Global Market Comments

April 14, 2020

Fiat Lux

Featured Trade:

(APRIL 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (SPY), (SDS), (BA), (VIX), (VXX), (GLD), (GDX),

(GOLD), (NEM), (QCOM), (HYG), (JNK)

(WHY SENIORS NEVER CHANGE THEIR PASSWORDS)

Global Market Comments

April 14, 2020

Fiat Lux

Featured Trade:

(APRIL 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (SPY), (SDS), (BA), (VIX), (VXX), (GLD), (GDX),

(GOLD), (NEM), (QCOM), (HYG), (JNK)

(WHY SENIORS NEVER CHANGE THEIR PASSWORDS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 8 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Is it premature to be buying long-term LEAPS?

A: Absolutely not—a long-term leap is a bet that your stock will recover beyond your strike prices in two years, which I certainly believe is the case with all of the quality tech and biotech names. These are pretty illiquid so the only way to get a good price is to have a bid in place on one of those absolute puke out days. You will never buy these at the bottom.

Q: Do you see a rally in the stock market in the fourth quarter of this year after the election?

A: For sure—we should be well clear of the pandemic by then, and all of the $6 trillion stimulus will be hitting at the same time.

Q: With the rally in the S&P 500, would you double up on the (SPY) put spread—the May $300-$310?

A: No, keeping your leveraged positions small is crucial in this kind of environment, and the big short play is basically behind us. Better to add the 2X ProShares Ultra Short S&P 500 (SDS) to catch a smaller move down.

Q: Will gold work if the market sells off as a safety trade?

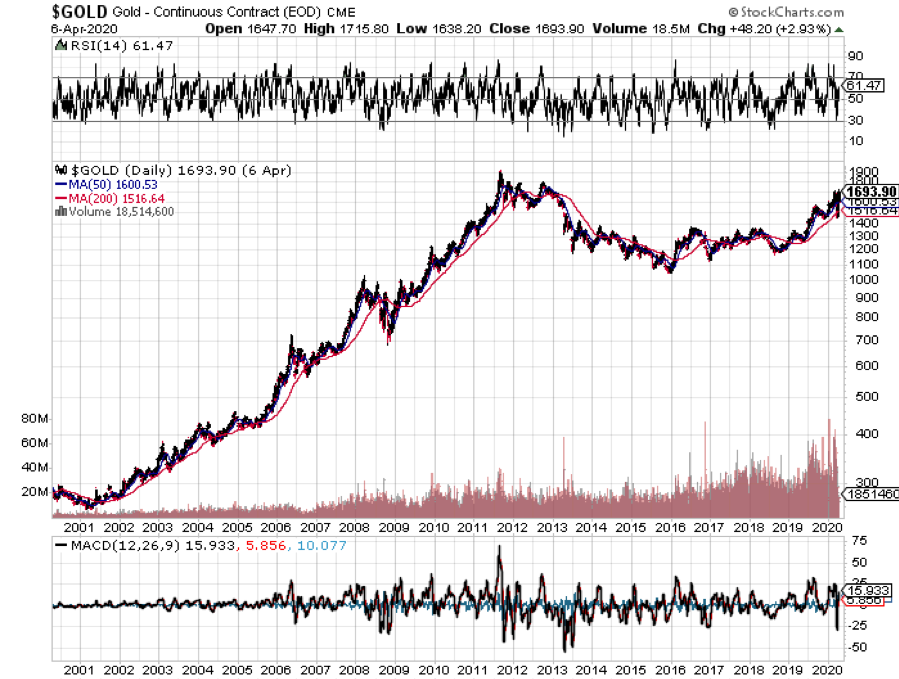

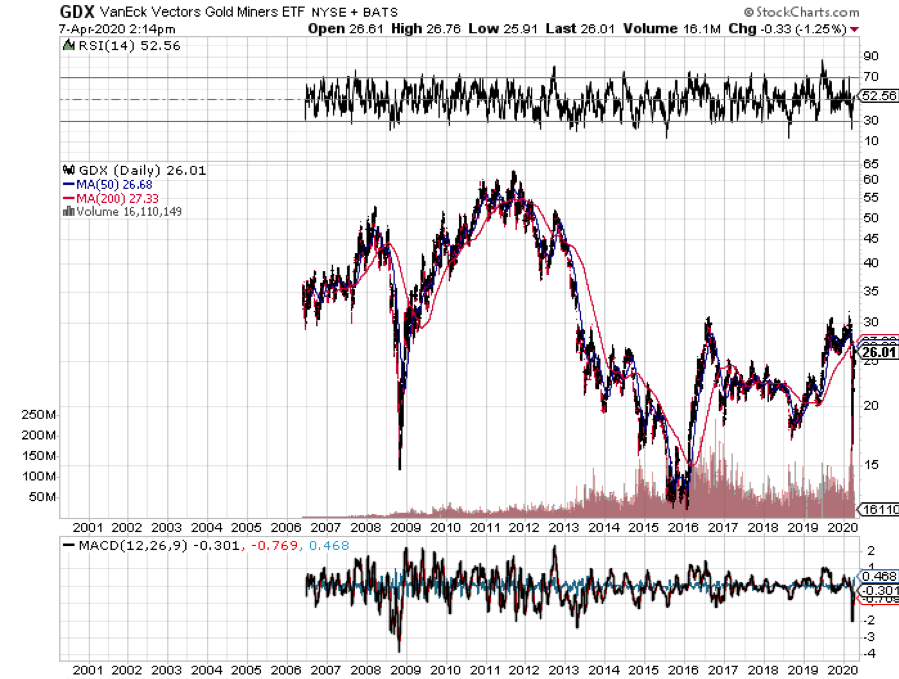

A: Yes, it will. Gold (GLD) had that big 15% selloff a couple of weeks ago when it looked like all financial markets worldwide were going to completely freeze up, and everyone got margin calls all at the same time. We are clear of that now and I expect gold and other traditional hedges like shorting volatility, for example, to also work as a hedge. Gold is going to a new all-time high soon. Buy (GLD), (GDX), (GOLD), and (NEM).

Q: When do you think international borders will open up again, and will that have a positive effect on the economy?

A: Absolutely. You can expect the market to rally 10% into the opening of borders, and then another 10% afterwards depending on where the starting point for the market is in that. As for timing, they may open up in June, and then close up in again in the fall when a second Corona wave hits.

Q: Will you teach us how to buy LEAPS?

A: Just go to my website, type in LEAPS in all caps, and everything you need to know about leaps is there. I will also be following up soon with more individual stock LEAPS ideas, but I don’t want to put them out now because we have just had a $5,000-point rally on the Dow.

Q: Please talk about 5G.

A: The best play is Qualcomm (QCOM). They have a near-monopoly on a 5G chip which virtually the entire world has to buy. The stock has also held up incredibly well. Buy two-year LEAPS on Qualcomm with probably a $90 or $100 strike price.

Q: What level in the S&P do you think this will fail?

A: I think it will fail right around here, so that's why I have been adding on the short positions on every rally. We are exactly at halfway point between the February high and the March low, which is a perfect bear market rally.

Q: What’s the definition of the next big dip?

A: You give up the 5000-point rally we just had, and whether we give up 4000 or 6000 of it, at these kinds of conditions, 1000 points in the Dow (INDU) is a round lot, like the daily move. So, looking at the charts and these lows, it could be a $19,000, $18,000, or $17,000.

Q: Fundamentals may tell you the virus may be peaking, but the worst of the economy is yet to come.

A: True. Do all the markets follow fundamentals now? No, they will look at the virus numbers. Economic numbers are utterly meaningless and out of date here. I wouldn’t depend on them at all, just look at the new cases every day from the Johns Hopkins website, and that gives you a better buy signal than any economic indicator can.

Q: Are all the good shorts are over?

A: When I say shorts are over, from here you’re not going to get the 80% and 90% down moves that we have seen so far; those are gone. The reason I bought the 2X ProShares Ultra Short S&P 500 (SDS) is to play for the bottom end of the range, which could be down 2000 to 4000 points from here, and also to hedge the short volatility (VXX) puts that I already have. A rising market should make the (VXX) go down, and a falling market will make the (VXX) and the (SDS) go up. So, it's both a hedge and a view on a range of a market.

Q: Could the Federal Reserve buy shares?

A: Yes, they have done that already in Japan, with no success whatsoever in helping the economy, but I doubt the Fed will buy shares here. The government will take minority share ownerships in the troubled industries like the airlines, much like they did with (GM) and the top 20 banks during the 2008-09 crash and sell them later at huge profits. I don't expect them to go beyond that. The Fed here has too many other things to buy, like all of our different bond and money markets; those don't exist in other countries like Japan or Europe. Stocks are often the only thing they can buy, and in Japan’s case, they already own the entire government bond market, so they had nothing else left to buy besides stocks.

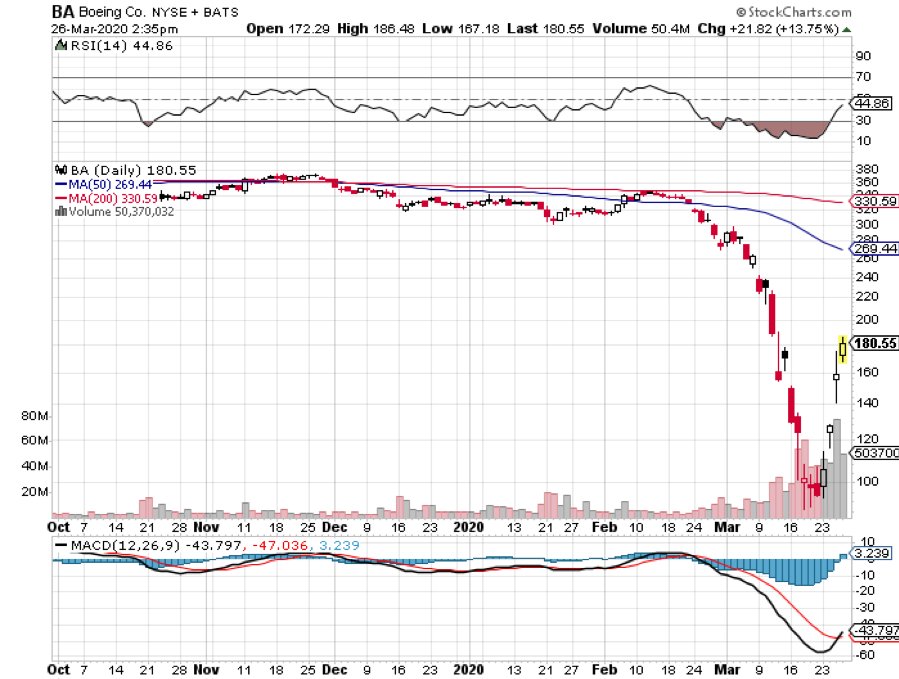

Q: How about buying Boeing (BA)?

A: I would buy Boeing LEAPS here, something like a $170-$180. If you’re going to make a 1,000% return on LEAPS on any one stock, it's going to be Boeing. That company will be around somehow, and you could get literally a 10-fold return just by going 50% out of the money on two-year LEAPS.

Q: How is liquidity on 2-year 30% out of the money LEAPS?

A: It is practically nonexistent. You have to put in a limit order and then wait for a dump in the market to get filled. That’s how all the people who have been doing LEAPS have been getting them. Put in a bid and when you get these cataclysmic, down-1,000-point days, they hit any bid. The algos go in there and they just say hit any bid, and you can get done at incredible prices in those situations.

Q: Are the fees on (SDS) a problem?

A: No, your standard equity commission is all you should be paying. They trade like water.

Q: Would you short junk bonds short-term?

A: No, because you short the (HYG) or the (JNK), you are shorting a 7.5% yield which you have to pay if you’re short, so the great short in junk bond play was in February when it was yielding 4.5%. It’s too late now.

Q: Will treasuries go to zero?

A: They could, but we’re close enough to zero where you might as well think of them at zero.

Stay healthy all.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 13, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE BEAR MARKET RALLY IS OVER),

(INDU), (SPX), (TLT), (VIX, (VXX), (GLD), (JPM), (AMZN), (MSFT)

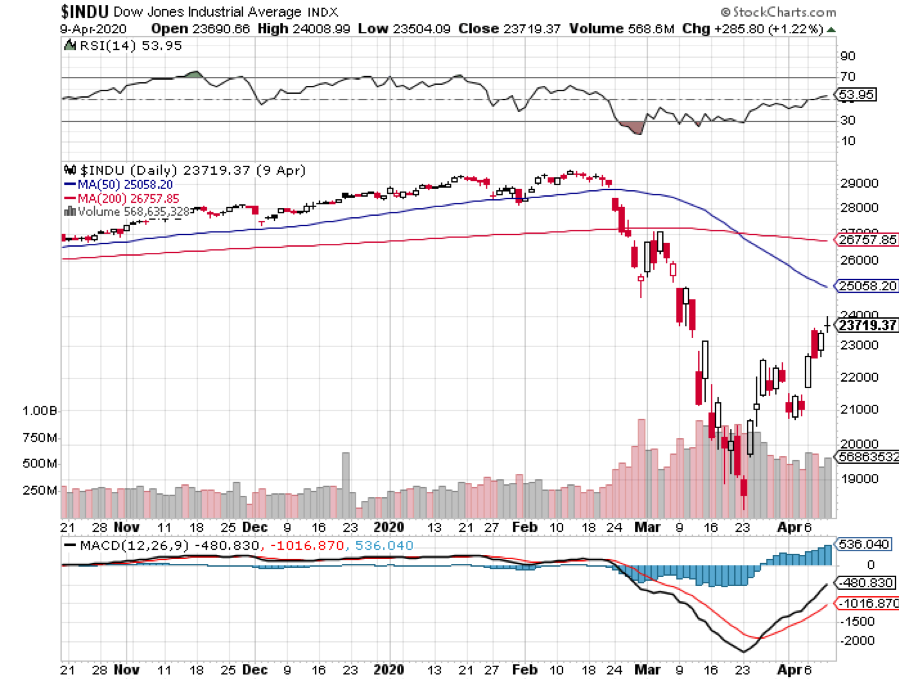

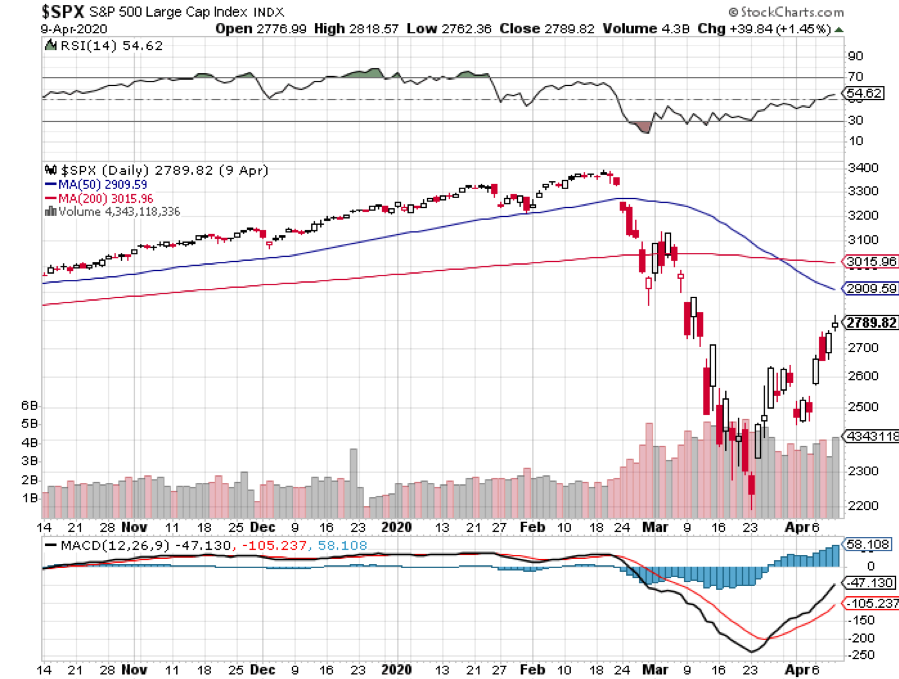

The Bear market rally is over, or at least that’s what Asian stock futures are screaming at us, and the shorts are piling back on….again.

For the first time in 16 years, I did not have to get up at 6:00 AM to hide Easter eggs. It’s not because my kids don’t believe in the Easter Bunny anymore. They’ll believe in anything that delivers them a free chocolate bunny. It’s because I couldn’t get any eggs. Much of the country’s egg production is being diverted into vaccine production for testing, of which, along with antivirals, there are more than 300 worldwide.

Enough of the happy talk.

It was a classic bear market rally we saw over the past two weeks in every way, retracing 50% of the loss this year. Junk stocks, like hotels, airlines, and cruise lines led, while quality big tech lagged. That’s the exact opposite of what you want to see for a new bull market.

At the Friday high, the Dow (IND) was down only 17% from the February all-time high at a two-decade 20X valuation high.

The US is now losing 2,000 citizens a day to the Coronavirus. That’s how many we lost at the peak of the Vietnam War in a month. We are suffering another 9/11 every day of the week.

More than 16.8 million have lost jobs in three weeks, more than all those gained in six years. Of all American companies with fewer than 500 employees, 54% have closed! JP Morgan (JPM) has just cut its forecast for Q2 GDP from a 25% loss to an end of world 40% decline on an annualized bases.

New York is losing 800 people a day and is burying many of them in mass graves. Bread lines have formed in countless major cities. And you think 17% is enough for a discount for stocks, given that a near-total shutdown will continue for another five weeks?

Are you out of your freaking mind?

Which leads me to believe that another retest in the lows is in the work, no matter how much government money is headed our way.

For a start, it will be three months before the Fed handouts show any meaningful impact on the economy. Second, we are due for a second wave of the virus in the fall, once the initial shelter-in-place ends. Markets will likely behave the same.

In the meantime, long term analysts of the global economic structure are going dizzy with possible permanent changes. I am in the process of writing a couple of pieces on this if I can only get away from the market long enough to do so.

It seems like half the country has lost their jobs, while the other half are now working double time without pay, like myself.

The market was stunned by 6.1 million in Weekly Jobless Claims, taking the implied Unemployment Rate to over 14%, more than seen during the 2008-2009 Great Recession. One out of four Americans will lose their jobs or suffer a serious pay cut in the next two months. At this rate, we will top the Great Depression peak of 25 million in two weeks.

The Fed launched a second $2.3 trillion rescue program, this time lending to states, local municipalities, and buying oil industry junk bonds. More money was made available to small businesses. Jay Powell is redefining what it means to be a central bank, but no one is complaining. It was worth one 500-point rally in the Dow Average, which we have already given back. At this point, almost the entire country is living on welfare.

Stocks soared firefly on falling death rates. Chinese cases are falling after the border closed, Italy and Madrid are going flat, and San Francisco is looking good. There is still a massive, but extremely nervous bid under the market. I’m selling into this rally. We will continue to chop in a (SPX) $2180-$2800 range for the foreseeable future.

Trump says there’s a light at the end of the tunnel, but he doesn’t tell you that the light is an oncoming express train. At the very least, the number of deaths will rise at least tenfold from here. That’s how many we lost in the Korean War. It hasn’t even hit the unsheltered states in the Midwest yet.

Gold (GLD) is making a run another all-time highs, topping $1,700. Expect everyone’s favorite hedge to go ballistic. QE infinity and zero interest rates will eventually bring hyperinflation and render the US dollar worthless. Gold production is falling due to the virus. Anything else you need to know?

Mortgage defaults are up 18-fold. People can’t even get through to their banks to tell them they are not going to pay. This is the next financial crisis. Fannie Mae and Freddie Mac are going to go broke….again.

Can the US government spend money fast enough, given that it has been shrinking for three years? I’m not getting my check until September. It’s not easy to spend $2 trillion in a hurry. I can’t even spend a billion in a hurry. It’s darn hard and I’ve tried. It suggests any recovery will be slower and lasts longer.

Here’s the bearish view on the economy, with Barclay’s Bank looking for an “L” shaped recovery, which means no recovery at all. I’m looking more for a square root type recovery, which means a sharp bounce back to a lower rate of growth. And there may be two “square roots” back to back.

Bond giant PIMCO predicts 30% GDP loss in Q2 on an annualized basis. Everyone staying home doing jigsaw puzzles isn’t doing much for our economic growth. This may end up becoming the most positive forecast out there.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $20 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had a tough week, destroying my performance back to positive numbers for the year. That is thanks to my piling on the shorts in a steadily rising market. This brings short term pain, but medium-term ecstasy.

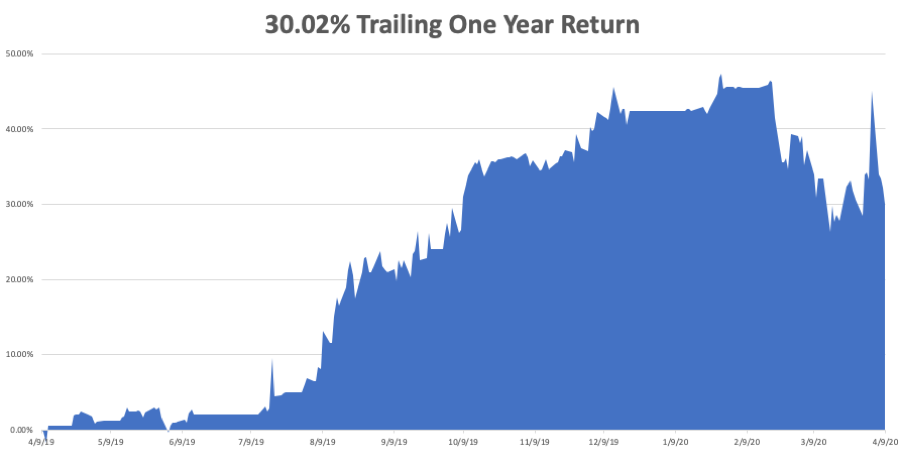

We are now down -3.99% in April, taking my 2020 YTD return down to -12.41%. That compares to an incredible loss for the Dow Average of -17% from the February top. My trailing one-year return sank to 30.02%. My ten-year average annualized profit was pared back to +33.51%.

My short volatility positions (VXX) were hammered even in a rising market, which means no one believes the rally, including me.

I took nice profits on two very deep in-the-money, very short dated call spreads in Amazon (AMZN) and Microsoft (MSFT), the two safest companies in the entire market, betting that we don’t go to new lows in the next nine trading days. As the market rose, I continued to add to my short position with the 2X ProShares Ultra Short S&P 500 (SDS).

This week, we get the first look at Q1 earnings. All economic data points will be out of date and utterly meaningless this week. The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, April 13 Citigroup (C) and JP Morgan (JPM) report earnings.

On Tuesday, April 14 at 11:30 AM, the API Crude Oil Stocks are announced.

On Wednesday, April 15, at 2:00 PM, the New York State Manufacturing Index is released.

On Thursday, April 16 at 8:30 AM, Weekly Jobless Claims are announced. The number could top 6,000,000 again. At 7:30 AM, US Housing Starts for March are published.

On Friday, April 17 at 7:30 AM, the Baker Hughes Rig Count is released at 2:00 PM. Expect these figures to crash as well.

As for me, before the market carnage of the coming week ensues, I shall be sitting down with my kids and touring the National Gallery of Art in Washington DC. Many art museums have now opened up their collections online, for free. There is a special exhibition of “Degas at the Opera.” Please enjoy by clicking here.

Next to come will be the Louvre in Paris (click here), and the National Museum of the Marine Corps in Triangle, VA (click here). I have them tracing the dog tags I brought back from Guadalcanal. I bet some of my old weapons are in there.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 8, 2020

Fiat Lux

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (GOLD), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

SPECIAL GOLD ISSUE

I have been bullish on gold (GLD) for the last three years and the payoff is finally here (click here).

How high could it really go?

The recent massive stimulus measures to fight the Coronavirus-induced depression is certainly bringing forward the rebirth of inflation. The Fed has just increased all of the $17 trillion quantitative easing created globally over the past decade by a staggering 50% in weeks!

This is hugely gold-friendly.

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now, we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it peaked in the summer of 2011, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant (click here).

The biggest buyers of gold in the world, Indian investors, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

You could also blame the China slowdown for the declining interest in the yellow metal, which is now in its sixth year of falling economic growth.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,300 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those giant six-foot high tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD) didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate as older mines carry costs that go all the way down to $600 an ounce.

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

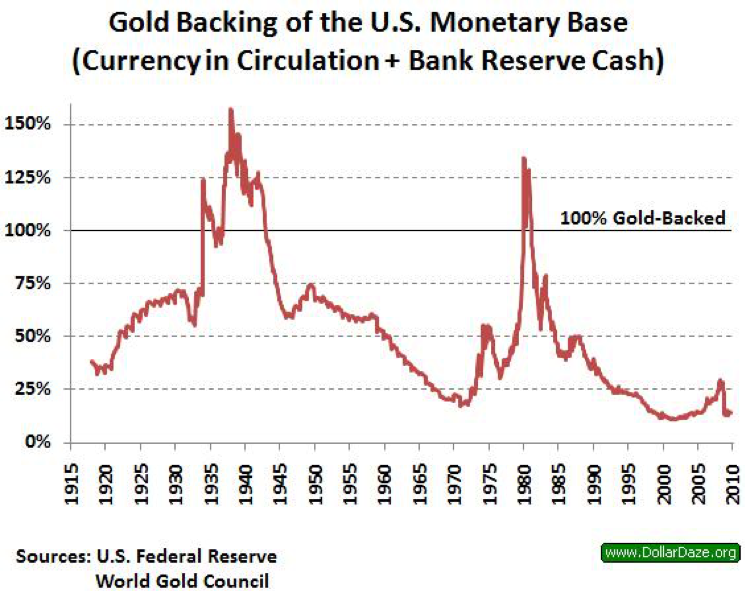

So, when the chart below popped up in my in-box showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce when the money supply was collapsing during the Great Depression and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten you interested yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980, to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and healthcare, but nowhere else. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid 2020s when shocking wage hikes spread elsewhere.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients other risk assets, good for you.

You’re finally learning!

Global Market Comments

March 27, 2020

Fiat Lux

Featured Trade:

(MARCH 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(ROM), (BA), (VIX), (UPRO), (SSO), (UBER), (LYFT), (MDT),

(GLD), (GOLD), (NEM), (GDX), (UGL)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 25 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Since we flipped the off button on the economy, I don’t see how we can simply flip the on button and have a V-shaped recovery. It seems much more unlikely that it will get back to pre-recession levels.

A: Actually, all we really need is confidence. Confident people can go outside and not get sick. Once we start seeing a dramatic decline in the number of new cases, the shelter-in-place orders may be cancelled, and we can go outside and go back to work. It’s really that simple. So, we will get an initial V-shaped recovery probably in the third quarter, and after that, it will be a slower return spread over several quarters to get back to normal. Everybody wants to get back to normal and let's face it, there's an enormous amount of deferred consumption going on. I have hardly spent any money myself other than what I’ve spent online. All of those purchases get deferred, so in the recovery, there's going to be a massive binge of entertainment, shopping, and travel that is all being pent up now—that will get unleashed once the airlines start flying again and the shelter-in-place orders are cancelled. We’re not losing so much of this growth, we’re just deferring it. Obviously, some of the growth is gone permanently; you can forget about any kind of vacation in the next couple of months. I would say, the great majority of consumption in the US—and thus growth and thus stock appreciation—is just being deferred, not cancelled outright.

Q: Other than the ProShares Ultra Technology ETF (ROM), do you have any other leveraged sectors coming into the recovery?

A: There is a 50/50 chance the Roaring 20s started 2 days ago, on Monday, March 23 at the afternoon lows. We may go back and test those lows one more time, which at this point is 3,700 points below here, but we are clocking 1,000 points a day. It doesn’t take much, like a bad non-farm payroll number, to go back and test those lows. The good news is out; they're not going to spend any more money other than the $10 trillion they're putting in now.

Q: Would you buy Boeing (BA) here? Is this the bottom?

A: The bottom was at $94 on Monday; we went up 100% in three days and now we’re at $180. Incredible moves, and a total lack of liquidity. One reason I haven't added any positions lately is that they have closed the New Yok Stock Exchange floor and its not clear that of I send out a trade alert, it could get done. We have gone totally online, so I just want to see what happens as a result of that. I don’t want to be putting out trade alerts that no one can get in or out of, heaven forbid.

Q: What do you mean by “The spike to $80 in the Volatility Index (VIX) was totally artificial?”

A: When you have a series of cascading shorts triggered by margin calls, that is artificial. I have seen this happen many times before, both on the upside and the downside. This happened twice in the (VIX) in the last two years. When you go from a (VIX) of $25 to $80 and back down to $39 in days, which is what we did, you know it was a one-time-only spike and we are not going to visit the $80 level again— at least not until the next financial crisis because those positions are gone and are never coming back. A (VIX) of $80 means we are going to have 1,000 point move in the Dow Average for the next 30 days.

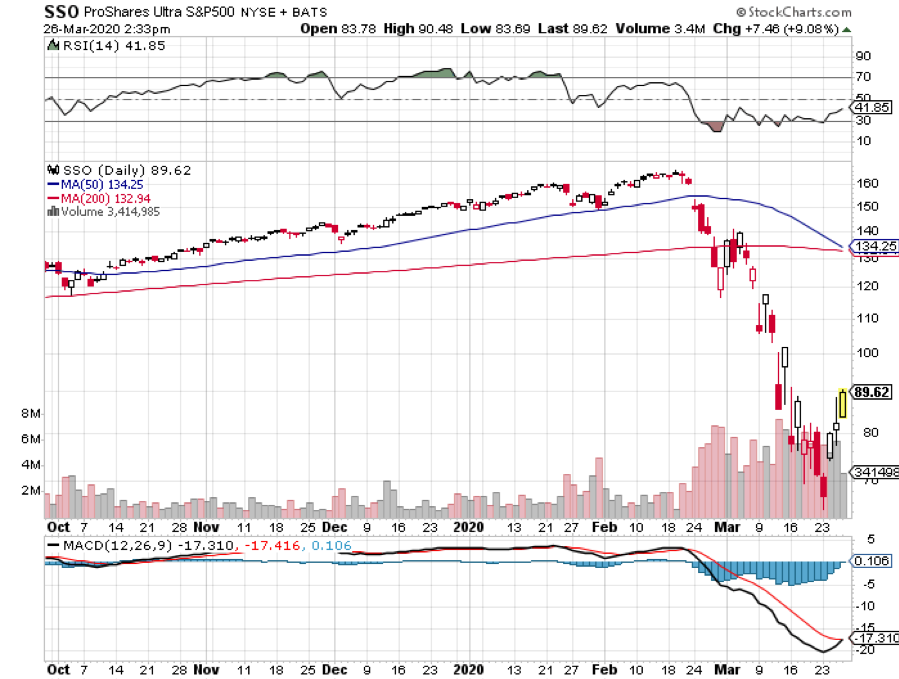

Q: I bought some ProShares Ultra Pro ETF (UPRO) which is the 3x long the S&P 500 at $1,829. Do I take profits by selling calls or just hold longer?

A: I would just sell the whole position outright. The (UPRO) is so incredibly volatile that you are rewarded heavily for just coming out completely and then reopening fresh positions on these big meltdown days. We will probably be doing trade alerts on (UPRO) or its cousin, the 2x long ProShares Ultra S&P 500 (SSO) sometime in the near future.

Q: With 2-year LEAPs, would you go at the money or out of the money?

A: This is the golden opportunity to go way out of the money because the return goes from 100% to 500%, or even 1000% if you go, say, 30%-50% out of the money. A lot of these stocks are ripe for very quick 30% bouncebacks, especially the (ROM). So yes, you want to do out of the money 20% to 30%. It will easily recover those losses in weeks if you are picking the right stocks. Over a two-year view, a lot of these big tech stocks could double by the time your LEAP expires, and then you will get the full profit. The rule of thumb is: the farther out of the money you go, the bigger the profit is. But I wouldn’t go for more than a 1000% profit in 2 years; you don't want to get greedy, after all.

Q: You called the Dow to hit 15,000. Is that still possible? We got down to the 18 handle.

A: Yes, if the coronavirus data gets worse, which is certain, we could get another panic selloff. How will the market handle 100,000 US deaths, given the exponential rise in cases we are seeing? With cases doubling every three days that is entirely within range. So, I would say, there is a 50% chance we hit the bottom on Monday at 18,000, and 50% chance we go lower.

Q: Do you know anything about the coronavirus stocks like Regeneron (REGN)?

A: Actually, I do, it's covered by the Mad Hedge Biotech & Health Care Letter, click here for the link. If you get the Biotech Letter, you already know all about stocks like Regeneron. Regeneron literally has hundreds of drugs in testing right now to work as vaccines or antivirals, and some of them, like their arthritis drug, have already been proven to work. So, we just have to get through the accelerated trials and testing to unleash it on the market. But for anybody who has a drug, it's going to take a year to mass-produce enough to inoculate the entire country, let alone the world. So, don't make any big bets on getting a vaccine any time soon—it's a very long process. Even in normal times, some of these drugs take months to manufacture.

Q: Are there any ventilator stocks out there?

A: There are; a company called Medtronic (MDT), which the Mad Hedge Biotech & Healthcare Letter also covers. They are the largest ventilator company in the US. Their normal production is 100 machines a week. Now, they are increasing that to 500 a week as fast as they can, but it isn’t enough. We need about 100,000 ventilators. China is now selling ventilators to the US. Elon Musk from Tesla (TSLA) just bought 1,000 ventilators in China and had them shipped over to San Francisco at his own expense, and Virgin Atlantic just flew over a 747 full of ventilators and masks and other medical supplies from China. So yes, there are stocks out there to play these things, they have already had large moves. We liked them anyway, even before the pandemic, so those calls were quite good. And China thinks their epidemic is over, so they are happy to sell us all the medical supplies they can make.

Q: Why did 30-year mortgage rates just go up instead of down? I thought the Fed rate cuts were supposed to take them down; am I missing something?

A: In order to get 30-year mortgage rates down, you have to have buyers of 30-year loans, and right now there are buyers of nothing. The lending that is happening is from banks lending their own money, which is only a tiny percentage of the total loan market. When the Fed moves into the mortgage market, you will see those yields move to the 2% range. The other problem is how to get a loan if all the banks are closed. They are running skeletal staff now, and you can’t close on real estate deals because all the notaries and title offices are closed; so essentially the real estate industry is going to shut down right now and hopefully, we’ll finish that in a month.

Q: Do you think Uber (UBER) and Lyft (LYFT) will go bankrupt?

A: It is a possibility because one to one human contact inside a car is about the last situation you want to be in during a pandemic. Their traffic was down 25% according to a number I saw. It’s very heavily leveraged, very heavily indebted, and those are the companies that don’t survive long in this kind of crisis. So, I would say there is a chance they will go under. I never liked these companies anyway; they are under regulatory assault by everybody, depend on non-union drivers working for $5 an hour, and there are just too many other better things to do.

Q: Is this the end of corporate buybacks?

A: To some extent, yes. A future Congress may make it either illegal or highly tax corporate buybacks, in some fashion or another because twice in 12 years now, we have had companies load up on buying back their own stock, boosting CEO compensation to the hundreds of millions—if not billions—and then going broke and asking for government bailouts. Something will be done to address that. If you take buybacks out of the market (the last 10,000-point gain in the Dow were essentially all corporate buybacks), we may not see a 20X earnings multiple again for another generation. Individuals were net sellers of stock for those two years. We only reached those extreme highs because of buybacks, so you take those out of the equation and it's going to get a lot harder to get back to the super inflated share prices like we had in January.

Q: How long before an Italian bank collapses, and will they need a bailout?

A: I don’t think they will get a collapse; I think they will be bailed out inside Italy and won’t need all of Europe to do this. But the focus isn't on Europe right now, it's on the US.

Q: Do you think this virus is really subsiding in China based on their past history of dishonest reporting?

A: Yes, that is a risk, and that's why people aren’t betting the ranch right now—just because China is reporting a flattening of cases. And China could be hit with a second wave if they relax their quarantine too soon.

Q: What's your opinion on how the Fed is doing and Steve Mnuchin in this crisis?

A: I think the Fed is doing everything they possibly can. I agree with all of their moves—this is an all-hands-on-deck moment where you have to do everything you can to get the economy going. Notice it’s Steve Mnuchin doing all the negotiating, not the president, because nobody will talk to him. For a start, he may be a Corona carrier among other things, and you’re not seeing a lot of social distancing in these press conferences they are holding. About which 50% of the information they give out is incorrect, and that's the 50% coming from Donald Trump.

Q: What do you think about no debt and no pension liability?

A: That’s why Tech has been leading the upside for the last 10 years and will lead for the next 10. You can really narrow the market down to a dozen stocks and just focus on those and forget about everything else. They have no net debt or net pension fund liabilities.

Q: Why have we not heard from Warren Buffet?

A: I'm sure negotiations are going on all over the place regarding obtaining massive stakes in large trophy companies that he likes, such as airlines and banks. So that will be one of the market bottom indicators that I mentioned a couple of days ago in my letter on “Ten Signs of a Market is Bottoming.”

Q: What’s the outlook for gold?

A: Up. We just had to get the financial crisis element out of this before we could go back into gold, so I would be looking to buy SPDR Gold Shares ETF (GLD), the gold miners like Barrick Gold (GOLD) and Newmont Mining (NEM), the Van Eck Vectors Gold Miners ETF (GDX), and the 2X long ProShares Gold ETF (UGL).

Q: Does the Fed backstop give you any confidence in the bond market?

A: Yes, it does. I think we finally may be getting to the natural level of the market, which is around an 80-basis point yield. Let’s see how long we can go without any 50-point gyrations.

Q: Do you foresee a depression?

A: We are in a depression now. We could hit a 20% unemployment rate. The worst we saw during the Great Depression was 25%. But it will be a very short and sharp one, not a 12-year slog like we saw during the 1930s.

Good Luck and Good Trading and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE PANIC IS ON),

(INDU), (SPX), (VIX), (VXX), (GLD), (USO), (TLT), (AAPL), (WYNN), (CCL), (UAL)

I just drove from Carmel, California to San Francisco on scenic Highway 1. I was virtually the only one on the road.

The parking lot at Sam’s Chowder House was empty for the first time in its history. The Pie Ranch had a big sign in front saying “Shut”. The Roadhouse saw lights out. It was like the end of the world.

The panic is on.

The economy has ground to a juddering halt. Most US schools are closed, sports activities banned, and travel of any kind cancelled. All ski resorts in the US are shut down as are all restaurants, bars, and clubs in California. Virtually all public events of any kind have been barred for the next two months. Apple (AAPL) and Nike (NIKE) have closed all their US stores.

The moment I returned from my trip, I learned that the Federal Reserve has cut interest rates by a mind-boggling 1.00% on the heels of last week’s 0.50% haircut. This is unprecedented in history. S&P Futures responded immediately by going limit down for the third time in a week.

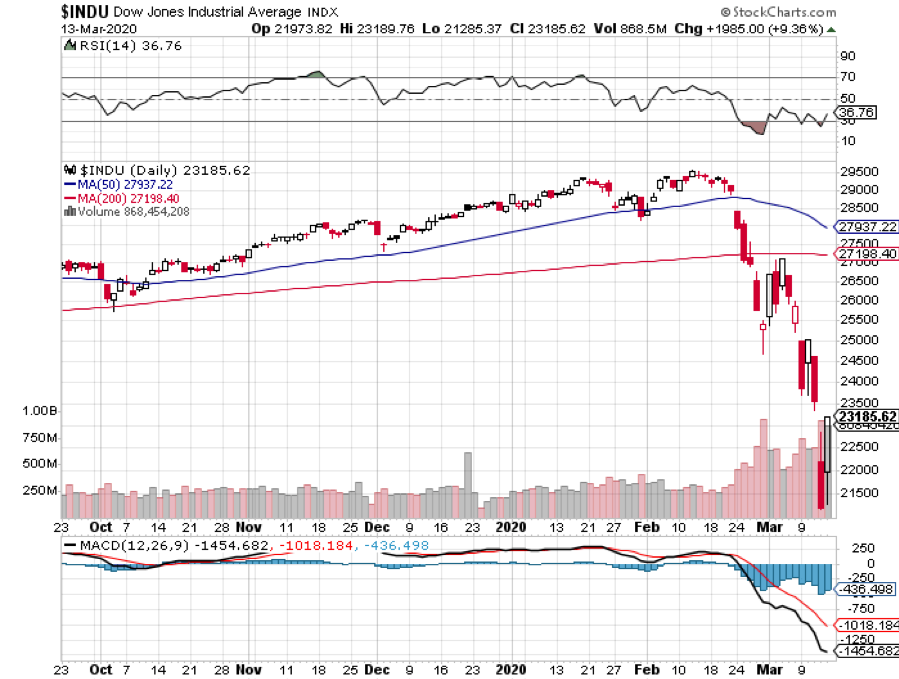

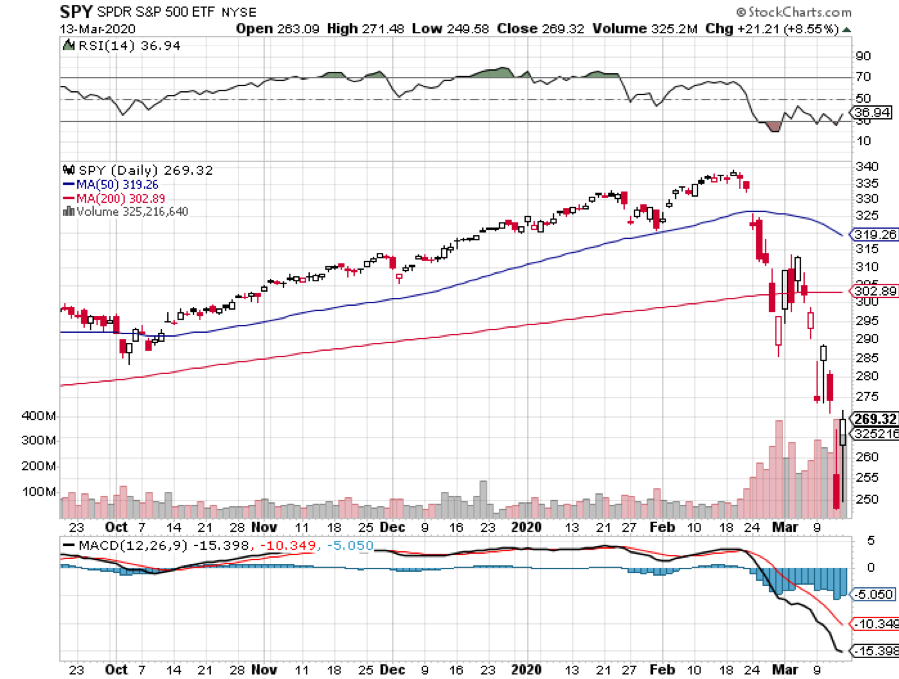

The most pessimistic worst-case scenario I outlined a week ago came true in days. The (SPX) is now trading at 2,500. Goldman Sachs just put out a downside target at 2,000, off 41% in three weeks.

That takes the market multiple down from 20X three weeks ago to 14X, and the 2020 earnings forecast to crater from $165 to $143. These are numbers considered unimaginable only a week ago.

You can blame it all on the Coronavirus. Global cases shot above 160,000 yesterday, while deaths exceeded 5,800. In the US, we are above 3,000 cases with 60 deaths. The pandemic is growing by at least 10% a day. All international borders are effectively closed.

The stock market has effectively impeached Donald Trump, unwinding all stock market gains since his election. At the Thursday lows, the Dow Average ticked below 20,000, less than when he was elected. Economic growth may be about to do the same, wiping out the 7% in economic growth that has taken place during the same time.

Leadership from the top has gone missing in action. The president has told us that the pandemic “amounts to nothing”, is “no big deal”, and a Democratic “hoax.” There is no Fed effort to build a website to operate as a central clearing house for Corona information. In the meantime, the number of American deaths has been doubling every three days.

There have only been 13,500 tests completed in the US so far and they are completely unavailable in my area. The bold action to stem the virus has come from governors of the states of all political parties.

The good news is that all this extreme action will work. If you shut down the economy growth, the virus will do the same. In two weeks, all carriers will become obvious. Then you simply quarantine them. Any dilution of the self-quarantine strategy simply stitches out the process and the market decline.

The hope now is that the recession, which we certainly are now in, will be sharp but short. “An ounce of prevention is worth a pound of cure” is certainly in control now.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $25 a barrel, and many stocks down by half, there will be no reason not to.

Oil (USO) crashed, taking Texas tea down an incredible $22 overnight. OPEC collapsed as Saudi Arabia took on Russia in a price war, flooding the market. All American fracking companies with substantial debt have just been rendered worthless. I told you to stay away from MLPs! It’s amazing to see how the effect of one million new electric cars can have on the oil market. Blame it all on Elon Musk.

The oil crash is all about the US. American fracking has added 4 million barrels a day of supply over the last five years and 8 million b/d during the last ten. Saudi Arabia and Russia would love to wipe out the entire US industry.

Even if they do, the private equity boys are lining up to buy assets at ten cents on the dollar and bring in a new generation of equity investors. The wells may not even stop pumping. How do you say “Creative Destruction” in Arabic and Russian? We do it better than anyone else.

Gold (GLD) soared above $1,700, on a massive flight to safety bid bringing the old $1,927 high within easy reach.

Bond yields (TLT) plunged to 0.31% as recession fears exploded. Looks like we are headed to 0% interest rates in this cycle. Corona cases top 4,000 in the US and fatalities are rising sharply. Malls, parking lots, and restaurants are all empty.

Trump triggered a market crash, with a totally nonsensical Corona plan. Banning foreigners from the US will NOT stop the epidemic but WILL cause an instant recession, which the stock market is now hurriedly discounting. This is an American virus now, not a foreign one or a Chinese one. The market has totally lost faith in the president, who did everything he could to duck responsibility. The US is short 100,000 ICU beds to deal with the coming surge in cases. No one has any test kits at the local level. We could already have 1 million cases and not know it.

The US could lose two million people, according to forecasts by some scientists. At 100 million cases with a 5% fatality rate, get you there in three months. That could cause this bear market to take a 50% hit. The US is now following the Italian model, doing too little too late, where bodies are piling up at hospitals faster than they can be buried.

Stocks are back to their January 2017 lows, down 1,000 (SPX) points and 9,500 Dow points (INDU) in three weeks. Yikes! Unfortunately, I lived long enough to see this. We’ve seen 14 consecutive days of 1,000-point moves. The speed of the decline is unprecedented in financial history.

The Recession is on. Look for a short, sharp recession of only two quarters. JP Morgan is calling for a 2% GDP loss in Q2 and a 3% hit in Q3. The good news is that the stock market has already almost fully discounted this. The only way to beat Corona is to close down the economy for weeks.

A two-week national holiday is being discussed, or the grounding of all US commercial aircraft. Warren Buffet has cancelled Berkshire Hathaway’s legendary annual meeting. All San Francisco schools are closed, events and meetings cancelled. The acceleration to the new online-only economy is happening at light speed.

Municipal bonds crashed, down ten points in three days to a one-year low. If you thought that you parked your money in a safe place, think again. Municipalities are seeing tax and fee incomes collapse in the face of the Coronavirus. Brokers are in panic dumping inventories to meet margin calls. There is truly no place to hide in this crisis but cash, which is ALWAYS the best hedge. I would start buying (MUB) around here.

Bitcoin collapsed 50% in two days, to an eye-popping $4,000. So much for the protective value of crypto currencies. I told you to stay away. No Fed help here.

My Global Trading Dispatch performance has gone through a meat grinder, pulling back by -10.36% in March, taking my 2020 YTD return down to -13.28%. That compares to an incredible loss for the Dow Average of -32% at the Friday low. My trailing one-year return was pared back to 35.31%. My ten-year average annualized profit shrank to +33.84%.

I have been fighting a battle for the ages on a daily basis to limit my losses. My goal here is to make it back big time when the market comes roaring back in the second half.

My short volatility positions have been hammering me. I shorted the (VXX) when the Volatility Index (VIX) was at $35. It then went to an unbelievable $76. I was saved by only trading in very long maturity, very deep out-of-the-money (VXX) put options where time value will maintain a lot of their value. These will all come good well before their one-year expiration.

I also took profits in four short position at the market lows in Apple (AAPL) and the three short positions in Corona-related stocks, (CCL), (WYNN), and (UAL), which cratered, picking up an 8% profit there.

At the slightest sign of a break in the pandemic, the economy and shares should come roaring back. As things stand, I can handle a 3,000 point in the Dow Average from here and still have all of my existing positions expire at their maximum profit point with the Friday options expiration.

On Monday, March 16 at 7:30 AM, the New York Empire State Manufacturing Index is out.

On Tuesday, March 17 at 5:00 AM, the Retail Sales for February is released.

On Wednesday, March 18, at 7:30 AM, the Housing Starts for February is printed.

On Thursday, March 19 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, March 20 at 9:00 AM, the February Existing Home Sales is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I went down to Carmel, California to hole up in a hotel near the most perfect beach in the state and do some serious writing. This is the city where beachfront homes go for $10 million and up, mostly owned by foreign investors and tech billionaires from San Francisco. Locals decamped from here ages ago because it became too expensive to live in.

This is also where my parents honeymooned in 1949, borrowing my grandfather’s 1947 Ford.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader