Global Market Comments

February 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GAMBLERS HAVE ENTERED THE MARKET),

($INDU), (TSLA), (TLT), (BA), (JPM), (MS), (GME), (STBX), (GE), (MRNA)

Global Market Comments

February 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GAMBLERS HAVE ENTERED THE MARKET),

($INDU), (TSLA), (TLT), (BA), (JPM), (MS), (GME), (STBX), (GE), (MRNA)

At long last, the 10% correction I have been predicting is happening. No, it wasn’t caused by the usual reasons, like a bad economic data point, an earnings disappointment, or a geopolitical event.

The market delivered the worst week since October because gamblers have entered the stock market. Perish the thought!

It turns out that if a million kids buy ten shares each of a $4 stock, they can wipe out even the largest hedge funds on their short positions. It also turns out they can wipe out their brokers, with infinite capital calls triggered by massive order flows.

If Chicago’s Citadel had not stepped in with a $1 billion bailout, Robin Hood would have gone under last week. Citadel buys Robin Hood’s order flow and is their largest customer. That’s where systemic risk enters the picture.

And it’s not like there was really any systemic risk. Markets have an inordinate fear of the unknown, and no one has ever seen a bunch of kids in a chat room like Redditt wipe out major hedge funds.

Fortunately, there are only a dozen small illiquid stocks that could be subject to such ‘buyers raids”. So, the spillover to the main market is very limited, probably no more than a week or two.

And the regulations to reign in such a practice are already in place. Whenever a broker gets more business than it can handle, it will simply shut it down. Robin Hood did that on Friday when it has limited purchases in 20 stocks to a single share, including Starbucks (STBX), Moderna (MRNA), and General Electric (GE).

What all this does is set up an excellent buying opportunity for you and me, of which there have been precious few in recent months. By ramping up the Volatility Index to $38, it is almost impossible to lose money on front month call options spreads. We are the real winners of the (GME) squeeze.

Stocks would have to fall another 10%-20% on top of existing 10%-20% declines, and that is not going to happen in 13 trading days to the February 19 options expiration with $20 trillion about to hit the economy and the stock markets. That breaks down to $10 trillion in stimulus and $10 trillion worth of global quantitative easing.

My own long, hard-won experience is that a (VIX) at $38 earns you about 20% a month in profits. Options prices are so elevated that scoring winners now is like shooting fish in a barrel. So, join the party as fast as you can.

On Friday, I was taking profits on exiting positions and shipping out new trade alerts in the best quality names as fast as I could write them. Where is that easy, laid back retirement I was hoping for!

Keep at the barbell portfolio. The big tech names are finishing up a six-month sideways “time” corrections. Their earnings are catching up with valuations at a prolific rate. The domestic recovery names have just given back 10%-20% and are ripe for another leg up. All of these are good candidates for 2023 options LEAPS.

After all, if an insurrection and the sacking of the capitol can’t take the market down more than 1%, GameStop (GME) is certainly not going to take it down more than 10%.

GameStop (GME) posted record volatility, up from $4 a month ago to $483. Even the biggest hedge funds can’t stand up to a million kids buying ten shares each at market. All single name shorts in the market are getting covered by hedge funds in fear of getting “Gamestopped”, producing a 700-point Dow rally.

Several brokers banned trading in the name and the SEC is all over this like a wet blanket. Trading is halted due to an excess of sell orders. The problem is that funds are selling real stocks to cover the losses we own, like JP Morgan (JPM) and Tesla (TSLA) and short (TLT).

In the meantime, the action has moved over the American Airlines (AA), which has soared by 50%. AMC Entertainment Holdings (AMC) saw a 400% pop, but I haven’t seen anyone rushing back into theaters to watch Wonder Woman. Blame Jay Powell for flooding the financial system with mountains of cash seeking a home. There is so much money in circulation that traders are invented asset classes to put it into. This can’t last. Buy the dip.

Here are the best short squeeze targets with the greatest outstanding short interests. GameStop (GME) tops the list with an eye-popping 139% short interest, followed by Bed Bath & Beyond (BBBY) (67%) and Ligand Pharmaceutical (LGND) (64%). National Beverage (FIZZ), The Macerich Company (MAC), and Fubo TV (FUBO) bring up the rear. These are all failed companies in some form or another, which is why hedge funds had such large short positions.

New Home Sales disappointed in December, up only 1.6% to 842,000 units. This is on a signed contract basis only. Affordability is the big issue caused by high prices. Who buys a house at Christmas anyway?

Case Shiller soared by 9.5% in November, the fastest home price appreciation in history. Phoenix (13.8%), Seattle (12.7%), and San Diego (12.3) were the big movers. Blame a long-term structural housing shortage, a huge demographic push from Millennials, near-zero interest rates, and a flight from the cities to larger suburban homes. The Pandemic is keeping millions of homes off the market.

US GDP may reach pre-pandemic high by end of 2021, it the vaccine gets distributed to every corner of the nation and aggressive stimulus packages pass congress. Growth should come in at a minimum of 5% or higher this year, wiping out last year’s disaster. Keeping interest rates near zero will be a big help, as Treasury Secretary Yellen is determined to do. China and India are already there.

Share Buybacks have returned, the catnip of share prices. Q4 saw a jump to $116 billion from $102 billion in Q2, and this year, banks now have free reign to buy back their own shares. That’s still below the $182 billion seen in Q4 2019. It can only mean that share prices are rising further.

California lifts stay-at-home regulations, enabling restaurants to open after a nearly two-month shutdown. It’s the first ray of hope that the pandemic will end by summer. It will if Biden hits his 1.5 million vaccinations a day target.

Tesla posts sixth consecutive profit quarter, taking the stock down $60 in the aftermarket momentarily on a classic “buy the rumor, sell the news” move. The once cash-starved company now has an eye-popping $19.4 billion in reserves. Revenues reached a massive $10.7 billion, better than expected. Gross margins reached 19.2%. Looking for 50% annual growth for several years. Shanghai, Berlin, and Austin will make their first deliveries this year. Cash flow is at $19.4 billion, enough to build six more factories. No short sellers left here. It’s a perfect entry point for a LEAP. Buy the March 2023 $1,150-$1,200 call spread for a ten bagger.

Space X rocket carries 143 spacecraft into space. The Falcon 9 rocket set a new record with new satellites launched at once. Yes, you too can put 200kg into orbit for only $1 million. Many are from small tech startups selling various types of data. Elon Musk’s hobby, now worth $20 billion according to its government contracts, could be his next IPO. Don’t pass on this one!

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned a blockbuster 10.21% in January, versus a Dow Average that is now down in 2021. This is my third double-digit month in a row.

I used the market selloff to take substantial profits in my short (TLT) holdings and buy new longs in Boeing (BA) and Morgan Stanley (MS). I rolled the strikes down on my JP Morgan (JPM) long by $10.

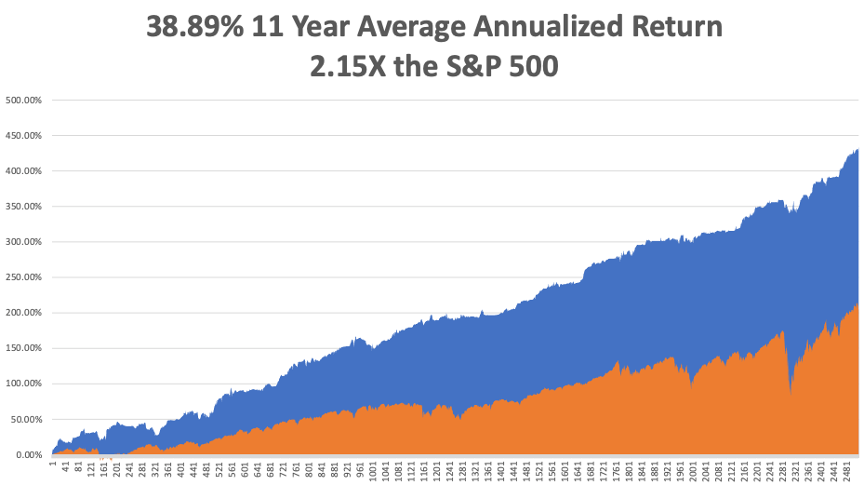

That brings my eleven-year total return to 432.76%, some 2.15 times the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.85%, a new high.

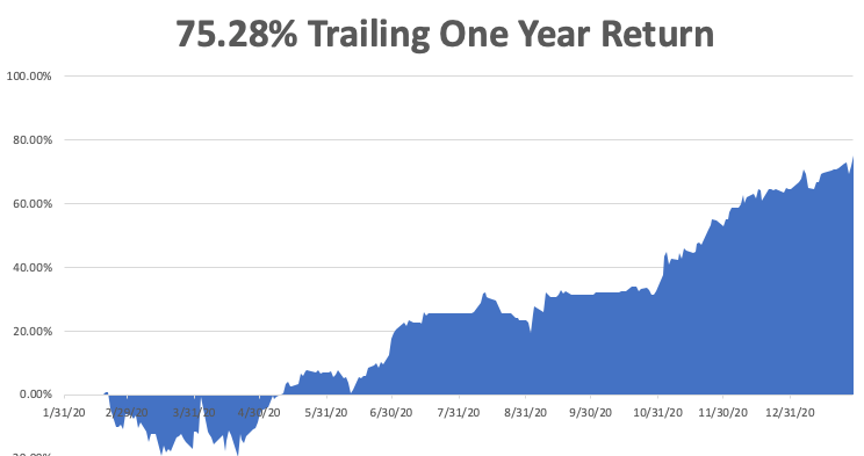

My trailing one-year return exploded to 75.28%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 91.43% since the March 20 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 26 million and deaths at 440,000, which you can find here. We are now running at a staggering 3,800 deaths a day.

The coming week will be all about the monthly jobs data.

On Monday, February 1 at 9:45 AM EST, the Markit Manufacturing PMI for January is out. Caterpillar (CAT) announces earnings.

On Tuesday, February 2 at 7:00 AM, Total Vehicle Sales for January are published. Alphabet (GOOG) and Amgen (AMGN) report.

On Wednesday, February 3 at 8:15 AM, the ADP Private Employment Report is published. QUALCOMM (QCOM) reports.

On Thursday, February 4 at 9:30 AM, Weekly Jobless Claims are printed. Gilead Sciences (GILD) reports.

On Friday, February 5 at 9:30 AM, the January Nonfarm Payroll Report is announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I am often kept awake at night by painful arthritis and a collection of combat injuries and I usually spend this time thinking up new trade alerts.

However, the other night, I saw a war movie just before I went to bed, so of course, I thought about the war. This prompted me to remember the two happiest people I have met in my life.

My first job out of college was to go to Hiroshima Japan for the Atomic Energy Commission and interview survivors of the first atomic bomb 29 years after the event. There, I met Kazuko, a woman in her late forties who was attending college in Fresno, California in 1941 and spoke a quaint form of English from the period. Her parents saw the war and the internment coming, so they brought her back to Hiroshima to be safe.

Her entire family was gazing skyward when a sole B-29 bomber flew overhead. One second before the bomb exploded, a dog barked and Kazuko looked to the right. Her family was permanently blinded, and Kazuko suffered severe burns on the left side of her neck, face, and forearms. A white summer yukata protected the rest of her, reflecting the nuclear flash. Despite the horrible scarring, she was the most cheerful person I had ever met and even asked me how things were getting on in Fresno.

Then there was Frenchie, a man I played cards with at lunch at the Foreign Correspondents Club of Japan every day for ten years. A French Jew, he had been rounded up by the Gestapo and sent to the Bergen-Belson concentration camp late in the war. A faded serial number was still tattooed on his left forearm. Frenchie never won at cards. Usually, I did because I was working the probabilities in my mind all the time, but he never ceased to be cheerful no matter how much it cost him.

The happiest people I ever met were atomic bomb and holocaust survivors. I guess, if those things can’t kill, you nothing can, and you’ll never have a reason to be afraid again. That is immensely liberating.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

January 27, 2021

Fiat Lux

Featured Trade:

(DINOSAURS OF TECH REINVENTING THEMSELVES)

(BB), (AMZN), (BIDU), (GME)

Tech companies change so quickly that sometimes companies have no choice but to reinvent themselves and that is exactly what BlackBerry (BB) has done as their stock has already delivered gains of 190% in 2021.

Historically known as a hardware business, BlackBerry decided to opt out of its legacy operations and elect for a push into enterprise software, internet of things (IoT), and cybersecurity, pivoting away from handsets as that business flagged.

That is where all the serious tech money is these days.

A torrent of positive announcement has rallied investors to this stock with the company announcing an expanded partnership with Baidu (BIDU) that will see it continue working on automated high-definition mapping software that Baidu uses in its autonomous driving technology.

Baidu is a Chinese tech company that is also hoping to reinvent themselves away from their legacy business of internet search.

Data and connectivity are opening new avenues for innovation in the automotive industry, and BlackBerry and auto companies share a common vision to provide automakers and developers with optimal data so that they can deliver new services to consumers.

The tie-up with Baidu caused the stock to shoot higher by 17.3% at $21.15 in premarket trading.

This move broadens the company's use of BlackBerry’s operating system in its "Apollo" autonomous driving open platform.

Under the expanded partnership, Baidu’s high-definition map will be integrated with BlackBerry’s QNX Neutrino real-time operating system.

The integrated system will be mass-produced and available on Guangzhou Automobile Group electric vehicle arm’s upcoming GAC New Energy Aion models.

The BlackBerry QNX software scores high in functional safety, network security, and reliability, while Baidu has achieved long-term development in artificial intelligence and deep learning.

GAC is one of China’s largest automakers. It also manufactures the Hycan 007 cars under a joint venture with EV startup NIO.

This is just an example of how BB is running to the part of the end zone where the ball is going to be thrown unlike other dinosaur tech like IBM.

The company’s stock has recently been included in strong dialogue on online message boards such as Reddit, which like GameStop (GME) has felt a sharp appreciation in price or probably better describes as rocket boosters.

GME is up 100% just today which can only be described as an epic short squeeze.

At a strategic level, the success of BlackBerry’s stock can be attributed in part to the strategic shift to cybersecurity and the Internet of Things.

The shift away from handheld devices is long due, and so what's really happening is the market is putting its stamp of approval on this new shift of BlackBerry away from its old business model and what it’s doing now.

BB holds more patents than any other company in Canada.

BlackBerry shares spiked as much as 20% after settling a patent infringement suit with Facebook.

BlackBerry first targeted Facebook with a lawsuit back in 2018, filing a 117-page complaint accusing the social network of infringing on Blackberry's innovative messaging technology.

The settlement removed any litigious uncertainty offering another clear pathway for the stock to rise.

The biggest strategic overhaul has been its recent partnerships with Amazon (AMZN) Web Services in December to use its cloud services.

They signed an agreement with Amazon for BB to develop a software platform that allows automakers to read vehicle sensor data, improving cloud-connected vehicles' performance.

Blackberry announced it sold 90 patents to China's largest phone manufacturer, Huawei.

Automakers can use this information to create responsive in-vehicle services that enhance driver and passenger experiences.

BlackBerry IVY addresses a critical data access, collection, and management problem in the automotive industry.

Cars and trucks use many different parts, with each vehicle model comprising a unique set of proprietary hardware and software components.

These components, which include an increasing variety of vehicle sensors, produce data in unique and specialized formats.

The highly specific skills required to interact with this data, as well as the challenges of accessing it from within contained vehicle subsystems, limit developers’ abilities to innovate quickly and bring new solutions to market.

BlackBerry IVY will solve these challenges by applying machine learning to that data to generate predictive insights and inferences, making it possible for automakers to offer in-vehicle experiences that are highly personalized and able to take action based on those insights.

Although many legacy tech companies get caught in the weeds, never to grow again. BB has sorted out its vision and is well on its way to delivering shareholder value back to the end investor.

Even though I would say the short-term price action in BB is at this point euphoric, it would serve any tech investor well to dip their toe into this stock long term when there is a pullback.

Mad Hedge Technology Letter

June 6, 2019

Fiat Lux

Featured Trade:

(THE SHAKEOUT IN GAME STOCKS)

(GME), (MSFT), (GOOGL), (APPL), (STX), (WDC)

Do not invest in any video game stocks that don’t make video games.

If you want to simplify today’s newsletter down to the nuts and bolts, then there you go.

The company that I have been pounding on the table for readers to sell on rallies has convincingly proven my forecast right yet again with GameStop (GME) capitulating 35%.

It’s difficult to find a tech company with a strategic model that is worse than GameStop’s, and my call to short this stock has been vindicated.

Other competitors that vie for awful tech business models would be in the hard disk drive (HDD) market, and that is why I have been ushering readers to spurn Western Digital (WDC) and Seagate Technology (STX).

This is a time when everybody and their grandmother are ditching hard drives and migrating to the cloud, while GameStop is a video game retailer who is set up in malls that add zero value to the consumer.

This also dovetails nicely with my premise that broker technology or in this case retail brokers of physical video games are a weak business to be in when kids are downloading video game straight from their broadband via the cloud and don’t need to go into the store anymore.

Let’s analyze why GameStop dropped 35%.

The rapid migration of the digital economy does not have room to accompany GameStop’s model of retail video game stores anymore.

It’s a 1990 business in 2019 – only twenty years too late.

This model is being attacked from all fronts - a live sinking ship with no life vests on board.

GameStop was already confronted with a harsh reality and pigeonholed into one of a handful of companies in need of a turnaround.

This isn’t new in the technology sector as many legacy firms have had to reinvent themselves to spruce up a stale business model.

The earnings call was peppered with buzz words such as “transformation” and “strategic vision.”

And when the Chief Operating Officer Rob Lloyd detailed the prior quarter’s results, it was nothing short of a stinker.

Total quarterly revenue dropped 13.3% in Q1 2019 which was down from the prior year of 10.3%.

The headline number did nothing to assuage investors that the ship is turning around, it appears as if the boat is still drifting in reverse.

Diving into the segments, underperformance is an accurate way to capture the current state of GameStop with hardware sales down 35%, software sales down 4.3% and selling pre-owned products declining 20.3%.

Poor software sales were blamed on weaker new title launches this year and comping the strong data war launched last year with increasing digital adoption.

The awful hardware sales were pinned on the late stages of the current generation PS4 and Xbox One cycle with GameStop awaiting an official launch date announcement from Sony and Microsoft for their new console products.

Pre-owned business fell off a cliff reflecting tepid software demand for physical games and the increasing popularity of the various digitally offered products via alternative channels.

The only part of GameStop going in the right direction is the collectibles business that increased 10.5% from last year but makes up only a minor part of the overall business.

Management has elected to remove the dividend completely to freshen up the balance sheet slamming the company as a whole with a black eye and giving investors even less reason to hold the stock.

Indirectly, this is a confession that cash might be a problem in the medium-term.

The move to put the kibosh on rewarding shareholders will save the company over $150 million, but the ugly sell-off means that investors are leaving in droves as this past quarter could be the straw that broke the camel’s back.

They plan to use some of these funds to pay down debt, and GameStop is still confronted by a lack of transformative initiatives that could breathe life back into this legacy gaming company.

It was only in 2016 when the company was profitable earning over $400 million.

Profits have steadily eroded over time with the company now losing around $700 million per year.

Management offered annual guidance which was also hit by the ugly stick projecting annual sales to decline between 5-10%.

GameStop is on a fast track to irrelevancy.

If you were awaiting some blockbuster announcements that could offer a certain degree of respite going forward, well, the tone was disappointing not offering investors much to dig their teeth into.

Remember that GameStop is now on a collision course with the FANGs who have pivoted into the video game diaspora.

GameStop will see zero revenue from this development and a boatload of fresh competition.

Microsoft (MSFT) has been a mainstay with its Xbox business, but Apple (AAPL) and Google are close to entering the market.

Google (GOOGL) plans to leverage YouTube and install gaming directly on Google Chrome with this platform acting as a new gaming channel.

The new gaming models have transformed the industry into freemium games with in-game upselling of in-game items, the main method of capturing revenue.

The liveliest example of this new phenomenon is the battle royale game Fortnite.

Nowhere in this business model includes revenue for GameStop highlighting the ease at which game studios and console makers are bypassing this retailer.

In this new gaming world, I cannot comprehend how GameStop will be able to stay afloat.

Unfortunately, the move down has been priced in and at $5, the risk-reward to the downside is not worth shorting the company now.

The company is the poster boy for technological disruption cast in a negative light and the risks of not evolving with the current times.

Mad Hedge Technology Letter

December 12, 2018

Fiat Lux

Featured Trade:

(WHY GAMERS ARE TAKING OVER THE WORLD)

(EA), (TTWO), (ATVI), (GME), (MSFT)

I nailed it.

The video game migration has been nothing short of bonkers for the average onlooker who has no interest in gaming.

Personally, I can’t really fathom spending every waking moment in front of a screen playing a game, but I was born in a different generation.

But for the younger generations, this is completely normal and a standard way to use extracurricular time.

This behavior is the origin hewing together a broader thesis of investing in behemoth video game companies boasting premium gameplay and high-quality content.

As the year inches closer to the finish line, I would have been proved correct if it wasn’t for one surprise that nobody could have ever predicted.

Enter Fortnite.

Fortnite has reigned supreme in 2018 and single-handedly tarnished the performance of the powerful trio of Electronic Arts (EA), Activision Blizzard (ATVI), and Take-Two Interactive (TTWO).

The multiplayer battle royale game is produced by Epic Games, an American video game developer based in Cary, North Carolina and this small town in Chatham County owns the video game world right now.

Funnily enough, the company was created by Tim Sweeney in 1991 in his parents' basement in Potomac, Maryland.

Epic Games blindsided the video game industry who believed barriers of entry were too high, and an outsider would have no chance to steal legitimate market share from the incumbents.

They thought wrong because Epic Games has done exactly that and more.

Instead of splurging on a pricey console and game titles, Fortnite has followed the cloud industry’s blueprint with a freemium model as an introductory way to lure in new users.

This must have Sony and Microsoft tearing their hair out because it could potentially rule the Xbox One and PS4 consoles obsolete.

How easy is it to play Fortnite?

Simply download and install the game for free on your Xbox One, Nintendo Switch, PlayStation 4, iPhone, Android, or Mac by opening the respective app store and selecting “Fortnite.”

That’s right, you can play this game on almost any platform appealing to the masses of fans.

Does this freemium model mean that Epic Games misses out on revenue?

Absolutely not.

The freemium model is just the conversional entry point to lure in new gamers.

Epic Games profits by selling in-game currency named V-Bucks or Vinderbucks used for purchasing items from the in-game Vindertech Store in Save the World, or to pocket cosmetic items from the Item Shop and the Battle Pass in Battle Royale.

V-Bucks revenue has been piling up with global gamers spending an average of $1.23 million per day in the iOS version for the month of November.

The number of total gamers recently eclipsed the 200 million mark and the previous recorded number was in June when Fortnite users totaled 125 million.

The 60% surge in five months has been the main catalyst for large video game makers to experience violent sell-offs because there is a direct correlation between growing Fortnite users and cratering usership from the traditional players.

Then throw in the mix of the secret recipe to Fortnite’s success - the mind-numbing speed and impact of the online updates enhancing the game; adding and adjusting weapons, providing new cosmetic items for players to buy and altering the game map.

Not only did Epic draw in new players in waves, it retained them just as well.

Putting the cherry on top, Fortnite made major cultural inroads into mainstream society legitimizing this title as the game of 2018.

This was evident during the Russia FIFA World Cup where star soccer players were doing Fortnite dances after scoring critical goals.

Put it this way, the game hasn’t even been allowed in China and is expected to earn over $2 billion in 2018.

As we speak, millions more plan to migrate from their former games enticed by the free battle royal platform.

The game is nothing short of a cultural phenomenon and none of the major video game developers can keep up.

Take-Two Interactive even had a smash hit come online with Red Dead Redemption 2, a Western-themed action-adventure game developed and published by Rockstar Games, lighting up screens all over the world.

Not even that could taper off the enthusiasm for Fortnite.

Activision cannot keep its gamers from jumping ship.

The mainstay game developer announced a major contraction of users from 345 million monthly active users for top games in its Candy Crush, World of Warcraft and Call of Duty franchises in the third quarter sharply down from 352 million users in the second quarter and 384 million users a year ago.

GameStop (GME) who recently slashed its full-year 2019 earnings outlook faces a grim 2019 as shares are down about 25% this year.

I perfectly predicted this and in almost every scenario, GameStop’s future looks ugly unless they do some major surgery to the business model.

There is no room for video game brokers anymore in this cloud-based world.

This is because new game studios will follow the Epic Games blueprint and bypass consoles all together and offer games for free.

The cloud will be the new go-to device for playing video games, and gamers will download games straight from the cloud via wireless broadband.

This trend is set to mushroom when 5G comes online in 2019 and 2020, connection speeds are expected to be 100 times faster than current 4G speeds.

In fact, the new consoles currently being developed by Nintendo, Microsoft, and Sony could be the last game consoles ever developed before they go extinct.

The digital revolution promises that hardware becomes incrementally slimmed down with every iteration until at some point there will be no hardware at all.

We have seen this trend in consumer devices with the smartphone, television, and desktop computer amongst other products.

This is why Microsoft (MSFT) has been busy buying up video game content producers, and confident in this sense that gold standard content truly is king.

It makes sense to put in more irons in the fire to potentially score a culture-shifting game like Fortnite. Not every video game will be a blockbuster hit, but the more video game developer Microsoft buys, there will be a higher chance of dominating the video game market.

Fortnite’s disruption of Activision, EA, and Take-Two Interactive signals a new beginning of the end for the traditional video game developers.

Darkhorse game developer could sprout up out of nowhere even more in 2019 offering console-less free games and leaner, nimbler models.

How are console manufacturers and game developers expected to keep up with the surge in gaming expectation?

The answer is they will not and look for these big three developers to attempt to stem the bleeding as Fortnite is expected to become even more thrilling next year tearing away more gamers from other systems in a dog-eat-dog world.

And then there is the possibility of the FANGs crossing over to gaming, searching for new growth drivers which would really flatten these shares like a pancake.

Microsoft is already deep into this industry, why wouldn’t their cousins follow them to profits too?

Ultimately, I am bearish on Activision, Electronic Arts, and Take-Two Interactive going into 2019 unless there is an upside catalyst that magically appears.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

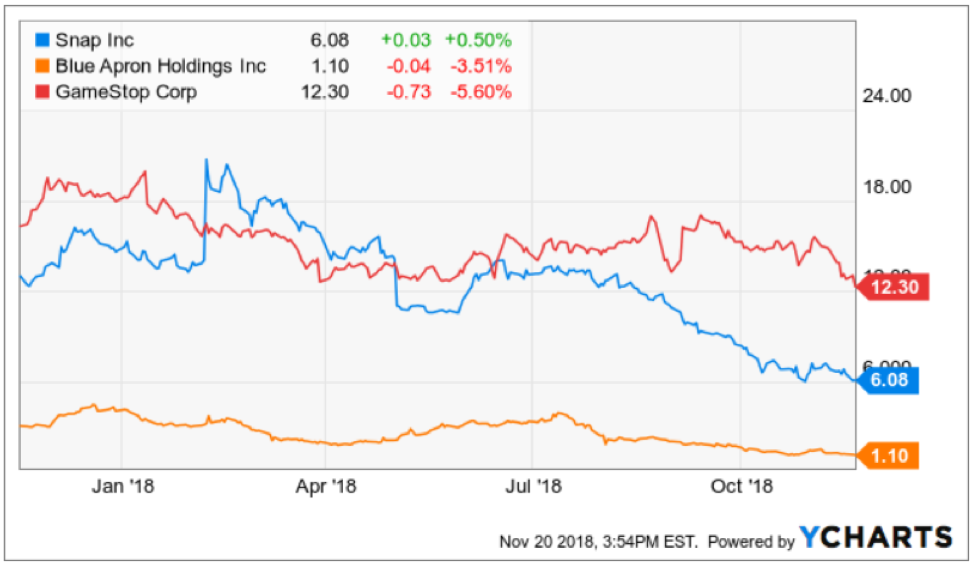

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.