Mad Hedge Technology Letter

December 11, 2020

Fiat Lux

Featured Trade:

(THE DIGITAL AD INDUSTRY COMEBACK)

(TTD), (GOOGL)

Mad Hedge Technology Letter

December 11, 2020

Fiat Lux

Featured Trade:

(THE DIGITAL AD INDUSTRY COMEBACK)

(TTD), (GOOGL)

It’s been a helter-skelter year for tech investors and The Trade Desk (TTD) is one of those examples of a company whose fortunes have gone from rags to riches.

The spring started off with unrelentless economic pressure forcing companies to slash their marketing budgets to preserve capital.

One of the victims were digital advertisers.

The Trade Desk's shares cratered 40% but has since reversed course and is up more than 200% so far this year.

That’s not to say that in today’s digital marketing world, we have utter clarity – we don’t.

But uncertainty around the pandemic and the notion that digital marketers have seen the worst of is starting to get baked into the pie which is why we are seeing this massive share appreciation into the end of the year.

The light is starting to appear at the end of the tunnel and companies that slashed their marketing budgets or advertising budgets are starting to ramp up spending as they plan their budgets for 2021.

Through all of this, I am thoroughly impressed with the robustness of The Trade Desk's business model, evident in its third-quarter 2020 results.

While most companies faced enormous headwinds, The Trade Desk reported record revenue of $216 million, up 32% from last year.

Net income more than doubled to $41 million thanks to the company's revenue growth and operating leverage.

This demonstrates the nimbleness of the business, which continued to profit during a once in a 100-year recession.

Consensus was expecting $181 million, and overdelivering by these wide margins is one of the catalysts shepherding the incremental investor into The Trade Desk.

It was only in the 2nd quarter that year-over-year revenue was actually down 13% and then to go from down 13% to up 32% is quite outstanding.

Last year when the company was mushrooming, revenue was up 38% for the year pointing to more signs that the company is back to where it was pre-COVID.

That in itself is a huge victory in the digital ad world.

Breaking out some of the segments, Connected TV was one of The Trade Desk's biggest growth markets.

Connected TV revenue grew over 100% year-over-year, and that was from a strong quarter last year.

Mobile video spending grew 70%, and audio spending grew 70%.

The Trade Desk obviously has its mojo back.

The Trade Desk will go from strength to strength as the vaccine starts to roll out to parts of the developed world and consumers start to return to spending behavior that looks more pre-COVID.

Another bullish sign is that founder Jeff Green is still CEO of the company and owns more than $5 billion of The Trade Desk stock.

As an owner-operator, Jeff has the incentive, as well as the clout to lead the company toward success.

He has a stellar track record.

TTD’s revenue rose 14-fold between fiscal 2014 and fiscal 2019 and has been profitable since 2013 all while many “growth” companies have been burning cash.

TTD is well-positioned to improve on its growth on the back of two major secular trends: the continued migration toward digital advertising and the transition to programmatic advertising.

Data suggests it owns around 1% of the total global ad market - the total addressable market stands at $725 billion.

Clearly, the runway for a company like this is long if they can execute which they have shown consistently is the case.

Compare this with Google (GOOLG), a firm that has mature businesses that rely on ad revenues, and they have had an interesting year enduring some of the elements like TTD because it's a sudden major recession out of the blue.

Companies have used the opportunity to cut their ad spend and rightly so because that’s what happens in recessions, but the interesting fact about TTD is that the TTD is in the sweet spot for where ad money is going to go.

It's throwing the ball to where the wide receiver will get open in the back of the endzone and that's a game-changing takeaway about this company.

In terms of recent cash spend in the U.S., around $600 million to $700 million of the $1 billion that's been spent on this presidential election for advertising goes to TV. It goes to TV ad spending, and that's fourth-quarter ad spend, not third-quarter. Most of that money has been spent in October, and not only that, that big chunk of ad spend goes into just one week.

There is no doubt in my mind that a significant chunk of that flowed through to TTD.

When you think about programmatic advertising next year that goes on TVs, even smart TVs, we have got the Summer Olympics in Japan along with the European soccer tournament that starts in June 2021.

This means huge revenue bumps as big events bring in many unique opportunities.

These are just some of the whispers going on in the industry and I also believe that 2021 will be a year to remember for the digital ad companies.

Remember that consumers are spending, but not on travel, people aren't flying to Bali or Phuket, but they are consuming content online.

I can truly say that the Trade Desk isn’t just a flash in the pan company and that long term, the prospects are incredibly positive for this company, and obviously, that is starting to reflect in a quickly appreciating stock.

Mad Hedge Technology Letter

December 2, 2020

Fiat Lux

Featured Trade:

(SALESFORCE TRIES TO STAY RELEVANT IN THE CLOUD)

(CRM), (WORK), (MSFT), (GOOGL)

This was basically a deal they had to do even though I believe Salesforce (CRM) massively overpaid for Slack (WORK).

The other option would be to fall even further behind Microsoft (MSFT) who has hit a home run with their own in-house iteration of Slack-ish software called Microsoft Teams.

In fact, this is the biggest acquisition in Salesforce’s software history and purchasing the software developer Slack for over $27 billion marks a new chapter in their history.

Through a combination of cash and stock, Salesforce is purchasing Slack for $26.79 a share and .0776 shares of Salesforce.

Other big software deals such as IBM’s $34 billion purchase of Red Hat in 2018, the largest in its history, followed by Microsoft’s $27 billion acquisition of LinkedIn in 2016 are also noteworthy.

Last year, the London Stock Exchange agreed to buy data provider Refinitiv for $27 billion, though the deal has yet to be cleared by European regulators.

Salesforce has decided to grow via M&A as CEO Marc Benioff hopes to stave off a growth downturn by pre-emptively addressing these potential problems.

His goal is to get more investors on board for the long haul.

In the short term, the jury is out on whether Salesforce can “grow into” the high valuation which they agreed to pay for Slack.

Other deals made by Salesforce are when the company spent $15.3 billion on data visualization company Tableau in 2019 and, a year earlier, they captured MuleSoft for $6.5 billion whose back-end software connects data stored in disparate places.

The future of enterprise software is transforming the way everyone works in the all-digital, work-from-anywhere world and Salesforce will be one of the leading voices in how this plays out.

Don’t forget that Salesforce started the enterprise cloud revolution, and two decades later, they are still tapping into all the possibilities it offers to transform the way we work.

For Slack, this is a major victory because they had begun to see the writing on the wall with two uninspiring earnings reports which signaled that Microsoft was having their cake and eating it too.

For Salesforce to pay a 30%-40% premium for Slack reveals the sense of desperation permeating into the ranks of Salesforce management.

Another takeaway is that enterprise software is putting their money where their mouth is convinced that the shelter-in-home economy will last long after the brutal public health crisis is over.

I tend to agree with this diagnosis, but I don’t agree with overpaying for Slack at the degree in which they did.

However, the climate of cheap rates and high liquidity feeds into the normalcy of overpaying for quality assets.

What’s so bad about Slack?

Slack has blamed the downturn in fortunes on some of its small business customers being hurt by the pandemic.

The company has loosened contract structures and extended credits to help them out which is a major red flag.

The slowdown has only fueled nervousness that Microsoft (MSFT) Teams’ ascent is weighing on Slack’s growth potential.

Teams now has more than 115 million users while Slack has a fraction of that, despite having the edge in the minds of most in terms of user interface.

Slack’s slowing growth, in turn, hurt its sentiment and ultimately its stock price.

Salesforce could have acquired Slack for a discount in a year or two, but by that time, Salesforce would be left in the dust.

Salesforce had to act with urgency even if Slack still expects to post a net loss this fiscal year. It’s unclear when Slack will turn a profit-making company even less attractive.

Salesforce will need to subsidize Slack’s losses for the time being.

What’s in it for Salesforce?

Salesforce could help easily scale up Slack to more high-paying corporate customers in a major challenge to Microsoft Teams which would vastly help Slack’s margins.

There are also numerous synergies in being under the Salesforce umbrella which would only strengthen the profit potential of the communications platform.

By acquiring Slack, a business chat service with over 130,000 paid customers, Salesforce is bolstering its portfolio of enterprise applications and filling out its broader software roster as it seeks additional growth engines.

Salesforce obviously believes that the sum of the parts will be greater than each individual segment and I agree.

Salesforce’s annualized revenue topped $20 billion in the fiscal second quarter, with growth of 29%. But the forecast for the full year of 21% to 22% growth would represent the company’s slowest rate of expansion since 2010.

Microsoft and Salesforce are direct rivals at this point and Salesforce is the dominant player in customer relationship management software, where Microsoft is a distant challenger. Both companies tried to buy LinkedIn, the professional networking site, but Microsoft was the ultimate winner.

The company’s core Sales Cloud product for keeping track of current and potential customers delivered $1.3 billion in revenue, up 12% year over year and that’s simply not good enough to be considered a “growth asset.”

Many investors won’t bite at the bid unless a burgeoning tech company is north of 20% and preferably plus 30%.

Salesforce will now embark on a narrative of engineering growth to fit its investors’ preferences, but I do hesitate to think that this will most likely mean continuing to overpay for software companies.

Salesforce does have the resources to absorb this pricey endeavor but is it sustainable when the likes of Microsoft, Google, and so on are competing for the same assets?

Does this mean that Twitter would be $60 billion in today’s climate?

That’s a scary thought.

M&A could disappear soon from tech because the valuations might reach some sort of peak that even cash-rich Silicon Valley firms might balk at.

Yes, we are getting to that stage of tech. Tech is becoming a luxury.

In the short term, buy Salesforce’s dip as some investors will sell as a way to signal to Salesforce that they aren’t happy with their capital allocation strategy and ultimately this isn’t a guarantee of adding growth and could possibly backfire in Benioff’s face.

Mad Hedge Biotech & Healthcare Letter

November 17, 2020

Fiat Lux

FEATURED TRADE:

(WHY TELADOC IS A WIN-WIN-WIN STOCK)

(TDOC), (GOOG), (GOOGL), (AAPL)

Digital health was a struggling sector before COVID-19, but the pandemic changed the game, driving customers and even providers to embrace digital health solutions.

As expected, frontrunner Teladoc Health (TDOC) surfaced as a major beneficiary of this booming industry, reporting a record high in the number of virtual care visits during the ongoing health and financial crisis.

While there are concerns that these rewards could be fleeting, COVID-19 appears to have contributed longer-lasting changes, particularly in consumer behavior.

More and more users are opting for digital health solutions, with total virtual care visits up by 206% to hit 2.8 million in the third quarter of 2020 alone.

A noticeable change in Teladoc’s portfolio is the diversity of diseases they handle.

Previously accounting for only a third of its total care visits in 2019, non-infectious conditions like hypertension, depression, anxiety, and back pain now account for half.

As for the virtual care visits for dermatology and behavioral health in their business-to-business transactions, the company enjoyed a 500% boost year over year.

For context, the total number of virtual visits to Teladoc in 2019 was only 4.1 million.

Since the year 2020 started, though, the company has already recorded almost twice that number at 7.6 million—and the fourth quarter is projected to become its best-performing period yet.

The shift was also evident in the third-quarter earnings report of Teladoc, which showed that the company’s top line jumped by 109% year over year to reach $289 million.

This marks the company’s highest quarterly top-line growth rate.

In fact, this growth rate exceeded even the company's expectations.

When Teladoc released its second-quarter earnings, its Q3 projections were only somewhere between $275 million and $285 million.

As the number of COVID-19 cases continues to climb, it is highly possible that the company will once again deliver much better results than the forecasted numbers in the fourth quarter.

In terms of its fourth-quarter projections, Teladoc is expected to reach roughly 3 million virtual visits in the last months of 2020.

The conservative estimate for Teladoc’s total virtual visits this year is at 10 million.

So far, Teladoc shares are up 133% year-to-date, with the company expected to cross the $1 billion revenue mark in 2020—an almost 100% increase from its 2019 projection.

In terms of future growth, Teladoc recently completed an $18.5 billion mega-merger with Livongo Health (LVGO), making it a one-stop-shop for every virtual care need.

As a combined unit, the Teladoc-Livongo partnership is hailed as the next-generation virtual care provider. Simply put, this newly formed company is the future of the healthcare industry in America.

This means that while Teladoc has more than doubled this 2020, the stock is still expected to continue soaring thanks to its recent merger with Livongo.

Here’s a brief background of Livongo.

This company gathers data and sends reminders to its users suffering from chronic diseases to encourage them to implement lifestyle and even behavioral changes that would improve their health.

Prior to its cash-and-stock merger with Teladoc, Livongo was doubling its membership, particularly among diabetes patients.

This deal is anticipated to elevate virtual care and push Teladoc front and center of the $121 billion digital health market in the United States alone—a number that is projected to grow at a rate of 16.9% until 2025.

Needless to say, Teladoc has set itself up to control a huge part of that total value.

So far, the most notable competitors of Teladoc in this space are technology giants like Google (GOOG) via its parent company Alphabet (GOOGL) and Apple (AAPL).

With all the opportunities and even with the challenges of new competitors in the market, Teladoc remains the leader in this explosive digital health industry, making it extremely attractive for investors to ignore.

Looking at its risk-reward proposition, the company is clearly a solid growth pick.

After all, telemedicine offers a long-term win-win-win situation for everyone in the healthcare industry.

It is a win for doctors because they can see more patients.

It’s a win for patients because they get to see doctors with ease and convenience.

Finally, it is a win for insurance agencies because they generally pay lower bills for virtual visits.

Mad Hedge Technology Letter

October 21, 2020

Fiat Lux

Featured Trade:

(WILL ANTITRUST PROBLEMS UNLEASH GOOGLE?)

(GOOGL), (AMZN), (FB), (AAPL)

The Department of Justice and 11 U.S. states filing an antitrust lawsuit against Google isn’t as bad as it seems.

Abusing its monopoly power to make Google the default search service on browsers, mobile devices, computers, and other devices has meant quarter after quarter of cash cow growth.

Alphabet’s cash reserves are to the point where they can fritter away capital on loss-making divisions like autonomous driving technology Waymo.

Yes, it’s true that Google is no longer the scrappy start-up that they once were, but that doesn’t matter, and they certainly have the financial balance sheet to deal with any litigation that might or might not take place.

Part of the Google shares not selling off was validation that they are resourceful enough to get through this unscathed and they certainly have had years to prepare how to defend itself through the courts.

Google let their position known publicly by tweeting that the “lawsuit by the Department of Justice is deeply flawed. People use Google because they choose to — not because they're forced to or because they can't find alternatives.”

The standard corporate speak that Google uses is just a sign of the times where big tech has dwarfed the banks, is too big to fail and of pure clout in American government, business and society.

This has been a long time coming as the firm has been under investigation by the Justice Department, the Federal Trade Commission, and state attorney general that its search engine and digital advertising businesses may operate as illegal monopolies.

The specific lawsuit will likely reference competitors like Bing for denying them access to user data, as well as targeting Google’s “search advertising.”

It was only in July, Alphabet CEO Sundar Pichai, along with the CEOs of Amazon (AMZN), Apple (AAPL), and Facebook (FB) appeared before a hearing of the House Judiciary Committee’s Subcommittee and were made to look bad for their dominant position in the digital ad game.

Google has repeatedly pointed to earlier antitrust investigations by the FTC and state attorney general into its display search business that concluded in 2013 and 2014 without incident but they surely have known that this issue would pop back up time and time again.

The knock-on effects have been drastic with American innovation sapped of its incubatory juices.

In the modern age of tech, it’s almost impossible to build a unicorn from scratch without getting your business model hijacked from one of the anti-competitive tech firms.

And now — there are 6 tech firms that use their scale and power to drag down innovation.

The consequences have been higher share prices for big tech because if they can’t scare competition out of place, they will either buy them or find internal ways to sabotage their business ala Yelp.

Google’s digital advertising business has faced accusations due to its unrivaled size and volume which is also why it makes so much money.

The company controls some of the most important links in the online advertising chain, centrally its DoubleClick platform, a premier tool for online publishers, helping them to create, manage, and track online marketing campaigns.

This is why the “internet” or the companies that have access to tracking technology know everything about you and can front run the marketing process to cater towards you.

Acquired in 2007, DoubleClick was cited by Senator Elizabeth Warren (D-MA) as one of the major acquisitions Google should be forced to unwind to improve competition in the advertising space.

If DoubleClick were to unwind itself from Google, they would be an instant unicorn out of the gate.

And that isn’t just the only unicorn in the stable, there are many stand-alone unicorns in Google’s umbrella of assets — from Gmail, Google Cloud, Google Maps, YouTube, and even Google’s hardware division that manufactures phones such as the Google Pixel line.

I believe in the argument that the sum of the parts is dragging down each segment meaning once broken from the Alphabet death grip, each unicorn would be able to pursue decisions that are best suited for their own division and not just the parent company Alphabet.

There is only so long that each unicorn is willing to play for the team and once they go out into the wild, each will become its own unique growth company.

One possibility is Google’s search business spun out while the other businesses stay inside under parent company which is also viable since the investigations specifically pinpoint Google search.

Google search controls more than 90% of the world’s search traffic market share and most notably, Yelp complain about Google favoring its own products in search results.

In July, a Wall Street Journal investigation found Google’s search algorithm biased towards its own YouTube videos in search results over those of other services.

Google’s repeated abuses would likely be mitigated just by spinning out Google search and not allowing them to favor itself.

It is highly unlikely that a stand-alone Google search business would cede market share because they are simply the best search engine by a country mile.

They would most likely expand on the lead they already have.

In either case, if Google isn’t broken up, they win, and the share price will rise.

If they are broken up, the victory will be even more emphatic while supercharging each individual asset ending up in an even higher share price.

This could finally offer a jolt of innovation into the stagnant tech space which honestly has too many too-big-to-fail companies that are focused more on financial engineering at this point.

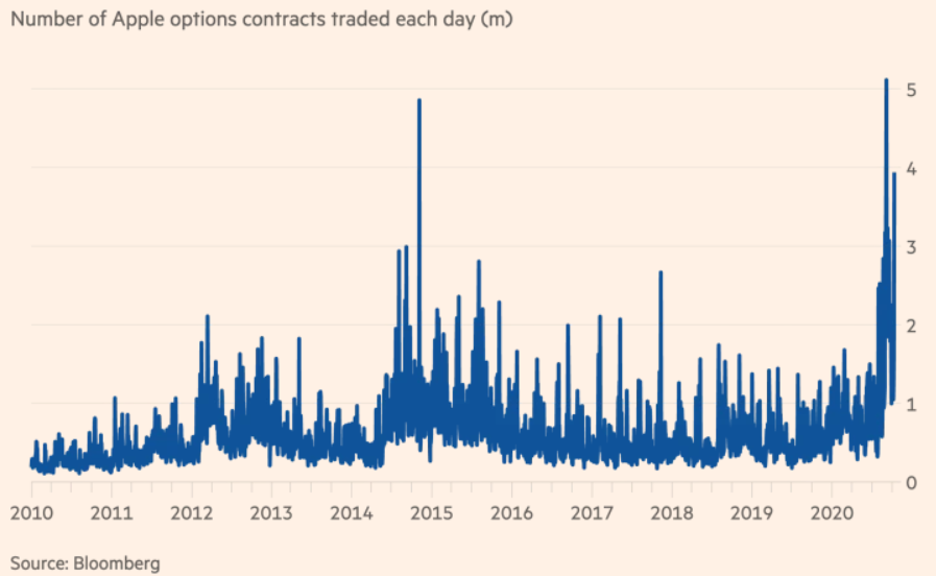

Mad Hedge Technology Letter

October 14, 2020

Fiat Lux

Featured Trade:

(TECH OPTION VOLUME UNHINGED)

($COMPQ), (APPL), (FB), (MSFT), (GOOGL), (NFLX)

The euphoria in big cap tech shares is the catalyst moving the Nasdaq index recently.

Call option activity is taking the top off of tech shares with usual low beta stocks surging over 5% in single trading sessions.

This unfortunately is causing our options trades to experience heightened stock volatility and the knock-on effect is our strikes getting blown out.

Some of the excess volatility comes down to traders making big bets in the run-up to the election.

Remember when Trump won in 2016, the market exploded higher when many “experts” guaranteed a massive sell-off would ensue.

In the short-term, the unsustainable pace of speculation in derivatives will translate into wild price swings. Monday brought the biggest rally for the Nasdaq 100 Index since April, but measures of volatility rallied as well.

One proxy for the froth still latent in options, the percentage of overall volume represented by single-stock contracts, remains up 19% from a year ago.

Most of the action is concentrated in mega cap technology and momentum-driven shares.

A consensus is coalescing around a few big buyers coming into the options market to corner it with rumors of purchases around $300 million worth of call contracts on tech stocks in a single day.

The Nasdaq 100 Index has gained in all but two sessions this month and just notched its best week since July after last month’s sharp drop.

Whipsawing markets are also possible when liquidity remains thin.

Trading in options showed itself capable of influencing share movement in August and September when dealer hedging (demand from people who sell options for the underlying stock) created feedback loops that helped drive the Nasdaq higher.

That dynamic can also make sell-offs worse than they should be as well as sellers adjust positions.

Big trades in thin markets, especially in technology or momentum trades considered overbought or oversold, increase the potential for exacerbated stock moves as dealers hedge exposure.

Call open interest in Facebook (FB), Amazon (AMZN), Netflix (NFLX), Alphabet (GOOGL), Apple (APPL) and Microsoft (MSFT) has averaged 12.8 million contracts over the 30 days through Friday, the highest since early 2019.

The tech-heavy Nasdaq index has gyrated an average of 1.8% per day since the beginning of September, while the broader market gauge has fluctuated by 1.2% over that time period.

Recent options activity has been momentum-based, meaning that stocks tend to attract more interest in calls when it’s rallying versus when it trades lower.

Throw in structural forces that are contributing to a sustained high implied volatility environment, and election hedgers have their work cut out for them.

There are fewer short-volatility players as well in the wake of the health crisis.

There’s also less volatility selling by retail investors after the delisting of some popular VIX products earlier this year like the volatility ETF ticker symbol XIV.

It could take a few years for the imbalances to work itself through the system.

Then there’s the resurfacing of an event similar to the “Nasdaq whale” which is reported as Softbank acting like a hedge fund and buying as many big tech call options they could afford.

Softbank CEO has essentially turned his failed hedge fund named the Vision Fund from a start-up investor into a speculative hedge fund in risky option contracts solely betting on the rise of Silicon Valley tech in the age of the coronavirus.

After being burnt by Uber and WeWork, he finally decided to stay out of the messy acquisitions/seed funding and just speculative through derivatives from Tokyo.

The avalanche of options volume will no doubt cause the tech markets to become jittery and it certainly puts a floor under tech implied volatility for a while.

Retail investors have taken notice of this insane volume and largely stayed on the sideline.

At the apex of the madness, retail traders spent more than $511 billion in notional value on call options and that figure was slashed to $343 billion in the first week of October.

Retail traders tend to buy less-expensive short-dated contracts which tend to have greater convexity and ability to exacerbate share movements.

The level of risk-taking occurring in the public markets is at an all-time high.

Just look at America’s most elite university endowments who have slashed their exposure to the stock markets to the lowest levels since before the crash of 1929. And now they’re betting the ranch on secretive, illiquid, and high-risk private-equity funds and hedge funds.

A US teachers’ pension fund has sued Allianz Global Investors, accusing one of the world’s biggest asset managers of employing a “reckless strategy” that cost retirees almost $800m during this year’s market turmoil.

This is just one example of the high-risk strategies taking place with pension money.

In a lawsuit filed on Monday in New York, the Arkansas Teacher Retirement System claims that Alpha Funds, investment vehicles marketed by AllianzGI, had placed bets against an escalation of market volatility in an effort to recover losses they incurred from the same strategy in February.

So here we stand with derivative trading in tech options and general equity strategies leveraged to the hills that are betting on the system not breaking, or at least not breaking yet.

Even if the system reaches breaking point, many of these private investors are betting on governments to come rescue them perpetuating the feedback loop and offers a conundrum to savvy asset managers to miss or partake in the gaps up themselves.