Global Market Comments

August 3, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Global Market Comments

August 3, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Mad Hedge Technology Letter

July 28, 2021

Fiat Lux

Featured Trade:

(THE REAL RULES OF TECH)

(MSFT), (FB), (GOOGL), (AAPL), (AMZN), (NFLX), (TSLA)

Northern Californian tech companies stopped innovating because of the monopolistic nature of current business models that nestle nicely in unfettered capitalism.

They only go by one principle these days – to crush anything remotely resembling competition and they are damn good at doing it.

This has been going on in Silicon Valley for years and the government has turned a blind eye since the beginning of it.

The end result is the absence of competition.

At a higher tech level, the strong get stronger by stockpiling cash and resources, all while taking advantage of historically low rates to finance their growth models.

Why does the U.S. government largely sit on the sidelines and act if nothing has really happened?

If I deploy the concept of Occam's razor to this situation, a philosophical rule that entities should not be multiplied unnecessarily which is interpreted as requiring that the simplest of competing theories be preferred, my bet is that most of U.S. Congress own stock portfolios, even if they are the index variety, and these portfolios are spearheaded by the likes of Apple (AAPL), Facebook (FB), Amazon (AMZN), Google (GOOGL), Microsoft (MSFT), Netflix (NFLX), and of course Tesla (TSLA).

This has come into the open frequently with members of Congress even front-running the March 2020 sell-off with their own portfolios like U.S. senator Kelly Loeffler from Georgia selling $20 million in stock after attending special intelligence briefings in the weeks building up to the coronavirus pandemic.

We definitely don’t get invites to those special intelligence briefings, but Loeffler getting off scot-free by mainly just playing down what she did proves the immunity that politicians accrue from their lofty positions.

It’s a direct conflict of interest, but that's not surprising for politics in 2021 and I would say it epitomizes the era we are in.

It’s also why Congress hasn’t acted on Silicon Valley’s excessive abuse of power, which is so glaringly blatant that excuses must be crafted just to make it seem they aren’t as bad as they are.

The government likes to jawbone to the public saying they will make competition a level playing field, but actions show they are doing the opposite.

Ultimately, Silicon Valley whispers in the ear of Congress and they listen.

Well, what now?

Tech has now turned mostly into a digital marketing lovefest harnessed around the smartphone and tablet with cheap shortcuts which is partly why the efficacy of the internet has dropped greatly.

The advent of 5G has also been a bust because these titans don’t feel the need to reinvest to make that killer 5G app when they don’t need to.

The truth is Silicon Valley couldn’t be more complacent in 2021.

They are the ultimate corporate entity and more monolithic than ever.

Smart CFO’s are continuing the gravy train by diving deep into stock buybacks to boost stock prices and the dividends are the extra kicker.

The iPhone maker repurchased $19 billion of stock in the first quarter, bringing the total for the past fourth quarters to $77 billion.

GOOGL repurchased a record $11.4 billion of stock in the first quarter, up from $8.5 billion a year earlier, and FB bought back $3.9 billion, triple the total a year ago.

Now, they even got the White House to do their dirty work.

Huawei, the Chinese telecom company, has been the punching bag for the White House’s tech war with China.

In remarks to reporters in March 2019, Chinese politician Guo Ping said, “The U.S. government has a loser’s attitude. They want to smear Huawei because they can’t compete with us.”

Let’s get this straight, U.S. tech was never behind China and still isn’t, but I do believe the U.S. should simply outcompete with Huawei because I know they can and have the capacity to do so.

China hasn’t done much with 5G as well aside from amassing the patents, but they haven’t made it quite practical to the Chinese public as a use case for consumer products.

Instead of competing, we have Facebook tapping the political back channels to encourage the U.S. government to ban TikTok, not because it threatens Facebook’s model but because Facebook is concerned about national security.

This is from the same Mark Zuckerberg that has been attempting to destroy Snapchat (SNAP) for years after SNAP’s CEO Evan Spiegel refused to sell it to Zuckerberg.

So why innovate? Why deploy capital into research and development when you can just nick a crown jewel and make it your own?

Exactly, so innovation does not happen and will not happen.

We, as consumers, have been thrust into the cluster of ever-degrading smartphone apps that offer less and less utility.

But ultimately, even if you hate Silicon Valley at a personal level, it is literally impossible to bet against them, because all this posturing behind the scenes does boost the share price and that’s what this technology letter is about.

As we are whipsawed into this muddling world of partially vaccinated economies, tech will consolidate after they deliver earnings only to prepare for the next leg up in shares.

Sure, this year’s growth and EPS estimates have been priced perfectly, but we will start to move onto next years’ bounty and these models have never been more profitable.

Don’t fight the trend.

Global Market Comments

July 26, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GETTING INTO STUDIO 54),

(AAPL), (AMZN), (TSLA), (GOOGL), (FB), (NVDA), (TLT)

During the heyday of my Morgan Stanley career in the 1980s, back when I had an unlimited expense account, a favorite place to take clients was Studio 54.

The place was full of rock stars, the music was piercing, and strange things were happening in dark corners. It was all the perfect adventure for the impressible visitor from the sedentary Midwest.

Studio 54 was notoriously difficult to get into. There were these hefty doormen dressed in black with big gold chains who did the vetting. If you were famous or a free-spending investment banker, the red ropes were cast aside, and you glided right in. $100 tips spoke volumes too. The hoi polloi could only watch with envy, even after spending hours in line.

The stock market has become a lot like Studio 54. It’s not letting you in. I had ten trade alerts lined up to get into the market on Friday and Monday. I only got off four. After a scant 3.2% decline, stocks turned around so fast it made your head spin. There are strange things happening in dark corners too.

Next week is the first time in a decade when the top five tech companies report earnings. If history is any guide, they will sell off sharply on the reports, form a base in August, then begin their yearend ramp up. This is why I have been hanging on to my short positions.

I continue to belie that the major miss by the markets is how much they are underestimating tech earnings. Maybe they have fully discounted 2021 earnings, but what about 2022-2030?

Let me give you the example of Apple alone. 5G wireless technology is rolling out now which is improving performance by ten times. What about 6G, 7G, and 8G? The cumulative performance gains of a decade of technological improvement is 10,000 times at zero cost!

Do you think Apple will buy more of its own stock in anticipation of this? Do you think everyone else will too?

You bet!

The “Delta” Correction lasted a day, with deaths in some states up 100% in a week. It is a pandemic of the unvaccinated and of children. The stock market was already ripe for a 5% correction. That’s what happens when you double in 16 months. The bond market at a 1.10% yield thinks the recovery is over and we’re going below 1.00% for the ten year.

Facebook is killing people, says Biden, through enabling the spread of vaccine information. Right-wing website says the vaccine causes sterility, alters your DNA, and enables the government to track your location. (FB) says members have the right to lie to each other. This isn’t going away. (FB) shares hit a new all-time high, taking its market cap into the trillion-dollar club.

That was the shortest recession in history in 2020, lasting only two months. Straight down and then straight up, making it the shortest recession in history. But what two months it was, with an eye-popping 22 million jobs disappearing in March and April. We have since made more than half back.

The month-end selloff is back in play, with the 800-point bounce behind us. That’s when big tech reports. With trillions of dollars struggling to get into the market on any dip, a two-day, 3.2% correction is all we are going to get. I managed to strap on stock longs and bond shorts yesterday, but even I got left on the sidelines with my other trade alerts.

Bitcoin breaks $30,000, then bounces back up. It seems to be an inflation/rising interest rate play which does poorly when ten-year yields hit 1.12%. It’s almost trading 1:1 with Freeport McMoRan (FCX). That has to mean we’re soon entering “BUY” territory.

Rents are soaring, up 6.6% in May YOY, according to data collection firm Corelogic. It’s the biggest gain since 2005. Single-family homes, about half of the rental market, are leading the charge. Phoenix is delivering the biggest increases, up 14% YOY, followed by Dallas and Atlanta. What a great time to own!

Share buybacks are turbocharging this market, which could reach an eye-popping record $1 trillion in 2021 and another $550 billion in dividends. Q2 has already seen $350 billion in buybacks. Apple (AAPL) is leading the charge with a monster $250 billion in cash. Alphabet (GOOGL), Microsoft (MSFT), and Berkshire Hathaway (BRKB) follow. Even companies that have never bought the stock before may enter the fray, like Netflix (NFLX), which is a cash flow cow. My yearend target of an S&P 500 at 4,750, up 9.2% from here, is now looking totally attainable.

Existing Home Sales are up 1.4% in June to 5.86 million units, less than expected. Inventories are down 18.8% YOY to 1.25 million units to a 2.6-month supply. The Northeast was the leader, up 2.8%. Median home prices are still soaring to $363,000 and up an eye-popping 23.4% YOY. Sales of homes priced over $1 million are up 147%. No typo here. Some 14% of homes are now sold to investors, while 23% were to all-cash buyers.

GM recalls 69,000 bolts over recharging fire risk. The Ev's use will be severely restricted until fixed, citing “rare manufacturing defects.” Bolts use imported Korean batteries from LG. It’s what happens when you move into a new technology a decade late and rush to catch up. GM will never catch (TSLA). Avoid (GM) and buy (TSLA).

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch profit suffered a -1.65% loss so far in July. My 2021 year-to-date performance appreciated to 66.95%. The Dow Average is up 14.57% so far in 2021.

Two of my positions, a long in (JPM) and a short in the (TLT) did great. But I really took it on the nose with my short positions in the (SPY) when the market melted up on Friday. That should turn out OK when all five big tech companies report this week, which historically marks a market top. That leaves me 60% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

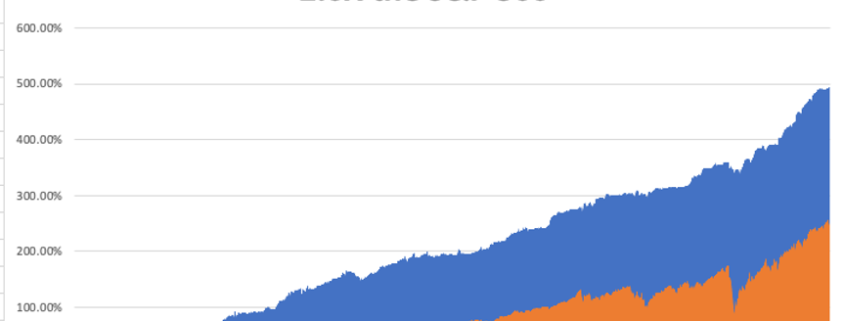

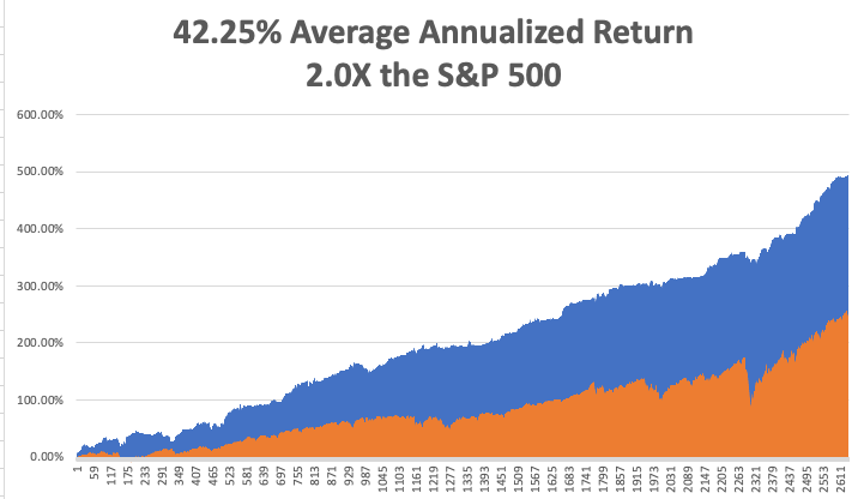

That brings my 11-year total return to 489.50%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.25%, easily the highest in the industry.

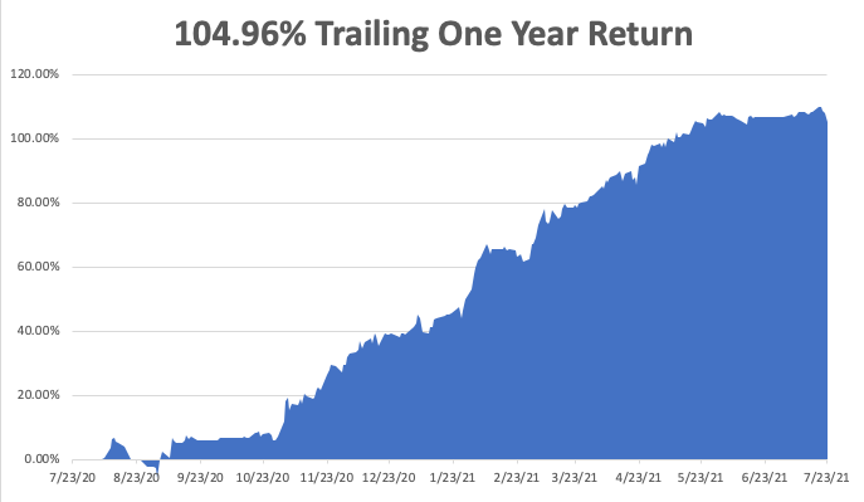

My trailing one-year return exploded to positively eye-popping 104.96%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 34.4 million and rising quickly and deaths topping 611,000, which you can find here. Some 34.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, July 26 at 11:00 AM, New Homes Sales for June are released. Alphabet (GOOGL), Tesla (TSLA), and Amazon (AMZN) report.

On Tuesday, July 27 at 10:00 AM, the S&P Case Shiller National Home Price Index for May is published. Apple (AAPL) reports.

On Wednesday, July 28 at 9:30 AM, the Wholesale Price Index for June is disclosed. Facebook (FB) and Microsoft (MSFT) report.

On Thursday, July 29 at 8:30 AM, we get Weekly Jobless Claims. We also learn the first look at Q2 US GDP, which should be a blockbuster.

On Friday, July 30 at 8:30 PM, we get Personal Income & Spending for June.

As for me, when I was shopping for a Norwegian Fiord cruise for next summer, each stop was familiar to me because a close friend had blown up bridges in every one of them.

During the 1970s at the height of the Cold War, my late wife Kyoko flew a monthly round trip from Moscow to Tokyo as a British Airways stewardess. As she was checking out of her Moscow hote, someone rushed at her and threw a bundled typed manuscript that hit her in the chest.

Seconds later, a half dozen KGB agents dog-piled on top of her. It turned out that a dissident was trying to get Kyoko to smuggle a banned book to the West and she was arrested as a co-conspirator and bundled away to Lubyanka Prison.

I learned of this when the senior KGB agent for Japan contacted me, who had attended my wedding the year before. He said he could get her released, but only if I turned over a top-secret CIA analysis of the Russian oil industry.

At a loss for what to do, I went to the US Embassy to meet with ambassador Mike Mansfield, who as The Economist correspondent in Tokyo I knew well. He said he couldn’t help me as Kyoko was a Japanese national, but he knew someone who could. Then in walked William Colby, head of the CIA.

Colby was a legend in intelligence circles. After leading the French resistance with the OSS, he was parachuted into Norway with orders to disable the railway system. Hiding in the mountains during the day, he led a team of Norwegian freedom fighters who laid waste to the entire rail system from Tromso all the way down to Oslo. He thus bottled up 300,000 German troops, preventing them from retreating home to defend themselves from an allied invasion.

During Vietnam, Colby became notorious for running the Phoenix assassination program.

I asked Colby what to do about the Soviet request. He replied, “give it to them.” Taken aback, I asked how. He replied, “I’ll give you a copy.” Mansfield was my witness so I could never be arrested for being a turncoat. Copy in hand, I turned it over to my KGB friend and Kyoko was released the next day and put on the next flight out of the country. She never took a Moscow flight again.

I learned that the report predicted that the Russian oil industry, its largest source of foreign exchange, was on the verge of collapse. Only massive investment in modern western drilling technology could save it. This prompted Russia to sign deals with American oil service companies worth hundreds of millions of dollars.

Ten years later, I ran into Colby at a Washington event and I reminded him of the incident. He confided in me, “You know that report was completely fake, don’t you?” I was stunned. The goal was to drive the Soviet Union to the bargaining table to dial down the Cold War. I was the unwitting middleman. It worked. That was Bill, always playing the long game.

After Colby retired, he campaigned for nuclear disarmament and gun control. He died in a canoe accident in the lake in from of his Maryland home in 1996.

Nobody believed it for a second.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

July 20, 2021

Fiat Lux

FEATURED TRADE:

(A SNAPSHOT ON HOW TO LIVE A BETTER LIFE)

(DXCM), (CVS), (WBA), (RAD), (MDT), (ABBT), (SENS),

(TDOC), (AMWL), (AMZN), (AAPL), (GOOGL), (GRMN)

The routine medical check-ups we have today are primarily based on physical exams that were developed way back in the 1820s, utilizing tools that haven’t been upgraded for over a century.

More alarmingly, all we go through is a “comprehensive” health check once every year, offering us just a snapshot of what’s truly going on in our bodies.

If anything, we monitor the releases of new software for our phones and laptops more than we pay attention to our own bodies.

As we’ve proven with the COVID-19 pandemic, so much can happen in a year

Truth be told, our bodies can deteriorate at lightning speed and without any warning. That’s why it’s terrifying to think that we’re not doing as much to monitor our health.

So, what can we do to change this? How can we be more proactive when it comes to our health?

The COVID-19 pandemic has brought many changes into our lives, and this is one of the biggest transformations it has done: an exponential spike in demand for telehealth services.

One of the major issues between patients and doctors at the height of the pandemic was how to go through the physical exams without actual physical contact.

Clearly, it’s not possible to hear a heart murmur or irregular breathing over a video call.

This is where a lot of innovative companies come in.

For a more specialized exam, HD Medical released a credit card-sized device called HealthyU.

Patients simply touch it with their finger, and the device can instantaneously measure their heart rate and sounds, temperature, and even oxygen saturation.

All these data would then be sent to their doctors or health providers in real-time.

HealthyU also has a remote EKG, which effectively allows it to serve as a portable roadmap to a patient’s heart health and helps doctors monitor for signs of heart attacks and arrhythmias.

For example, there’s this handheld exam kit called Tyto that patients can use to perform their own guided medical exams.

This palm-sized gadget is linked to an app, so your doctor can monitor you remotely.

Patients suffering from a sore throat can use Tyto’s camera to let the doctors see the back of their throats, while those struggling from chest pains can easily use the stethoscope to help their physicians listen to their lungs and hearts.

And these are just for physical exams. There are more advancements in health monitoring, and this is where wearable technology comes in.

Wearable technology is considered one of the most promising growth drivers, largely due to the health sector.

The market size for this segment is estimated to rise from $116.2 billion in 2021 to $265.4 billion by 2026, showing off an 18% CAGR growth within a 5-year period.

Applications for wearables have expanded to areas including medical surgery as well as internables and implantables or sensors, which can be fitted into our bodies to help doctors observe various health parameters.

It’s no wonder brands like Apple (AAPL) with Apple Watch, Google (GOOGL) with Fitbit, and Garmin (GRMN) have been working overtime to try to cover as much of the wearable health market as possible.

So far, these products provide extensive data ranging from calories burned to our heart rates.

Aside from them, there are other wearables in the market today that could change the landscape of the health industry.

One of them is the Oura Ring, which was first introduced in 2013.

Designed to be worn 24 hours a day, this device measures the bodily functions of the user. It gathers data through infrared light sensors that touch the finger arteries.

One of the most impressive things it can do is monitor your sleep movements to help determine early onset of some neurodegenerative diseases like Parkinson’s.

The information is all sent to the app, which users can access via their smartphones. The Oura Ring is somewhere between $299 and $999, depending on your preferences in style and color.

Although it’s yet to be a mainstream product, the Oura Ring was provided to NBA players when they resumed their season amid the COVID-19 pandemic.

The device was used to help the basketball stars monitor their health.

In fact, a joint study with the University of California San Francisco showed that the Oura Ring was able to help detect the common symptoms of COVID-19 three days earlier and with as high as 90% accuracy.

Another impressive health monitoring advancement covers the glucose monitoring product line of Dexcom (DXCM).

The primary goal of Dexcom is to take away the guesswork that comes with finger pricking.

By offering a wearable sensor, people with diabetes can easily and accurately monitor their glucose levels.

What’s even more convenient is that Dexcom’s wearable is available in practically all large pharmacies like CVS (CVS), Walgreens (WBA), and Rite Aid (RAD).

To date, Dexcom’s biggest competitors include Medtronic’s (MDT) Guardian Connect, Abbott’s (ABBT) Freestyle Libre, and Senseonics’ (SENS) Eversense.

These are only some of the emerging technologies that could help us improve the quality of our lives today, with thousands more expected to follow suit in the years to come.

For an endlessly advancing world with smartphones, supercomputers, smart homes, and even self-driving cars receiving software updates virtually every week, it’s absurd to think that we only allot a single check-in on our health annually.

But with the advent of these technologies and the increasing popularity of telehealth services spearheaded by the likes of Teladoc (TDOC), Amwell (AMWL), and even Amazon (AMZN), it looks like we’re starting to finally pay more attention to our health.

Mad Hedge Technology Letter

July 16, 2021

Fiat Lux

Featured Trade:

(THE CLOUD)

(AMZN), (GOOGL), (CRM)

Dealing with the Cloud works and for every relevant tech company, this division serves as the pipeline to the CEO position.

If that’s not the case, then there’s something egregiously wrong!

Take Andy Jassy, the mastermind behind Amazon’s lucrative cloud computing division, and is the man who will succeed company founder Jeff Bezos.

He’s been rewarded this important business based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon exactly 27 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Can you believe that Amazon's stock started out at $1.50 per share when adjusting for future equity splits?

It now trades at more than $3,500 per share and is worth over $1.8 trillion, making it one of the most valuable companies in the world.

Amazon's annual profit almost doubled in 2020 to $21.3 billion stoked by the pandemic that forced people to stay home and use Amazon services.

Consumers had no choice but to shop online, helping the company grow revenue 38% to $386.1 billion.

What exactly is the cloud that Amazon created?

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them working remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the recent ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Now you might digest somewhat how Amazon built their share price from $1.50 in 1997 to over $3,500 today.

Thanks to the cloud.

Mad Hedge Technology Letter

July 12, 2021

Fiat Lux

Featured Trade:

(RIDE THE MOMENTUM)

(SHOP), (NFLX), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)