Global Market Comments

January 9, 2023

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE “PULL FORWARD” MARKET)

(AAPL), (TLT), (TSLA), (BRKB), (GOLD), (WPM), (QQQ), (VIX)

Global Market Comments

January 9, 2023

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE “PULL FORWARD” MARKET)

(AAPL), (TLT), (TSLA), (BRKB), (GOLD), (WPM), (QQQ), (VIX)

The market went into the new year short. After listening to dire forecasts for 2023 and January in particular, institutional investors raised cash and hedge funds sold short. That was made clear by the explosive move up in the market on Friday.

Those blinkered by a short-term view got slaughtered. Those who pursued my own long-term view expounded in my Wednesday, January 4 letter made a killing.

The December Nonfarm Payroll Report was the trigger. The headline numbers were just warm, not hot. But the average hourly earnings dropped by half, meaning workers are getting hired at lower pay levels. If we get an even modest inflation print at 8:30 AM on Thursday, January 12, you could get another gap up move in “RISK ON” markets.

The financial markets continue “pull forward movement” as they did for much of the second half of 2022.

The post-Election rally happened in October.

The Santa Claus rally took place in November.

The New Year January selloff struck in December, closing the year near a low.

What happens next?

Another dive at the lows will attack in February.

This is typical of bear markets where liquidity is thin, trading is dominated by a handful of professionals and algorithms, and individual investors are missing in action.

What is most puzzling even to me is how the Volatility Index (VIX) is remaining artificially low at $22. Is the index storing up volatility for a future run at $30 or $40?

We shall see.

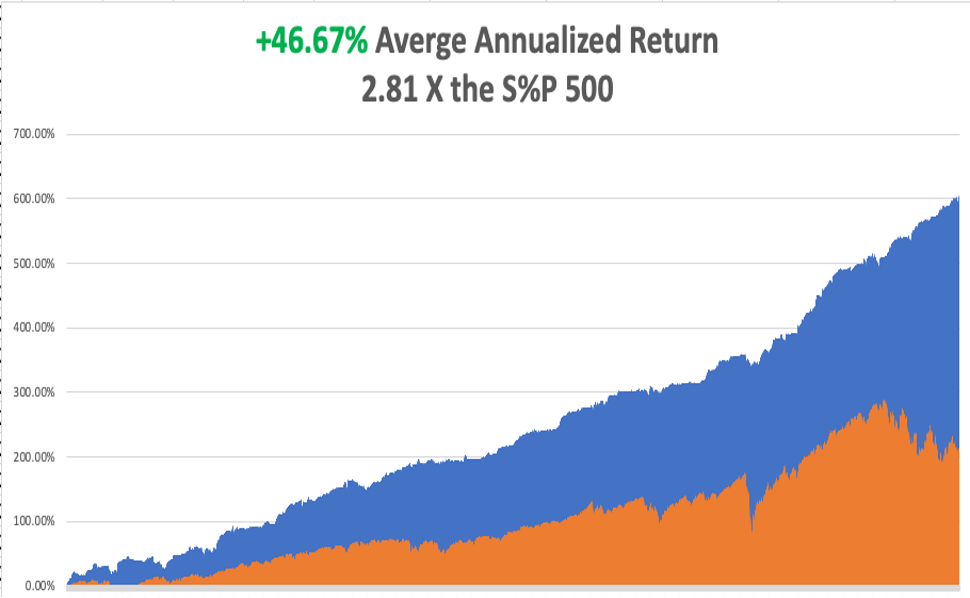

My performance in January has so far tacked on an explosive +13.39%. My 2023 year-to-date performance was the same at +13.39%, a spectacular new high. The S&P 500 (SPY) is up +2.29% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +98.02%.

That brings my 15-year total return to +610.58%, some 2.81 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.67%, easily the highest in the industry.

I used the new year to go maximum bullish. First, I covered my short in Apple (AAPL) for a nice profit. I took my weighting in long bonds (TLT) up to 50%, which then nicely went ballistic. I also poured on new longs in Tesla (TSLA), Berkshire Hathaway (BRKB), and the metals stocks Barrick Gold (GOLD) and Wheaton Precious Metals (WPM).

That leaves me 90% long and 10% in cash, which I am holding back to add a new short in the (QQQ) at the next market top.

I have been getting a lot of questions about the chaos in the US House of Representatives. It greatly raises the risk of a default on US government debt by the summer and certainly casts a shadow over my 50% long bond position.

It also makes a government shutdown a sure thing, which is a big market negative. However, I don’t expect it to last more than a month.

The US government is basically a big recycling machine which sucks money from the coasts and spends it inland. For example, New York and California get back 75 cents of every tax dollar they send to Washington, while Wyoming and North Dakota get $1.25. They have long distances and few people. The big winners are Alaska and Hawaii, which get back $7.00 and $8.00 because of massive infrastructure and military spending.

Once red states see cash flow from the federal government dry up, opposition to a budget deal will dry up. It always does, usually after one billing cycle.

But if prices flatline and don’t fall, I’ll still make my maximum profit. I’ll just get less sleep at night.

Nonfarm Payroll Report Comes in Warm at 223,000 for November, presenting markets with a Goldilocks scenario. The Headline Unemployment Rate fell to an eye-popping 3.5%, a post-Covid low. Average hourly earnings dropped by half to 0.3% and up 4.6% YOY. No stock market crash here. If the Fed is trying to cause mass joblessness with high interest rates to kill inflation, it’s failing miserably.

Tesla to Announce Fifth Factory in Mexico, near Monterey, the Detroit of Mexico. The move is an important step in taking Tesla to an annual production of 20 million units a year, or 20% of the global car market by 2030. Construction should cost $10 billion - $20 billion. The move is a stroke of genius and is reminiscent of the old Elon Musk. By setting up in Mexico, Tesla can gain ample cheap skilled labor from the General Motors, Ford, and Hyundai factories already there. They negotiated priority customs clearance for parts coming into Mexico and finished cars headed north by rail. It is close to Texas where Tesla is already ramping up production at an Austin plant. The most likely product will be the hot-selling Model Y.

Tesla Suspends Production at Shanghai Plant in response to a rampant Covid-19 wave far worse than disclosed. The Beijing government claims only 2.5 million cases in 2022. But a leaked top-secret report says the true figure is closer to 250 million. The final capitulation selloff in Tesla is at hand. Buy calls, call spread, shares, and two-year LEAPS.

Tesla Q4 Sales Come in Short, delivering 405,278 and 1.3 million for all of 2023. The slight miss took the shares down an astounding 14%, a huge overreaction. The stock is now selling for 22 times 2023 earnings and 11 times 2025 earnings, compared to an average of 17 times earnings for the top four tech companies. That’s an eye-popping 35% discount to big tech. It’s certainly worth taking a risk going long here for a company that is still growing earnings by 40% a year.

Japan Reverses 30-Year Easy Money Policy, allowing interest rates to float up from 0.25% to 0.50%. The Japanese yen soared 4% on the move, the world's most shorted currency, which hedge funds used to fund all positions. US bonds tanked $5 in two days, as Japan is the largest buyer of US Treasury bonds (TLT). Higher rates may bring some of that money back to Japan. It’s all an indication that the US dollar has hit a decades-long peak.

Existing Home Sales Collapse, down 7.7% in November to a seasonally adjusted 4.09 million units. They are off 35.4% YOY. The median sales price is still rising, up 3.5%, to $370,700. Supplies are still tight, so 61% of homes sold in less than a month.

Wells Fargo Gets Tagged for $3.7 Billion, in fines for its seemingly never-ending supply of past offenses. The shares dropped 10% on the news. Avoid (WFC) for now. There are better banks to buy, like (JPM), (BAC), and (C).

Shipping Costs Dive 40%, as supply chain problems end. Container prices from China cratered from $40,000 to $6,000. The market is now discounting a 2023 recession when nobody buys anything. Some retailers are dropping prices by 70%-80%, especially in clothing. The pandemic era over-ordering has come back to haunt buyers.

Case Shiller Drops to 9.24% Annual Gain in October with its National Home Price Index, the fourth consecutive monthly decline. Miami (+21.0%), Tampa (+20.5%), and Charlotte (15.0%) led the gains. The price increase rate has dropped by half in a year.

Fed Minutes Remain Restrictive at the December 12 meeting, with inflation cited as the greatest threat to the economy. Actually, I think the Fed is the threat. All governors voted to maintain a tight policy. They cautioned against an unwarranted early easing. They cited “data dependence,” meaning that when the recession hits in the coming year, they will lower rates then expect a below-trend growth for 2023. Not what a bull wanted to hear.

Natural Gas Crashes, down 10% on the first trading day of 2023 to a new one-year low. Oil also took a 3% hit. The European gas crisis is over and energy markets are discounting a Russian surrender sometime this year. Gas may also be discounting a full-blown recession and warmer weather to come. Avoid all energy plays like the plague. Gas is now cheaper than coal in a race to the bottom.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy is decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 9 at 8:00 AM, the Consumer Inflation Expectations are published.

On Tuesday, January 10 at 8:30 AM, the NFIB Business Optimism Index is out

On Wednesday, January 11 at 8:00 AM, a new batch of Mortgage Data is announced.

On Thursday, January 12 at 8:30 AM EST, the Weekly Jobless Claims are announced. So is the Consumer Price Index for December.

On Friday, January 13 at 8:30 AM EST, the Michigan Consumer Sentiment is disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, having visited and lived in Lake Tahoe for most of my life, I thought I’d pass on a few stories from this historic and beautiful place.

The lake didn’t get its name until 1949 when the Washoe Indian name was bastardized to come up with “Tahoe”. Before that, it was called the much less romantic Lake Bigler after the first governor of California.

A young Mark Twain walked here in 1863 from nearby Virginia City where he was writing for the Territorial Enterprise about the silver boom. He described boats as “floating in the air” as the water clarity at 100 feet made them appear to be levitating. Today, clarity is at 50 feet, but it should go back to 100 feet when cars go all-electric.

One of the great engineering feats of the 19th century was the construction of the Transcontinental Railroad. Some 10,000 Chinese workers used black powder to blast a one-mile-long tunnel through solid granite. They tried nitroglycerine for a few months but so many died in accidents they went back to powder.

The Union Pacific moved the line a mile south in the 1950s to make a shorter route. The old tunnel is still there, and you can drive through it at any time if you know the secret entrance. The roof is still covered with soot from woodfired steam engines. At midpoint, you find a shaft to surface where workers were hung from their ankles with ropes to place charges so they could work on four faces at once.

By the late 19th century, every tree around the lake had been cut down for shoring at the silver mines. Look at photos from the time and the mountains are completely barren. That is except for the southwest corner, which was privately owned by Lucky Baldwin who won the land in a card game. The 300-year-old growth pine trees are still there.

During the 20th century, the entire East shore was owned by one man, George Whittell Jr., son of one of the original silver barons. A man of eclectic tastes, he owned a Boeing 247 private aircraft, a custom mahogany boat powered by two Alison aircraft engines, and kept lions in heated cages.

Thanks to a few well-placed campaign donations, he obtained prison labor from the State of Nevada to build a palatial granite waterfront mansion called Thunderbird, which you can still visit today (click here). During Prohibition, female “guests” from California crossed the lake and entered the home through a secret tunnel.

When Whittell died in 1969, a Mad Hedge Concierge Client bought the entire East Shore from the estate on behalf of the Fred Harvey Company and then traded it for a huge chunk of land in Arizona. Today, the East Shore is a Nevada State Park, including the majestic Sand Harbor, the finest beach in the High Sierras.

When a Hollywood scriptwriter took a Tahoe vacation in the early 1960s, he so fell in love with the place that he wrote Bonanza, the top TV show of the decade (in front of Hogan’s Heroes). He created the fictional Ponderosa Ranch, which tourists from Europe come to look for in Incline Village today.

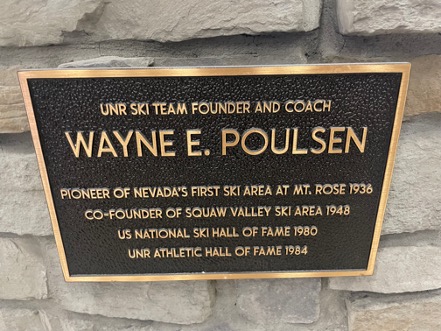

In 1943, a Pan Am pilot named Wayne Poulsen who had a love of skiing bought Squaw Valley for $35,000. This was back when it took two days to drive from San Francisco. Wayne flew the China Clippers to Asia in the famed Sikorski flying boats, the first commercial planes to cross the Pacific Ocean. He spent time between flights at a ranch house he built right in the middle of the valley.

His wife Sandy bought baskets from the Washoe Indians who still lived on the land to keep them from starving during the Great Depression. The Poulsens had eight children and today, each has a street named after them at Squaw.

Not much happened until the late forties when a New York Investor group led by Alex Cushing started building lifts. Through some miracle, and with backing from the Rockefeller family, Cushing won the competition to host the 1960 Winter Olympics, beating out the legendary Innsbruck, Austria, and St. Moritz, Switzerland.

He quickly got the State of California to build Interstate 80, which shortened the trip to Tahoe to only three hours. He also got the state to pass a liability limit for ski accidents to only $2,000, something I learned when my kids plowed into someone, and the money really poured in.

Attending the 1960 Olympics opening ceremony is still one of my fondest childhood memories, produced by Walt Disney, who owned the nearby Sugar Bowl ski resort.

While the Cushing group had bought the rights to the mountains, Poulsen owned the valley floor, and he made a fortune as a vacation home developer. The inevitable disputes arose and the two quit talking in the 1980s.

I used to run into a crusty old Cushing at High Camp now and then and I milked him for local history in exchange for stock tips and a few stiff drinks. Cushing died in 2003 at 92 (click here for the obituary)

I first came to Lake Tahoe in the 1950s with my grandfather who had two horses, a mule, and a Winchester. He was one-quarter Cherokee Indian and knew everything there was to know about the outdoors. Although I am only one-sixteenth Cherokee with some Delaware and Sioux mixed in, I got the full Indian dose. Thanks to him I can live off the land when I need to. Even today, we invite the family medicine man to important events, like births, weddings, and funerals.

We camped on the beach at Incline Beach before the town was built and the Weyerhaeuser lumber mill was still operating. We caught our limit of trout every day, ten back in those days, ate some, and put the rest on ice. It was paradise.

During the late 1990s when I built a home in Squaw Valley, I frequently flew with Glen Poulsen, who owned a vintage 1947 Cessna 150 tailwheel, looking for untouched high-country lakes to fish. He said his mother was lonely since her husband died in 1995 and asked me to have tea with her and tell her some stories.

Sandy told me that in the seventies she asked her kids to clean out the barn and they tossed hundreds of old Washoe baskets. Today Washoe baskets are very rare, highly sought after by wealthy collectors, and sell for $50,000 to $100,000 at auction. “If I had only known,” she sighed. Sandy passed away in 2006 and the remaining 30-acre ranch was sold for $15 million.

To stay in shape, I used to pack up my skis and boots and snowshoe up the 2,000 feet from the Squaw Valley parking lot to High Camp, then ski down. On the way up, I provided first aid to injured skiers and made regular calls to the ski patrol.

After doing this for many winters, I finally got busted when they realized I didn’t have a ski pass. It turns out that when you buy a lift ticket you are agreeing to a liability release which they absolutely had to have. I was banned from the mountain.

Today Squaw Valley is owned by the Colorado-based Altera Mountain Company, which along with Vail Resorts owns most of the ski resorts in North America. The concentration has been relentless. Last year Squaw Valley’s name was changed to the Palisades Resort for the sake of political correctness. Last weekend, a gondola connected it with Alpine Meadows next door, creating the largest ski area in the US.

Today, there are no Washoe Indians left on the lake. The nearest reservation is 25 miles away in the desert in Gardnerville, NV. They sold or traded away their land for pennies on the current value.

Living at Tahoe has been great, and I get up here whenever I can. I am now one of the few surviving original mountain men and volunteer for North Tahoe Search & Rescue.

On Donner Day, every October 1, I volunteer as a docent to guide visitors up the original trail over Donner Pass. Some 175 years later, the oldest trees still bear the scars of being scrapped by passing covered wagon wheels, my own ancestors among them. There is also a wealth of ancient petroglyphs, as the pass was a major meeting place between Indian tribes in ancient times.

The good news is that residents aged 70 or more get free season ski passes at Diamond Peak, where I sponsored the ski team for several years. My will specifies that my ashes be placed in the Middle of Lake Tahoe. At least, I’ll be recycled. I’ll be joining my younger brother who was an early Covid-19 victim and whose ashes we placed there in 2020.

The Ponderosa Ranch

The Poulsen Ranch

At the Reno Airport

Donner Pass Petroglyphs

An Original Mountain Man

Global Market Comments

December 2, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMD), ($INDU), (TLT), (RCL), (VIX), (RIVN), (TSLA), (NVDA), (SLV), (GOLD), (USO), (XOM), (ALB), (SQM), (FMC), (CCI)

Below please find subscribers’ Q&A for the November 30 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: You keep mentioning December 13th as a date of some significance. Is this just because the number 13 is unlucky?

A: December 13th at 8:30 AM EST is when we get the next inflation report, and we could well get another 1% drop. Prices are slowing down absolutely across the board except for rent, which is still going up. Gasoline has come down substantially since the election (big surprise), which is a big help, and that could ignite the next leg up in the bull market for this year. So, that is why December 13 is important. And we could well flatline, do nothing, and take profits on all our positions before that happens, because whatever it is you will get a big move one way or another (and maybe both) on December 13.

Q: I’m a new subscriber, and I am intrigued by your structuring of options spreads. Why do you do debit spreads instead of credit spreads?

A: It’s really six of one and a half dozen of the other—the net profit is pretty much the same for either one. However, debit spreads are easier to understand than credit spreads. We have a lot of beginners coming into this service as well as a lot of seasoned old pros. And it’s easier to understand the concept of buying something and watching it go up than shorting something and watching it go down. Now, doing the credit spreads—shorting the put spread—gives you a slight advantage in that it creates cash which you can then use to meet margin requirements. However, it’s only a small amount of cash—only the potential profit in that position. And guess what? All the big hedge funds actually kind of like easy-to-understand trade alerts also, so that’s why we do them.

Q: I have a lot of exposure in NVIDIA (NVDA), so is it worth trading out of it and coming back in at a lower rate?

A: NVIDIA is one of the single most volatile stocks in the market—it’s just come up 50%. But it could well test the lower limits again because it is so volatile, and the chip industry itself is the most volatile business in the S&P 500. If your view is short-term, I would take profits now, and look to go back in next time we hit a low. If you’re long-term, don’t touch it, because NVIDIA will triple from here over the next 3 years. I should caution you that if you do try the short-term strategy, most people miss the bottom and end up paying more to get back into the stock; and that's the problem with all these highly volatility stocks like Tesla (TSLA), NVIDIA (NVDA) and Advanced Micro Devices (AMD) unless you’re a professional and you sit in front of a screen all day long.

Q: Would you buy now and step in to make it long-term?

A: I think we get a couple more runs at the lows myself. We won’t get to the old lows, but we may get close. Those are your big buying points for your favorite stocks and also for LEAPS. And I’m going to hold back on new LEAPS recommendations—we’ve done 12 in the last two months for the Concierge members, and maybe half of those went out to Global Trading Dispatch before they took off again. So, that would be my approach there.

Q: How much farther can the Fed raise interest rates until they reverse?

A: 1%-2%, unless they get taken over by the data—unless suddenly the economy starts to weaken so much that they panic and reverse like crazy. I think that's actually what’s going to happen, which is why we went hyper-aggressive in October on the long side, especially in bonds (TLT). You drop rates on the ten-year from 4.5% to 2.5% in six months—that’s an enormous move in the bond market. That is well worth running a triple long position in it; I think that’s what's going to happen. That’s where we will make out the first 30% in 2023.

Q: Should I short the cruise lines here, like Royal Caribbean (RCL)?

A: They do have their problems—they have massive debts they ran up to survive the pandemic when all the ships were mothballed, so it is an industry with its major issues. The stock has already doubled since the summer so I wouldn’t chase it up here. I’m not rushing to short anything here right now though unless it’s really liquid or has horrendous fundamentals like the oil industry, which everyone seems to love but I hate—right now the haters are winning for the short term, until December 16, which is all I care about.

Q: Is the diesel shortage going to affect farmers and all other industries like the chip?

A: As the economy slows down, you can expect shortages of everything to disappear, as well as all supply chain issues, which is a positive for the economy for the long term.

Q: What about the 2024 iShares 20 Plus Year Treasury Bond ETF (TLT) 95—is that not a trade?

A: That’s a one-year position with a 100% potential profit. That is worth running to expiration unless we get a huge 20-point move up in the next 3 months, which is possible, and then there won’t be anything left in the trade—you’ll have 95% of the profit in hand at which point you’ll want to sell it. So, with these one-year LEAPS or two-year LEAPS, run them one or two years unless the underlying suddenly goes up a lot, and then grab the money and run; that's what I always tell people to do. Because if you sell your position, they can’t take the money away from you with a market correction.

Q: Is the current US economy the best economy in the world?

A: It is. If you look at any other place in the world, it’s hard to find an economy that's in better shape, and it’s because we have the best management in the world and hyper-accelerating technology which everyone else begs and borrows. Or steals. People who are predicting zero return on stocks for 10 years are out of their minds. You don’t short the best economy in the world. If anything, technology is accelerating, and that will take the stock market with it in the next year or so.

Q: Do you see the Dow ($INDU) outperforming the other indexes until the Fed positive pivots?

A: Absolutely yes, because the S&P 500 (SPY) has a very heavy technology weighting and technology absolutely sucks right now. That would probably be a good 3-month trade—buy the Dow, and short the S&P 500 in equal amounts. Easy to do—you might pick up 10% on a market-neutral trade like that.

Q: Do you see a Christmas rally this year?

A: Actually, I do, but it won’t start until we get the next inflation report on December 13, at which point I'm going 100% cash. I’ve made enough money this year, and this is a problem I had when I ran my hedge fund: when you make too much money, nobody believes it, so there's really no point in making more than 50% or 60% a year because people think it’s fake. This is true in the newsletter business as well. Markets also have a nasty habit of completely reversing in January; this year, we had one up day in January, and then it was bombs away and we just piled on the shorts like crazy, so you have to wait for the market to first give you the fake move for the year, and then the real one after that. The best way to take advantage of that is to be 100% cash, and that’s why I usually do.

Q: What indicators do you see that give you the most confidence that inflation has peaked?

A: There's one big one, and that’s real estate. Real estate is absolutely in a recession right now and has the heaviest weighting of any individual industry in the inflation calculation. If anybody thinks house prices are going up, please send me an email and tell me where, because I’d love to know. The general feeling is they’re down 10-15% over the last six months. New homes are only being sold with massive buydowns in interest rates and free giveaways on upgrades. It is an industry that is essentially shut down, with interest rates having gone from 2.75% to 7.5% in a year, so there’s your deflation, but unfortunately, real estate is also the slowest to price in in the Fed’s inflation calculation, so we have to go through six months of torture until the Fed finally sees proof that inflation is falling. So, welcome to the stock market because it's just one of those factors. Just for fun, I got a quote on financing an investment property. The monthly payment would have been double for half the house that I already have.

Q: Are LEAPS a buy with the CBOE Volatility Index (VIX) this low?

A: No, you want to look at stocks first, and then the VIX; and with all the stocks sitting on top of 30-50% rises, it’s a horrible place to do LEAPS. LEAPS were an October play—we bought the bottom in a dozen LEAPS in October, and those were great trades, except for Tesla (TSLA) and Rivian (RIVN) which still have two years left to run. Up here, you’re basically waiting on a big selloff before you go into these one to two-year options positions.

Q: Why does Biden keep extending student loans? Will this catch up at some point?

A: He’s going to take it to the Supreme Court, and if he loses at the Supreme Court, which is likely, then he’ll probably give up on any loan extensions. At this point, the loan extensions on student loans are something like 2 or 2.5 years. The reason he’s doing this is to get 26 million people back into the economy. As long as you have giant student loan balances, you can’t get credit, you can’t get a credit card, you can’t buy a house, you can’t get a home loan. Bringing that many new people into the economy is a huge positive for not only them but for everyone else because it strengthens the economy. That has always been the logic behind forgiving student loans—and by the way, the United States is virtually the only country in the world that makes students pay back their loans after 30 or 40 years. The rest give college educations away either for free or give some interest-free break on repayments until they can get a salary-paying job.

Q: Does the budget deficit drop impact the stock market?

A: Yes, but it impacts the bond market first and in a much bigger way. That’s one of the reasons that bonds have rallied $13 points in six weeks because less government borrowing means lower interest rates—it’s just a matter of supply and demand. This has been the fastest deficit reduction since WWII, and markets will discount that.

Q: Will the US dollar (UUP) crash?

A: Yes, it will. You get rid of those high interest rates and all of a sudden nobody wants to own the US dollar, so we have great trades setting up here against everything, except maybe the Yuan where the lockdowns are a major drag.

Q: Is silver (SLV) a buy now?

A: No, it’s just had a big 10% move; I would wait for any kind of dip in silver and gold (GOLD) before you go into those trades. And when/if you do, there are better ways to do it.

Q: How is the Ukraine war going?

A: It’ll be over next year after Ukraine retakes Crimea, which they’ve already started to do. Russia is running out of ammunition, and so are we, by the way. However, the United States, as everybody learned in WWII, has an almost infinite ability to ramp up weapons production, whereas Russia does not. Russia is literally using up leftover ammunition from WWII, and when that’s gone, they’ve got nothing left, nor the ability to produce it in any sizable way. All good reasons to sell short oil companies ahead of a tsunami of Russian oil hitting the market. By the way, oil is now down for 2022.

Q: What's the number one short in oil (USO)?

A: The most expensive one, that would be Exxon Mobile (XOM).

Q: What’s going to happen to the markets in January?

A: After this Christmas rally peters out, I’m looking for profit-taking in January.

Q: When is a good time to buy debit spreads on oil?

A: Now. Look at every short play you can find out there; I just don’t see a massive spike up in oil prices ahead of a recession. And by the way, if the war in Ukraine ends and Russian oil comes back on the market, then you’re looking at oil easily below $50.

Q: What is the best way to invest in iShares Silver Trust (SLV) in the long term?

A: A two-year LEAP on the Silver (SLV) $25-$26 call spread—that gets you a 100%-200% return on that.

Q: Is lithium a good commodity trade?

A: Lithium will move in sync with the EV industry, which seems to have its own cycle of being popular and unpopular. We’re definitely in the unpopular phase right now. Long term demand for lithium will be increasing on literally hundreds of different fronts, so I would say yes, lithium is kind of the new copper. Look at Albemarle (ALB), Societe Chemica Y Minera de Chile (SQM), and FMC Corp. (FMC).

Q: If we do a LEAPS on Crown Castle Incorporated (CCI), you won’t get the dividend right?

A: No, you won’t, it’s a dividend-neutral trade because you’re long and short in a LEAPS. You have to buy the stock outright and become a registered shareholder to earn the dividend which, these days, is a hefty 4.50%. That said, if you’re looking for a high dividend stock-only play, buying the (CCI) down here is actually a great idea. For the stock-only players, this would be a really good one right now.

Q: Do you know people who are selling because of large capital gains?

A: The only people I know who are selling have giant tax bills to pay because of all the money they made trading options this year. I happen to know several thousand of those, as it turns out. So yes, I do know and that could affect the market in the next couple of weeks, which is why I went with the flatlined scenario for the next two weeks. Most tax-driven selling will be finished in the next two weeks, and after that, it kind of clears the decks for the markets to close on a high note at the end of the year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING or DISPATCH TECHNOLOGY LETTER as the case may be, then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 30, 2022

Fiat Lux

Featured Trade:

(THE MAD HEDGE SEPTEMBER 13-15 SUMMIT REPLAYS ARE UP),

(WHY WARREN BUFFET HATES GOLD),

(GLD), (GDX), (GOLD), (NEM)

Global Market Comments

September 13, 2022

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPERCYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Those in the investment business are well used to the Armageddon crowd. These are the guys who are perennially predicting the collapse of the dollar, the default of the US government, hyperinflation, and the end of the world.

Maybe after 11 years of rising, stocks are finally expensive on a relative basis?

Their perennial recommendations are to keep all your assets in gold and silver, store at least a year’s worth of canned food, and keep your untraceable guns well-oiled and supplied with ammo, preferably in high capacity magazines.

If you followed their advice, you lost your shirt.

I have broken many of these wayward acolytes of their money-losing habits. But not all of them. There seems to be an endless supply emanating from the hinterlands.

The “Oracle of Omaha” Warren Buffet often goes to great lengths to explain why he despises the yellow metal.

The sage doesn't really care about the gold, whatever the price. He sees it primarily as a bet on fear. I imagine he feels the same about Bitcoin, the modern tulips of our age.

If investors are more afraid in a year than they are today, then you make money on gold. If they aren't, then you lose money.

The only problem now is that fear ain’t working.

If you took all the gold in the world, it would form a cube 67 feet on all sides, worth $5 trillion. For that same amount of money, you could own other assets with far greater productive earning power, including:

*All the farmland in the US, about 1 billion acres, which is worth $2.5 trillion.

*Two Apple’s (AAPL), the largest capitalized company in the world at $3 trillion.

Instead of producing any income or dividends, gold just sits there and shines, making you feel like King Midas.

I don't know. With the stock market at an all-time high, and oil trading at $70.49/barrel, a bet on fear looks pretty good to me right now.

I'm still sticking with my long-term forecast of the old inflation-adjusted high of $2,300/ounce. But it might be very long term.

It is just a matter of time before emerging market central bank buying pushes it up there. And who knows? Fear might make a comeback too.

Global Market Comments

March 4, 2022

Fiat Lux

Featured Trade:

(MARCH 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (TSLA), (FCX), (JPM), (BAC), (MS), (TLT),

(TBT),(BA), UPS (UPS), (CAT), (DIS), (DAL),

(GOLD), (VIX), (VXX), (CAT), (BA)

Below please find subscribers’ Q&A for the March 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Do you think Vladimir Putin will give up?

A: He will either be forced to give up, run out of resources/money, or he will suddenly have an accident. When the people see their standard of living go from a per capita income of $10,000/year today to $1,000—back to where it was during the old Soviet Union—his lifespan will suddenly become very limited.

Q: Would you be buying Invesco Trusts (QQQs) on dips?

A: I think we have a few more horrible days—sudden $500- or $1,000-point declines—but we’re putting in a bottom of sorts here. It may take a month or two to finalize, but the second buying opportunity of the decade is setting up; of course, the other one was two years ago at the pandemic low. So, do your research, make your stock picks now, and once we get another absolute blow-up to the downside, that is your time to go in.

Q: Materials have gone up astronomically, are they still a buy?

A: Yes, on dips. I wouldn't chase 10% or 20% one-week moves up here—there are too many other better trades to do.

Q: Is it time to go long aggressively in Europe?

A: No, because Europe is going to experience a far greater impact economically than the US, which will have virtually none. In fact, all the impacts on the US are positive except for higher energy prices. So, I think Europe will have a much longer recovery in the stock market than the US.

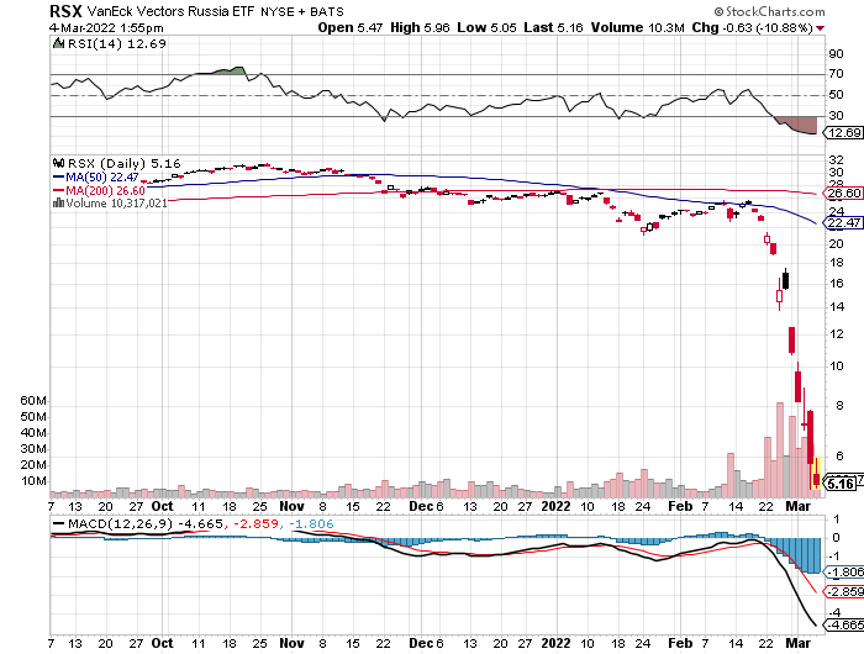

Q: Would you take a flier on a Russian ETF (RSX)?

A: No, most, if not all, of them are about to be delisted because they have been banned or the liquidity has completely disappeared. The (RSX) has just collapsed 85%, from $26 to $4. Virtually all of Russia is for sale, not only stocks, bonds, junk bonds, ETFs, but also joint ventures. ExxonMobil, Shell and BP are all dumping their ownership of Russian subsidiaries as we speak.

Q: Time for a Freeport-McMoRan (FCX) LEAP?

A: No, November was the time for an (FCX) LEAP—we’ve already had a massive run now, up 66% in five months, so wait for the next dip. The next LEAPS are probably going to be in technology stocks in a few months.

Q: My iShares 20 Plus Year Treasury Bond ETF (TLT) call $130 was assigned, What should I do?

A: Call your broker immediately and tell them to exercise your 127 to cover your short in the 130. They usually charge a few extra fees on that because they can get away with it, but you’ve just made the maximum profit on the position. If you haven’t been exercised yet, that 127/130 call spread will expire at max profit in 10 days.

Q: What if I get my short side called away on a position?

A: Use your long side calls to execute immediately to cover your short side. These call spreads are perfectly hedged positions, same name, same maturity, same size, just different strike prices. If your broker doesn’t hear from you at all, they will just exercise the short call and leave you long the long call, and that can lead to a margin call. So the second you get one of these calls, contact your broker immediately and get out of the position.

Q: Is it safe to put 100% of your money in Tesla (TSLA) for the long term?

A: Only if you can handle a 50% loss of your money at any time. Most people can't. It’s better to wait for Tesla to drop 50%, which it has almost done (it’s gotten down to $700), and then put in a large position. But you never bet all your money on one position under any circumstances. For example, what if Elon Musk died? What would Tesla’s stock do then? It would easily drop by half. So, I’ll leave the “bet the ranch trades” for the younger crowd, because they’re young enough to lose all their money, start all over again, and still earn enough for retirement. As for me, that is not the case, so I will pass on that trade. You should pas too.

Q: Do you foresee NASDAQ (QQQ) being up 5-10% or 10-20% by year-end?

A: I do actually, because business is booming across tech land, and the money-making stocks are hardly going down and will just rocket once the rotation goes back into that sector.

Q: We could see an awful earnings sequence in April, which could put in the final bottom on this whole move.

A: That is right. We need one more good capitulation to get a final bottom in, and then we’re in LEAP territory on probably much of the market. We know we’re having a weak quarter from all the anecdotal data; those companies will produce weak earnings and the year-on-year comparisons are going to be terrible. A lot of companies will probably show down turns in earnings or losses for the quarter, that's all the stuff good bottoms are made out of.

Q: What should we make of the Russian threats of WWIII going Nuclear?

A: I think if Putin gave the order, the generals would ignore it and refuse to fire, because they know it would mean suicide for the entire country. Mutual Assured Destruction (MAD) is still in place, and it still works. And by the way, it hasn’t been in the media, but I happen to know that American nuclear submarines with their massive salvos of MIRVed missiles, have moved much closer to Russian waters. So, you're looking at a war that would be over in 15 minutes. I think that would also be another scenario in which they replace Putin: if he gives such an order. This has actually happened in the past; people without top secret clearance don’t know this but Boris Yeltsen actually gave an order to launch nuclear missiles in the early 90s when he got mad at the US about something. The generals ignored it, because he was drunk. And something else you may not know is that 95% of the Russian nuclear missiles don’t work—they don’t have the GDP to maintain 7,000 nuclear weapons at full readiness. Plutonium is one of the world’s most corrosive substances and very expensive to maintain. Only a wealthy country like the US could maintain that many weapons because it’s so expensive. So no, you don’t need to dig bomb shelters yet, I think this stays conventional.

Q: Banks like (JPM), (BAC), AND (MS) are at a low—are they a buy?

A: Yes, but not yet; wait for more shocks to the system, more panic selling, and then the banks are absolutely going to be a screaming buy because they are on a long-term trend on interest rates, strong economy, lowering defaults—all the reasons we’ve been buying them for the last year.

Q: Should I short bonds or should I buy Freeport up 60%?

A: Short bonds. Next.

Q: Should I buy Europe or should I short bonds?

A: Short bonds. That should be your benchmark for any trade you’re considering right now.

Q: How much and how quickly will we see a collapse in defense stocks?

A: Well, you may not see a collapse in defense stocks, because even if Russia withdraws from Ukraine, they still are a newly heightened threat to the West, and these increases in defense spending are permanent. That’s why the stocks have gone absolutely ballistic. Yeah sure, you may give up some of these monster gains we’ve had in the last week, but this is a dip-buying sector now after being ignored for a long time. So yes, even if Russia gives up, the world is going to be spending a lot more on defense, probably for the rest of our lives.

Q: Just to confirm, LEAP candidates are Boeing (BA), UPS (UPS), Caterpillar (CAT), Disney (DIS), Delta Airlines (DAL)?

A: I would say yes. You may want to hold off, see if there’s one more meltdown to go; or you can buy half now and half on either the next meltdown or the melt-up and get yourself a good average position. And when I say LEAPS, I mean going out at least a year on a call spread in options on all of these things.

Q: Is $143 short safe on the (TLT)?

A: Definitely, probably. In these conditions, you have to allow for one day, out of the blue, supers pikes of $3 like we got last week, or $5 trins week, only to be reversed the next day. The trouble is even if it reverses the next day, you’re still stopped out of your position. So again, the message is, don’t be greedy, don’t over-leverage, don’t go too close to the money. There’s a lot of money to be made here, but not if you blow all your profits on one super aggressive trade. And take it from someone who’s learned the hard way; you want to be semi-conservative in these wild trading conditions. If you do that, you will make some really good money when everyone else is getting their head handed to them.

Q: Would you go in the money or out of the money for Boeing (BA) and Caterpillar (CAT)?

A: It just depends on your risk tolerance. The best thing here is to do several options combinations and then figure out what the worst-case scenario is. If you can handle that worst-case scenario without stopping out, do those strikes. These LEAPS are great, unless you have to stop out, and then they will absolutely kill you. And usually, you only do these with sustained uptrends in place; we don’t have that yet which is why I’m saying, watch these LEAPS. Don’t necessarily execute now, or if you do, just do it in small pieces and leg in. That is the smart answer to that.

Q: What’s the probability that the CBOE Volatility Index (VIX) makes a new high in the next 2 weeks?

A: I give it 50/50.

Q: Call options on the VIX?

A: No, that’s one of the super high-risk trades I have to pass on.

Q: How low can the VIX go down this month?

A: High ten’s is probably a worst-case scenario.

Q: LEAPS on Barrick Gold Corporation (GOLD)?

A: No, that was a 3-month-ago trade. Now it’s too late, never consider a LEAP at an all-time high or close to it.

Q: Time to short oil?

A: Not yet. We have some spike top going on in oil. It’s impossible to find the top on this because, while bottoms are always measurable with PE multiples and such, tops are impossible to measure because then you’re trying to quantify human greed, which can’t be done. So yeah, I would stand by; it’s something you want to sell on the way down. This is the inverse of catching a falling knife.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 15, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT VIDEOS ARE UP!)

(WHY WARREN BUFFET HATES GOLD),

(GLD), (GDX), (ABX), (GOLD)