Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-8.png422564Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-30 13:02:442021-07-30 14:11:16July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the June 16 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Lake Tahoe, NV.

Q: Does Copper (FCX) look like a buy now or wait for it to drop?

A: I would buy ⅓ now, ⅓ lower down, ⅓ lower down still. Worst case we get down to $30 in Freeport McMoRan (FCX) from $37 today. A new internal combustion engine requires 40 lbs. of copper for wiring, but new EVs require 200 lbs. per car, and the number of EV cars is about to go from 700,000 last year to 25 million in 10 years. So, you can do the math here. It's basically 24.3 million times 200 lbs., or 1.215 billion tons, and that's the annual increase in demand for copper over the next 10 years. There aren’t enough mines in the world to accommodate that, so the price has to go up. However, (FCX) has gone up 12 times from its 2020 low and was overdue for a major rest. So short term it's a sell, long term it's a double. That's why I put the LEAPS out on it.

Q: Lumber prices are dropping fast, should I bet the ranch that it’ll drop big?

A: No, I think the big drop has happened; we’re down 40% from the highs, the next move is probably up. And that is a commodity that will remain more or less permanently in short supply due to the structural impediments put into the lumber market by the Trump administration. They greatly increased import duties from Canada and all those Canadian mills shut down as a result. It’s going to take a long time to bring those back up to speed and get us the wood we need to build houses. Another interesting thing you’re seeing in the bay area for housing is people switching over to aluminum and steel for framing because it’s cheaper, and of course in an earthquake-prone fire zone, you’d much rather have steel or aluminum for framing than wood.

Q: I didn’t catch the (FCX) LEAP, can you reiterate?

A: With prices at today's level, you can buy the 35 calls in (FCX), sell short the 40 calls, and get nearly a 177% return by January 2022. That's an absolute screamer of a LEAPS.

Q: How do you see the working from home environment in the near future after Morgan Stanley (MS) asked everyone to return?

A: Well that’s just Morgan Stanley and that’s in New York. They have their own unique reasons to be in New York, mostly so they can meet and shake down all their customers in Manhattan—no offense to Morgan Stanley, but I used to work there. For the rest of the country, those in remote places already, a lot of companies prefer that people keep working from home because they are happier, more productive, and it’s cheaper. Who can beat that? That’s why a lot of these productivity gains from the pandemic are permanent.

Q: Is there a recording of the previous webinar?

A: Yes, all of the webinars for the last 13 years are on the website and can be accessed through your account.

Q: What makes Microsoft (MSFT) a perfect-looking chart?

A: Constant higher lows and higher highs. They also have a fabulous business which is trading relatively cheaply to the rest of tech and the rest of the main market. Of course, they were a huge pandemic winner with all the people rushing out to buy PCs and using Microsoft operating software. I expect those gains to improve. The new game now is the “wide moat” strategy, which is buying companies that have near monopolies and can’t be assailed by other companies trying to break into their businesses. The wide moat businesses are of course Microsoft (MSFT), Amazon (AMZN), Facebook (FB) and Alphabet (GOOGL). That's the new investment philosophy; that's why money has been pouring back into the FANGs for a month now.

Q: Do you have any concerns about Facebook’s (FB) advertising ability, given the recent reduction of tracking capabilities of IOS 4.5 users?

A: Well first of all, IOS 4.5 users, the Apple operating system, are only 15% of the market in desktops and 24% of mobile phones. Second, every time one of these roadblocks appears, Facebook finds a way around it, and they end up taking in even more advertising revenue. That’s been the 15-year trend and I'm sticking to it.

Q: Is Caterpillar (CAT) a LEAP candidate right now?

A: Not yet, but we’re getting there. Like many of these domestic recovery plays, it is up 200% from the March lows where we recommended it. The best time to do LEAPS is after these big capitulation selloffs, and all we’ve really seen in most sectors this year is a slow grind down because there's just too much money sitting under the market trying to get into these stocks. Let’s see if (CAT) drops to the 50-day moving average at $185 and then ask me again.

Q: If you have the (FCX) LEAPS, should you keep them?

A: I would keep them since I'm looking for the stock to double from here over the next year. If you have the existing $45-$50 LEAPS, I would expect that to expire at its max profit point in January. But you may need to take a little pain in the interim until it turns.

Q: Should I bet the ranch on meme stocks like (AMC) and GameStop GME)?

A: Absolutely not, I’m amazed you haven't lost everything already.

Q: Do you think Exxon-Mobile (XOM) could rise 30% from here?

A: Yes, if we get a 30% rise in oil. We are in a medium-term countertrend rally in oil which will eventually burn out and take us to new lows. Trade against the trend at your own peril.

Q: Disneyland (DIS) in Paris is set to open. Is Disneyland a buy here?

A: Yes, we’re getting simultaneous openings of Disneyland’s worldwide. I’ve been to all of them. So yes, that will be a huge shot in the arm. Their streaming business is also going from strength to strength.

Q: How long will the China (FXI) slowdown last?

A: Not long, the slowdown now is a reaction to the superheated growth they had last year once their epidemic ended. We should get normalized growth in China at around 6% a year, and I expect China to rally once that happens.

Q: Have you changed your outlook on inflation, real or imagined?

A: I don’t think we’re going to have inflation; I buy the Fed's argument that any hot inflation numbers are temporary because we’re coming off of a one-on-one comparisons from when the economy was closed and the prices of many things went to zero. If you look at that inflation number, it had trouble written all over it. Some one third of the increase was from rental cars. One of the hottest components was used cars. You’re not going to get 100% year on year increases next year in rental or used cars.

Q: When you issue a trade alert, it’s always in the form of a call spread like the Microsoft (MSFT) $340-$370 vertical bull call spread. What are the pros and cons of doing this trade on the put side, like shorting a vertical bear put spread?

A: It’s six of one, half a dozen of the other. There are algorithms that arbitrage between the two positions that make sure that they’re never out of line by more than a few cents. I put out call spreads because they’re easier for beginners to understand. People get buying something and watching it go up. They don’t get borrowing something, selling it short, and buying it back cheaper.

Q: Will gold (GLD) prices go up?

A: Yes, when inflation goes up for real.

Q: What is the future of the gig economy? How will that affect Uber (UBER) and Lyft (LYFT)?

A: I like both, because they just got a big exemption from California on part time workers, and that is very positive for their business models.

Q: Do you think the government doesn’t want to cancel student debt because it will unleash inflation?

A: It’s the exact opposite. The government wants to forgive student debt because it will unleash inflation. If you add 10 million new consumers to the economy, that is very positive. As long as former students have tons of debt, horrible credit ratings, and are unable to buy homes or get credit cards, they are shut out of the economy. They can’t participate in the main economy by buying homes, shopping, or getting credit. The fact that the US has so many college grads is why businesses succeed here and fail in every other country. That should be encouraged.

Q: Where is the United States US Treasury Bond Fund (TLT) headed?

A: Short term up, long term down.

Q: Options premiums are not melting away much today; I hope they start decaying after the Fed announcement.

A: In these elevated volatility periods—believe it or not, the (VIX) is still elevated compared to its historic levels—they hang on all the way to the very last day, before expiration, before they really melt the time value on options. It really does pay to run these into expiration now. When the VIX was down at like $9-$10, that was not the case.

Q: I bought a short term expiration going long the (TLT) to hedge my position; was this smart?

A: Yes, but only if you are a professional short-term trader. If you are in front of your screen all day and are able to catch these short term moves in (TLT), that is smart. My experience is that most individual investors don’t have the experience to do that, don’t want to sit in front of a screen all day, and would rather be playing golf. Such hedging strategies end up costing them money. Also, remember that half of the moves these days are at the opening; they’re overnight gap openings and you can’t catch that intraday trading—it’s not possible. So over time, the people who take the most risk make the most money. And that means the people who don’t hedge make the most money. But you have to be able to take the pain to do that. So that’s my philosophy talk on risk taking.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trade

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/john-beer.png437510Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-18 10:02:382021-06-18 14:13:32June 16 Biweekly Strategy Webinar Q&A

If you have to ask what this classic phrase from Britain’s colonial past means, you are too young to know.

The stock market equivalent is that there is nothing to do. Just sit back and relax, watching the value of your stocks go up every day. Let the greatest monetary and fiscal stimulus work its inevitable magic.

When I said last week that stocks might go up every day in April, I wasn’t kidding. NASDAQ (QQQ) has gone up every day this month except one. The S&P 500 has seen only two down days when it was virtually unchanged.

And the best may be yet to come.

The mere prospect of a $2.3 infrastructure trillion budget is enough to keep stocks powering upward for the foreseeable future. Biden may have to negotiate the total down to get it through congress and that may be the cause of the next correction…in about three months.

What really had the phones buzzing on Thursday was the bizarre move in the bond market. After seeing spectacularly positive data, the Weekly Jobless Claims plunging by 200,000 and Retail Sales coming in at a prolific 9.8%, bonds should have crashed.

Instead, the (TLT) jumped by $2.60. That took interest rate and inflation fears packing and sent the indexes soaring to all-time highs once again.

It’s proof yet again that inflation is the boogie man that will never show. Despite the incredible strength of the economy, any time anyone tries to raise prices, another company comes along with a better product or service at half the price. Such is the relentless tide of technology.

In the meantime, Goldilocks has moved in, unpacked her bags, gotten comfortable, and has settled in for the duration. I have been so aggressive in trading the market for the last six months it is wearing me out.

So, I took a rare Saturday off, weeding the garden, setting up a new computer, and generally fixing things that I haven’t had time to attend to since last year. I lived almost normally….for a day.

One of the best Earnings Seasons in history started last week, with 25% growth expected at 81% beating forecasts. JP Morgan (JPM) and Bank of America (BAC) kicks off on Wednesday, with the big kahuna, Apple (AAPL) reporting on April 28. Expect stocks to rally until then. It may give us the first hint of the massive stimulus on the economy to come. Q2 and Q3 will be the monster quarters.

Equity Funds pick up a half trillion dollars in five months, more than they attracted over the last 12 years. It’s all rocket fuel for the ongoing market melt-up. With the Volatility Index (VIX) at a one-year low at $17, the best may be yet to come. Equity investors are the most bullish in years.

Tesla is upgraded to $1,071 per share by research firm Canaccord Genuity. The company is transitioning from low-volume high-priced cars to high-volume low-priced cars, as seen in the 47% leaps in sales during Q1. The stationary battery business is booming, thanks to a new generation of technology. Tesla is developing an Apple-type brand value in the energy market, which is worth a big premium, which competitors can’t match. Tesla has brought a machine gun to a knife fight. Global chip shortages are a risk. The stock jumped $25 on the news.

Consumer Price Index comes in muted at 0.6% in April and 2.6% YOY. The market had been fearing worse, sparking another leg up in technology stocks. Much of the gain was from a jump in gasoline prices, which are now falling. Food prices are also rising.

JP Morgan pops on upside earnings surprise, with Q1 profits soaring from $2.9 billion a year ago to an eye-popping $14.5 billion. Revenues were up 14% to $33.1 billion. Loan demand is weakening because so many people are getting government money for free. Credit card debts are being paid down.

Retail Sales explode in March, up a staggering 9.8%. New spending at bars and restaurants was a major factor, and we haven’t even started yet! Stocks soar to new highs, and the bond market takes off like a scalded chimp, taking ten-year US Treasury yields below 1.57%. It confirms my thesis that when we see actual real numbers of an unprecedented recovery, we get another new leg in the bull market.

Weekly Jobless Claims collapse to 576,000, the lowest of 2021. That's down a massive 193,000 jobs from the previous week. Herd immunity is here! Keep getting those shots!

China’s (FXI) GDP grew by a staggering record of 18.3% in Q1 at an annualized rate YOY. Strong industrial production and exports were the leaders. It presages a similar explosive growth rate for the US in Q2. We won’t know until the end of July. Having your largest customers breaking growth records is great for your business too. Buy everything on dips.

Hedge funds nailed the Bond Crash, selling short some $100 billion in paper since January. It will be more than enough to cover their losses in equity shorts. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.17% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five positions expiring at their maximum profit points in (TSLA) and the (TLT). It’s been so long since I’ve had a loss, I forgot what they looked like.

I used a puzzling $2.60 spike in the (TLT) to add to my already substantial short position in bonds (TLT) with a distant May expiration. Ten-year US Treasury yields fell all the way to 1.51%.

My 2021 year-to-date performance soared to 51.26%. The Dow Average is up 12.9% so far in 2021.

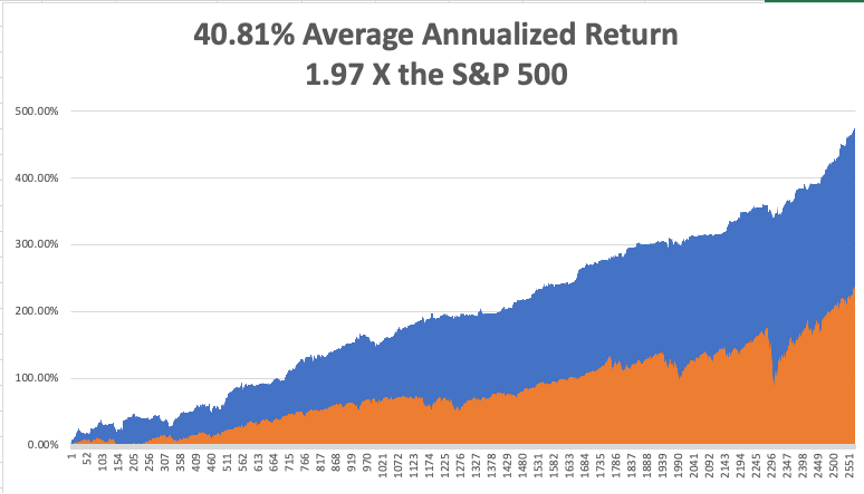

That brings my 11-year total return to 473.81%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.81%, the highest in the industry.

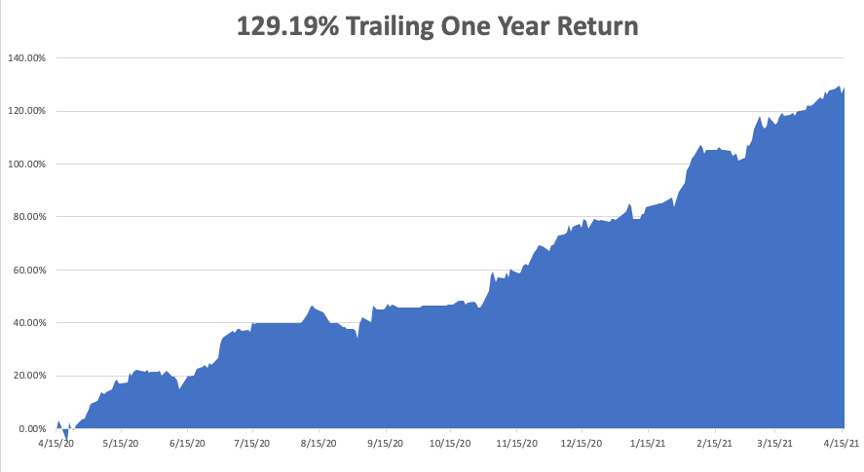

My trailing one-year return exploded to positively eye-popping 129.19%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, they increase by another 10% during the following two weeks.

We need to keep an eye on the number of US Corona virus cases at 31.6million and deaths topping 567,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 19 at 11:00 AM, earnings for (IBM), Coka-Cola (KO), and United Airlines (UAL) are released.

On Tuesday, April 20, at 4:30 PM, API Crude Stocks are published. We also get earnings for Johnson & John (JNJ) and Netflix (NFLX).

On Wednesday, April 21 at 1:00 PM, there is a big 20-year US Treasury bond auction. Chipotle (CMG) and Verizon (VZ) earnings are out. On Thursday, April 22 at 8:30 AM, the Weekly Jobless Claims are printed. At 10:00 AM Existing Home Sales for March are announced. Snap (SNAP) and Intel (INTC) announce earnings.

On Friday, April 23 at 10:00 AM, we get the New Home Sales for March. American Express (AXP) and Honeywell (HON) release earnings. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, someone commented that I walk kind of funny the other day, and the memories flooded back.

In 1975, The Economist magazine in London heard rumors that a large part of the population was getting slaughtered in Cambodia. We expected this to happen after the fall of Vietnam, but not in the Land of the Khmers. So my editor, Peter Martin, sent me to check it out.

Hooking up with a right-wing guerrilla group financed by the CIA was the easy part. Humping 100 miles in 100-degree heat wasn’t.

We eventually came to a large village that was completely deserted. Then my guide said, “Over here.” He took me to a nearby cave containing the bodies of over 1,000 women, children, and old men that had been there for months.

I’ll never forget that smell.

With the evidence and plenty of pictures in hand, we started the trek back. Suddenly, there was a large explosion and the man 20 yards in front of me disappeared. He had stepped on a land mine. Then the machine-gun fire opened up. It was an ambush.

I picked up an M-16 to return fire, but it was bent, bloody, and unusable. I picked up a second rifle and fired until it was empty. Then everything suddenly went black.

I woke up days chained to a palm tree, covered in shrapnel wounds, a prisoner of the Khmer Rouge. Maggots infested my wounds, but I remembered from my Tropical Diseases class at UCLA that I should leave them alone because they only ate dead flesh and would prevent gang green. That class saved my life. Good thing I got an “A”.

I was given a bowl of rice a day to eat, which I had to gum because it was full of small pebbles and might break my teeth. Farmers loaded their crops with these so the greater weight could increase their income. I spent my time pulling shrapnel out of my legs with a crude pair of plyers.

Two weeks later, the American who set up the trip for me showed up with cases of claymore mines, rifles, ammunition, and antibiotics. My chains we cut and I began the long walk back to Thailand.

It’s nice to learn your true value.

Back in Bangkok, I saw a doctor who attended to the 50 caliber bullet that grazed my right hip. It was too old to sew up so he decided to clean it instead. “This won’t hurt a bit,” he said as he poured in hydrogen peroxide and scrubbed it with a stiff plastic brush.

It was the greatest pain of my life. Tears rolled down my face.

But you know what? The Economist got their story and the world found out about the Great Cambodian Genocide, where 3 million died. There is a museum in Phnom Penh devoted to it today.

So, if you want to know why I walk funny, be prepared for a long story. I still set off metal detectors.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Doing Research

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-rifle.png681477Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-19 09:02:542021-04-19 11:13:14The Market Outlook for the Week Ahead, or Lie Back and Think of England

Landing my 1932 de Havilland Tiger Moth biplane can be dicey.

For a start, it has no brakes. That means I can only land on grass fields and hope my tail skid catches before I run out of landing strip. If it doesn’t, the plane will hit the end, nose over, and dump a fractured gas tank on top of me. Bathing in 30 gallons of 100 octane gasoline with sparks flying is definitely NOT a good long term health plan.

The stock market is starting to remind me of landing that Tiger Moth. On Friday, all four main stock indexes closed at all-time highs for the first time since pre-pandemic January. A record $115 billion poured into equity mutual funds in November. This has all been the result of multiple expansion, not newfound earnings.

Yet, stocks seem hell-bent on closing out 2020 at the highs.

And there is a major factor that the market is completely ignoring. What if the Democrats win the Senate in Georgia?

If so, Biden will have the weaponry to go bold. The economy goes from zero stimulus to maybe $6 trillion raining down upon it over the next six months. That will go crazy, possibly picking up another 10%, or 3,000 Dow points on top of the post-election 4,000 points we have seen so far.

That is definitely NOT in the market.

The other big decade-long trend that is only just starting is the weak US dollar. Lower interest rates for longer were reaffirmed by the appointment of my former economics professor Janet Yellen as Treasury Secretary.

A feeble dollar brings us a fading bond market, as half the buyers are foreigners. A sickened greenback also provides the launching pad for all non-dollar assets to take off like a rocket, including commodities (FCX), precious metals (GLD), (SLV), Bitcoin, and the currencies (UUP), (FXE), (FXA), (FXB), (FXY), and emerging stock markets like China (FXI), Brazil (EWZ), Thailand (THD), and Peru (EPU).

All of this is happening in the face of a US economy that is clearly falling apart. Weekly jobless claims for November came in at 245,000, compared to a robust 638,000 in October, taking the headline unemployment rate down to 6.9%. The real U6 unemployment rate stands at an eye-popping 12.0%, or 20 million.

Some 10.7 million remain jobless, 900,000 higher than in February. Transportation and Warehousing were up 140,000, Professional & Business Services by 60,000, and Health Care 46,000. Retail was down 35,000 as stores shut down at a record pace.

OPEC cuts a deal, adding 500,000 barrels a day to the global supply. The hopes are that a synchronized global recovery can take additional supply. Texas tea finally busts through a month's long $44 cap, the highest since March. Avoid energy. I’d rather buy more Tesla, the anti-energy.

Black Friday was a disaster, with in-store shopping down 52%. Long lines and 25% capacity restrictions kept the crowds at bay. If you don’t have an online presence, you’re dead. In the meantime, online spending surged by 26%.

Amazon (AMZN) hires 437,000 in 2020, probably the greatest hiring binge since WWII, and is continuing at the incredible rate of 3,000 a week. That takes its global workforce to 1.2 million. Most are $12 an hour warehouse and delivery positions. The company has been far and away the biggest beneficiary of the pandemic as the world rushed to online commerce.

Tesla’s (TSLA) full self-driving software may be out in two weeks, instead of the earlier indicated two years. The current version only works on freeways. The full street to street version could be worth $8,000 a car in upgrades. Another reason to go gaga over Tesla stock.

Goldman Sachs raised Tesla target to $780, the Musk increased market share to a growing market. No threat from General Motors yet, just talk. Volkswagen is on the distant horizon. In the meantime, Tesla super bear Jim Chanos announced he is finally cutting back his position. He finally came to the stunning conclusion that Tesla is not being valued as a car company. Go figure. Short interest in Tesla has plunged from a peak of 35% in March to 6% today. It’s learning the hard way.

The U.S. manufacturing sector pauses, activity in the U.S. manufacturing sector barely ticked up in November as production and new orders cratered, data from a survey compiled by the Institute for Supply Management showed on Tuesday. The ISM Manufacturing Report on Business PMI for November stood at 57.5, slipping from 59.3 in October.

Salesforce (CRM) overpays for workplace app Slack, knocking its stock down 9%. This is worth a buy the dip trade in the short-term and this is still a great tech company which is why the Mad Hedge Tech Letter sent out a tech alert on Salesforce on the dip.

Weekly Jobless Claims dive, with Americans applying for unemployment benefits falling last week to 712,000 down from 787,000 the week before. The weakness is unsurprising as we head into seasonal Christmas hiring.

The end of the tunnel for Boeing (BA) as they bring to an end an awful 2020. Irish-based airline Ryanair Holdings placed a large order for a set of brand new Boeing 737 MAX aircraft, giving the plane maker a shot in the arm as the single-aisle jet comes off an unprecedented 20-month grounding.

Ryanair, Europe’s low-cost carrier, has 135 Boeing 737 MAX jets on order and options to bring the total to 200 or more. Hopefully, they won’t crash this time around. My fingers are crossed.

Dollar Hits 2-1/2 Year Low. With global economies recovering, the next big-money move will be out of the greenback and into the Euro (FXE), the Aussie (FXA), the Looney (FXC), the Japanese yen (FXY), the British pound (FXB), and Bitcoin. Keeping interest rates lower for longer will accelerate the downtrend.

When we come out the other side of this pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch catapulted to another new all-time high. December is up 5.34%, taking my 2020 year-to-date up to a new high of 61.78%.

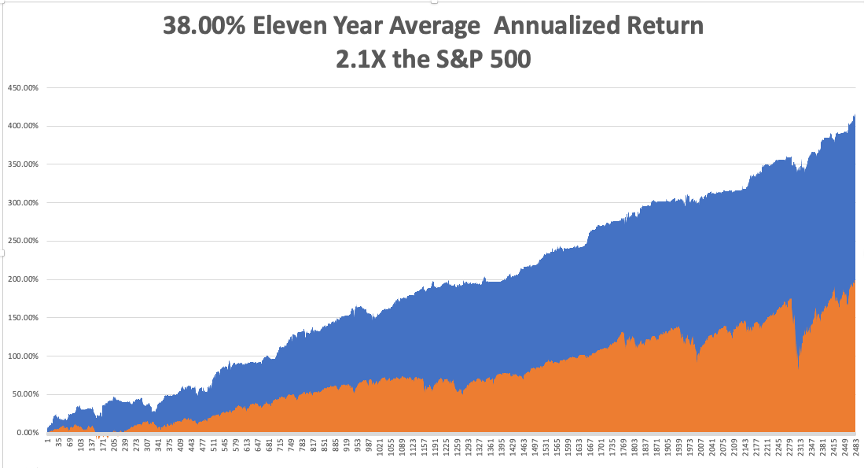

That brings my eleven-year total return to 417.69% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.00%. My trailing one-year return exploded to 64.56%. I’m running out of superlatives, so there!

I managed to catch the 50%, two-week Tesla melt-up with a 5X long position, which is always nice for performance.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 14.5 million and deaths at 285,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 7 at 4:00 PM EST, US Consumer Credit is out.

On Tuesday, December 8 at 11:00 AM, the NFIB Business Optimism Index is published.

On Wednesday, December 9 at 8:00 AM, MBA Mortgage Applications for the previous week are released.

On Thursday, December 10 at 8:30 AM, the Weekly Jobless Claims are published. At 9:30 AM, US Core Inflation is printed.

On Friday, November 11, at 9:30 AM EST, the US Producer Price Index is announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, at least there is one positive outcome from the pandemic. Boy Scout Christmas tree sales are absolutely through the roof! We took delivery of 1,300 trees from Oregon for our annual fundraiser expected to sell them in two weeks. We cleared out our entire inventory in a mere six days!

We sold trees as fast as we could load them. With the scouts tying the knots, only one fell onto the freeway on the way home. An “all hands on deck” call has gone out to shift the inventory.

It turns out that tree sales are booming nationally. The $2 billion a year market places 21 million trees annually at an average price of $8 and are important fundraisers for many non-profit organizations. It seems that people just want something to feel good about this year.

Governor Gavin Newsome’s order to go into a one-month lockdown Sunday night inspired the greatest sales effort I have ever seen, and I worked on a Morgan Stanley sales desk! We shifted the last tree hours before the deadline, which was full of mud with broken branches and had clearly been run over by a truck at a well-deserved 50% discount.

I can’t wait until next year!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-chainsaw-e1607348125295.png500328Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-07 09:02:522020-12-07 09:18:03The Market Outlook for the Week Ahead, or a Dicey Landing

Below please find subscribers’ Q&A for the September 16 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Is the Russian vaccine real or just a publicity stunt?

A: I would say it’s real. Russia is much more prone to experimentation, that is a luxury they have. If they kill off a million people because the vaccine is no good, there is no litigation risk. So, it may work, but it is a high-risk drug.

Q: What will a contested election mean for the markets?

A: The Dow (INDU) will be down 2,000 points in one day. But I don’t think it’s going to happen; I think the media has greatly exaggerated the chances of a Trump victory. I don’t think there are any undecided votes now. The only way you’d be undecided by now is if you’ve lived in a care for the past four years. The market has got this completely wrong, and once it’s clear who won, you’ll get a monster rally in the stock market that goes until this year’s end, and the game from here until election day is to try to get into the market as low as possible before then.

Q: Do you think big tech is a crowded trade, and what do you think will eventually happen?

A: It is an extremely crowded trade; eventually it will go down big. If you remember the Dotcom Bubble, everything dropped 80% or went to zero. Having said that, we’ve never had this amount of Fed stimulus before, so we should go higher first, especially after the election. The fact is that the big techs are growing gangbusters—30%, 40%, or 50% a year so spectacular multiples are called for. This is the argument Mad Hedge Fund Trader has been making for the last 10 years, by the way.

Q: Do you think the residential real estate market will crash before or after the election?

A: I would say well after the election because I don't think it will crash until 2030. All these millennial buyers are out there in droves, interest rates are at record lows, and you have this massive work-at-home trend going on, which is going to be largely permanent. So, all of a sudden, the demand is huge for homes that you can convert into a kitchen with 4 home offices. A lot of companies have discovered this to be a very profitable way to work. So, I don’t see any crash happening in housing, perhaps even in my lifetime. We’re not seeing all the excesses in housing now that we saw in the Great Recession 13 years ago.

Q: How will Joe Biden’s election change the wealth of America’s finances?

A: Move money from the extremely rich to the middle class. That is the one-liner. It looks like any tax increases for individuals who make less than $400,000 a year will be minimal. The big hit will be those that make over a billion a year, and that category could even see Roosevelt level tax rates of 90% or more.

Q: What do you think of the condo market in San Francisco?

A: It is terrible now with prices down about 20%. We’re seeing exactly the same thing in New York City as people flee to the suburbs, and in the meantime, we have bidding wars going on in the outer suburbs. This will continue for about another year until people pour back into the city once the pandemic all-clear signal is given. That may be in about two years.

Q: Tesla (TSLA) has retraced half of its recent losses; do you think it will go another leg higher?

A: At this point, Tesla is an extremely high-risk stock. I would only want to be day trading it. The overnight gaps are so enormous. At $500 a share, it’s discounting a best-case scenario for 2025 already, so that is kind of stretching it. Better to buy the car than the stock.

Q: Do you have any other names in the EV market to recommend?

A: Absolutely not; most of the other entrants in the market have no cars and no mass production abilities, which is the real challenge, and are lagging Tesla with terrible designs. Tesla essentially has the lock on that market, and a 10-year head start. They are accelerating their technology and the only other serious producer in volume is General Motors (GM) with their Bolt, but that hasn’t really taken off. It is cheap at $30,000 but the next thing to happen is that Tesla will drop the price of their model Y below the price of the Bolt which will kill it off. But no, I wouldn't touch any of these other things. The future is all electric. Many people also underestimate the decade-long torture Tesla had to go through to get to where they are. I remember it because I have been with Elon from day one during his PayPal (PYPL) days.

Q: Would you sell Disney (DIS) here at $130? The economic climate for 2021 doesn’t look great for public mass entertainment.

A: That is all true, but their streaming business, Disney Plus, is taking off like a rocket. They just released Mulan, which I watched over the weekend with my kids and loved it. It will undoubtedly be the largest streaming movie release in history once we get a look at the numbers next month. So, they are moving into the online business at an incredible speed, and it may be enough to offset the enormous losses they are running from their hotels, cruise ships, and parks. And also, this is a reopening play big time—one of the few quality reopening plays out there—and the only reason to sell Disney here is if you think the corona epidemic will get dramatically worse and stay worse well into next year.

Q: What about battery names?

A: Batteries are still either owned by giant companies like Tesla or they’re small startups that have a nasty habit of going bankrupt. There really aren't any good clean publicly-listed plays on batteries in the markets these days.

Q: What about a short on Nikola (NKLA)?

A: If I were an aggressive day trader, that would be right in my sights. You can expect nothing but bad news to come out about Nikola. Taking a truck with no motor and then rolling it downhill and calling it a successful trial just invites short-sellers by the hoards. It’s already off 65% from its peak.

Q: Why do you say there's no future in hydrogen?

A: You need to build a large national hydrogen distribution network to make this economically viable and it’s just too expensive. Electricity infrastructure is already in place and just needs to be upgraded and modernized. Electricity is also infinitely scalable in improvements in power output, but hydrogen is only capable of straight-line improvement. No contest.

Q: What about the Solid-State Batteries?

A: I actually wrote a piece about this earlier this week. Solid-State Batteries could allow a 20-fold increase in battery efficiency for cars and houses and that may only be 2 or 3 years off as there are several in development now. QuantumScape (KCAC) is the listed leader there. Bill Gates is a major investor (click here for the link).

Q: Can we play a short-term bounce in big oil like ExxonMobile (XOM)?

A: You can, but remember, this is a trading play only, not an investment play. The long-term future for these companies is to go to zero or to get into another line of business, like alternative energy.

Q: What will happen to the market after the Fed speaks today?

A: My guess is stocks will rally as long as Jerome doesn’t say anything horrendous like “this is your last freebie; I’m raising rates at the next meeting,” which he is not going to say at the last Fed meeting before the presidential election.

Q: I am trying to get through all the fluff of misinformation out there; I want your opinion on who is winning the US-China (FXI) trade war.

A: The simple answer is that China has been winning all along. The proof of that is that their economy is growing and ours is shrinking. That’s because China managed to cap their Corona deaths at 4,000 and ours are at 200,000. In the meantime, the technology improvements in China have been enormous over the last 4 years, so none of the trade war issues, which by the way, were all focused on the lowest margin businesses that China did, have had any effect. If anything, it’s forced China to offshore their low margin business to cheap countries like India, Vietnam, and Bangladesh so they disappear as China trade. I always thought the China trade war was a mistake—it’s always better to trade with someone than go to war with them. I’ve done both and prefer the former.

Q: Do you think Biden is bullish for stocks, considering all the regulations that will be put back?

A: I don’t think there will be many regulations put back except for the energy industry, which has essentially operated regulation-free for the last three years. All of those controls—on flaring, on pipelines, and so on—those will all get put back because they were implemented by executive order, which can be reversed with the stroke of a pen. I don’t see much regulation anywhere else in the economy coming back. And in fact, since Joe Biden pulled ahead in the polls in May, the stock market has gone up almost every day. So clearly, the market thinks Joe Biden will be positive for stocks, and the possibility that he might implement an extra $6 trillion dollars in fiscal spending once in office is the reason why. You have to look at what these people do, not what they say. And my bet is that since Trump set the precedent for record deficit spending, Biden will continue that. And we’ll only worry about things like deficits when the inflation rate tops 5%, when interest rates go back to 10% in five years—all the reasons that caused the massive rise in deficits during the late 70s and early 80s.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sitting Pretty

https://www.madhedgefundtrader.com/wp-content/uploads/2018/12/John-Thomas.png418627Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-18 09:02:322020-09-18 11:09:09September 16 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.