Global Market Comments

February 26, 2020

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

Global Market Comments

February 26, 2020

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

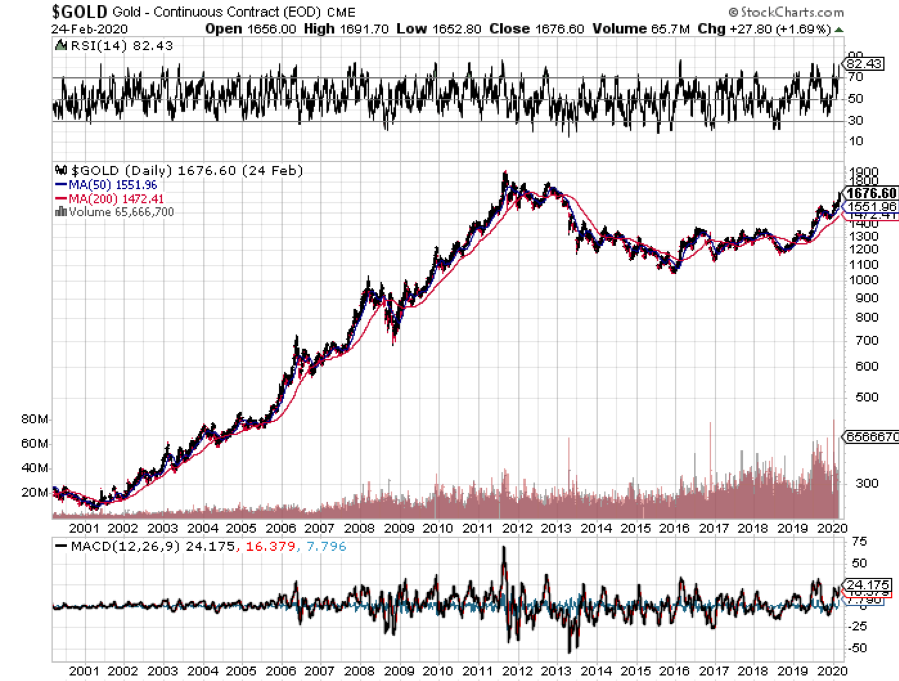

With global stock markets in free fall and interest rates everywhere headed to zero, the outlook for gold has gone from strength to strength.

Shunned as the pariah of the financial markets for years, the yellow metal has suddenly become everyone’s favorite hedge.

Now that gold is back in fashion, how high can it really go?

The question begs your rapt attention, as the Coronavirus has suddenly unleashed a plethora of new positive fundamentals for the barbarous relic.

It turns out that gold is THE deflationary asset to own. Who knew?

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage by gold over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week, due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

And last week, the virus went pandemic as silver rocketed 8.6% and others like Palladium (PALL) were also frenetically bid.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it last peaked in the summer of 2011 at $1,927 an ounce, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant.

The biggest buyers of gold in the world, the Indians, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,400 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD), the world’s largest gold miner, didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply. That has recently been happening on a large scale.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate, as older mines carry costs that go all the way down to $600 an ounce.

No one is going to want to supply the sparkly stuff at a loss. So, supply disappeared.

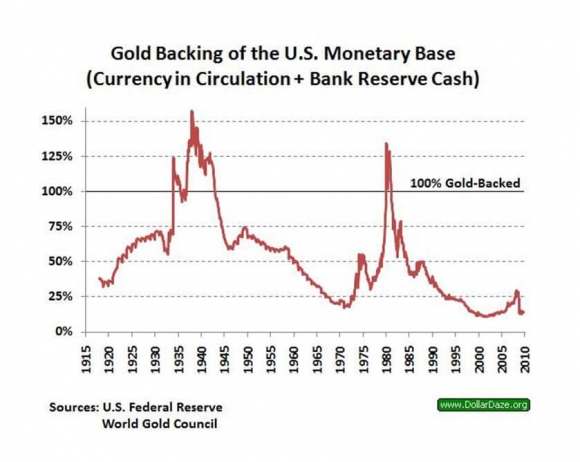

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value, and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

So, when the chart below popped up in my inbox showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce, when the money supply was collapsing during the Great Depression, and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten your attention yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah and teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980 to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and is slowly tricking down to minimum wage workers. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty-somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid-2020s, when shocking wage hikes spread elsewhere.

I’ll be back playing gold again, given a good low-risk, high-return entry point.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients' other risk assets, good for you.

You’re finally learning!

Global Market Comments

January 6, 2019

Fiat Lux

2020 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQQ), (XLF), (XLE), (XLY),

(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP)

(FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

(FCX), (VALE), (AMLP), (USO), (UNG),

(GLD), (GDX), (SLV), (ITB), (LEN), (KBH), (PHM)

Global Market Comments

December 20, 2019

Fiat Lux

Featured Trade:

(DECEMBER 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(BA), (CRSP), (BABA), (GLD), (PANW), (VIX), (VXX)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 18 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What is the status of Boeing (BA) and when should I buy it?

A: Their 737 production was shut down because they literally ran out of space to park completed planes. They have something like 400 of them now sitting around on tarmacs all around northern Washington state. This is the worst-case scenario so it is a very tempting place to buy; I would do something like a February 2020 $250-$270 vertical bull call spread, make 10% in a month, and be conservative. If it weren't year-end, and I didn't already have my year in the bag, I would probably buy Boeing right here.

Q: Do you recommend CRISPR (CRSP) therapeutics as a buy?

A: Yes, but on a dip. I always hate buying stocks after they doubled. At some point in 2020, we will see correction in biotech stocks, and then you want to load the boat again. Here, I’m buying nothing.

Q: Is Palo Alto Networks (PANW) a buy at these levels?

A: Yes, it’s already had its correction—it's one of the few stocks that are buyable at these levels. But I would do something like a call spread, which is limited risk. As far as a pairs trade with Palo Alto vs Nvidia...I would not touch that with a ten-foot pole, because you can’t know the internal nature of two companies like that well enough to buy one and sell short the other against it. You could really get destroyed on that pairs trade, so don’t make that mistake.

Q: Do you think the US dollar (UUP) will head higher or lower next year?

A: It will go a lot lower, as the chickens from all the government borrowing come home to roost. More borrowing brings a lower dollar, which brings lower everything in the US; all US dollar-denominated assets will get hurt, and this may be what eventually kills off the bull market in stocks. Start buying the Euro (FXE) on dips.

Q: What do you think about Boris Johnson winning the UK election?

A: It is a disaster and will lead to the end of Great Britain. Scotland will go independent, Northern Ireland will join the Republic of Ireland, and even Wales may break off and form its own country. So, England will be reduced to a tiny rump of a country with a much lower standard of living. It may take 10 years to happen, but that’s where it’s going.

Q: Does the recent positive housing data mean we aren’t having a recession in 2020?

A: Yes, in fact the market has been backing out of a 2020 recession for the last three months; and the leading sector in the recovery has been housing, caused partly by extremely low-interest rates but also partly by millions of new millennials pouring into the housing market for the first time. Finally, my basement is empty. That explains why the entry-level and middle level of the market are strong, and the high end is still decreasing in price.

Q: Back in August, the global economy looked to be stalling, yet it was a great time to buy stocks.

A: That is exactly when to buy stocks—when the economy is terrible. If you get used to buying on the bad news and selling on the good news you will do very well as a trader. Most people do the opposite—people were dumping stocks in August. And that of course was when we went with one of our rare 100% longs. By the way, this happens every August, which is why I take my vacations in July.

Q: Do you see a global slowdown during the melt-up?

A: Well, the economy is still slowing down. It never stopped slowing down—we’re probably looking at a 1.5% GDP this quarter. However, in liquidity-driven markets, you don’t look at fundamentals; you look at the amount of cash that is available to buy equities, that’s why you buy equities. That said, if we ever do get a real economic recovery, you might actually have stocks going down because a price-earnings multiple of 20X is not an ideal place to buy stocks.

Q: What do you prefer for a Volatility Index (VIX) trade?

A: An option on the iPath Series B S&P 500 VIX Short Term Futures ETN (VXX) is one. Go long dates, like a year, and deep out-of-the-money, like the $18 strike price, to minimize the hot from Time decay. If your (VIX) goes back up to $25 the (VXX) will soar to $27 and you will make a fortune.

However, if you have the facility to trade futures, then options on the futures in the VIX is how most professionals will trade that.

Q: Should we be worried about the Repo crisis as we approach the end of the quarter?

A: Absolutely, you should be worried—the Fed might have to come through with another round of quantitative easing in order to prevent a surprise overnight pop in interest rates to 5%. That’s what happened last quarter; it could certainly happen again. The basic problem is that the structure of the US debt markets aren't built to handle the volume of borrowing that’s coming through from the US government, so with debt at an all-time high, we’re kind of in new territory here in terms of whether or not markets can actually handle that amount of borrowing. Total government borrowing next year will probably be $1.75 trillion dollars.

Q: What do you make of gold (GLD) at these levels?

A: Cheap but getting cheaper. You want to buy it the day the stock market peaks out in Q1 2020.

Q: Are Chinese equities a buy after the phase one trade deal?

A: Yes, and Alibaba (BABA) is probably your first pick in the Chinese area. During the whole trade war, the Chinese took significant action to stimulate their economy in order to offset the drag on trade. That stimulus is still out there, so we could see a reacceleration in the economy now that the trade war is no longer worsening.

Global Market Comments

December 17, 2019

Fiat Lux

Featured Trade:

(WEDNESDAY, FEBRUARY 5 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED)

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

December 3, 2019

Fiat Lux

Featured Trade:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR), (BYND),

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX), (GOLD),

Global Market Comments

December 2, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or 2020 IS ALREADY HAPPENING),

(TSLA), (X), (GE), (FCX), (SLB), (GOOGL), (MSFT), (GLD)

You know the melt-up that is going on in the stock market right now? That is your 2020 performance being pulled forward.

One thing I have noticed over the past half-century of trading is that when market participants agree on a direction, it gets accelerated. Once the traditional October selloff failed to show, it was pedal to the metal to achieve new all-time highs.

Traders have become so overconfident that they have already completed this year’s performance and are now working on next year's. They are in effect pulling performance forward from 2020.

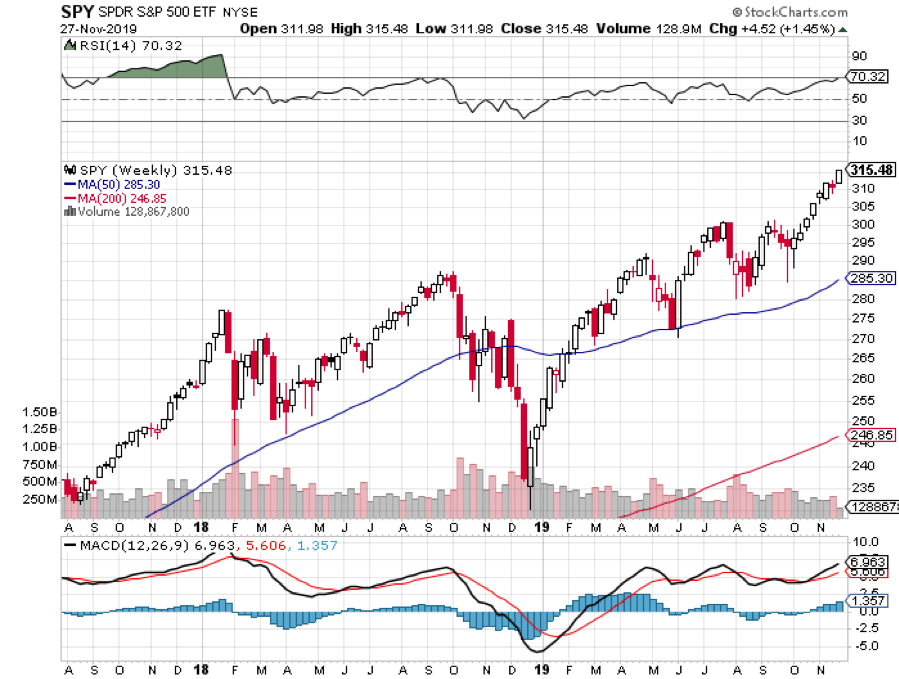

This historic run is taking place in the face of year-on-year earnings growth that is zero. ALL of the 29% price appreciation in the S&P 500 (SPY) in 2019 has been due to multiple expansion, from 14 times earnings to 19 times, a 20-year high. Market multiples rising by 50% anytime is almost unprecedented in history. I can only recall that happening twice: in 1929 and 1999.

So, that leaves only two possibilities for 2020. Either the multiple rises to a new 20-year multiple high, say to 20, 21, or 22, or the stock market goes down.

With a trade war-induced global economic slowdown still unfolding, don’t expect any respite from a sudden earnings recovery. Enjoy 2019 because the more we go up now means the more we will go down in 2020.

Were you waiting for the euphoria to make a market top? This is it. Sharply rising markets in the face of sharply falling earnings can only end in tears.

Needless to say, risk in the stock market is very high right now.

Jay Powell gave the market another boost, promising to hit the Fed’s 2% inflation target, giving plenty of room for wage hikes. The last inflation reading was 1.7% YOY. He might as well have said Dow 29,000 by yearend. I wish it were always this easy.

Hong Kong stalled the rally with the passage of a pro-democracy support by congress, with sanctions. China is warning of “firm countermeasures.” That throws cold water on any trade deal for 2019. New all-time highs for stocks may have to take a vacation.

US Q3 GDP was revised up to 2.1%, an improvement of 0.2% from the last read. The trade war seems to be costing us 1% of growth a year or about one-third of the total. That’s why we’re getting such a strong stock market move on the possibility of a trade deal. No-deal means lookout below.

Durable Goods came in at 0.6% in October, a nine-month high and better than expected. What does this week’s spate of positive data means, the first in many months? Is the recession risk over? If so, how much is already in the price?

Stocks love a steepening yield curve, with long term interest rates rising faster than short term ones. It puts the recession talk on hold, if not in abeyance.

It’s time to go dumpster diving, as the upside breakout in the Russell 2000 demonstrated last week. So, it’s time to start looking at the forlorn and the ignored of this bull market, like US Steel (X), General Electric (GE), Freeport McMoRan (FCX), and Schlumberger (SLB). There are no fundamentals in any of these names, they’ve just been down for so long anything looks like up from here. The liquidity-driven bull market has to find some fresh meat to rotate into, even temporarily, or it will die.

S&P Case Shiller rose 3.2% in September, the third consecutive month of price increases. Only San Francisco is showing falling prices. Phoenix (6.0%), Charlotte (4.6%), and Tampa (4.5%) are showing the greatest prices rises. Only a shortage of inventory is preventing prices from rising faster, now at a record low of 3.9 months. The builders who went under ten years ago aren’t building anymore.

New Home Sales drop 0.7%, in October, but are still up a massive 31.6% YOY. Sales in the northeast and south plunged, while those in the Midwest and west rise. The seasonally adjusted annual rate is 733,000 units. The Median Home Price fell 3.6% to $316,700. A 30-year fixed-rate mortgage at 3.66% is a major factor.

Merger mania in drug land continues, with the Novartis takeover of The Medicines Co. for $9.7 billion. It wants to take on Amgen (AMGN), Regeneron (REGN), and Sanofi in the heart drug space. No wonder this is the top-performing sector since I launched the Mad Hedge Biotech and Healthcare Letter.

Tesla shattered, both windows and sales records with an incredible 250,000 cyber trucks sold in a week. It’s one of the largest consumer orders in history, second only to the Tesla Model 3 launch four years ago. I may get one myself to make the Lake Tahoe run on a single 500-mile charge. Keep buying (TSLA) on dips. It is the clearest ten bagger out there.

Who is the mystery gold (GLD) buyer? Someone made a massive bet in the options market that gold will rise above $4,000 an ounce in 18 months. It would take a 32% move just to get gold back to its old $1,927 high. If the trade war continues, we may get it.

This was a week for the Mad Hedge Trader Alert Service to burst upon new all-time highs. I know this sounds boring, but I made all the money long technology stocks. This is net a -2.16% loss on my short position in Tesla (TSLA). If I’d only held on two more days this would have been a big winner over the disappointment over the shocking Cyber truck design. My long positions have shrunk to my core (MSFT) and (GOOGL).

By the way, running out of positions at a market top is a good thing.

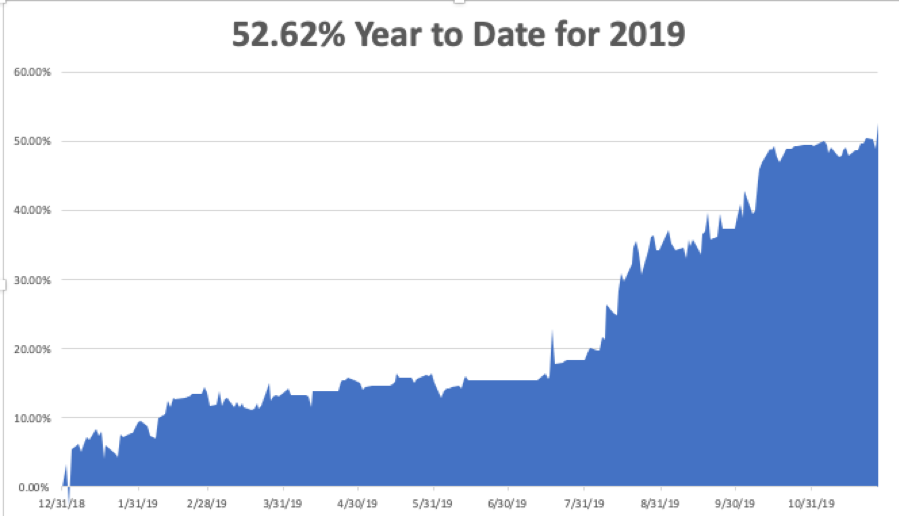

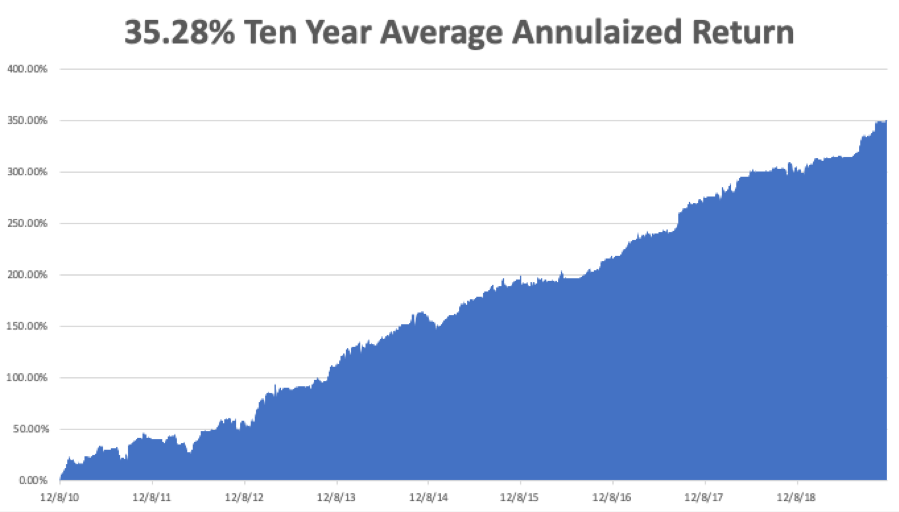

My Global Trading Dispatch performance held steady at +352.76% for the past ten years, pennies short of an all-time high. My 2019 year-to-date catapulted back up to +52.62%. We closed out November with a respectable +3.07% profit. My ten-year average annualized profit ground back up to +35.28%.

The coming week will be hot with the jobs data trifecta.

On Monday, December 2 at 8:00 AM, the ISM Manufacturing PMI for November is out.

On Tuesday, December 3 at 2:30 PM, the API Crude Oil Stocks are announced.

On Wednesday, December 4, at 6:15 AM, the private sector ADP Employment Report is published.

On Thursday, December 5 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, December 6 at 8:30 AM, the November Nonfarm Payroll Report is released.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am going to battle my way through the blizzards at Donner Pass this weekend to get back to the San Francisco Bay Area. There, I’ll be helping the local Boy Scout troop to set up their Christmas tree lot. The enterprise helps finance all the camping trips for the coming year.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 31, 2019

Fiat Lux

Featured Trade:

(WELCOME TO THE LAND OF ZEROS),

(TLT), (VIX), (GLD), (SLV), (FXY),

(A NOTE ON OPTIONS CALLED AWAY), (BA)

(TESTIMONIAL)