For a lifetime central bank watcher, like myself, this was one for the record books.

Reserve Bank of Australia, Glenn Stevens, said last week that he welcomed a weak Australia dollar and that it probably had further to fall. To put gasoline on the flames, he added that there was room for the RBA to further lower interest rates, assuring that more weakness in the Aussie was assured.

The Australian dollar didn?t have to be told twice what to do. All bids for the troubled currency immediately vaporized, and it gapped down two full cents to the 90-cent level, a three-year low. When the Aussie broke a crucial support level at parity in the spring, I predicted that 80 cents was in the cards.

That forecast, bemoaned and lambasted at the time, is now looking increasingly likely. This is why I have been warning my Australian friends all year to pay for their summer vacations in advance while their currency was still dear.

What is far more important here is what the RBA moves means for the global economy. It certainly raises the stakes in the international race to the bottom, where every country tries to devalue their way to prosperity. During the Great Depression, this was known at the ?beggar thy neighbor? policy, a term I?m sure you have all heard a lot about. A cheaper currency means your exports now cost less, so customers shift business from your neighbors to you, boosting your economy.

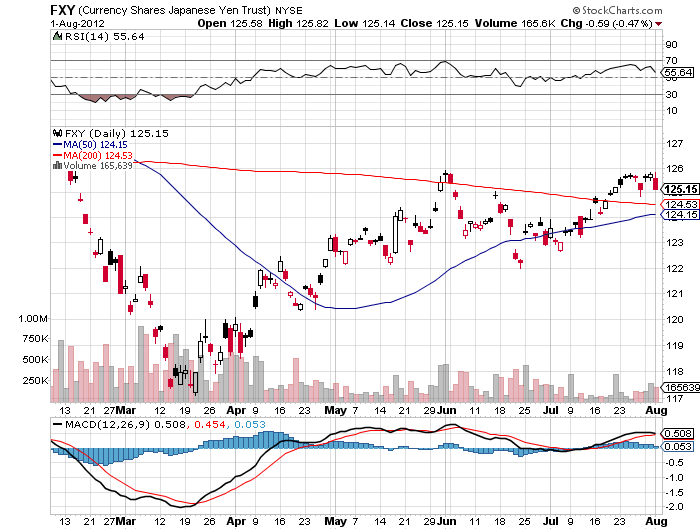

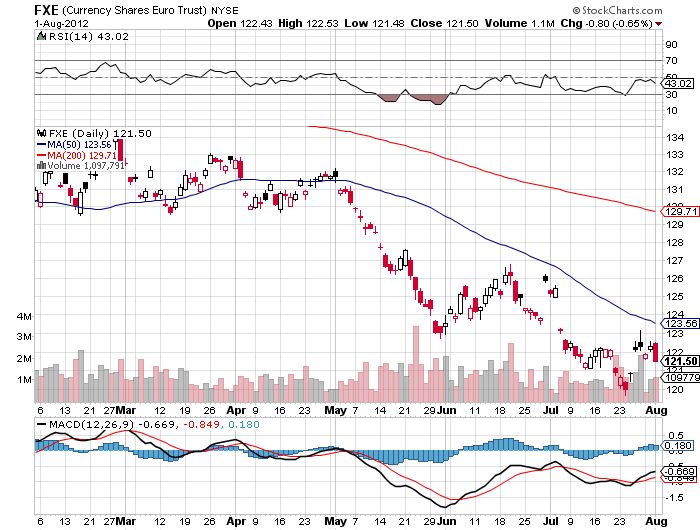

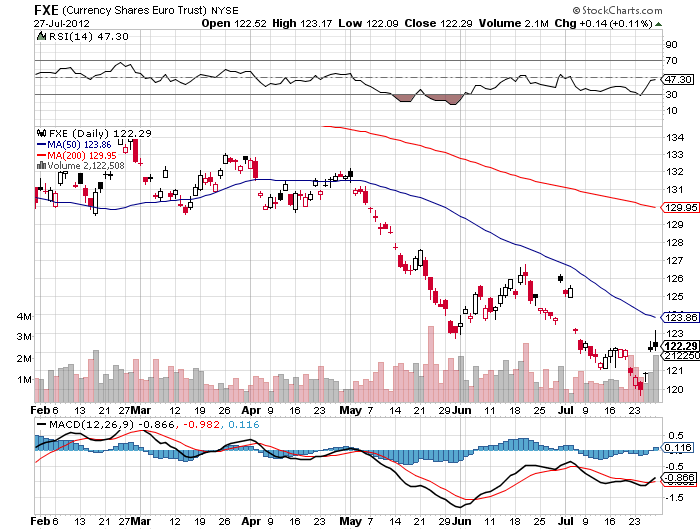

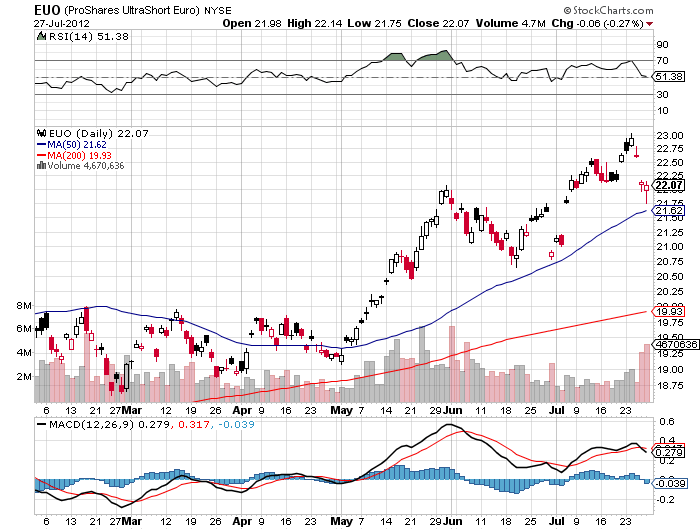

In recent years, the US was winning that game. Then Japan took over the lead in November, with a yen (FXY), (YCS) that has fallen 25% since. Now, Australia has grabbed first place, with a 15% plunge since March. Who is the big loser in all this? Europe, where even the guy who runs the beach mini mart in Mykonos tells me his economy sucks because his currency (FXE) is grotesquely overvalued.

The sad thing is, I don?t think a weaker Aussie will help the Land Down Under very much, if at all. Their problem is not a price one for their commodities, but a demand one. Everything Australia sells is a commodity where prices are set by a global marketplace.

The slowing of China?s economy is the big driver here, as orders for Australia?s exports of iron ore, copper, and coal fall precipitously. Grains (DBA) sales are hurt by America?s bumper crop, which is killing prices. Fukushima demolished uranium exports (NLR). Australian offshore natural gas (UNG), at $16/btu, doesn?t stack up very well against US fracking gas at $3.50. Gold (GLD) is not exactly flying off the shelf either, with prices at one point this year down 33% from the highs.

There is another big factor, which no one but myself seems to me noticing. The slowdown in Chinese commodity demand is not a temporary affair, it is a permanent one. The government there is making every effort to shift the economy away from commodity consuming, metal bashing exports, to a more services oriented one.

This more suitably matches the Middle Kingdom?s own resource base, of which there are few, towards a higher rung in its own development. You will probably start to hear about this from other strategists, gurus, and research houses in about a year. It is momentous in its implications.

The RBA?s move caught many traders off guard, as they had already begun scaling into long Australian dollar positions, looking for an autumn rally. Mad Day Trader, Jim Parker, knew better, and was advising Aussie shorts up to the 94 cent level.

As for me, I?ll be selling every decent Aussie rally for the foreseeable future, until global commodity prices finally bottom, or Australia changes central bank governors, whichever happens first. I bet a lot of Australians right now prefer the latter over the former.

The Thunder Down Under is Fading

https://www.madhedgefundtrader.com/wp-content/uploads/2013/08/Thunder-Down-Under.jpg406579Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-09 01:04:122013-08-09 01:04:12Ambush in Australia

I sit here on the Carrera marble paved terrace of the Emperor?s Suite of the Imperial Hotel, in Santa Margherita Ligure on the Italian Riviera. As the sun sets into a languid Mediterranean, a distant church bell tolls, calling the evening mass. A flock of larks perform a spectacular aerobatic display overhead. A never-ending torrent of Vespa?s speed past on the road below, driven by texting cigarette smoking young women, like a swarm of angry wasps.

A plaque on the wall tells me that the peace treaty that ended WWI between Germany and Russia was negotiated in my bedroom in 1922. At night, I count no less than 22 goddesses, nymphs, and cherubs gazing down on me from the fresco above. It seems that the hotel was once a summer palace for some long forgotten European nobility. Offshore, the mega yachts of Russian oligarchs bob at anchor, drifting with the tide, our visiting nouveau nobility.

All of which leads me to ponder the question of the day: ?Why is all of this so damn expensive?

Dinner down at the market corner trattoria is costing me $100, and it rises to $200 or $300 for the nicer places. A five-minute taxi ride set me back $20. Even a lowly, genetically engineered Big Mac here costs $5.

It?s not like our continental cousins are rolling in cash these days. Now that Japan is on the mend, thanks to Abenomics, Europe has the world?s worst economy. The unemployment rate is 26% in Spain, and 40% for those under 25. Rolling layoffs are hitting the French auto industry, long the last bastion of the protected job. Italy is in its third painful year of recession. Greece is only just getting off its back after a European Central Bank enforced austerity. Chinks are even starting to appear in the armor of the German economy.

The weak economy has fueled non-stop political crises in Spain, Portugal, and Greece. Italy is not even sure it has a government. The debt crisis is never ending. Even European Central Bank president, Mario Draghi, seems to be taking a page out of Ben Bernanke?s playbook. He has recently said that interest rates will remain ?at or below current levels for an extended period.? With all of this angst, you would think that the Euro was the greatest short on the planet.

Except that it isn?t.

So we have to search for he reasons why. The great mystery among economists, politicians, bankers, and hedge fund managers here this summer is why the Euro is so strong, given these desperate fundamentals.

I am now two weeks into making the rounds with the European establishment, and to a man, they are short the beleaguered continental currency in their personal accounts. There are really only two opinions here. One is that the Euro is headed to parity against the dollar, down 24% from here. The other is that it will revisit the old 2002 low of 86 cents, down 32%.

The reality is that while the Fed?s balance sheet continues to expand at a breakneck pace, the ECB?s is shrinking. This is because European banks are repaying the subsidized loans they received at the height of the crisis to shore up their balance sheets. It is a distinctly positive development for the Euro.

Relentless austerity measures have the unanticipated side effect of increasing the continent?s current account surplus. Imports are drying up, further boosting the Euro, much to the grief of China. While the economic news here is bad, it is better than it was a year ago. This is what the year on year precipitous drop in sovereign bond yields is telling you. So there is a huge amount of bad news already in the Euro price.

Global currency positioning may also have something to do with it. This year, the big play was in selling short the yen, Australian and Canadian dollars, and emerging market currencies against the greenback. The Euro is simply benefiting from inertia, or getting ignored.

In the meantime, some big hedge funds have been throwing in the towel on the Euro and shifting capital to greener pastures elsewhere. With all of Europe seemingly competing for my beach chair, who is left to sell the Euro?

In the end, the strength of the Euro may end up becoming one of those ephemeral summer romances. There is no doubt that the American economy is improving, and further distancing itself from Europe.

This will turbocharge that great decider of foreign exchange rates?interest rate differentials. That?s when rising US rates and flat or falling European ones can send the buck in only one direction over the medium term, and that is northward.

Then my European friends should become as rich as Croesus, and the price of that Big Mac will come more into line with the one I buy at home.

The Dalliance With the Euro Will Be Strictly a Summertime Affair

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/John-Thomas-Portofino.jpg373497Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-05 01:04:342013-08-05 01:04:34The Mystery of the Strong Euro

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950?s, and which I still remember fondly. This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call ?intergenerational arbitrage? will be the principal impetus. The main reason that we are now enduring two ?lost decades? is that 80 million baby boomers are retiring to be followed by only 65 million ?Gen Xer?s?. When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and ?RISK ON? assets like equities, and more buyers of assisted living facilities, health care, and ?RISK OFF? assets like bonds. The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward ten years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home. That is when you have 65 million Gen Xer?s being chased by 85 million of the ?millennial? generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes. The middle class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990?s.

The stock market rockets in this scenario. Share prices may rise gradually for the rest of the teens as long as growth stagnates. A 5% annual gain takes the Dow to 20,000 by 2020. After that, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 80,000 by 2030. Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well. The 100-year supply of natural gas (UNG) we have recently discovered through the new ?fracking? technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies. That?s why oil is now $70 a barrel in North Dakota versus $95 in Oklahoma 1,000 miles to the South.

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC?s share of global reserves is collapsing. This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.? Mileage for the average US car has jumped from 23 to 24.7 miles per gallon in the last couple of years. Total gasoline consumption is now at a five year low.

Alternative energy technologies will also contribute in an important way in states like California, accounting for 30% of total electric power generation. I now have an all electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy, with hugely positive implications for America?s balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term. That sets up a multiyear short for the world?s big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it?s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos. But at the enterprise level this is enabling speedy improvements in productivity that is filtering down to every business in the US.

This is why corporate earnings have been outperforming the economy as a whole by a large margin. Profit margins are at an all time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development. When the winners emerge they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area. This is because the Golden State thumbed its nose at the federal government ten years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn?t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 40 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday. What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver?s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can?t last forever. Eventually, one side or another will prevail with a clear majority. This will allow them to push through needed long-term structural reforms, the solution of which everyone agrees on now, but nobody wants to be blamed for. That means raising the retirement age from 66 to 70 where it belongs, and means-testing recipients. Billionaires don?t need the $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up. A Pax Americana would ensue. That means China will have to defend its own oil supply, instead of relying on us to do it for them. That?s why they?re in the market for a second used aircraft carrier.

Medicare also needs to be reformed. How is it that the world?s most efficient economy has the least efficient health care system? This is going to be a decade long workout and I can?t guess how it will end. Raise the growth rate and trim back the government?s participation in the credit markets, and you make the numerous miracles above more likely.

The national debt comes under control, and we don?t end up like Greece. The long awaited Treasury bond (TLT) crash never happens. Ben Bernanke has already told us as much by indicating that the Federal Reserve may never unwind its massive $3.5 trillion in bond holdings.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won?t kick in for another decade. But some individual industries and companies will start to discount this rosy scenario now. Perhaps this is what the nonstop rally in stocks since November has been trying to tell us.

Dow Average 1970-2012

Is Another American Golden Age Coming?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/57-T-Bird.jpg237305Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-04-01 01:02:502013-04-01 01:02:50Get Ready for the Next Golden Age

You couldn?t mistake the meaning of the cries of topless female protesters as they flung themselves at police guarding Italian polling stations on Monday. Basta! Basta! Enough! Enough! The purpose of their demonstration was visibly scrawled in large letters across their nubile bodies in black ink for all to see. Mille grazieProfesoressaFrancesca for being my Rosetta Stone!

Global equity investors could well be screaming enough, enough as well. Right when it became clear that the Italian election was not going according to script, the major indexes rolled over from substantial gains to even more impressive losses. The Volatility Index (VIX) blasted 35% to the upside, the biggest move since November, 2011, the last time the Land of Julius Caesar threatened a meltdown. The Italian Index ETF (EWI) really got decimated, posting an intraday fall of 18%, while the Euro (FXE), (EUO) took a two and a half cent dive against the greenback.

Up until today, the smart money was betting on a win by socialist Pier Luigi Bersani and some continuation of the recent reformist policies. What we got was a much stronger than expected showing by Silvio Berlusconi, who is using his billions of Euros to get elected to avoid going to prison. His platform is to undo all of the reforms of recent years, and basically send Europe back to the crisis days of 2010, when the European currency traded as low as the $1.17 handle. Note to self: the smart money isn?t always right.

Of course, I have been warning anyone who would listen that something like this was headed our way (click here for ?Is the Party Over? ). I was even so precise in my predictions that I said the trigger might come from the next leg of the European financial crisis.

To see the exact levels where major support kicks in on the charts for this selloff, please follow the link above. For the Legions who follow my market beating Trade Alert Service, take solace in the fact that our entire portfolio expires in just 13 trading days, and these levels only need to hold until then. After that, we want everything to go to zero, where we can buy them cheap.

Unhappy Italian Voter

Long Time No See

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Black-Swan.jpg444587Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-02-26 09:59:322013-02-26 09:59:32Suddenly Those Italian Lessons Are Paying Off

Even the Old Hands, like myself, are somewhat amazed by the strength of the global equity markets this month. The S&P 500 has risen 11 out of the last 12 trading days, and is up almost every day this month. It has been the best January in 18 years.

The first week saw the biggest inflows to equity mutual funds in 10 years. Yet, the market went up so fast, most of the largest investors were left at the starting gate, with the bulk of their new money yet to go into the market. If you weren?t as fast on the trigger as I was, you were left to read about it in the Wall Street Journal, and on your way to the Tombstone career cemetery. Hint to market strategists: that money is still out there trying to get in.

It appears that the race to the bottom for currencies is the race to the top for equities. The reality is that in such a competition, everyone wins. Since the mid November low, the (SPX) has risen by 12%. But Germany (EWG), which has had to carry the dead weight of an appreciating Euro, is up 29%. Japan, where the yen has plunged 16%, has seen the currency hedged equity ETF (DWJ) soar by 31%. My own Trade Alert Service tacked on 21%. For investors, this is a ?heads I win, tails you lose? market.

Certainly, the data flow has been there in abundance to justify such ebullience. Everywhere I look, I see improving PMI?s, increasing orders, rising real estate prices. Some 70% of American companies have, so far, beat earnings expectations.

In the US, business is running on all 12 cylinders (or all 80 kw of lithium ion battery power in my world), with the housing, energy, and auto industries all kicking in at once. Yesterday, weekly jobless claims hit a five year low at 335,000, and this morning the HKSB private Chinese PMI rose to a healthy 51.9.

The new Japanese stimulus efforts are so Godzilla like in proportions that the country?s GDP growth could flip from -3.5% to +3% in a mere two quarters. Do I hear the words ?global synchronized expansion?, anyone? Yikes. It makes the (SPX) at 1,500, and the (IWM) at $89 look positively cheap. Even the Federal Reserve?s own dividend discount valuation model says that the (SPX) should be worth 1,750 here.

Hedge funds are getting creamed, as usual, because their shorts are rising much faster than their longs. Look no further than Netflix (NFLX), which had a jaw dropping open short interest of 45%, but soared by a staggering 71% in two days after their earnings announcement. The pain trade is on. That?s why I have been going commando, without any shorts at all, save in the Japanese yen. Thank goodness I?m not in that business anymore. It is sooo last year?s game.

It is, in fact, a one stock market. But this time, there is only a single stock going down, Apple (AAPL), while everything else rises. A close friend whose market timing I respect told me on Tuesday, when the stock traded at $514, that it would hit a final bottom at $438 in three months. Three days later, and here we are at $437.

When the company announced an increase in cash on the balance sheet of $23 billion, the market took $100 billion off its market capitalization, depriving it of its vaunted ?largest company in the world? status. Go figure. This is truly a classic falling knife scenario, which is better observed from afar.

If you had asked me in September, when Apple was trading at $700, where would the (SPX) be if it fell to $437, I would have answered 1,000. Yet, here we are at 1,500. Here?s an intriguing thought, what if my friend is at least partly right, and Apple goes up from here? My own target of the (SPX) at 1,600 becomes a chip shot, possibly by March. Hey, if Ben Bernanke wants me to pile into risk assets, who am I to argue? I?ve always been a team player. I think I?ll buy more stocks (SPY), (IWM), sell more yen (FXY), (YCS), and drive the Tesla around the mountain one more time. Maybe I can get the clock up to 500 miles.

In this Market, You are Either Very Fast, or Very Dead.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Clint-Eastwood.jpg215309Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-01-27 23:02:192013-01-27 23:02:19The Race to the Bottom for Currencies Means a Race to the Top for Stocks

As I expected, the wildly optimistic expectations for further quantitative easing by the Federal Reserve at yesterday?s Open Market Committee meeting were not matched with substance. All we got was a continuation of existing modest programs and some minor tweaking of language.

Bernanke only managed to say that, ?further stimulus will be provided as needed.? The Fed left unchanged its statement that economic conditions would likely warrant holding the benchmark Fed funds rate near zero ?at least through late 2014.? It also said it would continue swapping $667 billion of short-term debt with longer-term securities to lengthen the average maturity of its holdings, an action intended to lower long-term interest rates known as Operation Twist.

Apparently, the slowdown in GDP growth from 2% in Q1 to 1.5% in Q2 was not enough to spur the Fed to action. Nor was a slowdown in jobs growth from an average 226,000 jobs per month to 75,000. The earliest the Fed can now take further accommodative action is at their next meeting on September 12-13, just seven weeks before the presidential election.

The dollar rose smartly against the yen and the Euro. Equities closed at their lows for the day. They could have fallen dramatically further. But I think that traders are holding fire until their learn the results of the ECB meeting on Thursday. If we get more rhetoric instead of action, and the Friday nonfarm payroll continues weak, then we will have a hat trick of disappointments that could trigger a more gut wrench plunge in the indexes going into next week.

At the very least, we should challenge the bottom the of recent upward channel, taking us down 50 points from here. That should double the value of my existing position in the (SPY) puts.

Ben, Where Were You?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-08-02 13:15:502012-08-02 13:15:50The Fed Says No QE3

A couple of alleged Tweets, a few rumored phone calls, and what have we got? $2 trillion in new global stock market capitalization in hours. That was the bottom line after the purported communication between the staffs of Germany?s Angela Merkel, France?s Jean Francois Hollande, and ECB president Mario Draghi. But is the creation of this immense new wealth, which would alone rank as 10th in terms of GDP after France, justified?

If the intention was to punish hedge funds, the goal was certainly accomplished. The plaintive bleatings in email and text messages I received from hedge fund friends back home has been overwhelming. It was clear from the price action, straight line moves with no pullbacks, that the pain trade was definitely on. Pre-Thursday, the consensus wisdom was that market would crash into the August doldrums in the face of global economic data that was deteriorating by the day. Such is the price of betting against central banks that I highlighted in my recent trope ?Why Ben Bernanke Hates Me? (click here at http://madhedgefundradio.com).

Leading research houses seemed to be in an arms race with government institutions to see who could cut growth forecasts the fastest. They were all egged on by US Q2 corporate earnings reports, that were highly fudged and indifferent at best, with the most honest wisdom provided by the shocker from Apple (AAPL).

However, in the financial markets that are more often driven by emotion than information, politics trump fundamentals every day. With the street heavily positioned on the short side, the conditions for a snap back rally were ripe. This is why I had no positions at all for 10 days, and no equity holdings for over a month. Rather than chase the market on the downside, I waited for it to come to me, which is usually the best thing to do.

I have always believed that Europe has the ability and the resources to solve its problems at any time. To read my advice to the German government in detail, please refer to my report from Frankfurt, which I will write in the next couple of days, when I get some time.

All that is required is for Europe to make some unpleasant admissions of truths, and adopt some policies and institutions that have already been proven to work in the US. These are hard things to do politically, but that can be done. Make the politicians earn their pay for a change, I say. This is what makes the short game in Europe so risky, and why I have recently been so wimpy on my short Euro (FXE), (EUO) recommendations (in the reports, but without trade alerts).

Words are cheap, and their true value will become apparent when it comes time for Mario Draghi to deliver. If he does so quickly, we could see a ?RISK ON?, rally that could last until the end of the year and possibly take the S&P 500 up to 1,500. If he doesn?t, the August crash scenario down to 1,200 is back on the table, but no more. That table loses another leg if Ben Bernanke fails to deliver QE3 on Wednesday.

If all of this leaves you confused and befuddled, then welcome to the club. There are times when markets are just not forecastable, when the number of large variables and unknowns are too great to even make an intelligent guess at outcomes, and this is one of them. That?s why I am still 70% in cash, limiting my ?RISK ON? exposure to small, profitable positions in short Treasury and short yen call spreads. That?s down from 100% I had just last Wednesday.

I think I?ll go climb that Alp over there.

The Pain Trade is on for Hedge Funds

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-07-30 22:46:492012-07-30 22:46:49Mr. Mario?s Big Bluff

It?s always nice when intelligent people agree with you. That was my feeling after the Federal Reserve gave notice today that it was downgrading its forecast of US economic growth for 2012 from 2.6% to 2.15%. That is a major step down from the 3% and higher predictions they were hanging on to earlier.

The news came in the written statement that followed the Fed?s somewhat disappointing decision today. As I expected, there will no QE3. The Fed needs to keep dry powder in case we get another market crash, possibly as early as this summer. Operation ?twist? was renewed for another year, but wasn?t extended to include mortgage backed securities. It was about as conservative of a conclusion one could have expected from the Fed, given the rapidly deteriorating economic data flow that I chronicle daily in these pages.

It brings the August panel of respected central bankers in line with my own 2% expectation, which I have been posting since January. Here?s a good rule of thumb from a four decade long Fed watcher: they are always behind the curve, sometimes way behind, often by a year or more.

The problem for you is that 2% is not my forecast anymore. As of today, I am ratcheting it down to 1.5%. Without a QE3 it is really hard to see where additional growth is going to come from this year. US corporations are producing record profits and sitting on mountains of cash, so they have absolutely no incentive to stick their necks out whatsoever. Additional government spending is hamstrung by an election year and a gridlocked congress.

Virtually the entire international arena is slowing, in some cases dramatically so. China is about to bust through the bottom of its target growth range at 7%, down from 13% a few years ago. Tsunami reconstruction spending in Japan has just about run its course. Europe is clearly in a major recession. Even powerhouse, Germany, is shrinking from 2% growth to 1% because of weakness in its major export markets.

The market implications of this lower growth rate are many. It means that the recent 100 point rally in the S&P 500 was built on so much hot air and false hope. It was never driven by more than a round of furious short covering and profit taking. Let the permabulls enjoy a few more days of summer, possibly taking the index as high as 1,400 by month end.

It also means that another round of pain for the Euro (FXE) (EUO) is not far off. The best case for Treasury bonds (TLT) is that they churn sideways until the next Fed meeting in six weeks. In the worst case, the spike up to challenge the old highs, taking yields up to 1.42% for the ten year once more.

The lows for the year haven?t been put in yet, but they are about to. Before, we had a 4% GDP stock market and a 2% GDP economy. Now we have a 4% GDP stock market and a 1.5% GDP real economy. Watch out below. The only question is whether 1,250 in the (SPX) holds this time, or whether we have to plumb the depths of 1,200 before the penance is paid for our hubris.

Sorry Guys, No QE3 Today

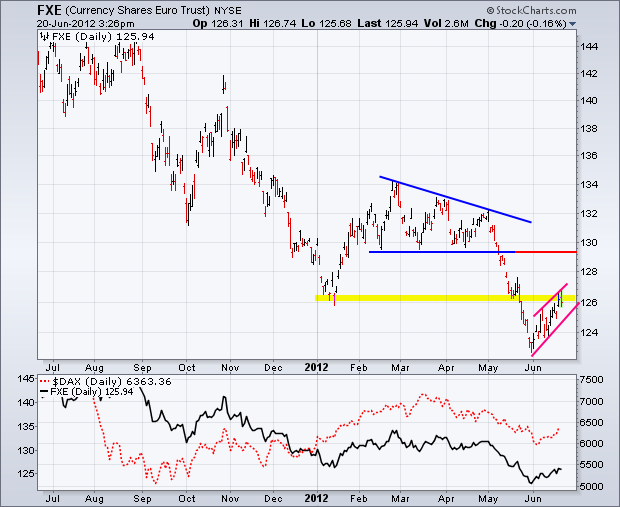

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-06-20 23:02:452012-06-20 23:02:45No Fed Action Disappoints QE Bulls

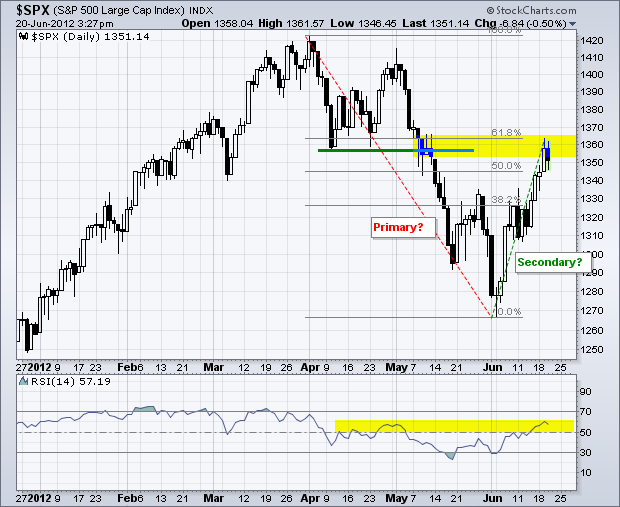

The abject failure of the equity indexes to breach even the first line of upside resistance does not bode well for the ?RISK ON? trade at all. Only a week ago I predicted that the markets would be challenged to top 1,340 in the (SPX) and $78 for the Russell 2000 (IWM). In fact, we made it up only to 1,335 and $77.90 respectively.

To see the melt down resume ahead of the month end window dressing is particularly concerning. That?s the one day a month that investors really try to pretend that everything is alright. People just can?t wait to sell.

Blame Europe again, which saw Spanish bond yields reach a 6.6% yield on the ten year and the Italian bond market roll over like the ?Roma? (a WWII battleship sunk by the Germans while trying to surrender to the Allies). Facebook didn?t help, knocking another $8 billion off its market capitalization, further souring sentiment.

Urging traders to head for the exits was confirming weakness across the entire asset class universe. The Euro is in free fall. Copper took a dive. Oil is plumbing new 2012 lows. Treasury bond prices rocketed, taking ten year yields to new all-time lows at 1.65%. It all adds up to a big giant ?SELL!?

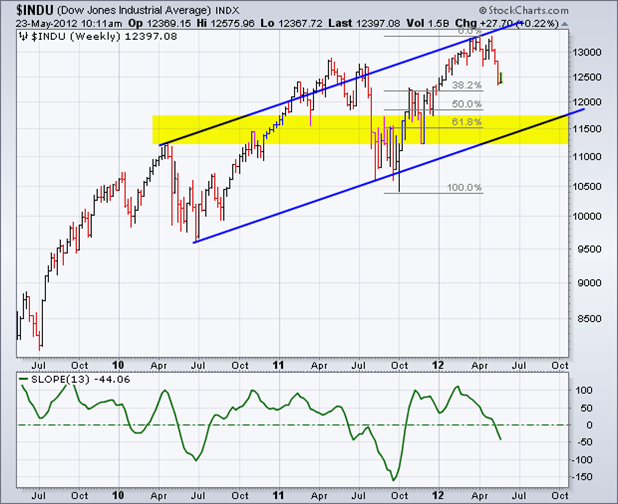

It is just a matter of days before we revisit the (SPX) 200 day moving average at 1,280. Thereafter, the big Fibonacci level at 1,250 kicks in. It is also exactly one half the move off of the October 2011 low, and unchanged on the year for 2012.

I am not looking for a major crash here a la 2011. There is just not enough leverage and hot long positions in the system to take us down to 1,060. It will be a case of thrice burned, four times warned. And remember, last year?s 1,060 is this year?s 1,100, thanks to the earnings growth we have seen since then. With 56% of all S&P 500 stocks now yielding more than the ten year Treasury bond, you don?t want to be as aggressive on the short side as in past years, when bond yields were 4 or higher.

By adding on a short in the (SPY) here, I am also hedging my ?RISK ON? exposure in the deep in-the-money call spreads in (AAPL), (HPQ), and (JPM), and my (FXY) puts. The delta on these out-of-the-money?s are so low that I can hedge the lot with one small 5% position in the at-the-money (SPY) puts.

If the (SPX) hits 1,280, the (SPY) puts will add 2.25% to our year to date performance. At 1,250 we pick up 4.00% and at 1,200 we earn 7.00%. I now have the option to come out at any of these points if the opportunity presents itself, depending on how the rapidly changing global macro situation unfolds. If we get another pop from here back up to the 1,340-1,360 range, I will double up the position and swing for the fences. There?s no way we are taking a run at new highs for the year from here.

Below, find today?s charts from my friends at www.StockCharts.com with appropriate support and resistance levels outlined. If I may make another observation, when you see the technicals work as well as they have done recently, it is only because the real long term end investors have fled. There are not enough cash flows in the market to overwhelm even the nearest pivot points. That leaves hedge fund, day, and high frequency traders to key off of the obvious turning points in the market. That also is not good for the rest of us.

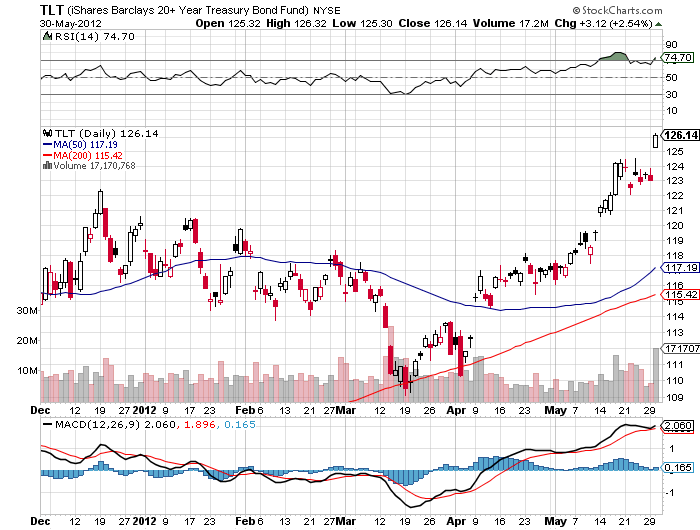

It?s a good thing that I?m not greedy. If I had sold short a near money call spread for the (TLT) on May 23, I would be in a world of hurt right now. Instead, I went six point out of the money. So when we get dramatic moves like we saw today that take bond yields to all-time lows, I can just sit back and say, ?Isn?t that interesting.? This spread expired in six trading days, which should be enough time to digest the big move today and expire safely out of the money and worthless. What?s better, I can then renew the trade at better strikes after expiration into the July?s and take in more money.

If you are wondering why I am not doubling up on the short Treasury bond ETF (TBT) down here, it?s because it doesn?t have enough leverage. In these conditions you need to go for instruments that can generate immediate and large profits, such as through the options market. The topping process for the Treasury market could go on for another month or two. Until that ends, I am happy to use price spikes like today?s to sell short limited risk (TLT) call spreads 6-8 points out of the money, which can handle a 20 basis point drop in yields and still make you money.

If you own the (TBT) and are willing to take a multi month view, you should be doubling up here. This ETF will have its day in the sun, it is just not today. We could see the $20 handle again and maybe even $30 within the next year. That makes it a potential ten bagger off of today?s close.

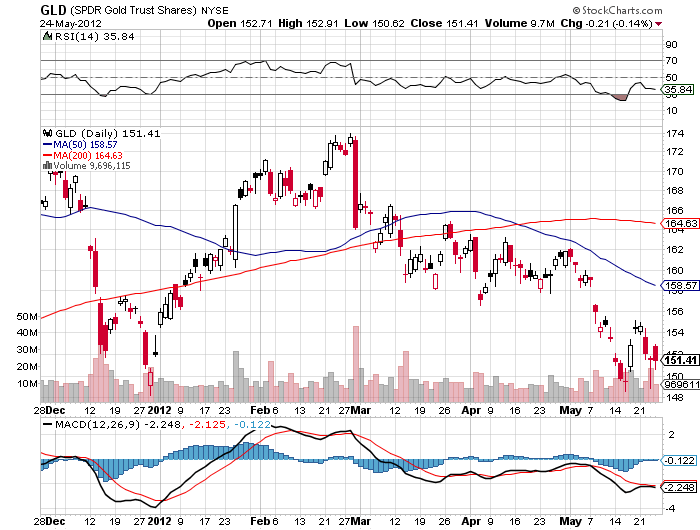

I don?t want to touch gold (GLD) or silver here. The barbarous relic is clearly trying to base at $1,500 an ounce. If it fails, it will probably only go down to only $1,450 before major Asian central bank buying kicks in. Better to admire it from afar, or limit your activity to early Christmas shopping for your significant other. We are months away from the next major rally in the yellow metal.

The Roma

Time to Puke Out Again

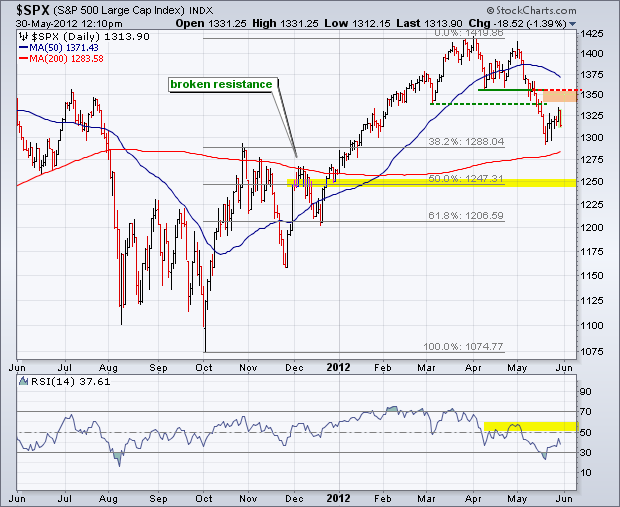

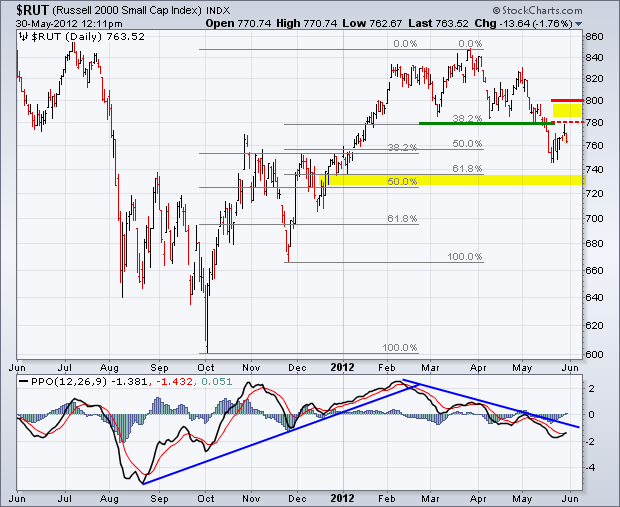

https://www.madhedgefundtrader.com/wp-content/uploads/2012/05/300px-Italian_battleship_Roma_1940_starboard_bow_view.jpg164300DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-05-30 23:02:052012-05-30 23:02:05My Tactical View of the Market

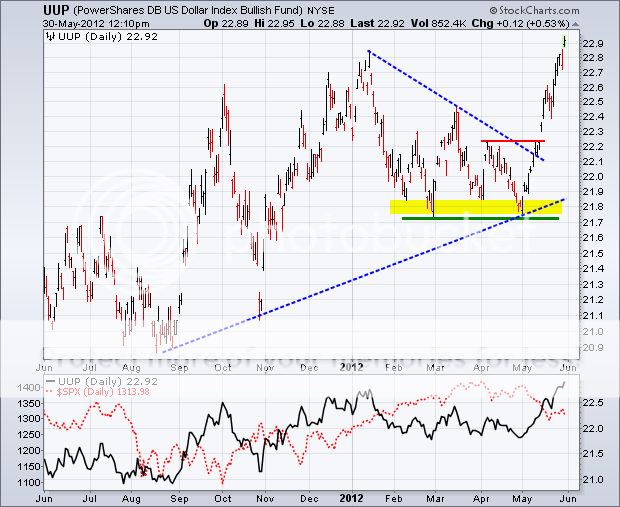

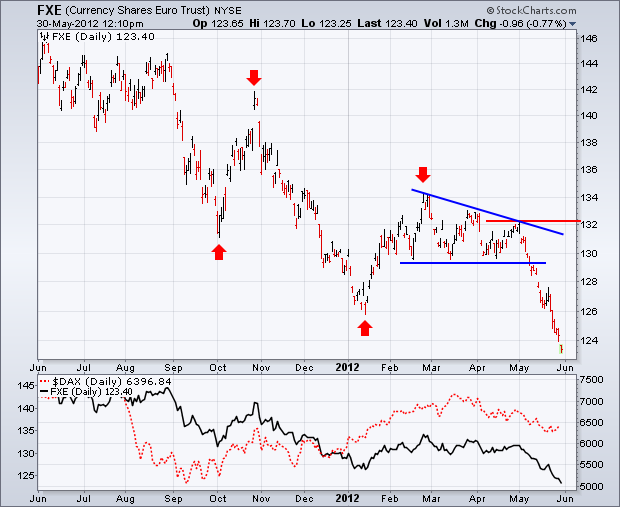

The easy money has been made on the short side this year for a whole range of asset classes. While we will probably see lower lows from here, the risk/reward ratio for taking short positions in (SPX), (IWM), (FXE), (FXY), (GLD), (SLV), (USO), and (CU) are less favorable than they were two months ago.

Of course, the ultimate arbiter will be the news play and the economic data releases. It they continue to worsen as they have done, you can expect a brief rally in the (SPX) up to the 1,340-1,360 range before the downtrend resumes. First, we will revisit the old low for the move at 1,290. Then 1,250 cries out for attention, which would leave us dead unchanged on the year. Lining up next in the sites is 1,200. But to get that low, probably by August, we would need to see something dramatic out of Europe, which we may well get. For the Russell 2000, look to sell it at the old support range of $78-80, which now becomes overhead resistance, to target $72 on the downside.

Don?t underestimate the devastating impact the Facebook (FB) debacle will have on the overall market. Retail investors lost $6 billion on the deal after institutional investors were given the heads up on the impending disaster and stayed away in droves. The media has plenty of blood on its hands on this one. The day before the pricing, one noted Cable TV network reported that the deal was oversubscribed in Asia by 30:1. Morgan Stanley reached for the extra dollars, increasing the size, and boosting the price by 15%. It all came to tears.

Expect investigations, subpoenas, congressional hearings, prosecutions, multi million out of court settlements, thousands of lawsuits, and many careers ended ?to spend more time with families.? Horrible thought of the day: Apply Apple?s (AAPL) 8X multiple, which is growing at 100% a year, to Facebook, which is not, and you get a (FB) share price of $5. None of this exactly inspires confidence in the stock market.

Notice that emerging markets have really been sucking hind teat this year, dragged down by falling commodity prices, a slowing China, and a general ?RISK OFF? mood. This is probably the first sector you want to go back in at the summer bottom to take advantages of their higher upside betas.

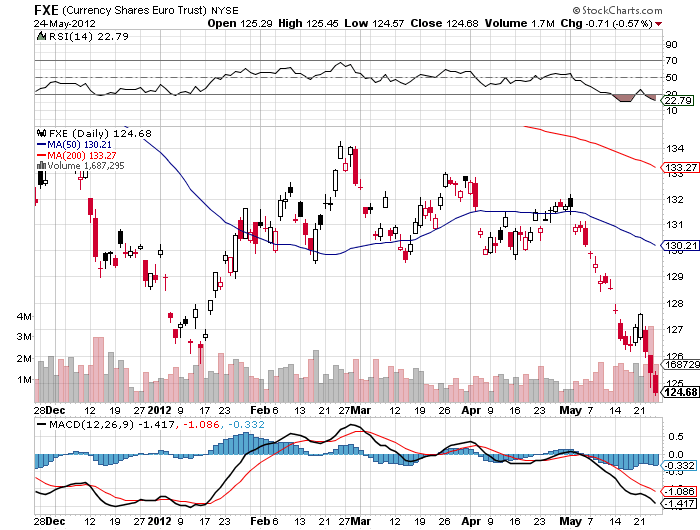

The Euro went through the old 2012 low at $1.260 like a hot knife through butter. On the breach, a lot of momentum programs automatically kicked in and doubled up their short positions. That is what has taken us all the way down to the high $124 handle in the cash. Let?s see how the market digests this breakdown. The commitment of traders report out on Friday should be exciting, as we already have all-time highs in short positions in the beleaguered European currency.

The problem is that any good news whispers or accidental tweets on the sovereign debt crisis could trigger ferocious short covering and gap openings which the continental traders will get a head start on. So again, this is not the low risk trade that it was months ago.

Still, the 2010 lows at $1.18 are now on the menu. I would sell all the ?good news? rallies from here two cents higher. Aggressive traders might consider selling penny rallies, like the one we got today. Notice that the Euro is rallying into the US close every day. This is caused by American traders covering shorts, not wishing to run them into any overnight surprises.

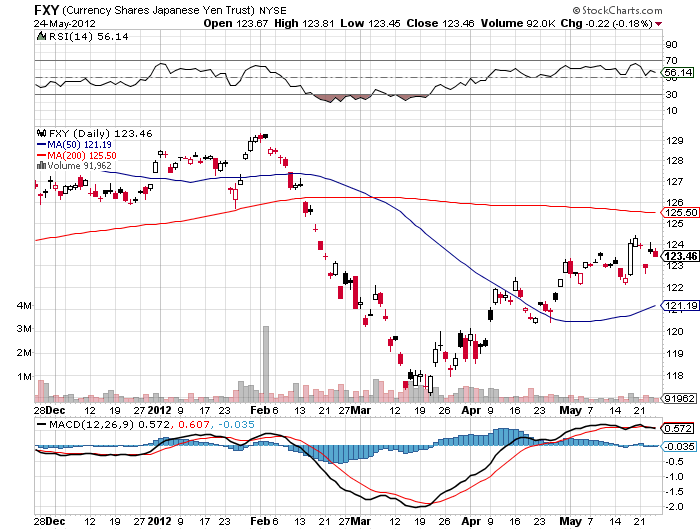

The Japanese yen seems to be stagnating here once again, now that the Bank of Japan has passed on another opportunity to exercise more much needed quantitative easing. Therefore, I will use the next dip to get out of my September put options at a small loss. There is a better use of capital and bigger fish to fry these days.

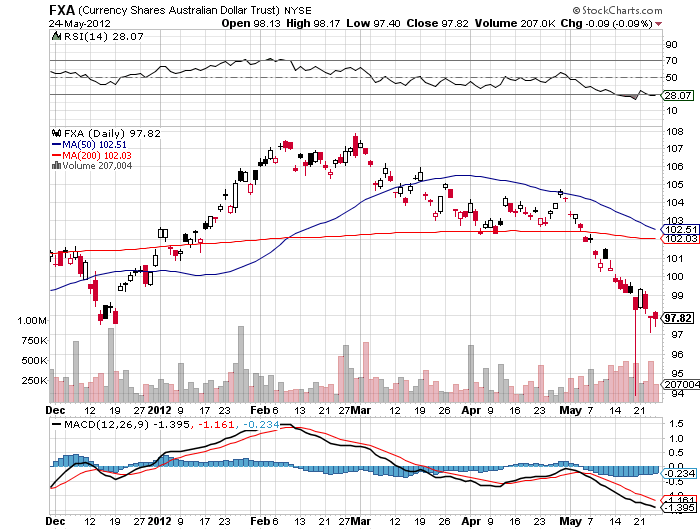

The Australian dollar has been far and away the world?s worst major currency this year, falling from $110 all the way down to $94 on a spike. It now languishes at $97. I long ago stopped singing ?Waltzing Matilda? in the shower. I hope all my Ausie friends took my advice at the beginning of the year and paid for their European and American vacations while their currency was still dear. We could see as low as $90 in the months to come.

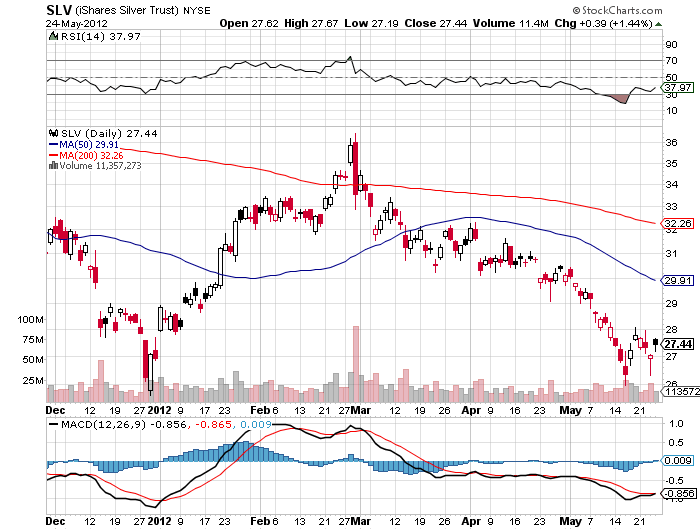

Gold (GLD) and silver (SLV) still look week, as this week?s failed rally attests. The strength of the Indian rupee still has the barbarous relic high priced for the world?s largest buyer, and this will continue to weigh on dollar based owners. But we are also reaching the tag ends of this move down from $1,922. Speculative short positions are at a multi-year low. It would take something pretty dramatic to get me to sell short gold again. For the time being, I am targeting gold at $1,500 on the downside, $1,450 in an extreme case, and $25 in silver.

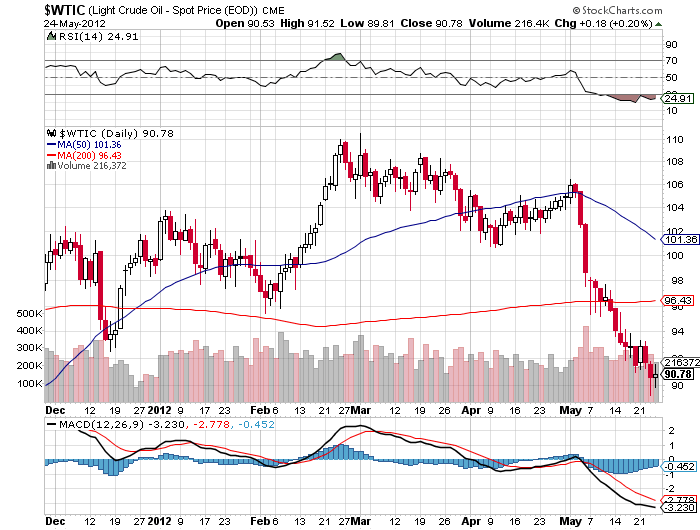

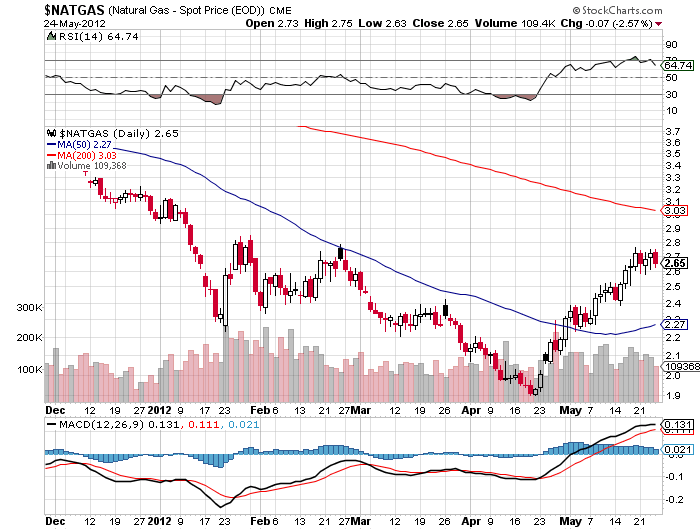

We are well into the move south for oil, which peaked just at the March 1 Iranian elections just short of $110/barrel. The market now seems to be targeting $87 for the short term. The global economic slowdown is the clear culprit here. But in the US, we are starting to see a clear drag on oil prices caused by the insanely low price of natural gas. You can see this clearly on the charts below where gas has been rising while Texas tea has been plunging. Utilities and industry are switching over to the cleaner burning ultra cheap fuel source as fast as they can. As a result, greenhouse gas emissions are falling faster in the US than any other developed country, according to the Paris based International Energy Agency. Sell any $4 rally in crude and keep a tight stop.

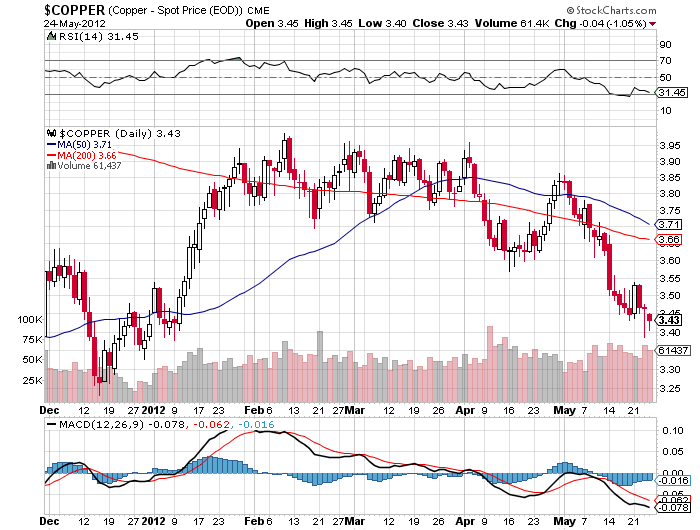

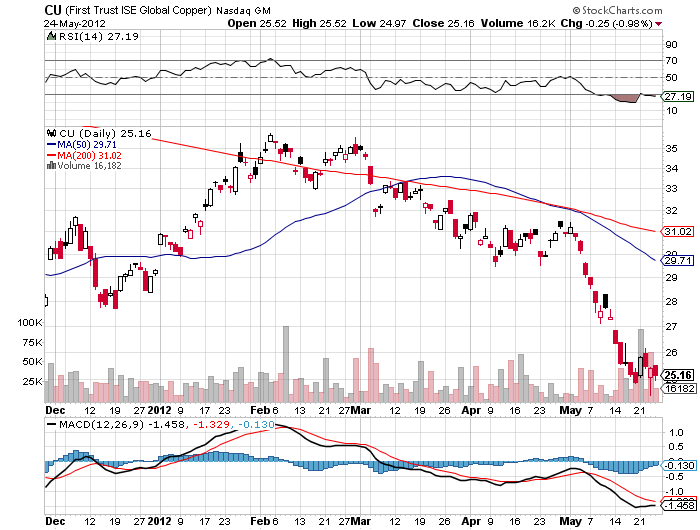

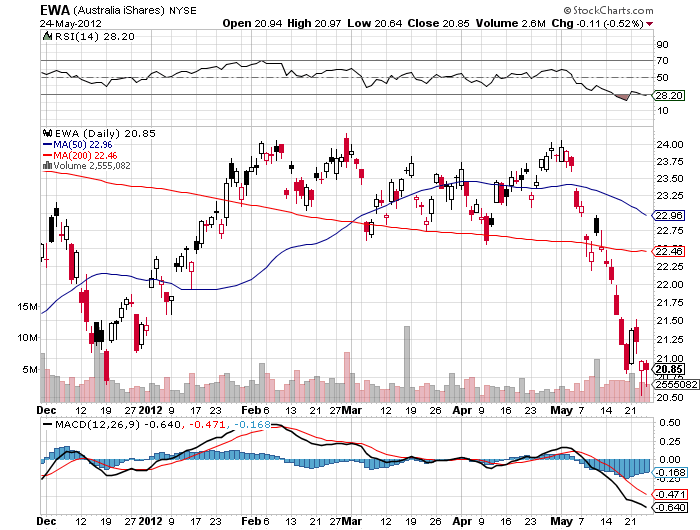

When China catches cold, copper gets pneumonia. So does Australia (FXA), (EWA), for that matter. The China slowdown will most likely continue on into the summer, knocking the wind out of the red metal. If copper manages to rally back up to $3.60, grab it with both hands and throw it out the window. Cover when you hear a loud splat. That works out to about $26.50 in the ETF (CU).

It all points to a highly choppy and volatile ?RISK ON? rally that could last a week or two. It will be a time when you wish you took your mother in law?s advice to get a real job by becoming a cardiologist or plastic surgeon. Do you want to know when I want to reestablish my shorts? If you get a modestly positive nonfarm payroll on at 8:30 am on Friday, June 1, that could deliver a nice two day rally that would be ideal to sell into.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-05-24 23:03:212012-05-24 23:03:21My Tactical View of the Market

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.