Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Jeff Bezos is a god.

Well, not quite but he is turning into one after Amazon delivered a mythical earnings report that left Amazon haters in awe.

The Amazon bears patiently waiting for the day of reckoning will have to wait longer as Amazon smashed earnings expectations by a magnitude of two or three.

Amazon had a lot riding on the most recent earnings report after racing to new highs in mid-March.

The brief macro-correction then gave investors yet another entry point into one of the best companies of our generation that is still up more than 30% this year.

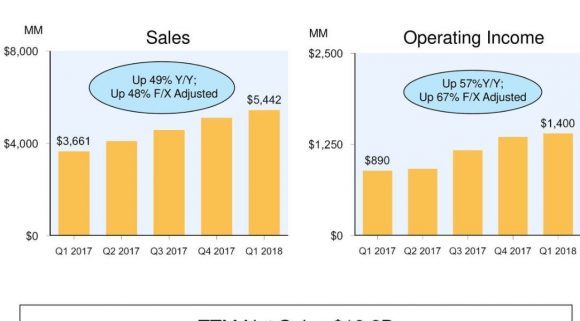

Amazon Web Services (AWS) revenue reaccelerated from its 42% growth last year to a high octane 49% YOY and made up a disproportionate 73% of Amazon's operating income.

Amazon is heavily reliant on the AWS segment to carry it through feast or famine.

According to Jeff Bezos, its critically acclaimed cloud segments' outstanding results originate from the "seven-year head start before like-minded competition."

This reaffirms the benefit of first-mover advantage with which large cap tech is obsessed.

There is room for other companies in the cloud space, with the cloud industry expanding 20% in 2018 to $186 billion.

Therefore, expanding by 20% is the bare bones minimum to be considered relevant.

Amazon has positioned itself to funnel in the most dollars that migrate toward the cloud as the industries pioneer and best of breed.

After the latest earnings report, Amazon is in pole position to become the first publicly traded $1 trillion company.

This latest quarter wrapped up its 62nd consecutive quarter of 20% plus growth.

And the commentary coming out of the earnings reports makes it almost certain that Amazon will capture more market share.

There were a few bombshells dropped that were unequivocal positives for investors.

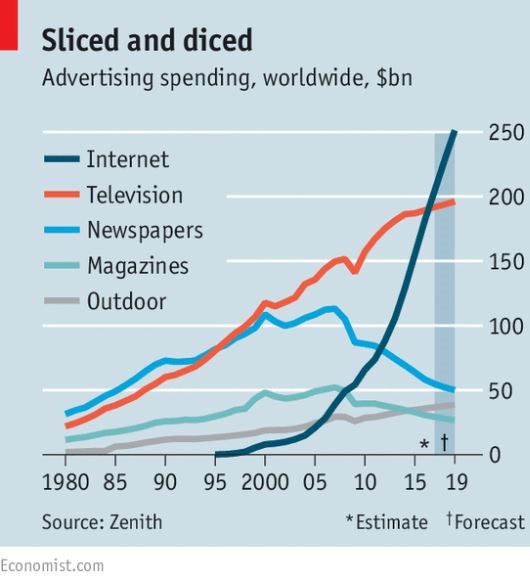

First, Amazon has become the third player in digital ad industry with the duopoly of Google search and Facebook.

Amazon revved up its digital ad revenue by 139% QOQ to a substantial $2.03 billion per quarter business.

This business is particularly appetizing because of its high margins and will help alleviate tight margins on the e-commerce side.

Amazon's digital ad business is by far the fastest growth lever in its portfolio. It will ramp up this side of the business whose main function is to match consumers with suitable products that consumers otherwise would miss out on in a standard Amazon search.

The extraordinary numbers support the notion that the hoopla of Washington regulation is all bark and no bite.

Facebook also delivered a prodigious quarter for the ages amid testimony and public backlash that resulted in immaterial damage to top- and bottom-line numbers.

The second bombshell announced was the change in pricing to prime members. Amazon upped its annual prime membership to $119 from $99.

This additional $20 price hike, or 20% on 100 million prime members, will swell revenue by an extra $2 billion of incremental revenue.

In total, Amazon will accrue a bonus of 4% of revenue by this price change.

Amazon has a high fixed-cost business, and slightly tweaking prices will create a huge windfall with the revenue almost entirely flowing down to the bottom line in the form of pure profit.

Many industry analysts claim that Amazon has the best management team in the industry and explicate this company as an "Internet staple."

More than 100 million products are delivered with free shipping for Amazon prime customers. This is starkly higher than the 20 million products shipped for free in 2014.

Amazon does everything in its power to offer a unique and efficient experience for customers.

The customer satisfaction reveals itself by the rock-bottom churn rate.

Amazon prime at an annual cost of $119 is such a value that no analysts even dared to ask Amazon CFO Brian Olsavsky if consumers would take issue with the rise in price.

Investors and strangers alike assume that broad-based reoccurring revenue from annual prime membership is a given.

In an era of mass-scrutinization, Amazon's earnings call seemed like a celebration of the mythical achievements that are changing consumer behavior by the day.

The lack of inquiry was justifiable this time because the one major shortcoming suddenly remedied itself.

Amazon's doubters frequently attack the lack of margin growth because its business model is first and foremost a land grab for market share ignoring any remnants of margin stability.

Now that Amazon's digital ad business has sprouted up, the margin story, starting from a miniscule base, will go from weakness to an unrelenting success.

Amazon started with its ultra-thin margin e-commerce business that made an operating loss of $160 billion in 2017.

Cranking up a shiny, high margin business will be hard for the other FANGs to compete with as they gyrate toward other businesses that have lower margins than Amazon's digital ad segment.

This is a horrible time to start fighting Amazon in price wars as the paradigm shift to quantitative tightening has made the cost of capital demonstrably pricier.

Operating margins almost doubled from 2% to 3.8% on $51 billion of quarterly sales.

This is a huge deal.

Amazon has been continuously harangued for "not making money." Well, that era is over.

Profits, and not only revenue, will start accelerating and Amazon will become the closest thing to a perfect company.

The years and years of plowing cheap capital back into fulfillment center and e-commerce activity gave Amazon a stained reputation for years.

However, as Amazon turns the screws and uses its foundational leverage to capture additional profits, the other FANGs will be forced down the same path ruining operating margins for the other big players.

Amazon telegraphed its quest for market share strategy to investors years ago, and investors understand they are paying for growth and growth only.

That will change now that profits have become a real part of its arsenal.

There is no doubt that Amazon will deploy its profits back into expanding its company because Jeff Bezos knows that if he can grow Amazon's top-line number, investors will follow suit.

Also, spending means improving the products, and Amazon has never hesitated to spend big.

The move into digital ad growth is a warning shot to Facebook and Google. Amazon will mobilize its workforce to take on other business, and anything that is high margin is fair game.

The future looks bleak for retail competitors Walmart and Target, as the contents of the earnings report reaffirms Amazon's unrelenting assault on the retail sector, which is systematically being dissected by Amazon for fun.

Google search and Facebook are in Amazon's crosshairs. Staving off this monster will be hard to do in the long run.

Amazon has a clear path to further market gains, and operating margins are almost at a tipping point.

Revenue is poised to re-accelerate because of the reignition of AWS to a higher growth trajectory.

Shoring up operating margins through a burgeoning digital ad division will only be a boon to earnings in the future.

Amazon is one of the best companies in the world, and any weakness in the stock should be bought and held forever.

_________________________________________________________________________________________________

Quote of the Day

"I do not fear computers. I fear a lack of them," - said writer Isaac Asimov.

Mad Hedge Technology Letter

April 25, 2018

Fiat Lux

Featured Trade:

(FANGS DELIVER ON EARNINGS, BUT FAIL ON PRICE ACTION),

(GOOGL), (AMZN), (MSFT), (AAPL), (FB),

(DBX), (NFLX), (BOX), (WDC)

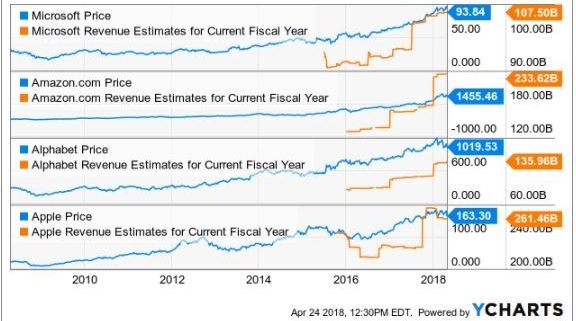

Alphabet (GOOGL) did a great job alleviating fears that large-cap tech would be dragged through the mud and fading earnings would dishearten investors.

The major takeaways from the recent deluge of tech earnings are large-cap tech is getting better at what they do best, and the biggest are getting decisively bigger.

Of the 26% rise to $31.1 billion in Alphabet's quarterly revenue, more than $26 billion was concentrated around its mammoth digital ad revenue business.

Alphabet, even though rebranded to express a diverse portfolio of assets, is still very much reliant on its ad revenue to carry the load made possible by Google search.

Its "other bets" category failed to impact the bottom line with loss-making speculative projects such as Nest Labs in charge of mounting a battle against Amazon's (AMZN) Alexa.

The quandary in this battle is the margins Alphabet will surrender to seize a portion of the future smart home market.

What we are seeing is a case of strength fueling further strength.

Alphabet did a lot to smooth over fears that government regulation would put a dent in its business model, asserting that it has been preparing for the new EU privacy rules for "18 months" and its search ad business will not be materially affected by these new standards.

CFO Ruth Porat emphasized the shift to mobile, as mobile growth is leading the charge due to Internet users' migration to mobile platforms.

Google search remains an unrivaled product that transcends culture, language, and society at optimal levels.

Sure, there are other online search engines out there, but the accuracy of results pale in comparison to the preeminent first-class operation at Google search.

Alphabet does not divulge revenue details about its cloud unit. However, the cloud unit is dropped into the "other revenues" category, which also includes hardware sales and posted close to $4.4 billion, up 36% YOY.

Although the cloud segment will never dwarf its premier digital ad segment, if Alphabet can ameliorate its cloud engine into a $10 billion per quarter segment, investors would dance in the streets with delight.

Another problem with the FANGs is that they are one-trick ponies. And if those ponies ever got locked up in the barn, it would spell imminent disaster.

Apple (AAPL) is trying its best to diversify away from the iconic product with which consumers identify.

The iPhone company is ramping up its services and subscription business to combat waning iPhone demand.

Alphabet is charging hard into the autonomous ride-sharing business seizing a leadership position.

Netflix (NFLX) is doubling down on what it already does great - create top-level original content.

This was after it shed its DVD business in the early stages after CEO Reed Hastings identified its imminent implosion.

Tech companies habitually display flexibility and nimbleness of which big corporations dream.

One of the few negatives in an otherwise solid earnings report was the TAC (traffic acquisition costs) reported at $6.28 billion, which make up 24% of total revenue.

An escalation of TAC as a percentage of revenue is certainly a risk factor for the digital ad business. But nibbling away at margins is not the end of the world, and the digital ad business will remain highly profitable moving forward.

TAC comprised 22% of revenue in Q1 2017, and the rise in costs reflects that mobile ads are priced at a premium.

Google noted that TAC will experience further pricing pressure because of the great leap toward mobile devices, but the pace of price increases will recede.

The increased cost of luring new eyeballs will not diminish FANGs' earnings report buttressed by secular trends that pervade Silicon Valley's platforms.

The year of the cloud has positive implications for Alphabet. It ranks No. 3 in the cloud industry behind Microsoft (MSFT) and Amazon.

Amazon and Microsoft announce earnings later this week. The robust cloud segments should easily reaffirm the bullish sentiment in tech stocks.

Amazon's earnings call could provide clarity on the bizarre backbiting emanating from the White House, even though Jeff Bezos rarely frequents the earnings call.

A thinly veiled or bold response would comfort investors because rumors of tech peaking would add immediate downside pressure to equities.

The wider-reaching short-term problem is the macro headwinds that could knock over tech's position on top of the equity pedestal and bring it back down to reality in a war of diplomatic rhetoric and international tariffs.

Google, Facebook, and Netflix are the least affected FANGs because they have been locked out of the Chinese market for years.

The Amazon Web Services (AWS) cloud arm of Amazon blew past cloud revenue estimates of 42% last quarter by registering a 45% jump in revenue.

Microsoft reiterated that immense cloud growth permeating through the industry, expanding 99% QOQ.

I expect repeat performances from the best cloud plays in the industry.

Any cloud firm growing under 20% is not even worth a look since the bull case for cloud revenue revolves around a minimum of 20% growth QOQ.

Amazon still boasts around 30% market share in the cloud space with Microsoft staking 15% but gaining each quarter.

AWS growth has been stunted for the past nine quarters as competition and cybersecurity costs related to patches erode margins.

Above all else, the one company that investors can pinpoint with margin problems is Amazon, which abandoned margin strength for market share years ago and that investors approved in droves.

AWS is the key driver of profits that allows Amazon to fund its e-commerce business.

Cloud adoption is still in the early stages.

Microsoft Azure and Google have a chance to catch up to AWS. There will be ample opportunity for these players to leverage existing infrastructure and expertise to rival AWS's strength.

As the recent IPO performance suggests, there is nothing hotter than this narrow sliver of tech, and this is all happening with numerous companies losing vast amounts of money such as Dropbox (DBX) and Box (BOX).

Microsoft has been inching toward gross profits of $8 billion per quarter and has been profitable for years.

And now it has a hyper-expanding cloud division to boot.

Any macro sell-off that pulls down Microsoft to around the $90 level or if Alphabet dips below $1,000, these would be great entry points into the core pillars of the equity market.

If tech goes, so will everything else.

If it plays its cards right, Microsoft Azure has the tools in place to overtake AWS.

Shorting cloud companies is a difficult proposition because the leg ups are legendary.

If traders are looking for any tech shorts to pile into, then focus on the legacy companies that lack a cloud growth driver.

Another cue would be a company that has not completed the resuscitation process yet, such as Western Digital (WDC) whose shares have traded sideways for the past year.

But for now, as the 10-year interest rate shoots past 3%, investors should bide their time as cheaper entry points will shortly appear.

_________________________________________________________________________________________________

Quote of the Day

"Technology is a word that describes something that doesn't work yet." - said British author Douglas Adams.

Mad Hedge Technology Letter

April 24, 2018

Fiat Lux

Featured Trade:

(WHAT THE MEDIA REALLY WANTS FROM YOU),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Publishing magnate and self-described populist William Randolph Hearst was a deep admirer of Adolph Hitler and did not shy away from using his newspapers as a de-facto mouthpiece spouting off Der Fuhrer's propaganda.

Hearst created content sympathizing with the Nazi ethos and even mobilized an embedded secret agent from the German government to act as a correspondent that followed hot, daily scoops inside Germany.

Hearst also used his publishing clout to pull the strings in the 1932 presidential election backing candidate John Nance Garner or "Cactus Jack" who later agreed to be Franklin D. Roosevelt's running mate.

The fusion of politics and media has been chiseled into human DNA since antiquity. However, the purpose of newspapers has evolved significantly since it became impossible to break even about 10 years ago.

Print newspapers are a lot like the US Postal Service - they specialize in losing money.

However, the (USPS) was never politicized as was the publishing industry until President Trump managed to commingle the loss-making mail outfit and Amazon as a joint problem roiling society.

The politicization comes at a cost to society.

All the well-intentioned journalists involved in earnest and quality journalism lose out because the new normal for newspapers has evolved into a William Hearst-like blatant tool promoting targeted interests.

Do you ever wonder why the Washington Post hardly ever publishes content harmful to the image of Amazon?

Because it is owned by the same man, Jeff Bezos, who founded Amazon (AMZN) in 1994, as he cruised in his car cross-country from New York to Seattle where he would start his tech empire.

Effectively, Jeff Bezos has the ear of each corner of the political power grid in Washington.

And while the president has been attacking Bezos as a job destroyer on a daily basis, Amazon has in fact been the largest private job CREATOR in the US. It added a staggering 130,000 new jobs in 2017, and an eye-popping 560,000 jobs over the past 10 years.

Last year saw Laurene Powell Jobs, widow to Steve Jobs, acquire the Boston-based American magazine The Atlantic.

The Atlantic earns more than $10 million per year in revenue and lures in over 33 million readers per month.

Billionaire biotech investor Patrick Soon-Shiong reached a deal with Tronc Inc. (TRNC), which possesses a vast array of various legacy media assets, to take over the LA Times and San Diego Union-Tribune for $500 million.

Tronc Inc. is on the verge of catching another bid with SoftBanks' (SFTBY) Masayoshi Son, looking to scoop up parts of the extensive portfolio.

Private equity group Apollo and media firm Gannett Company are also in the mix to acquire Tronc Inc.

Some of Tronc Inc.'s crown assets are the Chicago Tribune, the New York Daily News, and the Baltimore Sun among other regional newspapers with a large audience base.

Tronc's shares spiked almost 10% on whispers of the rumored news.

The courting of these news media assets comes at a time when Google (GOOGL) is funding a project to automate more than 30,000 stories per month for the local media as a cost-effective way to advance the business model.

Quality journalism written by a human is the last thing in which these mega-tech companies are interested.

The first thought that came into my head when I heard about SoftBank's vision fund swooping in for another company was data grab.

We have seen this story time and time again.

Newspapers and how an online subscriber behaves on a digital newspaper platform offer valuable data points that cannot be extracted elsewhere.

The data will reveal the political ideas, topics of interest, and other sensitive information deduced into a comprehensive data profile.

Effectively, a company such as SoftBank will be able to create a functional shadow profile for almost anyone.

The concept of shadow profiling emerged from the acrimony of Mark Zuckerberg's testimony in Washington and could be the next point of heated contention.

What are shadow profiles?

Shadow profiles are digital profiles crafted by data that were not directly handed over to Facebook (FB) by the user.

This data is extracted through fringe third parties, other friends on Facebook if they post content unique to you, and specifically through the "find your friends" function that recommends the uploading of an entire digital address book giving Facebook access to everyone you know.

Scarily, there is no opt-out for shadow profiling, and there probably won't be another congressional testimony about this topic anytime soon.

If Facebook wanted to turn into the FBI, it would be easy.

The treasure trove of data would give insight on the subtle nuances of authentic human behavior.

This artificial profile would seem real.

If you are an Android user like most of the world, Google could fill out the most comprehensive profile with a high degree of accuracy on most people.

The scandalous bit about shadow profiling is that these profiles are whipped up even if a user has never signed up for Facebook.

Shadow profiling, along with other data, becomes more precise as the volume of data piles up. To understand the behavior, trends, and tastes of most of the world's population is incredibly valuable.

Facebook could use this shadow profiling data to understand the wide range of non-Facebook user behavior.

This way of monetizing data would be highly illegal if leaked to an actionable third party and would be significantly worse than the Cambridge Analytica scandal.

This data should be deleted immediately, but Facebook has a backdoor way to keep the data in the system.

If Facebook got slammed for data leakage then others are in danger, too. That's because Facebook is not the only player mining data for money.

It wouldn't be surprising if other large cap tech companies started to create these shadow profiles to get dirt on their competitors as well as other use cases.

Tech is evolving at such a fast pace. It subconsciously encourages the never-give-up mentality that coerces firms to stay one step ahead, which Amazon has been able to do since its inception.

Newspaper companies are next in line to be absorbed by large cap techs continuously expanding web assets that hyper-focus on exponential data generation.

These newspapers will defend tech's interests in the economy similar to how newspapers were used as William Hearst's rallying cry for politics.

Jeff Bezos has chosen silence to react to President Trump's tweet offensive, but he could easily mobilize his newspaper to protect Amazon's interests.

Bezos just shrugs his shoulders and goes about his day because he knows Washington cannot do anything to change Amazon's dominance at the top of the tech food chain.

Better take the high road.

Not only do these big tech companies know who you talk to, what you buy, and where you are, but now they are given deeper access into the identity of users.

Be on the lookout for these assets to get cherry-picked and look forward to reading your future newspaper owned by Google, Facebook and the usual cast of characters.

The recently elevated existential risk that big cap tech is coping with will see meaningful reforms that will implement better defensive tactics, pre-emptive posturing to promote a positive big-picture narrative, and a bulletproof attempt to protect the moats around lucrative business models.

Stay away from these legacy newspaper stocks and only weigh up the media stocks that have already pivoted to the online streaming business model of scaling original premium content.

__________________________________________________________________________________________________

Quote of the Day

"The real danger is not that computers will begin to think like men, but that men will begin to think like computers." - said journalist Sydney Harris.

Mad Hedge Technology Letter

April 19, 2018

Fiat Lux

Featured Trade:

(HOW ROKU IS WINNING THE STREAMING WARS),

(ROKU), (FB), (AMZN), (NFLX), (GOOGL), (BBY), (DIS)

The whole digital ad industry dodged a bullet.

Facebook (FB) CEO Mark Zuckerberg's wizardry on Capitol Hill will stave off the data regulation hyenas for the time being.

One company in particular is perfectly placed to reap the benefits.

The Facebook of online streaming - Roku (ROKU).

Roku is a cluster of in-house, manufactured, online streaming devices offering OTT (over-the-top) content in the form of channels on its proprietary platform.

The company has two foundational drivers propelling business - selling hardware devices and selling digital ads.

It pays dividends to be entrenched at the intersection of two monumental generational trends of cord cutters' mass migration to online streaming, and the disruption of the digital ad revolution that is shaking up traditional media giants.

The percentage of American homes paying for an online streaming service ripped higher to 55% of households, which is up from 49% the previous year.

This $2.1 billion per month spend on streaming service is specifically as a result of access to premium content at an affordable price relative to traditional cable bundles.

Roku is a microcosm of the healthy climate for quality technology stocks in 2018.

It is among countless other firms that leverage large-scale data or cloud tools to capture profits.

Roku is best of breed of smart TV platforms and is in the early stages of robust growth.

This year will be the first year Roku's ad revenue surpasses hardware sales, indicating strong platform growth.

Roku pinpointed building account user growth, top-line gross revenue, and enhancing the platform capabilities as ways to move the business forward.

This year will also be the first year Roku posts an overall profit.

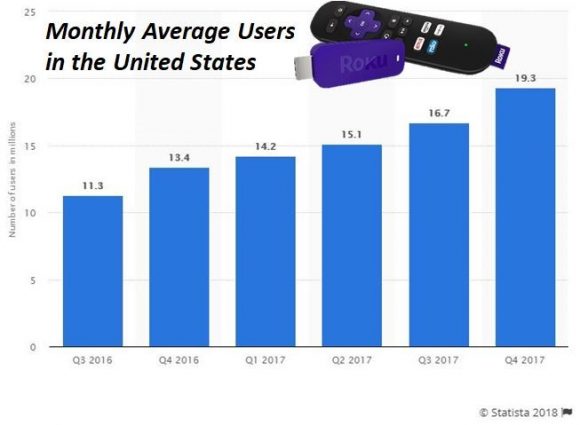

Active accounts grew 44% YOY to 19.3 million.

Roku offers consumers a cheap point of entry selling its Roku express box for only $29.99.

Its device is even free with a two-month purchase of Sling TV, which is the best online substitute to a legacy cable package. It has two sets of unique bundles available, charging $20 per month and $40 per month.

Once the Roku home screen populates, users can choose content through a la carte streaming options.

There is no monthly fee to operate Roku, and the device is used primarily by millennials.

More than 60% of 18- to 29-year-olds watch TV from online streaming, according to a Pew survey.

The quality and easy-to-use interface aids user navigation across the ecosystem.

It's the most convenient avenue to subscribe to multiple online streaming services all on one platform. It entices finicky users with extra mobility - those who love to jump around to different services based on particular upcoming content loaded up in the pipeline.

Many of these services offer no contract, cancel-anytime models that millennials love rather than the "old-school" rigid rules of cable providers that mostly charge a cancellation penalty of $300.

It is shocking how far traditional media fell behind the curve, but they are in rapid catch-up mode now.

Remember that content is king, and the overall boost in content quality has really shaken Hollywood executives to their core.

The golden age of streaming continues unabated with a Netflix 2018 annual content budget of $8 billion.

Roku does not create original content and it desires no skin in the game.

Content is expensive, and Roku would rather become the best place to host it.

Netflix's 2017 total revenue was a staggering $11.69 billion in 2017, and content costs will easily surpass 50% of total revenue in 2018. Overnight, it has become one of the biggest players in Hollywood, as its presence at the Emmy Awards amply demonstrates.

Exorbitant content costs are the new normal in 2018, and Spotify has reason to moan about the cost of content being 79% of total revenue.

Heightened content costs are the main reason why firms relying on content creation lose money each year.

However, as the overall pie grows, there is room for the tide to lift all boats. Being the premier platform to host premium content is why Roku's business model is eerily similar to Facebook's hyper-targeting ad model.

They make money the same way.

The incessant demand for online streaming functionality and smart TV operating systems show no signs of waning with Amazon (AMZN) announcing a new partnership with frenemy Best Buy (BBY) to produce smart TVs with Best Buy's in-house TV brand Insignia.

This is the first time Best Buy has been afforded a direct route to Amazon customers.

Disney (DIS) is turning around its legacy company into an online streaming behemoth announcing its first foray into online streaming with ESPN+.

Disney has tripled down on online streaming, acquiring New York-based BAMTech in late 2017, a company focused on developing streaming technology and made famous by its production of pro baseball's MLB TV.

BAMTech exudes pure quality. Anyone who has used MLB TV streaming service understands the great end-product it offers consumers.

The outstanding success with MLB TV attracted new online streaming converts to BAMTech to execute the transition to online streaming, including the WWE, Fox Sports, PlayStation Vue, and Hulu.

HBO went to BAMTech in 2014, after botching its attempt at creating a reliable stand-alone streaming service.

Disney's BAMTech-produced online streaming service will come to market in 2019, and will certainly be available on Roku TV.

Expect new blockbuster hits to debut on this new streaming service, such as new versions of Star Wars.

It is the perfect stock to mutate into an online streaming service because it possesses amazing content especially through ESPN.

The announcement of ESPN+ levitated Roku shares by 10% because investors understand this is the first baby step to shifting more of its content online.

This was on top of the announcement that Stephen A. Cohen's Point72 Asset Management had acquired a 5.1% stake in Roku for about $14 billion.

Furthermore, every major streaming service that enters Roku's system is worth an extra 5% to 10% bump in share price because of the wave of eyeballs and digital ads that grow Roku's coffers.

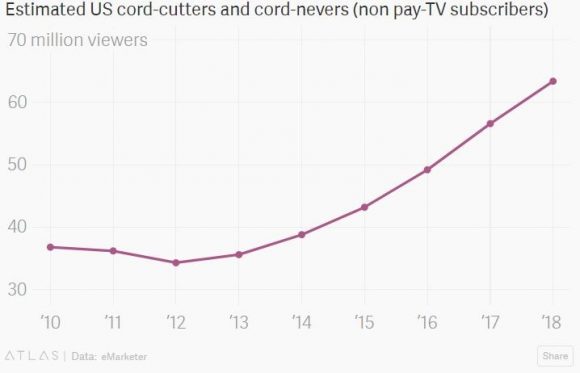

It is certain that 2018 and 2019 will sway more cord cutters to adopt Roku TV as this cohort approaches 70 million in 2018 on its way to 80 million in 2019.

The critical growth lever is its digital ad business as it hopes to take home a slice of this $70 billion per year business that is 75% controlled by Alphabet (GOOGL) and Facebook.

Roku has made great strides with half of Ad Age's top 200 advertisers already on the Roku interface.

Roku is taking the playbook right out from under Facebook's nose, piling funds into further enhancing its ad-tech division.

The blood, sweat, and tears shed is showing up in the financials with ARPU (Average Revenue per User) rocketing by 48% YOY, and more than 65% of this gap up is attributed to digital ad revenue.

Total revenue was up 29% YOY to $513 million, and platform revenue grew 129% in Q4 2017 to $85.4 million.

It is estimated that ad revenue will surpass $300 million in 2018, up from around $200 million in 2017.

Roku expects total revenue to grow 32% in 2018, approaching $700 million.

Profit margins are thriving under the platform segment, pumping out a stellar 74.6% in gross margin.

Roku does not make money on the hardware. Its push into ad distribution will ramp up as its digital ad revenue beelines toward an expected $700 million windfall by 2020.

Roku has a fantastic growth trajectory relative to other tech companies. Heightened volatility will make sell-offs hard to swallow but give fabulous entry points into a budding business.

The fertile path of international user adoption has barely scratched the surface. However, Netflix's successful foray abroad will inject confidence that Roku will have no problem expanding to greener pastures overseas as domestic account growth is always first to mature.

__________________________________________________________________________________________________

Quote of the Day

"AI is one of the most important things humanity is working on. It is more profound than electricity or fire." - said Google CEO Sundar Pichai

Mad Hedge Technology Letter

April 18, 2018

Fiat Lux

Featured Trade:

(WHY YOU SHOULD STILL BE BUYING FACEBOOK ON THIS DIP),

(FB), (GOOGL), (AMZN), (NFLX)

He did just enough.

He did 5% enough, but it should have been 10%.

That was the performance of the highly controversial data company Facebook (FB) in the wake of Mark Zuckerberg's (the aforementioned "he") testimony in front of politicians who failed to correctly pronounce his name let alone understand his business model.

But Zuckerberg did well.

Well enough that investors approved in droves.

Facebook shares tanked after the Cambridge Analytica scandal was disclosed, and the stock traded 16% below its February high.

The FANG stocks lost more than $200 billion in market value at one point when the headlines went viral.

Amazon (AMZN) and Netflix (NFLX) accounted for more than 30% of the S&P 500's 2018 gains in February, and their contribution has dipped to about 24% as of early April.

The leadership burden for large-cap tech is a resilient pillar propping up the equity market.

Let's get this straight - there has been no regulation as of yet but this moves forward any regulation that eventually was going to happen.

However, it could be a highly diluted version of any worst-case scenarios of which one could think.

The big question: Will earnings and guidance be sideswiped because of higher data costs?

And how many of the 2.2 billion MAU (Monthly Active Users) permanently deleted their Facebook accounts?

Facebook profile removals surged to 4,000 to 5,000 the first few days after the news hit and decreased to 2,000 per day in late March. The numbers further subsided to 1,000 at the start of April.

Deletions around the political testimony were clocking in between 1,000 to 2,000 per day.

To put this into perspective, the extirpation of accounts was only about 30% of the Snapchat rebellion where users quit in hoards because of a sub-optimal design refresh.

The media has done its best to sensationalize events and avoid the fact that hyper-targeting ad models has been around for years and has been used by various companies.

Facebook is not the only one.

Bottom line, there has been no material damage to user volume, and the testimony will empower tech because of Washington's botched question session.

Most of Facebook's profits come from less than 10% of user accounts.

Facebook is a one-trick pony with 98% of profits coming from ad revenue.

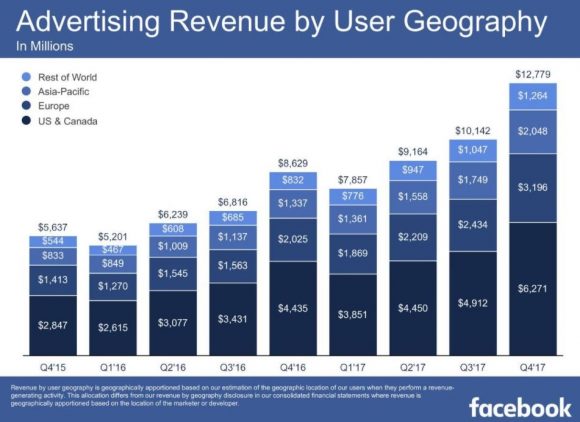

To add granularity, the bulk of revenue derives from developed nations mainly from North America, which make up more than 50%, and Europe at about 30% of total revenue.

Falling user engagement from the developed English speaking world would be a canary in the coal mine.

I am not talking about a few thousand profile deletions. However, a mass removal of 50,000 profiles or 100,000 profiles per day would throw Mark Zuckerberg into a tizzy.

If Facebook can convince users to stick around then Mark Zuckerberg is the ultimate winner.

With all the fearmongering, some facts get swept under the carpet. And it could be the case that many users are fine with Facebook possessing large swaths of their personal data.

In reality, users might prefer Facebook to Washington when it comes to possessing their personal information.

The performance of politicians lined up to interrogate Mark Zuckerberg was an unmitigated disaster for the political elite.

It is clear there is a competency issue with politicians. The generation bias has given us a fleet of politicians who have almost zero grasp of technology and its pervasive use in America's economy.

Many politicians showed a weak grasp of Facebook's profit engine.

Some politicians were more focused on Facebook's diversity policy than the real issue at hand.

Let's not forget Zuckerberg also controls 60% of voting rights through his accumulation of Facebook Class B shares and has an iron grip on any direction where the company traverses.

Any meaningful regulation costs will be passed onto the advertisers as a cost of doing business.

This is the key lever investors don't fully understand.

Facebook currently uses an auction-based system for ad pricing but could easily slip in stand-alone regulatory fees to compensate the extra costs.

The industries move from CPC (cost per click) to CPM (cost per impression) including duopoly playmate Alphabet (GOOGL) is a great strategy to pad profits.

The only real incurred cost to Facebook is the in-house DevOps team responsible for platform enhancement.

Facebook tried to experiment in 2016 by charging Facebook-owned smartphone messaging service WhatsApp users a $1 per year fee to use the messaging service.

It has done the groundwork to roll out a mass paid service.

Facebook later decided against this move as many users of WhatsApp are from undeveloped countries with no access to credit card payment services.

Zuckerberg is awkward. However, he has come a long way since his hoody days, even using smoke and mirrors to wriggle out of probing questions.

Half the "grilling" he received in Washington was met with the same vanilla answer saying that his team will get back to them.

The peak of evasiveness was Zuckerberg's response to a question about the willingness to change the business model in the interest of protecting individual privacy.

Zuckerberg stated he was "not sure what that means."

The hammering in Facebook shares was overdone.

It is obvious Washington is no match for large cap tech.

Facebook's upside trajectory has been sacrificed in the short term, but one could argue regulation was on the way - regardless of this data breach.

Regulation is a natural progression for an industry with almost no meaningful regulation.

Therefore, a little regulation for tech does not mean the end of tech.

Facebook is not going out of business. Not anytime soon.

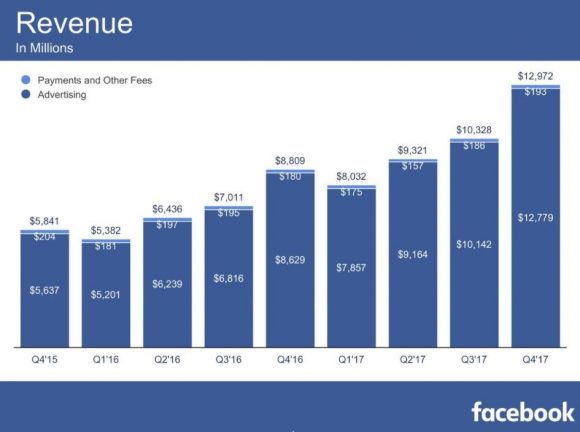

Facebook earned revenue of $27.64 billion in 2016, on the back of $40.65 billion in 2017.

Facebook does not need to be "fixed" - it just needs a few bandages in place before it goes back onto the field.

These bandages will damage operating margins that are currently at 57% in Q4 2017, but their long-term fundamentals are still intact.

The wall of worry is unfounded and ad engagement is still solid.

Facebook is in store for record bottom- and top-line numbers when earnings come out. Ad revenue numbers and the guidance will be the key metric to digest.

Investors might want Zuckerberg to kitchen sink the quarter because most of the bad news is already priced into the stock and might as well dig out all the skeletons in the closet.

Regulation is positive for Facebook because Facebook and the rest of the FANGs are in the best position to confront the regulations. The worst case scenario is finding a backdoor way to navigate through the new rules just as the backdoor way of profiting through ad distribution.

The headline hysteria makes it seem like Facebook is about to go under and file Chapter 11.

The bar has been set so low for upcoming earnings that any reasonable guidance will be seen as a victory.

Advertisers have no choice but to pay for Facebook ads if they want to grow business - that has not changed.

Facebook is growing so fast that the CEO could not name the competition when he was asked at the hearing.

There is a huge short squeeze setting up for the next earnings report due out on April 25, 2018.

Lastly, WhatsApp recently surpassed 1.5 billion MAU with users sending more than 60 billion messages every day.

Remember that Mark Zuckerberg purchased WhatsApp when it had around 500 million MAU back in February 2014.

This service hasn't even started to monetize yet and was a genius piece of business for $19.3 billion in 2014.

The valuation is at least double to triple the price of purchase now but seemed ludicrously expensive when Facebook snapped it up at the time.

Facebook has bottomed out, and the added bonus is it is quite insulated from all the tariff chaos whipsawing the equity markets.

__________________________________________________________________________________________________

Quote of the Day

"I'm on the Facebook board now. Little did they know that I thought Facebook was really stupid when I first heard about it back in 2005."- said founder and CEO of Netflix Reed Hastings