Global Market Comments

May 9, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADED FOR THE LEPER COLONY),

(SPY), (TLT), (TBT), (BRKB), (TSLA), (GLD), (AAPL), (GOOGL), (MSFT), (NVDA)

Global Market Comments

May 9, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADED FOR THE LEPER COLONY),

(SPY), (TLT), (TBT), (BRKB), (TSLA), (GLD), (AAPL), (GOOGL), (MSFT), (NVDA)

My worst-case scenario for the S&P 500 this year was a dive of 20%. We are now off by 14%. And of course, most stocks are down a lot more than that.

Which means that we are getting close to the tag ends of this move. The kind of wild, daily 1,000-point move up and down we saw last week is typical of market bottoms.

Some $7 trillion in market capitalization lost this year. That means we could be down $10 trillion from a $50 trillion December high before this is all over. That’s a heck of a lot of wealth to disappear from the economy.

So, it may make sense to start scaling into the best quality names on the bad days in small pieces, like Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), and NVIDIA (NVDA).

Whatever pain you may have to take what follows, the twofold to threefold gain that will follow over the next five years will make it well worth it. Is a 20% loss upfront worth a long-term gain of 200%? For most people, it is.

Bonds may also be reaching the swan song for their move as well. The United States Treasury Bond Fund (TLT) at $113 has already lost a gobsmacking $42 since the November $155 high.

The markets have already done much of the Fed’s work for it, discounting 200 basis points of an anticipated 350 basis points in rate rises in this cycle. Therefore, I wouldn’t get too cutesy piling on new bond shorts here just because it worked for five months.

Yes, there is another assured 50 basis point rise in six weeks towards the end of June. Jay Powell has effectively written that in stone. We might as well twiddle our fingers and keep playing the ranges until then. We have in effect been sent to the trading leper colony.

The barbarous relic (GLD) seems to be looking better by the day. Q1 saw a massive 551 metric tonnes equivalent pour into gold ETF equivalents, an increase of 203%. Of course, we already know of the step-up in Russian and Chinese demand to defeat western sanctions.

But the yellow metal is also drawing more traditional investment demand. Gold usually does poorly during rising interest rates. This time, it's different. An inflation rate of 8.5% minus an overnight Fed rate of 1.0%, leaving a real inflation rate of negative -7.5%. That means gold has 7.5% yield advantage over cash equivalents.

Gold’s day as an inflation hedge is back!

The April Nonfarm Payroll Report came in near-perfect at 459,000, holding the headline Unemployment Rate at 3.5%. It’s proof that a recession is nowhere near the horizon. A record 2 million workers have recovered jobs during the last four months and 6.6 million over the past 12.

Warren Buffet is Buying Stocks, some $51 billion in Q1. That includes $26 billion into California energy major Chevron (CVX), followed by a big bet on Occidental Petroleum (OXY). These are clearly a bet that oil will remain high for at least five more years. That has whittled his cash position down from $147 billion to only $106 billion. Buffet likes to keep a spare $100 billion on hand so he can take over a big cap at any time. Warren clearly eats his own cooking, buying $26 billion worth of his own stock in 2021. If you can’t afford the lofty $4,773 price for the “A” shares, try the “B” shares at $322.83, which also offer listed options on NASDAQ and in which Mad Hedge Fund Trader currently has a long position.

Elon Musk Crashes His Own Stock, selling $8.4 billion worth last week. His Twitter purchase has already been fully financed, so what else is he going to buy. The move generates a massive Federal tax bill, but Texas, his new residence, is a tax-free state. It continues a long-term trend of billionaires piling fortunes in high tax states, like Jeff Bezos in Washington, and then realizing the gains in tax-free states.

Adjustable-Rate Mortgages are Booming, replacing traditional 30-year fixed-rate mortgage at a rapid pace. Interest rates are 20% lower, but if rates skyrocket to double digits or more in five years, you have a really big problem. ARMs essentially take the interest rate risk off the backs of the lenders and place it firmly on the shoulders of the borrowers.

Travel Stocks are On Fire, with all areas showing the hottest numbers in history. Average daily hotel rates are up 20% YOY, stayed room nights 52%, airfares 39%, and airline tickets sold 48%. Expect these numbers to improve going into the summer.

JOLTS Hits a Record High, with 11.55 million job openings in March, up 205,000 on the month. There are now 5.6 million more jobs than people looking for them. No sign of a recession here. It augurs for a hot Nonfarm Payroll report on Friday.

Natural Gas Soars by 9% in Europe as the continent tries to wean itself off Russian supplies. In the meantime, US producers are refusing to boost output for a commodity that may drop by half in a year, as it has done countless times in the past. If the oil majors are avoiding risk here, maybe you should too.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

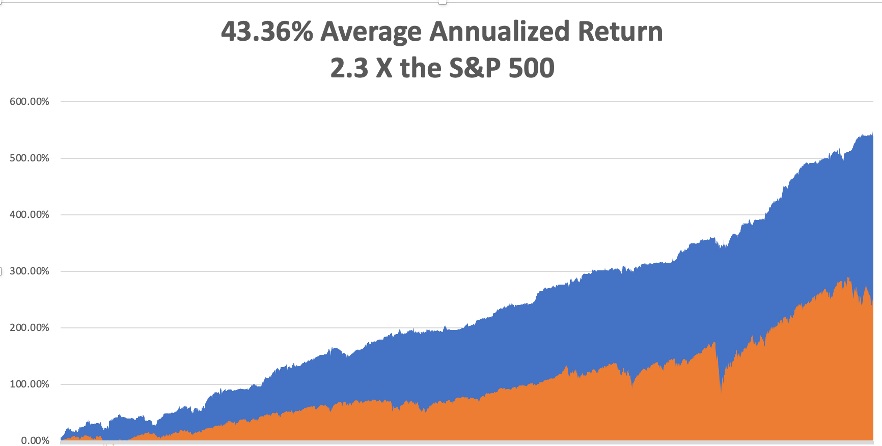

With some of the greatest market volatility seen since 1987, my May month-to-date performance lost 4.27%. My 2022 year-to-date performance retreated to 25.91%. The Dow Average is down -9.3% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 56.62%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 50% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 538.47%, some 2.30 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 43.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 81.9 million, up 500,000 in a week, and deaths topping 998,000 and have only increased by 5,000 in the past week. You can find the data here.

The coming week is a big one for jobs reports.

On Monday, May 9 at 8:00 AM EST, US Consumer Inflation Expectations are released.

On Tuesday, May 10 at 7:00 AM, the NFIB Business Optimism Index is confirmed.

On Wednesday, May 11 at 8:30 AM, the Core Inflation Rate for April is printed.

On Thursday, May 12 at 8:30 AM, Weekly Jobless Claims are disclosed. Conoco Phillips (COP) reports. We also get the Producer Price Index.

On Friday, May 13 at 8:30 AM, the University of Michigan Consumer Price Index for May is disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, not just anybody is allowed to fly in Hawaii. You have to undergo special training and obtain a license endorsement to cope with the Aloha State’s many aviation challenges.

You have to learn how to fly around an erupting volcano, as it can swing your compass by 30 degrees. You must master the fine art of getting hit by a wave on takeoff since it will bend your wingtips forward. And you’re not allowed to harass pods of migrating humpback whales, a sight I will never forget.

Traveling interisland can be highly embarrassing when pronouncing reporting points that have 16 vowels. And better make sure your navigation is good. Once a plane ditched interisland and the crew was found months later off the coast of Australia. Many are never heard from again.

And when landing on the Navy base at Ford Island, you were told to do so lightly, as they still hadn’t found all the bombs the Japanese had dropped during their Pearl Harbor attack.

You are also informed that there is one airfield on the north shore of Molokai you can never land at unless you have the written permission from the Hawaii Department of Public Health. I asked why and was told that it was the last leper colony in the United States.

My interest piqued, the next day found me at the government agency with application in hand. I still carried my UCLA ID which described me as a DNA researcher which did the trick.

When I read my flight clearance to the controller at Honolulu International Airport, he blanched, asking if a had authorization. I answered that yes, I did, I really was headed to the dreaded Kalaupapa Airport, the Airport of no Return.

Getting into Kalaupapa is no mean feat. You have to follow the north coast of Molokai, a 3,000-foot-high series of vertical cliffs punctuated by spectacular waterfalls. Then you have to cut your engine and dive for the runway in order to land into the wind. You can only do this on clear days, as the airport has no navigational aids. The crosswind is horrific.

If you don’t have a plane, it is a 20-mile hike down a slippery trail to get into the leper colony. It wasn’t always so easy.

During the 19th century, Hawaiians were terrified of leprosy, believing it caused the horrifying loss of appendages, like fingers, toes, and noses, leaving bloody open wounds. So, King Kamehameha I exiled them to Kalaupapa, the most isolated place in the Pacific.

Sailing ships were too scared to dock. They simply threw their passengers overboard and forced them to swim for it. Once on the beach, they were beaten a clubbed for their positions. Many starved.

Leprosy was once thought to be the result of sinning or infidelity. In 1873, Dr. Gerhard Henrik Armauer Hansen of Norway was the first person to identify the germ that causes leprosy, the Mycobacterium leprae.

Thereafter, it became known as Hanson’s Disease. A multidrug treatment that arrested the disease, but never cured it, did not become available until 1981.

Leprosy doesn’t actually cause appendages to drop off as once feared. Instead, it deadens the nerves and then rats eat the fingers, toes, and noses of the sufferers when they are sleeping. It can only be contracted through eating or drinking live bacteria.

When I taxied to the modest one-hut airport, I noticed a huge sign warning “Closed by the Department of Health.” As they so rarely get visitors, the mayor came out to greet me. I shook his hand but there was nothing there. He was missing three fingers.

He looked at me, smiled, and asked, “How did you know?”

I answered, “I studied it in college.”

He then proceeded to give me a personal tour of the colony. The first thing you notice is that there are cemeteries everywhere filled with thousands of wooden crosses. Death is the town’s main industry.

There are no jobs. Everyone lives on food stamps. A boat comes once a week from Oahu to resupply the commissary. The government stopped sending new lepers to the colony in 1969 and is just waiting for the existing population to die off before they close it down.

Needless to say, it is one of the most beautiful places on the planet.

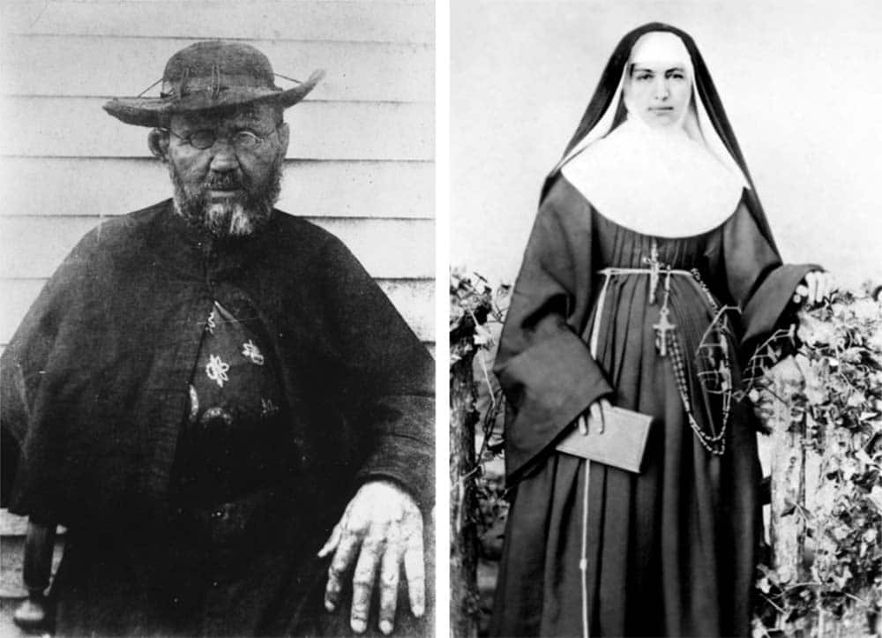

The highlight of the day was a stop at Father Damien’s church, the 19th century Belgian catholic missionary who came to care for the lepers. He stayed until the disease claimed him and was later sainted. My late friend Robin Williams made a movie about him but it was never released to the public.

The mayor invited me to stay for lunch, but I said I would pass. I had to take off from Kalaupapa before the winds shifted.

It was an experience I will never forget.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 27, 2022

Fiat Lux

Featured Trade:

(GOOGLE LAYS AN EGG)

(GOOGL), (TIKTOK), (NFLX), (FB)

It’s not that easy to make money in big tech these days – that is what the big takeaway was with the Google (GOOGL) or Alphabet earnings report that came out after the close yesterday.

The glory years are long gone.

First, it was almost like Groundhog Day with the Netflix-like streaming catastrophe that has now victimized yet another tech company.

YouTube competes differently with other streamers and is reliant on the digital ad model which is why an ad shows every 10 seconds when we watch YouTube.

I know it’s annoying but that’s how they grow revenue, and the blame was squarely attributed to China’s TikTok which is a short-form video platform eating everyone else’s lunch.

YouTube led all platforms in the first quarter of 2022 when respondents were asked which platform they used most often for mobile video, but YouTube dropped to 35% of respondents vs. 45% in the first quarter of 2021 while TikTok was #2 with 22%.

Besides, YouTube is literally entertainment, and with the health situation normalized again and the weather heating up, don’t blame others for grabbing a beer or two with their friends whom they haven’t seen for ages.

That clearly doesn’t help the YouTube ad revenue when people are out and about.

Google will need to deal with this TikTok problem because it’s real and it’s not disappearing anytime soon.

Google has a TikTok copy called YouTube Shorts and it’s not going that well if we compare it to TikTok which has surged to well over 1 billion subscribers.

If management allows the platform to get stale, it could become another dying tech company like Facebook.

The sum of the parts wasn’t particularly impressive either and that is weird to say based on Google’s history of outperformance.

Investors almost never see them miss on the top and bottom line and the EPS miss was not even close.

Things are getting more expensive for all of us, and Google just laid bare what we knew it our guts.

Just look at their research and development spend, it went from $7.5 billion to $9.1 billion which is a $1.6 billion increase in nominal spend.

They are also getting less revenue from Google Play which lowered developer fees to 15% or less for 99% of apps, down from 30% previously.

The bright spots were search advertising and cloud businesses.

Google Cloud has been growing quickly, but still remains unprofitable. It grew sales 43% for the first quarter to reach $5.8 billion, which was about in line with expectations. However, operating losses were wider than expected at $931 million.

Investing aggressively in the cloud is Google’s silver bullet, and that’s clearly having an impact in terms of the free cash flow numbers as well as the higher expenses and the margin compression we’re seeing not only in that segment but in the broader business.

Big Tech is decelerating, and external forces are magnifying the weakness in growth.

I do believe much of the negativity has been priced into GOOGL’s stock and this isn’t the case of a broken business model like Netflix (NFLX) or Facebook (FB).

I believe GOOGL shares will have a positive second half of the year.

Global Market Comments

April 20, 2022

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Global Market Comments

April 8, 2022

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 29, 2022 LONDON STRATEGY LUNCHEON)

(APRIL 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (TBT), (AAPL), (IBB), (GOOGL), (ADBE), (NVDA), (FXE), ($BTCUSD)

Below please find subscribers’ Q&A for the April 6 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: The iShares Biotechnology ETF (IBB) is down quite a bit—do I wait a bit longer to put on a debit call spread LEAPS for the end of this year and possibly the end of 2024?

A: This is really one of the two most interesting parts of the market right now. The biotech stocks have been absolutely destroyed over the past year—down 70, 80, 90% in some cases; and at that level, the worst-case scenario is in the price. Maybe we bounce along the bottom for another year. In the best case, these things all double or triple or even go up 10 times. We’re very close to putting on a 2024 call spread in the best biotech names, and if you get the Mad Hedge Biotech Letter (Click here for the link), you already know what they are because the downside risk on these things is getting close to nil, and the upside is 10 times. I like that kind of math—when the upside versus the downside is 10 to 1 in your favor. When I see specific LEAPS opportunities, I’ll send them out to you, but the answer is: not yet. We’re getting very close on biotech, however.

Q: I sold about a third of my ProShares UltraShort 20+ Year Treasury (TBT) position at $22.00 for a nice 40% gain, thank you very much. Should I hold the rest for a while? And is there a significant upside for 2022?

A: I’ve been telling everyone: hold those shorts. I know those of you who put on the December $150-$155 vertical bear put spread or the December $145-$150 vertical bear put spread already have substantial profits, but the time value on these options is still large, so there is still quite a lot of these profits to be made hanging on to all of your put spreads in the ProShares UltraShort 20+ Year Treasury Bond ETF (TLT). And is there a substantial downside from here? I think yes! If the Fed goes to a half-point rate hike schedule for the next 4 meetings, the (TLT) is absolutely going down to a $105 or $110 level or so. So, keep those shorts and add to shorts on rallies. We came close. I said sell on a $6 point rally and we got a $5 point rally. I didn't pull the trigger, and of course, now we’re here at new lows.

Q: Are we close to buying LEAPS in tech?

A: Yes, I think that once this current meltdown finishes, I want to go back in there. But I want to go long-dated.

Q: What does rapid unwind of the Fed balance sheet mean for the markets?

A: It’s terrible! The Fed has a balance sheet close to $9 trillion dollars. Before the financial crisis of ‘07, it was $800 million dollars, and in fact, in the last 4 years, it has gone up from $20 trillion to $30 trillion. So these are just bubblicious levels for the Fed to own. And what is QT or quantitative tightening? They sell those bonds. And of course, everyone knows they’re going to sell, so they’re dropping bids for bonds like crazy right now—that's why you’re getting the meltdown in the (TLT). This is bad for the stock market; there’s no world in which the stock market goes up with sharply rising interest rates. The best case is that you give up 20% and then make some of it back, and then give up 20% and then make some of it back. So yeah, expect to hear a lot about QT. We only ended QE or quantitative easing about 3 weeks ago, and it looks like we may go straight into QT as soon as May. And boy, the bond market is sure reflecting that today.

Q: How long will wage inflation last? Can I count on 10% pay increases forever?

A: No, it will last until the next recession. I have a feeling that the unemployment rate will hit all-time lows next month—probably 3.2% or 3.3%. And we’re essentially at a full employment economy right now. What happens next? Recession probably in one or two years. Then those wage hikes disappear completely, and people start getting laid off, and goodbye to inflation of all kinds since 60% or 70% of the inflation calculation is wage cost.

Q: What is a good age to retire?

A: Never. I can’t tell you how many friends I’ve had who retire and die within a year. I had one friend retire and he died the next day. What you could do is keep your old job and cut your hours by half, or you could retire from your old job to go on to a new job that you love, like opening a restaurant or a job built around your lifetime hobby, whatever that is. As long as you stay engaged, you keep Alzheimer’s at bay and you’re an active contributing person to society. As soon as you stop doing that and just start doing something like golf, your days are numbered.

Q: What factors will create a recession in 2022?

A: Well I don't think that's going to happen; that would be like multiple 1% rate rises by the Fed, and the Fed completely panicking like we said, and causing a premature recession. But I do think that by 2024 rates will be so high that we will get a recession, probably a short one, maybe 6 months. A lot also depends on the war and if Europe can replace their Russian gas/oil fast enough or they go into an oil shock and recession there.

Q: Will the Fed destroy the economy in order to save it?

A: Yes, they will, if we get inflation up into the teens, which we saw in the 1980s, they absolutely will raise rates. And then I think the 10-year made it to 12% in the early 80s when Volcker was around, and the overnight rate got to 18%. And I know that because I bought a coop in New York City with a mortgage rate of 18%. I took out one of the first floating rate mortgages and by the time I sold the house, the mortgage rate had dropped down to 11% and the value of the home had doubled.

Q: Google (GOOG), Adobe (ADBE), and Apple (AAPL) spreads are treading water.

A: That is a sign that these are the stocks that will lead the next recovery. So, only 20% down, top to bottom, in Apple while all other stocks were getting hammered for 40% or more means Apple is going to lead any recovery in the market. Watch these big tech stocks carefully—they are the new leaders, they just don’t know it yet.

Q: What will inflation do to the housing market? Should I sell or hold my investment properties?

A: Keep them. Housing is one of the biggest beneficiaries of inflation. Not only do the house prices go up, so does everything that goes into the house, like the copper, steel, lumber, kitchen appliances, etc. You really have the best play on inflation, and I don’t think interest rates will kill the housing market. I think all that will happen is people will move from 30-year fixed to 5-year adjustables, as they have done in previous high interest rate cycles.

Q: Where is the buy territory on the Mad Hedge Market Timing Index?

A: Below 20. It’s almost impossible to lose money when you buy at a market timing index of 20. You may get a day or two visit down into the teens, but if you hang on, that’ll become a big moneymaker for you. That’s been working for me for 50 years—it should work for you too.

Q: Do the chips and transports breaking down worry you about the general market?

A: No, I think they’re discounting a recession that isn’t going to happen. Remember half of all the recessions discounted in the market don’t actually happen, and I think that these are one of those non-recessionary selloffs. But it may take them a couple of months to figure out that this bull market still has a couple of years of life to it and that it’s too early to sell. By the way, once people realize that they discounted the recession too early, what are they going to pour back into the fastest? The semiconductor stocks. That's why I’ve got a laser focus on NVIDIA (NVDA).

Q: If there is no recession coming, are the retailers getting too oversold?

A: Yes, but in the world that’s out there, where you really only want to own two or three of the best sectors and avoid the other 97, retailers are the ones you want to avoid—unless there's some specific single company story that you know about.

Q: Housing prices can’t fall when there's such enormous demand coming from millennials, right?

A: That’s true. In fact, the number of houses that need to be built to meet this demand is anywhere from one to five million, so this is a shortfall that will take at least a decade to address, and house prices don’t fall in that situation. They may appreciate at a slower rate, but they will appreciate, nonetheless.

Q: Is there any level where you would consider a call spread in the TLT?

A: Well, I had the April $127-$130 vertical bull call spread and I had my head handed to me. So somewhere, but clearly not yet—again, it depends a lot on what the Fed does and how fast.

Q: What’s the outlook for the Euro (FXE), (NVDA)?

A: Lower. Until the Ukraine War ends, they get an economic recovery, and they wean themselves off of Russian energy and move over to American energy. And that's at least a year down the road, so I’m not rushing into any European investment—stocks, bonds, or currencies.

Q: Are rising interest rates good for banks?

A: Yes, but right now those benefits are being offset by recession fears which will probably go away in a couple of months. So that kind of makes banks a strong buy right here.

Q: When the Shanghai lockdown ends, will it create another surge in commodity prices?

A: Absolutely, yes. China is the world's largest consumer of commodities, and the restoration of any of their purchasing power will certainly be great for all commodity prices—food, energy, metals, you name it.

Q: Is Tesla (TSLA) a LEAPS candidate?

A: Yes but wait for it to take a run at the $700 low that we saw last month. We probably won’t get there, but $800 this time around is probably a great LEAPS candidate for Tesla going forward. I expect them to meet all of their goals for production this year.

Q: Won’t Bitcoin ($BTCUSD) keep falling if equity markets are lower?

A: Yes, but we don’t have that much lower to go in equity markets—maybe 10%. So just as we’re looking to buy equities and the smaller technology stocks on dips, we're also looking to buy Bitcoin on dips. If we can get back into the $30,000 handle, that might be a ripe buy territory for all the cryptocurrency plays.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 1, 2022

Fiat Lux

Featured Trade:

(THE CREATIVE CLOUD IS OVERSOLD)

(ADBE), (AAPL), (GOOGL)

Creative software giant Adobe (ADBE) has ironclad support at $440 on a technical basis and I am willing to go on a 13-day excursion with the underlying stock.

That being said, the macroeconomic picture leaves a lot to be desired and one could literally say that 100 times.

Many of the risks have yet to be unlocked if one rolls through the list of them like hyperinflation, spiking energy costs, the military conflict, rising rates, poor global government, and the list really could be added to for infinity at this point.

No need to beat a dead horse.

However, this breathtaking relief rally has turned into something that is probably more than just a relief rally and has told us investors one thing.

There is still way too much liquidity in the system and it’s still sloshing around.

And although I missed the bottom of the relief rally, I seek to benefit off the next stage of it with ADBE and GOOGL which are two highly sought-after tech stocks with a proven track record and whose technical picture looks positive in the short-term.

The cheat sheet for this exam is Apple (AAPL) whose bounce from $150 to $180 really summed up what’s going on in the tech ecosystem.

The best of breed is harvesting the bulk of the gains, and instead of fighting it from the other side, I’ll just traverse on the side of Apple and ride it up with them.

The dip-buying has been almost violent in this rally and although I do believe there will be some reduction in the pace of the up moves, it’s almost impossible to go completely bearish against tech right now.

Another key insight into recent stock movement is that the nominal size of the stock market at this point is so gigantic in terms of market cap that the leverage inside of it is causing volatility to go nuts.

I don’t think this will resolve itself in the near future and this sets the stage for some series of epic up moves moving forward to the second half of the year as a large swath of negativity has been priced into the news.

Tech could go back to its overshooting the rest of the market narrative and names like ADBE and GOOGL will perform splendidly with this type of boost.

Let’s get into the weeds and explain why I really do like ADBE as a standalone company?

The massive slide over the past few months was nothing structural. ADBE posted market-beating earnings for the first quarter, growing cloud revenue, one of the biggest markets in the tech world, to more than $2 billion. The firm has also been steadily shot up the digital subscription revenue ladder.

Yes, their product lines are slowing but they are at the cutting edge of digital innovation which with its terrific brand has great pricing power.

ADBE has transformed itself into a software behemoth, more than tripling its revenue since 2010. The company is famous for its namesake PDF-reader and photo-editing software Photoshop.

However, ADBE’s bread and butter is a full suite of software products monetized through a recurring subscription model.

ADBE transitioned from selling boxed software to recurring subscriptions in 2013 and revenues have gone parabolic since.

Readers must be practical at this point and not focus attention on the low end of tech.

Tightening conditions in the capital markets mean that there will be less resources to throw at the poor-quality tech names.

Practicality should be the foot forward with readers piling into the best of tech like APPL, AMZN, GOOGL, ADBE, and MSFT.

Don’t get too cute here.

Traders never go bankrupt from taking a profit.

Mad Hedge Technology Letter

March 21, 2022

Fiat Lux

Featured Trade:

(TRUST THE CLOUD)

(AMZN), (ZS), (CRM), (GOOGL)