Those planning a European vacation this summer just received a big gift from the people of Italy.

Since April, the Euro (FXE) has fallen by 10%. That $1,000 Florence hotel suite now costs only $900. Mille grazie!

You can blame the political instability on the Home of Caesar, which has not had a functioning government since March. The big fear is that the extreme left would form a coalition government with the extreme right that could lead to its departure from the European Community and the Euro. Think of it as Bernie Sanders joining Donald Trump!

In fact, Italy has had 61 different governments since WWII. It changes administrations like I change luxury cars, about once a year. Welcome to European debt crisis part 27.

I can't remember the last time markets cared about what happened in Europe. It was probably the first Greek debt crisis in 2011. This month, 10-year Italian bond yields have rocketed from 1% to 3%. But they care today, big time.

Given the reaction of the global financial markets, you could have been forgiven for thinking that the world had just ended.

U.S. Treasury Bond yields (TLT) saw their biggest plunge in years, off 15 basis points to 2.75%. The Dow Average ($INDU) collapsed by $500 to $24,250, with interest sensitive banks such J.P. Morgan Chase (JPM) and Bank of America (BAC) delivering the worst performance of the day.

Even oil prices collapsed for an entirely separate set of reasons - so far, the best performing commodity of 2018. The price of Texas Tea pared 10% in a week.

Saudi Arabia looks like it is about to abandon the wildly successful OPEC production quotas that have been boosting oil prices for the past year, and there are concerns that Iran will withdraw from the nuclear non-proliferation treaty. The geopolitical premium is back with a vengeance.

So, if the Italian developments are a canard why are we REALLY going down?

You're not going to like the answer.

It turns out that rising inflation, interest rates, oil and commodity prices, the U.S. dollar, U.S. national debt, budget deficits, and stagnant wage growth are a TERRIBLE backdrop for risk in general and stocks specifically. And this is all happening with the major indexes at the top end of recent ranges.

In other words, it was an accident waiting to happen.

Traders are extremely nervous, global uncertainty is high, the seasonals are awful, and Washington is s ticking time bomb. If you were wondering why I was issuing so few Trade Alerts in May these are the reasons.

This all confirms my expectation that markets will remain in increasingly narrow trading ranges for the next six months until the mid-term congressional elections.

Which is creating opportunities.

If you hated bonds at a 3.12% yield from two weeks ago, you absolutely have to despise them at 2.75% today. That's why I added outright bond put options today to my model trading portfolio.

Stocks are still wildly overvalued for the short term, so I'll keep my short position there. As for oil (USO), gold (GLD), and the currencies, I don't want to touch them here.

So watch for those coming Trade Alerts. I'm not dead yet, just resting.

Waiting for My Shot

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/JT-playing-pool-story-1-image-6-e1527632226975.jpg239300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-30 01:07:092018-05-30 01:07:09Italy's Big Wake-Up Call

Featured Trade: (FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON) (GET READY FOR THE COMING GOLDEN AGE),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call "intergenerational arbitrage" will be the principal impetus. The main reason that we are now enduring two "lost decades" of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million "Gen Xers."

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and "RISK ON" assets such as equities, and more buyers of assisted living facilities, health care, and "RISK OFF" assets such as bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the "millennial" generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 28,000 by 2019.

After that, after a brief dip, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030. If I'm wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

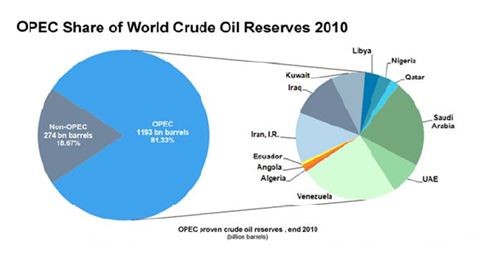

The 100-year supply of natural gas (UNG) we have recently discovered through the new "fracking" technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the United States Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC's share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average U.S. car has jumped from 23 to 24.7 miles per gallon in the past couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states such as California, accounting for 30% of total electric power generation by 2020, and 50% by 2030.

I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the U.S. from a net importer to an exporter of energy, with hugely positive implications for America's balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term.

That sets up a multiyear short for the world's big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it's great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level this is enabling speedy improvements in productivity that are filtering down to every business in the U.S., lowering costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government 10 years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn't afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver's seat on these innovations? The USA.

There is a political element to the new golden age as well. Gridlock in Washington can't last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but for which nobody wants to be blamed.

That means raising the retirement age from 66 to 70 where it belongs and means-testing recipients. Billionaires don't need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them. That's why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don't end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens. The Fed has already told us as much by indicating that the Federal Reserve will only raise interest rates at an infinitesimally slow rate of 25 basis points a quarter.

Sure, this is all very long-term, over-the-horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won't kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

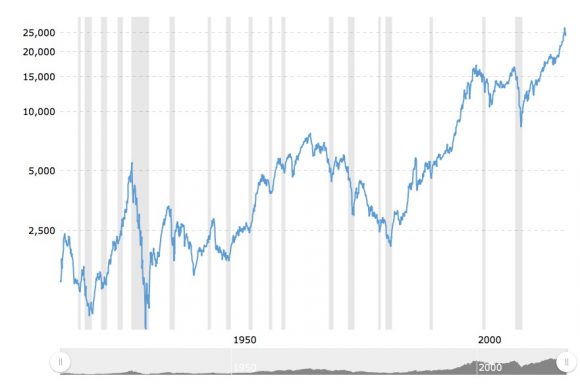

Dow Average 1908-2018

Another American Golden Age is Coming

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/50s-photo-story-2-image-3.jpg237305MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-15 01:06:182018-05-15 01:06:18Get Ready for the Coming Golden Age

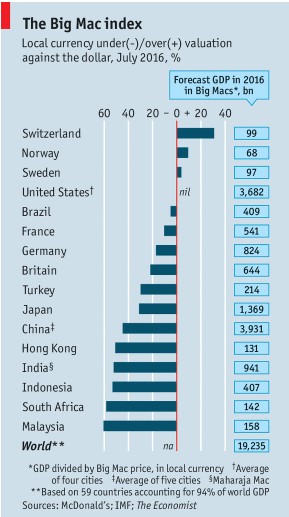

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The World's Most Expensive Big Mac

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Worlds-most-expensive-big-mac-story-2-image-2-e1523918262313.jpg225300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-04-17 01:06:412018-04-17 01:06:41Where The Economist "Big Mac" Index Finds Currency Value

Featured Trade:

(THE FED SIGNALS HALF SPEED AHEAD),

(TLT), (UUP), (FXE), (FXY), (FB),

(WHY YOU WILL LOSE YOUR JOB IN THE NEXT FIVE YEARS, AND WHAT TO DO ABOUT IT)

The Fed just raised interest rates by 25 basis points, taking the cost of overnight money for the big banks to a 1.50%-1.75% range.

The boiling frog analogy comes to mind. Keep raising the temperature so slowly you don't notice it until your portfolio eventually gets cooked.

I believe we have two years of quarter point rises ahead of us like clockwork. This will invert the yield curve in a year, meaning that short term interest rates will exceed the 10-year US Treasury bond, now at 2.87%.

A bear market in stocks ALWAYS follows in six to 12 months. So, make hay while the sun shines, because this bull is rapidly becoming a short-dated option, with only a year or more life left to it.

How could I be wrong? Inflation accelerates, forcing our august central banks to raise rates in one shot by 50 basis points instead of the expected 25.

That would really set the cat among the pigeons, and trigger our next Dow 1,000 point down day.

My long-term economic forecast is still holding water that the benefits of the tax cuts will be entirely offset by rising interest rates and costs, keeping GDP growth at 2.5%...and then to zero.

The unfolding global trade war may also take down global growth and bring forward the next bear market and recession by months, if not a full year. Watch those headlines!

At the end of the day, we will be left with zero economic growth (a recession), higher interest rates, and A LOT more debt, both at the personal and the national level, and naturally exploding deficits everywhere.

That certainly is how the foreign exchange market is reading it, which completely savaged the greenback today. The dollar (UUP) got slaughtered against the Euro (FXE) and the Japanese Yen (FXY). Bonds actually rose on the news, which is why I'm out of that market.

It all works for me, as there will be more trading opportunities playing out in this scenario than pimples at a high school prom.

The biggest imbalance in the current tax policy is allowing multinationals to bring trillions of dollars home by paying minimal tax.

The overwhelming majority of these are big technology companies, meaning that the money is coming back here in the San Francisco Bay Area, causing local asset prices to explode.

I just received a letter from a local real estate broker telling me that the value of my home has risen by 27% in the past year to $5 million, and that now is the best time in history TO SELL!

My former employer, The Economist, once the ever tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its ?Big Mac? index of international currency valuations.

Although initially launched by an imaginative journalist as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald?s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn?t agree more with many of these conclusions. It?s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool, than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/mcdonaldsJapan.jpg240320Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-07 01:08:232016-04-07 01:08:23Where The Economist ?Big Mac? Index Finds Currency Value

Economists around the world have been scanning the horizon with their high powered Zeiss binoculars in search of the cause of the next global recession.

It has been a conundrum of the first order because a recession has NEVER taken place in the face of LOW interest rates and LOW oil prices.

However, we may have just found the trigger.

The possible impending departure of the United Kingdom from the European community has cataclysmic implications for economies everywhere.

We?ll know for sure when the referendum is held on June 23.

Yikes! I?ll be in England then!

The move is being driven by the same factors present in the American Republican Party presidential nomination race.

Working class Brits have lost jobs to a tidal wave of immigrants from the rest of the EC, whose common passports allow unfettered access to Old Blighty.

Take a weekend trip to London, and chances are that the desk clerk is from Poland, the porter is from Croatia, the waitress is from Italy, and the cleaning ladies are from Spain and Greece.

Actual Englishmen are to be found only in distant suburbs, or in unemployment offices.

The recent influx of immigrants from the Middle East has also placed a massive strain on the country?s social services resources.

Visit your local neighborhood National Health GP, and you will share the waiting room with foreign refugees missing arms or legs, or bearing near fatal combat injuries. It?s almost like visiting a wartime MASH unit.

Net net, the view is that EC membership is costing England jobs and money, probably in the billions of pounds per year.

As with the US, the populist view is at odds with the economic reality.

While the UK is a net contributor to the Brussels budget, that misses the point. It is greatly outweighed by the additional economic growth generated by EC membership.

Goods flow freely, duty free between all 23 member countries.

A manufacturer in Birmingham, Leeds, or Manchester doesn?t think twice about jumping on the Channel train to call on customers in Paris, Munich, or Copenhagen.

I often sit next to them during my summer continental travels and also get an update on whatever business they may be in.

A British departure would take nearly 20 years of business integration and dump it into the dustbin of history.

That would be a crushing loss for the British economy, which would lose much of the nearly ?200 billion pounds worth of exports it sent to the EC in 2015. These exports have grown at an impressive 3.6% a year for the past 15 years.

It would also deliver a fatal blow to the City of London, the financial center for all of Europe and one of its largest employers.

I can see the dominoes fall from here.

Europe would lose a similar amount of trade with the UK, taking a chunk out of GDP growth there.

A weak Europe brings a stumbling China, which relies on the continent as its largest customer (yes, even bigger than the US). And a wobbling China will certainly torpedo US exports, increasing volatility in our own financial markets.

In fact, the EC is the world?s largest economic entity. It is hard to see trouble there not spreading everywhere.

The turmoil is already easily visible in the foreign exchange markets. The British pound (FXB) has suffered a gut churning 10.5% nosedive over the past four months to a new ten year low. It has also smothered in the crib the recent rally in the Euro (FXE).

A newly resurgent dollar (UUP) is starting to once again cast a shadow over US multinational earnings.

It seems like the UK is determined to shrink to a smaller country, either by hook or crook.? Only last year, Scotland mounted a campaign to split off from the UK, an effort that eventually failed.

However, it is another one of those cases of being careful what you wish for.

How do you spell ?GLOBAL RECESSION??

Caveat Emptor

I Don't See Anything Yet

https://www.madhedgefundtrader.com/wp-content/uploads/2016/03/Man-with-Binoculars-e1456964153541.png186400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-03-03 01:07:482016-03-03 01:07:48Will ?Brexit? Cause the Next Recession?

I have been to Greece many times over the past 45 years, and I?ll tell you that I just love the place. The beaches are perfect, the Ouzo wine enticing, and I?ll never say ?No? to a good moussaka.

However, I don?t let Greece dictate my investment strategy.

Greece, in fact, accounts for less than 2% of Europe?s GDP. It is not a storm in a teacup that is going on there, but a storm in a thimble. Greece is really just a full employment contract for financial journalists, who like to throw around big words like bankruptcy, default and contagion.

I have other things to worry about.

In fact, I am starting to come around to the belief that Europe is looking pretty good right here. Cisco (CSCO) CEO, John Chambers, announced that he was seeing the early signs of a turnaround.

Fiat CEO, Sergio Marchionne, the brilliant personal savior of Chrysler during the crash, thinks the beleaguered continent is about to recover from ?hell? to only ?purgatory.?

Only a devout Catholic could come up with such a characterization. But I love Sergio nevertheless because he generously helps me with my Italian pronunciation when we speak (aspirapolvere for vacuum cleaner, really?).

What are the two best performing stock markets since the big ?RISK ON? move started last Thursday? Greece (GREK) (+5%) and Russia (RSX) (+7.5%)!

And here is where I come in with my own 30,000 foot view.

The undisputed lesson of the past five years is that you always want to own stock markets that are about to receive an overdose of quantitative easing.

Since the US Federal Reserve launched their aggressive monetary policy, the S&P 500 (SPY) nearly tripled off the bottom.? Look how well US markets have performed since American QE ended 18 months ago.

Europe has only just barely started QE, and it could run for five more years. Corporations across the pond are about to be force-fed mountains of cash at negative interest rates, much like a goose being fattened for a fine dish of foie gras (only decriminalized in California last year).

Mind you, it could be another year before we get another dose of Euro QE, which is why I just bought the Euro (FXE) for a short-term trade.

A cheaper currency automatically reduces the prices of continental exports, making them more competitive in the international markets, and boosting their economies. Needless to say, this is all great new for stock markets.

Get Europe off the mat, and you can also add 10% to US share prices as well, as the global economy revives. The Euro drag dies and goes to heaven.

Buy the Wisdom Tree International Hedged Equity Fund ETF (HEDJ) down here on dips, which is long a basket of European stocks and short the Euro (FXE). This could be the big performer this year.

Praise the Lord and pass the foie gras!

It?s all a Matter of Perspective in Greece

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Foie-Gras-e1423777772497.jpg303400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-17 01:07:062016-02-17 01:07:06The Case for Europe

Those of a certain age can?t help but remember that things for the US went to hell in a hand basket after 1963.

That?s when President John F. Kennedy was assassinated, heralding decades of turmoil. Race riots exploded everywhere. The Vietnam War ramped up out of control, taking 60,000 lives, and destroying the nation?s finances. Nixon took the US off the gold standard.

When people complain about our challenges now, I laugh to my self and think this is nothing compared to that unfortunate decade.

Two oil shocks and hyper inflation followed. We reached a low point when Revolutionary Guards seized American hostages in Tehran in 1979.

We received a respite after 1982 with the rollback of a century?s worth of regulation during the Reagan years. But a borrowing binge sent the national debt soaring, from $1 trillion to $18 trillion. An 18-year bull market in stocks ensued. The United States share of global GDP continued to fade.

Basking in the decisive victories of WWII, the Greatest Generation saw their country account for 50% of global GDP, the largest in history, except, perhaps, for the Roman Empire. After that, our share of global business activity began a long steady decline. Today, we are hovering around 22%.

Hitch hiking around Europe in 1968 and 1969 with a backpack and a dog-eared copy of Europe on $5 a Day, I traded in a dollar for five French francs, four Deutschmarks, three Swiss francs, and 0.40 British pounds.

When I first landed in Japan in 1974, there were Y305 yen to the dollar. Even after a strong year, the greenback is still down by 75% against these currencies, except for sterling. How things have changed.

We now live in a world where the US suddenly has the strongest economy, currency and stock market in the world. Are these leading indicators of better things to come?

Is the Great American Rot finally ending? Is everything that has gone wrong with the United States over the past half century reversing?

The national finances are hinting as much. Over the last four years, the federal budget deficit has been shrinking at the fastest rate in history, from $1.4 trillion to only $483 million.

If the economy continues to grow at its present modest 2.5% rate, we should be in balance by 2018. Then the national debt, which will peak at around $18 trillion, will start to shrink for the first time in 20 years.

And since chronic deflation has crashed borrowing costs precipitously, the cost of maintaining this debt has dramatically declined.

A country with high economic growth, no inflation, generationally low energy costs, a strong currency, overwhelming technology superiority, a strong military and political stability is always a fantastic investment opportunity.

It certainly is compared to the highly deflationary, weak currency, technologically lagging major economies abroad.

You spend a lifetime looking for these as a researcher, and only come up with a handful. Perhaps this is what financial markets have been trying to tell us all along.

It certainly is what foreign investors have been telling us for years, who have been moving capital into the US as fast as they can (click here for ?The New Offshore Center: America?).

It gets even better. These ideal conditions are only the lead up to my roaring twenties scenario (click here for ?Get Ready for the Coming Golden Age?), when over saving, under consuming baby boomers enter a mass extinction, and a gale force demographic headwind veers to a tailwind.

That opens the way for the country to return to a consistent 4% GDP growth, with modest inflation and higher interest rates.

Which leads us all to the great screaming question of the moment: Why is the US stock market trading so poorly this year? If the long term prospects for companies are so great, why have shares suddenly started performing feebly?

Not only has it gone nowhere for three months, market volatility has doubled, making life for all of us dull, mean and brutish.

There are a few short-term answers to this conundrum.

There is no doubt that the Euro and the yen have fallen so sharply against the greenback that it is hurting the earnings of multinationals when translated back to dollars.

This has cut S&P 500 earnings forecasts for the year. And these days, everyone is a multinational, including the Diary of a Mad Hedge Fund Trader, where one third of our subscribers live abroad.

Another short-term factor is the complete collapse of the price of oil. Again, it happened so fast, and was so unexpected, that it too is having a sudden deleterious influence of broader S&P earnings.

Go no further than oil giant Chevron, which just announced a big drop in earnings and a massive cut in its capital spending budget for 2016.

The final nail in the Q4 coffin has been bank earnings, which all took big hits in trading revenues. Virtually all were taken short by the huge, one-way rally in bond prices in recent months and the collapse of interest rates.

This happens when panicky customers come in and lift the banks? inventories, and trading desks have to spend the rest of the day, week and month trying to get them back at a loss.

I have seen this happen too many times. This is why the industry always trades at such low multiples.

With no leadership from the biggest sectors of the market, financials and energy, and with the horsemen of technology and biotech vastly overbought, it doesn?t leave the nimble stock picker with too many choices.

The end result is a stock market that goes nowhere, but with a lot of volatility. Sound familiar?

Fortunately, there is a happy ending to this story. Eventually, all of the short-term factors will disappear. Oil prices and bond yields will go back up. The dollar will moderate. Corporate earnings growth will return to the 10% neighborhood. And stocks will reach new highs.

But it could take a while to digest all of this. This is a lot of red meat to take in all at one time. If the market grinds sideways in a 15% range all year, and then breaks out to the upside once again for a 5% annual gain, most investors would consider this a win.

Once again, index investors will beat the pants off of hedge fund managers, as they have for the past seven years.

In the meantime, I doubt the stock indexes will drop more than 6% % from here, with the (SPY) at $189, and we have already seen a 6% hair cut from last year?s peak.?

Knock a tenth off a 16.5 X forward earnings multiple with zero inflation, cheap energy, ultra low interest rates and hyper accelerating technology, and all of a sudden, stocks look pretty cheap again.

As the super sleuth, Sherlock Homes used to say, ?When you have eliminated the impossible, whatever remains, however improbable, must be the truth?.

It?s All Elementary

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Holmes-Watson.jpg308394Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-08 01:06:502016-02-08 01:06:50The Great American Rot is Ending

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.