Mad Hedge Biotech and Healthcare Letter

December 19, 2024

Fiat Lux

Featured Trade:

(SURVIVAL OF THE SOLVENT)

(KOD), (GOSS), (BLUE), (SIOX), (CDAK), (GLPG)

Mad Hedge Biotech and Healthcare Letter

December 19, 2024

Fiat Lux

Featured Trade:

(SURVIVAL OF THE SOLVENT)

(KOD), (GOSS), (BLUE), (SIOX), (CDAK), (GLPG)

The biotech industry likes to measure success in breakthroughs, but 2024 taught us to count it in survivors.

Sure, we saw remarkable wins in schizophrenia and obesity treatments - enough to keep Big Pharma writing checks that would make anyone pause.

But those layoff numbers? They keep climbing, and I've seen enough market cycles to know what that means.

Yes, the Nasdaq Biotechnology Index eked out a 5.4% gain in 2023, but don’t let that calm surface fool you.

Beneath it, some companies were taking on water faster than a paper boat in a tsunami. It’s not exactly the environment to make your local biotech cheerleader grin ear to ear.

Still, there is value in understanding what went wrong.

Take Kodiak Sciences (KOD) - and I mean that literally because the market sure did. They watched their high hopes for an age-related macular degeneration treatment encounter the brick wall of trial results that proved no better than existing standards of care.

The market’s reaction was swift and merciless, erasing more than 70% of Kodiak’s valuation. Back in my hedge fund days, we called this kind of drop a "character-building event."

Then there's Gossamer Bio (GOSS), which missed its endpoints in pulmonary arterial hypertension so badly you'd think they were aiming for a different disease altogether.

They learned the hard way that lofty ambitions can deflate at high altitudes when critical endpoints fail to materialize, leaving the company staring at a gaping hole where investor confidence used to be.

Bluebird Bio (BLUE)? They've been playing regulatory red light green light with their gene therapy platform.

Despite having the science that could make this possible, they struggled to justify the hefty R&D spending necessary to bring complex and costly treatments to a market that can turn stingy when results arrive late and uncertain.

Speaking of tough breaks, Sio Gene Therapies (SIOX) discovered the cruel reality that neurodegenerative pipelines rarely behave the way spreadsheets say they should.

And poor Codiak BioSciences (CDAK) - their exosome therapy platform imploded so spectacularly that they were forced to declare bankruptcy.

Even Galapagos NV (GLPG) found itself stuck reassessing once-promising late-stage candidates. Those strategic alliances they bragged about last year aren't looking quite so strategic anymore, either.

It would be easy to pin the blame on management missteps or scientific overreach, but the numbers are showing something else.

FDA’s Center for Drug Evaluation and Research did not exactly smile on the biotech crowd’s ambitions. In 2022, it approved 37 novel drugs. By December 2023, fewer than 30 had made the cut.

Want more sobering statistics? The probability of a drug making it from Phase I to FDA approval sits at 7.9%. In immuno-oncology alone, we've got over 1,500 active trials fighting for attention. Overcrowding would be an understatement.

Meanwhile, global biopharmaceutical R&D spending topped $200 billion in 2022 - that's a lot of investor cash burning through labs with no guarantee of return.

Remember the IPO party from a few years back? Well, 2023 saw fewer than 20 biotech IPOs brave the public markets. That's not caution - that's fear.

For those still interested in this sector - and I know you're out there - some of these disasters might offer lessons, or even opportunities.

The iShares Biotechnology ETF exists for those who prefer to spread their risk. Smart move, considering what we've seen this year.

Let's talk specific names. Bluebird Bio might still have a chance if they can get their regulatory act together and convince insurers to cover their therapies.

Sio Gene Therapies could find new partners - though I wouldn't hold my breath. Galapagos has Gilead (GILD) in their corner, which counts for something in this market.

So here's my take: hold Kodiak if you can stomach more volatility - they've already taken their biggest hits.

Same goes for Bluebird Bio, but only if you've got patience. Galapagos? Keep it, but watch those pipeline updates like a hawk.

Gossamer Bio? Time to consider an exit. Sio Gene Therapies lacks catalysts, and Codiak - well, bankruptcy speaks for itself.

The lesson from Kodiak, Gossamer, Bluebird, Sio, Codiak, and Galapagos is simple: brilliant science means nothing without solid analysis, realistic timelines, and serious cash. 2024 proved that point six times over.

Sure, everyone in biotech wants to change the world. The hard part? Staying solvent long enough to make it happen.

Mad Hedge Biotech and Healthcare Letter

November 4, 2021

Fiat Lux

Featured Trade:

(A LONG-TERM STOCK FOR MONOPOLY AFICIONADOS)

(VRTX), (ABBV), (GLPG), (CRSP), (MRNA)

Investors have a myriad of biotechnology stocks to choose from. However, most of these options are still in the developmental stage for their first blockbuster product that can hit at least $1 billion in sales annually.

Then, there are biotechnology companies like Vertex Pharmaceuticals (VRTX).

Vertex has a storied history of launching blockbuster names in the market for rare and hard-to-treat diseases.

Among the products in its portfolio, what stands out is Vertex’s work on cystic fibrosis (CF) treatments.

CF is an incurable genetic condition that can damage the lungs and the pancreas. So far, Vertex has four CF treatments available and holds 97% of the market share worldwide, valued at roughly $6.36 billion in 2020.

The company’s latest CF treatment, Trikafta, is already projected to generate roughly $5 billion in sales after only less than 2 years since its release.

Thus far, Vertex has reported an annualized sales run rate of $7.2 billion in its second-quarter earnings report for 2021. This number is expected to climb higher as the company increases its penetration rate in the CF market in the coming years.

Given its history and trajectory, Vertex is projected to generate $10 billion to $10.5 billion in sales for its CF franchise by 2024.

Considering the lucrative CF market’s potential, it no longer comes as a surprise that more and more competitors are entering the space. However, none can even be considered as a close second to Vertex.

AbbVie (ABBV) partnered with Galapagos (GLPG) to come up with a combination CF treatment a few years back, only to get stalled in Phase 2 trials.

It remains to be seen if AbbVie, which eventually acquired the entire CF line from Galapagos, will be able to develop a drug worthy of challenging Vertex’s dominance in the arena.

The driving force behind Vertex’s success is its operating model, which works overtime to exhaust all resources to protect its CF revenue.

Throughout the years, the company has been consistent in its efforts to keep developing innovative CF treatments and expanding its coverage to include more mutations.

In turn, these new drugs all but guarantee that Vertex enjoys a stable and secure cash flow for years.

For example, the IP protection for Trikafta will reach up to the late 2030s. If innovations on the drug are discovered, then this can very well extend into the 2040s.

Despite the overwhelming success of its CF franchise, Vertex knows not to rest all its eggs in one basket.

The company has been working on expanding its expertise. A telltale sign of this decision is its burgeoning partnership with CRISPR Therapeutics (CRSP).

So far, the two have created a promising gene-editing treatment, CTX001, which targets rare blood diseases and sickle cell disease.

Looking at their timeline, the therapy could be ready for regulatory review by 2023.

Other than CTX001, Vertex and CRISPR have been developing several mRNA-based treatments currently under Phase 2 trials.

Among them, the therapies generating the most excitement are the ones targeting pain and rare kidney diseases.

For acute pain treatments alone, the US market is already worth $4 billion. To this day, the non-opioid medication market remains an extremely attractive space.

Needless to say, a product offering an approved safety profile and high efficacy could easily grab the multi-billion sales potential.

Meanwhile, riding on the momentum of its mRNA programs, Vertex also partnered with Moderna (MRNA) to develop more therapies for rare and hard-to-treat diseases.

While its collaboration with Moderna has yet to reveal its prime candidates, there’s a strong possibility that one of them would be a gene therapy for CF.

CTX001’s addressable market is highly lucrative and still exclusive to hyper-specialized companies.

This top-priced orphan gene-editing treatment could rake in annual sales within the range of $3 billion and $4.5 billion. This estimate covers roughly 3,000 to 4,500 patients every year, with average individual spending of $1 million.

Although this price might sound too steep, keep in mind that CTX001 treats lifelong incurable diseases. Typically, patients spend an average of $200, 000 annually.

If successful, this treatment from Vertex and CRISPR could provide a one-and-done answer to the suffering of these patients, justifying the steep price tag.

Overall, I see Vertex as a stock selling a pretty reasonable price.

Considering its relatively young pipeline, though, this should be seen as a long-term investment—one that has been tested and proven to be successful at targeting multi-billion-dollar markets.

Over the past month, COVID-19 vaccine developers like Pfizer (PFE), Moderna (MRNA), and AstraZeneca (AZN) have offered the world a bit of good news.

For the first time since the pandemic started, we have seen a light at the end of this crisis’ tunnel.

This time around next year, the economy should be close to its normal state.

Before we see the struggling financial market completely recover, you might want to consider buying shares of an under-the-radar COVID-19 vaccine developer that could be on its way to performing better in 2021: Merck (MRK).

Major healthcare and drug stocks rarely get this cheap relative to the S&P 500 in the last 15 years, Merck is a prime example of this once-in-a-blue-moon phenomenon.

Although it was slow to start and report on updates in its COVID-19 vaccine, Merck has been making strides in emerging as a major competitor against Gilead Sciences (GILD) when it comes to developing a COVID-19 drug.

To date, Merck landed a $356 million supply agreement with the US government to deliver 60,000 to 100,000 doses of its oral antiviral drug for COVID-19.

While vaccines are definitely valuable in helping prevent the spread of the virus, there is another important market that healthcare companies are targeting: the hospitalized COVID-19 patients.

With this recent announcement from Merck, it’s obvious that the company has its hands on both the vaccine market and the hospitalized patient group.

In terms of vaccine development, Merck may be behind Pfizer and Moderna but this New Jersey-based titan has one of the leading vaccine franchises in the industry.

The frontrunner in Merck’s vaccine franchise is its cervical cancer vaccine Gardasil, which is estimated to be worth half of its current market value of approximately $200 billion.

The company is also anticipated to record high single-digit earnings growth in the years to come, thanks to the 2021 spinoff of its Organon unit.

Following Pfizer and Mylan footsteps in the newly formed Viatris (VTRS), Organon will be used to unload the slower-growth products from Merck’s current portfolio.

With the purging of its product portfolio of the low-performing treatments comes the expansion of Merck’s R&D courtesy of its $2.75 acquisition of biotechnology startup VelosBio.

Thanks to this deal, Merck will gain access to VelosBio’s prized VLS-101, which is basically a miniature chemotherapy grenade that would disintegrate cancer cells.

This collaboration could turn out into another moneymaker for the company.

Merck is no stranger when it comes to picking winning oncology investments.

The last massive deal it completed was a $1.16 billion deal with AstraZeneca in 2017, with the two companies agreeing to milestone payments of up to $6.15 billion.

This partnership brought to life one of the highest-selling cancer drugs in the world today, Lynparza.

To date, Lynparza is not only used for prostate cancer but also gained expanded approval for breast and pancreatic cancer.

In the third quarter of 2020 alone, even with the pandemic still wreaking havoc everywhere, Merck’s share of profits for Lynparza jumped 59% year over year to reach $196 million—a number that is projected to continue to climb as the drug awaits more approvals from the EU.

Merck offers the most attractive upside case among the healthcare stocks today, with the company projected to report consistent revenue growth until at least 2025.

Moreover, this pharmaceutical company has a strong balance sheet, as seen in its recent acquisitions and potential partnerships still underway.

So far, Merck’s shares are down 12% this year to only $80, with the stock trading 13 times its projected earnings in 2021 at $6.29 per share.

This pharmaceutical giant has a stable dividend yield of 3.3%, which is double the S&P 500.

As the economy continues with its recovery, you can expect Merck to get stronger and the stock should rally sooner rather than later.

Hence, buying it before it completely bounces back could allow you to cash in some spectacular returns.

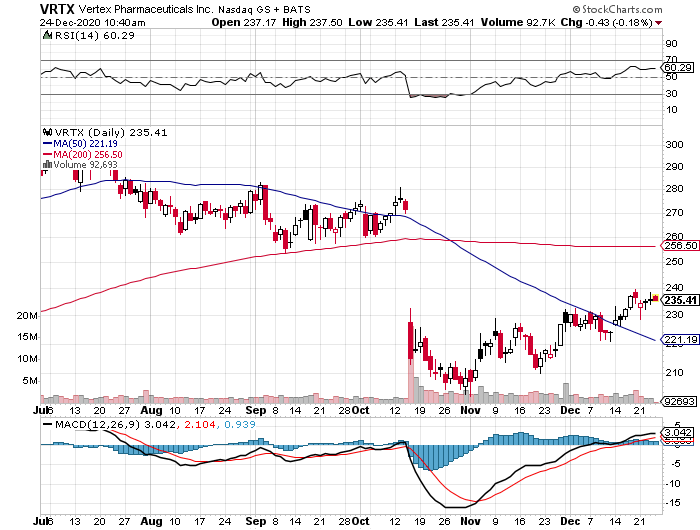

Mad Hedge Biotech & Healthcare Letter

December 24, 2020

Fiat Lux

FEATURED TRADE:

(HOW VERTEX IS CURING THE INCURABLE)

(VRTX), (PTI), (GLPG), (CRSP)

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.

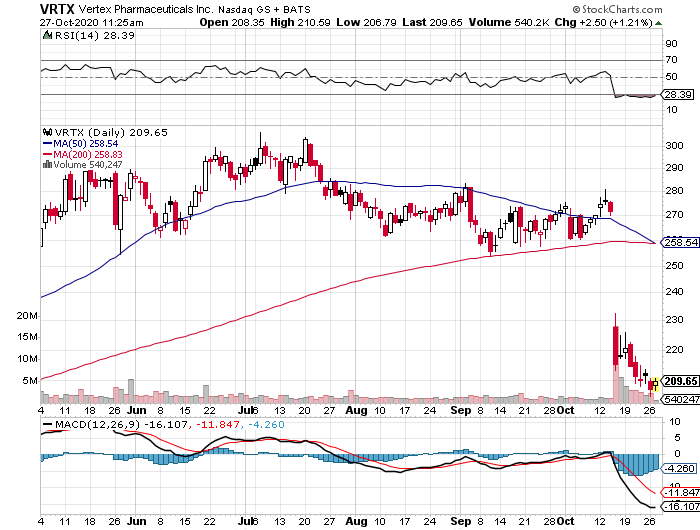

Mad Hedge Biotech & Healthcare Letter

October 27, 2020

Fiat Lux

FEATURED TRADE:

(HOW VERTEX IS CURING THE INCURABLE)

(VRTX), (PTI), (GLPG), (CRSP)

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.