It’s scary when the best chip company in the world rolls out new products.

It’s scary because others can’t compete and they get left further behind.

It’s scary because the high level of technology facilitates another new wave of technological expertise in other companies from the software and hardware side.

These new products are almost always faster, more efficient, and better than the previous products catalyzing a snowball effect that lifts everybody’s revenue.

This type of outstanding performance of late is the reason that made Nvidia (NVDA) into the world’s most valuable chipmaker and they have announced they are updating its H100 artificial intelligence processor, adding more capabilities to a product that has fueled its dominance in the AI computing market.

The new model, called the H200, will get the ability to use high-bandwidth memory, or HBM3e, allowing it to better cope with the large data sets needed for developing and implementing AI.

Amazon’s AWS, Alphabet’s Google (GOOGL) Cloud and Oracle’s (ORCL) Cloud Infrastructure have all committed to using the new chip starting next year.

Winning orders is easy with the outsized brand recognition and type of game changing product on offer.

The current version of the Nvidia processor is already experiencing accelerated demand.

But the product is facing stiffer competition: Advanced Micro Devices (AMD) is bringing its rival MI300 chip to market in the fourth quarter, and Intel Corp. claims that its Gaudi 2 model is faster than the H100.

AMD is another chip company that readers should feel comfortable diversifying into if they don’t feel comfortable putting all eggs into the Nvidia basket.

AMD’s stock is surging towards old highs around $125 and should overtake that soon after the nice rally in the 2nd half of the year.

With the new product, Nvidia is trying to keep up with the size of data sets used to create AI models and services.

Adding the enhanced memory capability will make the H200 much faster at bombarding software synthesizing data.

Large computer makers and cloud service providers are expected to start using the H200 in the second quarter of 2024.

Nvidia got its start making graphics cards for gamers, but its powerful processors have now won a following among data center operators.

That division has gone from being a side business to the company’s biggest moneymaker in less than five years.

Nvidia’s graphics chips helped pioneer an approach called parallel computing, where a massive number of relatively simple calculations are handled at the same time.

That’s allowed it win major orders from data center companies, at the expense of traditional processors supplied by Intel.

The growth helped turn Nvidia into the poster child for AI computing earlier this year — and sent its market valuation soaring.

Nvidia is like a freight train that has left the station.

The stock is up 9 straight days as we cruise into its earnings report on November 21st.

It’s hard to see this earnings report being nothing short of spectacular and Nvidia have become famous for forecasting the unthinkable.

They then go and surpass a high bar and push the envelope further so it’s not a bad idea to buy NVDA before the earnings report.

The speed at which they come out with products is astounding and now being able to boast the best server chip in the tech enterprise community, it just represents yet another powerful part of their stunning array of tech arsenal.

$600 per share is a no-brainer for Nvidia and that will be surpassed in 2024.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-13 14:02:452023-11-13 16:33:10Ride the Nvidia and AMD Roller Coaster

Tech (QQQ) earnings turned out to produce some positive performances.

Dominant companies can produce dominant earnings even in troubled times.

So what is the problem?

The sales outlook underwhelmed as the American consumer and business keep getting stretched to the limit.

I believe that traders shouldn’t expect a quick turnaround of sales projections for 2024 unless there are some material structural improvements in the business and consumer environment.

No savior is coming for 2024.

All signs point to more uncertainty and not less and rightly so as high inflation has only been replaced by a decrease in the rate of inflation.

Things are still expensive and that means less opportunity for tech to build a growth story.

Apple, Alphabet, Meta, and Tesla all gave investors reason to rub smiles off faces.

From Apple’s unimpressive holiday outlook to Alphabet’s tepid cloud computing sales results, a recurring theme for the group was weakness.

Meta warned that the year ahead is looking less predictable, while Tesla raised concerns that demand for electric cars is starting to weaken.

Despite Tesla's missing earnings, the group is poised to surpass the 36% increase estimates called for before earnings season began.

The tech sector in the S&P 500 still carries a nearly 36% premium to the index on a forward price-to-earnings basis, per data compiled by Bloomberg Intelligence.

There’s a lot of AI hype, but not every company is market-ready.

Everything can change in a heartbeat if there is economic or geopolitical upheaval, which would directly impact stocks.

The market is still pricing in no spreading of military activity as it looks through it as a self-contained area.

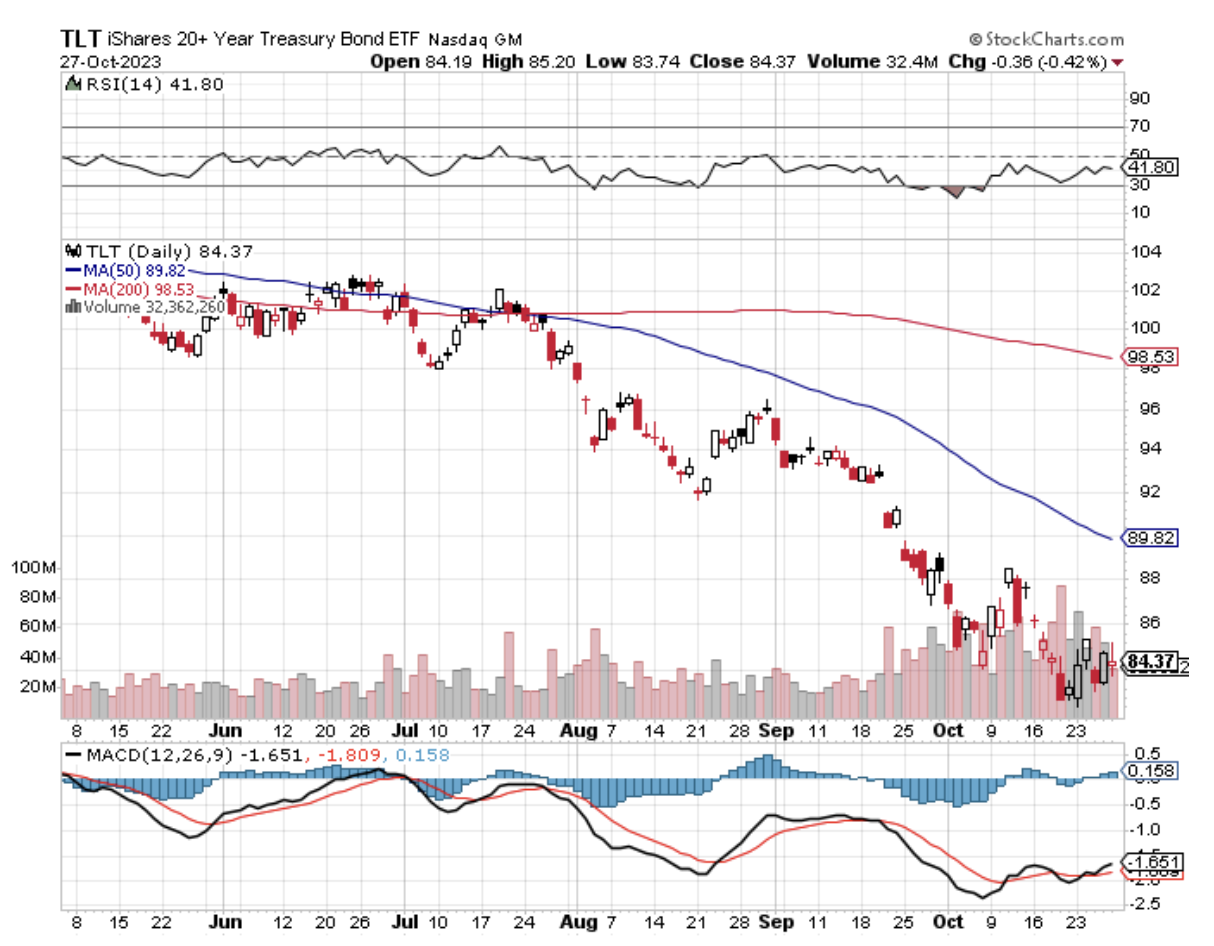

Therefore, the pendulum has swung the completely opposite direction as the U.S. 10-year treasury yield has dropped from 5% to 4.6%.

The strength in treasuries could be short-lived, because several have told me that traders are jumping back into the short-term trade which would signal higher for longer.

The Fed Futures show that the first 25 basis rate is forecasted for May 2024 with 2 more consecutive .25% rate cuts following the first.

The American consumer just might have enough juice for one more splurge that would then push back rate cuts from May to somewhere closer to July or August.

Therefore, it’s easy for me to see how this 6.5% surge has a little longer follow through only to soon clash with a “higher for longer” narrative.

The true tailwind for tech stocks here is that much of the bad news has been priced in and any violent surge in treasury yields seems like a low probability for the last 7 weeks of the year, unless another global conflict breaks out.

Seasonal buying could mean that November is more positive than negative for tech stocks and any big draw down should be bought in a quality tech name. December could be a harder slog for tech.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-11-06 14:02:192023-11-06 15:09:35Higher For Longer Is Not Off The Table

The tech industry is quickly morphing into a generative artificial intelligence success story or bust outcome for many involved.

This came pretty much out of nowhere.

December 2022 was the big announcement that ChatGPT went live and everybody in tech has basically been freaking out since then.

Big ideas like the internet and software also had the same type of effect on tech stocks back in the heyday.

What would have Microsoft (MSFT) been without the computer or Windows?

Even more urgent, once perceived growth tech companies like Tesla are starting to cut prices of products because the consumer is tapped out these days.

That means tech corporations can’t sell the current product by adding incremental iterations and passing it off as something “groundbreaking.”

Consumers need something more.

Consumers will spend on the next big thing and generative artificial intelligence still has a long way to go, but stocks participating in generative AI are starting to get those premium multiples that were only reserved for tech royalty.

Everyone is hoping to get in on the action as well as Alphabet.

They are racing to build a new search engine and add artificial intelligence features to its existing products in the face of rapid growth in the field by rivals such as Microsoft Bing.

Google is testing new features called "Magi," with more than 160 people working full-time on the project.

Google's new products will try to predict users' needs, with features such as helping users write software code and display ads in search results, and Google is also exploring mapping technology that allows users to use Google Earth with the help of AI and search music through conversations with chatbots.

Samsung Electronics is reportedly considering replacing Google with Bing, the main search engine on its phones, because of Bing's artificial intelligence capabilities. The Samsung contract is expected to generate $3 billion in annual revenue for Google, a revenue stream that is now in jeopardy. In addition, Google has a $20 billion contract with Apple for a similar default search engine, which is up for renewal this year.

Google’s search engine could be swept into the dustbin of history if they don’t get a move on it pronto.

The ecosystems like Apple and Samsung can easily opt for a better engine if Google falls behind and that is exactly what we are seeing from Samsung.

I would probably say that Google got a little too cocky when they decided to stop developing itself.

They thought that nobody could topple them.

The panoramic views from the ivory tower can look nice from the terrace for a while until somebody builds a bigger ivory tower that obstructs the view.

It’s been quite fascinating to see Google’s sense of urgency lately because it was always assumed they were part of a stable duopoly with Facebook.

Google’s panic indicates that Microsoft’s Bing is a real threat to their revenue stream and at the very minimum, bits and pieces of the new technology will be incorporated into a new version of a search engine that will behave as a supercharged version of the likes we have never seen before.

If Google can catch up then its stock price will go a lot higher from here.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-11-03 14:02:442023-11-03 13:44:06The Catch Up Plan

Circulating among the country’s top global strategists this year, visiting their corner offices, camping out in their vacation villas, or cruising on their yachts, I am increasingly hearing about a new investment theme that will lead markets for the next 20 years:

The Second American Industrial Revolution.

It goes something like this.

You remember the first Industrial Revolution, don’t you? I remember it like it was yesterday.

It started in 1775 when a Scottish instrument maker named James Watt invented the modern steam engine. Originally employed for pumping water out of a deep Shropshire coalmine, within 32 years it was powering Robert Fulton’s first commercially successful steamship, the Clermont, up the Hudson River.

The first Industrial Revolution enabled a massive increase in standards of living, kept inflation near zero for a century, and allowed the planet’s population to soar from 1 billion to 7 billion. We are still reaping its immeasurable benefits.

The Second Industrial Revolution is centered on my own neighborhood of San Francisco. It seems like almost every garage in the city is now devoted to a start-up.

The cars have been flushed out onto the streets, making urban parking here a total nightmare. These are turbocharging the rate of technological advancement.

Successes go public rapidly and rake in billions of dollars for the founders overnight. Thirty-year-old billionaires wearing hoodies are becoming commonplace.

However, unlike with past winners, these newly minted titans of industry don’t lock their wealth up in mega mansions, private jets, or the Treasury bond market. They buy a Tesla Plaid for $150,000 with a great sound system and full street-to-street auto-pilot (TSLA), and then reinvest the rest of their windfall in a dozen other startups, seeking to repeat a winning formula.

Many do it.

Thus, the amount of capital available for new ideas is growing by leaps and bounds. As a result, the economy will benefit from the creation of more new technology in the next ten years than it has seen in the past 200.

Computing power is doubling every year. That means your iPhone will have a billion times more computing power in a decade. 3D printing is jumping from the hobby world into large-scale manufacturing. In fact, Elon Musk’s Space X is already making rocket engine parts on such machines.

Drones came out of nowhere and are now popping up everywhere.

It is not just new things that are being invented. Fantastic new ways to analyze and store data, known as “big data” are being created.

Unheard new means of social organization are appearing at breakneck, leading to a sharing economy. Much of the new economy is not about invention, but organization.

The Uber ride-sharing service created $50 billion in market capitalization in only five years and is poised to replace UPS, FedEx, and the US Postal Service with “same hour” intracity deliveries. Now they are offering “Uber Eats” in my neighborhood, which will deliver you anything you want to eat, hot, in ten minutes!

Airbnb is arranging accommodation for 1 million guests a month. They even had 189 German guests staying with Brazilians during the World Cup there. I bet those were interesting living rooms on the final day! (Germany won).

And you are going to spend a lot of Saturday nights at home, alone if you haven’t heard of Match.com, eHarmony.com, or Badoo.com.

“WOW” is becoming the most spoken word in the English language. I hear myself saying I every day.

Biotechnology (IBB), an also-ran for the past half-century, is sprinting to make up for lost time. The field has grown from a dozen scientists in my day 40 years ago, to several hundred thousand today.

The payoff will be the cure for every major disease, like cancer, Parkinson’s, heart disease, AIDS, and diabetes, within ten years. Some of the harder cases, such as arthritis, may take a little longer. Soon, we will be able to manipulate our own DNA, turning genes on and off at will. The weight loss drugs Wegovy and Ozempic promise to eliminate 75% of all self-inflicted illnesses.

The upshot will be the creation of a massive global market for these cures, generating immense profits. American firms will dominate this area, as well.

Energy is the third leg of the innovation powerhouse. Into this basket, you can throw in solar, wind, batteries, biodiesel, and even “new” nuclear (see NuScale (SMR)).The new Tesla Powerwall will be a game changer. Visionary, Elon Musk, is ramping up to make tens of millions of these things.

Use of existing carbon-based fuel sources, such as oil and natural gas, will become vastly more efficient. Fracking is unleashing unlimited new domestic supplies.

Welcome to “Saudi America.”

The government has ordered Detroit to boost vehicle mileage to an average of 55 miles per gallon by 2030. The big firms have all told me they plan to beat that deadline, not litigate it, a complete reversal of philosophy.

Coal will be burned in impoverished emerging markets only, before it disappears completely. Energy costs will drop to a fraction of today’s levels, further boosting corporate profits.

Coal will die, not because of some environmental panacea, but because it is too expensive to rip out of the ground and transport around the world, once you fully account for all its costs.

Years ago, I used to get two pitches for venture capital investments a quarter, if any. Now, I am getting two a day. I can understand only half of them (those that deal with energy and biotech, and some tech).

My friends at Google Venture Capital are getting inundated with 20 a day each! How they keep all of these stories straight is beyond me. I guess that’s why they work for Google (GOOGL).

The rate of change for technology, our economy, and for the financial markets will accelerate to more than exponential. It took32 years to make the leap from steam engine-powered pumps to ships and was a result of a chance transatlantic trip by Robert Fulton to England, where he stumbled across a huffing and puffing steam engine.

Such a generational change is likely to occur in 32 minutes in today’s hyper-connected world, and much shorter if you work on antivirus software (or write the viruses themselves!). And don’t get me started on AI!

The demographic outlook is about to dramatically improve, flipping from a headwind to a tailwind in 2022. That’s when the population starts producing more big spending Gen Xers and fewer over-saving and underproducing baby boomers. This alone should be at least 1% a year to GDP growth.

China is disappearing as a drag on the US economy. During the nineties and the naughts, they probably sucked 25 million jobs out of the US.

With an “onshoring” trend now in full swing, the jobs ledger has swung in America’s favor. This is one reason that unemployment is steadily falling. Joblessness is becoming China’s problem, not ours.

The consequences for the financial markets will be nothing less than mind-boggling. The short answer is higher for everything. Skyrocketing earnings take equity markets to the moon. Multiples blast off through the top end of historic ranges. The US returns to a steady 5% a year GDP growth, which it clocked in the recent quarter.

What am I bid for the Dow Average (INDU), (SPY), (QQQ) in ten years? Did I hear 240,000, a seven-fold pop from today’s level? Or more?

Don’t think I have been smoking the local agricultural products from California in arriving at these numbers. That is only half the gain that I saw from 1982 to 2000, when the stock average also appreciated 17-fold, from 600 to 10,000.

They’re playing the same movie all over again. Except this time, it’s on triple fast forward.

There will also be commodities (DBA) and real estate booms. Even gold (GLD) gets bid up by emerging central banks bent in increasing their holdings to Western levels as well as falling interest rates.

I tell my kids to save their money, not to fritter it away day trading now because anything they buy in 2020 will increase in value tenfold by 2033. They’ll all look like geniuses like I did during the eighties.

What are my strategist friends doing about this forecast? They are throwing money into US stocks with both bands, especially in technology (XLK), biotech (IBB), and bonds (JNK).

This could go on for decades.

Just thought you’d like to know.

It’s Amazing What You Pick Up on These Things!

https://www.madhedgefundtrader.com/wp-content/uploads/2022/06/john-thomas-yatch.png404504Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-02 09:04:452023-11-02 12:14:52The Second American Industrial Revolution

At least that way I would know which direction the fire was coming from, the east. Back here in the US markets, the fire seemed to be coming from every direction all at once.

Good news was bad news and bad news even worse. An S&P 500 down 2.5% certainly left a bruise. The geopolitical outlook in the idle East is getting worse by the day.

But where others find nothing but despair, I see opportunity. Despite all the doom and gloom, all the elements of a yearend rally are setting up nicely. And it could be a sharp one as the time for it to play out is ever shrinking.

Hedge fund quantitative, momentum, and systemic shorts are at all-time highs, creating lots of buying power. AI has gone silent. Key earnings events will be done with the Apple announcement on Thursday, November 2. Ten-year bonds have repeatedly tried but failed to break the 5.00% yield.

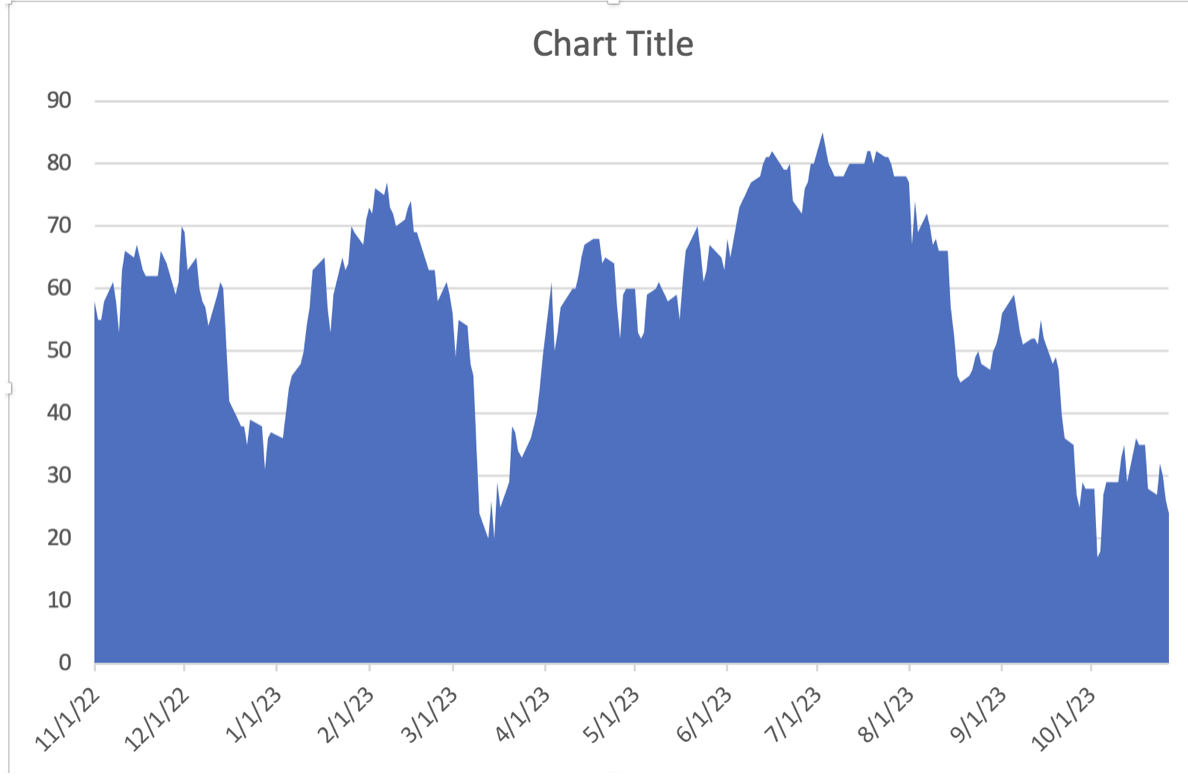

Major tech stocks like (TSLA), (NVDA), (GOOGL), and (AMZN) have seen 20% corrections. The Mad Hedge AI Market Timing Index is unable to close below $20 and has been chopping a lot of wood under $30. If a new House speaker cuts a deal to avoid a government shutdown before November 17, it could be off to the races.

The smart thing to do here is to build up a list of stocks higher leverage to falling interest rates. All stocks benefit from falling rates but some much more than others.

One of my favorites is Annaly Capital Management (NLY), one of the largest mortgage real estate investment trusts (REITS). The company borrows money, primarily via short-term repurchase agreements, and reinvests the proceeds in asset-backed securities.

The company’s shares are unusually sensitive to rising overnight interest rates, and its shares are down 50% in a year. A monster rally in the stock is brewing. Oh, and it has a 17% dividend, which will likely get cut but still remain extremely high.

Finally, I want to bid a sad farewell to my old friend and fellow iconoclast Byron Wien. Byron was late of Blackstone and much earlier from Morgan Stanley.

Byron was famed for his “Ten Surprises” which he published each New Year and with which I used to assist him in the early years. This was a list of possible developments which, if they occurred, would have a disproportionate effect on the market.

Byron was 90 and will be missed. One of his favorite pieces of advice was to never retire and Byron was working right up until last week.

Hmmmm. Sounds like good advice to me.

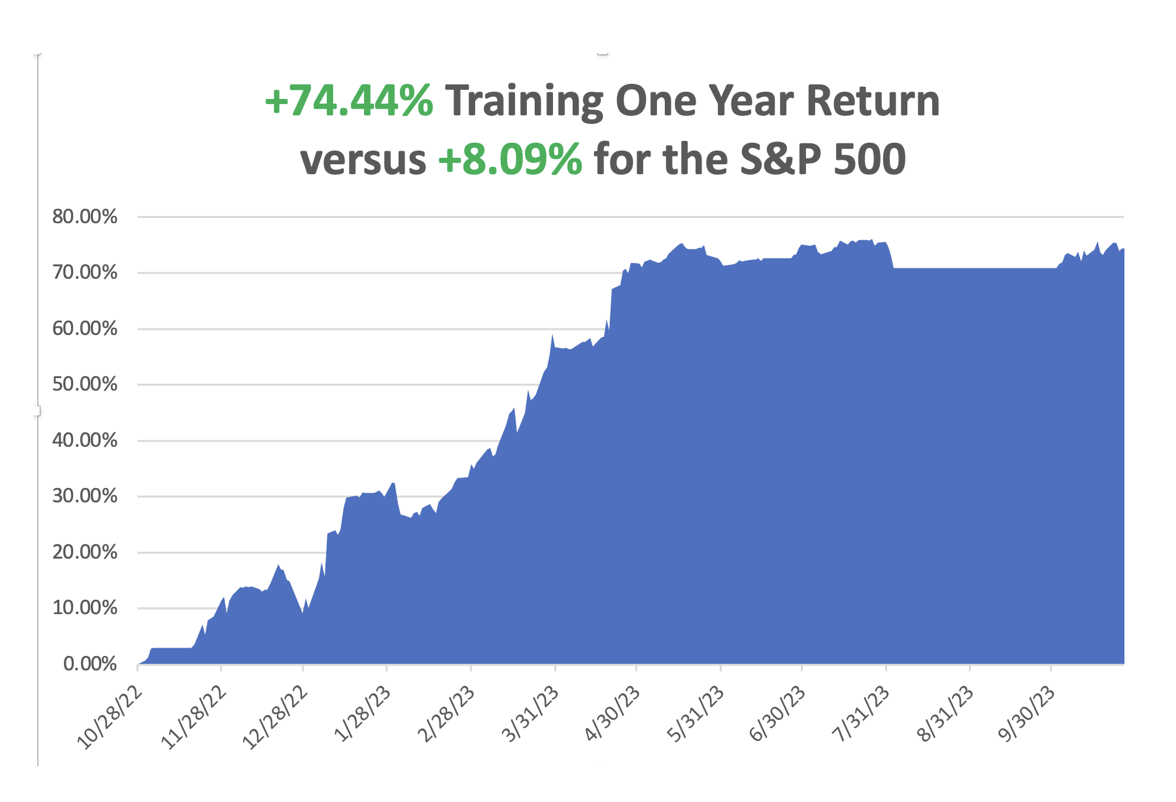

So far in October, we are up +3.56%. My 2023 year-to-date performance is still at an eye-popping +64.36%.The S&P 500 (SPY) is up +7.89%so far in 2023. My trailing one-year return reached +74.44% versus +8.09% for the S&P 500.

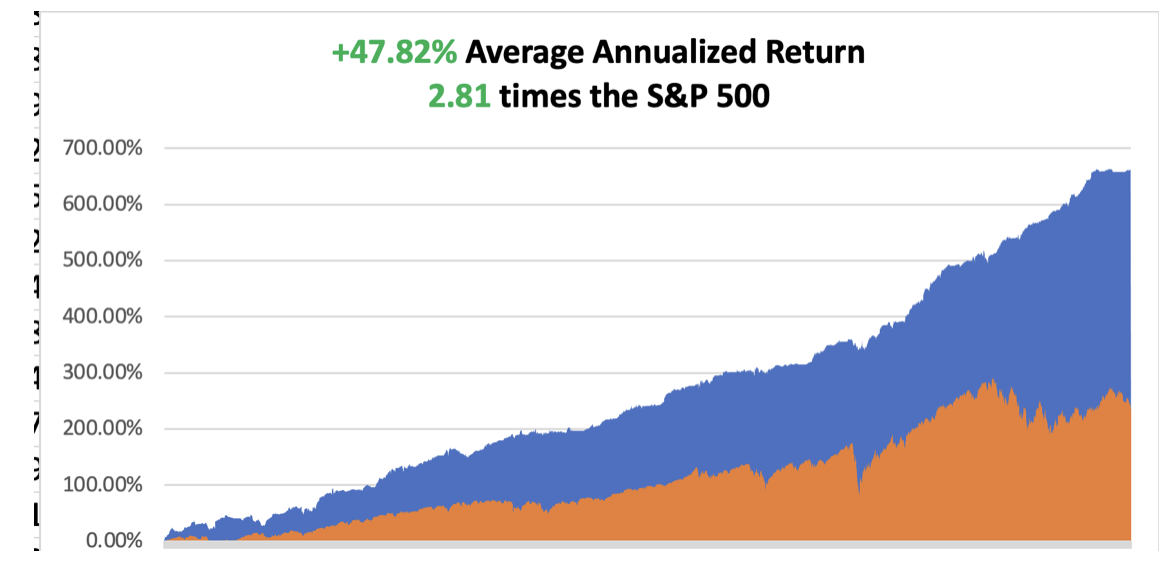

That brings my 15-year total return to +661.55%. My average annualized return has fallen back to +47.89%, some 2.81 times the S&P 500over the same period.

Some 44 of my 49 trades this year have been profitable.

Car Payment Delinquencies Hit Record Rate, with repossessions rising. With interest rate hikes making newer loans more expensive, millions of car owners are struggling to afford their payments. It’s a clear indication of distress at a time when the economy is sending mixed signals, particularly about the health of consumer spending. Usually, a recession indicator but not this time.

US Government Wraps up Fiscal 2023 with a $1.7 Trillion Deficit, up 23% from the previous year, which ended on October 31. It’s a major reason why bonds have been under such pressure since July. But the purchasing power of the total US national debt of $32 trillion fell by $260 billion last year, thanks to the torrid 8.1% inflation rate.

US Core PCE Jumps 0.3% in September, the most in four months. It’s the Fed’s favorite inflation indicator. Drugs, travel, and used cars saw the big price increases. Resilient household demand paired with a pickup in inflation underscores momentum heading into the fourth quarter

Ukraine War has Become a Big Generator at US Defense Companies. Companies such as Lockheed Martin (LMT), General Dynamics (GD), and others expect that existing orders for hundreds of thousands of artillery rounds, hundreds of Patriot missile interceptors, and a surge in orders for armored vehicles expected in the months ahead will underpin their results in coming quarters. Buy the sector on dips

Don’t Expect a Real Estate Crash Anytime Soon, with supplies at 40-year lows. Yes, 8% mortgages are a buzz kill, but 95% of homeowners with mortgages date back to the 3.0% era. No one wants to give up their free lunch. If you’re a mortgage originator, it’s another story.

Existing Home Sales Hit 13-Year Low at 1.13 million, down 8% YOY. The Median Home Price was up 2.8% to $394,300. This is 17% of the peak rate we saw in 2021 when overnight rates were still zero.

Pending Home Sales Rise 1.1% in September to 72.6, but are down 13% YOY. On a signed contract basis. But the absolute level is the lowest in two years. High mortgage rates are the buzz kill. Affordability is at a record low.

Adjustable Rate Mortgages Make a Big Comeback, with 5/1 ARMS costing only 6.99% compared to 8.0% for the conventional 30-year fixed, a 23-year high. Mortgage originations are now down 22% YOY.

US Economy Red Hot at 4.9% Growth Rate, the highest in two years. Unfortunately, the stock market sees a major slowdown in the current quarter. Consumer spending was the big driver.

Tech Selloff has Taken NVIDIA down to a 25 Times Earnings Multiple, the same as Walmart and Target, despite 50% earnings growth for the foreseeable future. This is just at the start of an AI super cycle. Get ready to start loading the boat.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 30 at 8:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, October 31 at 2:30 PM,the S&P Case Shiller National Home Price Index is released.

On Wednesday, November 1 at 8:30 AM, the JOLTS Job Openings Report is published.

On Thursday, November 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, November 3 at 2:30 PM, the October Nonfarm Payroll Report is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, one of the benefits of being married to a British Airways stewardess in the 1970s was unlimited free travel around the world. Ceylon, the Seychelles, and Kenya were no problem.

Usually, you rode in first class, which was half empty, as the British Empire was then rapidly fading. Or you could fly in the cockpit where, on long flights, the pilot usually put the plane on autopilot and went to sleep on the floor, asking me to watch the controls.

That’s how I got to fly a range of larger commercial aircraft, from a Vickers Viscount VC-10 to a Boeing 747. Nothing beats flying a jumbo jet over the North Pole on a clear day, where the unlimited view ahead is nothing less than stunning.

When gold peaked in 1979 at $900 an ounce, up from $34, The Economist magazine asked me to fly from Japan to South Africa and write about the barbarous relic. That I did with great enthusiasm, bringing along my new wife, Kyoko.

Sure enough, as soon as I arrived, I noticed long lines of South Africans cashing in their Krugerands, which they had been saving up for years in the event of a black takeover.

There was only one problem. My wife was Japanese.

While under the complicated apartheid system, the Chinese were relegated to second class status along with Indians, Japanese were treated as “honorary whites” as Japan did an immense amount of trade with the country.

The confusion came when nobody could tell the difference between Chinese and Japanese, not even me. As a result, we were treated as outcasts everywhere he went. There was only one hotel in the country that would take us, the Carlton in Johannesburg, where John and Yoko Lennon stayed earlier that year.

That meant we could only take day trips from Joberg. We traveled up to Pretoria, the national capital, to take in the sights there. For lunch, we went to the best restaurant in town. Not knowing what to do, they placed us in an empty corner and ignored us for 45 minutes. Finally, we were brought some menus.

The Economist asked me to check out the townships where blacks were confined behind high barbed wire fences in communities of 50,000. I was given a contact in the African National Conference, then a terrorist organization. Its leader, Nelson Mandela, had spent decades rotting away in an island prison.

My contact agreed to smuggle us in. While blacks were allowed to leave the townships for work, whites were not permitted in under any circumstances.

So, we were somewhat nonplussed Kyoko and I were asked to climb into the trunk of an old Mercedes. Really? We made it through the gates and into the center of the compound. On getting out of the trunk, we both burst into nervous laughter.

Some honeymoon!

After meeting the leadership, we were assigned no less than 11 bodyguards as whites in the townships were killed on sight. The favored method was to take a bicycle spoke and sever your spinal cord.

We drove the compound inspecting plywood shanties with corrugated iron roofs, brightly painted and packed shoulder to shoulder. The earth was dry and dusty. People were friendly, waving as we drove past. I interviewed several. Then we were smuggled out the same way we came in and hastily dropped on a corner in the city.

Apartheid ended in 1990 when the ANC took control of the country, electing Nelson Mandela as president. A massive white flight ensued which brought people like Elon Musk’s family to Canada and then to Silicon Valley.

Everyone feared the blacks would rise up and slaughter the white population.

It never happened.

Today, South Africa offers one of the more interesting investment opportunities on the continent. The end of apartheid took a great weight off the shoulders of the country’s economy. Check out the (EZA), which nearly tripled off of the 2020 bottom.

Kyoko passed away in 2002 at age 50.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-10-30 09:02:072023-10-30 12:26:49The Market Outlook for the Week Ahead, or The Trapped Market

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.