Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

Mad Hedge Technology Letter

November 26, 2018

Fiat Lux

Featured Trade:

(WILL THE FAANGS FINALLY KILL OFF TELEVISION?)

(AMZN), (DIS), (FOX), (ROKU), (FB), (AAPL), (GOOGL)

Are we already in a recession or still safely out of one?

That is the question painfully vexing investors after the stock market action of the past seven weeks.

There is no doubt that the economic data has suddenly started to worsen, setting off recession alarms everywhere.

October Durable Goods were down a shocking 4.4%. Weekly Jobless Claims hit 224,000, continuing a grind up to a 4 ½ month high. Is the employment miracle ending? Goldman Sachs says growth is to drop below 2% in 2019, well below Obama era levels. Maybe that’s what the stock market crash is trying to tell us?

The Washington political situation continues to erode confidence by the day. We have already lost real estate, autos, energy, semiconductors, retailers, utilities, and banks. But as long as tech held up, everything was alright.

Now it’s not alright.

The tech selloff we have just seen was far steeper and faster than we saw in the 2008-2009 crash. You have to go all the way back to the Dotcom Bust 18 years ago to see the kind of price action we have just witnessed. The closely watched ProShares Ultra Technology Fund (ROM) has cratered from $123 to $83 in a heartbeat, off 32.5%.

Which begs the question: Are we already ten months into a bear market? Or is this all one big fake-out and there is one more leg up to go before the fat lady sings?

I vote for the latter.

If this is a new bear market, then it is the first one in history with the lead sectors, technology, biotechnology, and health care, announcing new all-time profits going in.

So, either Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Google (GOOG) are all about to announce big losses in coming quarters, which they aren’t, or the market is just plain wrong, which it is.

Which leads us to the next problem.

Markets can be wrong for quite a while which is why I cut my positions by half at the beginning of last week. To quote my old friend, John Maynard Keynes, “Markets can remain irrational longer than you can remain liquid,” who lists his entire fortune in the commodities markets during the Great Depression.

To see this all happen in October was expected. After all, markets always crash in October. To see it continue well into November is nearly unprecedented when the strongest seasonals of the year kick in. This was the worst Thanksgiving week since 2011 when we were still a wet dog shaking off the after-effects of the great crash.

There are a lot of hopes hanging on the November 29 G-20 Summit to turn things around which could hatch a surprise China trade deal when the leaders of the two great countries meet. The Chinese stock market hit a one month high last week on hopes of a positive outcome. Do they know something we don’t?

There were multiple crises in the energy world. You always find out who’s been swimming without a swimsuit when the tide goes out. James Cordier certainly suffered an ebb tide of tsunami proportions when his hedge fund blew up taking natural gas (UNG) down 20% in a day.

Cordier got away with naked call option selling for years until he didn’t. All of his investors were completely wiped out. I have always told followers to avoid this strategy for years. It’s picking up pennies in front of a steamroller. Same for naked puts selling too.

The Bitcoin crash continued slipping to $4,200. I always thought that this was an asset class created out of thin air to absorb excess global liquidity. Remove that liquidity and Bitcoin goes back to being thin air, which it is in the process of doing.

Oil (USO) got crushed again, down an incredible 35.06% in six weeks, from $77 a barrel all the way down to $50 as recession fears run rampant. Panic dumping of wrong-footed hedge fund longs accelerated the slide. They all had expected oil to rocket to $100 a barrel in the wake of the demise of the Iran Nuclear Deal and the economic sanctions that followed.

Apparently, Saudi Arabia’s deal with the US now is that they can chop up all the journalists they want at the expense of a $27 a barrel drop in the price of oil. That will cut their oil revenues by a stunning $97 billion a year. That’s one expensive journalist!

Watch the price of Texas tea carefully because a bottom there might signal a bottom for everything including tech stocks. And I don’t see oil falling much from here.

As for performance, Thanksgiving came early this year, at least in terms of the skinning, gutting, and roasting of my numbers. If you do this long enough, it happens. Every now and then, markets instill you with a strong dose of humility and this is one of those time.

My year to date return dropped to +25.72%, and chopping my trailing one-year return stands at 31.71%. November so far stands at a discouraging -3.91%. And this is against a Dow Average that is down -2.01% so far in 2018.

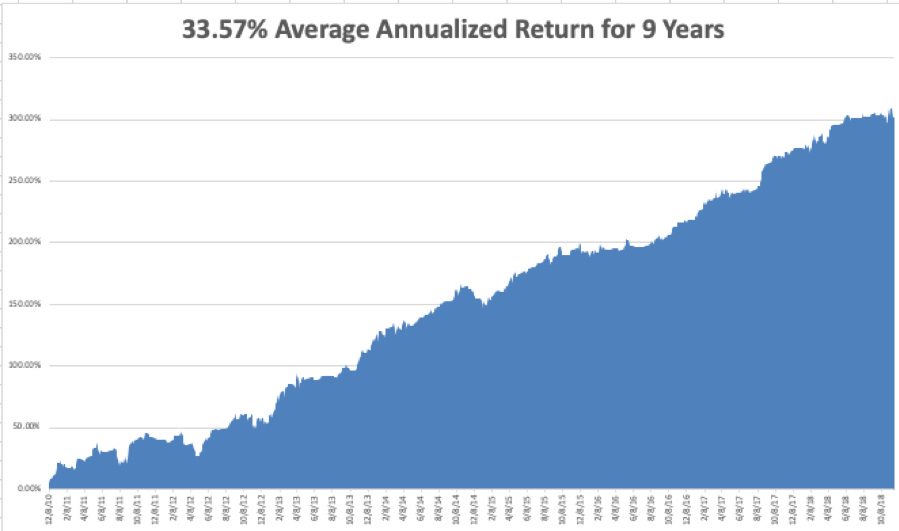

My nine-year return withered to +302.19%. The average annualized return retraced to +33.57%.

The upcoming week has some important real estate data coming. However, all eyes will be upon the Friday G-20 announcement from Buenos Aires. Will the trade war with China end, or get worse before it gets better?

Monday, November 26 at 8:30 EST, the Chicago Fed National Activity Index is published.

On Tuesday, November 27 at 9:00 AM, the all-important CoreLogic Case-Shiller National Home Price Index is out. It will be interesting to see how fast it is falling.

On Wednesday, November 28 at 8:30 AM, Q3 GDP is updated. How fast is it shrinking?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 29 at 8:30 we get Weekly Jobless Claims which have been on a four-month uptrend. At 10:00 AM, October Pending Home Sales are printed.

On Friday, November 30, at 9:45 AM, the week ends with a whimper with the Chicago Purchasing Managers Index.

The Baker-Hughes Rig Count follows at 1:00 PM. At some point, we will get an announcement from the G-20 Summit of advanced industrial nations.

As for me, I drove through the first blizzard of the year over Donner Pass to finally crystal clear skies of San Francisco. Long-awaited drenching rains had finally cleansed the skies. Every Tahoe hotel was packed with Californians fleeing the smokey skies.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

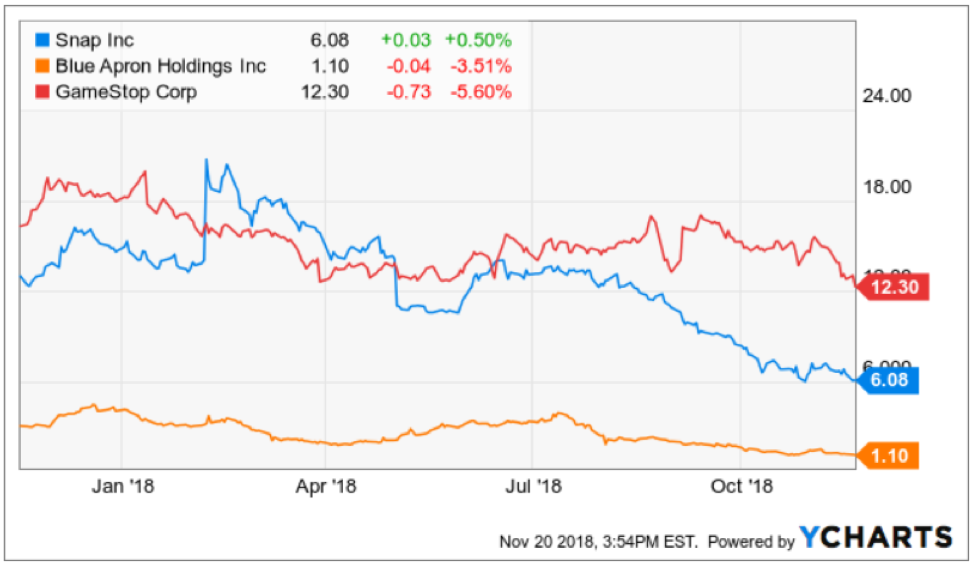

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Mad Hedge Technology Letter

November 19, 2018

Fiat Lux

Featured Trade:

(ROKU’S UNASSAILABLE LEAD)

(TIVO), (ROKU), (NFLX), (AMZN), (CHTR), (DISH), (FB), (AAPL), (GOOGL)

Shake off the rust.

That is exactly what management of a fast-growing tech company doesn’t want to hear.

Losing money isn’t fun. And investors only put up with it because of the juicy growth trajectories management promises.

Without the expectations of hard-charging growth, there is no attractive story in a world where investors need stories to rally behind.

Setting the bar astronomically high in the approach to management’s execution and product development will always be, the single most important element in a tech company.

This is the secret recipe for thwarting entropy and rising above the rest.

You might be shocked to find out that most tech firms die a harrowing death, the average Joe wouldn’t know that, with constant headlines glorifying our tech dignitaries.

Just look at the pageantry on display that was Amazon’s (AMZN) quest to find a second headquarter.

According to Apex Marketing, the hoopla that coalesced around Amazon’s year-long search netted Amazon $42 million in free advertising by tracking the absorbed inventory of exposure from print, TV, and online.

Social media traffic by itself rung up $8.6 million of freebies.

These days, tech really does sell itself, and I didn’t even mention the billions in tax breaks Amazon will harvest from their Willy Wonka and the Chocolate Factory style headquarter search.

The only thing I would have changed would have been extending the contest into the second year.

Amazon’s brand is probably the most powerful in the world, and that is not because they are in the business of only selling chocolate bars.

One company that might as well sell chocolate bars and has been stymied by the throes of entropy is TiVo (TIVO).

TiVo was once the darling of the technology world.

It was way back in 1999 when TiVo premiered the digital video recorder (DVR).

It modernized how television was consumed in a blink of an eye.

Broad-based adoption and outstanding product feedback were the beginning of a long love affair with diehard users wooed by the superior functionality of TiVo that allowed customers to record full seasons of television shows, and, the cherry on top, fast-forward briskly through annoying commercials.

The technology was certainly ahead of its time and TiVo had its cake and ate it for years.

The stock price, in turn, responded kindly and TiVo was trading at over $106 in August of 2000 before the dot com crash.

That was the high-water mark and the stock has never performed the same after that.

TiVo’s cataclysmic decline can be traced back to the roots of the late 90’s when a small up and coming tech company called Netflix (NFLX) quickly pivoted from mailing DVD’s to producing proprietary online streaming content.

Arrogant and set in their old ways, TiVo failed to capture the tectonic shift from analog television viewers cutting the cord and migrating towards online streaming services.

Consumer’s viewing habits modernized, and TiVo never developed another game-changing product to counteract the death of a thousand cuts to traditional television and its TiVo box that is still ongoing as I write this.

Like a sitting duck, Charter Communications (CHTR) and Dish Network (DISH) devoured TiVo’s market share in the traditional television segment constructing DVR’s for their own cable service.

And instead of licensing their technology before their enemies could build an in-house substitute, TiVo chose to sue them after the fact, resulting in a one-time payment, but still meant that TiVo was bleeding to death.

Enter Project Griffin.

Netflix (NFLX) spent years developing Project Griffin, an over-the-top (OTT) TV box that would host its future entertainment content and poured a bucket full of capital into the software and hardware of this revolutionary product.

Making the leap of faith from the traditional DVD-by-mail distribution model that would soon be swept into the dustbin of history was an audacious bet that looks even better with each passing year.

This Netflix branded OTT box was specifically manufactured for Netflix’s Watch Instantly video service.

In 2007, Netflix was just week’s away from rolling out the hardware from Project Griffin when CEO of Netflix Reed Hastings decided to trash the project.

His reason was that a branded Netflix box would hinder the software streaming content confining their growth trajectory to only their stand-alone platform.

This would prevent their streaming service to populate on other networks.

To avoid discriminating against certain networks was a genius move allowing Netflix to license digital content to anyone with a broadband connection, and giving them chance to make deals with other companies who had their own box.

It was the defining moment of Netflix that nobody knows about.

Netflix became ubiquitous in many Millennial households and Roku (ROKU) was spun-out literally bestowing new CEO of Roku Anthony Woods with a de-facto company-in-a-box to build on thanks to old boss Reed Hastings.

Woods cut his teeth borrowing TiVo’s technology and developed the digital video recorder (DVR) as the founder of ReplayTV before he joined Netflix and was the team leader of Project Griffin.

Now, he had a golden opportunity dropped into his lap and Woods ran with it.

Woods quickly became aware that hardware wasn’t the future of technology and switched to a digital ad-based platform model allowing any and all streaming services to launch from the Roku box.

No doubt Woods understood the benefits of being an open platform and not playing favorites to certain networks in a landscape where Apple (AAPL), Google (GOOGL), Facebook (FB), and Amazon have made “walled gardens” an important part of their DNA.

Democratizing its platform was in effect what the internet and technology were supposed to be from the onset and Roku has excavated value from this premise by playing nice with everyone.

This also meant scooping up all the ad dollars from everyone too.

At the same time, Wood’s mentor Hastings has rewritten the rules of the media industry parting the sea for Roku to mop up and dominate the OTT box industry with Amazon and Apple trailing behind.

Roku was perfectly positioned with a superior finished product, but also took note of the future and zigged and zagged when they needed to which is why ad sales have surpassed their hardware sales.

By 2021, over 50 million Americans will say adios to cable and satellite TV.

The addressable digital ad market is a growing $80 billion per year market and Roku will have a more than fair shot to secure larger market share.

The rock-solid foundations and handsome growth story are why the Mad Hedge Technology Letter is resolutely bullish on Roku and Netflix.

Roku and Netflix have continued to evolve with the times and TiVo is now desperately attempting to sell the remains of itself before the vultures feast on their corpse.

What is left is a portfolio of IP assets that brought in $826 million in 2017, and they have exited the hardware business entirely halting production of the iconic TiVo box.

Digesting 100% parabolic moves up in the share price is a great problem to have for Roku and Netflix.

These two are set to lead the online streaming universe and stoked by robust momentum to go with it.

The Mad Hedge Technology Letter currently holds a Roku December 2018 $30-$35 in-the-money vertical bull call spread bought at $4.35, and it is just the first of many tech trade alerts that will be connected to the rapidly advancing online streaming industry.

Global Market Comments

November 9, 2018

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS), (TLT)

(WHY TECHNICAL ANALYSIS DOESN’T WORK)

(FB), (AAPL), (AMZN), (GOOG), (MSFT), (VIX)

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

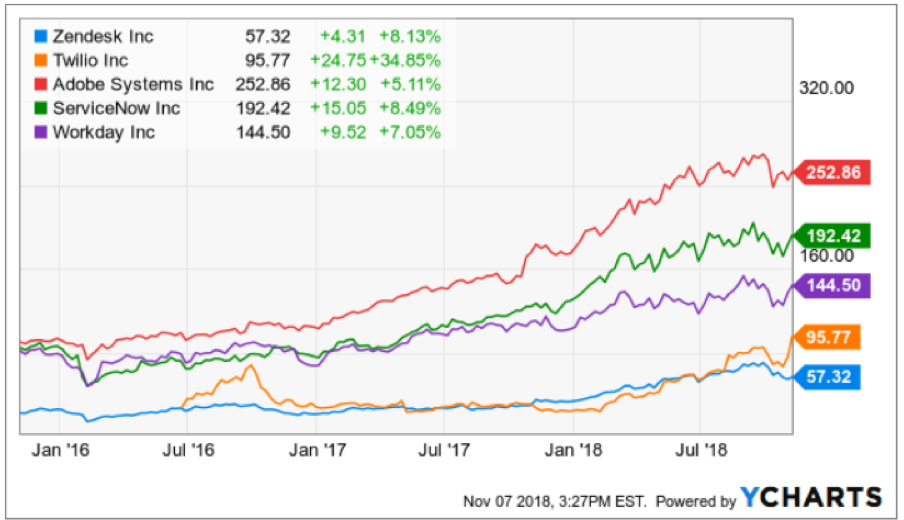

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

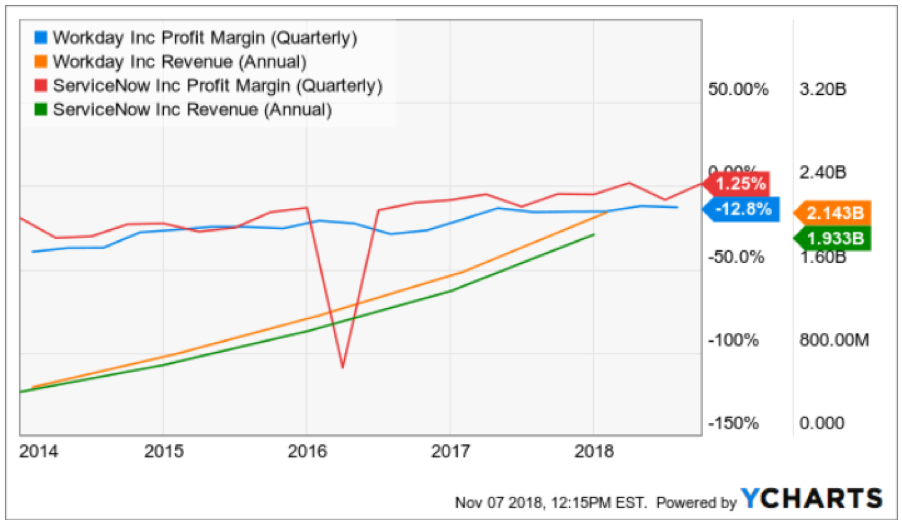

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.

Global Market Comments

November 5, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE MAD HEDGE FUND TRADER HITS A NEW ALL TIME HIGH),

(AAPL), (FB), (RHT), (GE), (VXX), (AMZN), (SPY), (IWM), (CRM)

I used to do a lot of skydiving from 20,000 feet. There’s nothing like a freefall, feeling the wind rip at your jumpsuit as you plunge towards the earth at terminal velocity of 125 miles per hour. In the beginning, the ground looks very far away. Then it suddenly gets very close, very fast.

I used to do this during the 1960s with WWII surplus silk parachutes with a “double L” cut. You hit the ground like a ton of bricks. Sometimes, we’d swing back and forth from the wings of the airplane before letting go just to have fun and freak out the pilot who had no chute.

Over time, you develop a very accurate sense of how fast the ground is approaching and when to pull the ripcord. If you’re wrong, you die.

That’s how I felt when markets went into freefall last Monday. However, after a half-century of trading, I have a highly developed sense of where the bottom is.

So, I piled on the “bet the ranch” longs in technology stocks and shorts in the bond market right at the absolute bottom. And to make sure everyone to a man got in, shares swooshed down one final time when rumors spread that Trump was escalating the trade war with China once again.

By Wednesday morning, the Mad Hedge Fund Trader model portfolio had booked its largest two day gain since the inception of this letter 11 years ago, some 12%. By miracle of miracles, we ended up positive for October, virtually the only one to do so in the entire hedge fund industry.

I would like to think that 50 years of toil in the markets is finally starting to pay off for me. The truth is, the harder I work, the luckier I get.

Stocks lost $2 trillion in market value in October, off 6.9%. Other than that, how was the play, Mrs. Lincoln? Tech took the worst hit in a decade, with many favorites down 20%-30%.

I am raising as much cash as I can ahead of the Midterm Elections tomorrow. Democrats seizing the House of Representatives is priced into the market already.

If the Republicans end up keeping the House, you can count on at least a 1,000-point rally in the Dow Average in the next few days as the door is now open for more tax cuts, more deregulation, and more deficit spending.

If the Democrats end up taking both the Senate and the House you can look for a 1,000 point drop in the Dow. That would bring on a huge “flight to safety” bid in the bond market and yet another opportunity to sell short at great prices.

Either way, I want more dry powder with which to take advantage of any extreme moves that may take place. “Extreme” seems to be the order of the day.

By the way, we are so far in the money with our remaining positions that even with a 1,000 point drop we should still reap the maximum profit with the November 16 option expiration in only 9 trading days.

Not that it matters, but October Nonfarm Payroll Report came in at a red-hot 250,000. The headline Unemployment Rate remained at a two-decade low at 3.7%. The Broader U-6 “Discouraged worker” unemployment rate fell 0.1% to 7.4%.

For the first time in yonks, no sector lost jobs last month. HealthCare added 36,000 jobs, Manufacturing 32,000 jobs, and Leisure & Hospitality 42,000 jobs.

However, the real blockbuster was that Average Hourly Earnings exploded to a 3.1% YOY rate, the highest in ten years. Yes, ladies and gentlemen, this is what inflation looks like, up close and ugly.

The number immediately knocked the wind out of the bond market taking it to a new low for the year. Yes, this is what double short positions in bonds are all about. I saw this coming a mile off.

The backdrop for the bond market is looking worse than ever. The budget deficit is about to break $1 trillion for the first time since the 2009 crash. Rising interest rates mean the government’s debt burden is about to grow by leaps and bounds, eventually becoming its largest expenditure.

The US Treasury is hitting the markets daily with massive new issuance, and the Chinese are dumping what US bonds they have to support the Yuan, now at a ten-year low. This is what Armageddon looks like in slow motion.

Last week was dominated by a China trade war that was on again, then off, then on one more time. The stock market ratcheted four-digit figures every time this happened.

Apple (AAPL) announced record profits yet again but countered with cautious forward sales guidance. Social media pariah Facebook (FB) delivered an earnings report beyond all expectations popping the stock $10.

IBM took over Red Hat (RHT) for $33 billion, the third largest merger in history. It’s too little too late for Big Blue as the stock falls on the news. It all reeks of a “Hail Mary.”

General Electric (GE) cut its dividend from 12 cents a share to one cent after reporting a breathtaking $22.8 billion loss. The Feds have opened a criminal investigation into accounting practices. This may define the final bottom in the stock. Take another look at those long-term LEAPS.

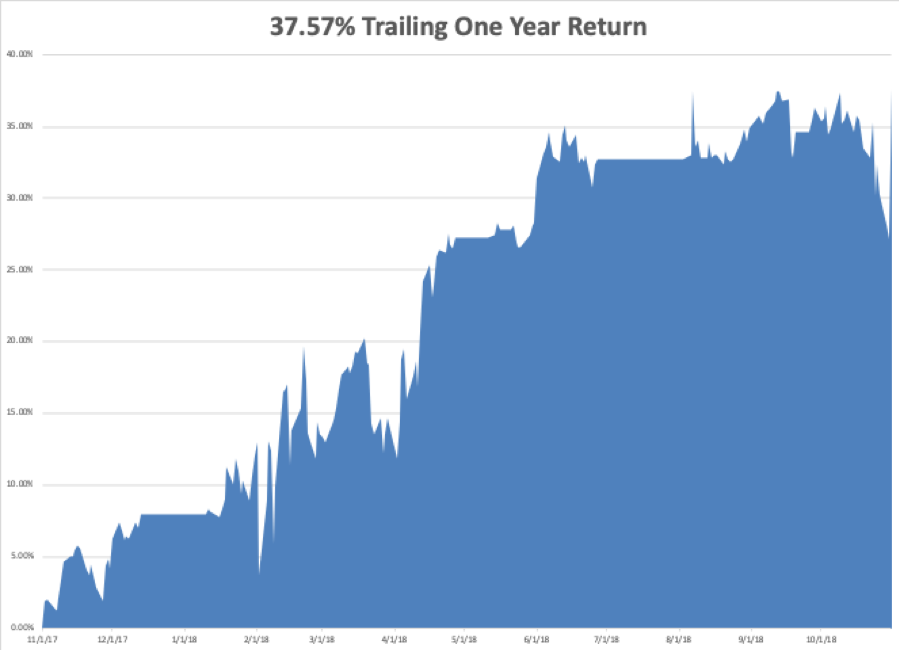

My year-to-date performance rocketed to a new all-time high of +33.17%, and my trailing one-year return stands at 37.57%. October finished at +1.24% and that includes an ill-fated -4.23% loss in the iPath S&P 500 VIX Short Term Futures ETN (VXX).

And this is against a Dow Average that is up a miniscule 1.9% so far in 2018. So far in November, we are up an eye-popping +3.54%.

Incredible as it may seem, the Mad Hedge Fund Trader has been up 18 consecutive months. That’s what you pay for and that’s what you’re getting. There’s nothing more fulfilling in life than making promises to friends, then delivering in spades.

As the market collapses, I scaled into longs in Amazon (AMZN), the S&P 500 (SPY), the Russell 2000 (IWM), and Salesforce (CRM). I used the flight to safety bid in the bond market to double up my short position there, and am kicking myself for not going triple weight.

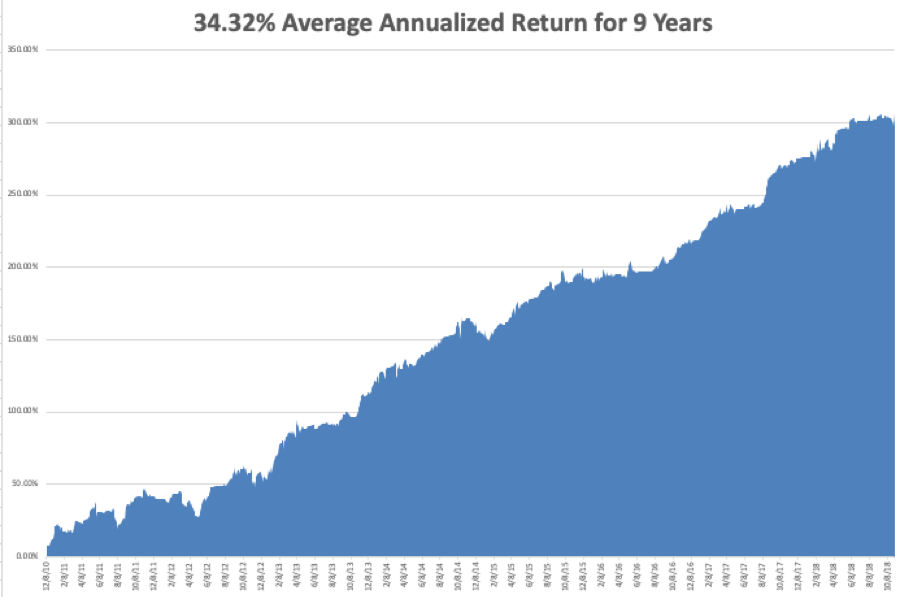

My nine-year return ballooned to 309.64%. The average annualized return stands at 34.72%.

All the BSDs are done reporting Q3 earnings and only a few tag ends are left to report. The carnage is over until we restart the cycle once again in February. In any case, economic data pales in comparison to the election in terms of market impact.

On Monday, November 5 at 10:00 AM, the ISM Manufacturing Index is out.

On Tuesday, November 6 is Election Day. Trading will be a subdued affair and the results will start coming out at 11:00 EST after the west coast polls close.

On Wednesday, October 24 we have the election aftermath to deal with. Up 1,000, down 1,000, or unchanged, who knows?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. The Federal Open Market Committee meets to discuss interest rates but will take no action.

On Friday, October 26, at 8:30 AM, the October Producer Price Index is out, an important read on inflation.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I made a massive amount of money personally in the October crash. I am going to plop down $150,000 and buy a brand new Tesla Model X for myself. The ashtrays are full on the old one, and besides, there is a tiny nick in the windshield from driving up to Lake Tahoe. I hear the new one has new “Summon” technology that allows it to drive into a parking lot by itself and drive around until it finds an empty space, then back into it, all untouched by human hands.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader