Global Market Comments

April 18, 2024

Fiat Lux

Featured Trade:

(APRIL 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (GLD), (GE), (GM), (NVDA), (TSLA), (ARKK), (MS), (GS)

Global Market Comments

April 18, 2024

Fiat Lux

Featured Trade:

(APRIL 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (GLD), (GE), (GM), (NVDA), (TSLA), (ARKK), (MS), (GS)

Below please find subscribers’ Q&A for the April 16 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Key West, Florida.

Q: If Elon Musk died, would you sell Tesla (TSLA)?

A: Yes. A lot of Tesla’s success is because Elon Musk alone can push people to do the impossible, only because he’s the largest shareholder and therefore is in complete control of all of the dozen or so Tesla major operations. Certainly, nobody else would be crazy enough to invest in so many businesses at once, like SpaceX, like the storage business, SolarCity, Nueralink, and AI, and get away with it. But then, very few people are willing to work 24 hours/day, 7 days/week either. Musk is also the world’s greatest risk-taker with his own money. So Elon Musk is a large part of the Tesla added value; if you take him away, it just becomes another General Electric (GE) (or worse, General Motors (GM)).

Q: Are geopolitical risks in the Middle East a threat to the stock market?

A: No. Several people commented in my Monday morning letter that I didn’t even mention the Middle East, and that’s because it has no market impact beyond a day. Nobody could care less. All we can do is feel sorry for all the civilians who are dying on both sides. In my lifetime, every geopolitical crisis has been a “BUY” in the stock markets, and in all risk assets. In the old days, it used to take them a month or two to figure it out, now it takes a few hours, so you just get one down day, everybody buys into that low, and markets continue up. Far more impact on the market these days is the inflation rate because that's what the Fed is looking at and they’re the ones who have their hands on the interest rate throttle. And even if inflation does stay where it is now, they’ll still have to eventually cut rates because otherwise the half of the economy that is dependent on interest rates will be destroyed. The other technology half doesn’t really care because they’re all positive cash flow, so they benefit from high interest rates.

Q: How do you select your spread prices?

A: I look at the bid-offer spread in the market, I send you a screenshot of that bid-offer spread, and then I move 5 or 10 cents off the bid side of the market. Normally, if you tighten the spread at the bid side, you will get filled on that order, and if you don’t, just leave it in there, and the second the market trends down you’ll get filled, or if you leave it the next day you’ll get filled. Remember that the second I put out a trade alert, algorithms take it up to the offered side of the market, but algorithms have to go 100% cash by the end of the day and dump all their positions, so if you leave an order in until the end of the day, often you get filled unless there’s been a major market move.

Q: Will gold continue higher?

A: Yes it will. For a start, it isn’t selling off with other risk assets in the recent correction. (GLD) only dropped $10 from an intra-day high of $225, and even though the Fed may not be cutting interest rates today, their next move will be a cut, even if that's in 3, 6, or 9 months. So, people are buying gold for that reason. Also, historically, it’s cheap relative to other asset classes such as stocks and bonds. On top of that, you have China and Russia buying record amounts of gold to bypass the Western financial system. They’ve done that for many years and it’s finally created a big short position on the market. Oh, and they’re not making gold anymore—the amount of gold being mined has been declining now a decade as the costs of mining gold rise.

Q: Why is inflation staying so high?

A: One of the reasons is that there were huge gaps in the supply/demand system due to COVID-19 still being addressed three years after the fact. That created price spikes and all kinds of unexpected consequences. Also, a lot of the government stimulus, or “COVID money,” hasn’t been spent yet; it’s still out there at the contract level and is still being committed. Even if you signed a contract two years ago, it can take two years to get a major construction project started with the planning, design, etc. Rule of thumb in dealing with all governments: everything happens slowly. All over the country, there are construction projects starting using the Federal stimulus money, so that also creates inflation when you have $3 trillion in new spending. That’s what your local traffic jam is all about. Here in Key West, they are rebuilding the Atlantic side waterfront, and that has to cost billions of dollars, far beyond what the locals could afford. But the major component of inflation, which is labor, is flatlining now. We are seeing a lot of one-time-only increases in pay going through, and then there won’t be any after that for a long time. Rising rents are a big problem now.

Q: Can you explain the market timing index?

A: The profit predictor updates itself every time we do a mouse click for all the different algorithms to kick in and generate a new number, and every piece of research we send out has an updated market timing index in it. So, if you get all of our services with Mad Hedge Hot Tips, the Global Trading Dispatch, the Trade Alerts, etc., we’re sending out at least ten updates a day for the market timing index. Suffice it to say, the more services you buy, the more updates you get on the market timing index.

Q: Will (USO) oil sell off on peace in the Middle East?

A: Well actually we’re seeing that today—we’re getting a selloff on the highs after Israel did not launch a tit-for-tat retaliation on the missile attacks from Iran. On the day they do, you will see prices go back up again. But the goal here is to dial back responses. The rule of thumb in defense for the US is: when somebody attacks you, you attack back with twice the force. That way you discourage any further retaliation from the enemy. That certainly is how our nuclear response is designed, and it’s pretty successful because only the US has the ability to execute unlimited increases in military response.

Q: Is Starlink a Tesla company?

A: Starlink is owned by SpaceX, which is an independent company owned by Elon Musk and several venture capitalists, but of course, Elon Musk is the largest shareholder. Space X is worth about $180 billion these days with several large government contracts. It’s why Elon Musk became a US citizen (foreigners are not allowed to launch our top-secret military satellites).

Q: How far-in-the-money do you go in your spread purchases?

A: It’s totally driven by the volatility of the individual stock. If you have a boring stock, you only go 5% in the money in order to earn enough money to make it worth it. If you have high volatility stocks like Tesla (TSLA) or Nvidia (NVDA) which both have options implied in the mid-40%s, you can get away with 20% in-the-money and still make a decent profit one month out. As you can tell, I tend to gravitate towards the highest volatility stocks in the market that are liquid.

Q: Will the 10% staff cut at Tesla hurt the stock?

A: Staff cuts mean bigger profits because you’re reducing the overhead by 10%. Staff cuts in almost every other technology company have been positive for the stocks for this reason. So I would say no, and Tesla has bigger problems than staff cuts like the nuclear winter going on in EV sales.

Q: Why won’t Nvidia (NVDA) go down?

A: Well, it’s because it has such a lead against all competitors. And, you know, in any other industry you’d just go hire the staff or buy the division in order to get it to hold in the market—you can’t do that with Nvidia because they’re all rich and have stock options priced at the $1 or $2 level to lock them in for life. The CEO Jensen Huang is now the sixth richest man in the world.

Q: Why have bonds failed to rally with the rest of the market?

A: Because the Fed isn’t cutting interest rates any time soon and bonds are dependent on the level of interest rates, which means they will rise once the Fed does cut.

Q: Should I buy Goldman Sachs Group (GS) on their great earnings report?

A: Yes, trading volumes look good for the rest of the year and that is how brokerage houses make their crust of bread. Buy Morgan Stanley (MS) too. It’s a better quality company with less dependence on trading revenues and more on fee income. After all, they hired me!

Q: Should I buy Cathie Woods’s Ark Innovation ETF (ARKK) fund here?

A: Absolutely not. Highly leveraged funds and the most leveraged stocks are the last thing you buy on market tops. That is a market bottom play, and the last real market bottom we had was in October.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2024 Key West Thinking of the Next Trade Alert

Global Market Comments

September 12, 2023

Fiat Lux

Featured Trade:

(THE GREAT AMERICAN ONSHORING TREND IS ACCELERATING),

(GE), (TSLA),

(MURRAY SAYLE: THE PASSING OF A GIANT IN JOURNALISM)

(THE LAST PEARL HARBOR ARIZONA SURVIVOR)

Onshoring, the return of US manufacturing from abroad, is rapidly gathering pace.

It is increasingly playing a crucial part in the unfolding American industrial renaissance. It could well develop into the most important new trend on the global economic scene during the early 21st century. It is also paving the way for a return of the roaring twenties to our home shores.

Of course, it is hard to quantify this assumption with hard data. US government statistics are a deep lagging indicator and are unable to keep up with a rapidly changing, interconnected, fluid world. No doubt, they will tell us this epoch-making sea change is underway in ten years.

However, it is possible to track what a single company is accomplishing. In 1973, General Electric (GE) ran the largest home appliance manufacturing facility in the world. Its Appliance Park in Louisville, Kentucky, employed 23,000 workers packed into six gigantic buildings, each as large as a shopping mall. It was so big, it even earned its own postal zip code (40225).

After that, the offshoring mania kicked in, with the firm motivated by a single factor: hourly wages. You could hire 30 men in China for the cost of one American union worker. The savings were too compelling to pass up, and The Great Hollowing Out of US manufacturing was off to the races.

GE tried to sell the entire operation but was too late. The 2008 financial crisis decimated the market for Midwest industrial facilities. You could only get the scrap metal value, or three cents on the dollar. By 2011 employment at Appliance Park had plunged to 1,863, and the region’s new “Rust Belt” sobriquet was well earned.

Then, almost imperceptibly at first, the trend started to reverse. Decades of 20% a year wage increases took the cost of a skilled Chinese worker from $300 a year to $25,000. The 2011 Japanese tsunami, followed by huge floods in Thailand, caused massive disruptions to the international parts supply network.

A minor strike by the Longshoreman’s Union at the Port of Oakland in California brought the distribution channel to a grinding halt. Business plans that looked great on an Excel spreadsheet turned out to be not so hot in practice.

It gets worse. When Chinese workers walked across the street to collect bigger pay packages, they often took blueprints, business plans, and proprietary software with them. Six months later, a local competitor would show up with a similar, although inferior, product at half the cost. Suddenly, globalization was not all it was cracked up to be.

In the meantime, the American labor force, reading the Chinese characters on the wall, evolved. Unions were disbanded. Antiquated work rules were tossed. The unions that were left agreed to two tier wage structures that had entry level employees coming in at $13.50 an hour, a fraction of the original rate.

Then management got smarter. By removing the assembly line from the marketplace, companies lost touch with customers. Designers lost contact with the manufacturing process, creating products that could only be built expensively, or not at all. Quality plummeted. Innovation suffered. By bringing manufacturing home, firms not only solved these problems, they were able to build better ones for less money.

China turned out to be farther away than people thought. Having middle management jet lagged up to three months a year proved to be very expensive. It takes six weeks to ship an appliance from the Middle Kingdom to the US if the shipping schedules are perfect.

An American plant can truck product to most US stores within two days. That wasn’t a problem when consumer products saw lives that ran into decades. It is a big deal when rapidly accelerating technological improvements require them to be turned over every three years or less, as they are today.

The energy picture is undercutting the arithmetic that used to justify offshoring. Oil prices levitating near $100 a barrel are up 400% in 14 years, elevating the cost of production in Asia and shipments to the US. In the US, the fracking boom has let lose a gusher of cheap oil. It has also freed up a few centuries worth of low carbon burning natural gas, giving American manufacturers a further cost advantage.

Better American management techniques are giving US based factories an edge. I saw this up close at the Tesla (TSLA) factory in Fremont, California, where workers have the ability to improve the assembly process daily and are incented to do so. The place was so clean and quiet, it felt more like a hospital than a factory. It turns out that a drive train with only 11 parts doesn’t require much labor to assemble it, and robots do most of that.

By adopting similar techniques, GE, is building the same number of appliances as it did during the 1960’s peak, about 250,000 a year, with one third of the employees.

Using the new thinking, many companies are finding out that offshoring was a big mistake in the first place, and are bringing production home. Some business analysts estimate that up to a quarter of the companies that offshored lost money doing it.

The fact that GE is onshoring is important. It is considered by many to be the best-run industrial company in the United States, and when it leads, many follow. On the heels of the GE move, Whirlpool has relocated its mixer assembly from China to Ohio, and Otis has brought home elevator making from Mexico.

Even Wham-O has jumped on board, the maker of Frisbees, Slinkies, and Hula Hoops, and a company that is dear to my heart (I dated the founder’s daughter in high school), moving production from the Middle Kingdom back to Southern California.

If I am right, and onshoring speeds up into the next decade, we may get another opportunity to relive the roaring twenties. By then, a shortage of workers will lead to higher wages, greater consumer spending, and rising standards of living. The price of everything will rocket, including your stocks and homes. US GDP growth will surge to 4%-5% a year. Inflation will, at long last, make its long-predicted return.

It will be an economy in which Jay Gatsby will feel right at home.

Global Market Comments

June 26, 2023

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IS THERE A COUP UNDERWAY IN RUSSIA?),

(AAPL), (GOOGL), (MSFT), (GE), (MU), (AMZN)

CLICK HERE to download today's position sheet.

I just received a call from the Marine Corps to go on emergency standby. This is not something the Corps does lightly.

The word is that there may be a coup d'etat underway in Russia and the entire US military has gone to a heightened alert status.

The Wagner group is Marching on Moscow with the intent of overthrowing the government, or at least the military. Putin took off in a plane which then disappeared radar, meaning he has either been shot down, or is flying low level to keep his destination secret.

This thing could go nuclear very easily, but only in Russia. It also could mean the end of the Ukraine War. There is nothing to do here as intelligence pours in over the weekend. We have ample satellites overhead and human intel on the ground.

Expect market volatility today. The markets are ripe for a black swan-inducted selloff, which a Mad Hedge Market Timing Index at 82 was screaming at us.

I will be monitoring the situation closely.

My view that the markets were topping was vindicated last week. The “Magnificent Seven” which gained a record 25% in market capitalization in only eight weeks led the downturn, as they always do. But the AI surge that prompted the fastest equity creation in history is only just getting started.

This is against a backdrop of savage cost-cutting by Big Tech, which has had the effect of boosting earnings by an impressive 7% in only three months. My cleaning lady, gardener, dry cleaner, and shoe shine boy have started giving me stock tips yet, as they did in 2000, 2008, and 2020….but they are thinking about it.

While attention is focused elsewhere, one should not underestimate the importance of India Prime Minister Modi’s meeting with Joe Biden in Washington.

It signifies a major geopolitical shift out of the Russian orbit into the US one. Decades ago, India obtained all its weapon systems and nuclear power plants from Russia and was a major trading partner.

Now partnering up with Apple (AAPL), Google (GOOGL), Microsoft (MSFT), and General Electric (GE) is a much more attractive option. It is gaining a $2.7 billion factory from Micron Technology (MU) and presents a major market for its products. Amazon (AMZN) is investing $13 billion in cloud infrastructure there. The subcontinent graduates some 2.5 million STEM graduates a year and they need to be put to work in the global economy. It shows how limited Russia’s future really is. It’s a major win for the US.

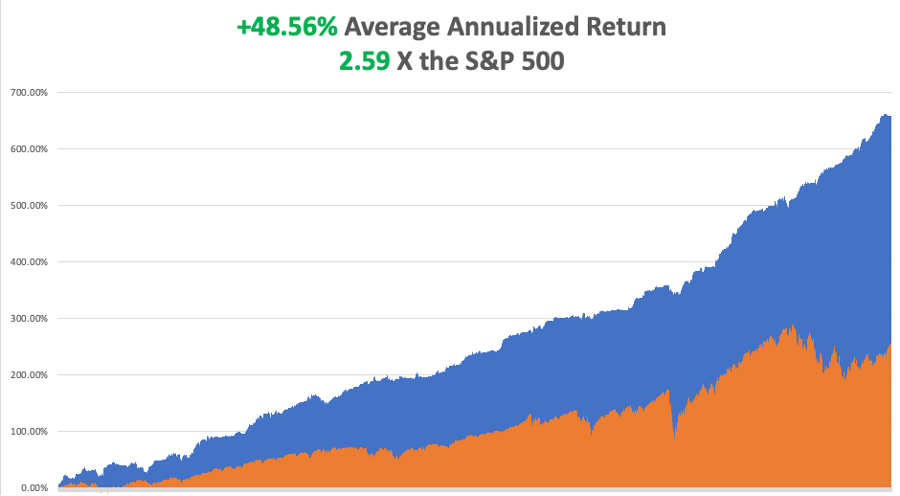

So far in June, we are up +0.47%. My 2023 year-to-date performance is still at an eye-popping +62.52%. The S&P 500 (SPY) is up only a respectable +14.00% so far in 2023. My trailing one-year return reached +96.63% versus +21.52% for the S&P 500.

That brings my 15-year total return to +659.71%. My average annualized return has blasted up to +48.56%, another new high, some 2.59 times the S&P 500 over the same period.

Some 42 of my 46 trades this year have been profitable. Only 23 of my last 24 consecutive trade alerts have been profitable.

The Mad Hedge December 6-8 Summit Replays are Up. Listen to all 28 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. It is a true smorgasbord of investment strategies. Find the best one to suit your own goals. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here and then choosing the speaker of your choice. We look forward to working with you.The next summit is scheduled for September 12-14.

$2 Billion Fled Stock Market Last Week, according to a Bank of America survey, in what it calls a “Baby Bubble.” The markets are showing all the signs of an interim top, with either a 10% correction or a three-month flat line ahead of us. Time to strap on those Buy Writes for long-term shareholders.

Short Bets on US stocks Hit $1 trillion, the highest since April 2022. Shorts have so far lost $101 billion in 2023, with much of this hedged. The market is way overdue for a correction so these guys may finally be right. Even a broken clock is right twice a day.

Germany Signs Massive US Natural Gas Contract, in a major move to end reliance on Russian natural gas. Venture Global LNG will supply EnBW with 1.5 million tons a year of LNG starting in 2026. The 20-year sales and purchase agreement is Germany’s first binding deal with a US developer since the government announced ambitious plans to begin importing the super-chilled fuel. The move does a lot to eliminate the glut of gas in the US currently plaguing producers. Buy (UNG) LEAPS on dips. When China comes back on line, watch out!

Volatility Index ($VIX) Hits the $12 Handle, in a new multiyear low. At the high for the year in the S&P 500, complacency is running rampant. Time to add some downside hedges.

Copper Should be a “Critical Metal”, says billionaire Robert Friedland. A looming structural shortage is the reason, with the world going to an all-electric auto fleet and doubling of the electrical grid to accommodate it. Buy more (FCX) LEAPS on dips.

Leading Economic Indicators Down 0.7% for the 15th consecutive negative month. We are approaching the bottom of the trough in this cycle. I’ll focus on the half of the economy that is growing.

Distressed Commercial Property Debt is Exploding, up 10% to Q1 to $64 billion. Another $155 billion is waiting in the wings. This will go away when interest rates start to drop in six months.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 26 at 8:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, June 27 at 6:00 PM, S&P Case-Shiller National Home Price Index is published.

On Wednesday, June 28 at 7:30 AM, the Fed Governor Jay Powell speaks.

On Thursday, June 29 at 8:30 AM, the Weekly Jobless Claims are announced. The Final Report for Q1 US GDP is printed.

On Friday, June 30 at 8:30 AM, Personal Income and Spending is announced.

As for me, when I first met Andrew Knight, the editor of The Economist magazine in London 45 years ago, he almost fell off his feet. Andrew was well known in the financial community because his father was a famous WWII Battle of Britain Spitfire pilot from New Zealand.

At 34, he had just been appointed the second youngest editor in the magazine’s 150-year history. I had been reporting from Tokyo for years, filing two stories a week about Japanese banking, finance, and politics.

The Economist shared an office in Tokyo with the Financial Times, and to pay the rent I had to file an additional two stories a week for them as well. That’s where I saw my first fax machine, which then was as large as a washing machine even though the actual electronics would fit in a notebook. It cost $5,000.

The Economist was the greatest calling card to the establishment one could ever have. Any president, prime minister, CEO, central banker, or war criminal was suddenly available for a one-hour chart about the important affairs of the world.

Some of my biggest catches? Presidents Gerald Ford, Jimmy Carter, Ronald Reagan, George Bush, and Bill Clinton, China’s Zhou Enlai and Deng Xiaoping, Japan’s Emperor Hirohito, terrorist Yasir Arafat, and Teddy Roosevelt’s oldest daughter, Alice Roosevelt Longworth, the first woman to smoke cigarettes in the White House in 1905.

Andrew thought that the quality of my posts was so good that I had to be a retired banker at least 55 years old. We didn’t meet in person until I was invited to work the summer out of the magazine’s St. James Street office tower, just down the street from the palace of then Prince Charles.

When he was introduced to a gangly 25-year-old instead, he thought it was a practical joke, which The Economist was famous for. As for me, I was impressed with Andrew’s ironed and creased blue jeans, an unheard-of concept in the Wild West where I came from.

The first unusual thing I noticed working in the office was that we were each handed a bottle of whisky, gin, and wine every Friday. That was to keep us in the office working and out of the pub next door, the former embassy of the Republic of Texas from pre-1845. There is still a big white star on the front door.

Andrew told me I had just saved the magazine.

After the first oil shock in 1973, a global recession ensued, and all magazine advertising was cancelled. But because of the shock, it was assumed that heavily oil-dependent Japan would go bankrupt. As a result, the country’s banks were forced to pay a ruinous 2% premium on all international borrowing. These were known as “Japan rates.”

To restore Japan’s reputation and credit rating, the government and the banks launched an advertising campaign unprecedented in modern times. At one point, Japan accounted for 80% of all business advertising worldwide. To attract these ads the global media was screaming for more Japanese banking stories, and I was the only person in the world writing them.

Not only did I bail out The Economist, I ended up writing for over 50 business and finance publications around the world in every English-speaking country. I was knocking out 60 stories a month, or about two a day. By 26, I became the highest paid journalist in the Foreign Correspondents’ Club of Japan and a familiar figure in every bank head office in Tokyo.

The Economist was notorious for running practical jokes as real news every April Fool’s Day. In the late 1970s, an April 1 issue once did a full-page survey on a country off the west coast of India called San Serif.

It warned that if the West coast kept eroding, and the East coast continued silting up, the country would eventually run into India, creating serious geopolitical problems.

It wasn’t until someone figured out that the country, the prime minister, and every town on the map were named after a type font that the hoax was uncovered.

This was way back, in the pre-Microsoft Word era, when no one outside the London Typesetter’s Union knew what Times Roman, Calibri, or Mangal meant.

Andrew is now 84 and I haven’t seen him in yonks. My business editor, the brilliant Peter Martin, died of cancer in 2002 at a very young 54, and the magazine still awards an annual journalism scholarship in his name.

My boss at The Economist Intelligence Unit, which was modeled on Britain’s MI5 spy service, was Marjorie Deane, who was one of the first women to work in business journalism. She passed away in 2008 at 94. Today, her foundation awards an annual internship at the magazine.

When I stopped by the London office a few years ago I asked if they still handed out the free alcohol on Fridays. A young writer ruefully told me, “No, they don’t do that anymore.”

Sometimes, change is for the worse, not the better.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 23, 2023

Fiat Lux

Featured Trades:

(JUNE 21 BIWEEKLY STRATEGY WEBINAR Q&A),

(AAPL), (ABNB), (GLD), (BA), (CAT), (DE), (X), (PYPL), (SQ), (MSFT), (GD), (GE), (INDA), (META) (GOOGL), (CCI), (NVDA), (ABNB), (SNOW), (PLTR), (TSLA)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the June 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, NV.

Q: When do we buy Nvidia (NVDA) and Tesla (TSLA)?

A: On at least a 20% dip. We have had ballistic moves—some of the sharpest up moves in the history of the stock market for large stocks—and certainly the greatest creation of market caps since the market was invented under the Buttonwood Tree in 1792 at 68 Wall Street. Tesla’s almost at a triple now. Tripling one of the world's largest companies in 6 months? You have to live as long as me to see that.

Q: Is it a good time to invest in Bitcoin?

A: No, absolutely not. You only want to invest in Bitcoin when we have an excess of cash and a shortage of assets. Right now, we have the opposite, a shortage of cash and an excess of assets, and that will probably continue for several years.

Q: Should I short Apple (APPL)?

A: Only if you’re a day trader. It’s hugely overbought for the short term, but still in a multiyear long-term uptrend. I think we could see Apple at $300 in the next one or two years.

Q: Is it better to focus on single stocks or ETFs?

A: Single stocks always, because a single stock will outperform a basket that's in an ETF by 2 to 1 or even 3 to 1. That's always the case; whenever you add stocks to a basket, it diversifies risk and dilutes the performance. Better to just own Tesla, and if you want to diversify, diversify to Nvidia, but then I live next door to these two companies. That's what I tell my friends. You only diversify if you don’t know what is going to happen, which is most investors and financial advisors.

Q: Is the bottom of the housing market in, and are we due for a spike in home prices when interest rates can only go lower?

A: Yes, absolutely. In fact, we will enter a new 10-year bull leg for housing because we have a structural shortage of 10 million homes and 82 million millennials desperately trying to buy them at any price. I just got a call from my broker and she is panicking because she is running out of inventory. Even the lemons are starting to move.

Q: When do you think energy will rise?

A: Falling interest rates could be a good key because it sets the whole global economy on fire and increases energy demand.

Q: Outlook for the S&P 500 (SPY) second half of the year?

A: We hit 4,800 at least, maybe even higher. That's about a little more than 10% from here, so it’s not that much of a stretch, not like it was at the beginning of the year when it needed to rise 25% to reach my yearend target.

Q: Best time to invest from here on?

A: Either a 10% pullback in the market, or a sideways move of 3 months—that's called a time correction. It usually counts as a price correction because of course, over 3 months, earnings go up a lot, especially in tech.

Q: I’m seeing grains (WEAT) in rally mode.

A: Yes, that's true. They are commodities, and just like copper’s been rallying, and it’s yet another signal that we may get a much broader global commodity rally in everything: iron ore, coal, energy, gold, silver, you name it.

Q: Will inflation drop to 2%, causing stocks to go on another epic run?

A: The answer is yes, I do see inflation dropping to 2% —maybe not this year, but next year; not because of any action the Fed is doing, but because technology is hyper-accelerating, and technology is highly deflationary. The tech product you bought two years ago is now half the price, and they offer you twice as much functionality with an auto-renew for life. So, that is happening across the entire technology front and feeds into the inflation numbers big time, including labor. There's going to be a lot of labor replacement by machines and AI in the coming years.

Q: Is Airbnb (ABNB) a good stock to buy?

A: Well, if we’re going into the most perfect travel storm of all time, which is this summer, and which is why I’m going to remote places only like Cortina, Italy. Airbnb is the perfect stock to own. It’s a well-run company even in normal times.

Q: Should I buy gold here on the pullback?

A: Yes, you should. Gold is also highly sensitive to any decline in interest rates, and by the way: buy silver, it always moves 2.5x as much as the barbarous relic.

Q: How can inflation not go up if commodities and wage demands are going up due to state and federal unions? What about farm equipment and truck supplies? Costs keep rising, should we buy John Deere (DE)?

A: There are three questions here. Inflation will not go up because, though commodities will rise, they are only 0.6% of the $100 trillion global economy, or $660 billion in 2022. That will be more than offset by technology cutting prices, which is 30% of the stock market. You have to realize how important each individual element is in the global picture. And regarding wage demands going up caused by state and federal unions, less than 11.3% of the workforce is now unionized and that figure has been declining for 40 years. Most growth in the economy has been in non-unionized technology firms which largely depend on temporary workers, by design. What IS unionized is mostly teachers, the lowest paid workers in the economy, so incremental pay rises will be small. Unions were absolutely slaughtered when 25 million jobs were offshored to China during the Bush administration. Buy farm equipment and trucks? Absolutely, buy John Deere (DE) and buy Caterpillar (CAT) on the next dip. I was actually looking at Caterpillar for the next LEAPS the other day, but it’s already had a big run; I'm going to wait for a pullback before I get CAT and John Deere. So, again, people see headlines, see union wage headlines—I say focus on the 89% and not on the 11% if you want to make good decisions.

Q: Is Boeing (BA) a buy on the dip?

A: Yes, they got 1,000 new aircraft orders and the stock hasn't moved. So yes, if you get any kind of selloff down to $200, I'd be hoovering this thing up.

Q: Can you please explain how the profit predictor works?

A: It’s a long story; just go to our website, log in and do a search for “profit predictor,” and you’ll get a full explanation of how it works. It’s actually where Mad Hedge has been using artificial intelligence for 11 years, which is why our performance has doubled. Just for fun, I'll run the piece next week.

Q: Gold (GLD) is having a hard time going up because Russia is being squeezed by other governments. Since they need cash, they may be either selling their gold or stop buying new gold.

A: That is a good point, but at the end of the day, interest rates are the number one driver of all precious metals—period, end of story. We’re long gold too, I’ve got lots of gold coins stashed around the world in various safe deposit boxes, and I'm keeping them. I’ve got even more silver coins, which take up a lot of space.

Q: Do you like India (INDA) long term?

A: Yes, it’s the next China. But as Apple is finding out it is very difficult to get anything done there. A radical reforming Prime Minster Modi may be changing things there with his recent Biden visit and (GE) contract to build jet engines.

Q: What do you think of General Dynamics Corp (GD)?

A: I like General Dynamics because I think defense spending is in a permanent long term upcycle as a result of the Ukraine war. And it won’t end with the Ukraine war—the threat will always be out there, and the buying is done by not only us but all the other countries that think Russia is a threat.

Q: Do you like MP Materials Corp (MP)?

A: Yes, I do. The whole commodities space is ready to take off and go on fire.

Q: What about Square (SQ)?

A: The only reason I’m not recommending Square right now is huge competition in the entire sector, where all the stocks including PayPal (PYPL) are getting crushed. I will pass on Square for now, especially when I can buy US Steel (X) at close to its low for the year.

Q: If you had to pick one: Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Meta (META), and Google (GOOGL), which is the best to buy for next year?

A: All of them. Diversify. If I have to pick the top performer, it’s going to be either Tesla or Nvidia, probably Nvidia. But you need at least a 10% correction before you do anything. Actually, the split-adjusted price for our first (NVDA) recommendation eight years ago was $2 a share.

Q: Do you like Crown Castle International (CCI)?

A: Yes, I like it very much—it has very high dividend yield at 5.5%. The reason it hasn’t moved yet is that as long as interest rates are high, any REIT structure will suffer, and (CCI) has a REIT structure. Sure, it’s in a great sector—5G cell towers—but it is still a REIT nonetheless, and those will start to recover when interest rates go down; that’s why we did a 2.5-year LEAPS on CCI. For sure interest rates are going to go down in the next 2.5 years, and you will double your money on (CCI). That’s why we put it out.

Q: Which mid cap will do best over the long term: Airbnb (ABNB), Snowflake (SNOW), or Palantir (PLTR)?

A: That’s easy: Snowflake. They have such an overwhelming technology on the database and security front; I would be buying Snowflake all day long. Even Warren Buffet owns Snowflake, so that’s good enough for me.

Q: Could you comment on the pace of EV adoption/potential for (TSLA) robot fleet acceleration and implications for oil investments in holding pattern till the eventual collapse to near 0?

A: Yes, oil may collapse to near zero, but it may take twenty years to do it—that’s how long it takes to transition an energy source. That’s how long it took the move from horses and hay to gasoline-powered cars at the beginning of the 20th century. A national robot fleet of taxis with no drivers at all is a couple of years off. There are about 1,000 of them working in San Francisco right now, but they still have more work to do on the software. When it gets foggy, they often congregate at intersections causing traffic jams. Suffice it to say that eventually Tesla shares go to $1,000 and after that, $10,000—that’s my bet. By the way, my Tesla January 2025 $595-$600 LEAPS are starting to look pretty good.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2018 in Australia

Mad Hedge Biotech and Healthcare Letter

March 14, 2023

Fiat Lux

Featured Trade:

(A MARKET LEADER SELLING AT A DISCOUNT)

(GE), (GEHC), (MTD), (DHR), (BSX), (TMO)

The spanking new multibillion-dollar healthcare spinoff from General Electric (GE) is gradually turning into a favorite in the industry.

The healthcare company, GE HealthCare (GEHC), was officially spun out of GE last January 4, but its shares began trading around mid-December. To date, GEHC is up about 30%. The stock has been trading for roughly 23 times its projected earnings in 2023.

While that value is already above the market multiple, GEHC is still anticipated to boost its earnings at an average of approximately 15% per year until 2026.

GEHC’s fourth-quarter earnings report was pretty solid. The company recorded $4.94 billion in revenue, rising by 8% year over year compared to the previous $4.59 billion. Most of the growth came from its imaging division, which climbed 11% from $2.44 billion to $2.71 billion thanks to the increasing demand.

For this year, GEHC is projected to generate over $19 billion in sales. This estimate is conservative since the company has yet to gain traction on Wall Street. Given its solid performance thus far, the company is expected to post a higher figure in the coming months.

Not much is known about GEHC yet. Aside from being an Illinois- based healthcare company focusing on medical technology, healthcare software and analytics, patient monitoring systems, and medical equipment maintenance and repair services, the spinoff only describes itself as “a leading global precision care innovator.”

That’s a relatively vague explanation that could cover much ground, but it appears to be focused on artificial intelligence (AI) in healthcare. After all, this is a lucrative and growing market that has sustained the ever-increasing demand.

Based on its records, GEHC generates the majority of its revenue from ultrasound and imaging services and products. These segments comprise about 75% of the company’s overall revenue. The rest are from various services, including clinical networking systems and financial solutions.

At the moment, more than 4 million of GEHC’s products are installed across the globe, lending support to over 2 billion patients since 2022.

Although this sounds less exciting than the other developments in the healthcare industry, the total addressable market for the medical imaging segment is impressively huge.

In 2021, this market was projected to reach $28 billion and will reach $47.4 billion by 2030. This represents a promising compounded annual growth rate of 4.9%. Critical to this growth and expansion is the climbing number of chronic diseases, which triggered earlier and more frequent checkups.

GEHC notably ensures that it sustains its momentum and gains a larger market share. The company has invested aggressively in research and development, allocating $2.7 billion to this effort alone from 2020 to 2022.

In February, the spinoff shelled out $3 billion to acquire Caption Health, a healthcare technology company developing AI software for medical imaging. The company's flagship product, Caption AI, is an FDA-approved medical imaging software that uses AI to guide healthcare professionals in acquiring and interpreting ultrasound images.

Basically, Caption AI is designed to help healthcare professionals who may need more specialized training in medical imaging, such as primary care physicians and nurses, to accurately and confidently perform and interpret ultrasound exams.

Apart from those, Caption Health's AI technology can assist in acquiring cardiac, lung, abdominal, and musculoskeletal images. It is intended to improve patient access to quality care by reducing the need for specialized medical personnel to conduct ultrasound exams.

By leveraging AI, these services could increase the speed and accuracy of diagnoses and treatment, ultimately improving patient outcomes. Needless to say, this deal significantly bolstered GEHC’s lineup and is expected to generate more than enough revenue to cover the price the company paid for the acquisition.

Despite its promising performance, GEHC remains under the radar and underappreciated. Comparing it to its peers, such as Mettler Toledo (MTD), Danaher (DHR), Boston Scientific (BSX), and Thermo Fisher (TMO), the company’s valuation looks discounted. Considering that it has the potential to become a long-term compounder, I suggest you buy the dip.