Global Market Comments

February 13, 2024

Fiat Lux

Featured Trade:

(WHAT THE ECONOMIST BIG MAC INDEX IS TELLING US NOW),

(FXF), (FXE), (FXA), (CYB)

Global Market Comments

February 13, 2024

Fiat Lux

Featured Trade:

(WHAT THE ECONOMIST BIG MAC INDEX IS TELLING US NOW),

(FXF), (FXE), (FXA), (CYB)

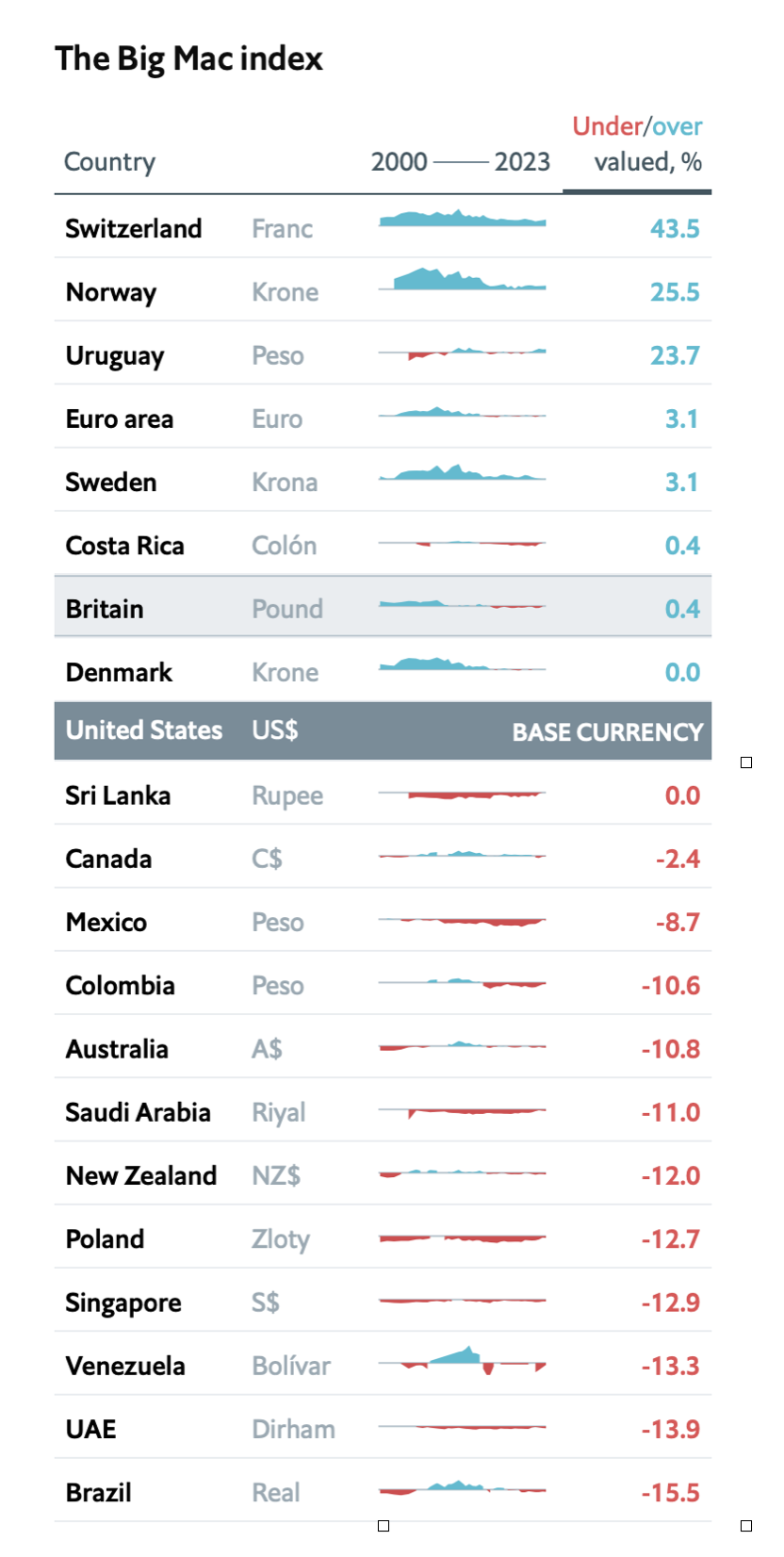

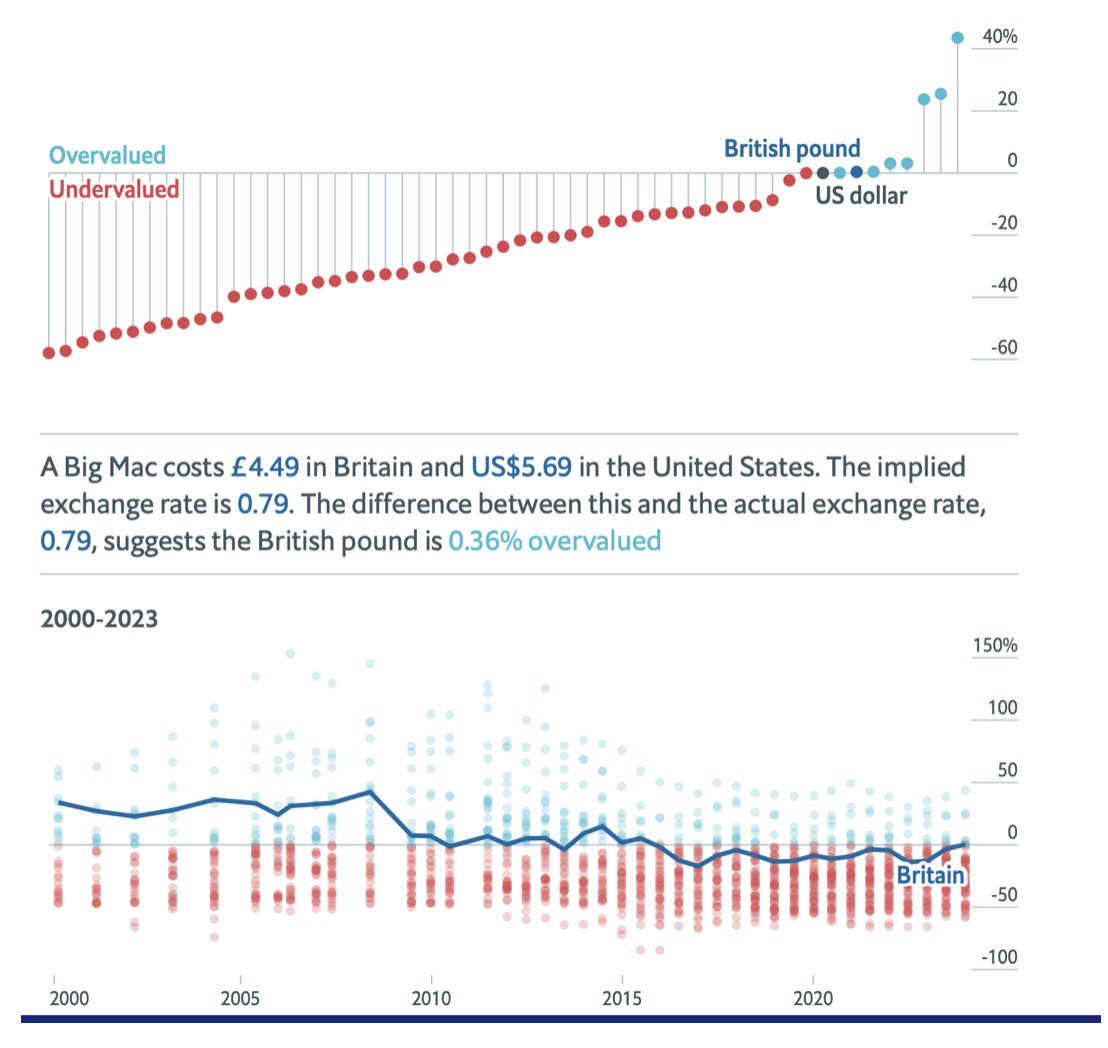

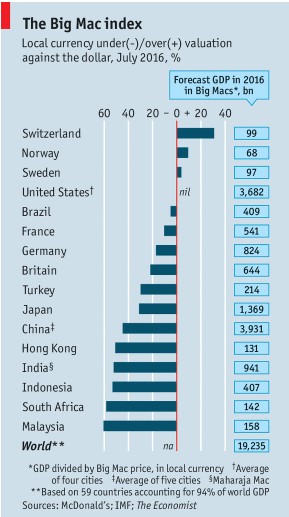

The Swiss franc is wildly overvalued, as are the Norwegian kroner and the Uruguayan peso. On the other hand, the Venezuelan bolivar, UAE dirham, and the Brazilian real off real value.

Who has the cheapest currency in the world? The Ukrainian hryvnia, which at 25 cents to the US dollar offers the cheapest Big Mac in the world. I had one in October, and they taste just the same, but is a bargain at $5.00. That explains the proliferation of McDonald's hamburger stands in the capital city of Kiev. They are always packed.

With interest rates and inflation the urgent topics of the day, everyone has their favorite inflation indicator. The Fed has money supply growth, you have yours, and well, I have mine.

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), released its “Big Mac” index of international currency valuations in 1987.

Although initially launched as a joke, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The heart attack on a plate costs $5.69 in most of the US.

The Economist index counts the cost of McDonald’s (MCD) premium sandwiches around the world, ranging from 142% the cost of an American Big Mac in Switzerland to only 84.5% in Brazil, and comes up with a measure of currency under and overvaluation.

I couldn’t agree more with many of these conclusions. It’s as if the August weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it directly to my middle. Better to use it as an economic forecasting tool, than a speedy lunch.

Having followed this index religiously for 37 years, I am able to make some astute long-term observations. For a start, the US dollar has been at the top of the range for most of its life. This is because the US has had the best major economic growth rate over the last four decades, averaging a real 3.0%.

Another factor is that America has also had the world’s highest large economy interest rates, thanks to a very tough inflation-fighting Federal Reserve. I doubt Jay Powell eats Big Macs. He’s too thin.

You will also find that the cheap end of the range is always populated by the same countries year in and year out. These are poorly governed, money-printing, economically chaotic countries with little regard for their currencies. Don’t cry for me Argentina and throw in Venezuela. They will always be cheap. Invest there at your peril.

And yes, making your currency calls based on the price of hamburgers has its risks. But it does give me a wonderful excuse to travel around the world taking pictures of fast-food stands.

The Big Mac in Swiss francs is Definitely Not a Buy

But it’s the Deal of the Century in Kiev

Global Market Comments

November 31, 2023

Fiat Lux

Featured Trade:

(WHERE THE ECONOMIST BIG MAC INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (FXA), (FXE), (CYB)

(THE FALLING MARKET FOR KIDS)

With interest rates and inflation topic number one of the day, everyone has their favorite inflation indicator. The Fed has its, you have yours, and well, I have mine.

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its “Big Mac” index of international currency valuations.

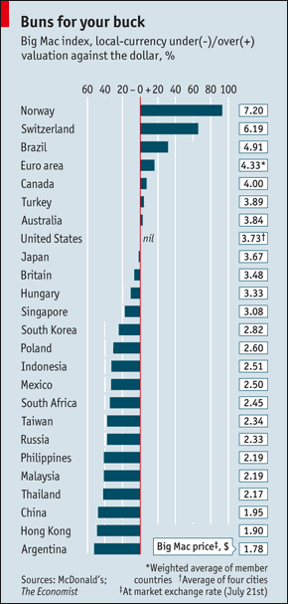

Although initially launched as a joke four decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The index counts the cost of McDonald’s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn’t agree more with many of these conclusions. It’s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my hip. Better to use it as an economic forecasting tool, than a speedy lunch.

Global Market Comments

July 5, 2019

Fiat Lux

Featured Trade:

(FRIDAY JULY 19 ZERMATT SWITZERLAND STRATEGY SEMINAR)

(WHERE THE ECONOMIST “BIG MAC” INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (FXA), (FXY), (CYB),

(WHY US BONDS LOVE CHINESE TARIFFS),

(TLT), (TBT), (SOYB), (BA), (GM)

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of a Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

Global Market Comments

July 17, 2018

Fiat Lux

(WHERE THE ECONOMIST "BIG MAC" INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (FXA), (FXY), (CYB),

(CATCHING UP WITH DOWNTON ABBEY),

(TESTIMONIAL)

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The World's Most Expensive Big Mac

My former employer, The Economist, once the ever tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its ?Big Mac? index of international currency valuations.

Although initially launched by an imaginative journalist as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald?s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn?t agree more with many of these conclusions. It?s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool, than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

The Big Mac in Yen is Definitely Not a Buy

I?ve just spent the entire morning on the phone, and it?s clear that thousands of individuals, hedge funds and brokers have just been wiped out as a result of The Swiss National Bank?s surprise move to remove its cap against the Euro.

This is a black swan on steroids.

And it hasn?t just been Swiss franc positions that have been bedeviling traders. You can add to the list bonds, energy, and this week, financial stocks as well. All of a sudden, the world seems to have gone mad.

The great flaw in the management of big brokers and hedge funds is that they base their risk models on historic data. It is rare to see a foreign currency move more than 1% against the US dollar in a day. You might see that one-day a year.

Risk models, and margin requirements, are therefore based on this assumption. To bomb proof themselves, margin departments might require clients to post collateral assuming that a 2% or even a 3% move in a currency will happen tomorrow.

Even with an ultra conservative 3% margin requirement, a house would only be protected by a move in the underlying of 33%. Any move greater than that, the customer account is completely wiped out, leaving the broker on the hook for the balance of the loss if they can?t get clients to pony up more money.

Of course, US based brokers can always sue their former clients and get their money back that way. But that is a three-year process. Just ask anyone who went through the whole MF Global disaster.

As a former broker myself, I can tell you that clients wiped out by margin calls have a bad habit of disappearing, changing their names and moving to unpronounceable countries to bury the paper trail, or move beyond the reach of extradition treaties. So good luck with that one.

After speaking to several foreign exchange traders, it seems that the first tick after the SNB?s announcement was up a staggering 40% from the last print. The world had stop loss orders to sell Euros as market, and this was the fill they got.

It gets worse. Some brokers, particularly small, undercapitalized foreign ones, were only demanding 0.5% margin or less. These guys are toast, but it may take weeks to find out exactly who.

The news services this morning are ablaze with such losses. Citibank (C) has admitted to a $150 million hickey. Very conservative Interactive Brokers has fessed up to a $120 million hit. FXCM is thought to be out $225 million. All of a sudden, foreign exchange brokers everywhere are for sale at fire sale prices.

These aren?t just some interesting, entertaining and colorful market anecdotes that I?m providing you. The debacle is so severe that it has cast a black cloud over all asset classes.

You see this in the sharply diminished trading volumes in all instruments, from stocks, to options, to futures contracts and exchange traded funds.

If you have just heard of a colleague or a counterparty who has just gone under, trading any of the recent straight line one way moves, guess what? You don?t go out and bet the ranch.

Your risk appetite has been diminished for weeks, if not months. In fact, you may not want to trade at all. This is not good for markets of any description.

I have been through many of these. The best thing to do is to shrink your book, hedge up what?s left, and put your more aggressive tendencies on hold. You may have noticed that the model portfolio for my Trade Alert service has just done exactly that.

Come back only when it?s safe to play, and the markets gets easy again.

Watch Out, They Can Bite

Watch Out, They Can Bite