Mad Hedge Technology Letter

July 1, 2020

Fiat Lux

Featured Trade:

(HOW THE “SPLINTERNET” IS TAKING OVER)

(TIKTOK), (FB), (GOOGL), (TWTR), (AMZN)

Mad Hedge Technology Letter

July 1, 2020

Fiat Lux

Featured Trade:

(HOW THE “SPLINTERNET” IS TAKING OVER)

(TIKTOK), (FB), (GOOGL), (TWTR), (AMZN)

The balkanization of the internet is spiking in the short-term, knocking off the value of multiple Fortune 500 companies in one fell swoop.

In technology terms, this is frequently referred to as “splinternet.”

A quick explanation for the novices can be summed up by saying the splinternet is the fragmenting of the Internet, causing it to divide due to powerful forces such as technology, commerce, politics, nationalism, religion, and interests.

What investors are seeing now is a hard fork of the global tech game into a multi-pronged world of conflicting tech assets sparring for their own digital territory.

The epicenter of balkanization is now heart and center in West Asia polarizing the Indian and Chinese tech economy after a skirmish along the shared border.

This is fast becoming a winner-take-all affair.

India had to do something after 20 dead Indian soldiers felled by the Chinese Army stoked a wave of national outcry against regional rival China.

The backlash was swift with the Indian government banning 59 premium apps developed by China citing “national security and defense.”

The ban includes the short-form video platform TikTok, which counts India as its biggest overseas market.

TikTok was projected to easily breeze past 300 million Indian users by the end of 2020 and was clearly hardest hit out of all the apps.

India is the second biggest base of global internet users with nearly half of its 1.3 billion population online.

The government rolled out the typical national security playbook saying that the stockpiling of local Indian data in Chinese servers undermines national security.

The ruling will impact roughly one in three smartphone users in India. TikTok, Club Factory, and UC Browser and other apps in aggregate tally more than 500 million monthly active users in May 2020.

Highlighting the magnitude of this purge - 27 of these 59 apps were among the top 1,000 Android apps in India last month.

China dove headfirst into the Indian market with their smartphones, apps, and an array of hardware equipment. Now, that is all on hold and looks like a terrible mistake.

Chinese smartphone makers command more than 80% of the smartphone market in India, which is the world’s second largest.

One of the reasons Apple (AAPL) could never make any headway in China is because they were constantly undercut by predatory Chinese phone makers with stolen technology.

TikTok is also being eyed-up for bans in Europe and the United States recently as it constantly curries to Beijing’s every whim by banning content unfavorable to the Chinese communist party and rerouting data back to servers in China.

I am surprised it hasn’t happened yet with an abundant phalanx of Chinese hawks in the conservative administration.

To be fair, China has rolled out the same playbook before when the state spews out nationalist narratives triggering local furor that resulted in bashing Japanese-made cars or shuttering Korean supermarket.

Chinese tech is clearly the main loser for their government’s “distract its own people at all costs” campaign to shield themselves from the epic contagion of the lingering pandemic.

What does this mean for American tech?

For one, India will strengthen ties with the U.S., being the biggest democracy in Asia, meaning a massive foreign policy loss and loss of face for the Chinese communist regime.

The resulting losses for Chinese tech will usher in a new generation of local Indian tech with Silicon Valley being the next in line playing the role of a wingman.

Even though the U.S. avoided the carnage from this round of balkanization, the situation in Europe is tenuous, to say the least.

Fault lines will compound the problem of a multinational tech revenue machine and the relationship with France is on the verge of becoming fractious.

I believe if the relationship worsens with the Europeans - France, Germany, and Britain could ban big tech companies like Facebook (FB), Twitter (TWTR), Google (GOOGL).

This would be a massive blow to not only revenue streams but also global prestige for American tech.

The U.S. is still licking its wounds after the EU announced a travel ban on American tourists who hoped to re-enter the Schengen Zone on its reopening on July 1st.

Not only do Silicon Valley leaders see a murky future outside its borders, but digital territories are also getting carved out as we speak domestically.

Amazon (AMZN)-owned Twitch and Twitter have clamped down on U.S. President Donald Trump’s account.

This could quickly spiral into a left-versus-right war in which there are competing apps for different political beliefs and for every subgenre of apps.

This would effectively mean a balkanization of tech assets within U.S. borders and division is the last thing Silicon Valley wants.

Silicon Valley wants products sold to the largest addressable market possible.

The balkanization of the internet is now turning into an equally high risk as the antitrust and regulatory issues.

The issues keep piling up, but nothing has been able to topple big tech yet as they lead the broader market out of the pandemic.

The key point to understand is that these are growing risks until they blow up in front of your eyes and become the next black swan like Covid-19.

Let’s hope that never happens.

Mad Hedge Technology Letter

June 15, 2020

Fiat Lux

Featured Trade:

(DON’T TAKE YOUR EYES OFF BIG TECH SHARES),

(GOOGL), (AAPL), (MSFT), (NFLX), (FB), (AMZN), (IBM), (CSCO)

There is literally no possible scenario in a post-second-wave lockdown where the 7 tech stocks of Facebook, Google, Apple, Microsoft, Netflix, Facebook, and Amazon don’t shoot the lights out unless the world ceases to exist.

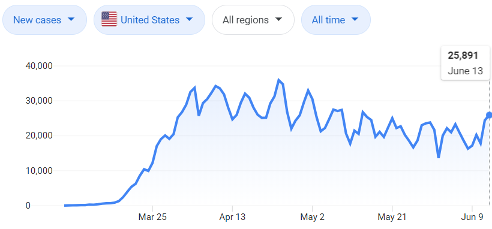

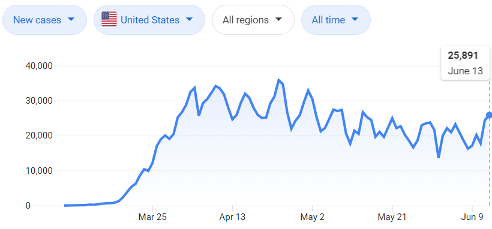

25,891 – that is the number of new coronavirus cases registered in the U.S. on June 13th, 2020 which is about in line with the recent near-term peaks of total daily U.S. coronavirus cases.

Why is this important?

Traders are calculating whether a “second wave” will possibly rear its ugly head to crush the frothy momentum in tech stocks.

That is where we are at now in the tech market.

Tech stocks could possibly ride another magnificent ride up in share appreciation if the reopening of the economy can kick into second gear.

Skeptics are sounding the alarms that this is not even the “second wave” and we still in the latter half of the first wave.

Consensus has it that this could be just a head fake.

The jitters are real with recent dive in tech shares.

The five biggest tech companies burned more than $269 billion in value last Thursday - the worst day for U.S. stocks since March and the 25th worst day in stock market history.

Nasdaq stocks ended the day largely 5% in the red with Microsoft shedding $80 billion in market cap in just one day.

Larger drops were led by IBM who lost 9% and Cisco who lost 8%.

It was a dreadful day at the office, to say the least.

We are teetering on a knife's edge and the tension is running high in the White House with Treasury Secretary Steven Mnuchin already announcing that the U.S. can’t afford another lockdown.

It’s not up to him in the end, it’s about how consumers will assess the confronted health risks.

Tech will undoubtedly be dragged down with the rest on the next lockdown sparing few survivors.

The housing market might actually go down as well as the initial push to the suburbs will dissipate and fresh forbearances will explode higher.

Consumers might not even have the cash to pay for their monthly Apple phone service or internet bill if the worst-case scenario manifests itself.

The health scare has already dented new software purchases by small and medium businesses (SMBs) and tech companies in industries such as travel, retail, and hospitality; online ad spending by the likes of automakers and online travel agencies; and smartphone, automotive and industrial chip purchases.

Small business has held off on reducing their tech software spending too much on the expectation that macro conditions will perform a V-shaped recovery.

Numerous tech firms have cited “demand stabilization,” but it’s not guaranteed to last if we revert to another lockdown.

If a lockdown happens again, it will be another referendum on Fed’s enormous liquidity impulses versus the drop in real earnings or flat out losses to tech business models.

Even with the media’s onslaught of vicious fearmongering campaigns, I do believe this is the time for long-term investors to scale into the best of tech such as Amazon, Apple, Google, Microsoft, Facebook, Netflix.

If you thought these 7 companies had anti-trust issues before, then look away.

We could gradually head into an economy where up to 40% of the public markets comprise of only 7 tech stocks which is at a mind-boggling 25% now.

Never waste a good crisis – tech is following through like no other sector!

Bonds don’t make money anymore and hiding out now means putting your life savings into these 7 premium tech stocks.

In the short-term, this is a good opportunity for a tactical bullish tech trade.

Mad Hedge Technology Letter

June 5, 2020

Fiat Lux

Featured Trade:

(EUROPE’S BIG TECH TAX GRAB),

(COMPQ), (NFLX), (APPL), (AMZN), (GOOGL), (MSFT)

Big Tech regulation gets the protection of the U.S. government.

The U.S. government has announced that it is looking into aggressive regulation originating from foreign countries that would die to have a FANG themselves.

This is just another salient data point to which tech will lead us through the maze of complexity that the world now finds itself in.

Many jumped on the bandwagon saying it was a matter of time before regulation destroys big tech, but I will argue that big tech has become too big to fail and the value generated from stock appreciation and tax revenue has become even more important.

Tech has been the only industry to not get pummeled by the coronavirus and the ramifications of social unrest.

The U.S. government doesn’t want to tip over the last remaining pillar the U.S. economy is clinging to, they are desperate to allow the U.S. tech models to stay intact.

The Federal and State budgets have massive holes in them and crushing tech’s contribution to the revenue coffers would be political suicide.

Understanding how the administration cherishes big tech means viewing them through the prism of how other countries treat U.S. tech companies hoping to take a piece of the pie themselves through clever “regulation.”

The European Union, the Czech Republic, and the U.K. plan to siphon off tax revenue from big tech even though confronted by possible trade sanctions from the U.S.

The U.S. probe also will look into the digital services tax plans of Austria, Brazil, Indonesia, Italy, Spain, and Turkey because they are all looking to skim some cash off of big tech’s cash cow.

To read more about the tax fiasco, please click here.

Europe and the emerging economies have been hit harder than the U.S., not in terms of deaths, but in relative economic terms because they don’t possess the rolodex of Fortune 500 companies that can just issue more corporate debt or a Fed central bank that is delivering trillions in liquidity that has saved the stock market.

Washington has specifically been eying up France for a section 301 investigation after it became the first country to fully implement a digital sales tax in July 2019.

France has been quite aggressive in calling out big tech for undermining and exploiting their economy by not paying tax due.

French Finance Minister Bruno Le Maire has been sharp-tongued criticizing America’s big tech companies for running wild in European markets.

A 3% digital sales tax was in the cards before the U.S. slapped on a counter tariff to French goods which delayed the frosty confrontation.

Europe’s vast network of splintered resources and unbalanced innovation combined with Europe’s infamous avalanche of bureaucracy meant that developing a famous tech company fell through the cracks.

Nothing even remotely close to Silicon Valley was ever conjured up inside the confines of the European Union.

The consequences have been costly with most Europeans relying on Apple cell phones, Google software, Netflix subscriptions, and Microsoft enterprise products to get them through the day just like most Americans.

The tax grab is out of desperation as the EU confronts a post-coronavirus world where they are increasingly controlled by decisions from the Communist Chinese and subject to a graying population that delivers a reduced tax revenue base.

The European Union is one of the biggest losers from the coronavirus.

The hands-off warning by the U.S. government on its own big tech companies puts a premium on their existence to the U.S. economy.

Instead of twisting their arm to squeeze every extra tax dollar out of them, they will most likely get more access to deliver the services most Americans are hooked on.

It’s not a secret that current U.S. President Donald Trump is hellbent on destroying big tech but there is no way to do it without destroying the U.S. economy and the U.S. stock market.

At this point, just a handful of tech companies comprises over 22% of the S&P and this will most likely continue as other industries are still licking their wounds with some analysts believing it will take 10 years to get back to late 2019 economic levels.

The most likely scenario for big tech is that the array of crises has delayed real regulation indefinitely and the U.S. will protect big tech from a tax grab abroad.

The best-case scenario is zero regulation leading to zero extra costs.

Either way, stock appreciation is in the cards for tech’s future.

The end result is that big tech could eventually comprise up to 30% of the S&P in the next 3 years which dovetails nicely with a recent analyst call that Microsoft will hit over $2 trillion in market capitalization in the next 2 years.

Mad Hedge Technology Letter

June 3, 2020

Fiat Lux

Featured Trade:

(ABOUT YOUR RIOT-PROOF PORTFOLIO),

(COMPQ), (WMT), (APPL), (AMZN), (TGT), (JWN), (EQIX), (GOOGL), (MSFT)

Social unrest will have NO material effect on tech shares moving forward.

Some investors expected the Nasdaq (COMPQ) index to roll over big time, throttled by a national insurrection. Anti-police-violence protests, some becoming riots, have broken out in more than 60 cities.

However, it appears to be another false negative for the Nasdaq as it motors upwards acting on the momentum of outperformance during the coronavirus.

One thing that the coronavirus pandemic, as well as protests, have taught investors is the unwavering faith in technology’s strength will continue powering the overall market rebound.

Any social unrest will not stop tech shares because they simply don’t subtract from their revenue models.

This will perpetuate into the rest of 2020 and beyond.

Much of the public reaction from big tech has been paying some form of lip service about the national situation being untenable followed up with a small donation.

Apple (AAPL) says it's making donations to various groups including the Equal Justice Initiative, a non-profit organization based in Montgomery, Alabama that provides legal representation to marginalized communities.

To read more about big tech’s donations, click here.

Aside from some PR formalities, it will be business as usual after things settle down.

Apple might suffer some slight inconveniences of having some stores looted, but that doesn’t mean consumers can’t buy products online.

Tech companies simply contort to fit the new paradigm and that is what they are best at doing.

Apple has charged hard into the digital service as a subscription world that has served Amazon, Apple, Google (GOOGL), and Microsoft (MSFT) so well.

To read more about the robust performance of software stocks, please click here.

Many of these tech companies don’t need a physical presence to drive forward earnings, revenue models, and widen their competitive advantages.

That’s the beauty of it and their brands are so entrenched that it doesn’t matter what happens in the outside world at this point.

It’s true that a few tech companies might have to scale back or modify operations until the storm subsides but not at a great scale that will worry investors.

Amazon is reducing deliveries and changing delivery routes in some areas affected by the protests.

Big tech dodged a bullet with the majority of the financial burden falling on the shoulders of big-box retailers like Walmart (WMT) and Target (TGT) and city center-located businesses.

Walmart closed hundreds of stores one hour early on Sunday, but most are slated to reopen. Nordstrom (JWN) temporarily closed all its stores on Sunday.

Amazon (AMZN)-owned Whole Foods are often located in neighborhoods that are perceived likely to escape the bulk of the turmoil.

The events of the last few days will have significant side effects on the normalcy of society or the new normal of it.

Combined with the pandemic, consumers will opt for more spacious housing options in less concentrated areas of the U.S.

The social unrest once again delivers the goodies into the hands of e-commerce as people will be less inclined to leave their house to consume.

A stock that really sticks out during all of this is the leader in interconnected data centers Equinix (EQIX) because of the explosion of data being consumed from the stay-at-home revolution.

Sadly, the price of tech share does not account for life quality which is part of the reason we see stocks lurching higher.

By the time all the different crises, including coronavirus and protests, are snuffed out, we could be in a world where the only strong companies left are technology, "big tech".

They have an insurmountable lead at this point with guns still blazing.

When you add the windfall of trillions in cash the Fed has pumped out and unwittingly diverted into tech shares recently, it is hard to envision ANY scenario in which the Nasdaq will be down a year from now.

I am bullish on the Nasdaq index and even more bullish on big tech.

Even the supposed “rotation” to value has only meant that tech shares haven’t gone down.

A dip now in tech shares means shares dip for two hours before resurging.

Why would anyone want to sell the best and highest growth industry in the public markets with unlimited revenue-generating potential?

Global Market Comments

May 26, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LOOKING FOR THE NEW AMERICA),

(FB), (AAPL), (NFLX), (GOOGL), (MSFT), (TSLA), (VIX)

We are getting some tantalizing tastes of the new America that will soon arise from the wreckage of the pandemic.

Companies are evolving their business models at an astonishing rate, digitizing what’s left and abandoning the rest, and taking a meat cleaver to costs.

The corporate America that makes it through to the other side of the Great Depression will earn far more money on far fewer sales. That has been the pattern of every recession for the past 100 years.

While the pandemic may take earnings down from $162 per S&P 500 share in 2019 to only $50 in 2020, it sets up a run at a staggering $500 a share during the coming Roaring Twenties and Golden Age. All surprises will be to the upside and anything you touch will make you look like a genius.

For example, Target’s online sales have exploded 153%, allowing customers to order their groceries online and pick them up at curbside. (TGT) pulled this off in a mere three weeks. Without a pandemic, it would have taken three years to implement such a radical idea, if ever.

Survival is a great motivator.

The (SPY) has been greatly exaggerating the public’s understanding of the stock market. Five FANGs and Tesla (TSLA) with 50%-200% moves off the bottom have made the index look irrationally strong.

The fact is that the majority who have shares have not even made a 50% retracement of this year’s losses. A lot of stocks, especially the reopening ones, are still crawling back of subterranean bottoms.

Investors now have the choice of chasing wildly expensive stocks that have already had spectacular runs, or cheap ones that will go bankrupt by the end of the year. It is a Hobson’s choice for the ages. I expect 10% of the S&P 500 to go under by the end of 2020.

I am spending a lot of time on the ground talking to businesses in California and Nevada and have come to two conclusions. They cannot fathom the true depth of the Depression we are now in and are greatly underestimating the length of time it may take to recover. We may not see the headline unemployment rate under 10% for years unless the government redefines the statistics, which they always do.

The S&P 500 is not the economy. It only employs 25% of America’s private sector labor force accounting for 20% of its total costs. Real estate accounts for another 15%. That leaves 35% of costs that can be completely eliminated or reengineered. This creates enormous share price upside possibilities.

The concentration of the market is the most extreme I have ever seen, with five stocks getting most of the action, (FB), (AAPL), (NFLX), (GOOGL), and (MSFT).

There is a staggering $3.6 trillion in equity allocations sitting on the sidelines in cash. All those who got out at the March bottom are now desperately trying to get back in at the May top. Algorithms are making sure you get out cheap and get back expensive.

It will all end in tears.

One of the stunning developments of the crash has been the near doubling of retail stock trading. Options trading has increased even more. Millions of stimulus check recipients have poured their newfound wealth into the stock market instead of spending it on consumer goods, like they were supposed to.

This explains the over-concentration on the five FANG stocks, (FB), (AAPL), (NFLX), (GOOGL), and (MSFT), the greatest momentum stocks are out age, but in high speculative ones like Tesla (TSLA). The lowest cost online platforms like Robin Hood (click here).

All of this is completely irrevocably changing the character of the stock market, perhaps permanently. This may also explain why the Volatility Index remains stuck above$26.

Fed Governor Jerome Powell said no recovery without vaccine, and that’s without a second wave. It could be a long wait. In the meantime, the Atlanta Fed said Q2 US GDP will be down -42%, the weakest quarter in American history. We find out mid-July.

Housing Starts collapsed by 30.2% in April, in the sharpest drop on record. But prices aren’t falling. There is still a massive bid under the market from still-employed millennials. Your home could be you best performing asset this year. The 30-year fixed rate mortgage at 3.0% is a big help.

Weekly Jobless Claims topped 2.4 million, taking the two-month total to a breathtaking 39 million. One out of four Americans is now unemployed, matching the Great Depression peak. US deaths just topped 98,000, 21 times China’s fatality rate where the disease originated and with four times our population. People will keep losing jobs until the death rate peaks, which could be many months, or years.

Leading Economic Indicators crashed by 4.4% for April, showing the economy is still in free fall. So, how much more stock do you want to buy here?

Up to 60% of mall tenants aren’t paying rent, with $7.4 billion skipped in April alone. See my earlier “Death of the Mall” piece. It’s another harsh example of the epidemic accelerating all existing trends.

The market is not reflecting the long-term damage to the economy, says my old buddy and Morgan Stanley colleague David Gerstenhaber. When the bailouts run out, the economy could go into free fall. It could take years to get below 10% unemployment rate again, as many of the layoffs and furloughs are permanent. Keep positions small. Anything could happen. I spent the 1987 crash with David.

Existing Home Sales cratered an incredible 17.8% in April to an annualized 4.88 million units, the largest one-month drop since 2010. Inventory dropped to an all-time low of only 1.7 million, down 19.7%, presenting a 4.1-month supply. Sellers failed to list and those who had a home took them off. Unbelievably, this pushed median home prices to a new all-time high of 286,000, up 7.4% YOY. The biggest sales fall in the west, where the US epidemic started.

China took over Hong Kong, suspending most civil liberties in response to Trump’s multiple attacks. And you know what? There is nothing we can do about it that hasn’t already been done. Talk about going into battle with no dry powder. I’m sure the US 7th Fleet will be out there soon to provoke an attack. Anything to distract attention from the 100,000 Americans who died from Covid-19 on Trump’s watch. As if markets didn’t already have enough to worry about.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

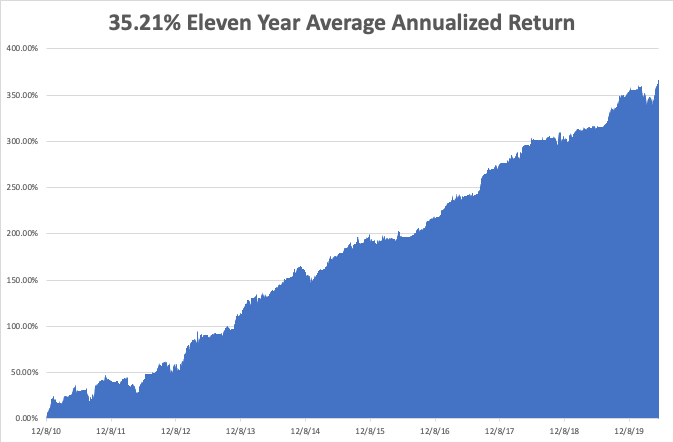

My Global Trading Dispatch performance had another fabulous week, up an awesome +4.97%, and blasting us up to a new eleven-year all-time high of 77%. It has been one of the most heroic performance comebacks of all time.

My aggressive short bond positions really delivered some nice profits, despite the fact the bond market went almost nowhere. That’s because time decay for the June 19 expiration is really starting to kick in. I also got away with a small long in the bond market for the second time in two weeks.

That takes my 2020 YTD return up to +10.86%. That compares to a loss for the Dow Average of -12.6%. My trailing one-year return exploded to 50.85%, nearly an all-time high. My eleven-year average annualized profit exploded to +35.21%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here at https://coronavirus.jhu.edu.

On Monday, May 25, I’ll be leading the neighborhood veterans parade for Memorial Day. Markets are closed.

On Tuesday, May 26 at 9:00 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, May 27, at 4:30 PM, weekly EIA Crude Oil Stocks are published.

On Thursday, May 28 at 8:30 AM, Weekly Jobless Claims are announced. We also get the second estimate for the Q1 GDP is printed. At 10:00 AM, April Pending Home Sales are announced.

On Friday, May 29, at 2:00 PM, the Baker Hughes Rig Count follows at 2:00 PM.

As for me, I will be hitting the town beaches at Lake Tahoe for the first time this spring, mask in hand, where waitresses serve you mixed drinks on order. Outdoors will be the only safe place this year.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader