Foreign exchange traders are an odd lot. They tend to maintain a laser like focus on specific numbers that are utterly meaningless to us mere mortals, but which have momentous importance to themselves.

Right now, one is hearing the battle cry over the 120/120 targets. Specifically, traders want to take the yen down to Y120 to the US dollar, and the Euro down to $1.20 by the last trading day of 2014.

They may well get their wishes.

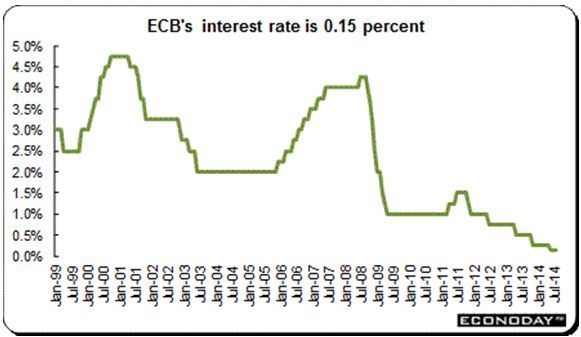

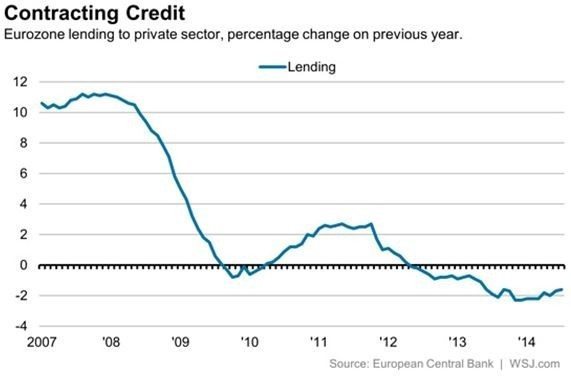

Powering the moves is the biggest policy divergence between central banks in a decade. The US Federal is threatening to take interest rates up every other day.

In the meantime, lower interest rates beckon in Europe and Japan as their economies lurch from one disaster to the next, dragging their own currencies down.

Accelerating the move is the gasoline that has been thrown on the economic fires caused by? You guessed it, plunging gasoline prices in the US, which is quickly turning into a massive stimulus program.

Wonder why Wal-Mart (WMT) has suddenly taken off to the races? It?s because their impoverished, gap toothed customers have suddenly received big cash bonuses, thanks to the war for market share among the members of OPEC.

Even a penny drop in the price of petrol adds $1 billion a year in consumer spending. Gas is so cheap that we might even break the $3 level here in high tax California.

Higher interest rates are great for the greenback because they prompt foreign investors to send more money here faster to chase higher returns than available at home.

The sharpest bond market move in history, taking ten year Treasury yields from 1.86% all the way up to 2.38% in four weeks, makes this view even more convincing.

Followers of this letter already know that the currencies have been in deep doo doo all year. That?s why I have been aggressively pushing out Trade Alerts to buy the dollar (UUP) and sell short the Euro (FXE), (EUO) and the Japanese yen (FXY), (YCS) for the past six months.

Readers have been laughing all the way to the bank.

The really thrilling part here is that this is only the beginning of a decade long move. My final target for the yen is Y150 and $1.00 for the Euro. This could be the trade that keeps on giving.

There are also important spillover implications for the stock market. It means more money for stocks at higher prices. The S&P 500 at 2,100 by yearend now looks like a chip shot, and we may probe even higher.

So why am I currently lacking any current positions in the currencies in my model trading portfolio? We are now at the end of extreme moves in all asset classes over the past month.

So, while everything looks hunky dory (a street in Yokohama where the cheap geishas used to hang out) in the markets, risk is, in fact, rising.

I have to admit that, being up 42.5% year to date, I have gotten spoiled. I am holding back for the low risk, high return type of entry points for new trades that my readers have become addicted to.

When I see one, you?ll be the first to know. Watch this space.

Gosh, I love this job.

See the Connection?

The Best Stimulus Program Ever

The Best Stimulus Program Ever