Mad Hedge Technology Letter

May 14, 2018

Fiat Lux

Featured Trade:

(MEET THE NEW FANG),

(AMZN), (WMT), (FB), (NFLX), (GOOGL), (UBER)

Mad Hedge Technology Letter

May 14, 2018

Fiat Lux

Featured Trade:

(MEET THE NEW FANG),

(AMZN), (WMT), (FB), (NFLX), (GOOGL), (UBER)

Yes, it's Wal-Mart (WMT).

No, I'm not making this recommendation because they let you park your RV in their parking lots at night for free.

And no, I'm not smoking California's biggest cash crop either (it's not grapes).

I predicted as much in my recent research piece, "Who Will Be the Next FANG?" by clicking here.

It is the dawn of a new era with the world absorbing yet another FANG to add to the list of Facebook (FB), Alphabet (GOOGL), Amazon (AMZN), and Netflix (NFLX).

As the tech world powers on to new heights, nothing can slow down these juggernauts.

Let's face it - companies are more lucrative when technical expertise is ramped up and infused into the business model.

Ground zero of the tech movement - Silicon Valley - has helped supercharge the economy and prodigious earnings' results support this thesis.

New innovations will fuel the next level up in the tech arm's race but more crucially, so will new geographical locations.

Instead of throwing a dart at a world map, the locations are a no-brainer because tech scavenger hunts orbit around one idiosyncrasy and that is scale.

Scalability is a sacred word in the tech world.

If a start-up cannot scale up, investors can't imagine future profits, entrepreneurs can't imagine growth, and funding dries up.

End of story.

For instance, Amazon's business model does not mesh kindly with pint-sized Iceland.

Not because Amazon discriminates against Iceland's culinary delicacy of sheep testicles but because the population is only around 330,000 people.

Scale equals success.

Indisputably, every country with an Amazon-esque business is being bid up because big tech firms know how to digitally monetize, effectively out-sourcing an incredibly profitable business model that has worked unabated for the developed world for the past decade or two.

The heightened awareness of existential survival is pitting foreign money against each other in far-flung places jostling for the same digital assets after a decade of cheap financing enriching tech companies.

Remember that first mover advantage leads to dominance in the datasphere because the volume of data is directly correlated to the bottom line.

Examples are rife around the world, for instance Amazon's $580 million purchase of Souq.com, described as the Amazon of the Middle East headquartered in Dubai and the biggest e-commerce site in the Arab world.

E-commerce commands a paltry 2% of sales in the region. That number is poised to explode as digital-savvy, tech Millennials reach peak consuming age and the migration to mobile erupts.

A preemptive strike is usually the most compelling strategy for large cap tech as it pushes out the smaller players, which lack the resources to compete.

Even the corporate offices of Walmart (WMT) in Bentonville, Arkansas, would wholeheartedly agree with me after doling out for its new toy.

Yes, Walmart acquired a 77% share in the Amazon of India, Flipkart, for $16 billion after the real Amazon failed to cut a deal with the most famous e-commerce unicorn in India.

This new development is a game changer.

India is a country that tech executives pinpoint as the future because of its massive population, economic growth, and economic potential foreign investors hope to tap up.

The International Monetary Fund (IMF) has anointed India as the fastest growing economy in 2018, and the 7.4% growth this year will follow with an even sturdier 7.8% in 2019.

Amazon has been well aware of India's ascent. Its CEO Jeff Bezos pledged to invest more than $5 billion in India and Amazon began its e-commerce operation in 2013.

Amazon's early entrance into the Indian e-commerce industry has paid off grabbing 31% of market share putting it in second place behind Flipkart's 40%, according to big data firms.

The Indian e-commerce space was $20 billion in 2017, and by 2019, expect that number to grow to $35 billion.

Walmart CEO Doug McMillon noted that by 2026, the Indian e-commerce industry will surpass $200 billion. When it comes to clothing and fashion, Flipkart has a 70% share in India.

Even more valuable than the economic growth is the new pipeline of tech talent that will help Walmart compete with Amazon.

The Trump administration's crackdown on H-1B visas that Silicon Valley utilizes to bring developers to American shores has forced American tech companies to implement a work-around.

Essentially, the only difference now will be that the past recipients of H-1B visas will be sitting in an air-conditioned office in Bengaluru, India, until the visa documents come through.

Flipkart has a deep pipeline into the best engineering schools in India and the staff of more than 30,000 employees work on Indian wage levels.

This deal is one of the biggest talent grabs of tech developers the world has ever seen. And this group has the know-how of building an Amazon-style digital marketplace platform from zero.

The Flipkart investment comes after Walmart's purchase of Jet.com, an e-commerce company based in Hoboken, New Jersey.

The $3.3 billion purchase of Jet.com in 2016 was the beginning of Walmart's digital strategy, and it has come a long way in a very short time.

Walmart is now a vaunted member of the FANG group and has a new army of developers to back up this claim.

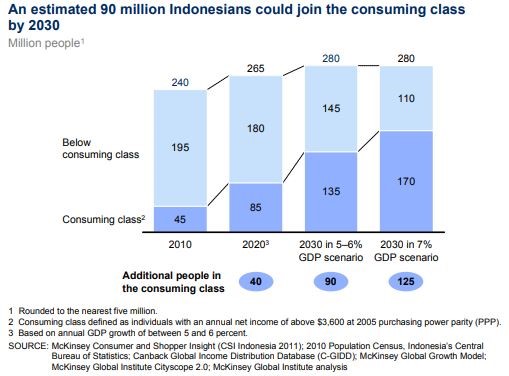

Glancing at the opportunities to scale, Indonesia is clearly the runner-up behind India.

Indonesia has been tagged as a tech new battleground with a population of 260 million in 2016 and growing.

The country has a medium age of 28, meaning this young population could turn into a reliable source of new tech developers who traditionally are young and digital natives.

Economic prosperity has been welcomed with open arms to this tropical island nation. It is poised to become the seventh largest economy by 2030, up from its rank of No. 16 today, creating a burgeoning middle class with newfangled discretionary spending.

The rural migration to urban environments will add another 90 million people living in Indonesian cities by 2030, while Internet access is growing by 20% each year in Indonesia.

Goldman Sachs recently issued a note to investors citing Indonesia's unbridled potential.

Capital is pouring into Indonesia at a breakneck speed with Alibaba investing $1.1 billion into Tokopedia, the Amazon of Indonesia.

Companies are coming to the stark realization that the domestic low hanging fruits have been picked, and aging developed countries are turning to undeveloped regions of growth to advance business objectives.

This is why South East Asia has been bombarded with an onslaught of Japanese, Korean, and Chinese investments and not only in the tech sector.

The Far East powerhouse countries are battling each other in Southeast Asia for consumer goods, infrastructure, high speed trains, and of course technology.

Uber just sold its Southeast Asian ride-sharing asset Grab to China's DiDi Chuxing and SoftBank for $2 billion.

The Southeast Asian region is one of the hottest places to make a deal because of a lack of FANG occupancy.

Walmart sold off on the Flipkart news because of the potential impairment to margins, but this move is a long-term positive for Walmart shareholders.

Flipkart does not turn a profit and Walmart is still solely judged by earnings. Unfortunately, it does not receive the same license to focus on growth like Tesla, Amazon, and Netflix.

However, I have a hunch that down the road, investors will agree this move by Walmart's McMillon was as shrewd as can be.

Like the colonial powers of yore, India and Southeast Asia are likely to be divvied up.

American companies already own more than 70% of market share in India e-commerce.

India is the biggest democracy in Asia and a staunch ally of the United States.

India's frosty relationship with China due to border spats and communist origins will stunt China's ability to take over and expand in India.

However, Southeast Asian countries are more likely to go the way of Cambodia, which is reliant on Chinese money to fund new initiatives, hamstrung by Chinese debt up to its eyeballs, and acquiesced political capital to the Mandarins.

Chinese investment's path of least resistance is Southeast Asia. This progression will be facilitated by the sizable Chinese expat population that resides in Indonesia, Vietnam, Thailand, Philippines, Myanmar, Laos and Cambodia.

Long-term shareholders of Amazon and Walmart will be rewarded. However, expect a few more Indians walking around Bentonville, Seattle, and Hoboken.

_________________________________________________________________________________________________

Quote of the Day

"My life is now a constant assessment of whether what's happening in real life is more entertaining than what's happening on my phone." - said television host Damien Fahey.

Global Market Comments

May 11, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON),

(MAY 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (MU), (NVDA), (AMZN), (GOOGL),

(TLT), (SPX), (MSFT), (DAL),

(MAD HEDGE DINNER WITH BEN BERNANKE)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader May 9 Global Strategy Webinar with my guest co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Would you still short Facebook (FB)?

A: Right now, no. I thought the dynamics changed off the last earnings report, so the answer is no. We have made a ton of money trading Facebook this year, and all of it has been from the long side.

Q: How will the election affect the market?

A: It will go down into the election, but you'll then get a strong rally as the uncertainty fades away. It really makes no difference who wins. It is the elimination of uncertainty that is the big issue.

Q: Do you have a price to buy Micron Technology (MU) or NVIDIA (NVDA), or do you want to wait for a crash day?

A: I want to wait for a crash day, because even though these are great companies, on the down days, they fall twice as fast as any other stock. Your entry point is very important in that situation.

Q: Do you see opportunities to sell short the U.S. Treasury bond market (TLT) again?

A: Yes. But wait for the four-point rally not the two-point rally.

Q: Rising interest rates should benefit banks - why are they such horrible performers?

A: The double in bank stocks in 2017 fully discounted this year's interest rate move. For banks to really perform interest rates have to move higher still, which they will eventually.

Q: When will the yield curve invert and what will be the implications?

A: You can take the Fed's current rate of interest rate rises (which is 25 basis points every three months) and essentially calculate that the yield curve inverts at the end of 2018 or the beginning of 2019. Recessions and bear markets always follow six months after that inversion takes place. That's when interest rates start to rise very sharply as bond investors panic and unwind all their leveraged long positions.

Q: Why are you not involved with Amazon (AMZN) and Google (GOOGL)?

A: I've already taken big profits in both of these and I'm just waiting for another serious dip before I get back in again.

Q: What happens to stock buybacks?

A: While other investors are pulling out of the market, stock buybacks are doubling. But, that is only happening, essentially, in the tech stocks - they're the buyback kings. If you don't have a serious buyback program this year, your stock is falling. Companies are the sole net buyers of the market this year, and they are only buying their own stocks.

Q: What do you see the upper and lower end of the S&P 500 (SPY) range to November?

A: I think we've already got it: 2,550 on the low side, 2,800 on the high side - that a 10% range and you can expect it to get narrower and narrower going into November. After that, we get an upside breakout to new all-time highs.

Q: When will rates be negative next?

A: In the next recession, the bottom of which will be in 2 to 2.5 years; that's when interest rates in the U.S. could go negative, as they did in Japan and Europe for several years.

Q: What is your No. 1 pick in the market today?

A: We love Microsoft (MSFT) long term. However, right now the background macro picture is more important than stock selection than any single name, so we're keeping a position in Microsoft in the Mad Hedge Technology Letter, but not in Global Trading Dispatch. We're sort of hanging back, waiting for another sell-off before we touch anything on the long side in GTD. Remember, the money is made on a buy in the new position, not on the sell going out.

Q: Was the semiconductor chip sell-off overdone?

A: Absolutely - the negative report was put out by a new analyst to the industry who doesn't know what he's talking about. If you ask all the end users of the chips, all they talk about is A.I., and that means exponential growth of chip demand.

Q: Is it a good time to buy airline stocks (DAL)?

A: No, until we get a definitive peak in oil, and a speed up again in the economy, you don't want to touch economically sensitive sectors like the airlines.

Mad Hedge Technology Letter

May 9, 2018

Fiat Lux

Featured Trade:

(HERE'S THE TOP STOCK IN THE MARKET TO BUY TODAY),

(MSFT), (AMZN), (AAPL), (APTV), (QCOM), (FB)

When the CEO of Microsoft, Satya Nadella, sits down for a candid interview, I move mountains then cross heaven and hell to listen to him, and you should, too.

Microsoft is at the top of my list as a conviction buy.

Nadella is one of the great CEOs of our time and was able to complete Microsoft's makeover after Steve Ballmer's insipid tenure at the helm.

Microsoft's Build conference is the perfect platform for Nadella to share his wisdom about the company, industry, and changes going forward.

In an age where tech CEOs thrive off of smoke and mirrors, Nadella was succinct conveying the concept of trust as the secret sauce that will help tech's digital footprint expand into new territories.

Trust infused products through the cloud and A.I. will be the perfect archetype of future tech that will encourage accelerated adoption rates.

A.I. was the message of the day at the Build conference. Nadella used the term A.I. 14 times and the word cloud four times when interviewed.

It was fitting that Microsoft wowed the audience with a sparkly, new-fangled demo.

The demo put on by Microsoft in conjunction with Amazon's (AMZN) Alexa showed smart-assistants working in collaboration.

Microsoft showed how it is possible to use a PC Windows desktop to order an Uber car through Amazon's Alexa.

This technology is very powerful and is a work-around for the "walled garden" problem where big companies are closing off their systems only to proprietary software and products limiting upside potential.

The ability to collaborate with multiple A.I. smart systems will generate a whole new layer of business catering toward the communication and business developments among A.I. systems.

Nadella also offered extended examples of A.I. applications, for instance, the capability of detecting cracks in an oil pipeline and running recognition software through a drone using a Qualcomm (QCOM) manufactured camera to monitor the state of containers.

Trusting A.I. will expedite the usage of A.I. business applications, and the companies diverting capital into A.I. enhancement will reap from what they sow.

The knock-on effect is that university A.I. staff members are being poached faster than a breakfast egg. There is a bidding war going on as we speak from both sides of the Pacific.

Facebook is opening new A.I. research centers in Seattle and Pittsburgh.

Previously, A.I. was a buzzword and companies would trot out a visually stimulating display with pizzazz. But that is all changing with A.I. swiftly moving into the backbone of all business operations.

Ottomatika, a company that develops software for autonomous cars acquired by Aptiv (APTV), was entirely a Carnegie Mellon University (CMU) in-house project that was picked up by Aptiv for commercial applications.

In one fell swoop, (CMU) lost a whole team of leading A.I. researchers.

Microsoft is a premium stock because it straddles both sides of the fence.

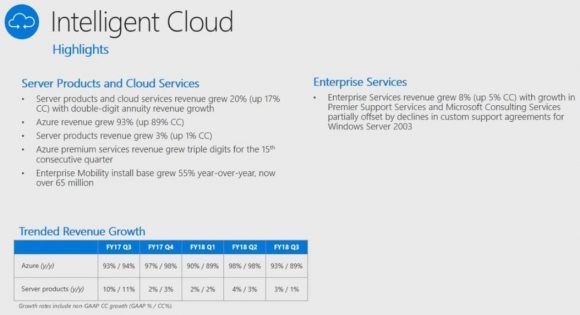

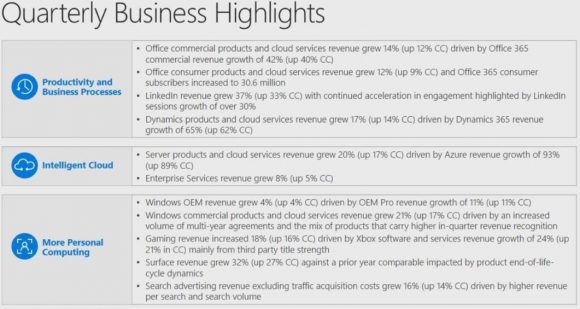

On one side, it's an uber growth company with Microsoft Azure growing 93% YOY satisfying investors requirement for insatiable growth.

On the other hand, Microsoft is robustly lucrative profiting $21.20 billion in 2017, and would be a Warren Buffett-type of cash flow reliant stock even though he has smothered any inkling of buying Microsoft shares because of his close relationship with co-founder Bill Gates.

Even Microsoft's legacy product Microsoft Office 365 is a gangbuster segment swelling 42% YOY.

This contrasts with other legacy companies that are attempting to wean themselves from their own outdated products.

Office 365 products are still embedded in daily life, and I am using it now to type this story.

On the technical side of it, Microsoft is beefing up its developer tools.

Microsoft will integrate Kubernetes, an open-source system for automating deployment, into the Azure as well as upping its Azure Bot Service adding 100 new features.

There are more than 300,000 developers who operate the Azure Bot Service alone.

The slew of upgrades for developers will enhance the power of Microsoft's software and ecosystem.

The overarching theme to the Build conference is the integration of A.I. into real life business applications and the importance of the cloud.

Now the Cloud.

Nadella reaffirmed Microsoft's position in the cloud wars characterizing the current environment as a duo of Amazon and Microsoft with Google trailing behind.

Microsoft has the potential to nick Amazon's position as the industry's cloud leader because of the unique set of products it can combine with the cloud.

Most of the world utilizes a mix of PC-based hardware, using Microsoft's software and operating system, supplemented by an Android-based smartphone.

As expected, Microsoft, Alphabet (GOOGL), and Amazon are spending a pretty penny advancing their cloud business.

Microsoft spends more than $1 billion per month on Azure cloud data centers.

This number now surpasses the entire annual Microsoft R&D budget.

In the interview, Nadella cited that Microsoft now has 50 domestic data centers.

Amazon habitually holds between 50,000 to 80,000 servers at each data center. Extrapolate the lower range of the number with 50 data centers and Microsoft could have at least 2.5 million servers working for its data needs.

The barriers of entry have never been higher in the cloud industry because the costs are spiraling out of control.

Few people have billions upon billions to make this business work at the appropriate scale.

Tom Keane, head of Global Infrastructure at Microsoft Azure, recently said that Azure meets 58 compliance requirements set forth by the federal government, industry, and local players.

Azure is the first cloud that satisfies the Defense Federal Acquisition Regulation Supplement criteria for contractors to handle Department of Defense work.

Regulation has emerged as one of the controversial issues of 2018, and this did not get lost in the shuffle.

The trust comment was clearly a thinly veiled swipe against Facebook's (FB) much frowned upon business model, making it commonplace these days for prominent CEOs to distance themselves from Mark Zuckerberg's creation.

Protecting a company's image and reputation is paramount in the new rigid era of big data.

Nadella's anti-Facebook rhetoric continued by noting the auction-based pricing standards are "funky," explaining the model is counterintuitive. His reason was that as demand increases, the price should drop and not rise.

Apple (AAPL) CEO Tim Cook has largely been negative about Facebook's tactics. The fury is justified when you consider Apple and Microsoft hustle industriously to develop software and hardware products while Facebook manipulates user data to profit from collected data. A nice shortcut if there ever was one.

It's clear that Apple and Microsoft have no interest in giving third parties access to personal data because the leadership understands it is a slippery slope to go down and unsustainable.

Nadella's emphasis on tech ethics is a breath of fresh air and the data Microsoft accumulates is used to improve the cloud and software products rather than pedal to mercenaries.

The companies that have staying power create proprietary products that cannot be replicated.

Microsoft's assortment of software products acts as the perfect gateway into the cloud and is a moat widening tool.

A.I. and the cloud are all you need to know, and Microsoft is at the heart of this revolutionary movement.

Any weakness of Microsoft's shares into the low-90s is a screaming buy.

_________________________________________________________________________________________________

Quote of the Day

"Innovation has nothing to do with how many R&D dollars you have. When Apple came up with the Mac, IBM was spending at least 100 times more on R&D. It's not about money. It's about the people you have, how you're led, and how much you get it." - said Apple cofounder Steve Jobs.

Mad Hedge Technology Letter

May 8, 2018

Fiat Lux

Featured Trade:

(BUFFETT GOES ALL IN WITH APPLE),

(SNAP), (WDC), (GOOGL), (AMZN),

(CRM), (RHT), (HPQ), (FB), (AAPL)

Not every stock comes with Warren Buffett's confession that he would like to own 100% of it. But, of course that stock would have to be a tech stock.

As it stands, the Oracle of Omaha owns 5% of Apple (AAPL), and his confession is still a bold statement for someone who seldom forays outside his comfort zone.

Buffett also continues to concede that he "missed" Google (GOOGL) and Amazon (AMZN).

What a revelation!

The outflow of superlatives invading the airwaves is indicative of the strength technology has assumed in the bull market.

The tech sector has been coping with obstacles such as higher interest rates, trade wars, data regulation, IP chaos, and the globalization backlash.

However, the tech companies have come through unscathed and hungry for more.

Their power is not contained to one industry, and techs' capabilities have been spilling over into other sectors digitizing legacy industries.

Every CEO is cognizant that enhancing a product means blending the right amount of tech to suit its needs.

It is not halcyon times in all of tech land either.

There have been some companies that have faltered or were naturally cannibalized by other tech companies that disrupt business.

Times are ruthless and this is just the beginning.

There will be winners and losers as with most other secular paradigm shifts.

Particularly, there are two types of losers that investors need to avoid like the plague.

The first is the prototypical tech company hawking legacy products such as Western Digital Corp. (WDC) that I have been banging on the table telling investors not to buy the stock.

The lion's share of revenue is still in the antiquated hard drive business that has a one-way ticket to obsolescence.

Yes, they are turning around product mixes to factor in its pivot to solid state drives (SSD), but they are late to the game and deservedly punished for it.

Compare WDC to companies that have completed the transition from legacy reliance to the cloud, and it is simple to understand that companies such as Microsoft, which struggled for years to turn around with CEO Satya Nadella, finally can claim victory.

The problem with WDC is the stock's price action performs miserably because the company is tagged as an ongoing turnaround story.

On the other hand, headliner cloud plays experience breathtaking gaps up due to the strength of the cloud such as Amazon (AMZN), Red Hat (RHT), and Salesforce (CRM), just to name a few.

To pour fuel on the fire, speculative reports citing NAND chip price "softening" beat down the stock into submission.

Effectively, legacy companies become sell the rallies type of stocks.

Transforming a legacy company into a high-octane cloud company is perilous to say the least. Jeff Bezos recently gloated that Amazon Web Service's (AWS) seven-year head start is all investors need to know about the cloud. There is some merit to his statement.

Examples are rife with bad executive decisions by legacy companies such as HP Inc. (HPQ), another legacy tech company that makes computers and hardware. It ventured out to buy Palm for $1.2 billion plus debt after a bidding war with legacy competitor Dell in 2010.

In 1996, the Palm PDA (Personal Digital Assistant) was the first smart phone on the market that predated BlackBerry's smart phone with the full keyboard made by RIM (Research in Motion).

The demise of Palm emerged from a hodgepodge of mismanagement, failed spin-offs, misplaced mergers, and resource wastefulness even with the preeminent technology of its time.

(HPQ)'s stab at the smartphone market resulted in purchasing Palm. However, after heavy selling pressure in its shares, HP shut down this division and sold off the remaining technology to Chinese electronics company TCL Corporation.

The sad truth is many transformations fail at step one, and there is no guarantee a newly absorbed business will perform as expected.

RIM, now changed to BlackBerry (BB), soon found out how it felt to be Palm when Steve Jobs dropped the first iPhone on the market, and the world has never been the same.

(BB) gradually morphed into an autonomous vehicle technology company after the writing was on the wall.

The other types of losers are companies with inferior business models such as Snapchat (SNAP), which I have written about extensively from the bearish side.

In an age where disruptors are being disrupted by other disruptors, CEOs must live in fear that their business will get undercut and hijacked at any time.

Instagram, a subsidiary of Facebook (FB), has permanently borrowed numerous features from Snapchat. Its Instagram "stories" feature is now used by more than 300 million daily users.

Snapchat is serving as Instagram's guinea pig while CEO Evan Spiegel finds an alternative way to survive against Facebook's unlimited resources.

Both are in the game of selling ads and nobody does it better than Facebook and Alphabet or has the degree of scale.

The recent redesign was met with a chorus of universal boos. The 60 minutes I spent testing the new design reconfirmed my fears that the new design was an unmitigated washout.

In short, Snap's redesign seemed like a different app and became incredibly difficult to use.

Compounding the deteriorating situation, Snapchat laid off 120 engineers due to sub-par performance and withheld last year's performance bonuses even though co-founder Evan Spiegel received $637 million in 2017.

The latest earnings report was a catastrophe.

Daily active user (DAU) growth, the most sought out metric for Snapchat, failed to deliver the goods. The street expected 194.2 million DAU and Snap reported 191 million. A miss of 3.2 million users and a deceleration of growth QOQ.

Remember that Snapchat is substantially smaller than Instagram and should have no problems surpassing expectations on a smaller scale, thus investors voted with their feet and bailed on the stock after the catatonic performance last quarter.

Instagram is six times larger with more than 800 million users as of the end of 2017.

Top line fell short of expectations and average revenue per user (ARPU) dropped to $1.21, far less than the expected $1.27.

The less than stellar redesign faced a rebellion from long-term Snapchat disciples. More than 1.2 million Snap diehards signed a petition hoping to revert back to the old interface, and its updated ratings in Apple's app store has fallen to 1.6 stars out of 5.

Then the perpetual question of why would advertisers want to pay for Snapchat digital ads when they earn more by buying Instagram ads?

This remains unsolved and appears unsolvable.

Snapchat is befuddled by the pecking order and the company is on a train to nowhere.

To hammer the nail in the coffin, Snapchat announced to investors that it expects revenue to "decelerate substantially" next quarter.

In an era where technology companies will lead the economy and stock market, and has an outsized influence in politics and culture, not all tech companies are one-foot tap-ins.

Investors need to separate the wheat from the chaff or risk losing their shirt.

_________________________________________________________________________________________________

Quote of the Day

"We have to stop optimizing for programmers and start optimizing for users." - said American software developer Jeff Atwood

Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

Everyone and their mother was waiting for Facebook (FB) to fluff their lines, but they defied the odds by posting solid performance.

The data police can go back to eating doughnuts because it is obvious that regulation won't fizzle out the precious growth drivers that Mark Zuckerberg relies on to please investors.

I even begged readers to buy the regulatory dip, and I was proved correct with Facebook shares rebounding from $155 to $173.

The dip buying was proof that investors have faith in Facebook's business model.

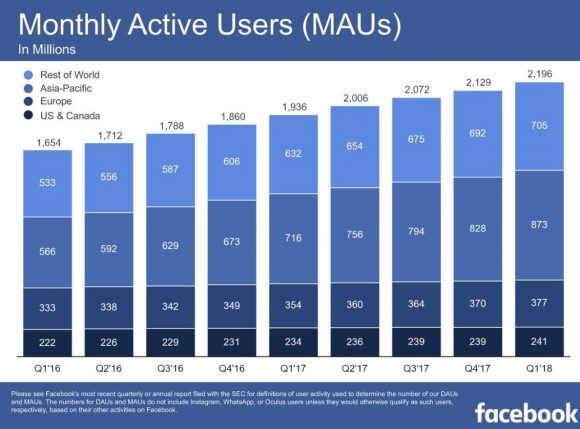

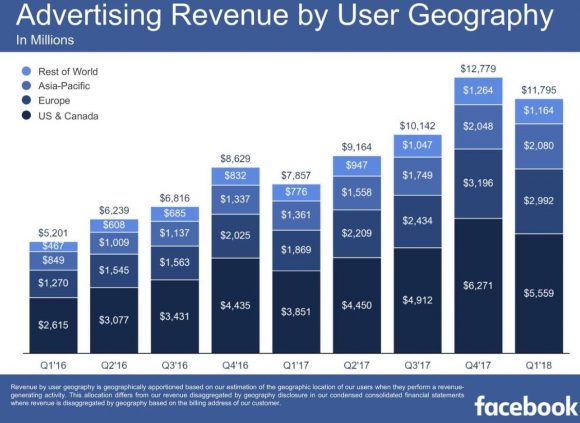

The Cambridge Analytica scandal threatened to tear apart the quarterly numbers and place Facebook in the tech doghouse, but stabilization in Monthly Active Users (MAU) and bumper digital ad revenue growth was the perfect elixir to an eagerly anticipated earnings report.

Facebook showed resilience by growing (MAU) to 2.2 billion, up 13% at a time when attrition could have reared its ugly head.

The market breathed a huge sigh of relief as the Facebook beat came to light.

The battering that Facebook received in the press effectively lowered the bar and Facebook delivered in spades.

The unfaltering migration to mobile continues throughout the industry with mobile digital ad revenue making up 91% of ad revenue, which is a nice bump from the 85% last quarter.

Overall, Facebook grew revenues 49% YOY to $11.97 billion.

There is no getting around that Facebook is a highly profitable business due to the lack of costs. I should be so lucky.

Remember at Facebook, the user is the product.

Instead of paying for rising TAC (Traffic Acquisition Costs) as does Google (GOOGL) or the $8 billion outlay for Netflix's (NFLX) annual content budget, Facebook pours its money into improving its digital platform and advancing its ad tech capabilities.

However, moving forward, Facebook will have to cope with extra regulatory costs.

Facebook recently hired a legion of content supervisors at minimum wage to root out the toxic content roaming around on its platform.

Site operators have doubled to 14,000. This number gives you a taste why the large cap tech names are best positioned to combat the new era of regulation.

Doubling the staff of any business would be a tough cost pill to swallow.

Many companies would go under, but Facebook has the cash to mitigate the additional cost of doing business.

This defensive initiative casts Facebook in a better light than before like a superhero rooting out the evil villain.

Facebook and its co-founder Mark Zuckerberg need to hire a better public relations team to ensure that Mark Zuckerberg isn't pigeonholed in mainstream media as the monster of tech.

The Amazon-effect is infiltrating every possible industry, and even the bigger tech names are coping with the Amazon (AMZN) spillage onto competitors' turf.

A risk down the line is Amazon's booming digital ad business nibbling away at Facebook's own digital ad model.

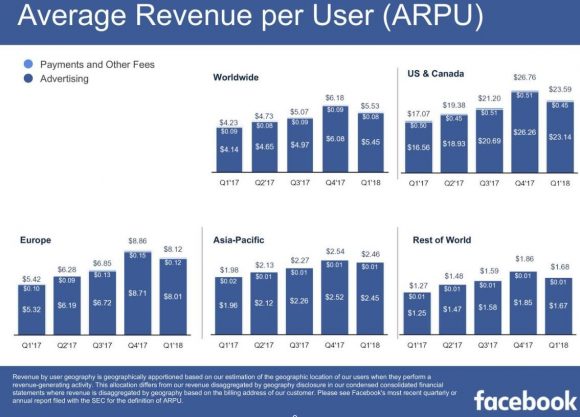

ARPU (Average Revenue Per User) remains robust with Facebook earning $23.59 per North American user, which is the most lucrative geographic location.

Artificial Intelligence (A.I.) is a tool that Facebook has implemented into its platform and monitoring apparatus.

Removing damaging content preemptively is the order of the day instead of being blamed for harboring nefarious content.

One example of this use case has been targeting ISIS- and Al Qaeda-related terror content with 99% of inappropriate content removed before being flagged by a human.

Heavy investments in A.I. will make Facebook a safer place to share content.

Big events exemplify the strength of Facebook.

During the Super Bowl in February, around 95% of national TV advertisers were simultaneously posting ads on Facebook because of the viral effect commercials and posts have during massive events.

Tourism Australia is another firm that bought ads on Instagram and Facebook platforms during the Super Bowl.

The campaign was hugely successful with half the leads for Tourism Australia coming directly from Facebook.

Facebook acts as the go-to provider for quality digital marketing and this will not change for the foreseeable future.

Investors can feel comfortable that there was no advertiser revolt after the big data chaos.

Facebook is improving its ad tech, and new ad products will be introduced to the 2.2 billion MAUs.

For instance, Facebook developed a carousel of rotating ads on Instagram Stories, and advertisers will be able to share up to three video or photos now instead of one. If the user swipes up, the swipe will take them directly to the advertisers' websites.

The shopping experience is more personalized now with an updated news feed that will show a full-screen catalog to help the user find whatever is in their search.

Facebook will only get better at placing suitable ads that mesh with the users' interests or hobbies.

Investors must be cautious to not let macro-headwinds sabotage existing positions.

Facebook's underlying growth drivers remain intact, but the stock is vulnerable to regulation headline risk that caps its short-term upside.

There is also the possibility that another Cambridge Analytica is just around the corner, which would result in a swift 10% correction.

Next earnings report should be interesting because it will reflect the first quarter that Facebook has operated with higher security expenses and will go a long way to validating its business model in a new era of rigid regulation.

If Facebook does not fill in the moat around the business, then Facebook is braced to grow top and bottom line with minimal resistance.

The cherry on top was the additional $9 billion of buybacks giving the stock price further support.

Facebook is a long-term hold but a risky short-term trade.

_________________________________________________________________________________________________

Quote of the Day

"Never trust a computer you can't throw out a window." - said Apple cofounder Steve Wozniak.