Mad Hedge Technology Letter

July 6, 2018

Fiat Lux

Featured Trade:

(HOW THE COBALT SHORTAGE WILL LEAD TO THE $2,000 IPHONE),

(AAPL), (SSNLF), (CMCLF), (FCX), (VALE), (GLNCY), (VLKAY), (BMWYY)

Mad Hedge Technology Letter

July 6, 2018

Fiat Lux

Featured Trade:

(HOW THE COBALT SHORTAGE WILL LEAD TO THE $2,000 IPHONE),

(AAPL), (SSNLF), (CMCLF), (FCX), (VALE), (GLNCY), (VLKAY), (BMWYY)

Hello $2,000 iPhone.

Flabbergasted consumers reacted last holiday season when Apple dared offer a $1,000 smartphone.

How confident this company has become!

Well, this is just the beginning.

Apple (AAPL) will be the first smartphone maker to offer a $2,000 phone, and I will tell you why!

The tech industry is going through a cumbersome wave of repricing after several high-profile debacles underscoring the true value of data.

The upward revision of data has seen more players pour into the game attempting to carve out a slice of the pie for themselves.

The reason why tech companies will start offering products at higher price points is because the inputs are rising at a rapid clip.

Apple's Development and Operations (DevOps) costs to design and maintain this outstanding product is going through the roof.

Apple's DevOps employees earn around $145,000 (before tax) per year and compensation is rising. Granted, the technology is developing and batteries are smaller, but salaries are rising at a quicker relative pace because of the dire shortage of DevOps talent in Silicon Valley.

It's possible that living in a shoebox at $4,200 per month in Mountain View, Calif., is off-putting for potential staff.

The most expensive part of an iPhone X is the OLED screen.

Apple estimated costs of $120 per screen manufacturing the Apple iPhone X. The cost doubled from LCD panels from $60 per screen.

Samsung (SSNLF) has been best of breed for screens for a while, and it is currently working on the next generation of Micro LED tech, which is the next gap up from the OLED displays of today.

Samsung has an inherent conflict of interest with Apple, creating tension between these tech stalwarts. Apple made the contentious decision to procure in-house screens at a secret manufacturing facility in Santa Clara, Calif., to avoid the constant friction.

It's common knowledge that the average price of technology shrinks over time, but the American smartphone industry has defied gravity with expected prices rising 6% to $324 in 2018.

The Apple iPhone X raw costs were around $400 per phone. There is zero chance that a next gen, enhanced Apple smartphone will cost this low ever again.

Confirming this trend are Chinese smartphones retail prices rising at 15% last year.

The cost of memory, DRAM and NAND chips, rose dramatically this past year too. As more memory is crowbarred into the design process, the costs keep trending higher.

Lithium-ion batteries only add up to 1% to 2% of OEM (Original Equipment Manufacturers) cost and probably only bumps up the cost of iPhones incrementally.

The more skittish situation is the EV (Electric Vehicles) snafu spiking total demand.

Volkswagen (VLKAY) announced its most wide-ranging electrification plans ever.

In order to achieve this lofty objective, Volkswagen has earmarked $25 billion for batteries from Samsung, LG, and Contemporary Amperex.

All told, the final investment in batteries will amount to $70 billion and another $25 billion in capital investment.

Volkswagen hopes to have 16 up and running (EV) factories by 2022, up from three today.

All told, this company will bring 80 new EV models to market by 2025.

The goal is unattainable because of a lack of in-house battery production.

CEO Matthias Muller said the reason for not manufacturing in-house batteries was, "Others can do it better than we can."

Muller will rue the decision down the line as a myriad of companies migrate toward in-house solutions, giving firms more control over the process and overhead.

More importantly, Muller will have to rely on the ebb and flow of rising cobalt prices.

A battery for an (EV) ranges between $8,000 to $20,000, comprising the largest input for the (EV) makers such as Tesla (TSLA) and Ford (F).

Making matters worse, companies cut from all cloth are hoarding cobalt reserves based on anticipating the potential demand.

This phenomenon will cause all big tech players to replenish any reserves of base materials immediately.

Apple has had chip shortage problems in the past. This year is even worse than 2017, with NAND and DRAM chip supply trailing demand by 30%.

Tech companies have been hastily locking down contracts in advance to ensure the necessary materials to produce their flashy gadgets on a highly pressurized deadline.

Lithium battery demand is expected to rise 45% between 2017 and 2020, and there has been no meaningful large-scale investment into this industry.

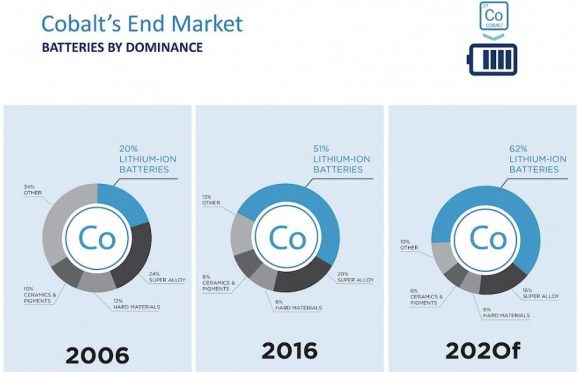

Battery production made up 51% of cobalt demand in 2016 and will hit around 62% by 2022.

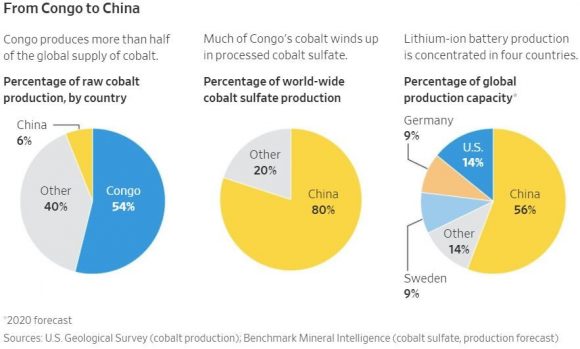

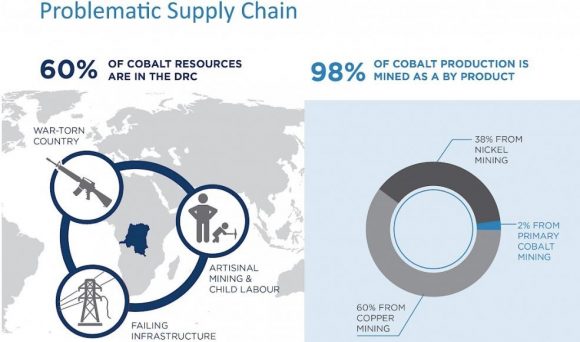

Compounding the complexity is 60% of global cobalt production is found in one country - the Democratic Republic of the Congo (DRC).

DRC is a hotspot for geopolitical fallout and its history is littered with civil war, internal conflict, and poor infrastructure.

The 21st century will be dependent on a chosen group of valuable materials. Cobalt is shaping up to be the leader of this pack and is needed in a plethora of business applications such as EVs, lithium-ion batteries, and PCs.

Cobalt is vital in metallurgical applications that include aerospace rotating parts, military and defense, thermal sprays, prosthetics, and much more.

The DRC recently proposed a revised mining law increasing taxes on cobalt and other precious metals. The legislation has yet to be written into stone and would certainly jack up the price of cobalt.

Everybody wants a cut of the cobalt game.

Glencore's (GLNCY) management has noted this mining tax is "challenging" at a time it is just completing its Katanga expansion.

Katanga has the potential to become the largest global copper and cobalt producer.

Copper is equally important to cobalt since cobalt production is a by-product of copper and nickel mining. Only 2% of cobalt results directly from cobalt mining, and 60% via copper mining, and 38% via nickel mining.

Last year, Freeport-McMoRan (FCX) was dangling its cobalt project to outside investors in the DRC but was unable to fetch a premium price.

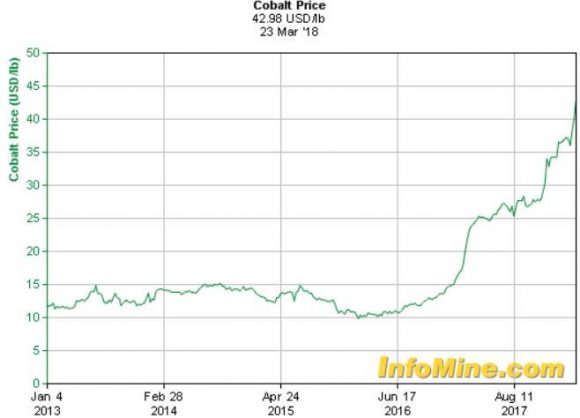

In a blink of an eye, China Molybdenum Co. (CMCLF) swooped in and (FCX) accepted an offer of $2.65 billion. (FXC) used the sale to pay down debt while the price of cobalt has taken off to the moon.

It gets worse. China owns 80% of refined global cobalt production and 90% of its operations are in the DRC.

China is attempting to corner the cobalt market in the DRC, gaining a stranglehold on future technological devices, (EV)s, and big data.

The keys to future technological hegemony lie in the sparsely inhabited jungles of the DRC. China has the first mover advantage and backing of the communist party as (CMCLF) strives to be a global dominator in cobalt production.

China has smartly wriggled its way down to the bottom of the supply chain capturing cobalt resources. If a trade war ensues, China can simply cut off cobalt supply lines to whomever.

There is nothing CFIUS or Donald Trump can do about it.

America's 14% of global cobalt production will be insufficient to produce the new (EV)s, iPhone 11s, gizmos and gadgets that American consumers have grown to embrace.

Analysts expected Apple to acquire some supplementary companies aiding in expansion following the overseas repatriation.

A thriving software outfit or a company of cloud developers would have sufficed. However, reports streaming in that Apple has entered into negotiations to buy a five-year supply of cobalt directly from miners for the first-time underscores where Apple's priorities lie.

Cobalt demand expects to increase by 30% from 2016 to 2020.

Apple is scared it will be locked out of the cobalt market or forced to pay ludicrous prices for its cobalt needs.

Considering the price of cobalt has quadrupled since June 2016, and smartphones are 25% of the cobalt market, it's a strategically prudent move by Apple's CEO Tim Cook in light of BMW (BMWYY) announcing the need of 10X more cobalt by 2025.

Going forward anything comprised of cobalt-based technology will garner a higher premium resulting in higher prices for consumers including that $2,000 iPhone.

(FCX) is a must buy for those who believe precious metals are the foundation to all future technology. Other intriguing names include Brazilian company Vale S.A. (VALE), and Glencore, the largest Swiss company by revenue.

Or if you have the cash, plunk it down on a cobalt mine in the DRC. But only if you're insane.

_________________________________________________________________________________________________

Quote of the Day

"Heavier-than-air flying machines are impossible," - said Lord Kelvin, President of the Royal Society, in 1895.

Mad Hedge Technology Letter

March 28, 2018

Fiat Lux

Featured Trade:

(HOW THE COBALT SHORTAGE WILL LEAD TO THE $2,000 IPHONE)

(AAPL), (SSNLF), (CMCLF), (FCX), (VALE), (GLNCY), (VLKAY), (BMWYY)

Hello $2,000 iPhone.

Flabbergasted consumers reacted last holiday season when Apple dared offer a $1,000 smartphone.

How confident this company has become!

Well, this is just the beginning.

Apple (AAPL) will be the first smartphone maker to offer a $2,000 phone, and I will tell you why!

The tech industry is going through a cumbersome wave of repricing after several high-profile debacles that have cast the light on the true value of data.

The upward revision of data has seen more players pour into the game attempting to carve out a slice of the pie for themselves.

The reason why tech companies will start offering their products at higher price points is because the inputs are rising at a rapid clip.

Apple's Development and Operations (DevOps) costs to design and maintain this outstanding product is going through the roof.

Apple's DevOps employees earn around $145,000 per year and compensation is rising. Granted, the technology is developing and batteries smaller, but salaries are rising at a quicker relative pace because of the dire shortage of DevOps talent in Silicon Valley.

It's possible that living in a shoebox at $4,200 per month in Mountain View, Calif., is off-putting for potential staff.

The most expensive part of an iPhone X is the OLED screen.

Apple estimated costs of $120 per screen manufacturing the Apple iPhone X. The cost doubled from LCD panels from $60 per screen.

Samsung (SSNLF) has been best of breed for screens for a while, and it is currently working on the next generation of Micro LED tech, which is the next gap up from the OLED displays of today.

Samsung has an inherent conflict of interest with Apple, creating tension between these tech stalwarts. Apple made the contentious decision to procure in-house screens at a secret manufacturing facility in Santa Clara, Calif., to avoid the constant friction.

It's common knowledge that the average price of technology shrinks over time, but the American smartphone industry has defied gravity with expected prices to shoot up 6% to $324 in 2018.

The Apple iPhone X raw costs were around $400 per phone. There is zero chance that a next gen, enhanced Apple smartphone will cost this low ever again.

Confirming this trend are Chinese smartphones retail prices rising at 15% last year.

The cost of memory, DRAM and NAND chips, rose dramatically this past year. As more memory is designed into these devices, the costs keep trending higher.

Lithium-ion batteries only add up to 1% to 2% of OEM (Original Equipment Manufacturers) cost and probably only bumps up the cost of iPhones incrementally.

The more skittish situation is the EV (Electric Vehicles) snafu.

Volkswagen (VLKAY) announced it will transform its entire fleet of 300 models into electrified versions by 2025.

In order to achieve this lofty objective, Volkswagen has earmarked $25 billion for batteries from Samsung, LG, and Contemporary Amperex. Volkswagen hopes to have 16 up and running (EV) factories by 2022, up from three today.

The goal is unattainable because of a lack of in-house battery production.

CEO Matthias Muller said the reason for not manufacturing in-house batteries was, "Others can do it better than we can."

Muller will rue the decision down the line as a myriad of companies migrate toward in-house solutions, giving firms more control over the process and overhead.

More importantly, Muller will have to rely on the ebb and flow of rising cobalt prices.

A battery for an (EV) ranges between $8,000- to 20,000, comprising the largest input for the (EV) makers such as Tesla (TSLA) and Ford (F).

Making matters worse, companies cut from all cloth are hoarding cobalt reserves based on anticipating the potential demand.

This phenomenon will cause all big tech players to replenish any reserves of base materials immediately.

Apple has had chip shortage problems in the past. This year is even worse than 2017, with NAND and DRAM chip supply trailing the demand by 30%. Tech companies have been hastily locking down contracts in advance to ensure the necessary materials to produce their flashy gadgets.

Lithium battery demand is expected to rise 45% between 2017 and 2020, and there has been no meaningful large-scale investment into this industry.

Battery production made up 51% of cobalt demand in 2016 and will hit around 62% by 2022.

Compounding the complexity is 60% of global cobalt production is found in one country - the Democratic Republic of the Congo (DRC).

DRC is a hotspot for geopolitical fallout and its history is littered with civil war, internal conflict, and poor infrastructure.

The 21st century will be dependent on a chosen group of valuable materials. Cobalt is shaping up to be the leader of this pack and is needed in a plethora of business applications such as EV, lithium-ion batteries, and PCs.

Cobalt is vital in metallurgical applications that include aerospace rotating parts, military and defense, thermal sprays, prosthetics, and much more.

The DRC recently proposed a revised mining law increasing taxes on cobalt and other precious metals. The legislation has yet to be written into stone and would certainly jack up the price of cobalt.

Glencore's (GLNCY) management has noted this mining tax is "challenging" at a time it is just completing its Katanga expansion.

Katanga has the potential to become the largest global copper and cobalt producer.

Copper is equally important to cobalt since cobalt production is a by-product of copper and nickel mining. Only 2% of cobalt results directly from cobalt mining, and 60% via copper mining, and 38% via nickel mining.

Last year, Freeport-McMoRan (FCX) was dangling its cobalt project to outside investors in the DRC but was unable to fetch a premium price.

In a blink of an eye, China Molybdenum Co. (CMCLF) swooped in and (FCX) accepted an offer of $2.65 billion. (FXC) used the sale to pay down debt while the price of cobalt has taken off to the moon.

It gets worse, China owns 80% of refined global cobalt production and 90% of its operations are in the DRC.

China is attempting to corner the cobalt market in the DRC, gaining a stranglehold on future technological devices, (EV)s, and big data.

The keys to future technological hegemony lie in the jungles of the DRC, and China has the first mover advantage and backing of the communist party as (CMCLF) strives to be a global leader in cobalt production.

China has smartly wriggled its way down to the bottom of the supply chain capturing cobalt resources, and if a trade war ensues, China can simply cut off cobalt supply lines to whomever.

There is nothing CFIUS or Donald Trump can do.

America's 14% of global cobalt production will be insufficient to produce the new (EV)s, iPhone 11s, gizmos and gadgets that American consumers demand for daily life.

Analysts expected Apple to acquire some supplementary companies that will aid in expansion following the overseas repatriation.

A thriving software outfit or a company of cloud developers would have sufficed. However, reports streaming in that Apple has entered into negotiations to buy a five-year supply of cobalt directly from miners for the first-time underscore where Apple's priorities lie.

Cobalt demand expects to increase by 30% from 2016 to 2020.

Apple is scared it will be locked out of the cobalt market or forced to pay ludicrous prices for its cobalt needs.

Considering the price of cobalt has quadrupled since June 2016, and smartphones are 25% of the cobalt market, it's a strategically prudent move by Apple's CEO Tim Cook in light of BMW (BMWYY) announcing the need of 10X more cobalt by 2025.

Going forward anything comprised of cobalt-based technology will garner a higher premium resulting in higher prices for consumers including that $2,000 iPhone.

(FCX) is a must buy for those who believe precious metals are the foundation to all future technology. Other intriguing names include Brazilian company Vale S.A. (VALE), and Glencore, the largest Swiss company by revenue.

Or if you have the cash, plunk it down on a cobalt mine in the DRC. But only if you're insane.

__________________________________________________________________________________________________

Quote of the Day

"Heavier-than-air flying machines are impossible." - Lord Kelvin, President of the Royal Society, in 1895