Global Market Comments

March 18, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR A STIFF DOSE OF HUMILITY),

(FCX), (AAPL), (IWM), (SPY), (BA), (FXI), (FXB)

Global Market Comments

March 18, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR A STIFF DOSE OF HUMILITY),

(FCX), (AAPL), (IWM), (SPY), (BA), (FXI), (FXB)

Sometimes markets have to give you a solid dose of humility, blindside you with a sucker punch, and slap you across the face with a wet kipper. Last week was definitely one of those weeks for me.

It was only just a matter of time before this happened. We posted new record gains for the first ten weeks of 2019. It was just a matter of time before the reality check kicked in.

I believed that we have seen the sharpest rally in stocks since the 2009 bottom, we were overdue for a respite. That respite came and only lasted a week. It has been an especially frustrating week for those few of us who watch economic data because it has been unremittingly awful while stocks rose daily.

There were really no reasons for shares to rise that week. There were also no reasons to sell, other than a dozen or so complete disasters that are looming just over the horizon. Still, to quote an old friend of mine, “Markets can remain irrational longer than you can remain liquid.”

The bull market reached ten years old last week, and if you read this letter you caught every dollar of the move up since then, plus some. But how much longer will it last? The technicals say it’s already in its death throes.

China trade negotiations (FXI) endlessly continued as they have for a year, but now the Chinese have thrown up a roadblock. They want everything in writing. In the wake of the North Korean disaster, can you blame them? This will weigh heavily on stocks until it's done.

Another day, another Brexit vote failed again. The pound (FXB) is doing the Watusi. Avoid all UK plays until the issue is decided.

The share buyback blackout started on Friday for many companies which are not allowed to repurchase their own shares up to 30 days ahead of the Q1 earnings reports. If you take the largest buyers of shares out of the market, what is left? Look to play the short side for the market.

Boeing (BA) hit bottom as the US became the last country to ban the 737 Max 8. Imagine being 35,000 feet in the air and you find out your plane is grounded for safety reasons, as 6,000 people did last week. Buy more (BA) on the dip. The next move is from $360 to $450.

Weekly Jobless Claims jumped, by 6,000 to a seasonally adjusted 229,000. Notice claims aren’t falling anymore. Another sign the tax cut stimulus is shrinking? Or that there is no one left to hire with any skills whatsoever?

Tesla (TSLA) released its Model Y SUV, but the cheaper $39,000 version won’t be available until 2021 and the stock dove. We are approaching the make or break level for the stock, the bottom of a two-year range. Get ready to buy on the meltdown. This is a ten bagger in a decade. Buy (TSLA).

The Mad Hedge Fund Trader lost ground last week. The tenth rally in 11 weeks made my short positions lose money faster than my long positions could make it back.

The Mad Hedge Technology Letter was stopped pit of a short position in Apple (AAPL) for a small loss a heartbreaking three days before its options expiration.

February came in at a hot +4.16% for the Mad Hedge Fund Trader. March started negative, down -2.18%.

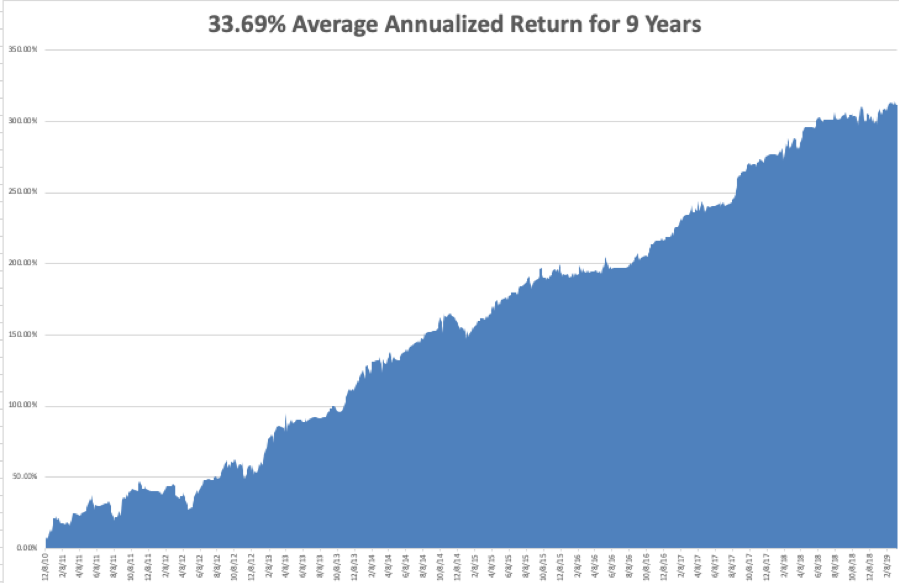

My 2019 year to date return retreated to +11.46%, a new all-time high and boosting my trailing one-year return back up to +23.72%.

My nine-year return pared back to +311.60%. The average annualized return appreciated to +33.69%.

I am now 60% in cash, 20% long Freeport McMoRan (GLD), 10% short the S&P 500, and 10% short the Russell 2000. My short bond position (TLT) expired at its maximum profit point of $1,140.

As for the Mad Hedge Technology Letter, it covered its short in Apple (AAPL) for a small loss.

Q4 earnings reports are pretty much done, so the coming week will be pretty boring on the data front after last week's fireworks.

On Monday, March 18, at 10:00 AM EST, the March Homebuilders Index is out.

On Tuesday, March 19, 8:30 AM EST, February Housing Starts is published.

On Wednesday, March 20 is the first official day of Spring, at last!

Thursday, March 21 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 10:00 AM, we get a new number for Leading Economic Indicators.

On Friday, March 22 we get a delayed number for Existing Home Sales.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, it’s fundraising time here in the San Francisco Bay Area for local schools and gala balls are now a weekly event. I, who have pursued a lifelong pursuit of low prices and great deals, ended up paying $1,000 for a homemade coffee cake, $7,000 for tickets to the Golden State Warriors, and $10,000 for the best table in the house. Hey, what’s the value of money if you can’t spend it? You can’t take it with you.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 8, 2019

Fiat Lux

Featured Trade:

(MARCH 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (SDS), (TLT), (TBT), (GE), (IYM),

(MSFT), (IWM), (AAPL), (ITB), (FCX), (FXE)

Well, that was some week!

After moving up in a straight line for ten weeks, markets are now doing their best impression of a Q4 repeat.

The transports Index (XTN), the most important leading indicator for markets, has been down for 11 straight days, the worst run in 40 years.

And now for the bad news.

Look at a long term chart for the S&P 500 (SPY) and the head and shoulder top practically leaps at you and grabs you by the lapels (that is, if you are one of the few who still wears a suit).

It makes you want to slit your wrist, jump off the nearest bridge, or binge watch all nine seasons of The Walking Dead. It neatly has the next bear market starting around say May 10 at 4:00 PM EST, a rollover point I put out two years ago.

However, hold that move! As long as we have a free Fed put under the market in the form of Jay Powell’s “patience’ policy, we are not going to have a major crash any time soon. That is 2021 business.

It's more likely we trade in a long sideways range until the economy finally rolls over and dies. So when we hit my first (SPY) downside target at the 50-day moving average at $269, which is a very convenient 5% down from the recent top, could well bounce hard and I might add some longs in the best quality names. It all sets of my dreaded flatline of death scenario for the rest of 2019.

Last week saw an unremitting onslaught of bad news from the economy.

The February Nonfarm Payroll report came in at a horrific 200,000 when 210,000 was expected, sending traders to man the lifeboats. The headline Unemployment Rate dropped 0.2% to 3.8%. Average Hourly Earnings spiked 11 cents to $27.66, a 3.4% YOY gain and the biggest pop since 2009.

Construction lost 31,000 jobs, while leisure and Hospitality added no jobs at all. The stunner is that the U6 long term structural “discouraged worker” unemployment rate dropped an amazing 0.8% to 7.4%, the sharpest drop on record. Fewer jobs, but at higher wages is the takeaway here, the exact opposite of what markets want to hear.

US Construction Spending fell off a cliff, down 0.6% in December. It seems that nobody wants to invest ahead of a recession.

The dollar soared (UUP), and gold (GLD) got hammered. You can blame the slightly stronger GDP print on Thursday the week before, which came in at 2.2% instead of 1.8%. As long as Jay doesn’t raise interest rates this is just a brief short covering rally for the buck.

China cut its growth forecast from 6.5% to 6.0% GDP growth for 2019. The trade war with the US and the stimulus hasn’t kicked in yet. The last time they did this, the market fell 1,000 points. Buy (FXI) on the dip.

US Trade Deficit hit ten-year high at $59.8 billion for December, and a staggering $419 billion for the year. It’s funny how foreigners stop buying your goods when you declare war on them. Even Teslas (TSLA) are being stopped at the border in China. Who knew?

New trade tariffs hit US consumers the hardest adding $69 billion to their annual bill. Falling real earnings and rising costs is hardly a sustainable model. Will someone please tell the president?

US growth is fading, says the Fed Beige Book, slowing to a “slight to moderate rate”. The government shutdown is the cause. With Europe already in recession, I’ll be using rallies to increase my shorts. Sell (SPY) and (IWM).

The European Central Bank axed its growth forecast sharply, from 1.7% to 1.1%. Stimulus to renew on all front, including more quantitative easing. It’s just a matter of time before their recession pulls the US down. Sell the Euro (FXE).

You lost $3.7 trillion in Q4, or so says the Fed about the decline of national personal net worth during the stock market crash, the sharpest decline in a decade. You’re now only worth $104.3 trillion.

The Mad Hedge Fund Trader actually gained ground last week, thanks to profits on our short positions rising more than our offsetting losses on our longs.

I have doubled up my overall positions, finally taking advantage of the rollover in all risk assets from a historic ten-week run to the upside. I added shorts in the S&P 500 (SPY) and the Russell 2000 (IWM) against a very deep in-the-money long in Freeport McMoRan (FCX) the world’s largest copper producer.

The thinking here is that with China the only economy in the world that is stimulating its economy and the planet’s largest copper consumer, copper makes a nice long side hedge against my short positions.

The Mad Hedge Technology Letter is happily running a short position is Apple (AAPL) which is now almost at its maximum profit point. We only have four days to run to expiration when the position we bought for $4.60 will be worth $5.00.

February came in at a hot +4.16% for the Mad Hedge Fund Trader. March started out negative, down -0.84%, thanks to a wicked stop loss on Gold (GLD). We had 80% of the maximum potential profit at one point but left the money on the table at the highs.

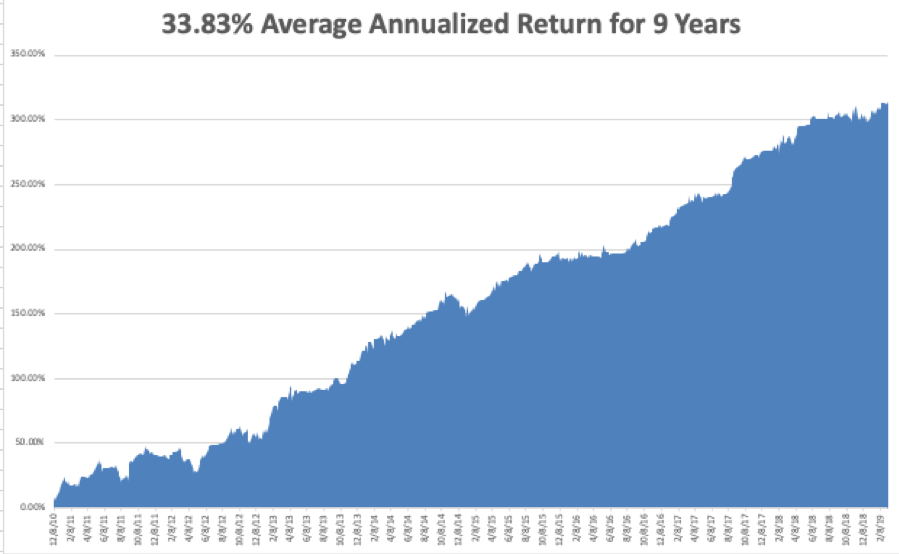

My 2019 year to date return ratcheted up to +12.84%, a new all-time high and boosting my trailing one-year return back up to +29.92%.

My nine-year return clawed its way up to +312.94%, another new high. The average annualized return appreciated to +33.83%.

I am now 50% in cash, 20% long Freeport McMoRan (FCX), and 10% short bonds (TLT), 10% short the S&P 500, and 10% short the Russell 2000.

We have managed to catch every major market trend this year, loading the boat with technology stocks at the beginning of January, selling short bonds, and buying gold (GLD). I am trying to avoid stocks until the China situation resolves itself one way or the other.

As for the Mad Hedge Technology Letter, it is short Apple (AAPL).

Q4 earnings reports are pretty much done, so the coming week will be pretty boring on the data front after last week's fireworks.

On Monday, March 11, at 8:30 AM EST, January Retail Sales is ut.

On Tuesday, March 12, 8:30 AM EST, the February Consumer Price Index is published.

On Wednesday, March 13 at 8:30 AM EST, the February Durable Goods is updated.

On Thursday, March 14 at 8:30 AM EST, we get Weekly Jobless Claims. These are followed by January New Home Sales.

On Friday, March 15 at 9:15 AM EST, February Industrial Production comes out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be headed to the De Young Museum of fine art in San Francisco to catch the twin exhibitions for Monet and Gaugin. When it rains every day of the week, there isn’t much to do but go cultural.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 8, 2019

Fiat Lux

Featured Trade:

(MARCH 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (SDS), (TLT), (TBT), (GE), (IYM),

(MSFT), (IWM), (AAPL), (ITB), (FCX), (FXE)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Are you sticking to your market top (SPY), (SDS) by mid-May?

A: Yes, at the rate that economic data is deteriorating, and earnings are falling, there’s no prospect of more economic stimulation here, my May top in the market is looking better than ever. Europe going into recession will be the gasoline on the fire.

Q: Where do you see interest rates (TLT) in 1-2 years?

A: Interest rates in 2 years could be at zero. If interest rates peaked at 3.25% last year, then the next move could be to zero, or negative numbers. The world is awash in cash, and without any economic growth to support that, you could have massive cuts in interest rates.

Q: Will (TLT) be going higher when a market panic sets in?

A: It will, which is why I’m being cautious on my short positions and why I’m only using tops to sell. You can be wrong in this market but still make money on every put spread, as long as you’re going far enough in the money. That said, when the stock market starts to roll over big time, you want to go long bonds, not short, and we may do that someday.

Q: Do you see a selloff to stocks similar to last December?

A: As long as the Fed does not raise interest rates, I don’t expect to get a selloff of more than 5% or 6% initially. If we do get a dramatic worsening of economic data and it looks like we’re headed in that direction, the Fed will start cutting interest rates, the recession signal will be on and only then will we drop to the December lows—and possibly as low as 18,000 in the Dow.

Q: General Electric has gone from $6 to $10; what would you do now?

A: Short term, sell with a 66% gain in a stock. Long term, you probably want to hold on. However, their problems are massive and will take years to sort out, probably not until the other side of the next recession.

Q: Microsoft (MSFT): long term hold or sell?

A: Absolutely long-term hold; look for another double in this company over the next 3 years. This is the gold standard in technology stocks today. Short term, you’re looking at no more than $15 of downside to the December low.

Q: Would you short banks (IYF) here since interest rates have failed to push them higher?

A: I would not; they’ve been one of the worst performing sectors of the market and they’re all very low, historically. You want to short highs like I’m doing now in the (SPY), the (IWM), and Apple (AAPL), not lows.

Q: Is the China trade deal (FXI) a ‘sell the news’ event?

A: Absolutely; there’s not a hedge fund out there that isn’t waiting to go short on a China trade deal. The weakness this week is them front-running that news.

Q: Do you see emerging markets (EEM) pushing higher from the 42 level, or will a global recession bring it back to earth?

A: First of all, (EEM) will go higher as long as interest rates in the U.S. are flatlining, so I expect a rally to last until the spring; however, when a real recession does become apparent, that sector will roll over along with everything else.

Q: Would you buy homebuilders (ITB) if this lower interest rate environment persists?

A: I wouldn’t. First of all, they’ve already had a big 28% run since the beginning of the year— like everything else—and second, low-interest rates don’t help if you can’t afford the house in the first place.

Q: Would you short corporate bonds if you think there’s going to be a recession next year?

A: I’m glad you asked. Absolutely not, not even on pain of death. I would buy bonds because interest rates going to zero takes bond prices up hugely.

Q: Should you buy stocks in front of a blackout period on corporate buybacks?

A: Absolutely not. Corporate buybacks are the number one buyers of shares this year, possibly exceeding $1 trillion. Companies are not allowed to buy their own stocks anywhere from a couple of weeks to a month ahead of their earnings release. By removing the principal buyer of a share, you want to sell, not buy.

Q: What are the chances the China trade deal (FXI) breaks down this month and no signing takes place?

A: I have a feeling Trump is desperate to sign anything these days, and I think the Chinese know that as well, especially in the wake of the North Korean diplomatic disaster. He has to sign the deal or we’ll go to recession, and that would be tough to run on for reelection.

Q: Which stock or ETF would you short on real estate?

A: If you short the iShares US Home Construction ETF (ITB), you short the basket. Shorting individual stocks is always risky—you really have to know what’s going on there.

Q: What’s the best commodity play out there?

A: Copper. If China is the only country that’s stimulating its economy right now, and China is the largest consumer of copper, then you want to buy copper. The electric car boom feeds into copper because every new vehicle needs 20 pounds of copper for wiring and rotors. Copper is also cheap as it is coming off of a seven-year bear market. What do you buy at market tops? Only cheap stuff.

Q: Why did you go so far in the money in the Freeport-McMoRan (FCX) call spread with only a 10% profit on the trade in five weeks?

A: In this kind of market, I’ll take 10% in 5 weeks all day long. But additionally, when prices are this high, I want to be as conservative as possible. Going deep in the money on that is a very low-risk trade. It’s a bet that copper doesn’t go back to the December lows in five weeks, and that’s a bet I’m willing to make.

Q: Will a new round of QE in Europe affect our stock market?

A: Yes, it’s terrible news. It will weaken the Euro (FXE), strengthen the dollar (UUP), and force US companies to lower earnings guidance even further. That is bad for the market and is a reason why I have been selling short.

Global Market Comments

February 27, 2019

Fiat Lux

Featured Trade:

(WHY CHINA’S US TREASURY DUMP WILL CRUSH THE BOND MARKET),

(TLT), (TBT), ($TNX), (FCX), (FXE), (FXY), (FXA),

(USO), (OXY), (ITB), (LEN), (HD), (GLD), (SLV), (CU),

(THE 13 NEW TRADING RULES FOR 2019)

Years ago, if you asked traders what one event would destroy financial markets, the answer was always the same: China dumping its $1 trillion US treasury bond hoard.

It looks like Armageddon is finally here.

Once again, the Chinese boycotted this week’s US Treasury bond auction.

With a no-show like this, you could be printing a 2.90% yield in a couple of weeks. It also helps a lot that the charts are outing in a major long term double top.

You may read the president’s punitive duties on Chinese solar panels as yet another attempt to crush California’s burgeoning solar installation industry. I took it for what it really was: a signal to double up my short in the US Treasury bond market.

For it looks like the Chinese finally got the memo. Exploding American deficits have become the number one driver of all asset classes, perhaps for the next decade.

Not only are American bonds about to fall dramatically in value, so is the US dollar (UUP) in which they are denominated. This creates a double negative hockey stick effect on their value for any foreign investor.

In fact, you can draw up an all assets class portfolio based on the assumption that the US government is now the new debt hog:

Stocks – buy inflation plays like Freeport McMoRan (FCX) and US Steel (X)

Emerging Markets – Buy asset producers like Chile (ECH)

Bonds – run a double short position in the (TLT)

Foreign Exchange – buy the Euro (FXE), Yen (FXY), and Aussie (FXA)

Commodities – Buy copper (CU) as an inflation hedge

Energy – another inflation beneficiary (USO), (OXY)

Precious Metals – entering a new bull market for gold (GLD) and silver (SLV)

Yes, all of sudden everything has become so simple, as if the fog has suddenly been lifted.

Focus on the US budget deficit which has soared from $450 billion a year ago to over $1 trillion today on its way to $2 trillion later this year, and every investment decision becomes a piece of cake.

This exponential growth of US government borrowing should take the US National Debt from $22 to $30 trillion over the next decade.

I have been dealing with the Chinese government for 45 years and have come to know them well. They never forget anything. They are still trying to get the West to atone for three Opium Wars that started 180 years ago.

Imagine how long it will take them to forget about washing machine duties?

By the way, if I look uncommonly thin in the photo below it’s because there was a famine raging in China during the Cultural Revolution in which 50 million died. You couldn’t find food to buy in the countryside for all the money in the world. This is when you find out that food has no substitutes. The Chinese government never owned up to it.

Global Market Comments

February 20, 2019

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX),

(WHY THE REAL ESTATE BOOM HAS A DECADE TO RUN),

(DHI), (LEN), (PHM), (ITB)

Global Market Comments

February 7, 2019

Fiat Lux

Featured Trade:

(WHAT TO BUY AT MARKET TOPS?),

(CAT), ($COPPER), (FCX), (BHP), (RIO),

(EUROPEAN STYLE HOMELAND SECURITY),

(TESTIMONIAL)