Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE ARTIFICIAL INTELLIGENCE CONUNDRUM),

(TSLA), (AMZN), (FB)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE ARTIFICIAL INTELLIGENCE CONUNDRUM),

(TSLA), (AMZN), (FB)

Anti-A.I. physicist Professor Stephen Hawking was a staunch supporter of preserving human interests against the future existential threat from machines and artificial intelligence (A.I.).

He was diagnosed with motor neuron disease, more commonly known as Lou Gehrig's disease, in 1963 at the age of 21 and sadly passed away March 14, 2018 at the age of 76.

Famed for his work on black holes, Professor Hawking represented the human quest to maintain its superiority against quickly advancing artificial acculturation.

His passing was a huge loss for mankind as his voice was a deterrent to A.I.'s relentless march to supremacy. He was one of the few who had the authority to opine on these issues. Gone is a voice of reason.

Critics have argued that living with A.I. poses a red alert threat to privacy, security, and society as a whole. Unfortunately, those most credible and knowledgeable about A.I. are tech firms. They have shown that policing themselves on this front is remarkably unproductive.

Mark Zuckerberg, CEO of Facebook (FB), has labeled naysayers as "irresponsible" and dismissed the threat. After failing to prevent Russian interference in the last election, he is exhibiting the same defensive posture translating into a de facto admission of guilt. His track record of shirking accountability is becoming a trend.

Share prices will materially nosedive if A.I. is stonewalled and development stunted. Many CEOs who stake careers on doubling or tripling down on A.I. cannot see it die out. There is too much money to lose.

The world will see major improvements in the quality of life in the next 10 years. But there is another side to the coin which Zuckerberg and company refuse to delve into...the dark side of technology.

Defective Amazon (AMZN) Alexa recently produced unexplained laughter because of a mistaken command to start laughing. Despite avoiding calamity, these small events show the magnitude of potential chaos capable of haywire A.I. functions. If one day a user attempts to order a box of tissues and Alexa burns down the house, who is liable?

Tesla's (TSLA) CEO Elon Musk has shared his anxiety about robots flipping the script on humans. Elon acknowledges that A.I. and autonomous vehicles are important factors in the battle for new technology. The winner is yet to be determined as China has bet the ranch with unlimited resources from Chairman Xi.

The quagmire with China has been squarely centered around the great race for technological supremacy.

A.I. is the ultimate X factor in this race and whoever can harness and develop the fastest will win.

Musk has hinted that robots and humans could merge into one species in the future. Is this the next point of competition among tech companies? The future is murky at best.

Bill Gates noted that robots should be taxed like humans. This reflects the bubble in which the ultra-elite reside. This comment implies that humans and robots are at the same level. It shows a severe lack of empathy for the 40% of working Americans who will be replaced by machines over the next 10 years.

The West is comprised of a deeply hierarchical system of winners and losers. Hawking's premise that evolution has inbuilt greed can be found in the underpinnings of America's economic miracle.

Wall Street has bred a culture that is entirely self-serving regardless of the bigger system in which it finds itself.

Most of us are participating in this perpetual money game chase because our system treats it as a natural part of life. A.I. will help more people do well in this paper chase to the detriment of the majority.

Quarterly earnings performance is paramount for CEOs. Return value back to shareholders or face the sack in the morning. It's impossible to convince anyone that America's capitalist model is deteriorating in the greatest bull market of all time.

Wall Street has an insatiable hunger for cutting-edge technology from companies that sequentially beat earnings and raise guidance. Flourishing technology companies enrich the participants creating a Teflon-like resistance to downside market risk.

The issue with Professor Hawking's work is that his timeframe is too far in the future. Professor Hawking was probably correct, but it will take 25 years to prove it.

The world is quickly changing as science fiction becomes reality. The year 2019 will signal the real beginning of A.I. in tangible form when autonomous fleets flood main streets and is another step in the direction of human's overreliance on machines.

People on Wall Street are a product of the system in place and earn a tremendous amount of money because they proficiently execute a specialized job. Traders are busy focusing on how to move ahead of the next guy.

Firms building autonomous cars are free to operate as is. Hyper-accelerating technology spurs on the development of A.I., machine learning, and enhanced algorithms. Record profits will topple, and investors will funnel investments back into an even narrower grouping of technology stocks after the weak hands are flushed out.

Professor Hawking said we need to explore our technological capabilities to the fullest in order to avoid extinction. In 2018, exploring these new capabilities still equals monetizing through the medium of products and services.

This is all bullish for equities as the leading companies associated with A.I. will not be subject to any imminent regulation, blowback, or government intervention.

And let me remind you that technology is still the least regulated industry on the planet.

It has its cake and is eating it too. Hence, technology is starting to cross over into other industries demonstrating the powerful footprint tech has extracted in economics and the stock market.

The only solution is keeping companies accountable by a function of law or creating a third-party task force to regulate A.I. In 2018, the thought of overseeing robots sounds crazy.

However, by 2019, it might be as normal as uncontrollable laughter from your smart home.

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT

OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

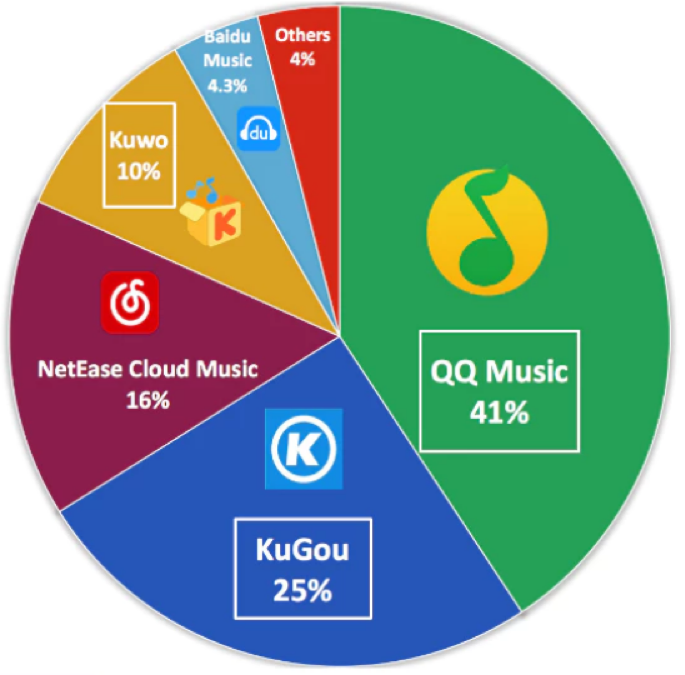

So you thought that Tencent Music Entertainment (TME), the Spotify (SPOT) of China, going public at $13 a share on the New York Stock exchange would mean the music streaming giant would potentially tyrannize the Western music streaming market.

Relax, it will never happen, China’s personal data laws are analogous to Facebook’s (FB) lax data guidelines multiplied by a factor of 10.

There is no possible scenario in which a Chinese content service constructed at the magnitude of Tencent Music Entertainment Group would ever get the thumbs up from American regulators.

The ongoing trade war has effectively barred any Chinese capital’s ability to snap up key American technological firms, as well as stymieing any Chinese tech unicorns dishing out streaming content in participating in a monetary relationship with the American consumer.

In August, the Department of the Treasury which chairs the Committee on Foreign Investment in the United States (CFIUS) rolled out an expansionary pilot program widening CFIUS’ jurisdiction to review foreign non-controlling, non-passive investments in companies that produce, design, test, manufacture, fabricate, or develop “critical technologies” within certain industries deemed paramount to national security.

Even though the amendment does not specify China, it means China.

If you had a hunch that Tencent would take over the music streaming world, then the better question is to ask yourself if Tencent Entertainment is equipped to take over the Chinese streaming world and monetize the product efficiently.

What really is (TME)?

(TME) is the Tsar of Chinese music streaming with apps that allow users to stream music, sing karaoke, and watch musicians perform live. (TME) dominates this sphere of Chinese tech with a combined 800 million monthly active users.

(TME) is a concoction of services including QQ Music, Kugou, Kuwo, and karaoke app WeSing making up over 70% of the music streaming industry in China.

Its daily active users (DAUs) spend over 70 minutes per day on the platform and have inked exclusive deals with elite Western artists.

Tencent Music's revenue nearly doubled YOY to $2 billion during the first nine months of 2018, and its net income more than tripled to $394 million.

The social entertainment services aspect has been a massive revenue driver for them including income from virtual gifts on WeSing, a platform where fans gift virtual items to favorite singers, and sign up for premium memberships giving users access to exclusive concerts.

This collection of clever services mixed with social media has been successful, and the reason why it comprises 70% of total revenue.

Paid membership has grown 24% YOY to 9.9 million while paid users only make up 4.4% in China. This is a huge change in the tech climate from the past when Chinese netizens would never pay for internet content. This has allowed the average revenue per user (ARPU) to creep up to $17.22 per paid user.

The other 30% of revenue can be attributed to its ad-less music service which is not ad-less for free users.

So, in fact, the 30% of the business that mirrors Spotify is its Achilles heels echoing the painstaking task of monetizing pure music content.

No company has ever shown that a pure music streaming internet model can be profitable, the music streaming graveyard is littered with the failed attempts of companies from the past.

The unit registered a mere $1.24 in average revenue per paid user during the third quarter, paltry compared to (TME)’s social media products.

(TME)’s combination of social media and music entertainment weighted towards virtual gifts’ income is a weak business model in the west and would not extrapolate in the western world.

It is a supremely China model only unique to China and other Asian countries.

Therefore, I would point out that even if this arm of Tencent could migrate to America, management knows better than to put square pegs in round holes.

That being said, its potential in China is its long runway and most Chinese content companies haven’t been able to crack the western market.

The only types of Chinese companies that have had any remnant of success in the west are hardware companies and look what happened to telecommunication equipment companies Huawei and ZTE recently – taken out by the western regulatory sledgehammer.

It’s crystal clear that the Chinese understanding of personal data and IP regulation simply don’t marry up with western standards, and that is why I suggested that these two massive tech worlds are in for a hard splintering dividing these two competing models.

There has been some intense jawboning going on behind the scenes as Huawei, who is in the lead to develop 5G technology, still needs Qualcomm’s radio access technology to make 5G a reality.

The scenario of a hard fork between western and Chinese 5G becomes more real each passing day.

Part of Tencent Music’s ability to perform revolves around its swanky position installed in the center of the most popular chat app in China called WeChat.

Using this position as a fulcrum, Tencent Music plans to invest 40% of the capital raised from its IPO on expanding its music library, 30% on product development, 15% on marketing, and the last 15% on M&A.

For right now, there is an elevated emphasis on growing the number of paid users and converting its free users to premium subscriptions.

Ironically enough, Spotify has a 9% stake in Tencent Music and Tencent has a 7.5% holding in Spotify. Just by having stakes in each other is enough reason to avoid migrating into the same competitive markets with each other.

If you read between the lines, the stakes seem more a pledge of trading expertise in developing each other’s business as you see traces of each other in both unicorns.

Would I invest in Tencent Music?

One word – No.

There are almost 1,000 pending lawsuits alleging copyright infringement, not a huge surprise here.

Tencent concedes around 20% of the music content is not licensed.

Pouring fuel on the fire, a Tencent Music executive is also being sued by a seed investor claiming he was bullied into selling his stake ahead of its IPO.

There are question marks surrounding this company and that might have been part of the justification of tapping up the American public markets to prepare for this next stage of uncertainty.

As it is, Spotify cannot make money because of the elevated royalty costs eroding its business model, (TME) probably can if it steals most of its music, but that is a suicide mission waiting to happen.

Fortunately, Tencent is a hybrid mix of not only pure music streaming but of social media fused with music apps through gift giving gimmicks and karaoke-themed services.

These higher margin drivers are the reason why Tencent is profitable and Spotify is not, plus the giant scale of servicing 800 million Chinese users that give credence to the freemium model.

However, it’s entirely feasible that Tencent Music could use a good portion of the $1.1 billion from the IPO to battle the slew of pending lawsuits waiting around the corner.

Would you want to invest in a company that went public just to fund their legal defense?

Definitely not.

Look at its streaming cousin iQIYI (IQ), shares peaked over $40 in June after its IPO and have swan-dived ever since going down in a straight line and is trading around $17 today.

In general, most Chinese tech stocks have been collateral damage of a wider trade war pitting the maestros of crude geopolitical strategies against each other.

This year has not been kind to Chinese tech shares, and considering most of Tencent’s music library has been stolen, investors would be crazy to invest in this company.

I am surprised this company held up as well as it did on IPO day because the timing of the IPO couldn’t have been worse in a segment of tech that is awfully difficult to become profitable in a country whose economy is softening by the day in an insanely volatile stock market.

And to be honest, I would have stopped listening about this company after knowing they face pending lawsuits of up to 1000.

As for Spotify, yes, they are the industry leader in music streaming but investors need concrete proof they can become profitable. I like the direction of increasing operating margins, but that all goes to naught if it’s in a perpetual loss-making enterprise. I would sit out on both these stocks with a much negative bias towards its ticking time bomb Chinese music version.

Regulation and the trade war have taken a huge swath of tech off the gravy trade such as semiconductors, Google, social media, hardware, American tech who possess supply chains in China and I would smush in Chinese tech ADR’s on that list too.

Stay away like the plague.

Mad Hedge Fund Trader John Thomas was interviewed on a major news network a few days ago talking out the state of the global financial markets. I thought you would be interested in the Q&A that followed.

Q: Bonds (TLT) have come down a lot on sudden flight to safety bid, with the 30-year yield under 2.9%. Do you see yields going back up in the short term?

A: Absolutely, yes. This is a one-time only panic triggered by the failure of the G-20 Summit in Buenos Aires. And we got the second leg down from the arrest of the CFO of Huawei, one of China's biggest companies, so that has triggered a short-term panic. It's temporary and we're going to bounce back strong. In fact, we already have. Now is a great time to be shorting bonds and buying stocks.

Q: How bad are things at Facebook (FB)? Is the bad news priced into the stock?

A: No, all the bad things are not priced into the stock. That’s why we are telling people that Facebook is a “No touch.” Bad news seems to come out every day, it’s a black swan a day stock, you don’t want to be anywhere near it. They will get some regulation, but nobody knows what it is, or how much it will affect profitability. But when a big company has to change their business model in a hurry, you don’t want to be anywhere near it. Far easier to buy it on the way up than on the way down.

Q: Will a cut in the oil supply by OPEC stem the spiraling down price of Oil (USO)? Is there a trade here?

A: “Yes” to both questions. OPEC will probably announce some sort of price cut/production cut in the next meeting which will get prices off the floor. Everyone ramped up their production to try to beat price falls which then makes the price fall worse, which is always what happens. So, yes, I would be buying oil here. I'd be buying oil stocks here too. There is your trade.

Q: Will the markets hold the February Lows?

A: Yes.

Q: If it does not hold, how far can it fall?

A: Worst case, you may get a fall straight down sucking all the sellers. But if you flip the algorithms to the buy side then it’s off the races. Markets have a habit of doing that quite a lot this year, so I think the lows have been made and you want to be buying stocks here. The fundamentals behind the market are just too strong to get beyond what algorithms are doing, what damage algorithms can do on a day trading basis. So yeah, I don't think that we're going to new lows, these are the new lows right here.

Q: Do you see an American Recession by the end of 2019?

A: Yes, I see the bull market ending in the next 3 to 6 months and recessions starting after that. That said, there is plenty to be made on the upside in coming months and then there's a ton of money to be made on the downside after that. That’s when you want to be attending my short selling school which you also get with a subscription to my service.

Q: Will the Chinese (FXI) allow the Yuan to collapse to fuel imports AND stimulate their GDP growth rate?

A: Yes. They have largely offset all of the import duties imposed by the US by depreciating their currency by 10%. If we raise duties more, they'll just cut their currency value by the same amount, so the actual dollar landed price is unchanged. There's nothing the US can do about that. We're already playing our best cards so it’s not like we can do to retaliate if they devalue their currency more. That’s the problem you have shooting all of your arrows on the first attack.

Q: Would you rotate some growth to value-based stocks on the expectation of interest rising next year in crush and grow stocks.

A: You got it half right. I would sell the high growth stocks into the next big rally, take my profits, and then go into cash! You don't want to own defensive stocks in bear markets, you want to own cash. Defensive stocks go down in a bear market, only at a slower rate, but go down they do nonetheless. Cash is king. You can earn 3 or 4% on your cash these days. That is much better than a stock that is going down.

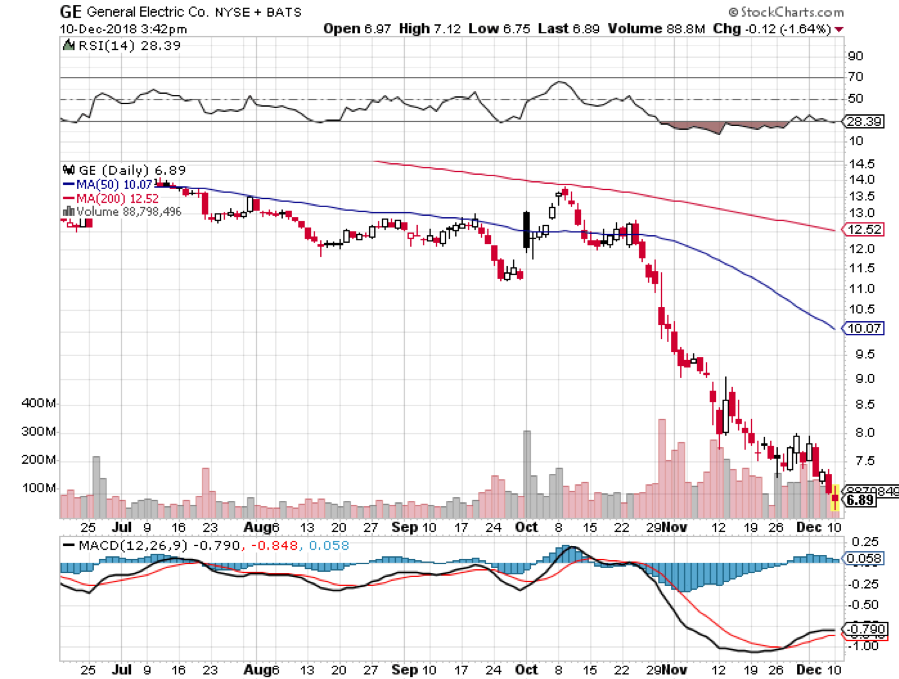

Q: I bought General Electric (GE) about a year ago at $17, and I thought it was a great deal at the time. Unfortunately, it was not, so can (GE) go any lower than it is now? I thought it would hold $10 dollars but then they cut their dividend to one cent and the shares have cratered to seven dollars. What should I do?

A: You're kind of asking me what to do after you close the barn door and the horses have already bolted. If you have (GE), I would keep it at seven dollars. The worst thing, it goes sideways from here. The best case is you get a strong rally and the stock doubles in coming months. This is not a chapter 11 situation as they have too many assets. It’s just a matter of how quickly they can turn around the company. By the way, we told people to stay away from (GE) from $31 all the way down to when it got to single digits. So, we missed that buy every dip mentality in (GE). Thank goodness for that.

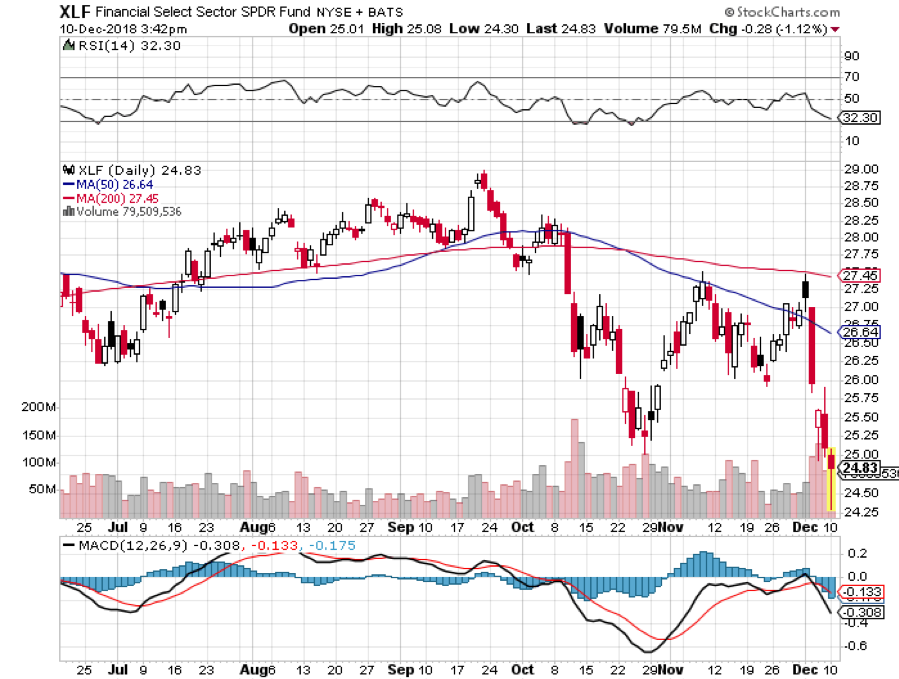

Q: Why won’t banks benefit in a rising interest rate environment?

A: The answer is very simple. These are the new buggy whip makers. You don't want to own big banks as they're hobbled by these gigantic branch networks which cost a fortune, and which are all going to disappear in ten years. Fintech companies like Square (SQ) and PayPal (PYPL), these little tiny apps that you've never heard of, they're eating the banks’ businesses one by one. And by the way, even though interest rates are rising, loan volume is falling at a faster rate, so they're making a lot less money than they used to. They're not really allowed to trade markets anymore because the risk is too high. So, even if they knew how to trade markets, they can’t rely on those earnings like they used to. So, avoid the banks like the plague.

Q: Is there any scenario you see stocks rising 10% next year?

A: No. Absolutely not. We're trying to call the top of a 10-year bull market here. The total return on the market in 2019 will probably be negative and could be negative by quite a lot. Maybe by 10%, 15%, or more. So yeah, if you're hanging on for new highs, I would give up that theory and find another one. It could be a very long wait, like a five-year wait before we go back to the old highs we saw in September and before that in January.

Q: Will Geopolitics drive the market more than it did in 2018?

A: Absolutely, it will. In the geopolitics category, you can include the China trade war, the Europe trade war, the possibility that Congress does not approve the new NAFTA. There's a ton of new things that could go wrong next year. And by the way, the burden of proof is now on stocks to prove how good they are. Risk is rising in the market and volatility is rising, but there still is good money to be made for a year-end rally.

Q: Why has gold (GLD) not performed so far?

A: We don't have inflation and gold really needs to get a good ramp up in inflation to get some serious price performance. That said, I expect a return in inflation. The economic data you get lags reality by anywhere from 3 to 6 months, so you will get a rise in inflation well above 3%. That’s when you really start to move on gold, that’s why I'm saying buy the dip.

Q: Would you buy the dollar (UUP)?

A: No, I would not. It’s looking like we have a couple of interest rates rising next year. The dollar will remain strong into that but in some point next year in the whole strong dollar story disappears as the rise in interest rates stops. If the interest rates level, all of the weak dollar plays will take off like a rocket. Those would include the Euro (FXE), Yen (FXY), and emerging markets (EEM). So, watch those spaces very carefully. There are gigantic moves coming in all of those once we stop raising interest rates and once the dollar peaks out.

Q: Will we close at the lows of the year?

A: No, we will not. The lows of the year probably happened right before this interview. I expect a strong rally from here driven by algorithms. Yes, they work on the upside just as well as they do on the downside side. In fact, algorithms really don’t care which way they go just as long as they go.

Q: What securities do you cover?

A: We cover stocks, bonds, commodities, precious metals, real estate, and every trade alert has a recommendation for a stock, an ETF, and an options trade so that way you can tailor the trade alert to meet your own experience level and risk tolerance.

Q: When does the letter come out?

A: It comes out roughly at midnight EST every day before the next trading day. That way early risers can read the letter and then enter their trade alerts at the market opening. It also helps the Europeans read it as their day starts. We have a big following in Europe and an even bigger following in Australia so that is the answer to that question.

Q: Can beginners with no previous experience use your service?

A: Absolutely. Training beginners how to enter the markets for the first time is one of the primary goals of this newsletter. We have customers that range in size from $20 billion dollar hedge funds all the way down to students trading off their dorm room beds with minimal one-contract trades. So yes, it’s for everybody and every trade alert that we send out has a link to a video showing you exactly how to execute this trade on your own trading platform

Q: Are you an algorithm?

A: Well, if I made a machine noise that would help. All I can say is come to one of my global strategy luncheons. You can pinch me and if I bleed, I am real.

Q: You obviously have enough money, why do you do this?

A: Leveling the playing field for the average guy is why I do this. When I worked on Wall Street, I saw so many people get ripped off it used to make me sick. So, this is my chance to get even. Helping you learn how to make money is my way of getting even. That's why I do this.

At the beginning of the interview, I promised you a seasonal trade alert, here is one of the most popular ones, Buy Home Depot (HD) in the Summer before the hurricane season. That’s good every year for a 15% rally and that’s exactly what we got this year. A 15% rally, 2 big hurricanes, big profits, goodbye, and then see you again next year.

Q: Thank you for coming today, John. It was a real pleasure.

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

Mad Hedge Technology Letter

November 28, 2018

Fiat Lux

Featured Trade:

(TRUMP'S TARIFF THREAT FOR APPLE))

(AAPL), (BABA), (EBAY), (WMT), (FB), (MSFT), (AMZN)

The administration’s threat of levying 10% on iPhones is a great sign for the technology sector as a whole.

The short-term media sensationalism has flipped this story the other way around crying about this as if it is a major penalty to Apple (AAPL).

Don’t get me wrong, these potential stiff tariffs have the possibility of triggering a $1 billion loss on Apple’s revenue, but this is all about protecting American technology long term.

This is not like taking a sledgehammer and ruining their business model, and it will not strip away this brilliant wealth creation vehicle.

Apple remains a cheap stock to buy for patient long-term holders and is one of the best run companies in the world with an operating maestro executing the roll-out of premium products named Tim Cook, the CEO of Apple.

The administration might not like some of technology firms’ tactics, but in reality, they are a pivotal reason why the economy has been humming along in the longest bull-market ever.

Effectively, the administration has put Apple and its peers up on a pedestal and is defending them from Chinese competition.

What industry wouldn’t want this?

Most of 2018, the current administration presided over a stock market that was going up in a straight line and the bulk of those gains were harvested by the major tech companies, mainly the FANGs.

The administration was quick to take credit for a strengthening stock market and would like to see rates suppressed to engineer more upside.

The FANGs are going through a reversion to the mean after 100% gains and giving back 20% or 30% of profits offer opportune entry point for long-term investors.

The only FANG that needs a structural change is Facebook (FB) and has the funds to do it. The other three plus Microsoft (MSFT) will lead the tech charge when the short-term weakness subsides.

If you think Chinese consumers would bail on Apple products because of the trade war, then you are wrong.

Apple has been grandfathered into Chinese society and it is one of the few iconic American products that can boast this achievement.

Apple is a luxury brand produced by an epochal superpower.

The presence of Apple products reverberates around China’s economic landscape, and even if Chinese people do not like America, they respect its economic prowess and wish to learn from its capitalistic ways.

This is the main reason they send their kids to American universities.

Historically, China was once entirely dependent on Russia to fill in its economic and social vision with the communist party sending its best and brightest to Moscow to study the Soviet Union’s secret sauce.

If you go to Beijing now, most of the second ring road of flats conspicuously remind me of Khrushchyovkas, the unofficial name of a type of low-cost, concrete-paneled or brick three- to five-storied apartment building which was developed in the Soviet Union during the early 1960s.

During this time, its namesake Nikita Khrushchev directed the Soviet government.

Pre-Deng Xiaoping Soviet influences can still be found everywhere in central Beijing.

Once the Chinese communist government realized that the Soviet model impoverished large swaths of society, they went on the open market to find a more optimal method to run their economy that could take advantage of their monstrous man power.

The model they decided on was a fusion of communism and capitalism, and for 30 years, this system fueled Chinese peasants out of poverty and to the promenades of Saint-Tropez.

Because of Chinese laser-like obsession on social status, material possessions are the most important way for them to differentiate against each other.

For Chinese women, the x-factor is skin tone, but for Chinese men, it is the brand, quality, and volume of possessions.

Even if rich Chinese hate Apple and their iPhones, they are permanently married to this product because owning a Chinese smartphone would be a monumental faux pas on the same level as American First Lady Melania Trump shopping for her new clothes at Walmart (WMT).

This is the same reason why every political who’s who in China drives an Audi A6, and every successful Chinese business executive drives a BMW.

Luxury brands are closely associated to the person’s social status in China and these unwritten rules have even more weight than the official rules in China partly because most Chinese over 40 are uneducated, plus China’s lack of public trust.

Apple’s tentacles reaching deep into Chinese society have in fact led to a situation where Apple-related jobs for Chinese citizens add up to over 5 million jobs which is over double the number of jobs Apple supports in America.

The result of Apple morphing into a pseudo-Chinese company is that pain for Apple means a loss of Chinese jobs on a large scale at a time when the Chinese economy is becoming more precarious by the day.

The Chinese economy is softening under a massive burden of crippling public and private debt that is putting the cap on growth.

As a result of the trade skirmish, China has temporarily halted its deleveraging effort that was intended to remedy the health of the economy and has reverted back to the China of old, low-quality infrastructure projects and heavily polluted coal production.

China’s rapid ascent to prosperity could also mean the Chinese consumer and economy could go through a reversion to the mean scenario with private and public companies loaded to their eyeballs with debt going bust and a looming economic stimulus in the cards if this plays out.

All this means is that Apple is too big to fail in China and CEO of Apple Tim Cook absolutely knows this.

Theoretically, Chinese consumers absolutely have access to local smartphone substitutes for $200 that would do the same job as a $1,000 iPhone.

I have tested out Huawei and Xiaomi premium smartphones costing $400, and they have more than enough firepower to be a reliable everyday smartphone and some.

The fact is that Chinese consumers intentionally choose not to substitute Apple products.

And I would go deeper than that by saying Steve Jobs is revered in China like a demigod and his passing turned him into a sort of tech martyr with a level of status that not even Alibaba (BABA) originator Jack Ma can touch.

Jack Ma performed miracles by copying eBay’s (EBAY) blueprint of e-commerce from a shabby Hangzhou flat ditching his former job as an English teacher then copying Amazon (AMZN) to juice up growth.

But Jack Ma never created the iPhone, iPod, tablet, or Apple app store from thin air. That he never did.

Making matters even more ironic is that most Chinese communist members actually use an Apple iPhone for the same reasons I mentioned earlier.

Not only that, the children of Chinese communist politicians take lavish vacations to Silicon Valley to take selfie’s in front of Apple’s spaceship headquarters in Cupertino and upload them onto social media.

They then proceed to visit the nearest Apple store right next door at the Apple Park visitor center which is essentially an Apple store on steroids to make bulk purchases of Apple tablets, watches, computers, iPhones for their extended circle of friends and distant relatives because they are “cheaper in America than in China” mainly due to the heavy import duties levied on Apple products in China.

As for tech equities, what this does is blunt short-term positive sentiment for tech stocks and particularly chip stocks that I have told readers to stay away from like the plague.

Apple’s supply chain frenemies don’t have the luxury of selling 80 million luxury phones at $1,000 per quarter and are often the recipient of indiscriminate sell-offs shellacking shares.

Even with the overhanging issue of rising tariffs, tech stocks should produce great earnings next year.

Look at Apple and the consensus EPS outlook for next quarter comes in at $4.73 and that is after EPS increasing 41% sequentially from the quarter before.

Apple will soon become a $300 billion of sales per year company with profitability expanding at a rapid clip.

They are a company that prints money then buys back their own stock profusely. Not many companies can do that.

These negative reports that have been coming fast and furious don’t help the momentum, but the share’s weakness solely means that better entry points are available for investors before Apple launches over $200 again.

There is a high chance that the administration is using Apple as a bargaining chip and nothing will come of it.

Think about it, after all this commotion about the trade war with China, revenue was up almost 20% last quarter in greater China, so what gives?

It means that things aren’t as dire as it seems. A lot of hot steam over nothing is a gift to long-term investors, but short-term traders will feel the pain of the temporarily elevated headline risk.

Global Market Comments

November 26, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or ARE WE IN OR OUT?)

(FB), (AAPL), (AMZN), (NFLX),

(GOOG), (SPY), (TLT), (USO), (UNG), (ROM)