Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Buy and hold domestic software companies for dear life because that is what the market is giving you.

Take them with both hands.

These revenue models should revolve around developing the lucrative North American digital consumer markets.

Tech is all about giving you pockets of dispersion and my job to herd you into these pockets of opportunity created by pockets of dispersion.

We have once again been delivered a few more poignant indicators allowing us to gauge the market appetite for certain tech barometers.

Incandescent as can be, recent news of hardware companies planning to bring exorbitant foldable phones to market has me profusely shaking my head.

Huawei announced plans to debut the Mate X foldable 5G smartphone with a price tag of a staggering $2,600.

This followed an announcement by Korean behemoth Samsung to roll out the Samsung's Galaxy Fold and the Koreans plan to sell this luxury product for $1,980.

Chinese Huawei Mate X is 5G-supported and can simply fold into a slimmer 6.6-inch smartphone or unfold into an 8-inch tablet.

This is another case of smart manufacturers overreaching for a market that doesn’t exist and shouldn’t exist.

I believe the demand for screen-related smart products at this price point is scant at best.

If you compare foldable phones to a $600 high-tier Samsung Android smartphone with a 6-inch screen, Samsung and Huawei would need to convince consumers the extra $1,500 or in Samsung’s case, $2,200 is worth the extra relative wad of cash.

My bet is that these foldable phones aren’t worth even $300 more of aggregated incremental value let alone $500 and for many consumers like me, it’s worth zilch.

In no way, aside from the gimmick of buying one of these novelties, does buying a foldable phone justify the price.

This is another example of the common-sense factor that has been completely absent from a product cycle.

Product viability and product desirability do not walk hand in hand.

The screen-related smart device market is saturated, evident by the elongated refresh cycle in smartphone usership.

Blame the expensive price tags of over $1,000 and the removal of carrier subsidies that have caused the upgrade cycle to skyrocket from 2.39 years in 2016 to 2.83 years in late 2018.

Then there is the touchy issue of cannibalizing other hardware product lines as many of the potential foldable phone customers might interchange the foldable phone with normal smartphones.

This all screams bad strategy with companies saddled in a glut of inventory.

It takes R&D years to follow through and develop the technology to bring it to market, and it is entirely conceivable this could become a big write-off.

If price cuts happen shortly after the debut, prospects look bleak.

In general, consumer sentiment has soured for more of this type of tech. Many people are just exhausted from screen time and the cycle of the newest hardware screens is failing to excite existing customers bases.

The only conclusion I can make is that tech today is about software, software, and particularly domestic software.

If you compare software to hardware head to head now, software functionality is still increasing 15% YOY juicing up efficiency and productivity.

What will foldable phones offer a digital nomad or working professional?

Not much.

It highlights the absence of a productivity or functionality boost that digital device users are scouring for now.

Stay away from hardware.

Why is domestic software preferred over international software that scales the earth five times around?

Regulation.

It has reared its ugly head again.

The avalanche of negative headlines applied to American big tech is finally becoming a self-fulfilling prophecy.

It was only a matter of time until someone took note, and in this case, various Asian governments have taken note.

In a bid to blunt American tech’s first mover advantage, the Indian government has written up a draft of regulatory measures in order to make the Indian tech landscape a fairer playground.

This will have the intended effect of creating a national powerhouse of tech firms employing local people.

India has effectively taken a page out of China’s playbook using home-field advantage to nurture homegrown talent.

Large American tech companies have made India a playground of binge investments lately with Amazon (AMZN) shelling out $5 billion and Walmart (WMT) brazenly pouring $15 billion into e-commerce heartthrob Flipkart.

This is awful news for them.

They will have to adjust to India’s new-found zeal for digital regulation and a heavy restructuring of the business model could be in the cards in 2019 along with higher costs of running these businesses.

India has followed China in its footsteps demanding data to be localized meaning data centers won’t be able to run and store Indian data abroad.

American participants will have no other choice but to pony up the extra costs.

Readers might forget that India is the current battleground of global tech growth and Amazon will not have unfettered market access like they did breaking into Europe and dominating e-commerce from the start.

Amazon and Walmart can thank Facebook (FB) which has been the main culprit in bringing wave after monstrous wave of heavy criticism on a whole industry.

Facebook has effectively brought forward the regulatory storm that otherwise would have happened a few years later down the road.

In any case, this makes life harder for data-oriented companies who wish to navigate hazardous foreign tech climates.

Domestic angst against local tech has given the rubber stamp for full-on data government mandates abroad from India to Vietnam.

What does this all mean?

In 2019, data regulation could shrink expected growth levers while hardware companies are becoming even more desperate as these Hail Marys could quickly turn into liabilities.

I nailed software picks Zendesk (ZEN) and Twilio (TWLO) amongst others from a strong group of enterprise software stocks.

Twilio’s performance could potentially become my best pick of 2019, it’s on a straight line up even with all this clutter and chaos around the world.

Mad Hedge Technology Letter

February 14, 2019

Fiat Lux

Featured Trade:

(FACEBOOK’S NEW PROBLEM),

(FB), (GOOGL), (TRIP), (EXPE)

A major catalyst exacerbating recent tech layoffs has been a decline in referral traffic to news publishers from Facebook (FB).

Blame the algos!

Referral traffic is a way of reporting visits coming from a site from sources outside of the original site.

When someone clicks on a hyperlink leading to a different website, data analytics classified this as a referral visit to the second site by tracking mechanisms.

The truth is that news publishers have a painfully smaller window to monetize content than ever before and this opinion is echoed by some of big media’s stalwarts such as Rupert Murdoch, the chairman of News Corp.

Facebook decided to give preference to content in the news feed that is shared between Facebook users over those by news organizations, ironically, the news is being stripped out of the news feed whether that seems logical or not.

Under the guise of protecting the platform, Facebook is applying this ploy to further cut off users from escaping its walled garden trapping them inside for the purpose of clicking around the Facebook website even more.

As the technology evolves, companies are becoming increasingly pedantic in finding any practical method of allowing users to escape to another part of the internet.

Diminishing user time equals fewer clicks followed by reduced digital advertising revenue.

Another shift in Facebook rules entails elevating and demoting media outlets by trust levels and credible content that ultimately Facebook makes the decision on.

The algorithms in this case would prop up the more renowned institutions and essentially cut out minnow news organization.

Algorithms are inherently biased, and sources of revenue are cut off or opened up by these algorithmic shifts.

The monopolistic status of Facebook has made it near impossible for stand-alone firms to develop organically and ramping up digitally means leveraging Facebook ads to lure new customers.

What does this all mean?

News publications are bracing themselves for an atrocious year.

The side effect from recent changes mean that Facebook will ultimately become the God of the news cycle choosing which news populates where on the news feed or if it shows up at all.

Being a left-leaning company, Facebook is likely to anoint left-leaning news organizations as “trustworthy” while demoting more right-wing news feeds pushing them further down the pecking order.

And for marginal start-up news companies praying for any exposure, this is effectively a death sentence because of the lack of footprint inside of Facebook’s current database.

Machine learning cannot account for new developments in the system, let alone system altering shifts causing this technology to be defective.

The technology handsomely rewards the entrenched that have cultivated a big footprint inside the database that decisions hinge on.

Its backward-looking nature to carry out a business that is forward-looking is utter nonsense.

Many third-party businesses attempt to stimulate Facebook users’ appetite in order to bridge them over and act as a stepping stone to their own website.

Small businesses should prepare for an era where this type of digital reach is stunted and at some point, completely disengaged.

Effectively, Facebook and the rest of the FANGs will do its best to cut off outside activity preferring to keep usership in-house.

News organizations are feeling the full brunt of these ripple effects with online media firms such as Vox Media and BuzzFeed cutting staff in response to these Facebook algorithm changes.

Which industry will get chopped down next?

Online travel aggregators.

TripAdvisor (TRIP) had a great winter quarter in 2018, but looking down the line, the business model could get bogged down by the algorithm problem.

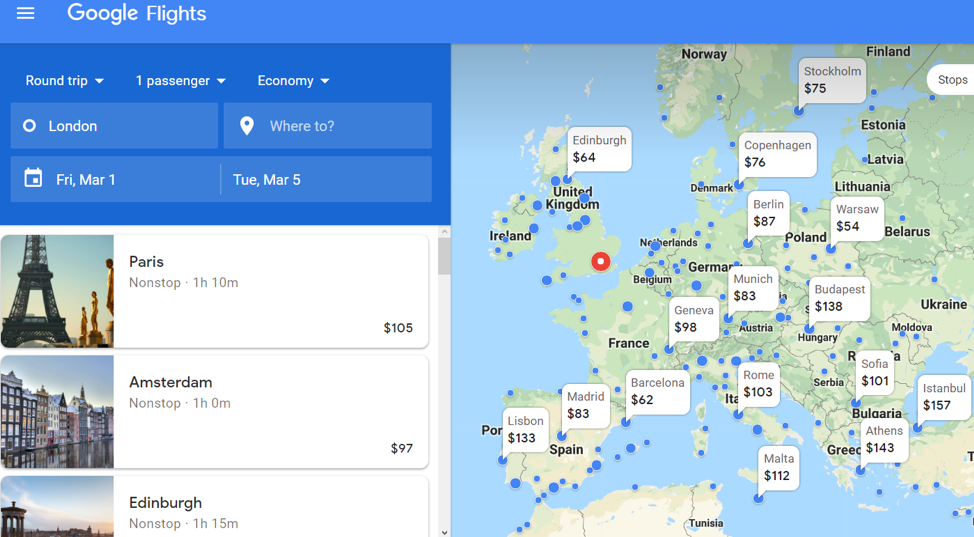

For instance, take the best flight purchase algorithm in the world Google Flights.

The United States Department of Justice Antitrust Division approved Google's $700 million purchase of ITA Software in 2011.

Within a few months, Google bent its algorithm into shape and reformulated it as Google Flights.

How does it stack up?

Easy to use, lack of digital ads, best of breed, and innovative are all ways I would describe this service.

That is why consumers prefer Google Flights over any other service.

It offers open-ended searches making the traditional flight search software seem pathetic.

Simply input the departure location and Google Flights will show the user every price to every location in the world on a visual map.

It’s travel transparency at its brightest and users can change trips in an instant if something attractive catches their eye.

The user can mix and match different destinations and dates until an optimal time and place can be calibrated along with a suitable price.

This gives the power back to the consumers.

Once in a while, dispersion between the Google Flight price and the official airline site price can be irritating, but the accuracy has improved over time.

Truth be told, it’s a waste of time to use a different flight search engine now after the existence of Google Flights.

Google is able to do this because they are masters at building algorithms and have an army of engineers at their disposal.

Online flight brokers such as Expedia (EXPE) and TripAdvisor are on a collision course for the beast that is the Google algorithm division.

This dovetails astutely with my overarching theme of technology destroying every broker industry because FANG algorithm teams do a way better job enhancing this segment of business than anyone else.

As you correctly guessed, I am bearish Expedia and TripAdvisor long term.

Travel fare aggregators can’t compete with Google and former CEO of Expedia Dara Khosrowshahi was smart to take the head job at Uber saving him from the future carnage.

Mad Hedge Technology Letter

January 30, 2019

Fiat Lux

Featured Trade:

(IS THE BOTTOM IN FOR FACEBOOK?),

(FB)

As much as I malign Facebook (FB) CEO and Founder Mark Zuckerberg, the risk-reward for Facebook’s earnings that come out after Wednesday’s close favor the upside.

Let me explain.

I have been bearish on this name for quite a while and I have been rewarded in spades.

From the Cambridge Analytica leak to firing the heads of Instagram and WhatsApp, last year was a year to forget and the stock was crushed.

This time, it’s a little different.

I believe the saturated business model has largely been priced in to the stock and the company is transitioning to a more lucrative side of the business with other levers they can pull.

Facebook can’t move mountains to raise the needle in the number of users in the western developed world.

The rich western world is Facebook’s profit engine with average revenue per user remarkably higher than its emerging user audience.

The company will change tact and seek to increase average revenue per user because of decelerating usership.

Emerging markets are the last bastion of growth for its user base, but unfortunately, this source of new users cannot be lucratively monetized like its staunch North America and Western European cash cows.

The lion's share of new users are from countries including India, Indonesia and Philippines where advertisers focus more on TV, print and physical advertising.

Expect Facebook to announce slowing user growth in the low single digits.

This likely won’t be a surprise to markets along with more rumblings about the average age of user increasing as Generation Z flees the platform.

The silver lining in this development is that Generation Z is fleeing Facebook and migrating to Instagram which is also owned by Facebook and a hyper-growth engine.

Even with the younger generation deleting Facebook in droves, Facebook still has a base of over 2 billion and every one of these customers use one of Facebook’s four services every day.

That is partly why it is attractive to digital advertisers and Facebook culls 98% of total revenue from ads.

If you forgot about last quarters earnings, Facebook handily beat EPS forecasts by 30 cents and barely missed on the top line, and that was in the face of disturbing ructions of a full-on regulation tech lash.

The first stage of negative regulation and the fallout have effectively been absorbed by the market and the second stage isn’t visible on the horizon as of today.

That day will eventually come but not before they come out with earnings later today, and not where near-term guidance will be materially affected.

If you read Mark Zuckerberg’s New York Times op-ed, he still believes that any road bump can be parsed over with marketing gibberish, and I would agree that the next stage of regulation that could damage the company is far away enough that this stall tactic will work for this particular earnings report.

However, this myopic and dangerous strategy must be managed quarter to quarter. There will be a time when the market needs to hear how Facebook will actually fix the model if a new wave of tech fury erupts.

The firm is safe now as the general trend for more robust regulation has started muted at the beginning of 2019 with congress and the administration busy with a closed government and political infighting bordering insanity.

This type of national news jumps to the forefront and pushes back the possible timeline for enforced regulation especially when 800,000 government workers were broadsided and couldn’t put food on the table or pay their rent.

To follow up on the political front, management is sure to take last year’s midterm election success and milk it for all its worth.

There were no disastrous scandals, recounts, or platform manipulation that could potentially do harm to the stock.

Facebook will tout this as a sign that its controls are starting to reap dividends and concrete evidence that they have shaped up since the Russian interference compromised the business model during last presidential election.

In late 2018, Facebook forecasted expenses to grow 40%-50% in 2019.

The headline expense number was set astronomically high in order for management to easily beat forecasts and announce that today.

Since management has categorized many material problems as marketing fixes, they have normalized doing the bare minimum as a stopgap measure masquerading as a real, full blown fix.

The one insight that keeps slamming me straight in the face like a gale force wind is that Zuckerberg likes his money which means he needs the stock to go up.

That would be the pitiful reason he offers these half-baked excuses as legitimate fixes because he understands that comprehensive solutions would be too costly damaging future earnings.

He also needs the stock to go up because many of the new faces at Facebook are compensated by stock because of a lack of cash on hand.

What is a meaningful catalyst to take Facebook higher?

The firings of the heads of WhatsApp and Instagram paved the way for the transition to 2019 where Facebook will monetize these other two services as well as integrating the back-end with Facebook.

This is viewed as the holy grail of Facebook growth and Zuckerberg incessantly refuted this would ever happen.

Well, the cat is out of the bag now.

In integrating the back-end of these three services, Facebook will extract a deeper insight into the behavior of their usership with a 360 degree view of their daily habits.

This deeper understanding of behavior will allow them to harvest the data in a way that is more valuable to digital ad buyers.

Facebook plans to compensate the lack of user growth for higher quality ads, and in turn they will be able to charge the ad buyers more per ad.

This strategy is a high risk, high reward maneuver because the company will intrude more into the personal data of their users than ever before.

On a business level, Zuckerberg has few options left up his sleeve and is predictably migrating towards the low hanging fruit as well as his best option today.

There is not much juice he can squeeze out of dinosaur Facebook anymore and margins will come down from now on.

However, WhatsApp and Instagram are fertile pastures for Zuck to wield his ad-hawking expertise.

Readers might forget that there are no ads on WhatsApp yet and its virgin provenance has been left largely unchanged from the beginning offering Zuck a golden project to mold his paws on.

If the CEO of Facebook goes into details about Facebook’s plan to ramp up these two social media platforms, the stock has a good chance to react positively.

The bar has been set quite low and Facebook has targeted this earnings report as an inflection point in the company’s history as they begin to pull alternative levers available to them.

This is a short-term prognosis in an otherwise murky future for the company.

Challenges are endless and part of the ceaseless issues involves Facebook not adding any real value as a technology platform or not possessing any ground-breaking technology or proprietary software.

Facebook is the used car salesman of the tech world and they are doing everything they can to stay relevant.

If Facebook does sell off after the WhatsApp and Instagram integration announcement, it is safe to deduce that Facebook is out of bullets and the stock becomes a sell on the rallies company until they can do something to stem the blood flow.

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

Global Market Comments

January 24, 2019

Fiat Lux

Featured Trade:

(FROM THE FRONT LINES OF THE TRADE WAR),

(AAPL), (AVGO), (QCOM), (TLT),

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE),

Mad Hedge Technology Letter

January 23, 2019

Fiat Lux

Featured Trade:

(WHY TECH IS FLEEING SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)