Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)

Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

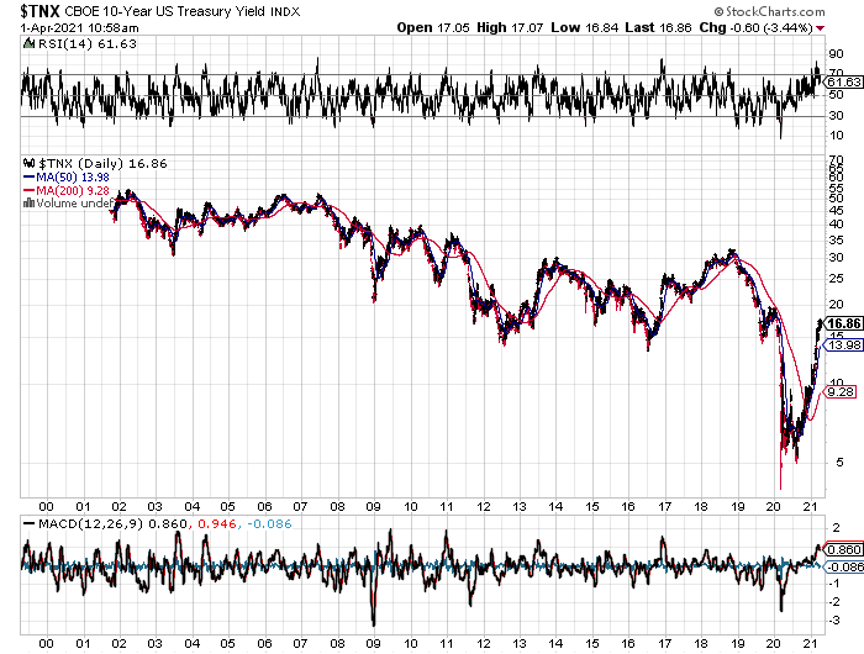

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & Healthcare Letter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 5, 2021

Fiat Lux

Featured Trade:

(MARCH 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (CRM), (ZM), (AAPL), (AMD), (DIS), (CRSP),

(BRKB), (PLTR), (NVDA), (TLT), (TSLA), (GLD),

(SLV), (VSAT), (EUO), (GME)

Below please find subscribers’ Q&A for the March 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are SPACs here to stay?

A: Yes, but I think that in the next bear market, 80% of these SPACs (Special Purpose Acquisition Companies) will disappear, will deliver large losses, and will continue charging you enormous fees until then. It’s either that or they won’t invest their money at all and give it back, net of the fees. So, I’m avoiding the SPAC craze unless it's associated with a very specific investment play that I know well. The problem with SPACs is that they all come out expensive—there are no bargain basement SPACs on launch day. Me, being the eternal cheapskate that I am, always want to get a great bargain on everything. The time to buy these is actually in the next bear market, if they still exist, because then investors will be throwing their positions away at 10 or 20% discounts. That’s always what happens with specialized ETF, closed-end funds, and so on. They are roach motel investments; you can check-in, but you can never check out.

Q: What do you think of Elizabeth Warren's asset tax idea?

A: It’s idiotic. It would take years to figure out how much Jeff Bezos is worth. And even then, you probably couldn't come within ten billion dollars of a true number. We already pay asset taxes, our local county real estate taxes, and those are bad enough, delivering valuations that are miles from true market prices. There are many other ways to fix the tax system and get billionaires paying their fair share. There are only three things you really have to do: get rid of carried interest so hedge funds can’t operate tax-free, get rid of real estate loss carry forwards which allow the real estate industry to basically operate tax-free, and get rid of the oil depletion allowance, which has enabled the oil industry to operate tax-free for nearly 90 years. So those would be three easy ones to increase the fairness of the tax system without any immense restructuring of our accounting system.

Q: When will share buybacks start?

A: They’ve already started and have been happening all year. There are two ways the companies do this: they either have an outside accounting firm, buying religiously every day or at the end of every month or something like that, so they can’t be accused of insider trading; or they are in there buying on every dip. Certainly, all the big cash-heavy companies like Berkshire Hathaway (BRKB) or Apple (AAPL) were buying their shares like crazy last March and April because they were trading such enormous discounts. So that is another trillion dollars sitting under the market, waiting to come in on any dip, which is yet another reason that we are not going to see any major sell-offs this year—just the 5%-10% variety that I have been predicting.

Q: Is it time to buy Salesforce (CRM)?

A: Yes, Marc Benioff’s goal is to double sales in two years, and the stock is relatively cheap right now because they’ve had a couple of weak quarters and are still digesting some big acquisitions.

Q: Is CRISPR Therapeutics (CRSP) good buy?

A: Yes, I would be buying right here; it’s a good LEAP candidate because the stock could easily double from here. We’ve only scratched the surface on CRISPR technology being adopted and the potential growth in this company is enormous—I'm surprised they haven’t been taken over already.

Q: Will you start a letter for investing advisors on how to deal with the prolific numbers of Bitcoin?

A: There are already too many Bitcoin newsletters; there are literally hundreds of them and thousands of experts on Bitcoin now because there’s nothing to know and nothing to analyze. It’s all a belief system; there are no earnings, there are no dividends, and there is no interest. So, you purely have to invest in the belief that somebody else is going to take you out at a higher price. I think there is a big overhang of selling in that when they raise the number of Bitcoin, we’ll get another one of those 90% crashes that Bitcoin is prone to. So, go elsewhere for your Bitcoin advice; your choices are essentially unlimited now, and they are much cheaper than me. In fact, people are literally giving away Bitcoin advice for free, which means you’re getting what you’re paying for. I buy Bitcoin when they have a customer support telephone number.

Q: Zoom (ZM) has come down a lot after a big earnings report—do you like it?

A: Long term, yes. Short term, no. You want to avoid all the stay-at-home stocks because no one is staying at home anymore. However, there is a long-term story in Zoom once they find their bottom because even after we come out of the pandemic, we’re all still using Zoom. I have like five or ten Zoom meetings a day, and my kids go to school on Zoom all day long. They’re also bringing out new products like telephone servers. They’re also raising their prices—I happen to be one of Zoom’s largest customers. I’m paying $1,100/month now, and that’s rising at 10% a year.

Q: What would be the best LEAP for Salesforce (CRM)?

A: The rule of thumb is that you want to go 30% out of the money on your first strike. So, find a current stock price; your first strike is up 30%, and then your second strike is up 35%. And all you need to double your money on that is a bounce back to the highs for this year, which is not unrealistic. That’s the lay-up there with Salesforce. That’s the basic formula; Advanced Micro Devices (AMD), Walt Disney (DIS), Berkshire Hathaway (BRKB), Palantir (PLTR), and Nvidia (NVDA) are all good candidates for LEAPS.

Q: How often do you update the long-term stock portfolio?

A: Twice a year, and we just updated in January, which is posted on the website in your membership area. If you can't find it, just email customer support at support@madhedgefundtrader.com and they’ll tell you where to find it. And we only do this twice a year because there just aren't enough changes in the economy in six months to justify a more frequent update.

Q: When do you think real estate will come back?

A: It never left. We’ve had the hottest real estate market in history, with 20% annual gains in many cities in 2020. And that will continue, but not at the 20% rate, probably at a more sustainable 5% or 6% rate. Guess what the best inflation play in the world is? Real estate. If you’re worried about inflation, you want to run out and buy a house or two. The only thing that will really kill that market is a rise in 30-year fixed-rate mortgages to 5%, and that is years off. Or a rise in the ten-year treasury to 5% or 6%—that is several years off also. So, I think we’ve got a couple of good years of gains ahead of us. I at least want the market to stay hot until my kids get out of high school, and then I can sell my house and go live on some exotic tropical island with great broadband.

Q: When you’re doing LEAPS, do you just do the calls only or do you do these as spreads?

A: You can do both. Just do the math and see what works for you on a risk/reward basis. You can do a 30% out of the money call 2 years out and get anywhere from a 1,000% to a 10,000% return—people did get 10,000% returns buying deep out of the money LEAPS in Tesla (TSLA) a year ago (that’s where all the vintage bourbon is coming from). Or you can do it more conservatively and only make 500% in two years on Tesla spread. For example; do something like a Tesla January 2023 $900-$950 call spread. If Tesla shares rise to $950, that position is an easy quadruple. But do the numbers, figure out the cost today, what the expiration value is in two years, and there you go.

Q: Do you think overnight rates could go negative as some people predict?

A: Not for a long time. They will go negative at the next recession because we’re starting off such a low base—or when we get the next pandemic, which could be as early as next year. We could get another one at any time from a completely different virus, and it would generate the same stock market results that we got last time—down 40% in a month. We’re not out of the pandemic business, we’re just having a temporary break waiting for the next one to come along out of China or some other country, or even right here in the USA. So that may be a permanent aspect of investing in the future. It could be the price we pay having a global population that's at 7 billion heading to 9 billion.

Q: Expiration on LEAPS?

A: I always go out two years. The second year is almost free, that’s why. So why not go for the second year? It gives you twice as much time to be right, always useful.

Q: My two-year United States Treasury Bond Fund (TLT) $125 put LEAPS have turned very positive. Is this a good trade?

A: That is a good trade, which you should put on during the next (TLT) rally. If you think we’re going to $105 in 2 years, do something like a $127-$130 two-year put LEAP, and there's a nice four bagger right there.

Q: Your Amazon (AMZN) price target was recently listed at $3,500, below last year's high, but I’ve also seen a $5,000 forecast in two years. Are you sticking with that?

A: Yes, I think when you get a major recovery in the economy, Amazon will be one of the only pandemic plays that keeps on going. It’s just taking a rest here with the rest of big tech. The breakup value of Amazon is easily $5,000 a share or more. Plus, they’re still going gangbusters growing into new industries that they’ve barely touched so far, like pharmaceuticals, healthcare, and so on. So yes, I would definitely be a buyer of LEAPS, and you could do something like the January 2023 $3700-$4000 LEAP two years out and make a killing on that.

Q: Anything you can do in gold (GLD)?

A: Not really. Although gold and silver (SLV) have been a huge disappointment this year, I think this could be the beginning of a capitulation selloff in gold which will bring us a final bottom, but it may take another month or two to get there.

Q: How can I sell short the dollar?

A: You sell short the (UUP), or there are several 1X and 2X short ETFs in the currencies that you can do, like the ProShares Ultra Short Euro ETF (EUO). That is the way to do it.

Q: What is the best timing for buying LEAPS?

A: Buy at market bottoms. A year ago, I was sending out lists of 10 LEAPS at a time saying please buy all of these. You need both a short-term selloff in the stock, and then an upside target much higher than the current price so your LEAP expires at its maximum profit point. And if you’re in the right names, pretty much all the names that we talk about here, you will have 30%, if not 300% or 3,000% gains in them in the next two years.

Q: Do you think Tesla’s Starlink global satellite system will disrupt the cell tower industry?

A: Yes, that is the goal of Starlink—to wipe out all ground communication for WIFI and for cell phones. It may take them several years to do it, but if they do pull it off, then it just becomes a matter of pricing. The last Starlink pricing I looked at cost about $500 to set up, open the account, and get your dish installed. And the only flaw I see in the Starlink system is that the satellite dishes are tracking dishes, which means they lock onto satellites and then follow them as they pass overhead. Then when that signal leaves, it locks onto a new satellite; at any given time they’re locked onto four different satellites. That means moving parts, and you want to be careful of any industry that has moving parts—they wear out. That’s the great thing about software and online businesses; no moving parts, so they don’t wear out. And that’s also why Tesla has been a success; they eliminated the number of moving parts in cars by 80%. I’m waiting for Starlink to get working so I can use it, because I need Internet access 24 hours a day, even if all the local hubs are out because of a power outage. I’m now using something called Viasat (VSAT), which guarantees 100 megabyte/second service for $55 a month. It's not enough for me because I use a gigabyte service landline, but when that’s not available then I can go to satellite as a backup.

Q: Is there too much Fed liquidity in the market already? Why is the $1.9 trillion rescue package still positive for the market?

A: Firstly, there is too much liquidity in the market; that is screamingly obvious. If you look at liquidity over the decades, we are just staggeringly high right now. M2 is growing at 26% against the normal rate of 5%-6%. What the stimulus package does is get money to the people who did not participate in the bull market from last year. Those are low-income people, cities, and municipalities that are broke and can’t pay teachers, firemen, and policemen. It also goes to individual states which were not invested in the stock market. It turns out that states that were invested in the stock market like California have money coming out of their ears right now. And it gets money to low wage workers with kids who are certainly struggling right now. So, it is rather efficiently designed to get the money to people who need it the most. There is still half the country that doesn't own any stocks or even have savings of any kind. One or two people might get it who don’t deserve it but try doing anything in a 330 million population country and have it be 100% efficient.

Q: Is inflation coming?

A: Only incrementally in tiny pieces, so not enough to affect the stock market probably for several years. I still believe technology is advancing so fast that it wipes out any effort to raise prices or increase wages, and that may be what the perennially high 730,000 weekly jobless claims is all about. Those jobs that might have been there a year ago have been replaced by machines, have been outsourced overseas, or the demand for the product no longer exists. So, as long as you have a 10% unemployment rate and a weekly jobless claim at 730, inflation is the last thing you need to worry about.

Q: Is there any way to cash in on Reddit’s Wall Street Bets action?

A: No, and I would bet the majority of people who are trading off of these emojis and Reddit posts are losing money. You only hear about these things after it’s too late to do anything about them. I don't think you’ll get any more $4 to $450 moves like you did with GameStop (GME) because in that one case only, there was a short interest of 160%, which should have been illegal. All the other high short interest stocks have already been hit, with short interests all the way down to 30%, so I think that ship has sailed. It has no real investing merit whatsoever.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 19, 2021

Fiat Lux

Featured Trade:

(FEBRUARY 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(USO), (XLE), (AMZN), (SPY), (RIOT), (T), (ZM), (ROKU), (TSLA), (NVDA) (TMQ) (TLRY), (ACB), (KO), (XLF), (AAPL) (REMX), (GLD), (SLV), (CPER)

Below please find subscribers’ Q&A for the February 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are we buying gold on dips?

A: Not yet. As long as you have a ballistic move in bitcoin going on, you don't want to touch gold. Eventually gold does get dragged up by the global bull market in commodities, but silver is more preferable since it moves up at twice the rate of gold in bull markets.

Q: Is it time to buy Amazon (AMZN) LEAPS?

A: Yes, I am looking for a move to $5,000 a share in Amazon with the onset of enormous GDP figures. Exploding consumer spending may be what breaks Amazon out of its current six-month range. I would do something like a two-year LEAP with the $3,600-$3,700 in Amazon. Be cautious and stay near the money. You should get like a 400% or 500% return on that LEAP at expiration, or sooner.

Q: What's your view on Tesla (TSLA)?

A: It looks tired—lower lows, lower highs. We’re in a short-term downtrend that could last several months. I’m holding off on buying Tesla until we find a bottom. I just have one $150 out-of-the-money call spread that expires in 20 days, and that’s it. We paired our position way back on Tesla. Wait for the market to come to you, if you can get Tesla under $700, that's a great time to buy LEAPS on Tesla.

Q: Are you still bearish on energy (XLE)?

A: Short term no, long term yes. You’re trying to catch a rally in a long-term bear market. Some people can do that, some people can’t. It’s the next buggy whip industry, the next American Leather, which completely vaporized.

Q: What about the calls for $100 oil (USO)?

A: Yes, after the markets went up $10 dollars in a day you always see calls for $100 oil. If the energy crisis in Texas shows us anything, it’s that we have to move away from oil as an energy source much faster than we thought because its distribution and production system freeze.

Q: Are you expecting a short-term correction (SPY)?

A: Yes but no more than 4%; there is still too much cash on the sidelines.

Q: Have airline leisure stocks run too far?

A: No, they are coming off of much lower lows so they can go to much higher highs. Almost all restrictions should be gone in six months—I’m trying to time my Australia trips and I think in six months may get to the point where, if you show proof of vaccination and submit to a 3 day test, they will let you into the country. But in six months you won’t be able to get an airline or hotel reservation.

Q: What about the AT&T (T) yield play and 5G play?

A: Yes, I still like AT&T and you should probably buy it about here. All these legacy telecom companies are going to have big moves once 5G accelerates allowing a vast expansion of streaming and other high-end services.

Q: Is CRISPR (CRSP) a good LEAP candidate?

A: Yes, and you can do something like the $200-$210 two years out because it’ll almost certainly get taken over before then.

Q: What’s a good LEAP for Tesla?

A: Wait for it to drop to $700 first and then buy something like the $900-$1000 two years out.

Q: What do you think of Apple?

A: Apple (AAPL) is taking a rest waiting for the 5G rollout to reaccelerate. Our target for Apple this year is $200.

Q: Do we sell in May and go away?

A: I would just go away and keep all your longs. The trouble is, trying to be ultra-smart and time all this stuff in a runaway bull market, you find it a lot harder to get in when you come back; you go “oh my gosh these things are up so much,” you don’t buy anything, and then it doubles. I’ve seen that a lot in the past, New York in 1971, Tokyo in 1987, Dotcom stocks in 1985, add US stocks in 2015.

Q: What do you think of Riot (RIOT) stock?

A: Wouldn't touch it with a ten-foot pole. If I didn’t want to buy bitcoin at $1, I'm not going to want to buy it at $51,000. Go elsewhere for your bitcoin advice, except you’ll hear the same thing: it will go up because it’s gone up. You should use it as a risk indicator. That’s essentially what all bitcoin analysts will tell you because there's nothing to analyze. There are no earnings, there's not even any physical presence anywhere to analyze, no customer support. If you can get seven 10 baggers like we did last year, with Zoom (ZM), Roku (ROKU), Tesla (TSLA), and Nvidia (NVDA) —why bother with cryptocurrencies?

Q: What are your thoughts on travel?

A: My take is that leisure travel is returning in mass but that the business travelers will shy away; and that will be true for this year but probably not next year. I think business travel will come back once it’s 100% safe and once all the companies are making money again and can afford travel.

Q: Is Trilogy Metals Inc. (TMQ) a good buy? It has Copper, Zinc, and some exposure to Gold and Silver.

A: Yes, it is a buy. Most commodity prices should double from these levels; and probably the smartest ones to buy are the ones that haven't moved yet—gold and silver, but silver especially. The world will come roaring back and it needs every possible metal it can get its hands on.

Q: What do you think of the cannabis stocks (TLRY), (ACB)?

A: That is one of several small bubbles in the markets that I don't want to touch at all. How hard is it to grow a weed? Barriers to entry are zero. Massive competition from the black market, as about 30% of the cannabis demand is still going to your local drug dealer who doesn’t have to pay taxes, whereas you get double taxed with a pot company—35% retail sales taxes and then taxes on the profits on top of that. So no thank you, Mary Jane.

Q: Do you think Warren Buffet is still the leading thought contributor to personal finance, or is he outdated?

A: Berkshire Hathaway is up 10% this year, and the Dow is up only 2.8%, so I would say he’s still pretty well in touch with the markets; and he has very heavy weightings in Coca Cola (KO), Financials (XLF), and Apple (AAPL), as well as some energy stocks. Good discipline and good strategy never go out of style.

Q: Is the Texas energy disaster going to set the US’ way on renewable energy faster?

A: Yes, it does force people to consider the move into alternative energy sources much faster, especially when the old energy sources go to zero and then have whole states lose their power sources. Look how the governor of Texas is blaming frozen windmills, which only account for 7% of the Texas energy supply. What a joke! I’ll lend him my hairdryer and they’ll work. Notice the propensity to immediately blame others for their own mistakes. That is terrible leadership. Texas is going to turn blue.

Q: Is climate change overhyped in the US stock market?

A: Absolutely yes, that’s why I haven’t been buying any of these. They tend to be smaller companies, and ever since Biden got the lead in the primaries and the polls last spring this whole sector, and ESG investing in general, has been on an absolute tear and is wildly expensive. I call these feel-good stocks; people buy them because they make them feel good but very few of these actually make real money. I prefer to stick to the real money plays of which there are more than enough around.

Q: Do you like rare earth such as the Van Eck Vectors Rare Earth/Strategic Metals ETF (REMX)?

A: I do like rare earths. You need them for practically anything electronic. China's been withholding supplies again, which they like to do from time to time just to rattle our cage because we need them for all our weapons systems. But this is also prone to bubbles, so be careful when you buy it that you’re not paying up too much. By the way, the (REMX) ETF was brought out at the absolute peak of the last rare earth bubble, which we covered extensively 11 years ago. We got people in at the very bottom of rare earth, and things went up ten times. Then we got everybody out and people said I was being bearish too soon, so I never got invited to conferences again. After that, it went down for eight straight years.

Q: Don’t you think frozen windmills and solar speak for more reliance on oil than less? Biden administration limits on oil will drive up prices.

A: You’re right on the second part; creating shortage of supply will cause price increases. But frozen windmills are a result of lack of capital investment and planning. It turns out all of the windmills in the northern part of the US have electric heaters, so they don’t freeze because it gets colder up there. They didn’t do that in Texas to save money, and now they have lost about 7% of the total Texas energy supply. So bad management was the issue there. Penny-wise and pound-foolish.

Q: Are commodities in general in play? What is the best ETF for commodities?

A: The trouble with commodities is there is no one big catch all commodity ETF. However, you can expect one soon; as things peak or have big runs, they tend to generate new ETFs like new children because the demand is there. In the commodities world, there are lots of individual 1x and 2x ETFs like the gold ETF (GLD), the silver (SLV), the copper (CPER), and so on. But there isn’t one good basket I’ve found. You can always create your own by buying small amounts of each of the leading companies, which is probably the best thing to do.

Q: What is the best property value right now?

A: That would be Mississippi; they have the lowest housing prices in the United States. Unfortunately, low cost of living, low tax states also have the worst education systems, which doesn’t matter of course if you don't have kids. In the end, you get what you pay for. It’s OK if you don’t mind dealing with stupid people every day, which I do. I can always tell when I’m dealing with customer support in the deep south because literacy falls off a cliff.

Q: Should we get a 10% correction soon?

A: Probably not; the last 10% correction needed a presidential election to scare the daylights out of you, and there's nothing like that on the horizon now. Maybe we’ll get another 5% correction on a game stop type incident, but there's just too many people trying to get into the stock market now. People who were selling last March/April are the same people who are buying now.

Q: Is there a bright future for hydrogen?

A: No, electricity is infinitely scalable, and hydrogen isn’t. It’s about as scalable as gasoline because you have to move it around in big tankers, keep it at 434.5 degrees Fahrenheit below zero, which is very expensive and has an unfortunate tendency to blow up. So, I never bought into the hydrogen thesis, except for local use of fleets where everyone gets all their hydrogen from a central facility.

Q: What will be the best performing sector in the next 1-3 months?

A: Your bond short and your financials. It’s the same trade. And it’s the one sector that no one asked about today.

Q: Do you think bitcoin is a bubble poised to pop at some point?

A: Yes, but who knows where that is; bubble tops are impossible to predict, especially when there are no valuation metrics. Bottoms can be measured with valuation metrics, but tops can’t because greed is an immeasurable quantity. However, it will certainly pop when they suddenly decide to increase the total outstanding number of bitcoins, which may seem unlikely now but is inevitable.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 11, 2021

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

February 5, 2021

Fiat Lux

Featured Trade:

(FEBRUARY 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(MRNA), (PFE), (JNJ), (AMZN), (SLV), (GME), (GLD), (CLDR), (SNOW), (NVDA), (X), (FCX),

(AAPL), (TSLA), (FEYE), (PANW), (SWI), (WYNN), (MGM), (LVS)

Below please find subscribers’ Q&A for the February 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV.

Q: Is there a big difference between COVID-19 vaccines?

A: The best vaccine is the one you can get. It’s better than being dead. But there are important differences. The Pfizer (PFE) and Moderna (MRNA) vaccines are RNA vaccines, they’re very safe, and getting similar results. But the evidence shows that about 15% of Moderna recipients are coming down with flu-like symptoms on their second shot. Nobody knows why, as the two are almost biochemically identical. AstraZeneca is a killed virus type vaccine, which means if they have a manufacturing error, you end up giving the disease to people by accident, as with the original polio vaccine. So that's the less safe vaccine. So far, that one has only been used in Europe and Australia, as it is made in England. There isn’t enough data about the John & Johnson (JNJ) single-shot vaccine.

Q: Is Moderna (MRNA) a long term buy?

A: The trouble with all the vaccine plays is that we’re heading for a global vaccine glut in about 4 months when we’ll have something like 12 companies around the world making them. The rush for everyone to get a vaccination as soon as possible is leading to inevitable overproduction and falling stock prices. Moderna is already a 12 bagger for us. I’m not really looking to overstay my welcome, so to speak. Time to cash in and say, “Thank you very much, Mr. Market.” There will be another cycle down the road for (MRNA) as its technology is used to cure cancer, but not yet.

Q: Would you recommend a silver (SLV) LEAP?

A: Yes, silver was run up 35% for a day by the GameStop (GME) crowd and crashed the next day, which was to be expected because there are no short positions in silver. Everything was just hedged to look like there were short positions because the big banks had huge open short options positions that were public and hedges in the futures and silver bars that were private. The (GME) people only saw the public short positions. Long term, I would go for a $30-$32 vertical call spread expiring in 2023. Go out 2 years, and I think you could get silver at $50. So, a good LEAP might get you a 1000% return in two years. Those are the kinds of trades I like to do.

Q: What do you think of Amazon now that Jeff Bezos is retiring?

A: Buy the daylights out of it. That was the great unknown overhanging the stock for years, Jeff’s potential retirement. Now it's no longer unknown, you want to buy (AMZN). Even before the retirement, I was targeting $5,000 a share in two years. Now we have everybody under the sun raising their targets to $5,000 or more— we even had one upgrade today to $5,200. There are at least half a dozen businesses that Amazon can expand into, like healthcare, which will be multibillion-dollar earners. And then if you break it up because of antitrust, it doubles in value again, so that's a screaming buy here. We have flatlined for six months, so this could be a trigger for a long-term breakout.

Q: Is there anything else left after GameStop? Another short play?

A: Well, this was the worst short squeeze in 25 years, and everyone else covered their other shorts because they don't want to get wiped out like the one Melvin Capital. There were only around a dozen potential single-digit heavily shorted stocks out there, and those are mostly gone. So, the GameStop crowd will have to roll up their sleeves and do some hard work finding stocks the old fashion way—by doing research. I’m guessing that GameStop was a one-hit-wonder; we probably won’t be surprised again. At the same time, you should never underestimate the stupidity of other investors.

Q: What do you think of the cloud plays like Cloudera and Snowflake?

A: I love cloud plays and there will be more coming. The entire US economy is moving on to the cloud. But everyone else loves them too. Snowflake (SNOW) doubled on its first day, and Cloudera (CLDR) doubled over the last three months, so they're incredibly expensive and high risk. But you can't argue with their business models going forward—the cloud is here to stay.

Q: Would you buy LEAPS in financials?

A: Absolutely yes; go out two years for your maturity and 30% on your strike prices, you will get a ten bagger on the trade. If I’m wrong, it only goes to zero.

Q: Is US Steel (X) a buy?

A: Yes. They are being dragged up by the global commodity boom triggered by the global synchronized recovery. (X) took a hit today because they just priced a $700 million secondary share issue which the flippers dumped like a hot potato. If given the choice, I’d rather do a copper play with Freeport McMoRan (FCX) which is seeing much more buying from China. I bought it on Monday.

Q: Any chance you can include one-, three-, and five-year price targets?

A: No chance whatsoever. I’ve never heard of a fund manager that could do that and be right. Stocks are just too imprecise an instrument with all the emotion that’s involved. But for the better stocks, you can with confidence predict at least a double. And by the way, all my predictions for the last 13 years have been way, way on the low side, so I tend to be conservative. Like, remember when Amazon was at $10? I said it would go to $20. Boy was I right!

Q: How can you say the next four years will be good for the stock market?

A: Well, $10 trillion in fiscal stimulus, $10 trillion in QE; stocks tend to like that. Oh, and technology exponentially accelerating on all fronts and far more broadly than what we saw in the 1990s. Also, there is a certain person who is no longer president, so add about 10-20% on top of all stock valuations. Companies can finally do long term planning again, after being unable to do so for four years because policies were anti-trade, anti-business, and flip-flopping every other day. So yes, I think that's enough to make the next 4 four years good; and actually, I think the next 8 years could be good—I'm predicting Dow 120,000 by 2030, if you recall.

Q: When do you expect the next 5% correction if there is one? February is always very volatile.

A: With an unlimited liquidity market like we have, it is really tough to see negatives of any kind. What kind of negatives are out there? The pandemic doesn’t stop—that's the main one. There’s another one people aren't talking about: the reason we got all these vaccines so fast is they took all regulation and threw it out the window. What if one of these vaccines kill off a million people? That would be pretty negative for the market. Interest rates could rocket faster than expected. But I’m always short there so that would be a moneymaker. But these are pretty out there possibilities, and that is why the market is not backing off, and when it does, it only gives us 5%.

Q: Is the Fed stimulating the economy too much?

A: The bond market says no with a ten-year yield of 1.10%, and the bond market is always the ultimate arbiter of when the stimulus ends. That’s because the Fed can’t directly control bond market interest rates, only overnight rates. But when we get bonds up to, say, a 3% yield (which is probably 2 or 3 years off), that’s when we’re getting too much stimulus, and we’ll probably take our foot off the pedal way before then. I know Janet Yellen and she agrees with me on this point. She’ll be throttling back well before we see a 3% yield in the Treasury market.

Q: Do you manage other people’s money?

A: No, because it costs a million dollars in legal fees to set up even a small fund these days. When I set up my hedge fund 30 years ago, there were no regulatory costs because no one knew what a hedge fund was; they all thought they were doing something illegal, so they didn't have to register for anything. That’s why it’s changed now.

Q: What is your target on NVIDIA (NVDA), and will it split?

A: It’s an easy double, with a global chip shortage running rampant. They make the best graphics cards in the world, bar none. These big tech companies tend not to split until they get share prices into the thousands, which is what Apple (AAPL) and what Tesla (TSLA) did three or four times.

Q: If we get 3.25% in bonds, is that going to hurt gold?

A: Yes, and that’s one of the reasons I bailed on my gold positions a couple of weeks ago. It effectively turned into a bond long. A sharp rise in interest rates is bad for gold because we all know that gold yields to zero.

Q: What about Fireye (FEYE)?

A: Yes, we also love Fireye in addition to Palo Alto Networks (PANW) because there is a near-monopoly—there are only about six players in the entire cybersecurity industry and hacking is getting worse by the day. Look at the Solar Winds (SWI) fiasco and the national Russian hack there.

Q: What about copper as a recovery play?

A: Well, I voted with my feet on Monday when I bought a position in Freeport McMoRan, after it just sold off 15%. I think (FCX) could double at some point in the coming economic recovery. So, copper is an absolute winner, and when having to choose between copper and steel, I’ll pick copper all day long.

Q: What do you recommend for gold (GLD)?

A: Gold is a trading range for the time being. Buy the dips, sell the rallies; you won’t get more than about 10% or 15% range on that. And there are just better fish to fry right now, like financials, which benefit from rising interest rates as opposed to being punished. Bitcoin is stealing gold’s thunder and the markets keep creating more Bitcoins.

Q: Should high-frequency trading be banned?

A: I don’t think it should be. It does create liquidity; the effect on the market is wildly overexaggerated. They’re basically trading for pennies or tenths of pennies, so they do provide buying on selloffs and selling at huge price spikes. They do have a positive effect and they’re probably only taking about $10 or $20 billion in profit a year out of the market.

Q: Should I buy Wynn Resorts (WYNN) here?

A: Buy the dips for sure; this is a major recovery play. We here in Nevada are expecting an absolute tidal wave of people to hit the casinos once the pandemic ends, and (WYNN), (MGM), and (LVS) would be a great play in those areas.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 2, 2021

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (MS), (GS), (BABA), (EEM), (FXA), (FCX), (GLD), (SLV), (TLT)