Global Market Comments

July 20, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE’S YOUR SERVING OF ALPHABET SOUP),

(SPY), (TLT), (GLD), (TSLA), (DRI), (WYNN), (H), (AMC)

Global Market Comments

July 20, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE’S YOUR SERVING OF ALPHABET SOUP),

(SPY), (TLT), (GLD), (TSLA), (DRI), (WYNN), (H), (AMC)

Here is your generous helping of alphabet soup. If you look very closely, you can find some bay leaves, oregano, black pepper, and lots of V’s, W’s, U’s, and L’s.

Now, let’s play a game and see who can pick the letter that most accurately portrays the current economic outlook.

Here is a code key:

V – the very sharp collapse we saw in Q1 and Q2 is followed by an equally sharp recovery in Q3 and Q4.

W – The sharp recovery in Q3 and Q4 fails and we see a double-dip extending into 2021.

U – The economy stays at the bottom for a long time before it finally recovers.

L – The economy collapses and never recovers.

The question is, in which of these forecasts should we invest our investment strategy?

For a start, you can throw out the “L”. Every recession flushes out a covey of Cassandras who predicts the economy will never recover. They are always wrong.

I believe what we are seeing play out right now is the “W” scenario. This is the best cash scenario for traders, as it calls for a summer correction in the stock market when we can load the boat a second time. If you missed the March low you will get a second bite of the Apple.

With corona cases soaring nationwide, and deaths skyrocketing, it is safe to write off the “V” recovery scenario.

If I’m wrong, we will get a “U”, a longer recovery. This cannot be dismissed lightly as the unemployment rate is about to take off as the PPP money runs out, state unemployment benefits are exhausted, and mass evictions ensue.

If I limited the outlook to only four possible scenarios, I’d be kidding you. The truth is far more complicated.

Each industry gets its own letter of the alphabet. Technology, some 27% of total stock market capitalization gets no letter at all because it is thriving, thanks to the global rush to move commerce online. That explains the single-minded pursuit of this sector by investors since the market 23 bottom.

Hotel chains like Hyatt Hotels (H) and casinos like Wynn Resorts (WYNN) get a “U” because they will recover after a long period of suffering. As for Movie theaters like AMC Entertainment Holdings (AMC) and restaurant chains such as Darden Restaurants (DRI), they get an “L” because it is hard to see any sustainable recovery before widespread use of a vaccine.

Weekly Jobless Claims remained at Historic Levels, at 1.3 million, reaching a total of 51 million since the pandemic began. We are about to see a huge surge in the unemployment rate as PPP money and state unemployment benefits run out. Without help from the federal government, millions will be thrown out on the street.

Tesla hit $1,800, up $255, on the news they may join the S&P 500 forcing a ton of institutional buying. Its market capitalization is now a staggering $330 billion, more than the entire global car industry combined. They also cut Model Y prices by $3,000, from $53,000 to $50,000, in another effort to keep new entrants at bay. The model Y is expected to be the biggest seller in history, hence the ballistic move in the shares now. Close your eyes and keep buying (TSLA) on dips.

Tesla is dead, long live Tesla, says Morgan Stanley analyst Adam Jonas. The big upside here will not be in (TSLA) itself, but in supplier companies such as ST Microelectronics, NXP Semiconductors (NXPI), Cree (CREE), and China’s CATL. Jonas, an early Tesla bull, still maintains a $3,000 target, but that is now only a double from here, a far cry from the 110X move behind us off the post IPO low.

5G cell phones could offset Corona losses to the global economy, or so says a French economic research institute. Productivity improvement alone could be worth $2.2 trillion a year. The big winner? Apple (AAPL). Is this really why stocks are going up so fast?

California shut down again as hospital emergency rooms approach capacity. All indoor business has ceased for a state that accounts for 21% of US GDP. The Golden State saw 8,357 new cases on Sunday. Unfortunately, it gives more credence to my “W” shaped recovery for the economy. Stocks noticed about three hours into the Monday session, diving 550 points. It’s not me! I tested negative last week.

Homebuilders saw the best June in history, up 55% YOY. Builders and supplies are now in short supply and prices are rising sharply. New homes are being favored over existing ones, which can’t be viewed through standardized virtual presentations. Keep buying (LEN), (KBH), and (PHM) on dips as the gale-force Millennial tailwind continues unabated.

Homebuilder Confidence jumped back to pre-pandemic levels, up a massive 14 points to 72. The golden age for the sector is just beginning as Millennials working in tech move to the burbs where the home office rules. Lumber is in short supply, thanks to Trump's tariffs with Canada, so prices just hit a two-year high. Keep buying.

We may get our fifth stimulus bill next week, as the Senate attempts to protect corporations from Covid-19 liability. Almost all of the $3 trillion in stimulus so far has ended up in the stock market, and another trillion can only be bullish.

Moderna claimed success with a true Covid vaccine, with 100% results in a 45-person human trial. (MRNA) soared by 15% on the news. A late July trial will involve 30,000. The company has never produced a product before using its RNA technology. Keep buying biotechs on dips. I’m long (SGEN), (ILMN), and (REGN). Dow futures up 300 in Asia on the news.

US air travel was down 89% in May, YOY. Whatever recovery you’re seeing in the economy it’s not happening here. I’m 200,000 miles a year guy and I probably won’t go near a plane until 2022. Avoid all airline stocks on pain of death. There are much better fish to fry.

Apple won a European antitrust case big time, ducking a massive 14.4 billion fine. Stock was up $7 on the news and is rapidly approaching my two-year target of $400. It's yet another case of “not invented here.” European regulators jealous of American success constantly assault US big tech. They view it as just another cost of doing business.

US budget deficit soared to $867 billion in June, taking it to an unprecedented $10.4 trillion annual rate. The national debt will rocket by 50% this year. Your grandkids are going to have a monster bill to pay. Keep selling every rally in the US dollar (UUP) and the bond market (TLT) and buy gold (GLD).

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

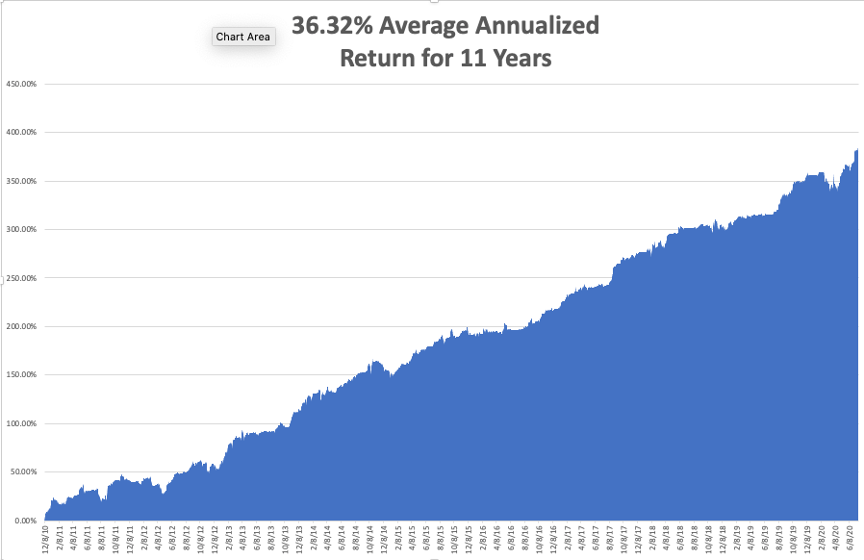

My Global Trading Dispatch enjoyed another sizzling week, up a red hot +2.73%. My eleven-year performance rocketed to a new all-time high of 384.54%. A triple weighting in biotech did the heavy lifting. A four-day short position in the bond market (TLT) was the icing on the cake.

That takes my 2020 YTD return up to an enviable +28.63%. This compares to a loss for the Dow Average of -6.2%, up from -37% on March 23. My trailing one-year return popped back up to a record 68.19%, also THE HIGHEST IN THE 13 YEAR HISTORY of the Mad Hedge Fund Trader. My eleven-year average annualized profit recovered to a record +36.32%, another new high.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here. It’s jobs week and we should see an onslaught of truly awful numbers.

On Monday, July 20, IBM (IBM) reports Q2 earnings.

On Tuesday, July 21 at 7:30 AM EST, the June Chicago Fed National Activity Index is released. Microsoft (MSFT), Tesla (TSLA), and Lockheed Martin (LMT) report earnings.

On Wednesday, July 22, at 7:30 AM EST, the all-important Existing Home Sales for June are published. Amazon (AMZN) and Thermo Fisher Scientific (TMO) report earnings. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, July 23 at 8:30 AM EST, the frightful Weekly Jobless Claims are announced. American Airlines (AA) report.

On Friday, June 24, at 7:30 AM EST, the New Home Sales for June are published. The Baker Hughes Rig Count is out at 2:00 PM EST. Verizon (VZ) reports earnings.

As for me, I have been going down memory lane looking at my old travel photos because that’s all I can do in quarantine.

I am now banned in Europe.

So are you for that matter. In fact, there are very few countries in the world that will accept an American visitor. With the world’s highest Covid-19 infection, rates we are just too dangerous to have around. This is tough news for a guy who usually travels around the world once or twice a year.

It’s not the first time I have been banned from a country.

During the 1980s, The Economist magazine of London sent me to investigate the remote country of Nauru, one-half degree south of the equator in the middle of the Pacific Ocean. They had the world’s highest per capita income due to the fact that the island was entirely composed of valuable bird guano.

During an interview with the president, I managed to steal a top-secret copy of the national budget. I discovered that the president’s wife had been commandeering aircraft from Air Nauru to go on lavish shopping expeditions in Sydney, Australia where she was blowing $200,000 a day, all at government expense.

It didn’t take long for missing budget to be found. I was arrested, put on trial, sentenced to death for espionage, and locked up to await my fate.

Then one morning, I was awoken by the rattling of keys. The editor of The Economist in London had made a call. I was placed in handcuffs and placed on the next plane out of the country. When I was seated next to an Australian passenger, he asked “Jees, what did you do mate, kill someone?” On arrival, I sent the story to the Australian papers (click here for the story).

I have not been back to Nauru since.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 17, 2020

Fiat Lux

Featured Trade:

(JULY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(EEM), (GLD), (GDX), (NEM), (GOLD), (UUP), (FXA), (FXE), (FXY), (AMZN), (AAPL), (GOOGL), (FB), (BIDU), (TLT), (TBT), (IBB), (ROM)

Below please find subscribers’ Q&A for the July 15 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you expect foreign equities to begin to outperform US equities sometime soon?

A: I expect them to outperform imminently simply because Europe did their shutdown properly, a total shutdown, and got rid of the virus, so their economy and schools are opening. We did a partial shutdown, some states did not shut down at all, and as a result, the epidemic is on fire here, and our shutdown will have to last an extra six months to a year. So that means you’ll probably want to be rotating out of US stocks and into emerging stocks, and the (EEM) is the ETF to go with there.

Q: Would you buy gold LEAPS at this point?

A: Normally, I say only buy LEAPS on capitulation selloffs like we had in March. We actually put out 25 LEAP recommendations on the long side in tech and biotech in March and they all proved spectacular winners. However, at this point, gold is just short of an all-time high; if you break the high you could get a $500 or $1,000 move very quickly to the upside. If you want to do LEAPS, I would go out one year, I would go fairly close to the money, something like a $200-$210 LEAP in the (GLD) ETF. Your much bigger bang, by the way, would be to do LEAPS on the individual stocks; go 10% or 20% out of the money, you might make 100%-200% on those and the stocks to do there would be Newmont Mining (NEM) and Barrick Gold (GOLD).

Q: Would the US or any other country consider backing their currency with gold?

A: Absolutely not. We went off the gold standard in 1972 for a reason. That’s because they're not making it anymore; there isn't enough gold to support growth in a global economy. On the other hand, a supply of paper is unlimited, and that's why we've had such terrific economic growth since we’ve gone off the gold standard.

Q: I’m seeing some really great deals in energy. Should I get involved?

A: Absolutely not. Don’t confuse “gone down a lot” with “cheap.” We think the oil business is long term going out of business. It can't compete with alternatives and electric cars; the economics for investing in a non-scalable energy form just are not there. It’s like asking an analog adding machine to compete with a computer.

Q: Is it too late to sell the US dollar or the Invesco DB US Dollar Index Bullish Fund ETF (UUP)?

A: No, we’re only in the very early stages of the collapse of the US dollar, so you want to be buying all of the nondollar ETFs like the Australian dollar (FXA), the euro (FXE), and the Japanese yen (FXY). Massive over issuance of currency will destroy its value, that’s one of the seminal lessons of currency markets. The US is not immune to that.

Q: Biotech is getting overheated here—should I buy the rumor, sell the news?

A: We’re also just in the opening stages of the biotech golden age. Even if they cure corona tomorrow, there are another 100 diseases they will cure over the next 10 years using all of the new advanced technology that has just been developed, like gene editing, monoclonal antibodies, and quantum computers. It’s another reason to subscribe to the Mad Hedge Biotech and Healthcare Letter for $1,500 a year (click here).

Q: I see Bill Gross is bullish on value stocks—would you go with that view?

A: No, leave the value stocks for Bill Gross. He's semi-retired and hasn’t been as good on the stock market lately as he used to be, as much as he is a dear friend. This is a chasing-a-winner type market. I would wait for value stocks. You could die a long horrible death by the time value stocks turn around so I would avoid them. Go for earnings growth, that’s the only thing that counts in the future.

Q: What would you recommend as a portfolio starter?

A: I would recommend 100% cash. I know you don’t want to hear that you should keep cash if you just bought an expensive trade alert service, but the fact is the risk now is the highest it’s been in years. I only add new trade at market sweet spots, and you don’t get those every day of the year. I will send you an alert if I see a low-risk high-return trade. Wait for the summer correction—that will set up another bet-the-ranch opportunity. Don’t worry about trade alerts, we’ll be doing about 400 of them this year, but they do tend to come in bunches at market bottoms and market tops.

Q: Do American companies have much of a chance against Chinese tech?

A: The US has an overwhelming lead, which will probably increase at an exponential rate. I think the threat of Chinese tech is vastly overstated by the administration. They needed an enemy to protect us from to stick around. The reality is that the US is so far ahead it’s unbelievable; that’s the reason they steal our technology. And they only have leads in very specific areas, such as surveillance of large populations. I wouldn’t worry too much about tech—if the Chinese really had a lead on tech, would Amazon (AMZN), Apple (AAPL), Alphabet (GOOGL), Facebook (FB) all be going to new highs every day, while Baidu (BIDU) lagged?

Q: Should we close out the Regeneron call spread?

A: At this point, we’re so far in the money I would just wait two more days and it will expire at its maximum $10 value, and you can avoid all the fees. You’ll end up making $1,600 or 16.28% 15 trading days.

Q: Presidential candidate Joe Biden has just had a huge surge in the polls in battleground states. Will he be damaging to the market?

A: No, ever since he started his rise in the polls, the stock market has been rising almost every day, and that’s even after announcing in advance that he’s going to raise corporate taxes from 21% to 28%. He’s also going to eliminate the carried interest, which should have been eliminated a long time ago. I imagine there will be some super punitive Roosevelt style 90% tax on net taxable income over a billion dollars—a real billionaire’s punishment tax, as they’ve basically made all the money for the last 30 years. The stock market is voting with confidence for the future Biden government, who am I to disagree? The market is always right.

Q: Will gold hit a new high?

A: Yes, I think we will have a new high in a couple of weeks. That's why I said it’s a rare case when you actually buy LEAPS in a rising market, especially if you go one or two years out. Guess where gold will be in two years? My bet is $3,000, so a $200/$210 LEAP in the (GLD) could bring in a 1,000% return, The overwhelming fundamentals are in favor of gold. I'll keep hammering away at that in the newsletter.

Q: I only trade stocks; how can I take advantage of your recommendations?

A: First of all, buy the stocks. Second, you can buy stocks on margin, which gives you double exposure. Third, there are many 2X ETFs on the stocks or sectors we recommend, like the (TBT), which you can also trade in a stock account. For example, for biotech, you can get your exposure there through the (IBB), and through tech, you can buy the 2X (ROM); but I wouldn’t buy it today because it is too high. In fact, only about 25% of our followers do options, the rest trade stocks or use it to manage their own long-term portfolios.

Q: Will we hit 0% yielding US Treasuries (TLT)?

A: Probably not, that move is behind us. We got down to a 31 basis points yield at the lows. Now, massive oversupply from the US government will be the primary factor dictating Treasury prices, and that means going down a lot.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 13, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COME HERD IMMUNITY),

(INDU), (TSLA), (SPY), (GLD), (JPM), (IBB), (QQQ), (AAPL), (MSFT), (DCUE), (NVDA)

The US passed a single-day record of 70,000 new cases for Covid-19 over the weekend, with Florida bringing in an astounding 15,300.

We missed a chance to stop the epidemic in January because we were blind. Then we missed again in April because we were lazy, when New York City was losing nearly 1,000 souls a day and ignored the lessons therein.

So, we relentlessly continue our march towards herd immunity, when two-third of the population gets the disease, protecting the remaining one third. That’s about a year off.

That implies total American deaths will reach 2.2 million, more than we have lost from all our wars combined.

The faster people die, the closer we are to the end of the plague, which is good news for everyone.

And the stock market keeps going up every day, the worse the news, the faster. That may be happening because the more severe the shock to the system, the faster companies must evolve to survive, making them ever more profitable.

Out with the Old America, in with the new. The future is happening fast.

We here at Mad Hedge Fund Trader have just delivered the most astonishing quarter in our 13-year record, up some 41.98% from the March 16 low.

That makes me cautious. Things never stay that good for long. Just because I can’t see the next black swan doesn’t mean it isn’t going to happen.

If stocks rise when corona cases are exploding, what do they do when cases fall? Do they fall too, or do they rise even faster?

That’s above my pay grade. I’m only a captain, not a general.

So, I will be moving to a 100% cash position in coming days and then let the next black swan tell me what to do. If we suffer a severe dive, and 10%-20% is entirely possible, then I’ll jump back in with my “BUY” hat on. That means testing the lower up of my six-month (SPX) 2,700-$3,200 range.

If we suddenly surge to far greater heights and new all-time highs, then I will be selling short as fast as I can write the trade alerts.

In the meantime, we have Q2 earnings to look forward to in the coming week, which will certainly be one for the history books. The bullish view is that they will be down only 44% from a dismal Q1. The bearish view is far worse. Banks (JPM) kick off on Tuesday.

NASDAQ (QQQ) hit a new high at 10,622, with Apple (AAPL) and Microsoft (MSFT) leading the charge. Elon Musk is now looking at another $1.7 billion payday with his shares touching $1,500. I’m moving to 100% cash, peeling off one profitable position a day as each option play reaches its maximum profit. I just had the best quarter in a decade, up an eye-popping 40%, and I’m just not that smart to keep it going. Humility always wins in the long-term.

Goldman Sachs chopped its growth forecast in the face of soaring Covid-19 cases, paring their Q3 prediction from +33% to +25%. Political campaign rallies are spreading the disease faster than expected. Q1 most likely came in at negative -5%. Expect worse to come. If the stock market can’t break at 135,000 corona deaths, it will at 260,000 or 520,000, which is certainly coming.

NVIDIA topped Intel as most valuable chip company. No surprise here. High-end graphics cards are worth a lot more money than plain commodity processors. Keep buying dips on (NVDA) which we’ve been loading the boat with now for four years. There’s an easy double from here.

Warren Buffet bought Dominion Energy (DCUE), in one of the only distressed sales available this year, thanks so much to government support. With natural gas prices at all-time lows, the big boys are throwing in the towel. Immense public pressure is forcing public utilities to abandon fossil fuels. Warren will sell all of his newfound energy in the $10 billion deal to China. It’s the beginning of the end for carbon. Buy (TSLA) on dips.

Dividend Cuts will drive stock trading in H2. Energy, airline, cruise lines, casinos, movie theaters, and hotels are most at risk, while big technology companies like Apple are the safest. Currently, the S&P 500 is yielding 2.0%, while the ten-year US Treasury bond is paying out 0.65%. Room for a cut?

Tesla to reach $100 billion in annual revenue by 2025, says San Francisco-based JMP Securities. The logic goes that if they can produce 90,000 vehicles a quarter during a pandemic, 140,000 a quarter should be no problem by yearend. The news delivered a move in the shares to a new all-time high of $1,549. Inclusion of (TSLA) in the S&P 500 would also deliver a lot of forced institutional buying, which might take the shares up 40% more. The future is happening fast. Keep buying (TSLA) on dips for a 2021 target of $2,500. If this keeps up, we may see it next week. Remember, I traded Tokyo in 1989. Nothing is impossible.

US student visas were canceled in ostensibly an administration coronavirus-fighting measure, but really in the umpteenth measure to shut foreigners out. “America first” is turning into “America only.” Midwestern schools in particular will be hurt by the loss of 400,000 full tuition-paying international students, especially when state education budgets are getting cut to the bone. That’s down from 800,000 three years ago. If they’re already here, how does this help us? Most colleges are moving to online-only models to limit infections.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch enjoyed another blockbuster week, up an astounding +2.28. It was a week when everything worked in the extreme….again.

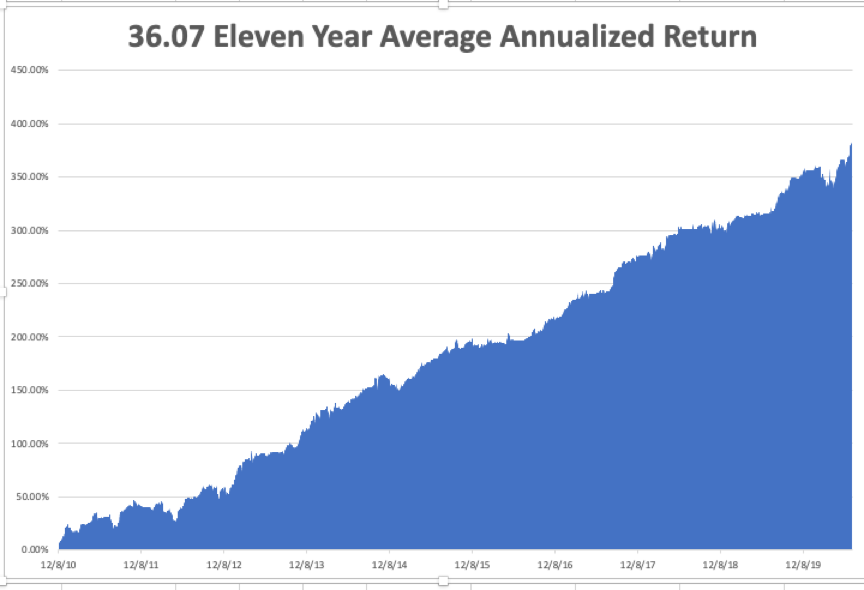

My eleven-year performance rocketed to a new all-time high of 381.74%. A triple weighting in biotech and a double weighting in gold were a big help. A foray into the banks proved immediately successful. I seem to have the Midas touch these days.

That takes my 2020 YTD return up to an industry-beating +25.83%. This compares to a loss for the Dow Average of -8.8%, up from -37% on March 23. My trailing one-year return popped back up to a record 66.22%, also THE HIGHEST IN THE 13-YEAR HISTORY of the Mad Hedge Fund Trader. My eleven-year average annualized profit recovered to a record +36.07%, another new high.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here. It’s jobs week and we should see an onslaught of truly awful numbers.

On Monday, July 13 at 10:00 AM EST, the June Inflation Expectations are out.

On Tuesday, July 14 at 7:30 AM EST, US Core Inflation for June is published

On Wednesday, July 15, at 7:30 AM EST, US Industrial Production for June is announced. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, June 16 at 8:30 AM EST, Weekly Jobless Claims are announced. At 7:30 AM, US Retail Sales for June is printed.

On Friday, June 17, at 7:30 AM EST, the US Housing Starts for June are released.

The Baker Hughes Rig Count is out at 2:00 PM EST.

As for me, I am training hard for my upcoming 50-mile hike with the Boy Scouts, knocking off 10 miles a day at 9,000 feet on the Tahoe Rim Trail. I have to confess that I’m feeling the knees like never before.

As they used to say in the Marine Corps, “Pain is fear leaving the body.” More than knowledge comes with age. Pain is there as well.

Marine Corps to Boy Scout leader. It’s been a full life.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

July 7, 2020

Fiat Lux

Featured Trade:

(JULY 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (VIX), (TLT), (GLD), (IBB), (QQQ), (SPY), (NEM)

(TESTIMONIAL)

Below please find subscribers’ Q&A for the July 1 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: You obviously do well with deep-in-the-money call and put spreads, but I struggle to get your prices.

A: Raise the strike prices or raise the price that you’re bidding for them closer to my limit. It’s really hard to keep current prices in this market with such extreme volatility (VIX), especially when you’re having melt-ups going on in Tesla (TSLA) and so on. Our trade alerts are just a starting point to get you going in the right direction in the right stock. The people who make the most money with the trade alert service are those who use my market timing to buy futures, either at the money risk reversals on stocks (long the call and short the put), or outright futures in gold (GLD), currencies (FXE), and bonds (TLT).

Q: How high can Tesla go?

A: My immediate target is $1200 (which has already been hit), and the rumors I'm hearing is that they will be good if you factor in the two months that the Fremont factory was closed. And after that, it’s $2,500 and then there's Ron Baron’s target of $5,000, who’s been in the stock himself since it was at $100 a share. Ron was a little late in finding my research on the company. I first got in at $16.50 after I toured the Fremont factory.

Q: Is it possible there will be a national mandate to wear masks, which could boost stocks?

A: Not under this president. Do not expect help from this administration on this pandemic. They've figured out they can’t beat it so they are just walking away and leaving the states to figure out what they can. You’ll have to wait for another president to get a national mask mandate if we’re still alive by that time. I am getting a lot of emails from Europe complaining that the United States is extending the pandemic by having so many people refusing to wear masks here or admit that the disease even exists. They are horrified.

Q: What do you think about the biotech ETF (IBB)?

A: I’d be buying it with both hands. Even without the pandemic, a new bull market started last September in biotech because the fundamentals long term were fantastic. But you had to be a scientist to see it back then. They really had the highest earnings growth with the lowest price earnings multiples in the entire stock market. The pandemic just gave it a supercharger. That’s why I started the Mad Hedge Biotech & Healthcare Letter (click here).

Q: Which ETF should I use for biotech?

A: The iShares NASDAQ Biotechnology ETF (IBB). It's a basket of the top 20 global biotech firms but will underperform single biotech stock picks by half, as any basket does.

Q: What about the long-term portfolio?

A: I will get to it. It seems like our long-term portfolio is changing every week, so it’s difficult to really look at anything in the long term. These days, long term is a week with all the volatility we’re getting. I imagine I’d be getting rid of any energy stocks on this rally though. I see oil going back to zero.

Q: You say stay long NASDAQ (QQQ) and short S&P 500 (SPY) for the rest of the year, but you project new highs for the S&P 500?

A: Yes, both can go up, but NASDAQ will go up faster, and that’s what hedge funds are doing. That gives you a market neutral position, sucks a lot of the risk out of that position, and it’s even crash-proof as we saw in the winter when the markets were melting down. And like hedge funds, you can leverage that up 5 or 10 times. So yes, that trade will work all day long, even if both indexes go to new highs. I imagine NASDAQ will outperform on the upside relative to SPY by a factor of two or three to one.

Q: Is there a good substitute to use versus your deep-in-the-money alerts if you have a smaller account?

A: You can just buy the stocks. Or, you can just buy the stocks on margin, which is 2 to 1—50% margin requirement there. There are many ways to skin a cat. The call spreads actually give you the most bang per buck because you get a lot of leverage with a small dollar amount upfront and limited risk.

Q: I heard that hedge funds have huge shorts. Is this setting up another short squeeze? Will they eventually be right?

A: Yes, that may have been what happened on Monday and Tuesday, a squeeze on the shorts driving prices much higher. They will eventually be right a little bit, but you’re certainly not going to get the major declines we saw in February/March because of all the QE and government support. The pandemic is no longer a surprise.

Q: Will COVID-19 fears keep volatility elevated until there is a vaccine?

A: Absolutely, yes. That’s great news for our options strategy, which is why we’re 100% invested almost all the time these days because higher volatility doubles the premiums you get for options. My current strategy is that once a position hits 90% of its maximum profit, I dump it and put on another position to take in an extra $1,500-$2,000. I did that with Tesla and gold (GLD) last week. This is the golden age of the in-the-money put and call spread strategy and we are better at executing it than anyone else.

Q: What do you have to say about the jobs report?

A: The entire US economic data system is breaking down because we’re seeing such immense swings month to month. Reporting lags are getting amplified one hundredfold. The June Nonfarm Payroll Report showed an increase of 4.8 million jobs and an unemployment rate of only 11.1% (I never thought I’d ever say “only 11.1%”). However, the state jobless claims are indicating an unemployment rate of at least 22%. Go walk down the Main Street of any town and you’ll see that the state figures are right. All the forecasting is relatively pointless. How can we get a fall in unemployment when nothing is open?

Q: Are you recording this webinar?

A: Yes, we usually post the recorded webinar on the site 2 hours after we finish so our many international subscribers don’t have to stay up until the middle of the night to watch it. That’s how long it takes to convert the webinar into a video format we can post online.

Q: When setting up LEAPS (Long Term Equity Participation Securities), do you buy straight calls at-the-money or in-the-money?

A: You buy deep, out-of-the-money spreads. Let's say you bought a (TSLA) $1,500/$1,550 deep-in-the-money call spread, and it expires at the maximum profit point with the stock over $1,550. You’ll make about a 500% return on that because it’s so far out of the money; the leverage is enormous. Will Tesla close over $1,550 in two years? Probably.

Q: How do I get into Tesla?

A: Close your eyes and buy at market, and hope we get $1,200 tomorrow on great Q2 sales numbers. Or, wait for another one of these huge selloffs—Tesla does have a history of selling off 50% at any given time, and then you go into a LEAPS there and get a 500% return. Most investors prefer the latter if they know about LEAPS. Remember, our last “BUY” into Tesla was a year ago when the stock was at $180. By the way, a lot of the shorts in Tesla stock were financed by big oil money and when oil crashed, they lost the ability to post more margin. So, they were forced to cover their shorts at gigantic losses, creating this super spike in the share price. Elon Musk, who owns 20% of the company, is laughing all the way to the bank.

Q: How do we pick the best strike prices for long-term LEAPS?

A: Go 30% out-of-the-money. There you get your 500% return. If you really want to be aggressive and you think the stock has 50% of upside, then go 50% out-of-the-money. There your return will be about a 1,000% profit over 2 years.

Q: How long are these trades for? I haven’t received any trade alerts.

A: Please contact customer support and we’ll find out if they are being filtered out by your spam folder. Global Trading Dispatch is sending out trade alerts virtually every day for all asset classes, so you should have received several of them by now. The Mad Hedge Technology Letter sends out fewer because they are confined to a narrow part of the market.

Q: What is your favorite stock in the gold space?

A: Newmont Mining (NEM). They have the strongest balance sheet of the major gold companies because they engage in fewer takeovers than the other big gold companies.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 25, 2020

Fiat Lux

Featured Trade:

(5 REASONS GOLD IS GOING TO A NEW HIGH),

(GLD), (GOLD), (NEM), (GDX)

Global Market Comments

June 17, 2020

Fiat Lux

Featured Trade:

(THE SECRET FED PLAN TO BUY GOLD),

(GLD), (GDX), (PALL), (PPLT),

(TESTIMONIAL)