Global Market Comments

January 23, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHERE IS THE BEAR MARKET?),

(GOLD), (GLD), (WPM), (SLV), (BRK/B), (TSLA), (OXY)

CLICK HERE to download today's position sheet.

Global Market Comments

January 23, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHERE IS THE BEAR MARKET?),

(GOLD), (GLD), (WPM), (SLV), (BRK/B), (TSLA), (OXY)

CLICK HERE to download today's position sheet.

The Pivot has started.

Not by the Fed, which is not expected to begin lowering interest rates by the summer or fall.

It's the stock market that has pirouetted, from bear to bull last October. The higher stocks rise in this miraculous, coming-from-nowhere rally, the more credibility this rally gains.

If a new bull market has well and truly begun, then there are an awful lot of portfolios out there that have the wrong stocks. Repositioning this late in the game could take the indexes to new all-time highs by yearend.

Some portfolio managers are whistling past the graveyard right now.

The Fed pivot may also take place ahead of schedule. The marketplace has shaved the February 1 interest rate hike from 50 basis points to only 25, which explains stocks’ recent virility.

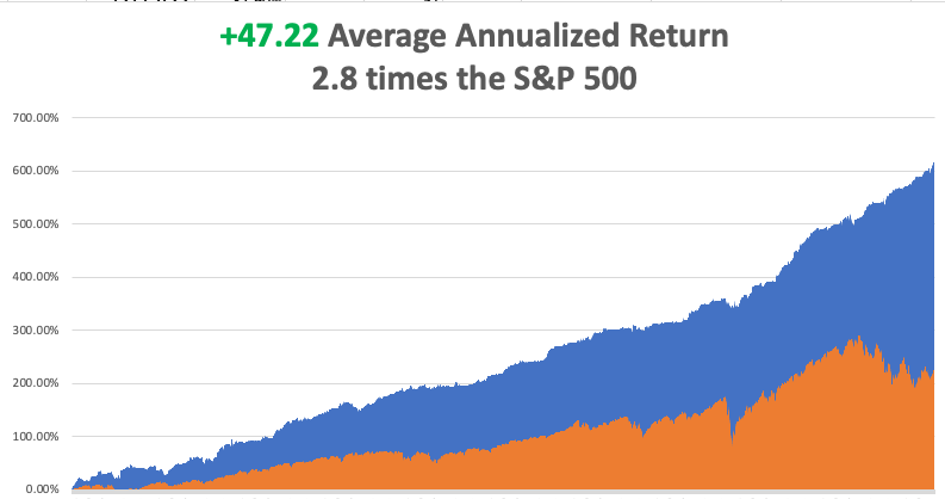

My trading performance certainly shows the possibilities, which so far has tacked on a robust +20.65%. My 2023 year-to-date performance is the same at +20.65%, a spectacular new high. The S&P 500 (SPY) is up +1.86% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky high +107.27%.

That brings my 15-year total return to +617.84%, some 2.8 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.22%, easily the highest in the industry.

Last week, I rode into the Friday options expiration with my 5X weighting in bonds, as well as additional longs in (TSLA), (GOLD), (WPM), and (BRK/B). Both my remaining positions are profitable, including longs in (TSLA) and (OXY) with 80% cash for a 20% net long position.

Stocks are not the only asset class on a tear because of an earlier than expected Fed easing.

Precious metals have been going virtually straight up. For the first time since the US went off the gold standard 50 years ago, gold (GLD) outperformed the S&P 500 in Q4, and silver (SLV) did even better.

Not only does gold benefit from falling inflation and interest rates, the end of the Fed’s quantitative tightening (QT) will provide a further steroid shot as well.

Sanctions against Russia and China have sent central bank purchases of the barbarous relic to new all-time highs. And you might speculate that the possible Russian use of nuclear weapons is also driving your gold northward, but you would be wrong. You may find this shocking, but Ukraine has their own nukes and if Russia attacked, Moscow would be radioactive that week.

The bottom line here is that the yellow metal could well remain strong all year and be a top performer.

Bonds continued their on again, off again rally. The prospects of falling interest rates pushes them up and then fears of a summer default push them back down again, some $2.50 for the (TLT) last week.

One thing is certain. If the Treasury is pushed into default the Fed definitely WILL NOT be raising interest rates. They won’t need to crush the economy. The House of Representatives will be doing their job for them.

The least appreciated piece of news last week was the report that China’s population fell for the first time in 50 years, thanks to a massive famine. I remember it like it was yesterday as I was there. Believe me, there are no substitutes for food. It took me a king’s ransom and some banned western books just for me to procure a single egg.

This will affect us all as there will be a sudden shortage of customers in the global economy in about 20 years. You may think that 20 years is a long time off, but the best run companies will start planning and investing for this now.

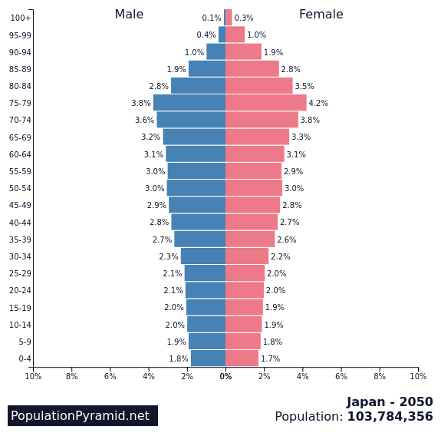

If you don’t think a shrinking population is bad for business, just ask Japan, where they’re not making Japanese anymore. Japan has suffered the worst performing stock market for the last 32 years and is still showing a negative return.

That was a nice bail!

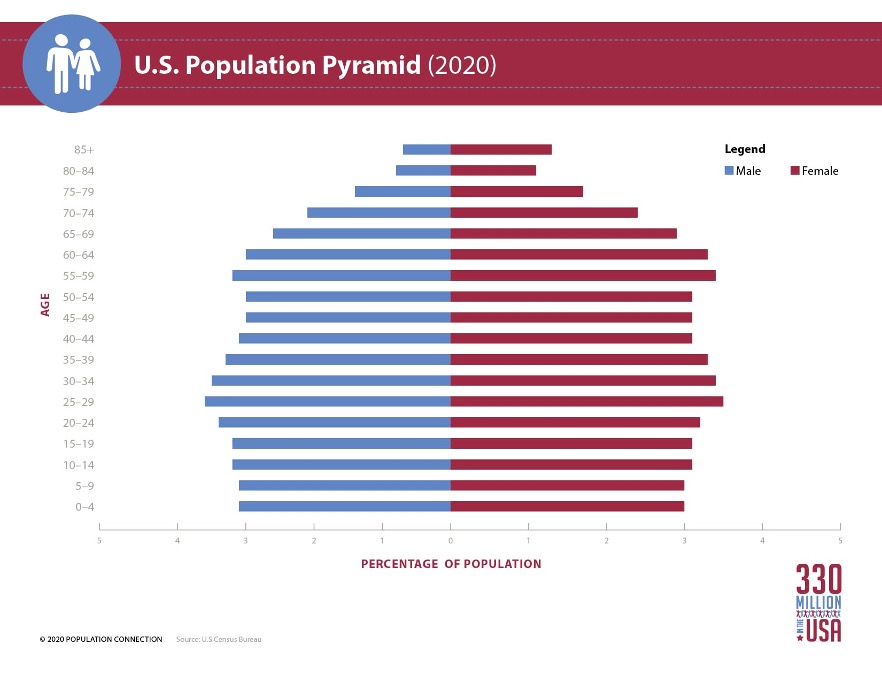

Remember, demographics is destiny. Check out the population pyramid charts below.

The Fed May Retreat to 25 Basis Point, in their February 1 rate hike, according to a Reuters poll. It might explain why stocks have been so hot in January.

Treasury Secretary Warns of Coming US Bond Default, saying the government runs out of money by June. Bonds plunged $2.00 on the news. The House of Representatives need to raise the debt ceiling before then, or the Treasury will cease paying interest on the $31.4 trillion national debt. This is for money already spent by administrations going back to the 1980’s. Rising interest rates have already taken America’s debt service from 5% to 10% of the total budget.

This Year Won’t Be as Bad as Last, or so hope the bulls that have been piling into stocks since January 3. The weakness in tech stocks actually understates the ballistic moves in value, metals, and financial stocks, which Mad Hedge is long. Things are better than they appear. That’s what six months of deflation will do.

China Reopening Accelerates and may well head off a global recession. Letting everyone get covid and achieving heard immunity turned out to be the key. It’s demolished the entire January selloff scenario.

Wholesale Prices Drop 0.5% in December versus an expected 0.1% in another big step toward the unwind of inflation. The energy sub index fell by 7.9%. I am looking like a 4% inflation rate by yearend.

Builder Sentiment Rose 4 Points in December according to the National Association of Homebuilders. It’s the first positive data point for housing in ages. Could this be the beginning of the big turn?

Mortgage Rates Plunge to 6.04% for the 30-year fixed, sparking a 28% gain week to week. A massive rally in the bond market is the big incentive, taking ten-year Treasury bonds to 6.37%, a new five month low. Inventory remains low. Mortgage rates could easily shed another 100 basis points by summer just on falling to the traditional premium over Treasuries, which is why housing stocks like (LEN), PHM), and (KBH) have been on fire.

Business Inventories up 0.4%, right in line with expectations. Retail Sales are falling, as is Consumer Spending. Department store sales were down 6.5%, once unimaginable to see during the Christmas season.

Netflix Blows it Away with 6.7 million new subscribers., taking the stock up 7%, and 125% from the May low. It’s proof that the FANG’s are not dead yet and that the predicted Q4 earnings shortfall may be overstated. CEO Reed Hastings semi-retires. Don’t touch (NFLX) as this train has left the station. There are better fish to fry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 23 nothing of note is announced. Baker Hughes (BKR) reports earnings from the oil patch.

On Tuesday, January 24 at 8:45 AM EST, the S&P Global PMIs for December is out. Johnson & Johnson (JNJ) and Microsoft (MSFT) report earnings.

On Wednesday, January 25 at 7:30 AM, the Crude Oil Stocks are announced. Tesla (TSLA) and Boeing (BA) report earnings.

On Thursday, January 26 at 8:30 AM, the Weekly Jobless Claims are announced. Retail Sales for November are printed. We also get US Q4 GDP. Visa (V) and Intel (INTC) report earnings.

On Friday, January 27 at 5:30 AM, the Personal Income & Spending for December is disclosed. American Express (AXP) and Chevron (CVX) report earnings. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I didn’t know what to expect when I landed on the remote South Pacific Island of Yap in 1979, one of the Caroline Islands, but I was more than pleasantly surprised.

Barely out of the Stone Age, Yap lies some 3,000 miles west of Hawaii. It was famed for the ancient lichen covered stone money that dotted the island which had no actual intrinsic value.

The value was in the effort that went into transporting them. With some cylindrical pieces larger than cars, geologists later discovered that they had been transported some 280 miles by outrigger canoe from the point of origin sometime in the distant past. Since Yap had no written language, there are no records about them, only folktales.

I often use the stone money of Yap as an example of the arbitrariness of fiat money. Who’s to say which is more valuable; a 500-pound piece of rock or a freshly printed $100 Benjamin from the US Treasury?

You decide.

The natives were a gentle and friendly people. They wore grass skirts purely for the benefit of Western visitors. They preferred to walk around as nature made them.

There was no hotel on the island at the time, so I was invited to stay with a local chief (picture below).

One of my hosts asked if I was interested in seeing a Japanese zero fighter. Yap wasn’t invaded by the US during WWII because it was bypassed by MacArthur on his way to the Philippines. The Japanese troops were repatriated after their war, but most of their equipment was left behind. It was still there.

So it was with some anticipation that I was led to a former Japanese airfield that had been abandoned for 35 years. There, still in perfect formation, was a squadron of zeroes. The jungle had reclaimed the field and several planes had trees growing up through their wings.

The natives had long ago stripped them of anything of value, the machine guns, nameplates, and Japanese language instruments. But the airframes were still there exposed to the elements and too fragile to move.

During my stay, I came across an American Peace Corp volunteer desperate for contact with home. A Jewish woman in her thirties, she had been sent there from New York City to teach English and seemed to have been forgotten by the agency.

I volunteered for the Peace Corps. myself out of college, but it turned out they had no need of biochemists in Fiji, so I was interested in learning about her experience. She confided in me that she had tried wearing a grass skirt to blend in but got ants on the second day. We ended up spending a lot of time together and I got a first-class tour of the island.

Suffice it to say that she was thrilled to run into a red-blooded American male. I wish I had taken a picture of her, but the nearest color film processing was back in Honolulu, and I had to be judicious in my use of film.

The highlight of the trip was a tribal stick dance put on in my honor around an evening bonfire among much yelping and whooping. It was actually a war dance performed with real war clubs and their furiousness was impressive.

I had the fleeting thought that I might be on the menu. Cannibalism had been practiced here earlier in the century. During the war when starvation was rampant, several of the least popular Japanese soldiers went missing, their bodies never found. When men come screaming at you with a club in the night, your imagination runs wild.

Alas, I could only spend a week on this idyllic island. I was on a tight schedule courtesy of Air Micronesia, and deadlines beckoned. Besides, there was only one plane a week off the island.

It was on to the next adventure.

A Few New Friends

Large Denomination Stone Money

My Accommodation

A Neglected Japanese Zero

China

Japan

US

Global Market Comments

January 17, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOING AGAINST THE CONSENSUS),

(TLT), (MUB), (JNK), (HYG), (GLD), (SLV), (GOLD), (WPM), (FCX), (BHP), (EEM), (MS), (GS), (JPM), (BAC), (C), (BRK/B), (SPY), (QQQ), (IWM), (VIX)

Going against the market consensus has been working pretty well lately.

When the world prayed for a Santa Claus rally, I piled on the shorts. When traders expected a New Year January crash, I filled my boots with longs.

That’s how you earn an eye-popping 19.83% profit in a mere nine trading says, or 2.20% a day.

The other day, someone asked me how it is possible to get mind-blowing results like these. It’s very simple. Get insanely aggressive when everyone else is terrified, which I did on January 3. I also knew that with the Volatility Index (VIX) falling to $18, pickings would quickly get extremely thin. It was make money now, or never.

To quote my favorite market strategist, Yankees manager Yogi Berra, “No one goes to that restaurant anymore because it’s too crowded.”

My performance in January has so far tacked on a welcome +19.83%. Therefore, my 2023 year-to-date performance is also +19.83%, a spectacular new high. The S&P 500 (SPY) is up +3.78% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +103.30%.

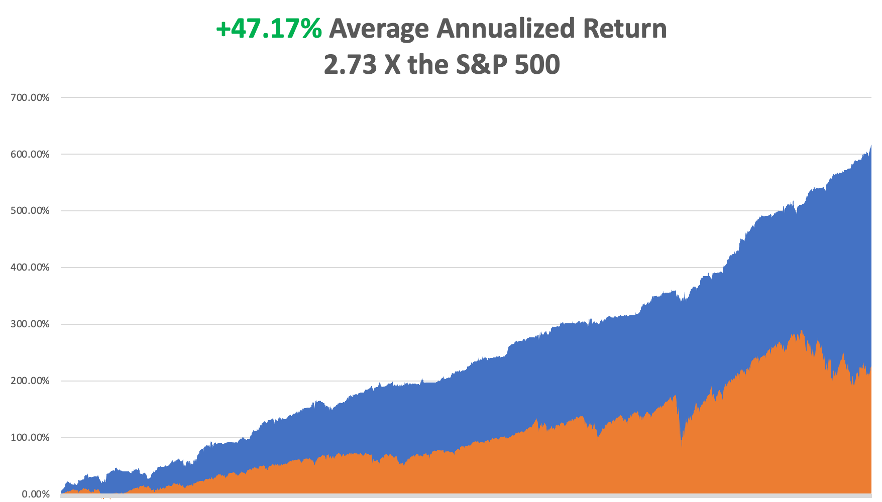

That brings my 15-year total return to +617.03%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.17%, easily the highest in the industry.

I took profits in my February bonds last week (TLT), taking advantage of a $5 pop in the market. All my remaining positions are profitable, including longs in (GOLD), (WPM), (TSLA), (BRK/B), and (TLT), with 30% in cash for a 10% net long position.

Since my New Year forecasts have worked out so well, I will repeat the high points just in case you were out playing golf or bailing out from a flood when they were published.

Buy Falling Interest Rate Plays, as I expect the yield on the ten-year US Treasury yield to fall from 3.50% to 2.50% by yearend. That means Hoovering up any kind of bond, like (TLT), (MUB), (JNK), and (HYG). Falling interest rates also shine a great spotlight on precious metals like (GLD), (SLV), (GOLD), and (WPM).

The US Dollar Will Continue to Fall. Commodities love this scenario, including (FCX), (BHP), and emerging markets (EEM).

Inflation Will Decline All Year and should go below 4% by the end of 2023. In fact, we have had real deflation for the past six months. Financials do well here, like (MS), (GS), (JPM), (BAC), (C), and (BRK/B).

Which creates another headache for you, if not an opportunity. We may have a situation where the main indexes, (SPY), (QQQ), and (IWM) go nowhere, while individual stocks and sectors skyrocket. That creates a chance to outperform benchmarks…and everyone else.

There has been a lot of discussion among traders lately about the collapse of the Volatility Index ($VIX) to $18, a two-year low and what it means.

They are distressed because a ($VIX) this low greatly shrinks the availability of low risk/high return trading opportunities. A ($VIX) this low is basically shouting at you to “STAY AWAY!”

Does it mean that an explosion of volatility is following? Or are markets going to be exceptionally boring for the next six months?

Beats me. I’ll wait for the market to tell me, as I always do.

Current Positions

Risk On

(TSLA) 1/$75-$80 call spread 10.00%

(GOLD) 1/$15.50-$16.50 call spread. 10.00%

(WPM) 1/$$36-$39 call spread. 10.00%

(BRKB) 1/$290-$300 call spread 10.00%

Risk Off

(TLT) 1/$96-$99 call spread - 10.00%

(TLT) 1/$95-$98 call spread -20.00%

Total Net Position 10.00%

Total Aggregate Position 70.00%

Consumer Price Index Falls 0.1% in December, continuing a trend that started in June. Stocks popped and bonds rallied. YOY inflation has fallen to 6.5%. “RISK ON” continues. Now we have to wait another month to get a new inflation number. The economy has now seen de facto deflation for six months. Gas prices led the decline, now 9.4%. We might get away with only a 0.25% interest rate hike at the February 1 Fed meeting.

Bond Default Risk Rises, as well as a government shutdown, as radicals gain control of the House. This is the group that lost the most seats in the November election. Bonds are the only asset class not performing today, and paper with summer maturities is trading at deep discounts. It certainly casts a shadow over my 50% long bond position. However, I don’t expect it to last more than a month and my longest bond maturity is in February.

The US Consumer is in Good Shape, according to JP Morgan’s Jamie Diamond. Spending is now 10% greater than pre covid, and balance sheets are healthy. No sign of an impending deep recession here.

Boeing Deliveries Soar from 340 to 480 in 2022, and 479 new orders. A sudden aircraft shortage couldn’t have happened to a nicer bunch of people. The 737 MAX has shaken off all its design problems after two crashes four years ago. Cost-cutting here can be fatal. Europe’s Airbus is still tops, with 663 deliveries last year. Don’t chase the stock up here, up 79% from the October lows, but buy (BA) on dips.

Small Business Optimism Hits Six-Month Low to from 91.9 to 89.8, adding to the onslaught of negative sentiment indicators, so says the National Federation of Independent Business (NFIB).

Copper Prices Set to Soar Further with the post-Covid reopening of China, according to research firm Alliance Bernstein. After a three-year shutdown, there is massive pent-up demand. Copper prices are at seven-month highs. Keep buying (FCX) on dips.

Australian Metals Exports Soar, as the new supercycle in commodities gains steam. Shipments topped $9 billion in November, 20% higher than the most optimistic forecasts. Keep buying copper (FCX), aluminium (AA), iron ore (BHP), gold (GLD) and silver (SLV) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 16, markets are closed for Martin Luther King Day.

On Tuesday, January 17 at 8:30 AM EST, the New York Empire State Manufacturing Index is out

On Wednesday, January 18 at 11:00 AM, the Producer Price Index is announced, giving us another inflation read.

On Thursday, January 19 at 8:30 AM, the Weekly Jobless Claims are announced. US Housing Starts and Building Permits are printed.

On Friday, January 20 at 7:00 AM, the Existing Home Sales are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, the University of Southern California has a student jobs board that is positively legendary. It is where the actor John Wayne picked up a gig working as a stagehand for John Ford which eventually made him a movie star.

As a beneficiary of a federal work/study program in 1970, I was entitled to pick any job I wanted for the princely sum of $1.00 an hour, then the minimum wage. I noticed that the Biology Department was looking for a lab assistant to identify and sort Arctic plankton.

I thought, “What the heck is Arctic plankton?” I decided to apply to find out.

I was hired by a Japanese woman professor whose name I long ago forgot. She had figured out that Russians were far ahead of the US in Arctic plankton research, thus creating a “plankton gap.” “Gaps” were a big deal during the Cold War, so that made her a layup to obtain a generous grant from the Defense Department to close the “plankton gap.”

It turns out that I was the only one who applied for the job, as postwar anti-Japanese sentiment then was still high on the West Coast. I was given my own lab bench and a microscope and told to get to work.

It turns out that there is a vast ecosystem of plankton under 20 feet of ice in the Arctic consisting of thousands of animal and plant varieties. The whole system is powered by sunlight that filters through the ice. The thinner the ice, such as at the edge of the Arctic ice sheet, the more plankton. In no time, I became adept at identifying copepods, euphasia, and calanus hyperboreaus, which all feed on diatoms.

We discovered that there was enough plankton in the Arctic to feed the entire human race if a food shortage ever arose, then a major concern. There was plenty of plant material and protein there. Just add a little flavoring and you had an endless food supply.

The high point of the job came when my professor traveled to the North Pole, the first woman ever to do so. She was a guest of the US Navy, which was overseeing the collection hole in the ice. We were thinking the hole might be a foot wide. When she got there, she discovered it was in fact 50 feet wide. I thought this might be to keep it from freezing over but thought nothing of it.

My freshman year passed. The following year, the USC jobs board delivered up a far more interesting job, picking up dead bodies for the Los Angeles Counter Coroner, Thomas Noguchi, the “Coroner to the Stars.” This was not long after Charles Manson was locked up, and his bodies were everywhere. The pay was better too, and I got to know the LA freeway system like the back of my hand.

It wasn’t until years later when I had obtained a high-security clearance from the Defense Department that I learned of the true military interest in plankton by both the US and the Soviet Union.

It turns out that the hole was not really for collecting plankton. Plankton was just the cover. It was there so a US submarine could surface, fire nuclear missiles at the Soviet Union, then submarine again under the protection of the ice.

So, not only have you been reading the work of a stock market wizard these many years, you have also been in touch with one of the world’s leading experts on Artic plankton.

Live and learn.

CLICK HERE to download today's position sheet.

1981 On Peleliu Island in the South Pacific

Global Market Comments

January 13, 2023

Fiat Lux

Featured Trade:

(JANUARY 11 BIWEEKLY STRATEGY WEBINAR Q&A)

(ROM), (FCX), (QQQ), (VIX), (TSLA), (TLT), (MSFT), (RIVN), (VIX), (BRK/B), (RTX), (LMT), (FXI), (UNG), (GLD), (GDX), (SLV), (WPM)

Below please find the subscribers’ Q&A for the January 11 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: In your trade alert you expected that the (TLT) might go up as much as 30% this year. But in your latest newsletter, you mentioned that the chaos in the US House of Representatives would greatly raise the risk of a default on US government debt by the summer and certainly cast a shadow over your 50% long bond position. Is it still a good idea to hold on to the (TLT) ETF over the next 2-6 months?

A: It is. The extremists who now control the House are not interested in governing or passing laws but gaining clicks, raising money, and increasing speaker’s fees. It may have converted (TLT) from a straight-up trade to a flat-line trade. We will still make the maximum profit on call spreads and LEAPS but with greater risk. But even chaos in the House can’t head off a recession, which the bond market seems intent on pricing in by going up. However, if you depend on government payments for any reason, be it Social Security, a government salary, a tax refund, or a payment for a contract, expect delays. The housing market also ceases because closings can’t take place during government shutdowns. Also, 30% of my bond longs expire in four trading days, and the remainder on February 17.

Q: Is it wise to sell the 2X ProShares Ultra Technology ETF (ROM) now or keep holding?

A: I think the (ROM), NASDAQ, and technology stocks in general may make several runs at the lows over the next six months but won’t fall much from here. A recession is priced in. Once we get through this, you’re looking at doubles and triples for the best names. So, the risk/reward overwhelmingly favors holding on to a one-year view.

Q: would you buy Tesla (TSLA) here?

A: I would start scaling in. The bad news is about to dry up, like Twitter, the recession, the pandemic in China, and Elon Musk selling shares. Then we face an onslaught of good news, like the new Mexico factory announcement, the Cybertruck launch, solid state batteries, and annual production hitting 2 million. At this level, the shares are priced in multiple worst-case scenarios. It is selling at 10X 2025 earnings, half the market multiple. At the end of the day, Tesla has an unassailable 14-year start over the rest of the industry and is the only company in the world that makes money on EVs. There’s an easy 10X here on two-year LEAPS.

Q: I’m in the Freeport McMoRan (FCX) January 25 2-year LEAP approaching the upper end of the 42/45 range. If it crosses 45, do we close the position?

A: Sell half, take your profit. If you’re in the LEAP, my guess is you probably have a 500% profit here in only 3 months, which is not bad. And then you keep the remaining half because you’re then playing with the house's money, and Freeport has a shot of going all the way to $100 a share by the 2025 expiration, and that will get you your full 1,000% return on the position. It’s always nice to be in a position where it’s impossible to lose money on a trade, and that certainly is where you are now with your (FCX) LEAP and everybody else in the FCX LEAP in October also.

Q: As a member of the Florida Retirement System, I’m curious how Blackrock (BLK) and other firms are dealing with the Santos’ plan for their portfolios.

A: Having a state governor manage your portfolio and make your sector and stock picks is an absolutely terrible idea. I can’t imagine a worse possible outcome for your retirement funds. Florida is not the only state doing this—Louisiana and Texas are doing it too. The goal is to drive money out of alternative energy and back into the oil industry, and obviously, this is being financed by the oil industry, which is pissed off over their low multiples. Suffice it to say it’s not a good idea to move out of one of the fastest-growing industries in the market and move into an industry that’s going to zero in 10 years. If that’s their investment strategy, I wish they’d stick to politics and leave investing for true professionals to do.

Q: What do you think about cannabis stocks?

A: I’m a better user of the product than the stock. How about that? How hard is it to grow weed? At the end of the day, these are just pure marketing companies, and that value added is low. Plus, they have huge competition from the black market still selling ½ to ⅓ below market prices because they’re tax-free; the local taxes on these cannabis sales are enormous.

Q: Would you recommend selling a bear market rally when the S&P goes to 405?

A: The (QQQ) would be the better short, something like the $310-320 vertical bear put spread for February to bring in some free money. That’s what I'm planning to do if we get up that high, which we may not.

Q: How do you take advantage of a low CBOE Volatility Index (VIX)?

A: You don’t; there’s nothing to do here with the (VIX) at $22. My trades this year were not volatility trades—because we did them with low volatility, they were pure directional trades betting that the longs would go up and the shorts would go down and they all worked.

Q: Will Rivian (RIVN) survive?

A: Yes, they have two years of cash flow in the bank, and they’re boosting production. However, a high-growth, non-earning stock like Rivian is just out of favor right now. Will they come back into favor? Yes, probably in a year or so, but in the meantime, people are much happier buying Microsoft (MSFT) at a discount than Rivian.

Q: Do you ever buy butterfly spreads?

A: No, four-legged trades run up a lot of commissions, are hard to execute because you have 4 spreads, and have lower returns. They are also lower risk and for people who have no idea what the market is going to do. I don’t need the lower risk trades because I know what markets are going to do.

Q: Do you suggest any Microsoft (MSFT) LEAPS?

A: Yes, go out two years with LEAPS and go out about 50% on your strike prices. A 50% move here in Microsoft in two years is a complete no-brainer.

Q: With weakness in retail, rising inventories, and high consumer debt, will consumers dip into savings?

A: Yes they will, but that will predominantly happen at the bottom half of the economy—the part of the economy that has minimal to no savings. The upper half seems to be doing well—the middle class and of course, the wealthy— and are not cutting back their spending at all, which is why this seems to be a recession that may not actually show up. So, what can I say? The rich are doing great and everyone else is doing less than great, and stocks are reflecting that. Nothing new here.

Q: Would you hold off on tech LEAPS for a bigger selloff, or closer to April?

A: If we do get another big selloff and challenge the October lows, I’ll be pumping out those LEAPS as fast as I can write them; except then, a two-year LEAPS will have an April of 2025 expiration.

Q: I just signed up. What are the advantages of LEAPS?

A: A possible 10x return in 2 years with very low risk. I would suggest going to my website, logging in, and doing a search for LEAPS. There will be a piece there on how to execute a LEAPS, and the Concierge members can also find that piece by logging into their website.

Q: Best and worst sectors?

A: First half, already mentioned them. We like commodities, healthcare, financials, and Berkshire Hathaway (BRK/B) in the first half and tech in the second half.

Q: Have we reached a low in cryptocurrencies?

A: Probably not, and I’ll tell you why I’ve given up on cryptos: I may not live long enough to see the bottom in crypto. It has Tokyo written all over it, and it took Tokyo 30 years to resume a bull market after it crashed in 1990. We’re still at the scandal stage where it turns out that the majority of these trading platforms were stealing money from customers. This is not a great inspiration for investing in that sector. When you have the best quality growth stocks down 80-90%; why bother with something that may not exist or may never recover in your lifetime? I’m out of the crypto business, but there are a wealth of crypto research sources still online and I’m sure they’d be more than happy to give you an opinion.

Q: Why have defense stocks like Raytheon (RTX) and Lockheed Martin (LMT) been weak recently?

A: A couple of reasons. #1 Just outright profit taking into the end of the year in one of the best-performing sectors. #2 The end of the war in Ukraine may not be that far off, and if that happens that could trigger a major round of selling in defense. We did get the three-day ceasefire over the Russian Orthodox New Year, that’s a possible hint, so that may be another reason.

Q: Political outlook on 2024?

A: It’s too early to make any calls, anything could happen; but if we get a repeat of the November election outcome, you could have Democrats retake control of both houses of congress—that’s where the betting money is going right now.

Q: Would you bottom fish in the United States Natural Gas Fund (UNG)?

A: No, I would not—I am avoiding energy like the plague. Remember the all-time low for natural gas is $0.95 per MM BTU, so we still could have a long way to go.

Q: Would you buy iShares China Large-Cap ETF (FXI) on a post-COVID breakout?

A: It looks like it’s already moved, so maybe kind of late on that. The problem is that in China, you don’t know what you are buying and the locals have a huge advantage in reading Beijing.

Q: What do you think about the Biden administration wanting to ban gas stoves?

A: That’s actually not a federal issue, it’s a state issue. California has already banned gas pipes for all new construction. It looks like New York will follow and that’s one-third of the US population. The goal is to replace them with electrical appliances which emit no carbon. I have a non-carbon house myself, I went down that path about 10 years ago, and it seems to be the only way to reduce carbon emissions—is to either price gasoline or oil out of the market, or to make it illegal, and they’re already making gasoline cars illegal, so gas and oil won’t be far behind. From 1900, we went from a hay powered economy to a gasoline-powered one in only 20 years so it should be doable.

Q: How can the push for all electric work well when we have so many shutdowns, much higher electricity cost, and cannot keep up with the demand already here?

A: Buy lots of copper for new local electric powerlines at the house level and buy lots of aluminum for the long-distance transmission lines. Global demand for both aluminum and copper has to triple to accommodate the grid buildout that is already planned. As far as hurricanes in Florida, there’s nothing you can do to stop those on a hundred-year view; I would move to higher ground, which is hard to do in Florida as the highest point in the state is only 345 feet and that’s a garbage dump.

Q: Can I get a copy of all these slides?

A: Yes, we post the PowerPoint on the website at www.madhedgefundtrader.com usually two hours after the production.

Q: Are you recommending buying precious metals right now (GLD), (GDX), (SLV), (and WPM) even after the upside breakout?

A: On upside breakouts, you buy the dips. A perfect dip would be a retest of the 200-day moving average. But we may not get that, since it seems to be everyone’s number-one choice right now. By the way, I haven’t been telling people to buy gold and LEAPS on all the gold plays since October—that’s where the big move has already been made.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

CLICK HERE to download today's position sheet.

With the Israeli Army in Jerusalem in 1979

Global Market Comments

January 4, 2023

Fiat Lux

2023 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (BAC), (C), (MS), (GS),

(X), (CAT), (DE),(TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD), (FXE), (EUO),

(FXC), (FXA), (YCS), (FXY), (CYB), (DIG), (RIG), (USO), (DUG), (UNG), (USO),

(XLE), (AMLP),(GLD), (DGP), (SLV), (PPTL), (PALL), (ITB), (LEN), (KBH), (PHM)

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 14 Pro Max.

Here is the bottom line which I have been warning you about for months. In 2023, we will probably top the 84.63% we made last year, but you are going to have to navigate the reefs, shoals, and hurricanes. Do it and you can laugh all the way to the bank. I will be there to assist you to navigate every step.

The first half of 2023 will be all about trading. After that, I expect markets to go straight up.

And here is my fundamental thesis for 2023. After the Fed kept rates too low for too long, then raised them too much, it will then panic and lower them again too fast to avoid a recession. In other words, a mistake-prone Jay Powell will keep making mistakes. That sounds like a good bet to me.

Let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2023

1) When will the Fed pivot?

2) How much of a toll will the quantitative tightening take?

3) How soon will the Russians give up on Ukraine?

4) When will buyers return to technology stocks from value plays?

5) Will gold replace crypto as the new flight to safety investment?

6) When will the structural commodities boom get a second wind?

7) How fast will the US dollar fall?

8) How quickly will real estate recover?

9) How fast can the Chinese economy bounce back from Covid-19?

10) How far will oil prices keep falling?

The Thumbnail Portfolio

Equities – buy dips

Bonds – sell buy dips

Foreign Currencies – buy dips

Commodities – buy dips

Precious Metals – buy dips

Energy – stand aside

Real Estate – buy dips

1) The Economy – Bouncing Along the Bottom

Whether we get a recession or not, you can count on markets fully discounting one, which it is currently doing with reckless abandon.

Anywhere you look, the data is dire, save for employment, which may be the last shoe to fall. Technology companies seem to be leading us in the right direction with never-ending mass layoffs. Even after relentless cost-cutting though, there are still 1.5 tech job offers per applicant, which is down from last year’s three.

The Fed is currently predicting a weak 0.5% GDP growth rate for 2023, the same feeble rate we saw for 2022. What we might get is two-quarters of negative growth in the first half followed by a sharp snapback in the second half.

Whatever we get, it will be one of the mildest recessions or growth recessions in American economic history. There is no hint of a 2008-style crash. The banking system was shored up too well back then to prevent that. Thank Dodd/Frank.

So far, so good.

2) Equities (SPX), (QQQ), (IWM) (AAPL), (XLF), (BAC) (JPM), (BAC), (C), (MS), (GS), (X), (CAT), (DE)

Since my job is to make your life incredibly easy, I am going to narrow my equity strategy for 2023.

It's all about falling interest rates.

When interest rates are high, as they are now, you only look at trades and investments that can benefit from falling interest rates.

In the first half, that will be value plays like banks, (JPM), (BAC), (C), financials (MS), (GS), homebuilders (KBH), (LEN), (PHM), industrials (X), capital goods (CAT), (DE).

As we come out of any recession in the second half, growth plays will rush to the fore. Big tech will regain leadership and take the group to new all-time highs. That means the volatility and chop we will certainly see in the first half will present a generational opportunity to get into the fastest-growing sectors of the US economy at bargain prices. I’m talking Cadillacs at KIA prices.

A category of its own, Biotech & Healthcare should do well on their own. Not only are they classic defensive plays to hold during a recession, technology and breakthrough new discoveries are hyper-accelerating. My top three picks there are Eli Lily (ELI), Abbvie (ABBV), and Merck (MRK).

Block out time on your calendars because whenever the Volatility Index (VIX) tops $30, I am going pedal to the metal, and full firewall forward (a pilot term), and your inboxes will be flooded with new trade alerts.

There is another equity subclass that we haven’t visited in about a decade, and that would be emerging markets (EEM). After ten years of punishment by a strong dollar, (EEM) has also been forgotten as an investment allocation. We are now in a position where the (EEM) is likely to outperform US markets in 2023, and perhaps for the rest of the decade.

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD)

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a new business. This time, bonds face the gale force headwinds of three promised interest rate hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

A Visit to the 19th Century

4) Foreign Currencies (FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

With a major yield advantage over the rest of the world, the US dollar has been on an absolute tear for the past decade. After all, we have the world’s strongest economy.

That is about to end.

If your primary assumption is that US interest rates will see a sharp decline sometime in 2023, then the outlook for the greenback is terrible.

Currencies are driven by interest rate differentials and the buck is soon going to see the fastest shrinking yield premium in the forex markets.

That shines a great bright light on the foreign currency ETFs. You could do well buying the Australian Dollar (FXA), Euro (FXE), Japanese yen (FXE), and British Pound (FXB). I’d pass on the Chinese yuan (CYB) right now until their Covid shutdowns end.

5) Commodities (FCX), (VALE), (DBA)

Commodities are the high beta play in the financial markets. That’s because the cost of being wrong is so much higher. Get on the losing side of commodities and you will be bled dry by storage costs, interest expenses, contangos, and zero demand.

Commodities have one great attribute. They predict recessions earlier than any other asset class. When they peaked in March of 2022, they were screaming loud and clear that a recession would hit in early 2023. By reversing on a dime on October 14, they also told us that the recovery would begin in July of 2023.

You saw this in every important play in the sector, including Broken Hill (BHP), Peabody Energy (BTU), Freeport McMoRan (TCX), and Alcoa Aluminum (AA). Excuse me for using all the old names.

The heady days of the 2011 commodity bubble top are about to replay. Now that this sector is convinced of a substantially weaker US dollar and lower inflation, it is once more a favorite target of traders.

China will still demand prodigious amounts of imported commodities once its pandemic shutdown ends, but not as much as in the past. Much of the country has seen its infrastructure built out, and it is turning from a heavy industrial to a service-based economy, much like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase three-fold in a decade to accommodate this increase, no easy task, or prices will have to rise.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate all commodities on dips.

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (XLE), (AMLP)

Energy was the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero sooner than you think. However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are bailing on their own industry. Instead of reinvesting profits back into their future exploration and development, as they have for the last century, they are paying out more in dividends and share buybacks.

Take the money and run.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and share prices for the energy industry.

Energy now counts for only 5% of the S&P 500. Twenty years ago, it boasted a 15% weighting.

The gradual shutdown of the industry makes the supply/demand situation infinitely more volatile.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

And guess who the world’s best oil trader was in 2022? That would be the US government, which drew 400 million barrels from the Strategic Petroleum Reserve in Texas and Louisiana at an average price of $90 and now has the option to buy it back at $70, booking a $4 billion paper profit.

The possibility of a huge government bid at $70 will support oil prices for at least early 2023. Whether the Feds execute or not is another question. I’m advising them to hold off until we hit zero again to earn another $18 billion. Why we even have an SPR is beyond me, since America has been a large net energy producer for many years now. Do you think it has something to do with politics?

To understand better how oil might behave in 2023, I’ll be studying US hay consumption from 1900-1920. That was when the horse population fell from 100 million to 6 million, all replaced by gasoline-powered cars and trucks. The internal combustion engine is about to suffer the same fate.

7) Precious Metals (GLD), (DGP), (SLV), (PPTL), (PALL)

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2022 was a terrible year for precious metals until we got the all-asset class reversal in October. With inflation soaring, stocks volatile, and interest rates soaring, gold had every reason to fall. Instead, it ended up unchanged on the year, thanks to a 15% rally in the last two months.

Bitcoin stole gold’s thunder until a year ago, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand were just not enough to keep gold afloat. That is over now for good and that is why gold is regaining its luster.

Chart formations are starting to look very encouraging with a massive head-and-shoulders bottom in place. So, buy gold on dips if you have a stick of courage on you, which I hope you do.

Higher beta silver (SLV) will be the better bet as it already has been because it plays a major role in the decarbonization of America. There isn’t a solar panel or electric vehicle out there without some silver in them and the growth numbers are positively exponential. Keep buying (SLV), (SLH), and (WPM) on dips.

8) Real Estate (ITB), (LEN), (KBH), (PHM)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Those in the grip of a real estate recession take solace. We are in the process of unwinding 2022’s excesses, but no more. There is no doubt a long-term bull market in real estate will continue for another decade, once a two year break is completed.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s. You don’t have a real estate crash when we are short 10 million homes.

The reasons, of course, are demographic. There are only three numbers you need to know in the housing market for the next ten years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The boomers (between ages 58 and 76) have been unloading dwellings to the Gen Xers (between ages 46 and 57) since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis. That has created a massive shortage of housing, both for ownership and rentals.

There is a happy ending to this story.

Millennials now aged 26-41 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes. They are also just entering the peak spending years of middle age, which is great for everyone.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to the pandemic and Zoom, many are never returning to the cities. That has prompted massive numbers to move from the coasts to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should continue to rise during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are considered. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 16 years. The 50% of small home builders that went under during the Financial Crisis never came back.

We are still operating at only a half of the 2007 peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

There is a new factor at work. We are all now prisoners of the 2.75% 30-year fixed rate mortgages we all obtained over the past five years. If we sell and try to move, a new mortgage will cost double today. If you borrow at a 2.75% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free. That’s why nobody is selling, and prices have barely fallen.

This winds down towards the end of 2023 as the Fed realizes its many errors and sharply lowers interest rates. Home prices will explode…. again.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now after you throw in all the tax breaks. It’s also a great inflation play.

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

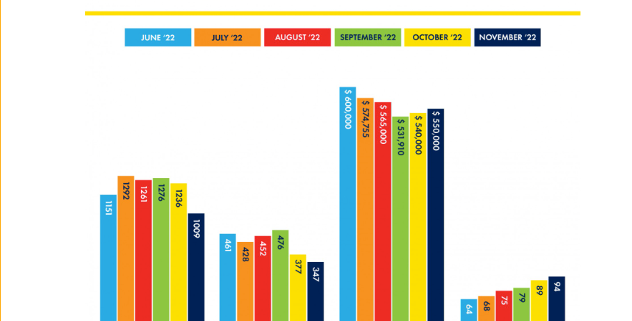

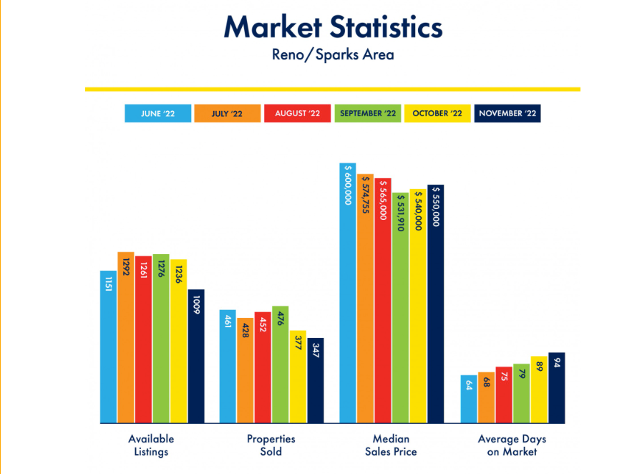

Recent Reno Real Estate Statistics

9) Postscript

We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff has made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2023!

John Thomas

The Mad Hedge Fund Trader

Global Market Comments

December 12, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HOW MARKETS WORK),

(SPY), (TLT), (TSLA), (GLD), (XOM), (OXY), (FXI), (JPM)

Last week, I spoke about the “smart” market and the “dumb” market.

Looking across asset class behavior over the last couple of years, it’s become evident, there is another major driver.

Liquidity.

Hedge fund legend George Soros was an early investor in my hedge fund because he was looking for a pure Japan play. But I learned a lot more from him than he from me.

No shocker here: it’s all about the money.

Follow the flow of funds and you will always know where to invest. If you see a sustainable flow of money into equities, you want to own stocks. The same is true with bonds.

There is a corollary to this truism.

The simpler an idea, the more people will buy it. One can think of many one or two-word easy-to-understand investment themes that eventually led to bubbles: the Nifty Fifty, the Dotcom Boom, Fintech, Crypto Currencies, and oil companies.

Spot the new trend, get in early, and you make a fortune (like me and Soros). Join in the middle, and you do OK. Join the party at the end and it always ends in tears, as those who joined crypto a year ago learned at great expense.

If I could pass on a third Soros lesson to you, it would be this. Anything worth doing is worth doing big. This is why you have seen me frequently with a triple position in the bond market, or the double short I put on with oil companies two weeks ago, clearly just ahead of a meltdown.

Which brings me back to liquidity.

There are only two kinds of markets: liquidity in and liquidity out. Liquidity was obviously pouring into markets from 2009. This is why everything went up, including both stocks and bonds. That liquidity ended on January 4, 2022. Since then, liquidity has been pouring out at a torrential rate and everything has been going down.

So, what happened on October 14, 2022?

The hot money, hedge funds, and you and I started betting that a new liquidity in cycle will begin in 2023 and continue for five, or even ten years. This is why we have made so much money in the past two months.

Notice that liquidity out cycles are very short when compared with liquidity in cycles, one to two years versus five to ten years. That’s because populations expand creating more customers, technology advances creating more products and services, and economies get bigger.

When I first started investing in stocks, the U.S. population was only 189 million, the GDP was $637 billion, and if you wanted a computer, you had to buy an IBM 7090 for $3 million. Notice the difference with these figures today: $25 trillion for GDP, a population of 335 million, and $99 for a low-end Acer laptop, which has exponentially more computer power than the old IBM 7090.

What did the stock market do during this time? The Dow Average rocketed by 54 times, or 5,400%. And you wonder why I am so long term bullish on stocks. The people who are arguing that we will have a decade of stock market returns are out of their minds.

Which reminds me of an anecdote from my Morgan Stanley days, in my ancient, almost primordial past. In September 1982, I met with the Head of Investments at JP Morgan Bank (JPM), Mr. Carl Van Horn. I went there to convince him that we were on the eve of a major long term bull market and that he should be buying stocks, preferably from Morgan Stanley.

Every few minutes he said, “Excuse me” and left the room to return shortly. Years later, he confided in me that whenever he left, he placed an order to buy $100 million worth of stock for the bank’s many funds every time I made a point. That very day proved to be the end of a decade-long bear market and the beginning of an 18-year bull market that delivered a 20-fold increase in share prices.

But there is a simpler explanation. Liquidity in markets are a heck of a lot more fun than liquidity out ones, where your primary challenge is how to spend your newfound wealth.

I vote for the simpler explanation.

Yes, this is how markets work.

My performance in December has so far tacked on another robust +4.85%. My 2022 year-to-date performance ballooned to +88.53%, a spectacular new high. The S&P 500 (SPY) is down -17.0% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +92.92%.

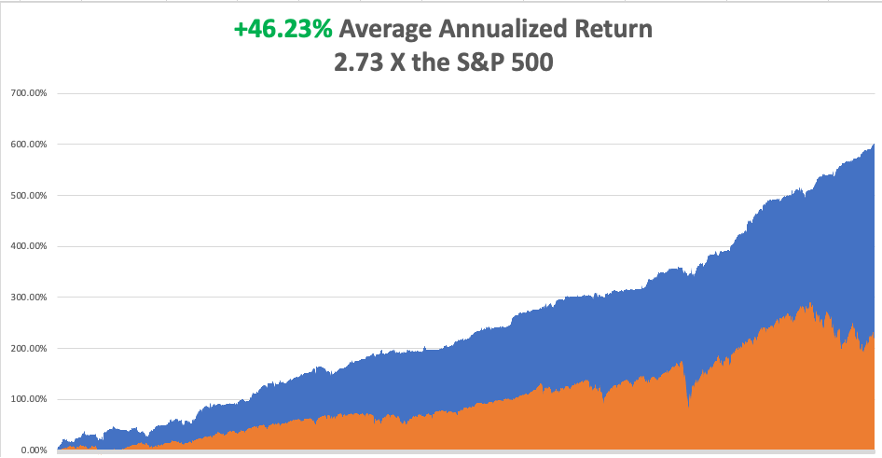

That brings my 14-year total return to +601.09%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.23%, easily the highest in the industry.

I took profits in my oil shorts in (XOM), (OXY), (SPY), and (TSLA). I am keeping one long in (TSLA), with 90% cash for a 10% long position.

Producer Prices Come in High, up 0.3% in November, driven by rising prices for services. It sets up an exciting CPI for Tuesday morning.

Emerging Markets Saw Massive Inflows in November, some $37.4 billion, the most since June 2021. Chinese technology stocks were two big beneficiaries, down 80%-90% from their highs. This could be one of the big 2023 performers if the US dollar and interest rates continue to fall. Buy (EEM) on dips.

Oil is in Free Fall, with 57 fully loaded Russian tankers about to hit the market. Nobody wants it ahead of a recession. All mad hedge short plays in energy are coming home. When will the US start refilling the Strategic Petroleum Reserve?

Turkey Blocks Russian Oil at the Straights of Bosporus, checking insurance papers, which are often turning out to be bogus. Insurance Russian tankers are now illegal in western countries. Many of these tankers are ancient, recently diverted from the scrapyard and in desperate need of liability insurance. Oil spills are expensive to clean up. Just ask any Californian.

Tesla Cuts Production in China, some 20% at its Shanghai Gigafactory for its Model Y SUV, or so the rumor goes. The short sellers are back! These are the kind of rumors you always hear at market bottoms.

US Unemployment to Peak at 5.5% in Q3 of 2023, according to a survey from the University of Chicago Business School. A tiny handful expects a higher 7.0% rate. Some 85% of economists polled expect a recession next year. After that, the Fed will take interest rates down dramatically to bring unemployment back down. No room for a soft landing here.

Home Mortgage Demand Plunges in another indicator of a sick housing market, which is 20% of the US economy. New applications are down a stunning 86% YOY despite a dive in the 30-year rate to 6.41%, but nobody is selling. Refis are now nonexistent.

Gold Continues on a Tear, hitting new multi-month highs. With interest rates certain to plummet in 2023 as the Fed reacts to a recession, Gold could be one of the big trades for next year. Buy (GLD), (GDX), and (GOLD) on dips.

Services PMI Hits New Low for 2022 at a recessionary 46.2. Nothing but ashes in this Christmas stocking. It didn’t help bonds, which sold off two points yesterday.

Demand Collapse Hits China (FXI), with US manufacturing there down 40% and many factories closing early for the New Year. Container traffic from the Middle Kingdom is down 21% over the past three months, astounding ahead of Christmas.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 12 at 8:00 AM, the Consumer Inflation Expectations for November is published.

On Tuesday, December 13 at 8:30 AM EST, the Core Inflation Rate for November is out

On Wednesday, December 14 at 11:00 AM EST, the Federal Reserve Interest rates decision is announced. The Press Conference follows at 11:30.

On Thursday, December 15 at 8:30 AM EST, the Weekly Jobless Claims are announced. Retail Sales for November are printed.

On Friday, December 16 at 8:30 AM EST, the S&P Global Composite Flash PMI for December is disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, in 1978, the former Continental Airlines was looking to promote its Air Micronesia subsidiary, so they hired me to write a series of magazine articles about their incredibly distant, remote, and unknown destinations.

This was the only place in the world where jet engines landed on packed coral runways, which had the effect of reducing engines lives by half. Many had not been visited by Westerners since they were invaded, first by the Japanese, then by the Americans, during WWII.

That’s what brought me to Tarawa Atoll in the Gilbert Islands, and island group some 2,500 miles southwest of Hawaii in the middle of the Pacific Ocean. Tarawa is legendary in the US Marine Corps because it is the location of one of the worst military disasters in American history.

In 1942, the US began a two-pronged strategy to defeat Japan. One assault started at Guadalcanal, expanded to New Guinea and Bougainville, and moved on to Peleliu and the Philippines.

The second began at Tarawa, and carried on to Guam, Saipan, and Iwo Jima. Both attacks converged on Okinawa, the climactic battle of the war. It was crucial that the invasion of Tarawa succeed, the first step in the Mid-Pacific campaign.

US intelligence managed to find an Australian planter who had purchased coconuts from the Japanese on Tarawa before the war. He warned of treacherous tides and coral reefs that extended 600 yards out to sea.

The Navy completely ignored his advice and in November 1943 sent in the Second Marine Division at low tide. Their landing craft quickly became hung up on the reefs and the men had to wade ashore 600 yards in shoulder-high water facing withering machine gun fire. Heavy guns from our battleships saved the day but casualties were heavy.

The Marines lost 1,000 men over three days, while 4,800 Japanese who vowed to keep it at all costs, fought to the last man.

Some 35 years later, it was with a sense of foreboding that I was the only passenger to debark from the plane. I headed for the landing beaches.

The entire island seemed to be deserted, only inhabited by ghosts, which I proceeded to inspect alone. The rusted remains of the destroyed Marine landing craft were still there with their twin V-12 engines, black and white name plates from “General Motors Detroit Michigan” still plainly legible.

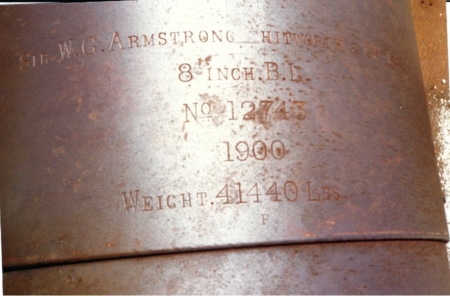

Particularly impressive was the 8-inch Vickers canon the Japanese had purchased from England, broken in half by direct hits from US Navy fire. Other artillery bore Russian markings, prizes from the 1905 Russo-Japanese War transported from China.

There were no war graves, but if you kicked at the sand human bones quickly came to the surface, most likely Japanese. There was a skull fragment here, some finger bones there, it was all very chilling. The bigger Japanese bunkers were simply bulldozed shut by the Marines. The Japanese are still in there. I was later told that if you go over the area with a metal detector it goes wild.

I spend a day picking up the odd shell casings and other war relics. Then I gave thanks that I was born in my generation. This was one tough fight.

For all the history buffs out there, one Marine named Eddie Albert fought in the battle who, before the war, played “The Tin Man” in the Wizard of Oz. Tarawa proved an expensive learning experience for the Marine Corps, which later made many opposed landings in the Pacific far more efficiently and with far fewer casualties. And they paid much attention to the tides and reefs, developing Underwater Demolition Teams, which later evolved into the Navy Seals.

The true cost of Tarawa was kept secret for many years, lest it speak ill of our war planners, and was only disclosed just before my trip. That is unless you were there. Tarawa veterans were still in the Marine Corps when I got involved during the Vietnam War and I heard all the stories.

As much as the public loved my articles, Continental Airlines didn’t make it and was taken over by United Airlines (UAL) in 2008 as part of the Great Recession airline consolidation.

Tarawa is still visited today by volunteer civilian searchers looking for soldiers missing in action. Using modern DNA technology, they are able to match up a few MIAs with surviving family members every year. I did the same in Guadalcanal.

As much as I love walking in the footsteps of history, sometimes the emotional price is high, especially if you knew people who were there.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tarawa November 1943

Broken Japanese Cannon

Armstrong 8-Inch Cannon 1900

US Landing Craft on the Killer Reef

How to Get to Tarawa

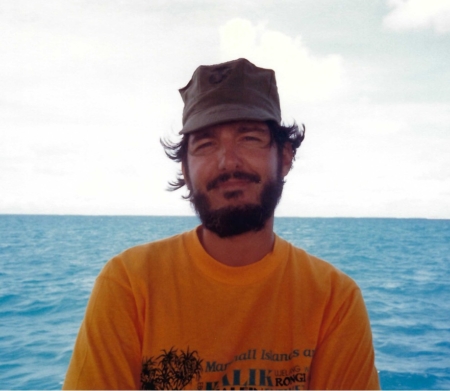

Roving Foreign Correspondent on Tarawa in 1978

Second Marine Division WWII Patch