Global Market Comments

April 9, 2020

Fiat Lux

Featured Trade:

(TEN LONG TERM LEAPS TO BUY AT THE BOTTOM)

(MSFT), (AAPL), (GOOGL), (QCOM), (AMZN),

(V), (AXP), (NVDA), (DIS), (TGT)

Global Market Comments

April 9, 2020

Fiat Lux

Featured Trade:

(TEN LONG TERM LEAPS TO BUY AT THE BOTTOM)

(MSFT), (AAPL), (GOOGL), (QCOM), (AMZN),

(V), (AXP), (NVDA), (DIS), (TGT)

I am often asked how professional hedge fund traders invest their personal money. They all do the exact same thing. They wait for a market crash like we are seeing now, and buy the longest-term LEAPS (Long Term Equity Participation Securities) possible for their favorite names.

The reasons are very simple. The risk on LEAPS is limited. You can’t lose any more than you put in. At the same time, they permit enormous amounts of leverage.

Two years out, the longest maturity available for most LEAPS, allows plenty of time for the world and the markets to get back on an even keel. Recessions, pandemics, hurricanes, oil shocks, interest rate spikes, and political instability all go away within two years and pave the way for dramatic stock market recoveries.

You just put them away and forget about them. Wake me up when it is 2022.

I put together this portfolio using the following parameters. I set the strike prices just short of the all-time highs set two weeks ago. I went for the maximum maturity. I used today’s prices. And of course, I picked the names that have the best long-term outlooks.

You should only buy LEAPS of the best quality companies with the rosiest growth prospects and rock-solid balance sheets to be certain they will still be around in two years. I’m talking about picking up Cadillacs, Rolls Royces, and even Ferraris at fire sale prices. Don’t waste your money on speculative low-quality stocks that may never come back.

If you buy LEAPS at these prices and the stocks all go to new highs, then you should earn an average 131.8% profit from an average stock price increase of only 17.6%.

That is a staggering return 7.7 times greater than the underlying stock gain. And let’s face it. None of the companies below are going to zero, ever. Now you know why hedge fund traders only employ this strategy.

There is a smarter way to execute this portfolio. Put in throw-away crash bids at levels so low they will only get executed on the next cataclysmic 1,000-point down day in the Dow Average.

You can play around with the strike prices all you want. Going farther out of the money increases your returns, but raises your risk as well. Going closer to the money reduces risk and returns, but the gains are still a multiple of the underlying stock.

Buying when everyone else is throwing up on their shoes is always the best policy. That way, your return will rise to ten times the move in the underlying stock.

If you are unable or unwilling to trade options, then you will do well buying the underlying shares outright. I expect the list below to rise by 50% or more over the next two years.

Enjoy.

Microsoft (MSFT) - March 18 2022 $180-$190 bull call spread at $2.67 delivers a 274% gain with the stock at $190, up 16% from the current level. As the global move online vastly accelerates the world is clamoring for more computers and laptops, 90% of which run Microsoft’s Windows operating system. The company’s new cloud present with Azure will also be a big beneficiary.

Apple (AAPL) – June 17 2022 $210-$220 bull call spread at $6.47 delivers a 55% gain with the stock at $226, up 14% from the current level. With most of the world’s Apple stores now closed, sales are cratering. That will translate into an explosion of new sales in the second half when they reopen. The company’s online services business is also exploding.

Alphabet (GOOGL) – January 21 2022 $1,500-$1,520 bull call spread at $7.80 delivers a 28% gain with the stock at $226, up 14% from the current level. Global online searches are up 30% to 300%, depending on the country. While advertising revenues are flagging now, they will come roaring back

QUALCOMM (QCOM) – January 21 2022 $90-$95 bull call spread at $1.55 delivers a 222% gain with the stock at $95, up 23% from the current level. We are on the cusp of a global 5G rollout and almost every cell phone in the world is going to have to use one of QUALCOMM’s proprietary chips.

Amazon (AMZN) – January 21 2022 $2,100-$2,150 bull call spread at $17.92 delivers a 179% gain with the stock at $2,150, up 15% from the current level. If you thought Amazon was taking over the world before, they have just been given a turbocharger. Much of the new online business is never going back to brick and mortar.

Visa (V) – June 17 2022 $205-$215 bull call spread at $3.75 delivers a 166% gain with the stock at $215, up 16% from the current level. Sales are down for the short term but will benefit enormously from the mass online migration of new business only. They are one of a monopoly of three.

American Express (AXP) – June 17 2022 $130-$135 bull call spread at $1.87 delivers a 167% gain with the stock at $135, up 28% from the current level. This is another one of the three credit card processors in the monopoly, except they get to charge much higher fees.

NVIDIA (NVDA) – September 16 2022 $290-$310 bull call spread at $6.90 delivers a 189% gain with the stock at $310, up 19% from the current level. They are the world’s leader in graphics card design and manufacturing used on high-end PCs, artificial intelligence, and gaining. They befit from the soaring demand for new computers and the coming shortage of chips everywhere.

Walt Disney (DIS) – January 21 2022 $140-$150 bull call spread at $2.55 delivers a 55% gain with the stock at $116, up 31% from the current level. How would you like to be in the theme park, hotel, and cruise line business right now? It’s in the price. Its growing Disney Plus streaming service will make (DIS) the next Netflix.

Target (TGT) – June 17 2022 $125-$130 bull call spread at $1.40 delivers a 257% gain with the stock at $130, up 16% from the current level. Some store sales are up 50% month on month and lines are running around the block. Their recent online growth is also saving their bacon.

Mad Hedge Technology Letter

March 27, 2020

Fiat Lux

Featured Trade:

(THE COMING AD HIT FOR GOOGLE AND FACEBOOK)

(FB), (GOOGL), (TWTR), (SNAP)

Expect lower revenues from Facebook (FB) and Google (GOOGL) because ad revenue has taken a hit.

It makes no sense to spend ad money on Facebook and Google ads for restaurants and hotels during times like this and that’s if they even still exist today.

The accumulative effect of the bankruptcies in other parts of the economy will shrink Google and Facebook’s ad dollar coffers.

The two internet giants together could see more than $44 billion in worldwide ad revenue evaporate in 2020, but that doesn’t mean these companies won’t be profitable.

For 2020, Google's total net revenue is now projected to be about $127.5 billion, down $28.6 billion for the year.

Facebook’s management said there was “a weakening in the ads business in countries taking aggressive actions to reduce the spread of COVID-19.”

Facebook’s overall usage has increased during the pandemic, with data up more than 50% over the last month in countries hit hardest by the virus, but the spike in volume isn’t in a form in which they can monetize it.

In 2021, Facebook’s advertising business is projected to recover growing 23% year-over-year to $83 billion.

I now expect Google to generate $54.3 billion in operating income (43% adjusted EBITDA margin) and Facebook will make $33.7 billion (49% margin), in 2020.

Digital platforms have felt the abrupt halt in spending, given the relative ease of stopping ad spend.

Secondary ad companies are also performing worse than expected with forecasted revenue for Twitter (TWTR) down by 18% (to expected revenue of $3.2 billion) while Snap (SNAP) ad revenue is expected at $1.66 billion, 30% lower.

Amazon’s ad business boasts a fortified moat because their revenue comes from product searches and those have experienced a surge in demand because of the coronavirus.

Facebook-owned WhatsApp has increased by 50% and that number is up 70% in Italy as the Italians go through a severe outbreak and lockdown.

Another side effect from the virus is the reduction of video streaming quality to ease the strain on internet networks, as YouTube and Netflix (NFLX) have also done.

Facebook is monitoring usage patterns in order to make the system more efficient, and add further capacity as required.

To help ameliorate potential network congestion, they temporarily reduced bit rates for videos on Facebook and Instagram in certain regions.

Facebook is conducting tests and further preparing to respond to any problems that might arise with network services.

Facebook and Google’s weakness proves that even the largest of Silicon Valley tech companies are battling with revenue restructuring while waiting for the U.S. economy to open up.

Although this is terrible news for Facebook and Google, the Nasdaq index is in the process of bottoming out.

The 3.28 million U.S. jobless claims were unprecedented but could very well represent a flushing out of the horrible news as the Nasdaq index spiked by 4% intraday.

Tech shares have had this job claim number baked into the share price for quite a while and we knew it was going to drop like an atomic bomb.

Some estimates had 4 million unemployed and the pain on main street is real, just search on Twitter – hashtag #lostmyjob.

The anecdotes stream down about individuals coming to grips with a sudden sacking and new reality of zero income.

This is just the first phase of job removals and the silver lining is that tech companies largely avoided the worst of the firings partly because many tech jobs can be moved remotely unlike many hospitality jobs.

The other silver lining is that the health scare is supercharging the digital ecosystem as society has effectively been moved online.

Any short-term weakness in tech companies will only be brief as tech stock will lead the recovery as the economy starts to open up again and the record amount of fiscal stimulus breathes life into hobbled companies.

Tech investors should prepare to pull the trigger.

I almost got to take a shower today.

However, whenever I got close to the bathroom, I'd get an urgent call from a concierge member, Marine buddy, Morgan Stanley retiree, fraternity brother from 50 years ago, or one of my kids asking me which stocks to buy at the bottom.

It’s been that kind of market.

I refer them to the research piece I sent out last week, “Ten Long Term LEAPs to Buy at the Bottom” for a quick and dirty way to get into the best names in a hurry (click here for the link).

I have been doing the same, and as a result, I have one of the largest trading portfolios in recent memory. When the Volatility Index is above $50, it is almost impossible to lose money as long as you remember to buy the 1,000 dips and sell the 1,000 point rallies.

In the run-up to every options expiration, which is the third Friday of every month, there is a possibility that any short options positions you have may get assigned or called away.

If that happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position. Whenever you have sold short an option, you run an assignment risk.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker saying that your call options have been assigned away. I’ll use the example of the Microsoft (MSFT) December 2019 $134-$137 in-the-money vertical BULL CALL spread.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point 8 days before the December 20 expiration date. In other words, what you bought for $4.50 last week is now with $5.00!

All have to do is call your broker and instruct them to exercise your long position in your (MSFT) December 134 calls to close out your short position in the (MSFT) December $137 calls.

This is a perfectly hedged position, with both options having the same expiration date, the same amount of contracts in the same stock, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

To say it another way, you bought the (MSFT) at $134 and sold it at $137, paid $2.60 for the right to do so, so your profit is 40 cents, or ($0.40 X 100 shares X 38 contracts) = $1,520. Not bad for an 18-day limited risk play.

Sounds like a good trade to me.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (MSFT) position after the close, and exercising his long December $134 call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it. They’ll tell you to take delivery of your long stock and then most additional margin to cover the risk.

Either that, or you can just sell your shares on the following Monday and take on a ton of risk over the weekend. This generates a ton of commission for the brokers but impoverishes you.

There may not even be and evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. It doesn’t pay. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many legal ways to steal money that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Global Market Comments

March 4, 2020

Fiat Lux

Featured Trade:

(TEN LONG TERM LEAPS TO BUY AT THE BOTTOM)

(MSFT), (AAPL), (GOOGL), (QCOM), (AMZN),

(V), (AXP), (NVDA), (DIS), (TGT)

Global Market Comments

March 3, 2020

Fiat Lux

Featured Trade:

(TEN STOCKS TO BUY BEFORE YOU DIE)

(MSFT), (AAPL), (GOOGL), (QCOM), (AMZN),

(V), (AXP), (NVDA), (DIS), (TGT)

A better headline for this piece might have been “Ten stocks to Buy at the Bottom”.

At long last, we have a once-a-decade entry point for the ten best stock in America at bargain basement prices.

Coming in here and betting the ranch is now a no-lose trade. If I’m right, the pandemic ends in three months, stocks will soar. If I’m wrong and the global epidemic explodes from here, you’ll be dead anyway and won’t care that the stock market crashed further.

Needless to say, I have a heavy tech orientation with this list, far and away the source of the bulk of earnings growth for the US economy for the foreseeable future. If anything, the coronavirus will accelerate the move away from shopping malls and towards online commerce as consumers seek to avoid direct contact with the virus.

What would I be avoiding here? Directly corona-related stocks like those in airlines, hotels, casinos, and cruise lines. Avoid human contact at all cost!

Microsoft (MSFT) – still has a near-monopoly on operating systems for personal computers and a huge cash balance. Their inroads with the Azure cloud services have been impressive. (MSFT) just reported an impressive $8.9 billion in Q4 earnings. It’s now yielding a respectable 1.26%.

Apple (AAPL) – Even with the Coronavirus, Apple still has a cash balance of $225 billion. Its 5G iPhone launches in the fall, unleashing enormous pent-up demand. Apple’s rapid move away from a dependence on hardware to services continues. It’s now yielding a respectable 1.13%.

Alphabet (GOOGL) – Has a massive 92% market share in search and remains the dominant advertising company on the planet. (GOOGL) just announced an incredible $8.9 billion in Q4 earnings.

QUALCOMM (QCOM) – Has a near-monopoly in chips needed for 5G phones. It also recently won a lawsuit against Apple over proprietary chip design.

Amazon (AMZN) – The world’s preeminent retailer is growing by leaps and bounds. Dragged down by its association with the world’s worst industry, (AMZN) is a bargain relative to other FANGs.

Visa (V) – The world’s largest credit company is a free call on the growth of the internet. We still need credit cards to buy things. And guess what? Coronavirus will accelerate the move of commerce out of malls, where you can get sick, to online.

American Express (AXP) – Ditto above, except it charges high fees, its stock has lagged Visa and Master Card in recent years and pays a 1.58% dividend.

NVIDIA (NVDA) – The leading graphics card maker that is essential for artificial intelligence, gaming, and bitcoin mining.

Advanced Micro Devices (AMD) – Stands to benefit enormously from the coming chip shortage created by the coming 5G.

Target (TGT) – The one retailer that has figured it out, both in their stores and online. It can’t be ALL tech.

Good Luck and Good Trading

John Thomas

Mad Hedge Technology Letter

February 28, 2020

Fiat Lux

Featured Trade:

(THE TRUE COST OF THE CORONAVIRUS)

(COMPQ), (PYPL), (MSFT), (AMZN), (GOOGL)

Tech shares are hoping to stage a rebound after the coronavirus-fueled rout that saw the Nasdaq’s 2-day drop by 6.38%, which is its worst since June 2016.

Readers can now pencil in a fresh readjustment to growth expectations of zero to low single digits in tech shares for fiscal year of 2020.

That is why Thursday morning was greeted by another 3% drop at the open - proceed with caution to not get trapped in the proverbial dead cat bounce vortex in the short-term.

A major tech consolidation could take place because let’s get real, the unpredictability is having a major impact on technology companies and uncertainty is a substantial input in heightened risk.

What are the realistic scenarios that are still left on the table?

Firms trading on the Nasdaq will slash price targets and profit estimates that could uncoil another leg down in the Nasdaq index.

In fact, it has already happened as PayPal (PYPL), Microsoft (MSFT), and Apple (AAPL) issued revenue warnings saying they do not expect to meet their revenue goals because of the coronavirus.

On an operational level, softness is what I see when delving into the semantics of Amazon (AMZN) whose ranking algorithm demotes product sellers who go out of stock.

The coronavirus has crippled supply chains, and to avoid a lack of stock, sellers are raising prices to slow sales, while planning to move production to other countries.

This is on top of the backbreaking supply problems that companies face because of the ill-effects of the trade war.

If the Amazon algorithm punishes the seller, once stock is replenished, they must overspend on advertising to climb back to the top of product searches.

The surveys I have taken out with Amazon sellers in the last few days show a precarious situation where sellers are stretched to the limit relying on numerous uncertain variables that are completely out of their control,

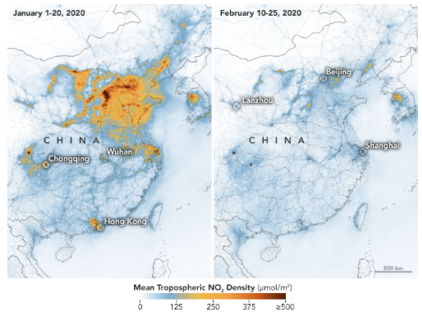

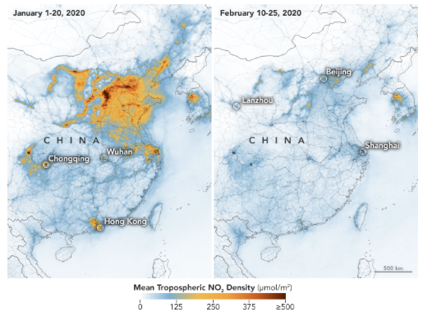

Even if the local government allows Chinese factories to restart, it will be understaffed while workers from other provinces self-quarantine.

The third-party marketplace accounts for more than half of Amazon’s retail sales with a robust base of manufacturers and sellers in China.

Google (GOOGL) and Microsoft are accelerating efforts to shift hardware production to Southeast Asia amid the worsening coronavirus outbreak, opening factories in Vietnam and Thailand as well.

Google is set to begin production of the Pixel 4A smartphone and also plans to manufacture its next-generation flagship smartphone called the Pixel 5 in Vietnam.

Google is also on the verge of building factories in Thailand for "smart home" related products, including voice-activated smart speakers like the Nest Mini.

Google and Microsoft’s plans are a giant shift away from their prior generation-long China manufacturing strategy and the coronavirus has only supported a strategy to remove China as a core manufacturing hub.

It is getting so bad in China that they are evaluating the feasibility and cost implications to uninstall some production equipment and ship it from China to Vietnam, literally packing up and taking their show on the road.

The have already initiated the process by asking a key sourcing contact to convert an old Nokia factory in the northern Vietnamese province of Bac Ninh to handle the production of Pixel phones.

Data center server production was also rerouted to Taiwan last year.

The coronavirus threat is only speeding up the move into South East Asia and Google and Microsoft hope to avoid the geopolitical risk in the region.

Remember that all of this rejigging of production will add costs and only the biggest can absorb mega hits to the balance sheets.

As for the coronavirus, business is becoming more complicated as the ban on Chinese nationals and flights from China could build barriers to business, and now South Korea has joined the list.

Korea’s Samsung Electronics, the world's largest smartphone maker, has operated a smartphone supply chain in northern Vietnam for years but still relies on some components made in China.

While there are many moving parts, the average investor needs to wait on optimal entry points.

Japan announced school shutdowns for a month and tech shares have only priced in the coronavirus eventually entering the U.S., but if there are mass shutdowns of American cities and schools, then tech shares will see another stinging sell-off.

The contagion could eventually lead to the Olympics in Tokyo being canceled, high-profile corporate management getting infected, and the Chinese economy being sidelined for most of 2020.

All of these events are highly negative to the global economy which is why potential risks have exploded through the roof in such a short time.

Slinging mud at the wall will not work in times like this, but this does have the makings of a once-in-a-year entry point into tech shares.