Mad Hedge Technology Letter

February 21, 2020

Fiat Lux

Featured Trade:

(WHY THE GOVERNMENT IS GUNNING FOR GOOGLE AND FACEBOOK)

(FB), (GOOGL), (TWTR), (ADBE), (FTNT), (EBAY)

Mad Hedge Technology Letter

February 21, 2020

Fiat Lux

Featured Trade:

(WHY THE GOVERNMENT IS GUNNING FOR GOOGLE AND FACEBOOK)

(FB), (GOOGL), (TWTR), (ADBE), (FTNT), (EBAY)

Google (GOOGL) and Facebook (FB) are dominant to the extent that the U.S. administration is hoping to dismantle them.

The two companies enjoy a flourishing duopoly and guzzle up digital ad dollars.

Governments around the world are scratching their heads attempting to figure out how to put a dent in these fortresses and so far, have been unsuccessful.

Big tech has made governments look bad, to say the least, and their response has been even more shambolic.

Alphabet installed Google CEO Sundar Pichai as the top decision-maker for all Alphabet assets preparing for the onslaught of digital privacy headwinds and regulation that the E.U., U.S., and everyone else will throw at them.

Luckily, they do not need to deal with the Chinese communist party as big tech minus Apple was effectively banned years ago.

What’s on Google and Facebook’s plate right now?

Attorney General William Barr has pointed the finger at these two platforms for hiding behind a clause that gives them immunity from lawsuits while their platforms carry material promoting illicit and immoral conduct and suppressing opinions.

Barr is currently looking into potential changes to Section 230 of the Communications Decency Act, which was passed in 1996 and has been also referred to as the supercharger to tech riches.

What could eventually come of this?

Barr could decide for the Justice Department to explore ways to limit the provision, which protects internet companies from liability for user-generated content.

This could open up Google and Facebook to higher costs of managing content on their platforms and lawsuits related to malcontent in which they fail to remove.

Even though platforms love to market that they actively thwart bad actors, at the end of the day, they aren’t on the hook for what happens.

Massive alterations could fundamentally weaken their business models and force them to review each word and photo that is thrown upon their platform.

They have already hired an army of hourly paid contractors, but at their massive scale, content is simply impossible to smother.

Content generators understand how to sidestep machine learning algorithms which are based on backdated data, meaning they would not be able to catch a new iteration of past content.

Absolving themselves of any responsibility for policing their platforms has been an important catalyst in the outperformance in shares for both Facebook and Google.

The social side of this has cringeworthy unintended consequences.

The Computer & Communications Industry Association, a tech trade group that counts Google and Facebook as members want the government to stay out of it as they believe they are overreaching.

Government has been slowly making inroads in combatting the strength of these digital platforms, and the first successful foray was when Congress eliminated the liability protection for companies that knowingly facilitate online sex trafficking.

Big tech won’t go with a whimper and they will propose a range of changes to avoid direct damage to their business model such as raising the bar a smidgeon on which companies can have the shield, to carving out other laws negating attempt to weaken their platforms, to delaying the repealing of Section 230.

There is too much shareholder value on the line and as the coronavirus rears its ugly head, it’s ironic that investors perceive safety in not only the U.S. dollar but in the vaunted FANG tech group.

Ultimately, the math wins out and these companies with gargantuan earnings can weather any storm with a moat as wide as ever.

It’s to the point that a $10 billion fine is a massive victory, and what other group of companies can boast about that?

We can only trade the market we have in front of us and not the one we want.

I pulled the trigger on a Google call spread and I believe this narrow group of power tech players and their partners in crime cloud stocks of the likes of Twitter (TWTR), eBay (EBAY), Fortinet (FTNT), Adobe (ADBE), and a few others will hoist the market on its back like I predicted it would at the beginning of the trading year.

Global Market Comments

February 20, 2020

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

We all love our FANGS.

Not only have Facebook (FB), Apple (AAPL), Netflix (NFLX), and Alphabet (GOOGL) been at the core of our investment performance for the past decade years, we also gobble up their products and services like kids eating their candy stash the day after Halloween.

Three of the FANGs have already won the race to become the first $1 trillion in history, Apple, Amazon, and Microsoft.

In fact, the FANGs are so popular that we need more of them, a lot more. So how do we find a new FANG?

Here is where it gets complicated. None of the four have perfect business models. All excel in many things but are deficient at others.

So, there are at least four different answers as to what makes a FANG. A more accurate answer would probably be 4 squared, or four to the tenth power.

I will list the eight crucial elements that make a FANG.

1) Product Differentiation

In medieval times, location was the most important determinant of business success. If you owned Ye Olde Shoppe at the foot of London Bridge, you prospered.

Then, great distribution was crucial. This occurred during the 19th century when the railroads ran the economy.

Products followed with the automobile boom of the 20th century, when those who dreamed up 18-inch tailfins dominated. This strategy was applied to all consumer products.

The Financial age came next, when cheap money was used to assemble massive conglomerates that was the primary determinant of success.

The eighties and nineties spawned the era of global brands, be it Coca Cola, MacDonald’s, Lexus, or Gucci.

Today, the global economy is ruled by those who can provide the best services. Facebook offers you personal access to a network of 1.5 billion. Apple will sell you a phone that can perform a magical array of tricks.

Netflix will stream any video content imaginable with lightning speed. Alphabet will deliver you any piece of information you want as fast as you can type, but charges advertisers hundreds of billions of dollars to get in your way.

This has created what I call an “Apple” effect. It stampedes buyers to pay the highest premiums for the best products, assuring global dominance.

While Apple accounts for less than 10% of the smart phone market, it captures a stunning 92% of the net profits. Everyone else is just an “also ran.”

Instead of driving my car into a dingy dealership every few months to get ripped off for a tune up, Tesla (TSLA) does it remotely, online, while I sleep, for free.

Unlike battling for a smelly New York taxi cab in a snow storm, a smiling Uber driver will show up instantly, know where to go, automatically bill me at a discount price, and even give me restaurant recommendations in Kabul.

And you all know what Amazon can do. It beats the hell out of looking for a parking space at a mall these days, only to be told they don’t have your size (48 XLT).

2. Visionary Capital

If you have a great vision, you can get unlimited financing free from investors anywhere. That puts those who must pay for expensive external financing for growth at a huge disadvantage.

Have a great vision, and the world is your oyster.

Elon Musk figured this out early with Tesla. By promising a “carbon-free economy,” he has been able to raise tens of billions of equity capital even though his firm has never made a real profit.

Alphabet is “organizing the world’s information”, while Facebook is “connecting the world.”

Chinese Internet giant Alibaba (BABA) invented a holiday from scratch, “Singles Day,” November 11, which has quickly become the most feverish shopping day in history. In 2019, they booked an unbelievable $30.8 billion in sales in a single 24 hours period, up 27% from the previous year.

And you know the great thing about visions? Not only do venture capitalists and consumers love them, so do stock investors.

3) Global Reach

You have to go global or be gone. A company with 7 billion customers will beat one with only 330 million all day long.

Go global, and economies of scale kick in enormously. This is only possible if you digitize everything from the point of sale to the senior management. Some two-thirds of Facebook users are outside the US, although half its profits are homegrown.

By the way, the Mad Hedge Fund Trader is global, with readers in 135 countries. Our marginal cost of production is zero, and the entire firm is run off my American Express card. It’s a great business model. And boy, do I get a ton of frequent flier points! Whenever I board Virgin Atlantic’s nonstop from San Francisco to London, the entire crew stands up to salute.

4) Likeability

Who doesn’t like Mark Zuckerberg, with his ever-present hoodies, skinny jeans, and self-effacing demeanor. And who did Facebook send to Washington to testify about internet regulation but the attractive, razor-sharp, and witty Sheryl Sandberg? The senators ate out of her hand.

Bill Gates and Steve Ballmer? Not so likable. Their arrogance invited a ten-year antitrust suit against Microsoft (MSFT) from the Justice Department which half the legal profession made a living off of.

And here’s the thing. If people like you, so will consumers, regulators, and yes, even equity investors. It makes a big difference to the bottom line and your investment performance.

5) Vertical Integration

Crucial to the success of the FANGs is their complete control of the customer experience through vertical integration.

When FANGs don’t manufacture their own products, as Apple does, they source them, rebrand them, and sell them as their own, like Amazon.

The return on investment for advertising is plummeting. Just ask the National Football League. So, it has become essential for companies to keep a death grip on the customer the second they enter your site.

Some, like Amazon again, will keep chasing you long after you have left their sites with special offers and alternative products. Even if you change computers they will hunt you down.

One of my teenaged daughters used my computer to buy a swimsuit last summer, and let me tell you, booting up in the morning has been a real joy ever since.

This was the genius of the Apple store network. Buy one Apple product and they own you for life, like an indentured servant. They all integrate and talk to each other, a huge advantage for a small business owner. And they are cool.

No pimple-faced geeks wearing horn-rimmed glasses here. Get your iPhone fixed and you don’t talk to a technician, but a “genius.” It’s all about control.

Expect other strong brands to open their own store chains soon.

6) Artificial Intelligence

There is probably no more commonly known but least understood term in technology today. It’s like counting the number of people who have finished Dr. Stephen Hawking’s “A Brief History of Time” (I have).

A trillion-dollar company absolutely must be able to learn from human data input and then use algorithms to analyze it. Data has become the oxygen of the modern economy.

The company then use other algos to predict what you’re most likely buying next and then thrust it in front of your face screaming at the top of its lungs.

This has been evolving for decades.

First, there was demographic targeting. White suburban middle-class guys have all got to like Budweiser, right?

This turned into social targeting. If two friends “liked” the same brand, regardless of their demographics, they should be targeted by same advertisers.

Now we live in the age of behavioral targeting. There is no better predictor of future purchases than current activities. So, if I buy a plane ticket to Paris, offerings of Paris guidebooks, tours, French cookbooks, French dating services, and even seller of discount black berets suddenly start coming out of the woodwork.

It would be a vast understatement to say that behavioral targeting is the most successful marketing strategy ever invented. So, guess what? We’re going to get a lot more of it.

As depressing as this may sound, the number one goal of almost all new technological advancements these days is to get you to buy more stuff.

Better to use the public computer at the library to buy your copy of “50 Shades of Gray.”

7) Accelerant

If you want to throw gasoline on the growth of a company, you absolutely have to have the best people to do it. The companies with the smartest staff can suck in free capital, invent faster, develop speedier services, and always be ahead of the curve when compared to the competition.

This has led to enormous disparities in income. Companies will pay anything for winners, but virtually nothing for losers.

I’ll never forget the first day I walked on to the trading floor at Morgan Stanley (MS). I am 6’4” and am used to towering over those around me. But at Morgan, almost all the salesmen were my height or a few inches shorter.

The company specifically selected these people because they delivered better sales records. Height is intimidating, especially to short customers.

And that’s what the FANGs have, the programming equivalents of a crack all-6’4” sales team.

A few years ago, my son got a job as the head of International SEO at Google. He was rare in that he spoke fluent Japanese and carried three passports, US, British, and Japanese (born in London with a Japanese mom and American dad).

However, when he met his team, they all spoke multiple languages, were binational, and were valedictorians, National Merit Scholars, and Eagle Scouts to boot!

This is why immigration is such a hot button issue in Silicon Valley these days. If you can’t get a work visa for a graduating PhD in Computer Science from Stanford, he’ll just go back to China or India to start a local competitor that may someday eat your lunch.

By the way, if you get a FANG on your resume, even for a short period, you are set for life. Oh, and by the way, Apple gets 100,000 resumes a month!

8) Geography

It all about location, location, location. It’s no accident that Silicon Valley took root near two world class universities, the University of California at Berkeley (my alma mater), and the godless heathens at Stanford across the bay.

When the pioneers moved west in covered wagons in 1849, they came to a fork in the road. The god fearing families went right to the verdant farmland of Oregon, while young men cashing in on the latest get-rich-quick scheme chose left for the gold fields of California. Nothing has changed since.

Cal in particular was the recipient of massive government funding for the Manhattan Project that built the first atomic bomb during WWII. The tailwind lingers to this day. The world’s first cyclotron still occupies a local roundabout.

Universities provide the raw materials essential to create hot house local economies like the San Francisco Bay Area. And as much as every region in the US or country in the world would like to do this, none have been able to.

There is only one place in the world were a company can hire 1,000 engineers from scratch on short notice, and that is the Bay Area.

Also, innovation is city centered. Some two-thirds of future GDP growth will emanate from cities.

So, if you want to move your career forward, you better count on spending some serious time in Silicon Valley, New York, London, and Tokyo.

I’ve done all four and it paid handsomely.

So there you have it. Now we know what makes a FANG. I’ll be addressing who the most likely FANG candidates are in a future letter.

I want to thank my friend, Scott Galloway of New York University’s Stern School of Business for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Mad Hedge Technology Letter

February 14, 2020

Fiat Lux

Featured Trade:

(DATA TELLS THE WHOLE STORY)

(FB), (GOOGL), (NFLX), (AMZN), (EBAY), (TWTR)

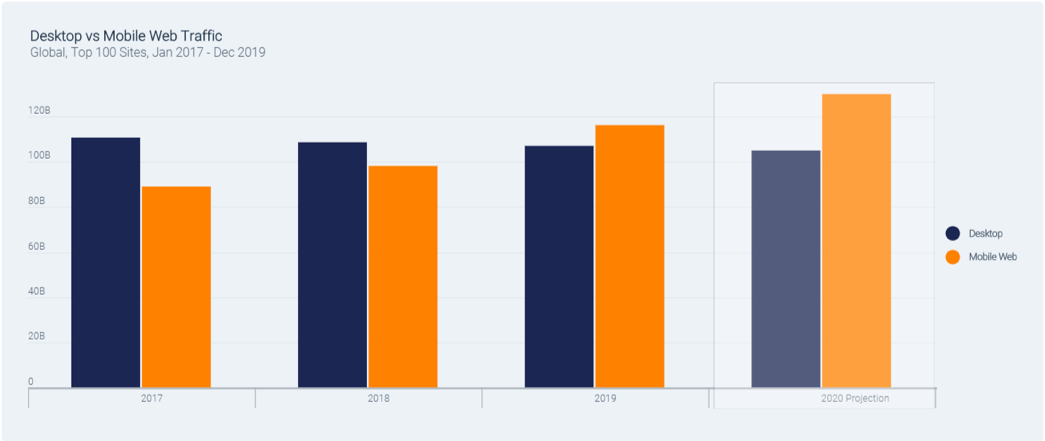

Behavioral trends have a sizable say in which tech companies will outperform the next and a recent report from SimilarWeb offers insight into how much users navigate around the monstrosity known as the internet.

The optimal way to comprehend the trends are from a top-down method by absorbing the divergence between desktop traffic and mobile traffic.

It’s no secret that the last decade delivered consumers a massive leap in mobile phone performance in which tech companies were able to neatly package applications that acted as monetization platforms by offering software and services to the end-user.

Thus, it probably won’t shock you to find out that desktop traffic is down 3.3% since 2017 as users have migrated towards mobile and the trend has only been exaggerated by the younger generations as some have become entirely mobile-only users.

All told, the 30.6% expansion in mobile traffic has penalized tech firms who have neglected mobile-first strategies and one example would be Facebook (FB), who even though has a failing flagship product in Facebook.com, are compensated by Instagram, who is showing wild growth numbers.

The fact that mobile screens are smaller than desktop screens means that users are staying on web pages not as long as they used to – precisely 49 seconds to be exact.

This trend means that content generators are heavily incentivized to frontload content and scrunch it up at the top of the page. This also means that sellers who don’t populate on Google’s first page of search results are practically invisible.

The high stakes of internet commerce are not for the faint of heart and numerous companies have complained about algorithm changes toppling their algorithm-sensitive businesses.

Even using a brute force analysis and investing in companies that are in the top 15 of internet traffic, then the companies that scream undervalued are Twitter (TWTR) and eBay (EBAY).

Twitter is a company I have liked for quite a while and is definitely a buy on the dip candidate.

The asset is the 7th most visited property on the internet behind the likes of Instagram, Google, Baidu, Wikipedia, Amazon, and Facebook.

This position puts them just ahead of Pornhub.com, Netflix, and Yahoo.

And if you take one step back and analyze traffic from the top 100 sites, traffic is up 8% since 2018 and 11.8% since 2017 averaging 223 billion visits per month.

Rounding out the top 15 is eBay who I believe is undervalued along with Twitter - these two are legitimate buy and holds.

Ebay was the recipient of poor management for many years and they are now addressing these sore points.

Certain content is suitable for mobile such as adult sites, gambling sites, food & drink, pets & animals, health, community & society, sports, and lifestyle.

And just over the last year or two, other categories are gaining traction in mobile that once was dominated by desktop such as news and media, vehicle sites, travel, reference, finance, and others.

Many consumers are becoming more comfortable at doing more on mobile and spending more to the point where people are making large purchases on their iPhones.

The biggest loser by far was news - they are losing traffic in droves.

Traffic at the top 100 media publications was down 5.3% year-over-year from 2018 to 2019, a loss of 4 billion visits, and down by 7% since 2017.

Personally, I believe the state of the digital news industry is in shambles, and Twitter has moved into this space becoming the de facto news source while pushing the relevancy of news sites down the rankings.

Facebook and Twitter are essentially undercutting the news by forcing news companies to insert them between the reader and the news company because they have strategized a position so close to the user’s fingertips.

The negative sentiment in news is broad based on popular news, entertainment news and local news all showing decreases of more than 25%.

Finance and women’s interest news categories are the only ones showing positive traffic growth.

The state of internet traffic growth supports my underlying thesis of the big getting bigger and the subsequent network effect stimulating further synergies that drop straight down to the bottom line.

The top 10 biggest sites racked up a total of 167.5 billion monthly visits in 2019, up 10.7% over 2018 and the remaining 90 largest sites out of the top 100 only increased 2.3%.

This has set the stage for just five gargantuan tech firms to become worth more than $5 trillion or 15.7% of the S&P 500’s market value and 19.7% of the total U.S. stock market’s value.

Now we have real data backing up my iron-clad thesis and these cornerstone beliefs underpins my trading philosophy.

Many of the biggest wield a two-headed monster like Google who has Google.com and YouTube video streaming and Facebook, who have Facebook.com and Instagram.

It doesn’t matter that Facebook has lost 8.6% of traffic over the past year because Instagram compensates for Facebook being a poor product.

And if you are searching for another Facebook growth driver under their umbrella of assets then let’s pinpoint chat app WhatsApp who experienced 74% year-over-year traffic.

Beside the news sites, other outsized losers were Yahoo’s web traffic shrinking by 33.6% and Tumblr, which banned adult sites in 2018, leading to a 33% loss in traffic.

If I can sum up the data, buy the shares of companies who are in the top 15 of internet traffic and be on the lookout for any dip in eBay or Twitter because they are relatively undervalued.

Mad Hedge Technology Letter

February 12, 2020

Fiat Lux

Featured Trade:

(UBER’S DARK FUTURE)

(UBER), (LYFT), (FB), (AMZN), (NFLX), (GOOGL)

Autonomous or bankrupt; that is the ultimate fate of Uber (UBER).

In the short-term, Uber is a master at moving the goalposts in order to breathe life in the stock.

CEO of Uber Dara Khosrowshahi can only pray that the Fed will continue to pump cheap money into the market because without artificially low-interest loans, tech firms like Uber would implode.

Is it really time to give Uber the benefit of the doubt?

No more hype, just profits? Is the calculus to profits legitimate?

That's what we call a bubble. Bubbles always burst. Here's the scary part.

Many people are counting on the continued existence of Uber and Lyft to provide "cheap transportation."

Commuters will have to get suddenly unused to it.

There are many companies today that are running the same scheme as Uber in the “gig economy.”

It’s true that management loves to use a lot of flowery language to disguise a lack of profitability.

But as the conditions are ripe for a leg up in tech, the tide rises, and even Uber’s boat rises with it.

I have yet to see even one realistic analysis of how Uber or Lyft is going to become profitable - not even basic math!

I have met a plethora of drivers for both companies, and hope they do well, but there is only so long that one can put lipstick on a pig.

So here we are, Uber in the green everyday because they moved the goalposts yet again and promise us earlier than expected profitability but still losing billions of dollars.

Lyft and Uber have apparently increased revenues somewhat by reducing promotional discounts to riders, but that does not project to even a breakeven point and the unit economics tell me no even if my heart says yes.

The only trick up their sleeve seems to be fare increases, but where is the roadmap detailing this treacherous path?

Once we get to the point in time when Uber is supposed to be profitable, I bet that management will call in another trick play and move the goal posts yet again.

It is quite laughable when so called “tech experts” want Uber to join the ranks of Facebook Inc. (FB), Amazon.com Inc. (AMZN), Netflix Inc. (NFLX), and Alphabet Inc.’s Google (GOOGL) as part of a FANGU acronym.

Reasons for this new bundle is thought to be because of the ability to take advantage of its massive scale while working toward profitability.

Uber is the global ridesharing leader and is becoming the global food delivery leader, but do they really add value?

What if the local government finally got their finger out and built a proper transport system?

They are merely taking advantage of a broken system and passing on the costs of paying drivers to the drivers themselves by designating them as hourly workers.

Are we supposed to celebrate when Uber becomes more “rational?”

Meaning that players have limited their attempts to undercut one another with the sorts of pricing and big discounts that had at one time suggested the business might be a race to the bottom.

Uber projected a lower loss than analysts were expecting for 2020, does less loss mean profits in 2020?

And I do agree that it is encouraging that the company is finally disclosing more data, but shouldn’t they be doing that in the first place?

Love it or hate it, there is a “war” going on between profitability and growth at Uber as the company manages the trade-offs.

Uber had previously talked up that it would become Ebitda profitability by the end of 2021, but Khosrowshahi now forecasts profitability for the fourth quarter of this year.

He says it is possible because Uber initiated a “belt-tightening program” in the last half of 2019, exiting unprofitable ventures and laying off about 1,000 employees.

For instance, Uber sold its food-delivery business in India to a local startup, Zomato, in return for a 9.9% stake in that company.

I do believe that they haven’t done enough to build credibility with investors and the stock’s price action is behaving as we should trust Uber’s management with whatever comes out of their mouths.

The lack of visibility and uncertainty around trends in ridesharing and Eats outside the U.S. continue to be hard to quantify.

So that sounds great! Uber is more serious than ever about becoming profitable and investors have backed them up with the stock flying to the moon.

The trend is your friend and I would suggest readers to get out of the way of this one because you could get trampled on just like the Tesla bears.

And I do support Uber in making steps in the right direction and it also can be said that stocks appreciate the fastest when they transform from a horrible company to a less horrible company.

But there is no way that I am giving Khosrowshahi a pass for Uber’s current situation and no chance I am praising him to the hills.

It is what it is, and Uber is less bad than before, and if they don’t meet their targets, I don’t think investors will believe Khosrowshahi version of a spin doctor forecast anymore.

Uber will rise in the foreseeable future and if they fail to become profitable by 4th quarter, expect a massive drawdown.

If they succeed, expect a vigorous wave of new players to buy into Uber shares.

The stakes have never been higher for Uber and Khosrowshahi.

Mad Hedge Technology Letter

February 10, 2020

Fiat Lux

Featured Trade:

(THE MODERN AGE TECH FORCE MULTIPLIER)

(GOOGL)

In a blink of an eye – I missed my entry point again!

The earnings report gave us mixed messages, but the weakness in shares will naturally be short-lived.

Sometimes, people really forget to understand how powerful and dominant Google (GOOGL) really is.

As the stock kept running away from me and the math looked less and less appetizing, I decided to wait for the next go-around to execute a call spread on Google.

Even though sometimes Google gets slapped on the wrist for some minor blemishes on its earnings report, this time around they gave us new revenue disclosures and higher-than-expected share buybacks.

The stock cratered 2.82% to $1,440 a share in early trading last Tuesday but is still up around 25% year-over-year.

Google’s earnings per share of $15.35 was more than enough to beat expectations, but revenue was $46.08 billion, missing expectations of $46.94 billion.

Google's operating margin of 20% missed by 1%.

Google has been notoriously private about their revenue hoard but they did chime in with some more color when Google's CFO Ruth Porat, said, "to provide further insight into our business and the opportunities ahead, we’re now disclosing our revenue on a more granular basis, including for Search, YouTube ads and Cloud."

Google is still and will be at the forefront of any technological innovation of this generation buttressed by a staunch digital ad business to fund anything they want to do.

I looked into buying a call spread last Tuesday and the stock took off like a scalded chimp muddying option prices.

My big-picture thesis is unchanged, and I tell anyone and everyone in the aisles of Whole Foods to buy Google on any short-term weakness.

It’s uncanny ability to drive engagement and monetization across its 9 products with 1 billion plus users is a rare phenomenon.

Even though the law of large numbers creeps up to hurt the company, it still has strong engagement, advertiser value, and monetization possibilities.

Disclosure will give investors a more transparent way to calculate the monetization engines like Maps, Discover, and e-commerce suite of products.

What did we find out?

YouTube did $15 billion of revenue in 2019.

Google Cloud does $9 billion of annual revenue growing 50% year-over-year.

Google’s cloud business is practically the same size as Amazon Web Services (AWS) in 2016, but expanding slower than AWS did at that time.

The company has such a strong balance sheet that share repurchases were higher than expected at $6.1 billion vs. $4.0 billion.

Another sore point would be that headcount and capex in data centers, servers continue to be on the high side.

Google revealing numbers for YouTube and cloud for the first time is clearly because they felt comfortable in doing so.

I believe that they will start disclosing more detail going forward especially as the cloud division continues to ramp up and contribute meaningfully to its earnings.

And remember that it was only in July that Google said its cloud unit had just reached $8 billion in annualized revenue and planned to triple its sales force over the next few years.

Combined with installing Sundar Pichai as the new Alphabet CEO, this is a conscious move to provide more transparency to put its revenue drivers in the shop window.

Former Alphabet CEO and Google founder Larry Page and co-founder Sergey Brin stepped down from the positions last December, leaving Pichai as the big boss with power to make all game-changing decisions.

The aforementioned two still retain voting shares in the company.

The last talking point is that Google has been under intense scrutiny by federal and state regulators hoping to prove anti-competitive behavior.

A collection of 50 attorney generals from different states are investigating Google’s ad business.

But many experts believe that Google has a good chance of winning or stalling the feds, yet, the most likely outcome is that Google will be able to keep its business model but pay another massive fine which is a net positive.

Basically, Google’s narrative is intact, and any selling should be met by a wave of buying.