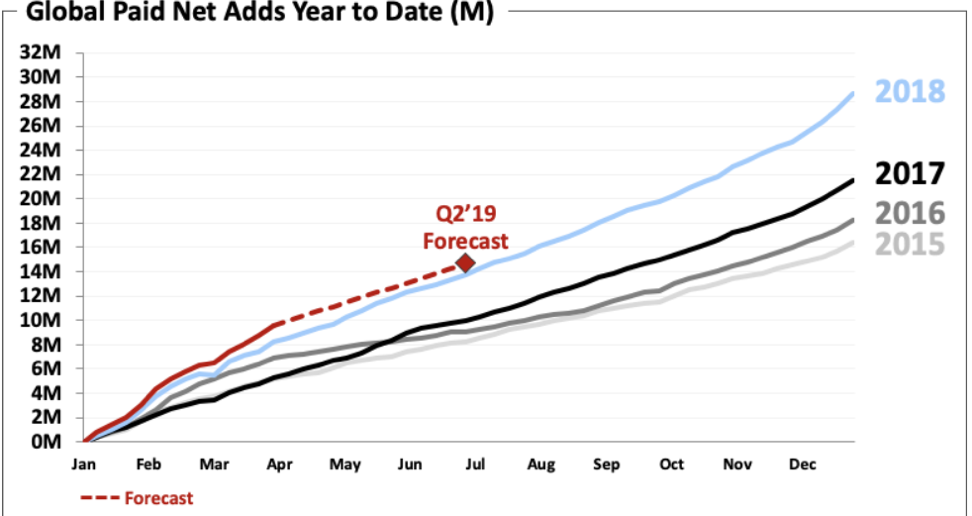

The firm issued poor guidance for next quarter projecting total paid net adds of 5.0m, representing -8% YOY with only 300,000 adds in the US and 4.7m for the international segment.

Alarm bells should be sounding in the halls when the most lucrative segment is estimated to decelerate by 8% YOY.

Domestic subscriptions deliver higher margins bumping up the average revenue per user (ARPU).

Contrast this with Netflix’s basic Indian package costing $7.27 or 500 rupees and a mobile package of $3.63 or 250 rupees.

In my opinion, domestically decelerating in the high single digits does not justify the additional annual cash burn of half a billion dollars even if you accumulate millions of more Indian adds at lower price points.

This leads me to surmise that the quality of growth is beginning to slip, and Netflix appears to be running into the same type of quagmire Facebook (FB) is facing.

These models are grappling with stagnating or slowing North American growth and an emerging market solution isn’t the panacea.

The Netflix Indian packages are actually considered expensive by local standards meaning that Netflix’s won’t be able to crowbar in price hikes like they did in America.

On the positive side, Netflix did beat Q1 estimates with paid net adds up 9.6 million with 1.74m in the US and 7.86m internationally, up 16% YOY.

Netflix was able to reach revenue of $4.5B, a company record mostly due to the $2 price hike during the quarter in America.

The letter to shareholders simplifies Netflix’s tactics to investors explaining, “For 20 years, we’ve had the same strategy: when we please our members, they watch more and we grow more.”

What this letter doesn’t tell you is that Disney and the looming battle with Netflix will reshape the online streaming landscape.

In simple economics, an increase of supply caps demand, and don’t get sidetracked by the smoke and mirrors, Disney and Netflix are absolutely fighting for the same eyeballs no matter how much Netflix plays this down.

To highlight an example of how these two are directly competing against each other – let’s take the cast of Monica, Chandler, Rachel, Ross, Joey, and Phoebe – in the hit series Friends.

Netflix acquired the broadcasting rights from Warner Bros, who owns Disney, and it was the most popular show on Netflix.

Warner Bros, knowing that Disney were on the verge of rolling out an online streaming product, renewed Netflix for 2019 at $80 million.

Not only were they hand feeding the enemy in broad daylight, but they handicapped their new products as it is about to debut.

Whoever made that decision must go into the hall of shame of boneheaded online content decisions.

Once 2020 rolls around, Disney will finally be able to slap Friends on Disney Plus where it belongs, and the streaming wars will heat up to a fever pitch.

Ultimately, when Netflix brushes off reality proclaiming that if they please viewers with the same strategy, then everything will be hunky-dory, then I would say they are being disingenuous.

The online streaming industry has started to become more complex by the minute and the “same strategy” that worked wonders in a vacuum before must evolve with the times.

At $360, I would short Netflix in the short to medium term until they prove the headwinds are a blip.

If it goes up to $400, it’s a screaming short because accelerating cash burn, poor guidance, decelerating domestic net adds, and a jolt of new competition aren’t the catalysts that will take shares above the heavenly lands of $400, let alone $450.

Netflix is still a fantastic company though – I’m an avid viewer.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/multimedia.png822972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-18 01:06:482019-07-10 21:49:49Netflix's Worst Nightmare

America is full – that is what domestic social media growth is telling us.

The once mesmerizing service that captured the imagination of the American public has soured in the country that created it.

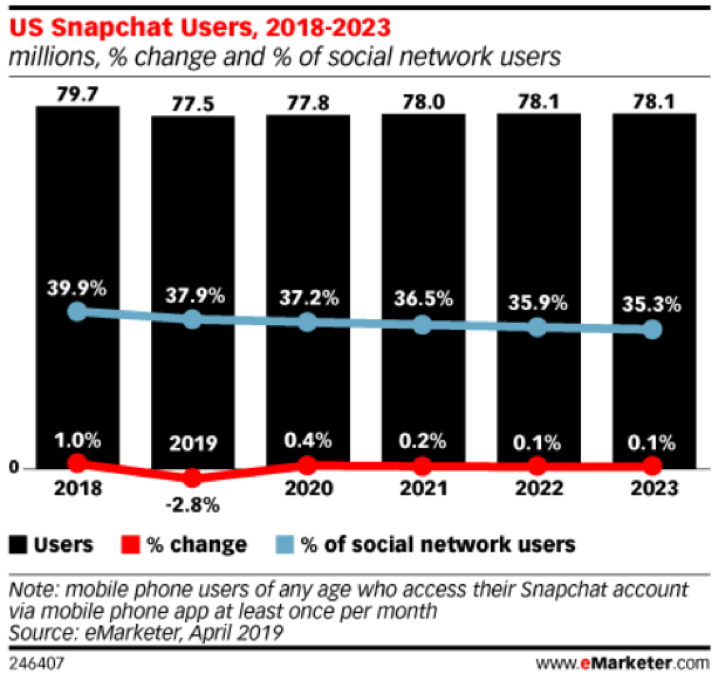

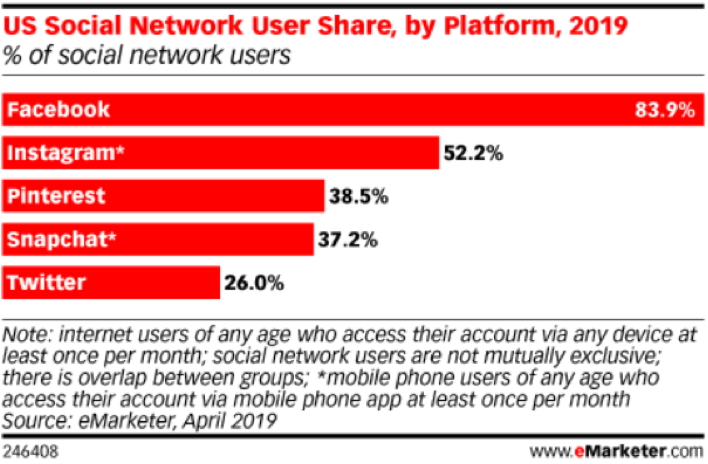

Online advertising consultant emarketer.com issued a report showing that Snapchat (SNAP), the worst of the top social media outlets, will lose users in 2019.

The 77.5 million users forecasted by the end of 2019 represents a 2.8% YOY decrease.

This report differs greatly from the report eMarketer issued just past August showing that Snapchat was preparing for a rise of 6.6% YOY in 2019.

The delta, rate of change, represents a massive downshift in expectations and the sentiment stems from the widespread saturation of social media assets.

Market penetration has run its course and the players have run out of bullets mainly targeting Generation Z.

These platforms have given up on baby boomers and Snap feels that pursuing the millennial demographic would be an exercise in futility.

Even more disheartening is that between 2020-2023, there will be only a minor uptick of user growth by 600,000 users clamping down on the impetus of a comeback of sorts shackling the business model.

The trend is not mutually exclusive to Snap, Twitter or Facebook, social media as a group will only expand the overall user base by 2.4% in 2020 hardly satisfying the appetite for growth that these companies publicly advertise.

Remember that much of Instagram’s growth originates from borrowing Snapchat users by way of copying their best features.

Even with this dirty tactic, growth seems to be petering out.

Snap’s shares have made a nice double after peaking shortly over $25 after the IPO.

But the double was a case of investors believing that management and execution had hit rock bottom – the proverbial dead cat bounce in full effect.

Now investors will pause to reassess whether there is another reasonable catalyst to drive the stock higher.

First, investors will need to ask themselves, is Snap in for another double?

Absolutely not.

So where does Snap go from here?

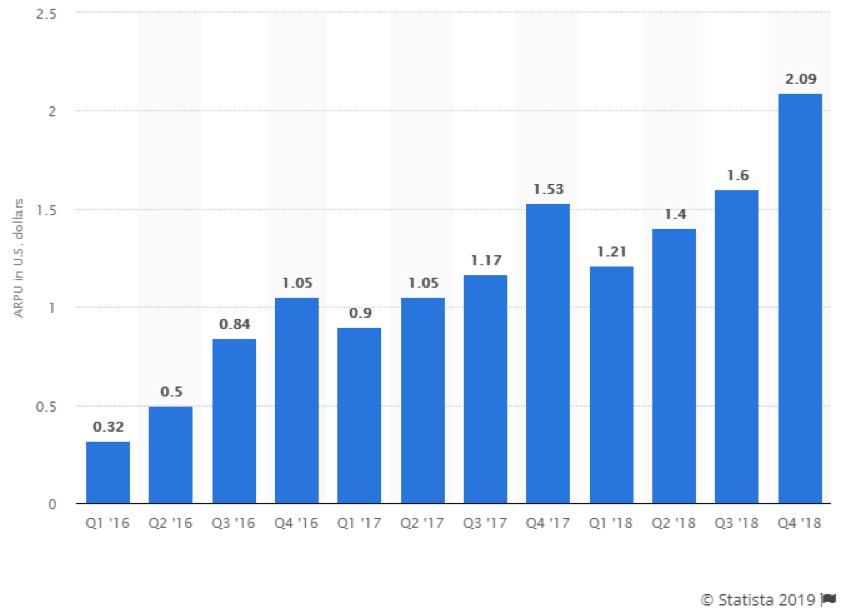

I believe they will borrow from the playbook of Mark Zuckerberg and attempt to emphasize supercharging average revenue per user (ARPU).

Whether the company arrives at this conclusion by chance or strategy, they must confront the reality that there are almost no other levers to pull if they want to perpetuate this growth story.

M&A is also off the table because the company is burning through cash.

Facebook’s (ARPU) came in at $7.37 last quarter indicating how Snap needs to make substantial headway in this metric with last quarter’s paltry (ARPU) at $2.09.

Essentially, management will conclude that each user isn’t absorbing enough ads because of declining user engagement.

Snap CEO Evan Spiegel will need to improve the pricing power charging advertisers at higher rates.

Obviously, the lack of an attractive platform resulting from poor execution and engineering problems needs a quick turnaround.

It’s not all smooth sailing for Facebook either, they keep chopping and reshaping strategy by the day attempting to minimize costs as the regulation burdens rot at the bottom line.

On the bright side, regulation hasn’t been as bad as initially thought – usership hasn’t dropped by orders of magnitudes.

In fact, Facebook’s users have shown a resurgent indifference to Facebook chopping up their data and repackaging it to 3rd parties, meaning Facebook has come through rather unscathed in the face of a PR storm.

There have even been recent reports of Zuckerberg being persuaded to start paying journalists for original content, a vast pivot for his hyped-up propaganda machine of being in the distribution business.

Juicing up (ARPU) is the lowest hanging fruit on offer for Snapchat and Facebook right now, overperforming in this sphere will improve financials and keep the mosquitoes away while affording them time to ponder how to reaccelerate user growth.

One outsized negative trend is that 90% of user growth appears to originate from undeveloped nations with a lack of discretionary spending power showing that this strategy has its limits.

Searching for another tool in its toolkit will redefine Snapchat, Twitter, and Facebook as we know it.

I would even classify it as an existential crisis.

Instagram have bought Facebook the most time to readjust its future direction highlighting that stealing Snapchat’s audience is still effective, expecting user growth to climb to 106.7 million US users, up 6.2% from 2018.

Instagram will continue its expansion by adding nearly 19 million new US users by 2023, but as much as it adds to its new social media asset, Facebook will be struggling for new net adds.

Snapchat is in dire straits and the stock market bubble could support the share price for up to another 8-12 months, but when the guillotine drops on Snapchat, the blood will smatter everywhere.

The company also plans to introduce a gaming service to take advantage of the popularity with its core users, Generation Z.

This should be the trick that breathes life into operating margins and (ARPU) which is why I believe the stock will hold up for the next period of time.

But with the gaming initiatives also comes rampant competition with the likes of Alphabet (GOOGL) and don’t forget Fortnite is still the 800-pound gorilla.

These trends also bode negatively for Pinterest (PINS) who might be going public as the last shot of tequila is downed at the after party.

SNAPCHAT ARPU

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/snap-users.png677720Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-15 08:06:512019-07-10 21:50:42Reaching Peak Social Media

I love doing presentations to small businesses on my free time, partly to stay in touch with the pulse of the Davids who have the unenviable task of fighting uphill against the Goliaths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher ups, but don’t forget they have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining their competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has grinded to a halt because of the PageRank algorithm from Google, everybody is making websites the same, a top nav, descriptive text, a smattering of images and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of their ecosystem have perverted the chance to have a unique online experience.

Most internet users have probably discovered that most websites don’t work well and the execution of them is lousy.

Many companies are not contributing enough resources to build out their site properly, or just don’t have the cash to fund it or a mix of the two.

About 95% of customer service calls originate from the company’s webpage because of payment problems, disfunction, misleading content, or simply because the website is down.

Ask any small business and they will tell you they deal with their domain being down for hours at a time because of some unknown server problem.

Not only is capitalism only working for a small group of Americans, but so are websites, such as massive companies like Amazon.com who have worked wonders with its e-commerce site.

Because the internet and namely websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking their own products at the top of page one of any Google search.

Amazon has followed the same practice by sticking their in-house brands at the top of any Amazon search on Amazon.com.

And remember that none of this can be called “antitrust” because these borderline tactics offer consumers lower prices but that is only because consumers are brainwashed to believe Amazon offers the lowest price.

What if the same products are available for half of Amazon’s in-house brands, would Amazon volunteer to post their in-house brands on the second page, the graveyard of search results?

I would guess no.

Websites used to give businesses a chance, remember in the mid-90s when a website of any ilk was impressive as if someone was walking on water.

What can we expect next?

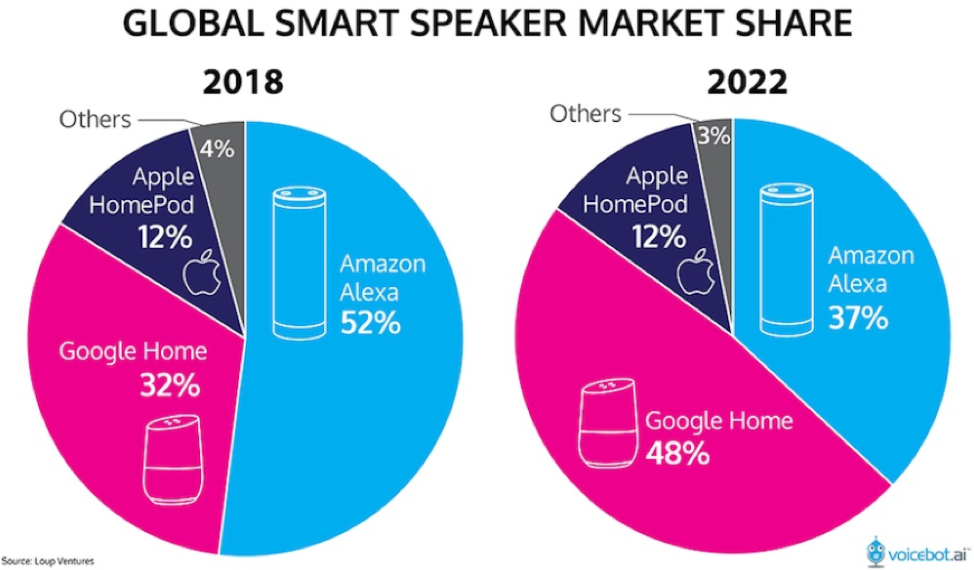

Amazon, Google, and Apple are taking their shows to artificial intelligence voice platforms.

SMEs could at least throw hail marys on standard internet searches with visual screens, but once content migrates over to voice platforms owned by Silicon Valley, then its game, set, and match.

For instance, a local business such as Joe’s Furniture Moving Business who, with the internet and visual screens, is searchable through search engines and can be even located on Google Maps with a concrete address.

Once we migrate the lions share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they make more money offering you information of a moving service they own or have a stake in.

The advent of 5G will refine the voice technology and enhance the machine learning techniques needed to complete the migration of content.

Once the world crosses an inflection point where the technology and volume of content on smart speakers outweigh the hassle to use a keyboard or mobile screen, this effectively makes these smart speaker manufacture Gods of the World because they will own the voice-based internet.

They will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

By the end of 2019, 74 million Americans will be using smart speakers, giving these smart speaker firms adequate data to fine tune their products.

Eventually, all Americans will be forced to use it or will not be able to function, similar to the effects of a laptop, email, and smartphone combination now.

Once these voice platforms become ubiquitous, websites will be deemed irrelevant – consumers will simply have a choice of Google Home, Amazon Alexa, and Apple HomePod and blindly trust what they tell you is in your best interests.

Pick your poison.

That’s right, users won’t control content in about 15 years, a scary thought, and now you understand why these companies will even give their voice A.I. platforms for free if they have to and probably will in the future.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/smart-speakers.png483566Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-11 01:06:362019-07-10 21:51:06The Means to a Frightening End

FANGS, FANGS, FANGS! Can’t live with them but can’t live without them either.

I know you’re all dying to get into the next FANG on the ground floor, for to do so means capturing a potential 100-fold return, or more.

I know because I’ve done it four times. The split adjusted average cost of my Apple shares is only 25 cents compared to today’s $174, so you can understand my keen interest. My average on Tesla is $16.50.

Uncover a new FANG and the riches will accrue rapidly. Facebook (FB), Amazon AMZN), Netflix (NFLX), and Alphabet (GOOGL) didn’t exist 25 years ago. Apple (AAPL) is relatively long in the tooth at 40 years. And now all four are in a race to become the world’s first trillion-dollar company.

One thing is certain. The path to FANGdom is shortening. It took Apple four decades to get where it is today, Facebook did it in one. As Steve Jobs used to tell me when he was running both Apple and Pixar, “These overnight successes can take a long time.”

There is also no assurance that once a FANG always a FANG. In my lifetime, I have seen far too many Dow Average components once considered unassailable crash and burn, like Eastman Kodak (KODK), General Electric (GE), General Motors (GM), Sears (SHLD), Bethlehem Steel, and IBM (IBM).

I established in an earlier piece that there are eight essential attributes of a FANG, product differentiation, visionary capital, global reach, likeability, vertical integration, artificial intelligence, accelerant, and geography.

We are really in a “What have you done for me lately” world. That goes for me too. All that said, I shall run through a short list for you of the future FANG candidates we know about today.

Alibaba (BABA)

Alibaba is an amalgamation of the Chinese equivalents of Amazon, PayPal, and Google all sewn together. It accounts for a staggering 63% of all Chinese online commerce and is still growing like crazy. Some 54% of all packages shipped in China originate from Alibaba.

The juggernaut has over half billion active users, and another half billion placing orders through mobile phones. It is a master of AI and B2B commerce. There is nothing else like it in the world.

However, it does have some obvious shortcomings. Its brand is almost unknown in the US. It has a huge problem with fakes sold through their sites.

It also has an ownership structure for foreign investors that is byzantine, to say the least. It is a contractual right to a share of profits funneled through a PO box in the Cayman Island. The SEC is interested, to say the least.

We also don’t know to what extent founder Jack Ma has sold his soul to the Beijing government. It’s probably a lot. That could be a problem if souring trade relations between the US and the Middle Kingdom get worse, a certainty with the current administration.

Tesla (TSLA)

Before you bet on a new startup breaking into the Detroit Big Three, go watch the movie “Tucker” first. Spoiler Alert: It ends in tears.

Still, Tesla (TSLA) has just passed the 270,000 mark in the number of cars manufacturered. Tucker only got to 50.

Having led my readers into the stock after the IPO at $16.50, I am already pretty happy with this company. Owning three of their cars helps too (two totaled). But Tesla still has a long way to go.

It all boils down to the success of the $35,000, 200-mile range Tesla 3 for which it already has 500,000 orders. So far so good.

It’s all about scale. If it can produce these cars in sufficient numbers, it will take over the world and easily become the next FANG. If it can’t, it won’t. It’s that simple.

To say that a lot is already built into the share price would be an understatement. Tesla now trades at ten times revenues compared to 0.5 for Ford (F) and (General Motors (GM). That’s a relative overvaluation of 20:1.

Any of a dozen competing electric car models could scale up with a discount model before they do, such as the similarly priced GM Bolt. But with a ten-year lead in the technology, I doubt it.

It isn’t just cars that will anoint Tesla with FANG sainthood. The firm already has a major presence in rooftop solar cell installation through Solar City, utility sized solar plants, industrial scale battery plants, and is just entering commercial trucks. Consider these all seeds for FANGdom.

One thing is certain. Without Tesla, there wouldn’t be s single mass-market electric car on the road today.

For that, we can already say thanks.

Uber

In the blink of an eye, ride sharing service Uber has become essential for globe-trotting travelers such as myself.

Its 2 million drivers completely disrupted the traditional taxi model for local transportation which remains unchanged since the days of horses and buggies.

That has created the first $75 billion of enterprise value. It’s what’s next that could make the company so interesting.

It is taking the lead in autonomous driving. It could also replace FeDex, UPS, DHL, and the US post office by offering same day deliveries at a fraction of the overnight cost.

It is already doing this now with Uber Foods which offers immediate delivery of takeouts (click here if you want lunch by the time you finish reading this piece.)

UberCopters anyone? Yes, it’s already being offered in France and Brazil.

Uber has the potential to be so much more if it can just outlive its initial growing pains.

It is a classic case of the founder being a terrible manager, as Travis Kalanick has lurched from one controversy to the next. The board finally decided he should spend much time on his new custom built 350-foot boat.

Its “bro” culture is notorious, even in Silicon Valley.

It is also getting enormous pushback from regulators everywhere protecting entrenched local interests. It has lost its license in London, the only place in the world that offered a decent taxi service pre-Uber. Its drivers are getting beaten up in Paris.

However, if it takes advantage of only a few of the doors open to it, status as a FANG beckons.

Walmart (WMT)

A few years ago, I was heavily criticized for pointing out that half the employees at my local Walmart (WMT) were missing their front teeth. They have since received a $2 an hour's pay raise, but the teeth are still missing. They don’t earn enough money to get them fixed.

The company is the epitome of bricks and mortar in a digital world with 12,000 stores in 28 countries. It is the largest private employer in the US, with 1.4 million workers, mostly earning minimum wage.

The Walmart customer is the very definition of the term “late adopter.” Many are there only because unlike Amazon, Wal-Mart accepts cash and Food Stamps.

Still, if Walmart can, in any way, crack the online nut, it would be a turbocharger for growth. It moved in this direction with the acquisition of Jet.com for $3 billion, a cutting-edge e-commerce firm based in Hoboken, NJ.

However, this remains a work in progress. Online sales account for only 4% of Walmart’s total. But they could only be a few good hires at the top away from success.

Microsoft (MSFT)

Talk about going from being the 800-pound gorilla to an 80 pound one, and then back to 800 pounds.

I don’t know why Microsoft (MSFT) lost its way for 15 years, but it did. Blame Bill Gates’s retirement from active management and his replacement by his co-founder Steve Ballmer.

Since Ballmer’s departure in 2014, the performance of the share price has been meteoric, rising by some 125% over the past two years.

You can thank the new CEO Satya Nadella who brought new vitality to the job and has done a complete 180, taking Microsoft belatedly into the cloud.

Microsoft was never one to take lightly. Windows still powers 90% of the world’s PCs. No company can function without its Office suite of applications (Word, Excel, and PowerPoint). SQL Server and Visual Studio are everywhere.

That’s all great if you want to be a public utility, which Microsoft shareholders don’t.

LinkedIn, the social media platform for professionals, could be monetized to a far greater degree. However, specialization does come at the cost of scalability.

It seems that the future is for Microsoft to go head to head against next door neighbor Amazon (AMZN) for the cloud services market while simultaneously duking it out with Alphabet (GOOGL).

My bet is that all three win.

Airbnb

This is another new app that has immeasurably changed my life for the better. Instead of cramming myself into a hotel suite with a wildly overpriced minibar for $600 a night, I get a whole house for $300 anywhere in the world, with a new local best friend along with it.

Overnight, Airbnb has become the world’s largest hotel chain without actually owning a single hotel. At its latest funding round in 2017, it was valued at $31 billion.

The really tricky part here is for the firm to balance out supply and demand in every city in the world at the same time. It is also not a model that lends itself to vertical integration. But who knows? Maybe priority deals with established hotels are to come.

This is another firm that is battling local regulation, that great barrier to technological innovation. None other than its home town of San Francisco now has strict licensing requirements for renters, a 30 day annual limitation, and a $1,000 a day fine for offenders.

The downtowns of many tourist meccas like Florence, Italy and Paris, France have been completely taken over by Airbnb customers, driving rents up and locals out.

IBM (IBM)

There was a time in my life when IBM was so omnipresent we thought like the Great Pyramids of Egypt it would be there forever. How times change. Even Oracle of Omaha Warren Buffet became so discouraged that he recently dumped the last of his entire five-decade long position.

A recent 20 consecutive quarters of declining profits certainly hasn’t helped Big Blue’s case. It is one of the only big technology companies whose share price has gone virtually nowhere for the past two years.

IBM’s problem is that it stuck with hardware for too long. An entrenched bureaucracy delayed its entry into services and the cloud, the highest growth areas of technology.

Still, with some $80 billion in annual revenues, IBM is not to be dismissed. Its brand value is still immense. It still maintains a market capitalization of $144 billion.

And it has a new toy, Watson, the supercomputer named after the company’s founder, which has great promise, but until now has remained largely an advertising ploy.

If IBM can reinvent itself and get back into the game, it has FANG potential. But for the time being, investors are unimpressed and sitting on their hands.

The Big Telecom Companies

My final entrant in the FANGstakes would be any combination of the four top telecommunication companies, Verizon (VZ), AT&T (T), Comcast (CMCSA), and Time Warner (TWX), which now control a near monopoly in the US.

There is a reason why the administration is blocking the AT&T/Time Warner merger, and it is not because these companies are consistently cited in polls as the most despised in America. They are trying to stop the creation of another hostile FANG.

Still, if any of the big four can somehow get together, the consequences would be enormous. Ownership of the pipes through which the modern economy courses bestows great power on these firms.

And Then….

There is one more FANG possibility that I haven’t mentioned. Somewhere, someplace, there is a pimple-faced kid in a dorm room thinking up a brand-new technology or business model that will take the world by storm and create the next FANG.

Call me crazy, but I have been watching this happen for my entire life.

I want to thank my friend, Scott Galloway, of New York University’s Stern School of Business, for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Creating the Next FANG?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/02/tech-guys.jpg368550Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2019-04-03 01:06:312019-04-02 17:47:43Who Will Be the Next FANG?

Mad Hedge Technology Letter April 2, 2019 Fiat Lux

Featured Trade:

(HOW TO GET CONTROL OF YOUR LIFE) (GOOGL), (FB), (LYFT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-02 08:07:002019-04-02 08:36:04April 2, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.